One-Asia Morning Focus - May 14, 2020

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

May 14, 2020

One-Asia Morning Focus

Top story: Samsung Electronics (005930 KS/Buy/TP: W68,000)

- For 2021, we forecast SEC’s foundry capex at W9.2tr or higher, which we estimate will translate into a roughly

W40tr boost to the company’s value.

- We believe SEC’s conservative DRAM investments will help keep DRAM prices steady.

- In NAND, we believe SEC will continue to execute massive capex and enjoy a dominant earnings share.

Today’s reports

Asia Strategy – Buy the two worst performing markets: Indonesia and India

YG Entertainment (122870 KQ/Trading Buy/TP: W36,000) Downgrade rating/Lower TP – Concerts halted

Pan Ocean (028670 KS/Buy/TP: W4,000) Raise TP – Expectations on 2H20 turnaround remain intact

KEPCO KPS (051600 KS/Buy/TP: W40,000 Lower TP – IPP strength to continue

Emart (139480 KS/Buy/TP: W190,000) – Moderate 1Q20 results; Look for improvement in 2H20

Netmarble (251270 KS/Buy/TP: W130,000) Raise TP – Earnings to rebound in 2Q20

Banks – April financial market trends: Corporate loans register another record increase

Global performance monitor: Two-day change (%)

Asia xJPN World EM World DM Korea Japan China Taiwan HK India Indonesia Singapore Thailand

Index -1.01 -0.72 -1.28 -0.02 -0.14 -1.03 -0.91 -1.46 1.61 -2.71 -1.27 0.42

Growth -0.25 -0.82 -1.99 0.63 0.85 -0.85 -1.26 -1.30 2.30 -2.11 -1.27 -0.11

Value -1.22 -1.16 -2.10 -0.82 -1.23 -1.28 -0.54 -1.64 0.96 -3.46 -1.28 1.00

Semicon. & equip. -1.53 -1.55 -2.08 -1.33 0.77 1.52 -1.09 0.24 N/A N/A N/A N/A

Tech hardware & equip. -1.21 -1.22 -1.03 0.37 -0.54 0.43 -0.36 -0.25 3.46 N/A -0.13 N/A

Comm. & prof. services -0.25 -0.25 -0.97 4.32 0.98 1.09 -0.53 N/A -3.31 -1.72 N/A N/A

Software & services 0.74 0.47 -1.93 -1.09 3.94 -0.15 0.96 -0.55 1.64 N/A -3.84 N/A

Media & entertainment -0.41 -0.33 -1.62 2.28 2.96 1.04 4.40 0.71 4.21 N/A -3.94 N/A

Consumer goods -1.59 -1.53 -1.07 -3.76 0.42 -0.10 -1.35 0.60 3.27 0.93 N/A -1.16

Consumer services -0.90 -0.32 -1.92 -7.19 0.14 -1.65 -0.11 -2.26 6.25 -4.71 -0.72 0.34

F&B & tobacco 0.66 0.18 0.14 1.96 0.79 2.09 -0.73 -0.45 0.84 0.59 12.64 1.52

Food & staples retailing -0.22 -0.92 -0.26 1.15 2.54 3.13 -0.02 -0.21 2.03 N/A -0.70 -2.47

Retailing -1.75 -1.13 -1.55 -1.48 -1.37 -0.04 -1.52 -2.21 1.30 -7.08 -0.80 1.65

HH & personal products -1.01 -1.27 0.11 -0.27 1.29 2.06 -2.16 N/A -1.29 2.32 N/A N/A

Pharma & life sciences 0.01 0.17 -0.16 2.13 2.91 2.47 0.75 -2.99 -1.27 1.24 N/A N/A

Autos & parts -1.02 -0.98 -1.33 -1.50 -3.25 -1.58 -2.54 -0.66 3.34 -4.70 N/A N/A

Transportation -0.54 -0.67 -1.28 -0.75 -1.90 -0.89 -0.52 -0.82 6.03 -9.60 -7.50 0.79

Capital goods -1.11 -0.91 -1.53 -1.39 -0.41 -0.26 -2.53 -1.43 4.48 N/A -0.67 N/A

Materials -1.03 0.27 -0.66 -0.32 -0.88 -0.44 -1.42 N/A 3.96 -1.47 N/A 1.03

Real estate -2.29 -2.01 -3.41 -1.97 -3.38 -1.20 -1.30 -2.46 6.19 -7.91 -2.57 0.69

Energy -2.93 -1.10 -1.10 -2.45 0.42 -1.09 -1.64 0.46 -3.74 -3.35 -1.05 2.00

Banks -0.97 -0.79 -1.66 -1.60 -0.71 -0.85 -0.73 -1.19 5.25 -4.20 -1.04 0.71

Diversified financials -0.03 -0.81 -1.69 -1.93 -1.17 -0.07 -0.34 0.63 5.79 N/A -0.37 4.74

Telecom services -0.54 -0.08 0.03 2.45 -0.04 -1.14 -0.46 -1.98 4.20 -1.62 -1.88 -0.72

Utilities -0.73 -0.86 -0.21 -0.02 1.87 0.09 0.40 -0.63 4.64 -4.32 N/A -0.44

This publication contains summaries of reports prepared by Mirae Asset Daewoo Co., Ltd. and/or its non-US affiliates (“Mirae Asset Daewoo”). Please review the compliance notices contained in

the original reports. Information and opinions contained herein have been compiled in good faith from sources deemed to be reliable. However, the information has not been independently

verified. Mirae Asset Daewoo makes no guarantee, representation, or warranty, express or implied, as to the fairness, accuracy, or completeness of the information and opinions contained in this

document. Mirae Asset Daewoo accepts no responsibility or liability whatsoever for any loss arising from the use of this document or its contents or otherwise arising in connection therewith.

Information and opinions contained herein are subject to change without notice. This document is for informational purposes only. It is not and should not be construed as an offer or solicitation

of an offer to purchase or sell any securities or other financial instruments. This document may not be reproduced, further distributed, or published in whole or in part for any purpose.

May 14, 2020

One-Asia Morning Focus

Key thematic ETFs: Change (%) Market movers

Mkt cap US dollar total returns (%)

Name Ctry Sector

Robotics & AI (Global X) (US$mn) 1D 1M 3M 6M 1Y 3Y

Cloud Computing (Global X) Top seven performers

Lithium & Battery (Global X) Hartalega MY Healthcare 6,931 17.8 19.3 39.1 62.1 78.9 226.3

Internet of Things (Global X) Top Glove MY Healthcare 5,517 16.6 39.5 52.0 102.7 95.0 280.4

Digitalisation (iShares) Samsung SDI KR Information tech. 17,605 9.1 27.5 -11.1 26.5 37.7 89.0

FinTech (Global X) Bandhan Bank IN Financials 5,384 7.9 32.1 -47.2 -57.3 -57.2 NA

Genomics & Biotech (Global X) Axis Bank IN Financials 15,475 7.1 -0.3 -47.7 -44.3 -47.1 -29.0

Health & Wellness (Global X) Adani Ports & SEZ IN Industrials 8,334 6.3 19.0 -19.9 -19.2 -19.5 -24.5

Ageing Population (iShares) UltraTech Cement IN Materials 13,588 6.2 3.7 -24.6 -17.5 -23.3 -30.6

EM Consum Growth (iShares)

Clean Energy (iShares)

Singapore Airlines SG Industrials 8,357 -6.9 -7.6 -35.3 -40.4 -40.5 -43.0

Water Resources (Invesco)

Barito Pacific ID Materials 7,027 -6.6 36.5 -11.8 7.3 42.6 250.2

Agribusiness (iShares)

Nestle India IN Consumer staples 21,105 -5.3 0.5 -4.9 11.3 52.8 116.7

Global Infrastructure (iShares)

SM Prime Holdings PH Real estate 16,404 -3.5 -4.5 -32.1 -26.3 -23.1 -9.7

ESG US Leaders (iShares)

NCsoft KR Commun. services 12,935 -3.4 10.2 10.8 32.8 38.2 96.6

2D 10D

(9) (6) (3) 0 3 6 9 Gulf Energy Dev. TH Utilities 12,806 -3.0 11.0 -1.9 9.5 80.6 NA

Global Power Synergy TH Utilities 6,331 -2.9 9.7 -8.1 -17.9 33.3 161.6

MSCI valuations (DM, EM, Asia ex-JP)

14 12M forward P/E (x) 18 2.0 12M trailing P/B (x) 2.8

17

13 2.6

1.8

16

2.4

12 1.6

15

2.2

14

11 1.4

2.0

13

10 1.2

12 1.8

9 11 1.0 1.6

May-19 Aug-19 Nov-19 Feb-20 May-19 Aug-19 Nov-19 Feb-20

MSCI Asia ex-JP (L) MSCI World EM (L) MSCI World DM (R) MSCI Asia ex-JP (L) MSCI World EM (L) MSCI World DM (R)

MSCI 12M forward P/E (x) Currencies

(vs. USD) Value Change (%)

