Presentation Slides UBS ASEAN Conference 2012 - Finanznachrichten

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Presentation Slides

UBS ASEAN Conference 2012

Monday, 3 September 2012

Moving People, Enhancing Lives

To be the customer’s choice by providing a safe,

reliable and friendly travel experience that is

enhanced through convenient and innovative

services

CORE VALUES

Excellence

Respect

Responsibility & Recognition

Commitment to the public,

shareholders & employees

Multi-Modal Land Transport Operator

MRT LRT Bus

Fare

Business

Engineering

Taxi Rental & Advertising Consultancy & Services

Non-fare

Business

3

Business Segmentation

FY2012 Revenue (S$1.06b)

Rental Eng & Others

7% 3%

Advertising

3%

Taxi

11%

Rail

Bus 55%

21%

Fare Business : 75.7% of Revenue and 38.6% EBIT

Non-Fare Business: 24.3% of Revenue and 61.4% EBIT

4

Fare Business – At A Glance

• Dominant rail operator in Singapore with 25 years of

O&M experience since 1987

• Operates the North-South East-West Line and Circle

Line with 78 stations and total route length of 128.6km

• Commands about 78% market share with average daily

ridership of 1.8 million

• Operates first LRT system at Bukit Panjang since 1999

• Network comprises 7.8km of elevated guide ways

linking 14 stations in Bukit Panjang

• Average daily ridership of 51,500

North-South East-West Line

Circle Line

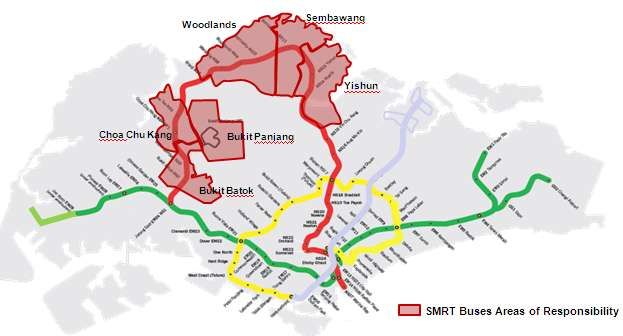

• Owns about 1,050 buses running 94 basic bus services

between Western and North-Western areas and the rest North-East Line

of Singapore

• About 25% market share based on average daily

ridership of 888,000

5

License and Operating Agreement

Ownership of

Ownership Of

Non- Operating Maintenance Terms

Operating Assets

Assets

License effective from 1998

- 2028 (30 years)

NSEW Line Pays nominal annual

license Fee

Complies with performance

standards

License effective from 2009

*First 10 years

(10+30 years)

Circle Line Pays nominal annual

license Fee

Complies with performance

standards

*Operating assets (trains, signaling systems , automatic fare collection systems etc) for CCL are paid and owned by LTA for the first

10 years. SMRT trains will have to purchase the operating assets after 10 years based on its net book value.

6

Regulated Fare Adjustments

*Formula to yield maximum fare adjustment for the year:

0.5 x CPI + 0.5 x WI – 1.5%

where 1.5% is the productivity index valid for 3 years;

CPI is Consumer Price Index and WI is Wage Index

*Formula is currently being reviewed by the Fare

Review Mechanism Committee (FRMC).

Implementation of

50 Distance-based fare in July 2010;

40 expiry of temporary 3% fare rebate

25 25

1.7 1.1 0.7 1.0

0.5

-4.6

2006 2007 2008 2009 2010 2011

Rebates (cents) 1 Actual Fare Increment (%)

1 Transfer rebates are applicable for the second and subsequent legs of a public transport trip

7

Rising Rail and Bus Ridership

(Millions)

700.0 14.0%

654.4

603.9

600.0 12.6% 12.0%

536.6

510.2

500.0 469.3 10.0%

434.9 8.7%

8.3%

7.9%

400.0 8.0% Trains

7.0%

Buses

300.0 6.0% Train yoy growth

5.1% 5.2%

4.9%

Buses yoy growth

3.9%

200.0 4.0%

270.3

2.6% 311.2 326.4

277.3 288.0 290.8

1.9%

100.0 2.0%

0.7%

0.0 0.0%

FY2007 FY2008 FY2009 FY2010 FY2011 FY2012

For monthly ridership figures, please refer to http://www.smrt.com.sg/AboutSMRT/InvestorRelations/KeyOperatingMatrix/Trains.aspx

8

Expanding the MRT Network

New Opportunities!

