OFFERING MEMORANDUM LITTLE BAY APARTMENTS - 846 Little Bay Ave Norfolk, VA 23503 - LoopNet

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

OFFERING MEMORANDUM

LITTLE BAY APARTMENTS

846 Little Bay Ave • Norfolk, VA 23503

1

NON-ENDORSEMENT AND DISCLAIMER NOTICE

Confidentiality and Disclaimer

The information contained in the following Marketing Brochure is proprietary and strictly confidential. It is intended to be reviewed only by the party receiving it from Marcus & Millichap and

should not be made available to any other person or entity without the written consent of Marcus & Millichap. This Marketing Brochure has been prepared to provide summary, unverified

information to prospective purchasers, and to establish only a preliminary level of interest in the subject property. The information contained herein is not a substitute for a thorough due

diligence investigation. Marcus & Millichap has not made any investigation, and makes no warranty or representation, with respect to the income or expenses for the subject property, the

future projected financial performance of the property, the size and square footage of the property and improvements, the presence or absence of contaminating substances, PCB's or

asbestos, the compliance with State and Federal regulations, the physical condition of the improvements thereon, or the financial condition or business prospects of any tenant, or any

tenant's plans or intentions to continue its occupancy of the subject property. The information contained in this Marketing Brochure has been obtained from sources we believe to be reliable;

however, Marcus & Millichap has not verified, and will not verify, any of the information contained herein, nor has Marcus & Millichap conducted any investigation regarding these matters

and makes no warranty or representation whatsoever regarding the accuracy or completeness of the information provided. All potential buyers must take appropriate measures to verify all of

the information set forth herein. Marcus & Millichap is a service mark of Marcus & Millichap Real Estate Investment Services, Inc. © 2018 Marcus & Millichap. All rights reserved.

Non-Endorsement Notice

Marcus & Millichap is not affiliated with, sponsored by, or endorsed by any commercial tenant or lessee identified in this marketing package. The presence of any corporation's logo or name

is not intended to indicate or imply affiliation with, or sponsorship or endorsement by, said corporation of Marcus & Millichap, its affiliates or subsidiaries, or any agent, product, service, or

commercial listing of Marcus & Millichap, and is solely included for the purpose of providing tenant lessee information about this listing to prospective customers.

ALL PROPERTY SHOWINGS ARE BY APPOINTMENT ONLY.

PLEASE CONSULT YOUR MARCUS & MILLICHAP AGENT FOR MORE DETAILS.

LITTLE BAY APARTMENTS

Norfolk, VA

ACT ID Z0600038

2

LITTLE BAY APARTMENTS

TABLE OF CONTENTS

SECTION

INVESTMENT OVERVIEW 01

Offering Summary

Regional Map

Local Map

Aerial Photo

MARKET COMPARABLES 02

Sales Comparables

Rent Comparables

FINANCIAL ANALYSIS 03

Rent Roll Summary

Rent Roll Detail

Operating Statement

Notes

Pricing Detail

Acquisition Financing

Growth Rate Projections

Cash Flow

MARKET OVERVIEW 04

Market Analysis

Demographic Analysis

3

LITTLE BAY APARTMENTS

INVESTMENT

OVERVIEW

4

LITTLE BAY APARTMENTS

OFFERING SUMMARY

EXECUTIVE SUMMARY

VITAL DATA

Price $690,000 CURRENT YEAR 1

Down Payment 25% / $172,500 CAP Rate 7.08% 7.80%

MAJOR EMPLOYERS

Loan Amount $517,500 GRM 7.41 7,19

Net Operating

Loan Type Proposed New $48,830 $53,836 EMPLOYER # OF EMPLOYEES

Income

Net Cash Flow United States Dept of Navy 4,446

Interest Rate / Amortization 4.75% / 30 Years 14.06% / $24,248 16.96% / $29,255

After Debt Service

Price/Unit $69,000 Total Return 14.06% / $24,248 21.59% / $37,240 USS Wasp Lhd 1 1,500

Price/SF $81.18 Naval Aviation Engrg Svcs 1,100

Number of Units 10 Veterans Affairs Medical Ctr 1,060

Rentable Square Feet 8,500

Commander Atlantic Division 1,000

Year Built 1985

Swells Point Branch Med Clinic 924

Lot Size 0.26 acre(s)

US Atlantic Fleet 700

US Army Future Center 628

US Navy Fleet Training Center 609

UNIT MIX Helicpter Mine Countermeasures 600

NUMBER APPROX. Navy Exchange 600

UNIT TYPE

OF UNITS SQUARE FEET

Walmart 577

2 One Bedroom, One Bathroom 850

8 Two Bedroom, One Bathroom 850

DEMOGRAPHICS

10 Total 8,500

1-Miles 3-Miles 5-Miles

2017 Estimate Pop 4,323 31,912 98,223

2017 Census Pop 4,312 31,631 96,811

2017 Estimate HH 1,960 12,380 39,767

2017 Census HH 1,965 12,327 39,370

Median HH Income $45,788 $48,872 $48,780

Per Capita Income $33,665 $24,598 $27,441

Average HH Income $60,433 $60,656 $66,183

#5

LITTLE BAY APARTMENTS

OFFERING SUMMARY

INVESTMENT OVERVIEW

The Little Bay Apartments offers potential buyers the opportunity to purchase a well-maintained asset with tremendous upside potential. As is, the property offers potential

investors a 14.06 percent cash on cash return and an equally lucrative IRR. By maintaining current operating efficiency’s, controlling vacancy rates, and building on the

rents a purchaser can acquire a long term upside in appreciation.

The Subject Property is serviced by four dynamic corridors in the Hampton Roads area; Hampton Roads Beltway, Tidewater Drive, Granby Street, and E Ocean View

Avenue allowing residents access to Norfolk's top employment drivers including the US Department of Defense, Sentara Healthcare Centers, Old Dominion University,

BAE systems, Norfolk State University and more. Tenants with school-age children have access to public schools a mile away. The Norfolk International Airport, which

serves the entire Hampton Roads, is located only 7.5 miles from the property.

The Hampton Roads economy is supported by manufacturing, maritime and logistics, cybersecurity, biomedical technology, and a dependable military presence. The US

Department of Defense, a major employer for the area, houses eight military installations and the second largest concentration of military personnel in the United States.

Naval Station Norfolk (5.5 miles), the worlds largest naval base employs upwards of 67,000 people and yields 6,200 acres of the Hampton Roads commercial acquisition.

With the inauguration of republican leadership, military funding and employee benefits are expected to grow in salary increases, branch wide budget expansion, and more.

Investors are moving out of major metro areas into secondary and tertiary markets, such as the Hampton Roads/ Tidewater area, in search of higher rates of return.

Although a few distressed assets are still available at cap rates above eight percent, more investors are targeting stabilized properties with higher cash cows. Apartments

near large employers, military bases and institutions of higher learning, such as Old Dominion University, provide a steady renter base with cap rates for Class A/B assets

typically in the seven percent area.

INVESTMENT HIGHLIGHTS

• Turn-Key Asset with Value-Add Potential

• Pristine Chesapeake Bay Beaches within Walking Distance

• 5.5 Miles from Naval Station Norfolk

• 3,500 New Jobs Within Ten Miles Entering Market

• 10 Yr. Levered IRR of 22.63%

6

LITTLE BAY APARTMENTS

OFFERING SUMMARY

PROPERTY OVERVIEW

Marcus & Millichap is pleased to present the exclusive offering memorandum for Little Bay Apartments located in

the Willoughby Split neighborhood of Norfolk, VA. The Subject Property consists of 10 market-rate units built in

1985, and situated on .26 Acres. Little Bay Apartments neighbors Interstate 64; a prominent traffic artery through

the South Hampton Roads region, and a dominant route through The City of Norfolk.

846 Little Bay Avenue consists of (2) one-bedroom, one-bathroom units and (8) two-bedroom, one-bathroom

flats. Located along the beach front, the Subject Property offers an array of ample maritime activities, outdoor

attractions, and a charming waterfront community. Due to a shortage in larger housing for rent and a convenient

location near primary roadways, major military installations, and Downtown Norfolk, this unit mix caters well to

the demographic composition of the sub-market. The Norfolk Premium Outlets is located 9 miles away and

provides tenants with access to the area's premier shopping and dining options.