Korea Vietnam 1D 3M YTD

12

KRW 1,223.8 -0.09 3.46 5.82

11 19

CNY 7.1 0.07 1.63 1.84

10

16 JPY 107.1 -0.11 -2.46 -1.44

9 IDR 14,885.0 -0.13 8.81 7.22

8 13 HKD 7.8 0.00 -0.20 -0.53

TWD 29.9 -0.02 -0.36 -0.34

7

May-19 Aug-19 Nov-19 Feb-20

10 SGD 1.4 0.18 2.13 5.47

May-19 Aug-19 Nov-19 Feb-20

THB 32.1 -0.18 3.02 7.06

Indonesia 20 India INR 75.5 -0.07 5.80 5.73

17

PHP 50.3 -0.09 -0.48 -0.76

15 18 MYR 4.3 -0.08 4.52 5.79

VND 23,347.5 0.06 0.46 0.76

13 16

11 14

Commodities

9

Latest Change (%)

12

May-19 Aug-19 Nov-19 Feb-20

May-19 Aug-19 Nov-19 Feb-20

close 1D 3M YTD

Crude oil (US$/bbl) 29.6 0.0 -55.8 -56.3

17

Hong Kong

13

China Thermal coal (US$/tonne) 58.6 0.0 -11.5 -12.6

Iron ore (US$/tonne) 87.8 1.3 -5.2 -4.1

15 12

Copper (US$/tonne) 5,234.0 0.1 -15.1 -15.0

Nickel (US$/tonne) 12,275.0 0.7 -12.8 -12.3

Tin (US$/tonne) 15,417.0 0.1 -10.1 -8.5

13 11

Gold (US$/ozt) 1,704.4 0.5 11.8 12.2

Palm oil (INR/tonne) 688.8 -0.1 -21.6 -20.9

11 10

May-19 Aug-19 Nov-19 Feb-20

Soybean oil (c/lb) 24.6 -1.9 -30.2 -28.3

May-19 Aug-19 Nov-19 Feb-20

Corn (US$/bu) 3.1 1.2 -22.1 -21.4

Wheat (US$/bu) 5.2 -0.6 -6.9 -6.6

Source: FactSet, Mirae Asset Daewoo Research (updated on 5/13/20 at 23:00 KST)

Samsung Electronics

(005930 KS)

Bet on potential returns on invested capital

Technology

Investment points

Initiation Report I. Increased visibility on foundry capex to drive up valuation: For 2021, we forecast

May 14, 2020 Samsung Electronics’ (SEC) foundry capex at W9.2tr or higher, which we estimate will

translate into a roughly W40tr boost to the company’s value.

II. Lower DRAM investments to support structural earnings growth: We believe SEC’s

conservative DRAM investments will help keep DRAM prices steady, leading to

(Initiate) Buy sequential earnings growth and the opening of a structural growth phase.

III. NAND market share expansion to boost earnings: We expect SEC’s NAND capex to

Target Price (12M, W) 68,000 far exceed the market average. We believe SEC will continue to execute massive capex

and enjoy a dominant earnings share in the NAND market.

Share Price (05/13/20, W) 48,550

Earnings outlook

Expected Return 40% For 2Q20, we forecast SEC to post revenue of W48.1tr (-14.3% YoY, -13.1% QoQ) and

operating profit of W5.9tr (-10.4% YoY, -8.3% QoQ). By business division, we expect: 1)

operating profit of W5.2tr for semiconductor; 2) an operating loss of W0.6tr for display;

OP (20F, Wbn) 30,807

3) operating profit of W1.2tr for IT & mobile communications (IM); and 4) operating

Consensus OP (20F, Wbn) 32,904

profit of W0.3tr for consumer electronics (CE).

EPS Growth (20F, %) 11.2

We estimate foundry capacity will expand 43,000 wpm in 2020 and 53,000 wpm in

Market EPS Growth (20F, %) 28.1

2021. With a utilization rate at the 90% level, we expect such capacity expansion to lead

P/E (20F, x) 13.8

to revenue growth. For 2020, we forecast the foundry and system LSI division to see

Market P/E (20F, x) 12.8

revenue of W17.3tr (+17.3% YoY) and OP margin of 10.4%. For 2021, we forecast the

KOSPI 1,940.42

division to deliver revenue of W21.3tr (+23.3% YoY) and OP margin of 13.4%, as foundry

Market Cap (Wbn) 289,833 supplies to Qualcomm and Nvidia should gather traction.

Shares Outstanding (mn) 6,793

Initiate coverage with Buy rating and target price of W68,000

Free Float (%) 74.8

Foreign Ownership (%) 55.0 We initiate our coverage on SEC with a Buy rating and target price of W68,000. We

Beta (12M) 0.97 derived our target price using a SOTP methodology, applying an average EV/EBITDA of

52-Week Low 41,200 5.9x to 2020F EBITDA estimates. By division, we applied an EV/EBITDA multiple of 5.3x

52-Week High 62,400 for semiconductor, 4.0x for display, 10.7x for IM, and 5.5x for CE. We believe our target

multiple of roughly 6.0x is highly reasonable, representing only a 14.7% premium to

(%) 1M 6M 12M the average 2020F EV/EBITDA of pure memory names Micron and SK Hynix.

Absolute 0.5 -7.5 13.8

Relative -5.4 1.2 22.0

160 Samsung Electronics KOSPI

140

120

100

80

60

5.19 9.19 1.20 5.20

Mirae Asset Daewoo Co., Ltd.

[Semiconductors] FY (Dec.) 12/17 12/18 12/19 12/20F 12/21F 12/22F

Revenue (Wbn) 239,575 243,771 230,401 218,366 255,586 299,150

Young-gun Kim

+822-3774-1448 OP (Wbn) 53,645 58,887 27,769 30,807 45,409 53,642

younggun.kim.a@miraeasset.com OP margin (%) 22.4 24.2 12.1 14.1 17.8 17.9

Yumi Cha NP (Wbn) 41,345 43,891 21,505 23,903 34,545 40,186

+822-3774-1770 EPS (W) 5,421 6,024 3,166 3,519 5,086 5,916

yumi_cha@miraeasset.com ROE (%) 21.0 19.6 8.7 9.1 12.2 13.1

P/E (x) 9.4 6.4 17.6 13.8 9.5 8.2

P/B (x) 1.8 1.1 1.5 1.2 1.1 1.0

Dividend yield (%) 1.7 3.7 2.5 3.3 3.7 3.7

Note: All figures are based on consolidated K-IFRS; NP refers to net profit attributable to controlling interests

Source: Company data, Mirae Asset Daewoo Research estimates

Analysts who prepared this report are registered as research analysts in Korea but not in any other jurisdiction, including the U.S.

PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS IN APPENDIX 1 AT THE END OF REPORT.

May 14, 2020 Samsung Electronics

Investment points

Point I: Increased visibility on foundry capex to drive up valuation

SEC’s 2021 foundry capex to reach at least W9.2tr (+77% YoY)

For 2021, we forecast SEC’s foundry capex at W9.2tr or higher, which we estimate will

translate into a roughly W40tr boost to the company’s value (based on TSMC’s average ROIC

of 23.5% and P/E of 18x). We believe that capital recovery seems very likely in the 7nm-or-

below segment, in which the company enjoys a duopoly alongside TSMC.

Technological and capital requirements form high barriers to entry

Amid massive capital investments by leading foundries and logic chipmakers, the threat of

new entrants has been easing significantly. During the most recent five years, pure memory

players invested an average of US$7.9bn annually, while foundry/logic firms executed

average capex of US$11.6bn. SMIC, the leading Chinese foundry, spent a meager US$2bn

annually.

Moreover, in 7nm-or-below processes, SEC and TSMC have held a duopoly since

GlobalFoundries ceased all 7nm development in 2018. For reference, there are five

foundries/integrated device manufacturers (IDMs) in the 20nm segment and around 10 in

40nm. We note that Intel is scheduled to begin 10nm production shortly, and could

potentially pursue a node shrink to 7nm.

Another barrier to entry is the limited availability of lithography machines, which are

essential to fabrication at 7nm or below (excluding TSMC’s N7 process). ASML usually ships

only around 10 EUV lithography machines quarterly, and in 2Q20, only two units were

shipped amid the COVID-19 outbreak. Demand for EUV lithography systems is rising due to

their adoption in memory chip production, and players that fail to secure the machines will

be unable to migrate to the 7nm process.