Thomson Line

30km underground line to relieve

crowding on NS Line

Expected to open in 2019

Eastern Region Line

13km underground line to relieve

crowding on EW Line

Expected to be completed by 2020

Tuas West Extension Marina Bay Extension

Extends from Joo Koon station Connects to the Marina Bay Cruise centre.

7.5km, 4 stations Expected to be completed in 2014

Expected to be completed by 2016

9

Bus Business

New Eco-friendly MAN A22 Buses

94 Public Bus Services

Fleet Expansion - 954 buses in FY2010 to

more than 1,050 buses

45 chartered bus services SMRT Buses operates 6 bus interchanges, 3 depots and 2 bus terminals.

More than 50 buses and mini-buses

BSOL agreement

10 year license due in Sept 2016

Bus routes to operate are awarded as part of license

PTOs have to comply with QoS standards – Reliability; Loading; Availability; Safety

Fare formula similar to trains

Upgrading more than 300 articulated buses

over the next five years.

10Fare Historical Financials

Fare Revenue ($m) EBIT from Fare Operations ($m)

700 140.0 130.4

128.9 129.3

580.0 113.1

600 120.0

536.5

483.5 489.4

500 445.5 100.0 90.7

400 80.0

300 60.0

207.2 213.1 220.4

195.9 199.7

200 40.0

100 20.0

1.5 (4.9) (11.6)

(1.9) (1.7)

0.0

0

2008 2009 2010 2011 2012

2008 2009 2010 2011 2012

(20.0)

Bus Rail Bus Rail

*Rail financials include MRT and LRT

11Non-Fare Business - At A Glance

• Manages and leases a fleet of more than 3,000 taxis, with more than 95% average

hired-out rate

• Approximately 12% market share; continuing to renew & expand taxi fleet

RENTAL

• Leases approximately 34,400sqm of commercial space within the train network

• More than 720 shop units with 98% occupancy rate

• Refurbished a total of 43 stations (78 stations in network) since FY2005

• Provides advertising spaces on trains, buses, taxis and stations

• Leverage on growing riderships and interactive media platforms to attract

advertisers – e.g iViewSMRT, iMobSMRT etc.

• Pursuing overseas land transport opportunities

• Pursuit of opportunities relating to O&M franchises, consultancy and training,

focusing on the Middle East and Asia Pacific markets

12Taxi Industry Landscape

Singapore taxi fleet operators and fleet size

TOL agreement

10 year license from 1 June 2003

License fee payable is based on 0.1% of revenue derived from taxi operations

Current QOS based on Taxi Availability, Safety, Customer Satisfaction

13Diverse Taxi Fleet

Chevrolet Epica Taxi Chrysler Taxi Mercedes-Benz Taxi

London Cab 7-Seater SPACE Taxi Paratransit Taxi

14

14Growing Rental & Advertising

Launch of Orchard

Launch of Launch of

$m Esplande

Xchange & Jurong

3 Xchanges East Xchange

Xchange

90.0

81.5

80.0 73.6

70.0 65.0

63.0

57.5 57.0

60.0

50.8

46.5

50.0

42.0

40.0

30.9

30.9

30.0 25.4

22.5 22.5

19.8

20.0 19.2

17.2

15.0 15.0

13.1

10.0

0.0

FY2008 FY2009 FY2010 FY2011 FY2012

Rental Revenue Rental EBIT Advertising Revenue Advertising EBIT

15Developing Commercial Opportunities

Raffles Xchange (1,300 sqm)

Raffles Xchange (2,600 sqm)

Total 9 Xchanges with

lettable space of over

14,000 sqm

Chua Chu Kang Xchange (100 sqm) Chua Chu Kang Xchange (1,000 sqm)

16New Rental Opportunities

Adding about 1,700 sqm by end FY2013

Bayfront Marina Bay Woodlands Xchange

Gardens by the Bay

Marina Bay Financial Centre

• Approximately 80 sqm • Approximately 300 sqm • Approximately 1,400 sqm

•Connects to several tourist • Connects to offices, retail space • 50 shop units

attractions: - and event grounds:

• Gardens by the Bay • Marina Bay Financial Centre • High passenger volume with

• Marina Bay City Gallery • Marina Bay Link Mall commuters travelling to/from

• Marina Bay Sands • The Promontory@ Marina Malaysia

Bay

1717Mobile Advertising

Wide network of trains & stations, buses & interchange & taxis

Increasing Ridership

Captive Audience with average 17.7 min exposure per journey

Trains

Concept Trains – Exterior,

Windows, Hangars, etc

Taxis Buses

18Advertising Solutions

Trackside Fare Gates

Stairways

Plasma Frame Benches

Platform Screens

Floor Stickers

Event Spaces

19Innovative Digital Platforms

iMobSMRT

Projection

Screen @

Orchard

iViewSMRT

iMobSMRT allows commuters with Near Field

Communication (NFC) tags or Quick Response (QR) Digital posters integrated with eyeball tracking technology to monitor your

codes to make transactions and exchange digital content audiences. The tracking software is integrated on iViewSMRT screens to capture

via their smartphones. the number of people looking at the ads.