Chuck Rigney, Director of the Economic Development Department states, “Recently, the City of Norfolk has

played host to many development and redevelopment projects, with over $1 billion in new private/public Common Area Amenities

investments and the addition of close to 6,000 new jobs in 2017.” Downtown Norfolk recently renovated; the

Waterside District ($50 Million), Hilton Main Hotel ($150 Million), The ICON Luxury Apartments ($100 Million), and • Centrally Located Between Banger Pier and

ADP ($32.5 Million). Automatic Data Processing (ADP) is expected to bring an estimated 2,000 jobs to the area East Ocean View Pier

and is anticipated to produce annual regional earnings of about $158 million as the overall economic impact • Water Front Accessibility

climbs to almost $465 million, alone. The Norfolk Premium Outlets, a 332,000 sq. ft outlet mall located 9 miles • 9 Miles from Norfolk Premium Outlets

away, opened June 2017 and has 50 retail and restaurant locations for residents and tourists to experience high-

end shopping. The completion of the outlets adds an additional 500 new full-time jobs to the local sub-market.

Norfolk’s oceanfront, a huge tenant driver to the area, recently completed, “The Nourishment Plan” which Unit Amenities

expanded and heightened the beach along Willoughby Spit. Internationally owned brand, Ikea Furniture Store,

broke ground for construction late last year with completion expected to conclude in mid-2019. This $75 million • HVAC In All Units

investment will provide the area with 500 additional mid-to-low level jobs and authenticate Virginia as a • Ample Off-Street Parking

successful commercial corridor for further international companies to come. • Spacious Floor Plans

• Full Functioning Kitchen

#7

LITTLE BAY APARTMENTS

OFFERING SUMMARY

PROPERTY SUMMARY

THE OFFERING PROPOSED FINANCING

Property Little Bay Apartments First Trust Deed

Price $690,000 Loan Amount $517,500

Property Address 846 Little Bay Avenue, Norfolk, VA Loan Type Proposed New

Assessors Parcel Number 1531380534 Interest Rate 4.75%

Zoning R-12 Amortization 30 Years

SITE DESCRIPTION Loan Term 10 Years

Number of Units 10 Loan to Value 75%

Number of Buildings 1 Debt Coverage Ratio 1.99

Number of Stories 2

Year Built/Renovated 1985

Rentable Square Feet 8,500

Lot Size .26 acre(s)