Figure 1. Annual capex trends and forecasts for global semiconductor companies

(US$bn)

20 Intel TSMC SK Hynix

Micron SMIC

15

Foundry/logic 5Y avg. capex: US$11.6bn

10

Pure memory 5Y avg. capex: US$7.9bn

5

0

2006 2008 2010 2012 2014 2016 2018 2020F

Source: Thomson Reuters, Mirae Asset Daewoo Research

Mirae Asset Daewoo Research 2

May 14, 2020 Samsung Electronics

Figure 2. GlobalFoundries ceased 7nm development in August 2018

Source: GlobalFoundries, Mirae Asset Daewoo Research

Figure 3. Foundry players by process node

28 25 18 13 13 9 6 5 3 2(3) 2(3)

Silterra

X-FAB

DB하이텍

ADI ADI

Atmei Atmei

Rohm Rohm

Sanyo Sanyo

Mitsubishi Mitsubishi

ON Semiconductor ON Semiconductor

Hitachi Hitachi

Cypress Cypress Cypress

Sony Sony Sony

Infenion Infenion Infenion

Sharp Sharp Sharp

Freescale Freescale Freescale

Renesas Renesas Renesas Renesas Renesas

Toshiba Toshiba Toshiba Toshiba Toshiba

Fujitsu Fujitsu Fujitsu Fujitsu Fujitsu

Texas Instrument Texas Instrument Texas Instrument Texas Instrument Texas Instrument

Panasonic Panasonic Panasonic Panasonic Panasonic Panasonic

STMicro STMicro STMicro STMicro STMicro STMicro

UMC UMC UMC UMC UMC UMC

IBM IBM IBM IBM IBM IBM IBM

SMIC SMIC SMIC SMIC SMIC SMIC SMIC SMIC

GF(AMD) GF(AMD) GF(AMD) GlobalFoundries GlobalFoundries GlobalFoundries GlobalFoundries GlobalFoundries

Intel Intel Intel Intel Intel Intel Intel Intel Intel (Intel) (Intel)

Samsung Samsung Samsung Samsung Samsung Samsung Samsung Samsung Samsung Samsung Samsung

TSMC TSMC TSMC TSMC TSMC TSMC TSMC TSMC TSMC TSMC TSMC

180nm 130nm 90nm 65nm 45nm/40nm 32nm/28nm 22nm/20nm 16nm/14nm 10nm 7nm 5nm

Source: WikiChip, Mirae Asset Daewoo Research

Figure 4. ASML: Lithography equipment shipments by technology

(Units)

80 I-line KrF ArF dry ArF immersion EUV

60

40

20

4 7 7 8

0 2

4Q13 2Q14 4Q14 2Q15 4Q15 2Q16 4Q16 2Q17 4Q17 2Q18 4Q18 2Q19 4Q19

Source: ASML, Mirae Asset Daewoo Research

Mirae Asset Daewoo Research

May 14, 2020 Samsung Electronics

Demand for SEC’s 7nm-or-below products to expand

Qualcomm: Mass production of 5nm modem chips to start in 2021

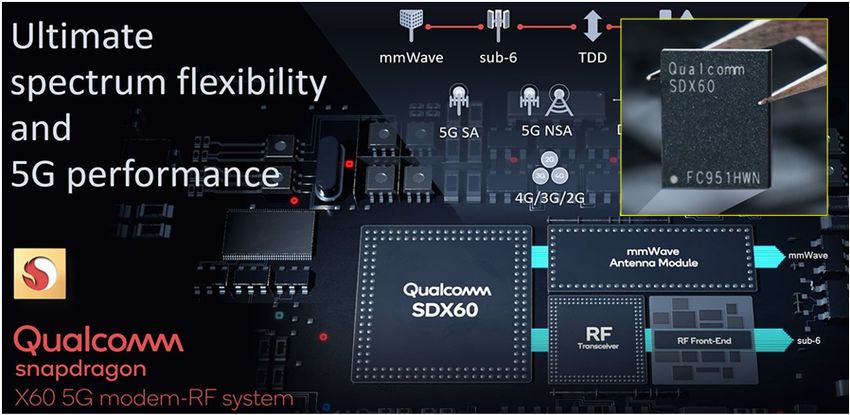

SEC’s foundry unit has won orders for Qualcomm’s Snapdragon X60, the world's first 5nm

5G baseband modem, with mass production scheduled to begin in 2021. We note that,

beginning with the Snapdragon 865 5G platform, Qualcomm has separated its modem and

application processor (AP) orders. While SEC will provide X60 modem chips built on its 5nm

low-power early (LPE) process, TSMC will supply APs built on its N5 process.

Order volumes should be dictated by 5G smartphone demand. Qualcomm is looking for

450mn smartphone sales in 2021 and 750mn units in 2022, and Strategy Analytics forecasts

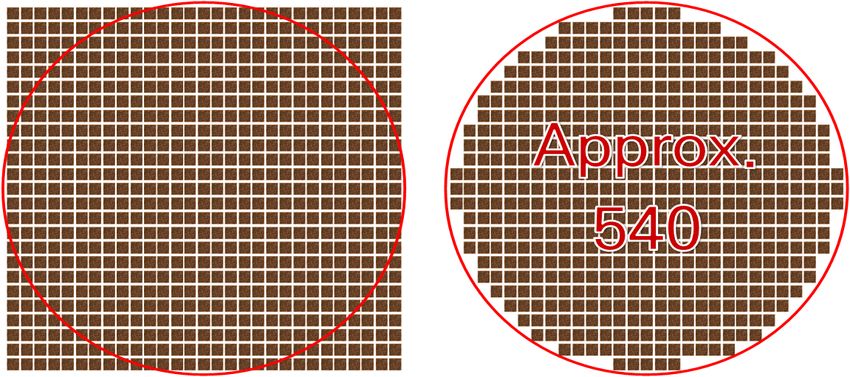

Qualcomm’s 5G modem shipments at 150mn units. The exact die size of the X60 is not yet

known, but based on the Snapdragon 845’s relatively small die size (91mm2), the production

of 150mn chips annually will require capacity of 30,000 wpm (12”). If mass production

progresses smoothly in 2021, Qualcomm could decide to use SEC’s 4nm LPE process to

manufacture its 5G modems in 2022, in which case additional capex will be needed in 2021.

Figure 5. Snapdragon X60 modem chip to be produced on SEC’s 5nm process (2021)

Source: Qualcomm, Mirae Asset Daewoo Research

Figure 6. 5G smartphone shipment estimates

(mn units) (%)

1,000 5G smartphone shipments 950 80

5G smartphone penetration

Qualcomm est.:

750mn

750 60

Qualcomm est.:

450mn 600

500 40

400

250 190 20

70

0 0

2019 2020F 2021F 2022F 2023F

Source: Gartner, Mirae Asset Daewoo Research

Mirae Asset Daewoo Research

May 14, 2020 Samsung Electronics

Figure 7. 5G baseband shipment forecasts

(mn units)

400 SEC

Qualcomm

300 110

243

200 63

140

27 248

100

180

6 113

1 32

0 6

2019 2020F 2021F 2022F 2023F

Source: Strategy Analytics, Mirae Asset Daewoo Research

Figure 8. Snapdragon 845 die

9.5mm

Source: TechInsights, Mirae Asset Daewoo Research

Figure 9. Snapdragon 845 production: 540 dies per wafer (12”)

Source: Company materials, Mirae Asset Daewoo Research

Mirae Asset Daewoo ResearchMay 14, 2020 Samsung Electronics

Nvidia: Ampere architecture rollout in 2020

One of the key events for SEC’s foundry business this year will be the start of mass

production for Nvidia’s next-generation graphic processing units (GPUs) based on the new

Ampere microarchitecture. After lengthy negotiations, SEC is believed to have taken mass

production orders for the new GPUs, which Nvidia is set to showcase at the GPU Technology

Conference (GTC) scheduled for May 14th. While Ampere has been rumored to be designed

for the 7nm process, actual production is expected to take place on the 8nm node.

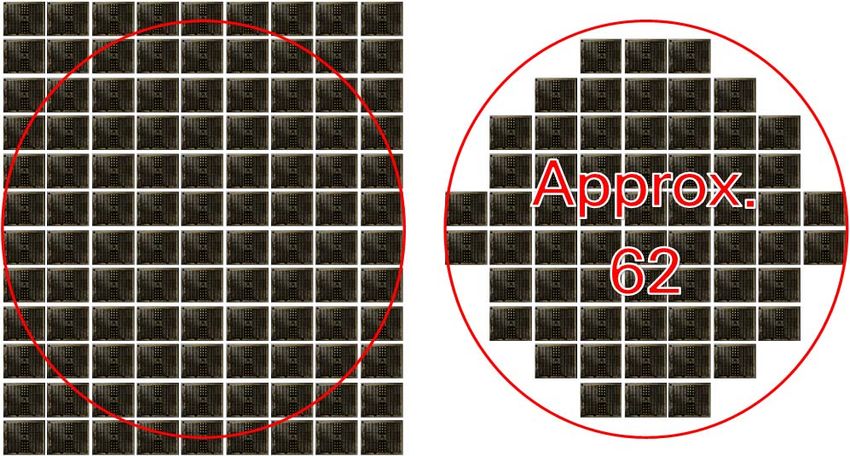

Nvidia’s GPU dies are larger than those of SEC’s existing chips. For instance, the die size of

Nvidia’s TU106 GPU (Turing) is 445mm2, around five times larger than that of the

Snapdragon 845 (91mm2). The upcoming Ampere chips are believed to feature a larger die

size than existing GPUs, given its sharply increased transistor count despite the use of the

7nm process.

A larger die size generally implies higher foundry capacity requirements. Accordingly, SEC

will need to add capacity to handle mass production. Considering that larger chips suffer

from greater wafer yield losses than smaller chips, successful production of Nvidia’s new

GPU will help SEC establish a strong track record in large-sized chip mass production.