20Engineering & International Business Operations & Maintenance (Consultancy, Training, Operator) Engineering (Consultancy & project management) Upgrading/Enhancement of SMRT’s assets

Current Projects

China

1. 49% equity stake in Shenzhen Zona

2. Project Management for Dalian Metro

Dubai Metro Advertising Dalian Metro

UAE

1.Metro, Bus & Marine Fleet Advertising in Dubai

2.Safety Operations Readiness Assessment Consultancy - Masdar City

Personal Rapid Transit System

3.Cost and operational review for Dubai RTA

South Korea

Project Management Consultancy

Singapore

for ShinBundang Line Consultancy, Project Management

& Maintenance for Sentosa Express

Masdar PRT India

Safety audit for Mumbai Monorail

Sentosa Express

22Engineering Solutions

Enhancing SMRT’s rail assets with in-house technology

Implemented in train stations; potential to offer solutions to overseas

operators

TITAN Automatic Fare Gates

Staris Travel and Information System

23Delivering Stable Financial Returns

Historical Financial Performance

Revenue vs PAT ($m)

1200.1 20

18.7 18.9

18.5 19

1000.1

18

16.6

17

800.1

16

600.1 15

1,057.2

969.7 13.4 14

879.0 895.1

400.1 802.1

13

12

200.1

11

149.9 162.7 169.5* 161.1 141.6*

0.1 10

2008 2009 2010 2011 2012

Group Revenue PAT PAT Margin

*Before Bus goodwill impairment of S$6.6 m (2010) and S$21.7m (2012)

25Historical Financial Performance

930.6

Operating Expenses Trend ($m)

794.3

741.0

716.9

645.0

13.9% 16.6% 14.1% 15.4% 17.9%

0.9%

2.3%

19.0% 18.8% 20.3%

20.1%

20.2% Energy costs

9.8% 10.7% Impairment of goodwill

9.2% 9.8%

9.1%

16.4% Other operating expenses

15.4% 15.8% 15.0%

13.9% Repairs and maintenance costs

Depreciation of PPE*

Staff and related costs

40.9% 38.7% 39.8% 39.5% 36.5%

FY2008 FY2009 FY2010 FY2011 FY2012

*Depreciation of PPE net of amortization of asset related grant

26Historical Financial Performance

Fare Vs Non-Fare

Revenue(S$m) EBIT(S$m)

1200 250

1,057.2

969.5 204.9 195.7

1000 200

894.9 187.1

879.0 256.7 176.3

802.1 219.9 170.0*

800 743.3 205.8 77.5

188.2 143.0 61.6

160.7 150 45.9 84.3

140.4

600 34.9 90.7

100

400 749.6 800.5

641.4 690.7 689.1

602.9 130.4 125.5 127.4

200 50 108.1 111.4

79.0

0

0

2007 2008 2009 2010 2011 2012

2007 2008 2009 2010 2011 2012

Fare Non-fare

Fare Non-Fare

*Excludes Bus goodwill impairment of S$21.7m

27Sound Financial Position

Strong Cashflow From Operations S$’m

400.0

300.0

200.0

326.6 283.3 282.1

100.0 163.4

148.0

0.0

FY2008 FY2009 FY2010 FY2011 FY2012

Solid Balance Sheet Net Cash Gross Gearing DEBT/ EBIDTA

As at 31 March 2012 $$45.3m 19.0% 0.5X

S&P Rating: AAA

Capex FY13 Budget ~ Approx S$500m FY12: S$496.1m

28Maintaining Shareholder Value

cents

Dividend Policy

10.00 82%

80% 80%

Endeavour to maintain or increase dividend

9.50

79% payout each year in terms of cents per share,

80%

9.00 78% targeting a minimum payout ratio of 60% of

8.50 PATMI per year for the interim and final ordinary

78%

8.00 dividend.

7.50 76%

7.00 Policy takes into account our long term objective

8.50 8.50 74% of maximising shareholder value, the availability

6.50 7.75 7.75

7.45 of cash and retained earnings, our expected

6.00

72%

72% financial performance and projected capital

5.50 expenditure and other investment plans.