Type of Ownership Leased Fee/Ground Fee

Parking Off-Street

Parking Ratio 1:1

Landscaping Flat

UTILITIES

Water/Sewer Tenant Paid

Electric/Gas Tenant Paid

CONSTRUCTION

Foundation Concrete Slab

Exterior Wood Joist/Brick

Parking Surface Asphalt

Roof Flat

MECHANICAL

HVAC Electric

Fire Protection City Code

8

LITTLE BAY APARTMENTS

LOCATION SUMMARY

BANGER

PIER

EAST OCEAN VIEW

FISHING PIER

L I T T L E B AY

APARTMENTS

CHESAPEAKE BAY

BEACHES

NAVAL STATION

NORFOLK JOINT BASE

LITTLE CREEK – FORT STORY

NORFOLK

PREMIUM OUTLETS

MACARTHUR CENTER

SHOPPING MALL

DOWNTOWN

NORFOLK

DOWNTOWN

NORFOLK

9

LITTLE BAY APARTMENTS

REGIONAL MAP

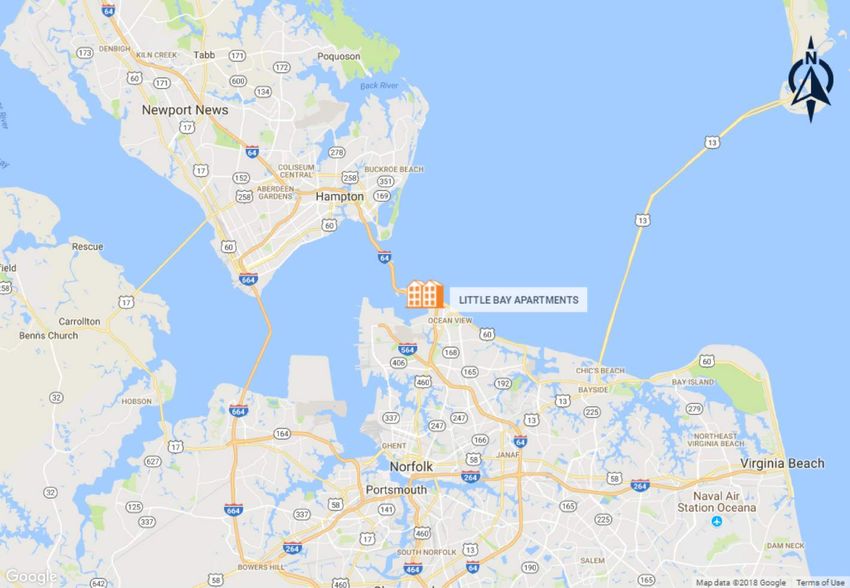

10LITTLE BAY APARTMENTS

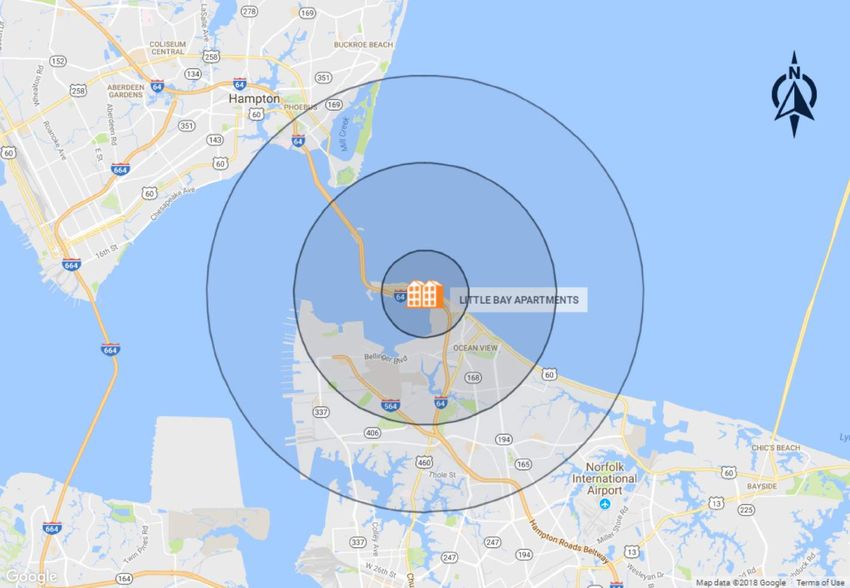

LOCAL MAP

11LITTLE BAY APARTMENTS

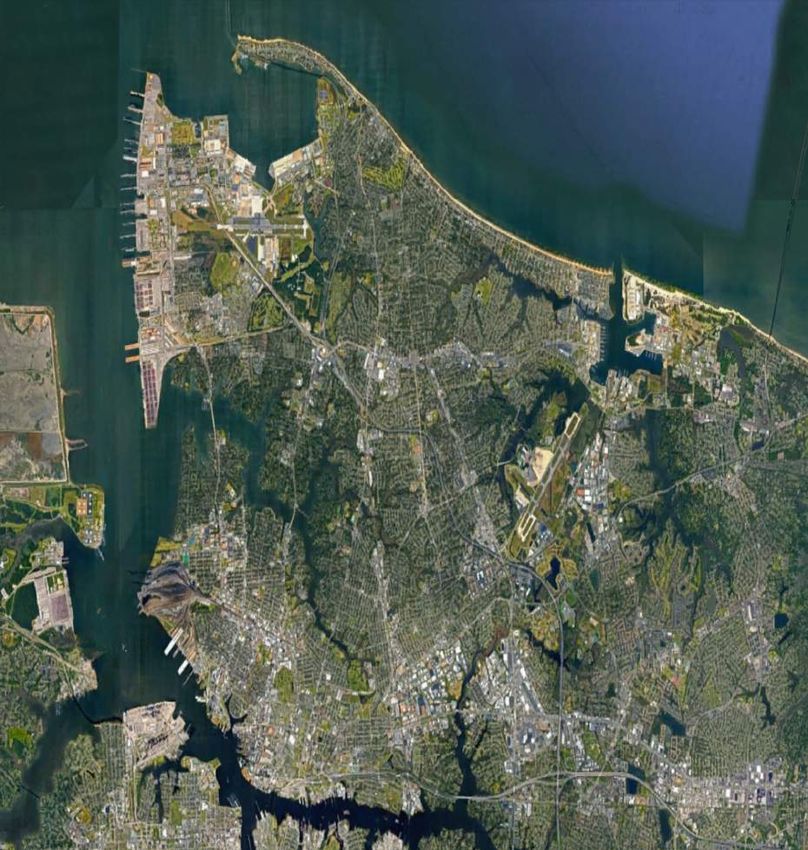

AERIAL PHOTO

12LITTLE BAY APARTMENTS

MARKET

COMPARABLES

13LITTLE BAY APARTMENTS

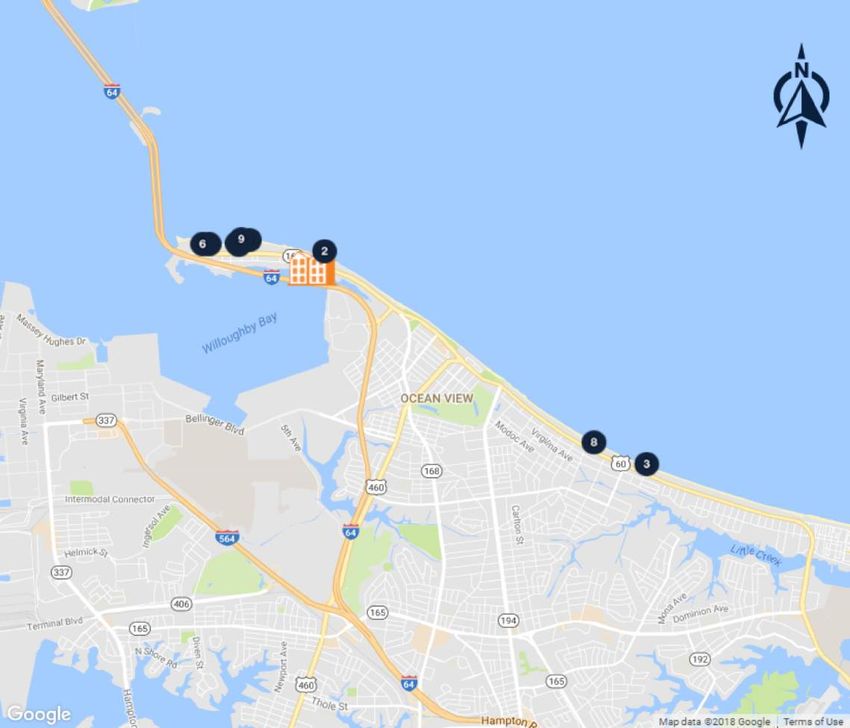

SALES COMPARABLES MAP

LITTLE BAY APARTMENTS

(SUBJECT)

1 Fish Tails

810 West Ocean View

2

Avenue

3 Castaways

4 Blue Marlin

5 Beach House

6 Neptune's Water

7 Fish Heads

8 Havana Beach

9 Tradewinds

SALES COMPARABLES

14PROPERTY

LITTLE BAY APARTMENTS

NAME

SALES COMPARABLES

SALES COMPARABLES SALES COMPS AVG

Average Price Per Unit

$80,000

Avg. $73,095

$72,000

$64,000

$56,000

$48,000

$40,000

$32,000

$24,000

$16,000

$8,000

$0

Little Bay Fish Tails 810 West Castaways Blue Marlin Beach House Neptune's Fish Heads Havana Tradewinds

Apartments Ocean View Water Beach

Avenue

15PROPERTY

LITTLE BAY APARTMENTS

NAME

SALES COMPARABLES

MARKETING TEAM

SALES COMPARABLES

FISH TAILS 810 WEST OCEAN VIEW AVENUE

LITTLE BAY APARTMENTS 9627-9631 Leclair St (Part of Multi-Property Sale), Norfolk, VA, 810 W Ocean View Ave, Norfolk, VA, 23503

846 Little Bay Ave, Norfolk, VA, 23503 23503

1 2

Units Unit Type Units Unit Type Units Unit Type

Offering Price: $690,000 2 One Bdr, One Bath Close Of Escrow: 3/30/2018 12 1 Bdr 1 Bath Close Of Escrow: 11/3/2017 12 2 Bdr 2 Bath

Price/Unit: $69,000 8 Two Bdr, One Bath Sales Price: $1,311,429 6 2 Bdr 1 Bath Sales Price: $1,050,000 2 3 Bdr 3.5 Bath

Price/SF: $81.18 Price/Unit: $72,857 Price/Unit: $75,000

CAP Rate: 7.08% Price/SF: $115.16 Price/SF: $95.63

GRM: 7.41 Total No. of Units: 18 CAP Rate: 6.63%

Total No. of Units: 10 Year Built: 1972 Total No. of Units: 14

Year Built: 1985 Year Built: 2000

rentpropertyaddress1 rentpropertyaddress1 rentpropertyaddress1

Underwriting Criteria

Income $86,870 Expenses $38,041

NOI $48,830 Vacancy ($7,411)

NOTES NOTES

Fully-renovated apartments featuring hardwood flooring, custom ceramic The owners have spent over $170,000 in renovation including new roofs,

tile floors in baths, custom wood-trim throughout, upgraded appliances and widows, HVAC units, kitchen/bath upgrades and other. Highlights include;

refrigerators. Dishwashers included. Portfolio sale of nine (9) multi-family Well Maintained Waterfront Property, High Historical Occupancy, Solid

complexes totaling 104 units on Ocean View Avenue in Norfolk, Virginia. Construction, Close Proximity to NAB/Norfolk Naval Station, Recently

This portfolio sale closed on 3/30/2018 for $7,650,000. Brick Lane Renovated, Clean Well Maintained Beach. An individual acquired a 14 unit

purchased as an investment sale with a cap rate 7.50%. apartment on November 3rd, 2017 for $1.05M or $75,000 per unit.

16PROPERTY

LITTLE BAY APARTMENTS

NAME

SALES COMPARABLES

MARKETING TEAM

SALES COMPARABLES

CASTAWAYS BLUE MARLIN BEACH HOUSE

2007 E Ocean View Ave, Norfolk, VA, 23503 1411 W Ocean View Ave, Norfolk, VA, 23503 1212 W Ocean View Ave, Norfolk, VA, 23503

3 4 5

Units Unit Type Units Unit Type Units Unit Type

Close Of Escrow: 3/30/2018 6 1 Bdr 1 Bath Close Of Escrow: 3/30/2018 14 2 Bdr 1 Bath Close Of Escrow: 3/30/2018 1 Studio 1 Bath

Sales Price: $437,143 Sales Price: $1,020,000 Sales Price: $1,238,571 16 1 Bdr 1 Bath

Price/Unit: $72,857 Price/Unit: $72,857 Price/Unit: $72,857

Price/SF: $145.71 Price/SF: $183.98 Price/SF: $111.06

Total No. of Units: 6 Total No. of Units: 14 Total No. of Units: 17

Year Built: 1961 Year Built: 1973 Year Built: 1971

rentpropertyaddress1 rentpropertyaddress1 rentpropertyaddress1

NOTES NOTES NOTES

Castaways has extra large units with hardwood floors. The property has Fully-renovated apartments featuring hardwood flooring, custom ceramic Fully-renovated apartments featuring hardwood flooring, custom ceramic

extensive landscaping, a courtyard and semi-private decks. Oversized tile floors in baths, custom wood-trim throughout, upgraded appliances and tile floors in baths, custom wood-trim throughout, upgraded appliances and

windows offer plenty of natural light. Portfolio sale of nine (9) multi-family refrigerators. Dishwashers included. Portfolio sale of nine (9) multi-family refrigerators. Dishwashers included. Portfolio sale of nine (9) multi-family

complexes totaling 104 units on Ocean View Avenue in Norfolk, Virginia. complexes totaling 104 units on Ocean View Avenue in Norfolk, Virginia. complexes totaling 104 units on Ocean View Avenue in Norfolk, Virginia.