We forecast SEC’s foundry revenue from Nvidia at W0.8tr in 2020 and W2.5tr in 2021.

Table 1. Nvidia GPU specifications

Name GK180 GM200 GP100 GV100 TU106 GA100 GA103 GA104

Architecture Kepler Maxwell Pascal Volta Turing Ampere Ampere Ampere

Transistor count 7bn 8bn 15bn 21bn 11bn 30bn+ Approx. 22bn Approx. 16bn

Process 28nm 28nm 16nm FinFET+ 12nm FFN 12nm FFN 7nm 7nm 7nm

Die size 551mm2 601mm2 610mm2 815mm2 445mm2 Huge Big Moderate

Launch date 3Q20 3Q20 2021

Source: Nvidia, Mirae Asset Daewoo Research

Figure 10. Nvidia GPU (Turing) production: 62 dies per wafer (12”)

Source: Company materials, Mirae Asset Daewoo Research

Mirae Asset Daewoo ResearchMay 14, 2020 Samsung Electronics

AMD vs. Intel rivalry in 2022 and beyond

The CPU rivalry between Intel and AMD is intensifying. In recent years, AMD has gained

ground with its 7nm technology, while Intel has been held back by delays to the launch of

its 10mn process and poor yields. The primary foundries with which AMD does business are

TSMC (7nm) and GlobalFoundries (14nm+). With Intel already planning to migrate to 7nm

due to poor 10nm yields, AMD will likely have to adopt 5nm to maintain competitiveness.

According to recent press releases, AMD is aiming to kick off 5nm mass production in 2021,

with TSMC handling manufacturing. Meanwhile, the company is likely to gradually replace

its 14nm CPUs with 7nm CPUs, but this migration should prove complicated given

GlobalFoundries’ abandonment of 7nm development. As such, in 2021, we believe that AMD

will decide between: 1) relying solely on TSMC for chip manufacturing; or 2) choosing to

partner with SEC. We believe that both options will be beneficial to SEC. Indeed, even

though the first scenario will not directly benefit the Korean giant, it should be positive to

overall supply/demand dynamics given the likely increase in capacity utilization on 7nm-or-

below processes.

Figure 11. Intel’s manufacturing road map: 7nm CPUs in 2021

Source: Company materials, Mirae Asset Daewoo Research

Figure 12. AMD’s CPU and GPU manufacturing road map: 7nm already in place

Source: Company materials, Mirae Asset Daewoo Research

Mirae Asset Daewoo ResearchMay 14, 2020 Samsung Electronics

All in all, we think there are three major factors that will affect SEC’s foundry demand in

2021 and beyond:

1) 5nm production for Qualcomm’s 5G modems and potential orders for 4nm fabrication

2) Successful mass production of Nvidia’s new Ampere GPU

3) Whether the company can displace GlobalFoundries to become one of AMD’s two primary

7nm-or-below manufacturing foundry partners

For 45nm+ processes, leading-edge capacity utilization is already high at major foundries

(including SEC); this means that ramp-ups will be required to meet additional demand.

Furthermore, Qualcomm, Nvidia, and AMD—all of which are growing increasingly reliant on

SEC and/or TSMC—are forecast to report above-market revenue growth in the coming

years. The three companies are projected to report combined growth of 19.0% in 2020 and

20.6% in 2021, while the other PHLX Semiconductor Sector Index constituents are

anticipated to display growth of 6.3% and 10.2%, respectively.

Figure 13. Global foundry utilization: Leading-edge utilization for 45nm+ is near full capacity

('000 wafers) (%)

24,000 Capacity (L) Shipments (L) 120

Foundry utilization (R) Leading-edge utilization (R) 101.0

95.8

91.5 91.0 90.2

18,000 90

12,000 60

6,000 30

0 0

1Q17 3Q17 1Q18 3Q18 1Q19 3Q19 1Q20F 3Q20F

Source: Gartner, Mirae Asset Daewoo Research

Figure 14. PHLX Semiconductor Sector Index constituents: Revenue and growth forecasts

(US$bn) (%)

400 AMD (L) Nvidia (L) Qualcomm (L) 90

Other PHLX (L) Qualcomm YoY (R) Nvidia YoY (R)

AMD YoY (R) Other PHLX YoY (R)

300 60

200 30

100 0

0 -30

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020F 2021F

Source: Thomson Reuters, Mirae Asset Daewoo Research

Mirae Asset Daewoo ResearchMay 14, 2020 Samsung Electronics

Given the strong demand prospects, we anticipate that SEC’s foundry business, which is

operating at near full capacity, will need additional capacity of 40,000 wpm in 2020. Fabs

that are well positioned to add capacity include the S3, S4 (Line 11 for CIS), and S5 (EUV line).

In 2021, we project that SEC will need additional capacity of 50,000 wpm, which translates to

capex of W9.2tr (+76.3% YoY). Among the firm’s facilities, we think the new P2 fab in

Pyeongtaek is best positioned to add capacity. While others (P3 in Pyeongtaek and S2 in the

US) could also be considered for expansion, we believe P2 will be first in line given its

existing back-end infrastructure, etc.

Table 2. SEC: Foundry wafer capacity trends and forecast (‘000 wpm)

Group Fab Site Wafer size Products 2016 2017 2018 2019 2020F 2021F

Line 4 Giheung 150mm (6") LED 55 55 55 55 55 55

Line 5 Giheung 200mm (8") CIS, smart card IC 50 50 50 50 50 50

Legacy fab

Line 6 Giheung 200mm (8") PMIC, DDI, CIS 80 80 80 80 80 80

Line 7 Giheung 200mm (8") RF/IoT, FPS 70 70 70 70 70 70

Line 8 Giheung 200mm (8") 70 70 70 70 70 70

S1 Line 14 Giheung 300mm (12") Logic (AP, etc.), CIS 45 45 45 45 45 45

Line S Giheung 300mm (12") 40 40 40 40 40 40

S2 SAS Austin 300mm (12") Logic (AP, etc.) 50 50 50 50 50 50

Quarter of Line

S3 Hwaseong 300mm (12") 7-10nm, EUV 0 3 18 20 30 40

17

S4 Line 11 Hwaseong 300mm (12") CIS 0 2 11 15 23 25

V1 EUV fab Hwaseong 300mm (12") 7nm or below (planned), EUV 0 0 0 0 23 30

New fab - - 300mm (12") 7nm or below (planned), EUV 0 0 0 0 1 19

Total wafer capacity (12" equiv.) 269 274 302 314 334 379

Source: Mirae Asset Daewoo Research

Figure 15. SEC: Foundry capacity trend Figure 16. SEC: Foundry capex trend

('000 wafers) (Wtr) (%)

SEC foundry capex (L)

10 300

400 YoY (R) 9.2

Total capacity

Total capacity (12" equiv.)

300 8 200

6.7

5.2

200 5 100

100 3 0

0 0 -100

2008 2010 2012 2014 2016 2018 2020F 2005 2007 2009 2011 2013 2015 2017 2019 2021F

Source: Mirae Asset Daewoo Research Source: Mirae Asset Daewoo Research

Mirae Asset Daewoo ResearchMay 14, 2020 Samsung Electronics

High visibility on ROIC for leading-edge foundry investments

We believe visibility on the the ROIC outlook for SEC’s foundry investments is improving

amid: 1) rising barriers to entry; and 2) signs of structural demand growth.

Our analysis of global pure semiconductor plays shows that memory manufacturers such as

Micron and SK Hynix exhibit high ROIC volatility due to the cyclical nature of the memory

industry and the high sensitivity of supply/demand dynamics to capex. In contrast,

semiconductor manufacturers such as Intel and TSMC have generally managed to keep

their ROIC steady at around 25%, as: 1) non-memory facility investments are unlikely to

cause oversupply; and 2) the oligopolistic market structure ensures a high likelihood of

capital recovery.

Going forward, SEC is likely to concentrate its capex in 7nm-or-below processes, where new

competition is unlikely to emerge. As mentioned earlier in this report, we project that SEC

will execute foundry capex of W9.2tr in 2021 to meet growing demand. We believe that once

a consensus on the scale of capex is formed, the firm’s foundry investments will be priced

into shares. Assuming SEC’s foundry ROIC matches TSMC’s level (23.5%), we believe that

TSMC’s valuation multiple (18x P/E) should be applied to earnings on invested capital. This

would add roughly W39tr (18x W2.2tr) to SEC’s market cap.

Figure 17. ROIC by semiconductor manufacturer

(%)

50 SEC SK Hynix TSMC Micron

SMIC UMC Intel

TSMC ROIC avg.: 23.5x

25

0

-25

-50

1Q10 1Q11 1Q12 1Q13 1Q14 1Q15 1Q16 1Q17 1Q18 1Q19

Source: Thomson Reuters, Mirae Asset Daewoo Research

Figure 18. TSMC’s 12-month-forward P/E

(x)

24

18 18.0

Avg. since 2019: 18.0x

12

6

0

1/15 10/15 7/16 4/17 1/18 10/18 7/19 4/20

Source: Thomson Reuters, Mirae Asset Daewoo Research

Mirae Asset Daewoo ResearchMay 14, 2020 Samsung Electronics

We believe the case of TSMC illustrates how the market reflects capex into share price. The

foundry player’s 12-month-forward P/E—which gradually rose from an average of 13x in

2016 to 15x in 2017 and 16x in 2018—displayed its sharpest rise ever in 2019. Indeed, while

2020-21 earnings forecasts were left virtually unchanged last year, the stock’s valuation

increased by 20%.

