RESEARCH - MARKET OVERVIEW AUGUST 2019 SPEC DEVELOPMENT DRIVES INDUSTRIAL MARKET

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

RESEARCH MARKET OVERVIEW AUGUST 2019 SPEC DEVELOPMENT DRIVES INDUSTRIAL MARKET

Population Growth

AUS: 1.6% VIC: 2.2%

YoYΔ: Dec ‘18

Surging population development with much of this

Economic Growth stimulates growth in E- development concentrated in

commerce Melbourne’s western suburbs.

AUS: 2.8% VIC: 3.5%

YoYΔ: Jun ‘18 Victoria’s economy continues to perform Record infrastructure

strongly off the back of record population investment, especially in

Unemployment Rate growth. According to the Australian Melbourne’s west

Bureau of Statistics, over the last CY

AUS: 5.2% VIC:4.5% Victoria’s population grew by 2.2%, The State Government has responded to

As at: Jun ‘19 ahead of the national growth figure of Melbourne’s unprecedented growth – a

1.6%, and in line with this over the 2017- record $54.4 billion worth of

18 FY the state’s economy grew by 3. infrastructure projects are currently

Online Retail Trade 5%, against the national rate of 2.8%. underway in Victoria, with the potential

for a further $80 billion of investment.

AUS:+12% (at $1,644.7m) Victoria’s booming population is having a Reflecting the growth in industrial activity

YoYΔ: May‘19 flow-on effect on E-commerce. in Melbourne’s west, a considerable

According to Australia Post, at a state focus of Victoria’s current infrastructure

level Victoria recorded the second development lies in the western suburbs.

Investment in strongest YOY growth in online shopping,

Infrastructure with the number of online sales up by Most notably, the western roads upgrade

VIC: $14.2bn 22.2%. will transform 8 priority roads in the west

with many of these in the key industrial

FY ’19-20

E-commerce and tight suburbs of Truganina (Palmers road and

supply drives Melbourne’s Leakes road) and Laverton North

industrial market (Doherty’s road), and the West Gate

Tunnel project will deliver a vital

Set against the backdrop of an alternative to the West Gate Bridge,

increasingly tight industrial property providing a much needed second river

market, the growth in online shopping is crossing, quicker and safer journeys, and

creating significant demand for logistics remove thousands of trucks from

and warehousing space, and this is residential streets.

creating an appetite for speculative

Victorian Government’s Infrastructure Investment (GII)

(in $ billions)

16

14

12

10

8

6

4

2

0

Associate Director 2014-15 2015-16 2016-17 2017-18 2018-19 2019-20(f) 2020-21(f) 2021-22(f) 2022-23(f)

2

MELBOURNE INDUSTRIAL JULY 2019 RESEARCH

Rents, Incentives & Outlook

Record take-up levels drive being met with 200,000 sq m of enquiry. (per sq m) Prime Secondary

decline in prime vacancy Rents $88 $71

2020 supply levels are likely to exceed YoY Δ Jul’19: +6.0% +5.2%

Melbourne’s industrial vacant space long term averages, driven by the recent

(5,000 sq m+) sits at 712,044 sq m. uplift in spec development. However, the Incentives 16.0% 14.6%

Vacancy has increased by 10% since the expectation is this stock will be absorbed

Rents

start of the year off the back of a 30% quickly given the demand for quality Outlook

increase in existing secondary stock warehousing space is expected to remain

levels, with this increase driven by the strong. land values rising by 100%. Rents have

north where secondary vacancy has also risen considerably (25%-30%) in the

increased by 145.1% since January. Rents rise from the increase supply starved Fringe. Rents are

in land values expected to grow further due to

Despite the rise in overall vacancy, the expectation of continued tight supply,

amount of prime grade vacant space has A surge in land values has placed upward sustained tenant demand and the need to

declined by 5.6% since January, with pressure on rents, in particular in the cover rising development costs related to

prime vacancy levels now among the south east where rents have risen by the need for automation and technology.

lowest recorded for half a decade. almost 10% since July 2018 in line with

Melbourne Industrial Vacancy Melbourne Industrial New Supply Melbourne Industrial Rents

Available Space by Grade New Industrial Developments by Precincts Net Face Rents by Grade excl. City Fringe