This portfolio sale closed on 3/30/2018 for $7,650,000. Brick Lane This portfolio sale closed on 3/30/2018 for $7,650,000. Brick Lane This portfolio sale closed on 3/30/2018 for $7,650,000. Brick Lane

purchased as an investment sale from Boardwalk Realty & Development purchased as an investment sale with a cap rate 7.50%. purchased as an investment sale with a cap rate 7.50%.

with a cap rate 7.50%. The seller wanted cash to pursue other real estate

ventures. All information was verified by the seller.

17PROPERTY

LITTLE BAY APARTMENTS

NAME

SALES COMPARABLES

MARKETING TEAM

SALES COMPARABLES

NEPTUNE'S WATER FISH HEADS HAVANA BEACH

1443-1447 W Ocean View Ave (Part of Multi-Property Sale), 1265 W Ocean View Ave, Norfolk, VA, 23503 1721 E Ocean View Ave, Norfolk, VA, 23503

Norfolk, VA, 23503

6 7 8

Units Unit Type Units Unit Type Units Unit Type

Close Of Escrow: 3/30/2018 8 2 Bdr 1 Bath Close Of Escrow: 3/30/2018 14 2 Bdr 1 Bath Close Of Escrow: 3/30/2018 14 1 Bdr 1 Bath

Sales Price: $582,857 Sales Price: $1,020,000 Sales Price: $1,020,000

Price/Unit: $72,857 Price/Unit: $72,857 Price/Unit: $72,857

Price/SF: $161.10 Price/SF: $84.02 Price/SF: $91.07

Total No. of Units: 8 Total No. of Units: 14 Total No. of Units: 14

Year Built: 1953 Year Built: 1973 Year Built: 1965

rentpropertyaddress1 rentpropertyaddress1 rentpropertyaddress1

NOTES NOTES NOTES

Portfolio sale of nine (9) multi-family complexes totaling 104 units on Ocean Fully-renovated apartments featuring hardwood flooring, custom ceramic Fully-renovated apartments featuring hardwood flooring, custom ceramic

View Avenue in Norfolk, Virginia. This portfolio sale closed on 3/30/2018 for tile floors in baths, custom wood-trim throughout, upgraded appliances and tile floors in baths, custom wood-trim throughout, upgraded appliances and

$7,650,000. Brick Lane purchased as an investment sale from Boardwalk refrigerators. Dishwashers included. Portfolio sale of nine (9) multi-family refrigerators. Dishwashers included. Portfolio sale of nine (9) multi-family

Realty & Development with a cap rate 7.50%. The seller wanted cash to complexes totaling 104 units on Ocean View Avenue in Norfolk, Virginia. complexes totaling 104 units on Ocean View Avenue in Norfolk, Virginia.

pursue other real estate ventures. All information was verified by the seller. This portfolio sale closed on 3/30/2018 for $7,650,000. Brick Lane This portfolio sale closed on 3/30/2018 for $7,650,000. Brick Lane

purchased as an investment sale with a cap rate 7.50%. purchased as an investment sale with a cap rate 7.50%.

18PROPERTY

LITTLE BAY APARTMENTS

NAME

SALES COMPARABLES

MARKETING TEAM

SALES COMPARABLES

TRADEWINDS

1252 W Ocean View Ave, Norfolk, VA, 23503

9

rentpropertyname1 rentpropertyname1

Units Unit Type

Close Of Escrow: 3/30/2018 6 2 Bdr 1.5 Bath

Sales Price: $437,143

Price/Unit: $72,857

Price/SF: $66.23

Total No. of Units: 6

Year Built: 1981

rentpropertyaddress1 rentpropertyaddress1 rentpropertyaddress1

NOTES

Beautifully appointed units with stone-surround fireplaces, washer/dryer

hook-up, bedroom decks, large kitchens, serving counter and dining room.

Portfolio sale of nine (9) multi-family complexes totaling 104 units on Ocean

View Avenue in Norfolk, Virginia. This portfolio sale closed on 3/30/2018 for

$7,650,000. Brick Lane purchased as an investment sale from Boardwalk

Realty & Development with a cap rate 7.50%.

19LITTLE BAY APARTMENTS

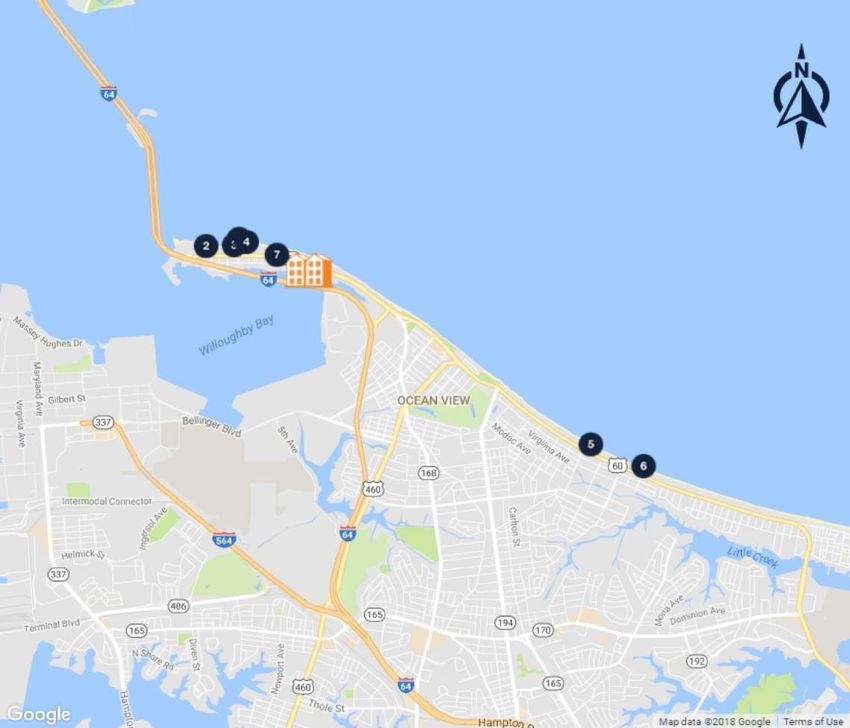

8 RENT COMPARABLES MAP

LITTLE BAY APARTMENTS

(SUBJECT)

1 Surf Rider

2 Blue Marlin

3 Fish Heads

4 Beach House

5 Havana Beach

6 Castaways

7 Casa Playa

8

9

10

11

12

13

14

15

16

17

18

20

20PROPERTY

LITTLE BAY APARTMENTS

NAME

RENT COMPARABLES

AVERAGE RENT - MULTIFAMILY

1 Bedroom 2 Bedroom

$900 $2,000

Avg. $828

$810 $1,800

$720 $1,600

$630 $1,400

$540 $1,200 Avg. $1,092

$450 $1,000

$360 $800

$270 $600

$180 $400

$90 $200

$0 $0

Little Bay Surf Rider Blue Marlin Fish Heads Beach House Havana Castaways Casa Playa Little Bay Surf Rider Blue Marlin Fish Heads Beach House Havana Castaways Casa Playa

Apartments Beach Apartments Beach

21PROPERTY

LITTLE BAY APARTMENTS

NAME

RENT COMPARABLES

MARKETING TEAM

SURF RIDER BLUE MARLIN

LITTLE BAY APARTMENTS

rentpropertyname1 1240 W Ocean View Ave, Norfolk, VA, 23503 1411 W Ocean View Ave, Norfolk, VA, 23503

846 Little Bay Ave, Norfolk, VA, 23503

rentpropertyaddress1

1 2

rentpropertyname1 rentpropertyname1

Unit Type Units SF Rent Rent/SF Unit Type Units SF Rent Rent/SF Unit Type Units SF Rent Rent/SF

One Bdr, One $825- $975-

2 850 $688 $0.81 1 Bdr 12 849 $1.06 2 Bdr 14 800 $1.36

Bath $975 $1,200

Two Bdr, One $1,000- Total/Avg. 14 800 $1,088 $1.36

8 850 $798 $0.94 2 Bdr 20 950 $1.24

Bath $1,350

Total/Avg. 10 850 $776 $0.91 Total/Avg. 32 912 $1,072 $1.18

YEAR BUILT: 1985 OCCUPANCY: 94% | YEAR BUILT: 1964 OCCUPANCY: 93% | YEAR BUILT: 1973

rentpropertyaddress1 rentpropertyaddress1 rentpropertyaddress1

22PROPERTY

LITTLE BAY APARTMENTS

NAME

RENT COMPARABLES

MARKETING TEAM

FISH HEADS BEACH HOUSE HAVANA BEACH

1265 W Ocean View Ave, Norfolk, VA, 23503 1212 W Ocean View Ave, Norfolk, VA, 23503 1721 E Ocean View Ave, Norfolk, VA, 23503