We believe the re-rating was driven by capex outlook upgrades rather than by earnings

forecasts. While earnings projections stayed flat, market expectations for TSMC’s 2020

capex were revised upward by 30% in the second half of 2019. As a consensus formed that

the firm’s investments would translate safely into earnings, upward revisions to capex

projections were accompanied by market value expansion. Like TSMC, we expect SEC to see

a valuation re-rating driven by a promising foundry investment outlook.

Figure 19. TSMC: Quarterly capex Figure 20. TSMC: Quarterly OP

(US$bn) (US$bn)

6.0 6.0

4.5 4.5

3.0 3.0

1.5 1.5

0.0 0.0

1Q15 1Q16 1Q17 1Q18 1Q19 1Q20F 1Q21F 1Q15 1Q16 1Q17 1Q18 1Q19 1Q20F 1Q21F

Source: Thomson Reuters, Mirae Asset Daewoo Research Source: Thomson Reuters, Mirae Asset Daewoo Research

Figure 21. TSMC: 12-month-forward P/E Figure 22. TSMC: OP and capex consensus throughout 2019

(x) (US$bn)

22 21 2020F OP

20.8

2021F OP

2020F capex

19 18

18.0

15.9

16 16.3 15

14.6

12.9

13 12

10 9

1/16 7/16 1/17 7/17 1/18 7/18 1/19 7/19 1/19 3/19 5/19 7/19 9/19 11/19

Source: Thomson Reuters, Mirae Asset Daewoo Research Source: Thomson Reuters, Mirae Asset Daewoo Research

Mirae Asset Daewoo ResearchMay 14, 2020 Samsung Electronics

Point II: Lower DRAM investments Structural earnings growth

We expect SEC to remain conservative on DRAM investments, in light of the following

factors:

1) The firm needs to channel resources to its foundry business. Against this backdrop, we

believe that SEC is likely to remain conservative on DRAM investments to keep

secmiconductor capex at an appropriate level relative to EBITDA.

2) Conservative DRAM investments will help stabilize DRAM prices. The DRAM industry’s

expansion is driven by price increases rather than by bit growth. When the demand outlook

is subdued (as it is currently), price stability, not shipment growth, holds the key to

maximizing market share gains and margins.

3) Even if SEC makes aggressive capital investments to increase its market share, well-

financed rivals are likely to follow suit. We believe aggressive DRAM capex is more likely to

cause DRAM price declines than to bring about the desired result.

All in all, SEC’s conservative DRAM investments should help keep DRAM prices steady,

leading to sequential earnings growth and the opening of a structural growth phase. For

2020, we estimate that the firm will execute W7.2tr (-11.1% YoY) in DRAM capex (or wafer

capacity additions of 40,000 wpm), and that DRAM ASP will continuously increase, driving

quarterly earnings growth.

Figure 23. SEC: DRAM capex trend Figure 24. SEC: DRAM wafer capacity trends

(Wtr) SEC DRAM capex (L) (%) ('000 wpm)

16 YoY (R) 300 100 Increase

13.7 Decrease

Avg. capacity chg. 60

12 200 50 39 40

30 30

21

15 14

8.1 7.8

8 7.2 100 0

-15 -19

4 0 -50

0 -100 -100

2005 2008 2011 2014 2017 2020F 2014 2015 2016 2017 2018 2019 2020F 2021F

Source: Mirae Asset Daewoo Research Source: Mirae Asset Daewoo Research

Figure 25. SEC: DRAM ASP trend Figure 26. SEC: DRAM revenue and OP forecasts

(%) (Wbn) (%)

30 16,000 Revenue (L) OP (L) OP margin (R) 80

15 12,000 60

53.0

0 8,000 40

32.2

-15 4,000 20

-30 0 0

1Q14 1Q15 1Q16 1Q17 1Q18 1Q19 1Q20P 1Q21F 1Q16 1Q17 1Q18 1Q19 1Q20P 1Q21F

Source: Mirae Asset Daewoo Research Source: Mirae Asset Daewoo Research

Mirae Asset Daewoo ResearchMay 14, 2020 Samsung Electronics

Rationale behind our conservative DRAM capex outlook: 1) SEC needs to make

room for foundry capex

As we highlighted in our first investment point, SEC needs to significantly increase its

foundry capex in 2021. However, the foundry business does not yet generate enough

EBITDA to fund the required capex. We estimate foundry capex executed in 2017 and 2019

was equivalent to more than 150% of the EBITDA generated in the respective year. In our

view, SEC needs to secure sufficient funds for investment within the semiconductor

business, while also striking a balance between EBITDA and capex. We believe the

semiconductor division’s overall capex has never once exceeded 70% of EBITDA since 2014.

We think conservative spending on DRAM is a sensible move from this perspective. More

disciplined DRAM capex would allow SEC to generate stable profits (rather than expand

market share) and dedicate more resources to the foundry business. After expanding

capacity through aggressive capex in the past, TSMC has now entered a virtuous cycle, in

which the company is making stable profits from its facilities following the end of

depreciation, which is, in turn, leaving more room for investments in advanced processes.

Similarly, we believe the DRAM business can serve as a cash cow for SEC. In 2020-21, we

forecast DRAM capex to be W15.0tr. We expect DRAM EBITDA to be around W52.2tr. Even

after taking into account foundry capex of W14.6tr, this should be enough to still keep the

semiconductor division’s overall EBITDA/capex ratio at 50.0%, in line with the level seen

during the 2018 memory up cycle.

Figure 27. SEC foundry business: EBITDA and capex Figure 28. SEC semiconductor business: EBITDA and capex

(Wbn) Foundry EBITDA (%) (Wbn) Total semiconductor EBITDA (%)

10,000 Foundry capex 200 80,000 Total semiconductor capex 100

Capex/EBITDA

Capex/EBITDA

161.7

150.8

7,500 132.5 150 60,000 68.7 75

68.3

54.5

99.4 55.0 50.3

47.3 50.0

5,000 93.8 100 40,000 50

80.1

38.2

2,500 56.3 61.4 50 20,000 25

0 0 0 0

2014 2015 2016 2017 2018 2019 2020F 2021F 2014 2015 2016 2017 2018 2019 2020F 2021F

Source: Mirae Asset Daewoo Research Source: Mirae Asset Daewoo Research

Figure 29. SEC DRAM business: EBITDA and capex Figure 30. TSMC: EBITDA and capex

(Wbn) DRAM EBITDA (%) (US$bn) TSMC capex (%)

48,000 DRAM capex 60 32 TSMC EBITDA 100

Capex/EBITDA

85.7 Capex/EBITDA

78.8 79.3

75.7

71.1

36,000 45 24 75

40.0

58.8 60.0

39.2 34.5 33.8 55.2

31.3 51.8

48.0 47.6

24,000 26.6 30 16 50

24.3

12,000 15 8 25

0 0 0 0

2014 2015 2016 2017 2018 2019 2020F 2021F 10 11 12 13 14 15 16 17 18 19 20F

Source: Mirae Asset Daewoo Research Source: TSMC, Thomson Reuters, Mirae Asset Daewoo Research

Mirae Asset Daewoo ResearchMay 14, 2020 Samsung Electronics

Rationale behind our conservative DRAM capex outlook: 2) SEC needs to keep

DRAM prices stable

DRAM revenue and profit growth moves in tandem with price changes. It is safe to say that

during the past decade, DRAM revenue and profits have never increased during periods of

price decline. Unlike the NAND market, whether DRAM revenue and profits grow is

determined by whether ASP is rising or falling (not by the price elasticity of shipments), with

bit growth largely fixed.

That said, aggressive pricing strategies do work during down cycles. In 2016 and 2019, SEC

was able to either expand or maintain its market share (45.3% 48.0% in 2016; 43.9%

43.7% in 2019) by employing an aggressive bit growth strategy. During these years,

operating profit across the DRAM industry declined 30.7% and 66.6%, respectively, but SEC’s

share of overall profits increased from 58.3% to 68.8% and from 47.9% to 52.0%,

respectively. In other words, the company’s strategy of overcoming market downturns

through preemptive inventory depletion worked well.

However, the DRAM cycle is set to undergo a recovery from 2020. In this case, maintaining

stable prices is likely to take priority over aggressive spending or shipments. Due to SEC’s

conservative capex stance, we expect quarterly ASP to move up in 2020. The uptrend in ASP

should continue through 2021, driving strong profit growth. We forecast SEC’s DRAM

operating profit to grow 12.1% to W13.5tr in 2020 and 55.1% to W21.0tr in 2021.