'000 sq m

700 90

$/ sq m

85

600

80

500

75

400

70

300

65

200

60

10YR Growth Rate

100 55 Prime: +18.9%

Secondary: +19.5%

0 50

Jul-11

Jul-12

Jul-13

Jul-14

Jul-15

Jul-16

Jul-17

Jul-18

Jul-19

Jan-12

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

Jan-18

Jan-19

Jul-11

Jul-12

Jul-13

Jul-14

Jul-15

Jul-16

Jul-17

Jul-18

Jul-19

Jan-12

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

Jan-18

Jan-19

PRIME SECONDARY

PRIME SECONDARY

Currently in the east there is no prime

vacant space, and vacancy in the south

east has declined by 16.4%. The decline Recent Leasing Activity Melbourne (YTD June 2019)

in prime vacancy can be linked to a

record 267,678 sq m of prime stock that Net Rent Area

Address Region Type Tenant

($/sq m) (sq m)

was absorbed over the last quarter, with

the bulk of this take-up emanating from 47 & 53 Foundation Rd,

the west and south east regions. West 78.0* 33,310 Spec Seacon Group

Truganina

Underlying tenant demand has been

driven by the E-commerce and food Maker Pl, Truganina West 75.0 30,885 Spec HB Commerce

manufacturing sectors. The brief uptick in

prime vacancy in Q1 2019 was caused 52 Dunmore Dr, Truganina West 80.0 20,946 Spec ADN

by the increase in spec stock presented

24 Logis Blvd, Dandenong South

to the market, which has since been 75.0* 15,797 Direct AFS Logistics

South East

taken up with most of this supply coming

from the west. And yet despite the high South

2 Beyer Rd, Braeside 90.0 9,146 Spec Gale Pacific

East

levels of spec activity, supply is lagging

in the west with 150,000 sq m of supply

3

Completed 2019 5,000—10,000 sq m

Under construction 10,000—20,000 sq m

Proposed 2019 & 2020 20,000 sq m+

Land values take off development, especially within development is due to land in the west,

Melbourne’s west where there is the which is approaching double what was

Industrial land values in Melbourne greatest capacity for expansion. The recorded in 2018 (87,390 sq m).

have increased considerably in the last strong demand for spec development is Demand in the west is such that more

12-24 months, driven by increases in reflected in short take-up periods with than half the spec space due to come

prices recorded in the south east and spec builds averaging 2 months on the online in the west is already under offer.

west. In the last 3 years, the value of 1- market following completion.

5 hectare lots in the south east has

grown by 10-15% YOY, while the value More than half (56%) of the industrial Land Values & Outlook

of 10+ hectare lots in the west has development due to land in Melbourne

soared in the last 12 months - in May in 2019 is speculative. In total 280,000 (per sq m) < 5,000 1-5 ha

2019, a land parcel in Truganina sold sq m of spec build is scheduled for

Values $440 $320

for $237/sq m; 12 months earlier land in 2019, which is more than double what YoY Δ Jul’19 +14% +20%

the same area sold for $102/sq m. The was recorded in 2018 (110,500 sq m).

surge in land values has been brought And 142,334 sq m of this spec

Outlook

upon by strong demand, low levels of

new supply and in turn rising rents,

underpinned by convenience of

location. Strong pre-leasing activity and Recent Land/Development Sales Activity Melbourne

a restricted short term supply pipeline

Price Area Sale

in the east and south east will ensure Address Region $ / sq m Purchaser

$ mil (sq m) Date

land values continue to rise.

875 Taylors Rd, South

80.0 413,000 194 Frasers Property Apr-19

Dandenong South East

Spec development drives

industrial activity 62-87 Horsburgh Dr &

720 Kororoit Creek Rd, West 54.7 209,300 261 ISPT Mar-19

Altona North

The rise in land values has had a flow-

210 Swann Dr,

on effect on rents, which coupled with West 11.5 45,310 254 Air Trunk May-19

Derrimut

a rise in demand for logistics and

1-4/678 Boundary Rd,

warehousing property spurred by the West 6.2 26,267 237 CRC Group May-19

Truganina

continued growth of E-commerce has

created an appetite for speculative

4

MELBOURNE INDUSTRIAL JULY 2019 RESEARCH

CY 2018 ($1.42 billion) and CY 2017

Current Yields & Outlook

($1.38 billion). The decline in sales Melbourne Industrial Yields

(in %) Prime Secondary volume however should not be Yields by Grade plus Risk Spread

interpreted as a reflection of waning

Yields 5.85 - 6.55 6.50 - 7.50 demand for industrial assets. Rather,

YoYΔ Jul’19: -30bps -30bps

strong tenant demand and rising rents

have made industrial assets increasingly

Outlook attractive to investors and set against a

backdrop of an already tight market this

Transaction volumes has made accessing prime grade

decline despite rising industrial properties increasingly

demand challenging.