3 4 5

rentpropertyname1 rentpropertyname1 rentpropertyname1

Unit Type Units SF Rent Rent/SF Unit Type Units SF Rent Rent/SF Unit Type Units SF Rent Rent/SF

$950- Studio 1 $750 1 Bdr 1 Bath 12 800 $850 $1.06

2 Bdr 14 900 $1.13

$1,075

$775- Total/Avg. 12 800 $850 $1.06

Total/Avg. 14 900 $1,013 $1.13 1 Bdr 1 Bath 16 800 $1.05

$900

Total/Avg. 17 800 $832 $1.05

OCCUPANCY: 100% | YEAR BUILT: 1973 YEAR BUILT: 1971 OCCUPANCY: 92% | YEAR BUILT: 1965

rentpropertyaddress1 rentpropertyaddress1 rentpropertyaddress1

23PROPERTY

LITTLE BAY APARTMENTS

NAME

RENT COMPARABLES

MARKETING TEAM

CASTAWAYS CASA PLAYA

2007 E Ocean View Ave, Norfolk, VA, 23503 1033 Little Bay Ave, Norfolk, VA, 23503

6 7

rentpropertyname1 rentpropertyname1 rentpropertyname1

Unit Type Units SF Rent Rent/SF Unit Type Units SF Rent Rent/SF

$750- 1 Bdr 1 Bath 4 700 $750 $1.07

1 Bdr 1 Bath 6 800 $1.00

$850

Total/Avg. 6 800 $800 $1.00 4 Bdr 2 Bath 1 1,800 $1,500 $0.83

Total/Avg. 5 920 $900 $0.98

OCCUPANCY: 95% | YEAR BUILT: 1961 YEAR BUILT: 1969

rentpropertyaddress1 rentpropertyaddress1 rentpropertyaddress1

24LITTLE BAY APARTMENTS

FINANCIAL

ANALYSIS

25LITTLE BAY APARTMENTS

FINANCIAL ANALYSIS

RENT ROLL SUMMARY

26LITTLE BAY APARTMENTS

FINANCIAL ANALYSIS

OPERATING STATEMENT

27LITTLE BAY APARTMENTS

FINANCIAL ANALYSIS

NOTES

28LITTLE BAY APARTMENTS

FINANCIAL ANALYSIS

PRICING DETAIL

29LITTLE BAY APARTMENTS

ACQUISITION FINANCING

MARCUS & MILLICHAP CAPITAL CORPORATION WHY MMCC?

CAPABILITIES Optimum financing solutions to

enhance value

MMCC—our fully integrated, dedicated financing arm—is committed to

providing superior capital market expertise, precisely managed execution, and

unparalleled access to capital sources providing the most competitive rates and Our ability to enhance buyer

terms. pool by expanding finance

options

We leverage our prominent capital market relationships with commercial banks,

life insurance companies, CMBS, private and public debt/equity funds, Fannie

Mae, Freddie Mac and HUD to provide our clients with the greatest range of Our ability to enhance

financing options. seller control

• Through buyer

Our dedicated, knowledgeable experts understand the challenges of financing

qualification support

and work tirelessly to resolve all potential issues to the benefit of our clients.

• Our ability to manage buyers

finance expectations

• Ability to monitor and

manage buyer/lender progress,

insuring timely,

predictable closings

• By relying on a world class

Closed 1,707 National platform $5.63 billion Access to more

set of debt/equity sources

debt and equity operating total national capital sources

financings within the firm’s volume in 2017 than any other and presenting a tightly

in 2017 brokerage offices firm in the underwritten credit file

industry

30LITTLE BAY APARTMENTS

FINANCIAL ANALYSIS

GROWTH RATE PROJECTIONS

31LITTLE BAY APARTMENTS

FINANCIAL ANALYSIS

CASH FLOW

32LITTLE BAY APARTMENTS

MARKET

OVERVIEW

33LITTLE BAY APARTMENTS

MARKET OVERVIEW

HAMPTON ROADS

OVERVIEW

Norfolk is the cultural heart of the Hampton Roads, and quickly

becoming the prominent business district for the surrounding area.

Hampton Roads is recognized for its miles of waterfronts and beaches,

industrial and private sector strength, harbors, shipyards and coal piers,

and a dependable military presence. In 2017, the Hampton Road’s

invested nearly $3 billion in development and redevelopment projects

with growth continuing to rise exponentially through local, national, and

international investment. New projects such as Wegmans Grocery

Store, Norfolk Premier Outlets, The “Wave” Surf Park, and

internationally owned Ikea Furniture Store foreshadow a shift of

successful economic strength.

METRO HIGHLIGHTS

MILITARY CONCENTRATION

The Hampton Roads is home to several Fortune 500

Companies including Dollar Tree, Huntington Ingalls

Industries, and Norfolk Southern. Hampton Roads

also has the second-largest concentration of military

personnel in the U.S. with eight military installations

in the market providing a large portion of jobs.

HOSPITALITY AND TOURISM

Visitors are drawn to Williamsburg and the multiple

beaches and resorts in the area that have activities for

everyone.

SKILLED LABOR POOL

Technical knowledge learned in the military helps to

provide a highly educated and skilled labor force.

341LITTLE BAY APARTMENTS

MARKET OVERVIEW

ECONOMY

§ The local economy is best known for tourism and defense, but advanced manufacturing,

maritime and logistics, cybersecurity and biomedical technology are growing sectors.

§ Top employment drivers for the area include Sentara Healthcare, GEICO General Insurance

Co., Nasa Langley Research University and more. Local companies; Norfolk Southern, Dollar

Tree and Huntington Ingalls Industries, ranked top 380 in the 2017 Fortune 500 List. Other

internationally owned companies headquartered within the Hampton Roads include Gold Key

PHR, Amerigroup, Anthem and Stihl.

§ The only high speed transatlantic data cable put in place by Microsoft, Facebook, and Telxius

now runs 4,000 miles from Spain to Virginia Beach sending record speeds of 160 terabits of

data per second. This is expected to lead to strong IT industry growth in Hampton Roads for

years to come.

MAJOR AREA EMPLOYERS

Huntington Ingalls Industries Inc.

Sentara Healthcare

Naval Medical Center Portsmouth

Norfolk Naval Shipyard

Riverside Health System

The Colonial Williamsburg Foundation

Joint Expeditionary Base Little Creek-Ft. Story

GEICO General Insurance Co.

Naval Air Station Oceana-Dam Neck

* Forecast

Nasa Langley Research University

SHARE OF 2017 TOTAL EMPLOYMENT

7%

MANUFACTURING

14%

PROFESSIONAL AND

21%

GOVERNMENT

11%

LEISURE AND HOSPITALITY

5%

FINANCIAL ACTIVITIES

BUSINESS SERVICES

17% 5% + 15% 1% 35 5%

TRADE, TRANSPORTATION CONSTRUCTION EDUCATION AND INFORMATION OTHER SERVICES

AND UTILITIES HEALTH SERVICES

2

40LITTLE BAY APARTMENTS

MARKET OVERVIEW

DEMOGRAPHICS

§ The metro is projected to expand by 58,200 people through 2022, resulting in the

formation of 28,200 households during this period. SPORTS

§ Median home prices that are above the U.S. level contribute to a homeownership rate

of 61 percent, which is slightly below the national rate of 64 percent.

§ Approximately 29 percent of residents age 25 and older hold a bachelor’s degree; of

those residents, 11 percent also have earned a graduate or professional degree.