Figure 31. Global DRAM: ASP, bit, revenue, and OP growth

(%) ASP chg. Bit growth Sales growth OP growth

240

160

2011-12

Industry-wide losses

80

50.4 47.1

28.6 26.6 34.1

22.8 23.7 19.9 21.0 19.0

2.3 14.8

0

-0.9

-20.0 -27.0

-29.8

-49.9 -46.7

-80

2011 2012 2013 2014 2015 2016 2017 2018 2019

Source: DRAMeXchange, Mirae Asset Daewoo Research estimates

Figure 32. SEC DRAM business: ASP, bit, revenue, and OP growth

(%)

240 ASP chg. Bit growth Sales growth OP growth

160

80

49.8 54.1 48.2

30.1 35.8

27.1 25.8 19.5 23.1 21.1

14.7 16.7

12.3 3.9

0

-6.3 -5.0 -9.1

-17.5

-29.3 -29.7

-45.8 -49.2

-80

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020F 2021F

Source: Company data, Mirae Asset Daewoo Research estimates

Mirae Asset Daewoo ResearchMay 14, 2020 Samsung Electronics

Figure 33. Global DRAM: M/S by revenue

Others

Nanya

Powerchip

ProMOS

Elpida

Micron

45.3 48.0 45.8 43.9 43.7 SK Hynix

36.9 42.3 40.9 39.6

33.3 36.7

SEC

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Source: DRAMeXchange, Mirae Asset Daewoo Research estimates

Figure 34. Global DRAM: M/S by OP

3.6

12.8 10.6

7.5 18.6 18.1 20.9 21.5

27.9 Nanya

25.2

24.1 28.5 Powerchip

34.5 28.9

30.5 29.1 25.1

ProMOS

99.7 100.0 Elpida

72.1 68.8 Micron

59.8 58.3

50.9 47.0 51.4 47.9 52.0 SK Hynix

SEC

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Source: DRAMeXchange, Mirae Asset Daewoo Research estimates

Figure 35. Global DRAM: OP trends

(Wtr) (%)

99.7 100.0

75 100

72.1 -66.6%

50 68.8 75

59.8 58.3

50.9

47.0

25 -30.7% 52.0 50

-71.9% 51.4

47.9

-41.9%

0 25

Nanya Powerchip

ProMOS Elpida

Micron SK Hynix

-25 SEC SEC OP share (R) 0

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Note: OP growth figures for 2011 and 2012 represent chg. in the sum of profits, excluding operating losses.

Source: DRAMeXchange, Mirae Asset Daewoo Research estimates

Mirae Asset Daewoo ResearchMay 14, 2020 Samsung Electronics

Rationale behind our conservative DRAM capex outlook: 3) Competitors to follow

suit

If SEC were to execute capex exceeding demand in order to expand its market share, its

competitors would most likely follow suit. SK Hynix has room for an additional 20,000 wpm

at its C2E fab in Wuxi, China, and is set to complete construction of its M16 fab (designed

capacity of around 100,000 wpm). Micron is also likely to complete construction of its

Taichung fab in Taiwan and its Hiroshima fab in Japan by the end of the year. As such, DRAM

makers are well-positioned to increase capacity swiftly if necessary. And considering that

they differ very little in terms of cost competitiveness, any competition to expand capacity

would likely only lead to price declines, rather than market share gains. As such, we expect

SEC to focus its investments on bolstering its cost competitiveness.

Until early this year, many expected SEC to pursue aggressive DRAM capex as part of its

efforts to widen its lead over rivals. During past periods of rapid growth, all DRAM makers

vied for market share gains via capacity additions. But with the market now stable and

controlled by a handful of players, aggressive capex would be a recipe for losses rather than

market share gains. As such, we believe mega-fabs represent the best strategy, and one

that is already adopted by all DRAM makers. By maintaining sufficient room in such facilities

for potential lines and clean rooms, companies can expand capacity flexibly depending on

market conditions, thus preventing unnecessary capex spending based on excessive

projections.

Figure 36. SEC: DRAM breakdown by tech node (%) Figure 37. SK Hynix: DRAM breakdown by tech node (%)

Average tech node factor (R) Average tech node factor (R) 1Znm

100 1Znm 35 100 35

1Ynm

1Ynm

75 30 75 1Xnm 30

1Xnm

23nm

21nm

20nm

50 25 50 25

25nm 25m

25 20 25 29nm 20

35nm

38nm

0 15 0 15

1Q14 1Q15 1Q16 1Q17 1Q18 1Q19 1Q20 1Q14 1Q15 1Q16 1Q17 1Q18 1Q19 1Q20

Source: DRAMeXchange, Mirae Asset Daewoo Research Source: DRAMeXchange, Mirae Asset Daewoo Research

Figure 39. Average tech node factors of three major DRAM

Figure 38. Micron: DRAM breakdown by tech node (%)

makers

Average tech node factor (R) (nm)

100 35

1Znm 35 SEC

SK Hynix

1Ynm

75 30 Micron

30

1Xnm

20nm

50 25

25

25m

25 20

30nm 20

0 15

15

1Q14 1Q15 1Q16 1Q17 1Q18 1Q19 1Q20

1Q14 1Q15 1Q16 1Q17 1Q18 1Q19 1Q20

Source: DRAMeXchange, Mirae Asset Daewoo Research Source: DRAMeXchange, Mirae Asset Daewoo Research

Mirae Asset Daewoo ResearchMay 14, 2020 Samsung Electronics

Point III: NAND market share expansion to boost earnings

We expect SEC’s NAND capex to far exceed the market average for several reasons.

First, competitors’ poor earnings leave them minimal financial room for investments. In

1Q20, most NAND suppliers, with the exception of SEC, recorded losses. In 2016, a pickup in

NAND prices improved margins across the industry, triggering massive capacity expansions.

However, the resulting oversupply drove down SEC’s NAND margins to near breakeven in

2019. We do not expect this situation to recur.

Second, massive NAND capex can stimulate demand. Unlike in the DRAM market, where

growth has been driven by steady price increases, a major driver of NAND market growth

has been the demand stimulated by persistent price declines (given NAND’s nature as a

substitute good). In 2017, however, NAND prices climbed sharply on supply shortages,

slowing the growth of NAND content in client SSDs. In 2018, prices started to fall again,

leading to higher sales volume and content. With the price elasticity of NAND confirmed, we

expect SEC to pursue a bit-growth-oriented strategy for client SSDs. As such, we expect SEC

to continue to execute massive capex and enjoy a dominant earnings share in the NAND

market. In 2020, we expect SEC’s NAND capex to come in at W8.8tr, equivalent to 90,000

wpm.

Figure 40. SEC: NAND capex forecasts Figure 41. SEC: NAND wafer capacity forecasts

(Wtr) (%) ('000 wpm)

16 SEC NAND capex (L) 300 120 Increase 100

Decrease 90

YoY (R) 80

Avg. capacity chg.

12 200 60 47

40 41

9.7 23

8.8 18 11

7.8

8 7.0 100 0

-30

4 0 -60

0 -100 -120

2005 2008 2011 2014 2017 2020F 2014 2015 2016 2017 2018 2019 2020F 2021F

Source: Mirae Asset Daewoo Research Source: Mirae Asset Daewoo Research

Figure 42. SEC: NAND ASP chg. Figure 43. SEC: NAND revenue and OP forecasts

(%) (Wbn) (%)

Revenue (L)

30 12,000 60

OP (L)

OP margin (R)

15 8,000 40

22.4

20.5

0 4,000 20

-15 0 0

1Q16 1Q17 1Q18 1Q19 1Q20P 1Q21F

-30

-4,000 -20

1Q14 1Q15 1Q16 1Q17 1Q18 1Q19 1Q20P 1Q21F

Source: Mirae Asset Daewoo Research Source: Mirae Asset Daewoo Research

Mirae Asset Daewoo ResearchMay 14, 2020 Samsung Electronics

Rationale behind our aggressive NAND capex outlook: 1) Revisit previous cycle

In 1Q20, margins dipped below breakeven for all NAND makers except SEC, which recorded

an OP margin at the low-20% level. The firm accounted for more than 90% of overall NAND

market profits in the quarter. As SEC will likely strive to maintain its current profit share and

margin levels, we believe it will continue to execute capex in line with demand growth.

We believe NAND makers’ 2016-18 capex strategy is worth revisiting. NAND ASP/GB, which

had declined continuously from 1Q10, picked up in 2H16 on wafer capacity shortages

arising from the conversion to 3D NAND. At that time, both first-tier (including SEC) and

second-tier NAND suppliers enjoyed high margins. Amid high margins and optimistic

demand forecasts, NAND makers executed aggressive capex.

Althrough SEC’s NAND capex spending in 2017 was the largest in the industry, its 2018

capex accounted for only 30% of overall market spending. Thus, the firm displayed below-

industry NAND wafer capacity growth and bit growth in 2017-18. In 2018, prices plunged

due to oversupply stemming from aggressive shipments by chipmakers, driving down

NAND makers’ profits to near or below break-even levels. Of note, the easing of the

oversupply seen in 2019 was mainly driven not by demand growth, but by reduced supply

caused by Toshiba Memory’s power outage.