In the first half of 2019 Melbourne’s Industrial the future of ‘new’

industrial sales volume ($10 million+) retail

totaled $615.2 million across 23

transactions. At the current rate, 2019 Indeed, the outlook for industrial

CY transaction volumes will fall property is very promising. Lured by the

marginally short of what was recorded in promise of strong long term returns, a

weight of capital is now looking to invest

in industrial assets as investors display

renewed confidence in an industrial Yield compression arc

Melbourne Industrial Sales ($10 mil+) property market buoyed by the growth nearing completion

Purchaser Profile—YTD Jun ‘19 of the E-commerce sector.

A climate of sustained tight supply of

Responding to the headwinds presented investment grade assets and strong

Private Investor

2% by the downturn in the retail sector, demand caused yields to compress

Developer

29%

A-REIT institutional investors are shifting the notably throughout the course of FY

16%

focus of their property portfolios away 2018, with current yields sitting at 30

from non-core retail assets towards year record lows.

industrial assets with an emphasis on

logistic and warehousing facilities. As In light of the recent strong uptick in

evidence of this broader structural land values, the primary driver of

change, as part of a retail divestment performance in the industrial property

strategy Stockland recently sold their market is likely to transition from yield

Owner Tooronga shopping centre in Glen Iris to compression to rental growth. While

Occupier Newmark Capital for $63 million, and in yields may well continue to tighten,

12% Offshore

29% late 2018 GPT purchased land at Shiny with the recent interest rate drop, the

Unlisted Fund/ Syndicate rate of compression is expected to

12% Drive in Truganina with a view to

speculatively developing 130,232 sq m slow. Indeed, already yields have

of warehouse space. remained unchanged over Q2 2019.

Recent Sales Activity Melbourne

Price Bldg Area Core Mkt WALE Sale

Address Region Vendor Purchaser

$ mil (sq m) Yield (%) (yrs) Date

30 Logistics Dr, Truganina West 69.6 48,769 5.3* 10.0 Goodman Group LOGOS Property Q2-19

182-198 Maidstone St,

West 41.2 37,906 7.6* 3.0 Abacus/ GAW Capital Cache Logistics/ ARA Q1-19

Altona

63-69 Pipe Rd, Laverton West 25.2 25,774 6.8 4.5 DEA Nominees Pty Ltd Harmony Property Q4-18