2017 Population by Age

6% 19% 9% 28% 25% 13%

0-4 YEARS 5-19 YEARS 20-24 YEARS 25-44 YEARS 45-64 YEARS 65+ YEARS

EDUCATION

2017 2017 2017 2017 MEDIAN

POPULATION: HOUSEHOLDS: MEDIAN AGE: HOUSEHOLD INCOME:

1.8M 658K 35.5 $60,500

Growth Growth U.S. Median: U.S. Median:

2017-2022*: 2017-2022*:

3.3% 4.3% 37.8 $56,300

QUALITY OF LIFE

Known for its beaches and water recreation, the region has much to offer by way of outdoor

activities and entertainment. Busch Gardens Williamsburg, Colonial Williamsburg, the USS

Wisconsin and the Virginia Aquarium are prominent attractions that draw tourist and locals ARTS & ENTERTAINMENT

alike. Cultural activities are available at the Virginia Museum of Contemporary Art, Virginia

Aquarium & Marine Science Center and Virginia Beach Amphitheater. Sports teams play at

the Virginia Beach Sportsplex, Harbor Park and Scope Arena, while the Kingsmill

Championship is held here as a part of the LPGA Tour. Universities include the College of

William & Mary, Old Dominion University, Virginia Wesleyan College, Hampton University

and Norfolk State University.

* Forecast

Sources: Marcus & Millichap Research Services; BLS; Bureau of Economic Analysis; Experian; Fortune; Moody’s

Analytics; U.S. Census Bureau

3LITTLE BAY APARTMENTS

MARKET OVERVIEW

2018 PRICING & VALUATION TRENDS

Yield Range Offers Compelling Options for Investors; Most Metros Demonstrate Strong Appreciation Rates

* 2007-2017 Average annualized appreciations in price per unit

Sources: Marcus & Millichap Research Services; CoStar Group, Inc.; Real Capital Analytics

37LITTLE BAY APARTMENTS

MARKET OVERVIEW

AVERAGE PRICE PER UNIT RANGE**

(Alphabetical order within each segment)

** Price per unit for apartment properties $1 million and greater

Sources: Marcus & Millichap Research Services; CoStar Group, Inc.; Real Capital Analytics

38LITTLE BAY APARTMENTS

MARKET OVERVIEW

2018 NATIONAL MULTIFAMILY INDEX

U.S. Multifamily Index

Coastal Markets Top National Multifamily Index;

Several Unique Markets Climb Ranks

Trading places. Seattle-Tacoma leads this year’s Index after moving up one notch, driven by robust

employment in the tech sector and soaring home prices that keep rental demand ahead of elevated deliveries.

The metro outperforms last year’s leader, Los Angeles (#2), which slid one spot. Midwest metro Minneapolis-

St. Paul (#3) rose one notch as its diverse economy generates steady job growth and robust rental demand,

maintaining one of the lowest vacancy rates among larger U.S. markets. San Diego (#4) jumped five spots as

deliveries slump while household formation proliferates, resulting in sizable rent growth. Portland (#5) inches up

a slot to round out the top five markets. East Coast markets fill the next two positions: Boston (#6) moves down

three slots as rent growth slows while vacancy ticks up, and New York City (#7) rises three places as stout

renter demand holds vacancy tight.

Index reshuffles with big moves. Sacramento (#8) posted the largest increase in the Index, vaulting 12

positions to lead a string of California markets that fill the next five slots. Robust rent growth and low vacancy

pushed the market up in the ranking. Other double-digit movers were Orlando (#17) and Detroit (#28), which

each leaped 10 places. Employment gains and in-migration are generating the need for apartments in Orlando,

maintaining ample rent advancement. In Detroit, steady employment and a slow construction pipeline keep

demand above supply, allowing rents to flourish. The most significant declines were registered in Austin,

Nashville and Baltimore. Austin (#31) tumbled nine spaces as elevated deliveries overwhelm demand slowing

rent growth. Nashville (#35) and Baltimore (#45) each moved down six steps as demand has yet to absorb

multiple years of elevated inventory gains. Although Kansas City (#46) retains the bottom slot, there is greater

change in the lower half of the NMI as more Midwest markets rise.

39LITTLE BAY APARTMENTS

MARKET OVERVIEW

U.S. ECONOMY

Growth Cycle Invigorated by Confidence;

Tax Laws Could Transform Housing

Tight labor market restrains hiring as confidence surges. The steady economic tailwind benefiting

apartment performance is poised to carry through 2018 as a range of positive factors align to support growth.

Consumer confidence recently reached its highest point since 2000 while small-business sentiment attained a

31-year record level, both reinforcing indications that consumption and hiring will be strong. The total number of

job openings has hovered in the low-6 million range through much of 2017, illustrating that companies have

considerable staffing needs, but with unemployment entrenched near 4 percent, companies will continue to face

challenges in filling available positions. These tight labor conditions should place additional upward pressure on

wages, potentially boosting inflationary pressure in the coming year. The strong employment market, rising

wages and elevated confidence levels could unlock accelerated household formation, particularly by young

adults. Last year, the number of young adults living with their parents ticked lower for the first time since the

recession, signaling that these late bloomers may finally be considering a more independent lifestyle.

Housing preferences may change under new tax laws. The new tax laws could play a significant role in

shaping both the economy and housing demand in 2018. Reduced taxes will be a windfall for corporations,

potentially sparking invigorated investment into infrastructure. The rise in CEO confidence over the last year

already boosted companies’ investment by more than 6 percent, accelerating economic growth. However, the

tax incentive-based stimulus will likely offer only a modest bump to GDP in 2018 because corporate investment

comprises just 12 percent of economic output. One factor that could weigh on economic expansion under the

new tax laws is the housing sector, which added just 3 percent to the economy last year, about two-thirds of

normal levels. The increased standard deduction and restrictions on housing-related deductions will reduce

some of the economic incentive to purchase a home, further sapping the strength of the housing sector.

Nonetheless, the increased standard deduction could benefit apartment investors, encouraging renters to stay

in apartments longer and reducing the loss of tenants to homeownership.

* Forecast

** Through 3Q

40LITTLE BAY APARTMENTS

MARKET OVERVIEW

U.S. ECONOMY

2018 National Economic Outlook

§ Labor force shortage weighs on job creation. The economy has added jobs every month for more than

seven years, the longest continuous period of job creation on record. The trend will continue in 2018, but the

pace of job additions will moderate, falling below 2 million for the year as the low unemployment rate

restricts the pool of prospective employees.

§ Wage growth poised to accelerate. Average wage growth has been creeping higher in the post-recession

era, with compensation gains in construction, professional services and the hospitality sectors outpacing the

broader trend. The tight labor market will continue to pressure wage growth, potentially sparking inflation in

the process.

§ Tax laws could invigorate apartment demand. Since 2011 household formations have outpaced total

housing construction, a key ingredient in the tightening of apartment vacancies. The new tax laws could

cause homebuilders to reduce construction while shifting a portion of the housing demand from

homeownership to rentals, and a rental housing shortage could ensue. If this behavior change occurs in

conjunction with additional young adults moving out of their own, apartment demand could dramatically

outpace completions.

* Forecast

** Through 3Q

41LITTLE BAY APARTMENTS

MARKET OVERVIEW

U.S. APARTMENT OVERVIEW

Demand Outlook Sturdy as Pace

Of Construction Begins to Retreat

Investors wary of apartment construction. The wave of apartment completions entering the market in recent

years has permeated the investor psyche, raising concerns of overdevelopment and escalating vacancy rates,

but numerous demand drivers have held this risk in check. Steady job creation, positive demographics, above-

trend household formation and elevated single-family home prices have converged to counterbalance the

addition of 1.37 million apartments over the last five years, at least on a macro level. Though a small number of

markets have faced oversupply risk, the affected areas tend to be concentrated pockets, with upper-echelon

units facing the greatest competition. For traditional workforce housing, Class B and C apartments, the risks

stemming from overdevelopment have been nominal, and in most metros, even the Class A tranche has

demonstrated sturdy performance. In the coming year, rising development costs, tighter construction financing

and mounting caution levels will curb the pace of additions from the 380,000 units delivered in 2017 to

approximately 335,000 apartments. However, the list of markets facing risk from new completions will stretch

beyond the dozen metros that builders have concentrated on thus far. This will heighten competition, requiring

investors to maintain an increasingly tactical perspective integrating vigilant market scrutiny and strong property

management.