As the NAND market is still not fully concentrated, we think SEC is highly likely to

aggressively ramp up its NAND capex going forward, setting the stage for another game of

chicken among NAND makers. We see NAND prices stabilizing from 2H20 amid a slowdown

in price growth. With upside to NAND prices likely limited, we believe only players capable of

reducing costs will benefit. All in all, we expect SEC to maintain its leading position in the

NAND space (in terms of capex and operating profit) for some time.

Figure 44. Global NAND makers: OP margin trends Figure 45. SEC: NAND capex trend

(%) SEC SK Hynix (Wtr) (%)

80 Micron Intel

16 SEC NAND capex (L) 300

Toshiba

YoY (R)

40 12 200

9.7

8.8

7.8

0 8 7.0 100

-40 4 0

-80 0 -100

1Q11 1Q12 1Q13 1Q14 1Q15 1Q16 1Q17 1Q18 1Q19 2005 2008 2011 2014 2017 2020F

Source: Mirae Asset Daewoo Research Source: Mirae Asset Daewoo Research

Mirae Asset Daewoo ResearchMay 14, 2020 Samsung Electronics

Figure 46. Global NAND makers: Capex trends

(US$mn) (%)

32,000 60

Intel

Micron

24,000 Toshiba/SanDisk 45

SK Hynix

SEC

16,000 SEC share of global NAND capex (R) 30

30.4

8,000 15

0 0

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Source: DRAMeXchange, Mirae Asset Daewoo Research

Figure 47. Global NAND makers: Bit growth trends

(%) SEC Kioxia (Toshiba Memory) Western Digital Micron SK Hynix Total

80

67.5

60

49.9 48.1

45.4

41.6 42.7

40.3

40 34.6 33.4

29.0

26.6 24.7

20

0

2016 2017 2018 2019 2020 2021

Source: DRAMeXchange, Mirae Asset Daewoo Research

Figure 48. Global NAND M/S breakdown in terms of OP

100%

75%

Toshiba

Intel

50% 95.5 Micron

SK Hynix

59.3

25% 45.8 48.3 46.4 SEC

44.3

36.6 38.4 37.3

0%

2011 2012 2013 2014 2015 2016 2017 2018 2019

Source: Company data, Mirae Asset Daewoo Research

Mirae Asset Daewoo ResearchMay 14, 2020 Samsung Electronics

Rationale behind our aggressive NAND capex outlook: 2) Higher client SSD

demand needed

DRAM market growth has been driven mainly by steady price increases. In contrast, a major

driver of NAND market growth has been the demand stimulated by persistent price

declines, given NAND’s nature as a substitute good for hard disk drives (HDDs). Indeed,

NAND ASP/GB has been trending downward since 2007, supporting continuous bit growth.

In 2017, however, the spike in NAND prices caused by supply shortages crippled growth in

SSD penetration and content in PCs. From 2012 to 2016, overall NAND market bit growth

averaged 48.2%, with ASP declining 27.2% annually. In 2017, bit growth slowed to 35.7%,

and ASP climbed 36.9%.

As for enterprise SSDs, bit growth improved to 63.8% in 2017 on the back of stronger

demand for cloud SSDs, even though prices (ASP/GB) declined at a much slower rate of

around 5%. We believe enterprise SSD bit growth was more affected by server-class SSDs—

which benefited from robust server demand—than by storage-class SSDs (HDD substitute).

For smartphone NAND, content per unit expanded 56% YoY in 2017 even though mobile

NAND ASP increased 24.5% YoY. To sum up, for both enterprise SSDs and mobile NAND, the

expansion of applications had a greater impact on bit growth than price changes.

For client SSDs, sales volume and content per PC increased at CAGRs of 27% and 13%,

respectively, from 2012 to 2016. In 2017, these growth rates slowed to 7.6% and 3%,

respectively, as ASP increased 16% YoY. In 2018, prices started to fall again, leading to

higher sales volume and content. With client SSDs’ relatively high price elasticity confirmed,

we expect SEC to pursue a bit-growth-oriented strategy for client SSDs.

Indeed, we see limited upside to top-line growth of the PC SSD market going forward, as

SSDs are already used in a significant portion of consumer PCs. Going forward, we think a

major factor in the market’s growth is highly likely to be the content per unit trend.

For consumer PCs, average SSD content per unit stands at just 351GB, much lower than the

average HDD content range of 1.1TB (2.5”)-2.3TB (3.5”). Going forward, we expect storage

capacity of 1TB+ to become the status quo for consumer PCs. With average spending on

storage capacity per PC likely to remain flattish, we forecast average SDD content per PC to

expand to the level of HDD content in line with SSD price declines.

Figure 49. NAND flash: Bit, sales, and ASP growth trends

(%)

240 ASP chg. Bit growth Sales growth

160 151.2

117.7

77.4

80 68.5 67.7

58.4 51.4

45.3 39.8 46.3 36.9 44.9

35.7 31.7

0

-15.1 -18.1 -22.6 -23.5

-32.1 -30.7 -26.5 -27.6

-41.1 -43.5

-80 -57.0 -62.5

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Source: DRAMeXchange, Mirae Asset Daewoo Research

Mirae Asset Daewoo ResearchMay 14, 2020 Samsung Electronics

Figure 50. Enterprise SSDs: Bit, sales, and ASP growth

(%) Enterprise SSD bit growth

180 Enterprise SSD ASP chg.

Enterprise SSD unit growth

120 111.3

82.7 76.6

62.6 63.8

60 51.9

41.4 37.4 41.8

30.0 32.8 27.4 26

15.3 12.5 10.5 10.3

0

-6 -5

-17

-35

-38 -40 -50

-60

2014 2015 2016 2017 2018 2019 2020F 2021F

Source: Gartner, Mirae Asset Daewoo Research

Figure 51. Storage-class enterprise SSDs: Bit, sales, and ASP Figure 52. Server-class enterprise SSDs: Bit, sales, and ASP

growth trends growth trends

(%) PB chg. ASP/GB chg. Unit growth (%) PB chg. ASP/GB chg. Unit growth

300 300

200 200

100 100 70

50 44

11

0 0

-1 -6

-100 -100

2013 2014 2015 2016 2017 2018 2019 2020F 2021F 2013 2014 2015 2016 2017 2018 2019 2020F 2021F

Source: Gartner, Mirae Asset Daewoo Research Source: Gartner, Mirae Asset Daewoo Research

Figure 53. Client SSDs: Sales volume and content per PC Figure 54. Client SSDs: Content per PC trend

(mn units) PC SSD (L) PC HDD (L) (%) (GB) Mainstream PC SSD content/unit (L) (%, YoY)

600 PC SSD penetration (R) PC SSD unit growth(R) 80 600 Mainstream PC SSD content/unit growth (R) 32

67.7 28.3

59.4

450 60 450 24

51.4

351

46.1

37.2 14.4

300 40 300 16

12.8

29.3 14.0

10.4 15.0

26.7

150 13.3 20 150 8

18.8 7.2 3.0 5.6

7.6

0 0 0 0

2014 2016 2018 2020E 2014 2016 2018 2020E

Source: Gartner, Mirae Asset Daewoo Research Source: Gartner, Mirae Asset Daewoo Research

Mirae Asset Daewoo ResearchMay 14, 2020 Samsung Electronics

Figure 55. Mobile storage (eMMC MLC) spot price trend

(US$/GB) (%)

0.60 30

eMMC MLC QoQ (R)

eMMC MLC price (1GB eq., L)

15.8

0.45 15

6.4 6.2 5.6 4.8

3.9 4.1

1.5 1.6 1.8

0.30 0

-1.4

-4.3 -5.2 -5.8

-7.5 -6.4 -6.9 -6.6

-8.9

0.15 -10.7 -15

-12.5

-16.1

-16.9

0.00 -30

4Q14 3Q15 2Q16 1Q17 4Q17 3Q18 2Q19 1Q20

Source: Trendforce, Mirae Asset Daewoo Research

Figure 56. Mobile storage (eMMC, TLC) spot price trend

(US$/GB) (%)

0.40 30

eMMC TLC QoQ (R)

eMMC TLC price (1GB eq., L)

17.2

0.30 15

9.4

3.8 4.7 5.1

1.9 3.0

0.3 0.5

0.20 0

-1.6 -2.1

-5.2

-7.5 -6.0

0.10 -12.1 -15

-18.1 -17.4

-22.5

0.00 -30

1Q16 3Q16 1Q17 3Q17 1Q18 3Q18 1Q19 3Q19 1Q20

Source: Trendforce, Mirae Asset Daewoo Research

Figure 57. Smartphone NAND content per unit trend

(GB) (%)

Smartphone NAND content/unit (L)

200 56.0 60

YoY growth (R)

150 45

100 30

50 15

0 0

2015 2016 2017 2018 2019 2020F 2021F

Source: IDC, Mirae Asset Daewoo Research

Mirae Asset Daewoo ResearchAsia Strategy

Buy the two worst performing markets:

Indonesia and India

Time to buy the poorest performers on a two-year time horizon

Emerging markets have performed poorly during the course of the global COVID-19

Strategy Report pandemic, with foreign investors pulling money out and local currencies depreciating

against the US dollar. In Asia, the worst performers YTD (in US dollar terms) have been

May 13, 2020 Indonesia and India. While investors are rightfully worried about the business and

economic impacts of the pandemic, history has shown that stock markets and

currencies eventually rebound once crises subside. From this perspective, we have a

positive view on India and Indonesia. Admittedly, it may seem a bit early for such a

Mirae Asset Securities (HK) Ltd. recommendation, but we note that a return to pre-pandemic levels translates to

Joe Liew potential returns of 37% for the JCI and 31% for the Sensex from current levels.