414-416 Somerville Rd,

West 22.0 24,343 6.5 2.9 ITI Timber Centennial Property Q4-18

Tottenham

5-9 Kitchen Rd, South

23.0 18,372 6.4 10.0 Shearform Centennial Property Q4-18

Dandenong South East

5

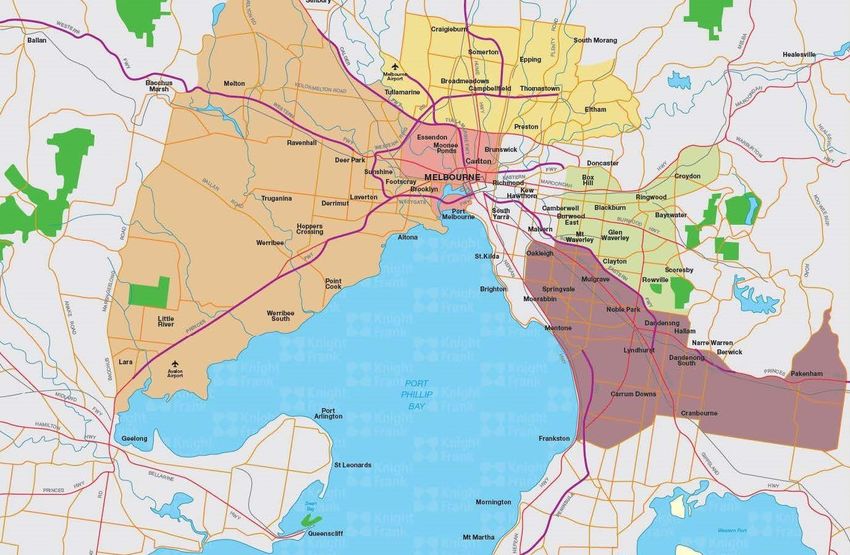

City Fringe North East

Vacancy Vacancy Vacancy

Prime: N/A* Prime: 70,332 sq m Prime: N/A*

Secondary: 17,404 sq m Secondary: 95,005 sq m Secondary: 89,644 sq m

Land Land Land

MELBOURNE INDUSTRIAL JULY 2019 RESEARCH

South East West

Vacancy Vacancy

Prime: 72,962 sq m Prime: 201,670 sq m

Secondary: 106,526 sq m Secondary: 58,501 sq m

Land Land

RESEARCH

Finn Trembath

Associate Director, Victoria

+61 3 9604 4608

Finn.Trembath@au.knightfrank.com

Kanwal Singh

Research Analyst, Victoria

+61 3 9604 4627

Kanwal.singh@au.knightfrank.com

Ben Burston

Partner, Head of Research &

Consulting

+61 2 9036 6756

Ben.Burston@au.knightfrank.com

INDUSTRIAL

Gab Pascuzzi

Partner, Head of Division

+61 3 9604 4649

Gab.Pascuzzi@au.knightfrank.com

Definitions:

Core Market Yield: The percentage return/yield analysed when the assessed fully leased net market Adrian Garvey

income is divided by the adopted value/price which has been adjusted to account for property Director

specific issues (i.e. rental reversions, rental downtime for imminent expiries, capital expenditure, +61 3 8545 8616

current vacancies, incentives, etc). Adrian.Garvey@au.knightfrank.com

Prime Grade: Asset with modern design, good condition & utility with an office component 10-30%.

Located in an established industrial precinct with good access. Joel Davy

Secondary Grade: Asset with an older design, in reasonable/poor condition, inferior to prime stock, Director

with an office component between 10-20%. +61 3 9604 4674

WALE: Weighted Average Lease Expiry. Joel.Davy@au.knightfrank.com

Methodology:

This analysis collects and tabulates data detailing vacancies, net face rents and yields (5,000 sq m+,

Marco Sandrin

sales of $3mil+) within industrial properties across all of the Melbourne Industrial Property Market.

The buildings are categorised into 1) Existing Buildings – existing buildings for lease. 2) Speculative Director

Buildings – buildings for lease which have been speculatively constructed and although have +61 3 9604 4731

reached practical completion, still remain vacant. 3) Spec. Under Construction – buildings for lease Marco.Sandrin@au.knightfrank.com

which are being speculatively constructed and will be available for occupation within 12 months.

Brent Glassford

Director

+61 3 9604 4683

Brent.Glassford@au.knightfrank.com

Knight Frank Research provides strategic advice, consultancy services and forecasting NATIONAL

Robert Salerno

to a wide range of clients worldwide including developers, investors, funding

Partner, Head of Industrial

organisations, corporate institutions and the public sector. All our clients recognise the +61 2 9761 1871

need for expert independent advice customised to their specific needs. Robert.Salerno@au.knightfrank.com

VALUATIONS & ADVISORY

Michael Schuh

Partner, Joint Managing Director

+61 3 9604 4726

Mschuh@vic.knightfrankval.com.au

VICTORIA

James Templeton

Partner, Managing Director

+61 3 9604 4724

James.Templeton@au.knightfrank.com

Sydney Industrial Melbourne Industrial Brisbane Industrial Active Capital View

Market Overview Market Overview Market Overview Outlook

January 2019 January 2019 March 2019 2019

Knight Frank Research Reports are available at KnightFrank.com.au/Research

Important Notice

© Knight Frank Australia Pty Ltd 2019 – This report is published for general information only and not to

be relied upon in any way. Although high standards have been used in the preparation of the

information, analysis, views and projections presented in this report, no responsibility or liability

whatsoever can be accepted by Knight Frank Australia Pty Ltd for any loss or damage resultant from

any use of, reliance on or reference to the contents of this document. As a general report, this material

does not necessarily represent the view of Knight Frank Australia Pty Ltd in relation to particular

properties or projects. Reproduction of this report in whole or in part is not allowed without prior

written approval of Knight Frank Australia Pty Ltd to the form and content within which it appears.

You can also read