Competitive nuances increasingly granular. Although the pace of apartment completions will moderate in

2018, additions will still likely outpace absorption. This imbalance will most substantively affect areas where

development has been focused, such as the urban core where vacancy rates have risen above suburban rates

for the first time on record. Nationally, Class A vacancy rates have advanced to 6.3 percent in 2017 and will

continue their climb to the 6.8 percent range over the next year. Vacancy rates for Class B and C assets will

rise less significantly in 2018, pushing to 5.0 percent and 4.7 percent, respectively. Although vacancy levels are

rising, three-fourths of the major metros have rates below their 15-year average. Still, the magnitude of new

completions coming to market and the high asking rents these new units command will spark increased

competition for tenants, generating a more liberal use of concessions in 2018 as landlords attempt to entice

move-up tenants.

* Forecast

42LITTLE BAY APARTMENTS

MARKET OVERVIEW

U.S. APARTMENT OVERVIEW

2018 National Apartment Outlook

§ Rent growth tapers as concession use edges higher. Average rent growth will taper to 3.1 percent in

2018 as concessions become more prevalent, particularly in Class A properties. Rent gains in the Class C

space, which were particularly strong last year, will face greater challenges as affordability restrains

demand. Although job growth has been steady for seven years, wage growth has been relatively weak,

particularly for low-skilled labor.

§ Congress may nudge apartment demand. The new tax laws could reinforce apartment living as the larger

standard deduction reduces the economic incentive of homeownership. Previous tax rules encouraged

homeownership with itemized deductions for property taxes and mortgage interest that often surpassed the

standard deduction. These advantages have largely been eliminated, particularly for first-time buyers.

§ Are millennials finally moving out on their own? The 80 million-strong millennial age cohort, now

pushing into their late 20s, may finally be showing independence. Since the recession, the percentage of

young adults living with their parents increased dramatically, but last year that trend reversed. Should the

share of young adults living with family recede toward the long-term average, an additional 3 million young

adults would need housing.

** Estimate

43LITTLE BAY APARTMENTS

MARKET OVERVIEW

U.S. CAPITAL MARKETS

Fed Normalization Portends Rising Interest Rates;

Capital Availability for Apartments Elevated

Fed cautiously pursues tighter policies. Investors have largely adapted to the modestly higher interest rate

environment, and most anticipate additional increases in 2018 as the Federal Reserve normalizes both its

policies and its balance sheet. The Fed is widely expected to continue raising its overnight rate through 2018 as

it tries to restrain potential inflation risk and create some dry powder to combat future recessions. The Fed will,

however, be cautious about pushing short-term rates into the long-term rates, which would create an inverted

yield curve. The spread between the two-year Treasury rate and the 10-year Treasury rate has tightened

significantly, and if the Fed is too aggressive in its policies, the short-term interest rates could climb above long-

term rates. This inversion is a commonly watched leading indicator of an impending recession. The new

chairman of the Fed, Jerome Powell, will likely make few changes to the trajectory of Fed policies, and he is

widely expected to continue the reduction of the Fed balance sheet. Powell may consider accelerating the

balance sheet reduction to ensure long-term rates move higher. That said, Powell is widely perceived to be a

dovish leader who will advance rates cautiously.

Readily available debt backed by sound underwriting. Debt availability for apartment assets remains

abundant, with a wide range of lenders catering to the sector. Apartment construction financing has

experienced some tightening, a generally favorable trend for most investors. Fannie Mae and Freddie Mac will

continue to serve a significant portion of the multifamily financing, with local and regional banks targeting

smaller transactions and insurance companies handling larger deals with low-leverage needs. In general,

lenders have been loosening credit standards on commercial real estate lending, but underwriting standards

remain conservative with loan-to-value ratios for apartments in the relatively conservative 66 percent range. An

important consideration going forward, however, will be investors’ appetite for acquisitions as the yield spread

between interest rates and cap rates tightens.

* Through December 12

** Through December 6

44LITTLE BAY APARTMENTS

MARKET OVERVIEW

U.S. CAPITAL MARKETS

2018 Capital Markets Outlook

§ Yield spread tightens amid rising interest rates. Average apartment cap rates have remained relatively

stable in the low-5 percent range for the last 18 months, with a yield spread above the 10-year Treasury of

about 280 basis points. Many investors believe cap rates will rise in tandem with interest rates, but this has

not been the case historically. Given the strong performance of the apartment sector, it’s more likely the

yield spread will compress, reducing the positive leverage investors have enjoyed in the post-recession era.

§ Inflation restrained but could emerge. Inflation has been nominal throughout the current growth cycle, but

pressure could mount as the tight labor market spurs rising wages. Elevated wages and accelerating

household wealth could boost consumption, creating additional economic growth and inflation. The Fed has

become increasingly proactive in its efforts to head off inflationary pressure, but the stimulative effects of tax

cuts could overpower the Fed’s efforts.

§ Policies likely to strengthen dollar and could pose new risks. One wild card that could create an

economic disruption is the strengthening dollar. The economic stimulus created by tax cuts together with

tightening Fed monetary policy place upward pressure on the value of the dollar relative to foreign

currencies. This could restrain foreign investment in U.S. commercial real estate, but it could also weaken

exports and make it more difficult for other countries to pay their dollar-denominated debt, which in turn

weakens global economic growth.

* Through December 12

Estimate

45LITTLE BAY APARTMENTS

MARKET OVERVIEW

U.S. INVESTMENT OUTLOOK

Apartment Investors Recalibrate Strategies;

Broaden Criteria to Capture Upside Opportunities

Appreciation flattens as buyers recalibrate expectations. The maturing apartment investment climate has

continued its migration from aggressive growth to a more stable but still positive trend. Investors have reaped

strong returns in the post-recession era through significant gains in fundamentals and pricing, but the growth

trajectory has flattened as the market has normalized. The pace of apartment rental income growth has moved

back toward its mid-3 percent long-term average and investor caution has flattened cap rates, moderating

appreciation. With much of the gains created by the post-recession recovery absorbed and most of the value-

add opportunity already extracted, it has been increasingly difficult for investors to find opportunities with

substantive upside potential. At the same time, apartment construction has finally brought macro-level housing

supply and demand back toward equilibrium, restraining upside potential in markets with sizable deliveries.

These challenges have been compounded by a widened bid/ask gap, with many would-be apartment sellers

retaining a highly optimistic perception of their asset’s value. It will take time for investor expectations to realign,

but buyers and sellers are discovering a flattening appreciation trajectory. Still, a range of opportunities remain.

Investors broaden criteria as they search for yield upside. Investors are recalibrating strategies, broadening

their search and sharpening their efforts to find investment options with upside potential. They have expanded

criteria to include a variety of Class B and Class C assets, outer-ring suburban locations, and properties in

secondary or tertiary markets. The yield premium offered by these types of assets has drawn an increasing

amount of multifamily capital. In the last year, nearly half of the dollar volume invested in apartment properties

over $1 million went to secondary and tertiary markets, up from 42 percent of the capital in 2010. This influx of

activity has caused cap rates in tertiary markets to fall from the high-8 percent range in 2010 to their current

average near 6 percent. During the same period, national cap rates of Class B/C apartment properties have

fallen by 200 basis points to the mid-5 percent range. Considering the low cost of capital, these yields have

remained attractive to investors with longer-term hold plans.

* Through 3Q

** Trailing 12 months through 3Q

46LITTLE BAY APARTMENTS

MARKET OVERVIEW

U.S. INVESTMENT OUTLOOK

2018 Investment Outlook

§ New tax laws could shift investor behavior. Additional clarity on taxes should alleviate some of the

uncertainty that held back investor activity over the last year while helping to mitigate the expectation gap

between buyers and sellers. Reduced tax rates on pass-through entities could spark some repositioning

efforts, bringing additional assets to market and supporting market liquidity.

§ Tighter monetary policy could narrow yield spreads. Prospects of a rising interest rate environment

could weigh on buyer activity as the yield spread tightens. Cap rates have held relatively stable over the last

two years, and the sturdy outlook for apartment fundamentals is unlikely to change substantively in the

coming year. As a result, investors’ pursuit of yield will likely push activity toward assets and markets that

have traditionally offered higher cap rates.

§ Transaction activity retreats from peak levels. Apartment sales continued to migrate toward more normal

levels last year as investors’ search for upside and value-add opportunities delivered fewer candidates.