+852-2514-1336

Recovery likely to come, albeit slightly later than in other markets

Joe.liew@miraeasset.hk

Two historical examples—the Asian financial crisis in 1997-98 and the 2008 global

financial crisis—can serve as a guide. In each case, markets in Asia fully recovered one to

PT. Mirae Asset Sekuritas two years after the initial declines. Of note, Indonesia is much stronger now than it was

Indonesia during the Asian financial crisis, with a banking system that is on more solid footing and

a political landscape marked by much lower uncertainty. In India, the government is

Hariyanto Wijaya

beginning to ease restrictions in recognition of the severe economic impact of continued

+62-21-5088-7056 lockdowns. Looking at China, Korea, and Hong Kong, which are further along on the

hariyanto.wijaya@miraeasset.co.id road to recovery, economic activity has picked up significantly over the last month. We

Anthony Kevin also see reason for optimism that a vaccine could be developed in a shorter-than-usual

+62-21-5088-7000 (ext. 165) time frame, given the sheer level of global attention and political will.

anthony.kevin@miraeasset.co.id

Local investors have been buying; smart money?

Foreign investors have been net sellers of Asian stock markets since March. Despite

Mirae Asset Capital Markets

the selling, markets have bounced off their lows (excluding a one-off drop on 23

(India) Pvt. Ltd. March), implying that local investors have been more than able to absorb the selling.

Achala P. Jethmalani As long as there are no shocks to the global financial system (a risk the Fed has

minimized by pumping trillions into the US financial system), we expect local buying

+91-22-6266-1370

(including in Indonesia and India) to continue, providing support to the market.

achala.jethmalani@miraeassetcm.com

Economic activity to trough in 2Q

Mirae Asset Daewoo Co., Ltd. We expect a trough in Indonesia’s and India’s economic activity to occur in 2Q,

Jay (Jaeil) Lee corresponding to the two countries’ peak enforcement of social distancing measures.

Globally, we think restrictions will be relaxed gradually toward the end of 2Q and into

+822-3774-1388

3Q. We project Indonesia’s GDP to contract 1.5% YoY in 2Q before rebounding in 3Q

Jay_lee@miraeasset.com

(+1.5%) and 4Q (+4.5%), and we see India’s GDP falling 5.0% YoY in 2Q before

improving in 3Q (-1.5%) and 4Q (+5.2%). For buy ideas from our research team in

Indonesia, please refer to pages 12-13. For exposure to the Indian market, we would

advise selecting an Indian ETF (e.g., INDY US).

Key risk

The key risk remains the possibility of an especially deep and protracted global

recession caused by COVID-19. This would adversely affect demand for exports out of

Asia as well as global commodity prices.

Economic growth in India and Indonesia to trough in 2Q20

(%)

YoY GDP growth

9 Indonesia India

6

3

0

-3

-6

1Q19 3Q19 1Q20 3Q20F

Source: Bloomberg, Mirae Asset Sekuritas Indonesia Research, Mirae Asset Capital Markets (India) Research

Analysts who prepared this report are registered as research analysts in Hong Kong, Korea, India, or Indonesia, but not in any other

jurisdiction, including the US. PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS IN APPENDIX 1 AT THE END

OF THE REPORT.YG Entertainment

(122870 KQ)

Lineup is back, but concerts come to a halt

Entertainment

1Q20 review: Widely anticipated weakness

For 1Q20, YG Entertainment announced consolidated revenue of W52.8bn (-18.3% YoY;

Company Report all growth figures hereafter are YoY) and an operating loss of W2.1bn (remaining in the

May 14, 2020 red). Fewer artist activities and poor subsidiary earnings were mainly to blame for the

quarterly loss. That said, the weakness stemming from the company’s artist void was

widely anticipated.

At the parent level, the company posted operating profit of W1.9bn (-33.2%).

Elsewhere, losses from YG PLUS (W2.2bn), YGX (dance academy), and YG Japan totaled

(Downgrade) Trading Buy W4bn. Looking at core businesses, album/digital music sales and management

revenue fell 12% and 15.2%, respectively. The company recorded 120,000 copies of

Target Price (12M, W) ▼ 36,000 album sales and recognized concert income from WINNER’s Asia tour and BLACKPINK’s

Japan dome tour (partial). On the non-operating side, the company booked W4.5bn in

valuation losses on securities (Tencent Music Entertainment, etc.).

Share Price (05/13/20, W) 30,650

Lineup is back, but monetization faces challenges

Expected Return 17% Big Bang has finally made its comeback. After a busy global schedule in 2H19,

BLACKPINK looks ready to make its return. The new group Treasure’s debut also

appears imminent. The active presence of five groups with the potential to attract

OP (20F, Wbn) 2

arena-level attendance and the liquidation of loss-making businesses are all positives

to the company.

Consensus OP (20F, Wbn) 18

However, the COVID-19 outbreak has brought concerts to a complete halt, putting a

EPS Growth (20F, %) - break on the company’s artist monetization. Over the past five years, concerts

Market EPS Growth (20F, %) 28.1 (excluding those in Japan) accounted for 13.9% of overall revenue. Further including

P/E (20F, x) 108.3 royalties from Japanese concerts (17.2% of revenue), which directly translate into

profits, concerts represent a significant portion of the company’s revenue.

Market P/E (20F, x) 12.8

KOSDAQ 691.53 Suspension of tours is worrying, given ties to album releases

Because the biggest appeal of concerts is the “liveness” of the experience, we think

Market Cap (Wbn) 558

technology advancements are unlikely to completely fill the gap. We thus believe

Shares Outstanding (mn) 18 entertainment agencies need to focus on propping up other existing revenue sources

Free Float (%) 65.7 (album/digital music/TV appearances), while also taking steps that can boost the

Foreign Ownership (%) 15.8 expected returns on concerts once things get back to normal. However, recent

concerns over a second outbreak suggest the return of live concerts could be further

Beta (12M) 0.80 pushed back. Given that new album releases are typically tied to tour schedules,

52-Week Low 19,450 uncertainties surrounding concerts could lead to a prolonged slump in album releases.

52-Week High 35,850 As of now, Lady Gaga’s new album (which features BLACKPINK) will be released in May,

while Treasure’s debut album is set to come out in July.

(%) 1M 6M 12M

Absolute 9.5 20.0 -8.6

Downgrade to Trading Buy and cut TP to W36,000

Relative -5.5 14.8 -6.4 We cut our target price on YG Entertainment by 10% to W36,000, as we revised down

our 2021F net profit by 10% in light of the uncertainties related to concerts. Due to the

110 YG Entertainment KOSDAQ

reduced upside potential, we downgrade our rating to Trading Buy.

100

We continue to favor YG Entertainment over the other two major entertainment

90 agencies, as we believe the company stands to benefit the most from an improvement

80 in Korea-China relations, given Big Bang/BLACKPINK’s significant presence in China (as

70 demonstrated by recent ads and TV appearances). We are also bullish on the

60 company’s expanding lineup and potential for success in North America (through

50

partnerships and YouTube). For these reasons, we believe the company merits a higher

5.19 9.19 1.20 5.20 valuation. That said, the delays in earnings improvement due to COVID-19 are a

concern. We recommend taking a trading approach, paying attention to both potential

improvements in Korea-China relations and risks of a second wave of infections.

Mirae Asset Daewoo Co., Ltd.

[Media] FY (Dec.) 12/16 12/17 12/18 12/19 12/20F 12/21F

Revenue (Wbn) 322 350 269 264 237 311

Jeong-yeob Park

+822-3774-1652 OP (Wbn) 32 24 20 1 2 31

jay.park@miraeasset.com OP margin (%) 9.9 6.9 7.4 0.4 0.8 10.0

NP (Wbn) 19 18 18 -22 5 26

EPS (W) 1,094 931 911 -1,118 283 1,438

ROE (%) 7.7 5.7 5.1 -6.2 1.5 7.4

P/E (x) 25.9 31.0 52.2 - 108.3 21.3

P/B (x) 1.8 1.6 2.6 1.5 1.6 1.5

Dividend yield (%) 0.7 0.5 0.3 0.0 0.0 0.0

Note: All figures are based on consolidated K-IFRS; NP refers to net profit attributable to controlling interests

Source: Company data, Mirae Asset Daewoo Research estimates

Analysts who prepared this report are registered as research analysts in Korea but not in any other jurisdiction, including the U.S.

PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS IN APPENDIX 1 AT THE END OF REPORT.You can also read