5.00 70%

FY2008 FY2009 FY2010 FY2011 FY2012

DPS (cents) Payout %

29Going Forward

Evolving Maintenance Regime to recognize

ageing & increased usage

Early Detection Systems

S$900m asset renewal plan to be spread

over 8 years, which will be co-shared with

LTA.

Main items will change-out of sleepers

along the ballasted tracks on the NSEWL

(approx $600m) and resignalling works Resleepering

Resignalling to overcome obsolescence

and improve headway from 120s to 100s;

fully bi-directional (Approx $200m)

31Government Initiatives

Spending S$60 billion to double rail network from 138km to 278km by 2020

Extensions to the North South and East West Lines

Three major lines will be added to the existing rail network in the coming years.

I. Downtown Line (estimated completion by 2017)

II. Thomson Line (estimated completion by 2018)

III. Eastern Region Line (estimated completion by 2020) Source: Singapore Budget 2012

S$1.1 billion Bus Services Enhancement Programme (BSEP)

Adding about 800 buses (or 20% increase) over next 5 years.

The Government will fund the purchase of 550 buses from 2012 till 2016. The fund also includes

the operating costs for 10 years.

The remaining 250 buses will be purchased by Public Bus Operators.

The significant increase in bus capacity is expected to reduce crowding and waiting times.

32Key Takeaways

Near Term Long Term

Operating cash flow remains strong New Land Transport Master Plan in 2013

Improving service reliability of Trains and New Rail opportunities open for bidding

Buses

Fare Formula Review

Growing Train & Bus ridership

New Rail Financing Framework

Growing Rental & Advertising income

Bus business sustainability needs to be

Pressure from rising staff cost and addressed

depreciation but volatility of energy cost

is capped through hedging Developing commercial opportunities

adjacent to train network & overseas

$900 million asset renewal plan over 8

years, mitigated through cost sharing

arrangement with LTA

33

33Factsheet

MARKET STATISTICS

Company SMRT Corporation Ltd

Listing Status SGX Main Board since 26 July 2000

Share price S$1.640 (30 August 2012)

Issued Shares 1,520,217,046

Market Capitalization S$2.5 billion

P/E ratio (trailing) 20.8 X

P/NAV 3.15 X

Dividend Yield 4.5% (FY2012 total dividend: 7.45cents)

Major Shareholders Temasek Holdings (Private) Limited – 54.23%, Capital Group – 3.37%

9. J.P. Morgan Securities Singapore Private

1. CIMB Research Pte Ltd

Limited

2. Citigroup Global Markets Singapore Pte Ltd

10. Kim Eng Research Pte Ltd

3. CLSA Singapore Pte Ltd

11. Macquarie Securities (Singapore) Pte Ltd

Analyst Coverage 4. Credit Suisse

12. Nomura Singapore Ltd

(16 Houses) 5. DBS Vickers Securities (Singapore) Pte Ltd

13. OCBC Investment Research Pte Ltd

6. Deutsche Securities Asia Limited

14. Phillips Securities Research Pte Ltd

7. DMG & Partners Research Pte Ltd

15. UBS Securities Pte Ltd

8. HSBC Global Research

16. UOB Kay Hian Research Pte Ltd

34Disclaimer

The statements or information in this presentation which are not of historical fact may constitute “forward looking

statements” relating to financial trends for future periods, compared to the results for previous periods, financial

forecasts, profit projections, or expected growth of SMRT. These statements if any are “forward looking

statements” and accordingly, are only predictions. These statements are based on management's current

views, expectations and assumptions including, but not limited to, prevailing or future economic and market

conditions.

These forward looking statements involve known and unknown risks, uncertainties and other factors that may

cause the actual results, performance or achievements or events to differ materially from those in the statements

as originally made. Such statements are not, and should not be construed as a representation as to future

performance of SMRT.

Therefore, we advise you not to place undue reliance on those statements. In particular, such targets should not be

regarded as a forecast or projection of future performance of SMRT. It should be noted that the actual performance

of SMRT may vary significantly from such targets. SMRT do not represent or warrant the actual future results,

performance or achievements of SMRT will be as discussed in those statements.

For enquiries from analysts/investors, please contact:

Roger Ng; Investor Relations

Tel: (65) 6331 1211 Fax: (65) 6334 1407

Email: ngroger@smrt.com.sg

Visit http://www.smrt.com.sg/investors/investors.asp for media releases, announcements and presentations

35You can also read