Markets with a limited construction pipeline but with respectable employment and household formation

growth will see accelerated activity, while markets facing an influx of development could see moderating

investor interest.

* Through 3Q

** Trailing 12 months through 3Q

47LITTLE BAY APARTMENTS

MARKET OVERVIEW

REVENUE TRENDS

Five-Year Apartment Income Growth by Metro FIVE-YEAR TREND:

Percent Change 2013-2018* Outperforming Through

Development Cycle

2013-2018*

§ U.S. creates 11.8 million jobs over five years

§ Developers add 1.5 million new apartments

§ Absorption totals 1.4 million apartments

§ U.S. vacancy rate to match 2013 at 5.0 percent

§ U.S. average rent rises 23.2 percent

* Forecast

48LITTLE BAY APARTMENTS

MARKET OVERVIEW

2018 NATIONAL INVENTORY TREND

Five-Year Development Wave Transforms Rental Landscape

Inventory Growth 2013-2018

Inventory Change by Market

2013 to 2018

Sources: Marcus & Millichap Research Services; MPF Research

49LITTLE BAY APARTMENTS

MARKET OVERVIEW

2018 NATIONAL INVENTORY TREND

Top 10 Markets by Inventory Change

Largest Growth Five-Year Inventory Change Five-Year Rent Growth

Austin 23.6% 22%

Charlotte 22.9% 30%

Nashville 21.7% 31%

Salt Lake City 20.9% 31%

Raleigh 19.5% 27%

San Antonio 18.7% 20%

Denver 17.9% 41%

Seattle-Tacoma 15.9% 41%

Orlando 15.3% 35%

Dallas/Fort Worth 15.3% 30%

U.S. 9.8% 23%

Smallest Growth Five-Year Inventory Change Five-Year Rent Growth

Cincinnati 6.6% 24%

Chicago 6.2% 21%

Oakland 5.8% 40%

Riverside-San Bernardino 5.6% 36%

St. Louis 5.5% 14%

Los Angeles 5.4% 31%

New York City 4.6% 15%

Cleveland 4.6% 15%

Sacramento 3.8% 48%

Detroit 2.9% 25%

Sources: Marcus & Millichap Research Services; MPF Research

50PROPERTY

LITTLE BAY APARTMENTS

NAME

DEMOGRAPHICS

MARKETING TEAM

Created on May 2018

POPULATION 1 Miles 3 Miles 5 Miles HOUSEHOLDS BY INCOME 1 Miles 3 Miles 5 Miles

§ 2022 Projection § 2017 Estimate

Total Population 4,185 31,861 97,541 $200,000 or More 0.97% 1.61% 2.84%

§ 2017 Estimate $150,000 - $199,000 4.07% 2.54% 3.22%

Total Population 4,323 31,912 98,223 $100,000 - $149,000 9.13% 8.43% 9.77%

§ 2010 Census $75,000 - $99,999 11.71% 12.17% 11.23%

Total Population 4,312 31,631 96,811 $50,000 - $74,999 20.99% 24.11% 21.60%

§ 2000 Census $35,000 - $49,999 20.99% 18.19% 16.46%

Total Population 9,706 46,931 111,391 $25,000 - $34,999 9.84% 12.15% 11.70%

§ Daytime Population $15,000 - $24,999 11.57% 10.52% 10.87%

2017 Estimate 15,564 61,803 121,444 Under $15,000 10.72% 10.28% 12.30%

HOUSEHOLDS 1 Miles 3 Miles 5 Miles Average Household Income $60,433 $60,656 $66,183

§ 2022 Projection Median Household Income $45,788 $48,872 $48,780

Total Households 1,891 12,413 39,823 Per Capita Income $33,665 $24,598 $27,441

§ 2017 Estimate POPULATION PROFILE 1 Miles 3 Miles 5 Miles

Total Households 1,960 12,380 39,767 § Population By Age

Average (Mean) Household Size 2.18 2.30 2.37 2017 Estimate Total Population 4,323 31,912 98,223

§ 2010 Census Under 20 19.59% 24.44% 24.34%

Total Households 1,965 12,327 39,370 20 to 34 Years 40.75% 35.68% 30.98%

§ 2000 Census 35 to 39 Years 5.75% 6.43% 6.31%

Total Households 2,712 13,084 39,362 40 to 49 Years 9.40% 9.93% 10.30%

Growth 2015-2020 -3.52% 0.27% 0.14% 50 to 64 Years 17.65% 15.87% 17.25%

HOUSING UNITS 1 Miles 3 Miles 5 Miles Age 65+ 6.85% 7.63% 10.82%

§ Occupied Units Median Age 29.14 29.30 31.60

2022 Projection 1,891 12,413 39,823 § Population 25+ by Education Level

2017 Estimate 2,403 13,816 43,690 2017 Estimate Population Age 25+ 2,677 19,494 63,029

Owner Occupied 434 4,716 16,904 Elementary (0-8) 0.83% 1.16% 1.92%

Renter Occupied 1,526 7,664 22,863 Some High School (9-11) 8.81% 7.15% 8.29%

Vacant 443 1,436 3,922 High School Graduate (12) 23.15% 30.61% 28.85%

§ Persons In Units Some College (13-15) 33.37% 29.23% 27.10%

2017 Estimate Total Occupied Units 1,960 12,380 39,767 Associate Degree Only 12.32% 10.65% 8.67%

1 Person Units 35.00% 32.48% 31.35% Bachelors Degree Only 13.28% 13.83% 15.39%

2 Person Units 34.34% 33.23% 32.44% Graduate Degree 8.04% 6.64% 8.87%

3 Person Units 16.33% 16.85% 16.84% § Population by Gender

4 Person Units 8.93% 10.75% 11.38% 2017 Estimate Total Population 4,323 31,912 98,223

5 Person Units 3.88% 4.32% 5.10% Male Population 58.22% 53.21% 50.91%

6+ Person Units 1.48% 2.37% 2.88% Female Population 41.78% 46.79% 49.09%

Source: © 2017 Experian

51PROPERTY

LITTLE BAY APARTMENTS

NAME

DEMOGRAPHICS

MARKETING TEAM

Population Race and Ethnicity

In 2017, the population in your selected geography is 4,323. The The current year racial makeup of your selected area is as follows:

population has changed by -55.46% since 2000. It is estimated that 70.34% White, 18.48% Black, 0.17% Native American and 2.35%

the population in your area will be 4,185.00 five years from now, which Asian/Pacific Islander. Compare these to US averages which are:

represents a change of -3.19% from the current year. The current 70.42% White, 12.85% Black, 0.19% Native American and 5.53%

population is 58.22% male and 41.78% female. The median age of the Asian/Pacific Islander. People of Hispanic origin are counted

population in your area is 29.14, compare this to the US average independently of race.

which is 37.83. The population density in your area is 1,375.03 people

per square mile. People of Hispanic origin make up 10.10% of the current year

population in your selected area. Compare this to the US average of

17.88%.

Households Housing

There are currently 1,960 households in your selected geography. The The median housing value in your area was $299,304 in 2017,

number of households has changed by -27.73% since 2000. It is compare this to the US average of $193,953. In 2000, there were 585

estimated that the number of households in your area will be 1,891 owner occupied housing units in your area and there were 2,127

five years from now, which represents a change of -3.52% from the renter occupied housing units in your area. The median rent at the

current year. The average household size in your area is 2.18 time was $448.

persons.

Income Employment

In 2017, the median household income for your selected geography is In 2017, there are 1,183 employees in your selected area, this is also

$45,788, compare this to the US average which is currently $56,286. known as the daytime population. The 2000 Census revealed that

The median household income for your area has changed by 35.60% 59.13% of employees are employed in white-collar occupations in this

since 2000. It is estimated that the median household income in your geography, and 42.00% are employed in blue-collar occupations. In

area will be $60,434 five years from now, which represents a change 2017, unemployment in this area is 2.91%. In 2000, the average time

of 31.99% from the current year. traveled to work was 24.00 minutes.

The current year per capita income in your area is $33,665, compare

this to the US average, which is $30,982. The current year average

household income in your area is $60,433, compare this to the US

average which is $81,217.

Source: © 2017 Experian

52LITTLE BAY APARTMENTS

8 DEMOGRAPHICS

53You can also read