Monthly Market Commentary - Unique Wealth

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Monthly Market Commentary

July 2021

Where We Are

In 44 BC, the Roman Senate changed the name of Quintilis (the fifth month) to Julius Mensis — what we

now call July — to honor the Roman military commander, author, historian, and statesman Julius Caesar and

to recognize his introduction in 46 BC of the 365-day Julian calendar to ensure that the civil year could

properly keep pace with the seasons. In the Northern Hemisphere — with its celebrations of Independence

Day in the United States (on the 4th) and Bastille Day in France (on the 14 th) —July is considered a festive

month as it marks the beginning of summer and the second half of the calendar year.

Spurred forward by optimism (i) that the post-pandemic U.S. economic recovery is continuing, (ii) that

inflation appears to be transitory, and (iii) that the Federal Reserve will keep interest rates low for a while

longer, June has confirmed a festive span for U.S. equities. The S&P 500 index rose +2.2% for the month,

+8.2% for 2Q21 (its fifth quarterly gain in a row, and all five of these gains have exceeded +5%, only the

second time since 1945 — the other time was in 1954 — that the index has managed such a performance),

and +14.4% for 1H21. This is the S&P 500’s best six-month period in 23 years. (Source: The Wall Street

Journal)

Two-year U.S. Treasury yields in June reflected recent higher CPI, PPI, and Personal Consumption

Expenditures inflation reports, rising 11 basis points from 0.14% on May 28 th to 0.25% on June 30th.

Nevertheless, during the month of June, indicating that these price increases may be temporary,

intermediate- and longer-term U.S. Treasury yields actually declined. Ten-year U.S. Treasury yields fell 13

basis points in June, from 1.58% on May 28th to 1.45% on June 30th, and 30-year U.S. Treasury yields

declined 20 basis points, from 2.26% on May 28th to 2.06% on June 30th.

Over the course of the month, following the course of the higher inflation readings and higher two-year U.S.

Treasury yields, in June the six major currencies DXY U.S. dollar index rose +2.6%, from 90.06 on May 28 th to

92.44 on June 30th.

As shown in the table on the following page, the technology-heavy NASDAQ Composite index finished 1H21

+12.5% and had its best month of the year in June, rising +5.5%. The Russell 2000 index of small- and mid-

cap companies rose +1.8% in June and is up +17.0% YTD for the first half of the year. Pummeled by rising

short-term interest rates and a stronger dollar in June, gold experienced its worst month of the year,

declining -7.3% and is now down -6.5% YTD through June 30th.

Buoyed by (i) disciplined management of supply by OPEC and its allies, as well as by U.S. shale producers,

and (ii) significant demand growth from the developed world more than offsetting still-soft oil demand from

the developing world, West Texas Intermediate crude oil prices closed at $73.47 per barrel on June 30 th,

+10.8% in the month and +51.4% YTD for 1H21.

Past and projected performance

1

does not guarantee future results.

MARKET COMMENTARY - JULY 2021

Monthly and Year-to-Date Price Performance

YTD

Index/Commodity Jan. Feb. Mar. Apr. May Jun. (through 6/30)

S&P 500 -1.1% +2.6% +4.2% +5.2% +0.5% +2.2% +14.4%

Nasdaq Composite +1.4% +0.9% +0.4% +5.3% -1.5% +5.5% +12.5%

Russell 2000 +5.0% +6.1% +0.9% +2.1% +0.1% +1.8% +17.0%

Gold -2.6% -5.9% -1.6% +3.6% +7.9% -7.3% -6.5%

West Texas Int. Oil +7.5% +18.0% -3.8% +7.3% +4.4% +10.8% +51.4%

Source: The Wall Street Journal.

After a classically powerful price rebound from the March 23rd, 2020 pandemic-induced stock market lows,

financial market participants appear to be well into embarking on “Phase Two” of the equity market’s story

while continuing to search for some sort of coherent narrative during the month of June. During the month,

stocks experienced both their worst week since October 2020 as well as their best week since February of

this year. Amidst rather subdued equity market volatility, investors seem to be looking for a directional

catalyst, all the while seeking a degree of clarity, some sort of definable trend, and rational insights as to the

path of asset prices.

In June, equities, bond yields, and currency exchange rates have tended to trace a seesaw, teeter-totter,

roller-coaster, zigzag pattern in reaction to economic data. This is because virtually every piece of positive

news has in many cases tended to be accompanied by an offsetting qualification, and every piece of less-

favorable news has not infrequently also carried a silver lining.

For instance, while monthly U.S. employment gains have risen from +269,000 in April to +583,000 jobs in

May, and +850,000 jobs in June (of which government hiring represented +193,000), the U.S. labor market

still is not yet experiencing broad-based and inclusive full employment. And despite June’s robust pickup in

overall hiring, the labor force participation rate of 61.6% remains 1.7 percentage points below its pre-

pandemic ratio and the employment-population ratio, at 58.0%, came in 3.1 percentage points below pre-

Covid levels. Based on careful analysis of the numbers comprising the June jobs report, bond market

investors subsequently sent intermediate- and long-term U.S. Treasury yields lower, not higher.

Still another example of “sweet and sour” economic results involves the June ISM Manufacturing index —

which registered a quite strong reading of 60.6, down from 61.2 in May (with any reading above 50.0

indicating expansion). When the details are subjected to closer scrutiny, the ISM-Manufacturing number

represents another example of headline strength, albeit with modification. The Prices index — an

important data point in an atmosphere of heightened concern over inflationary pressures — rose 4.1 points

to a very elevated 92.1, which represents the highest reading in 42 years, and the Employment component

of the report declined by 1.0 point to enter contraction territory for the first time in seven months.

As shown in the two adjacent charts on the next page, each of which covers the 1950–2020 time frame, (i)

despite the third quarter generating historically the lowest quarterly returns for the S&P 500 index

(averaging only +0.7%, with 62.0% of the third quarters in positive territory), (ii) July as a month has turned

out on average to be very strong month generally, particularly in post election years.

Past and projected performance

2

does not guarantee future results.

MARKET COMMENTARY - JULY 2021

The following sections examine how asset prices may be influenced by The Inflation Outlook, Corporate

Profits, and Investor Liquidity/Exuberance.

Inflation Concerns

Opinion remains divided on whether consumer and producer price inflation rates are likely to be transitory

or enduring in the months ahead, and to our way of thinking for the time being, “the jury is out,” in terms of

attempting to arrive at a definitive conclusion. Set forth below are some of the arguments adduced on

either side of this important question.

Past and projected performance

3

does not guarantee future results.

MARKET COMMENTARY - JULY 2021

Factors indicating that inflation rates are likely to be elevated and enduring include:

i. Reported Consumer Inflation metrics have risen — the May 2021 Personal Consumption Expenditures

price index rose +3.9% year-over-year, while the May Consumer Price Index increased +5.0% year-over-

year;

ii. The May Purchasing Managers Index from the Institute of Supply Management showed the prices

subindex at 88%, slightly below April, yet appreciably higher than November (65.4%) and December

(77.6%), suggesting that prices may continue to rise;

iii. Semi-permanent to permanent structural changes (such as retirement and career changes) in the

supply of labor may be putting more long-lasting than anticipated upward pressure on labor costs;

iv. Because the Federal Reserve has altered its monetary policy from a forecast-based approach to

becoming “data dependent,” it is possible that it could fall sufficiently “behind the curve” in countering

inflationary pressures to such a degree that actual and expected inflation rates could become

embedded in market participants’ expectations; and

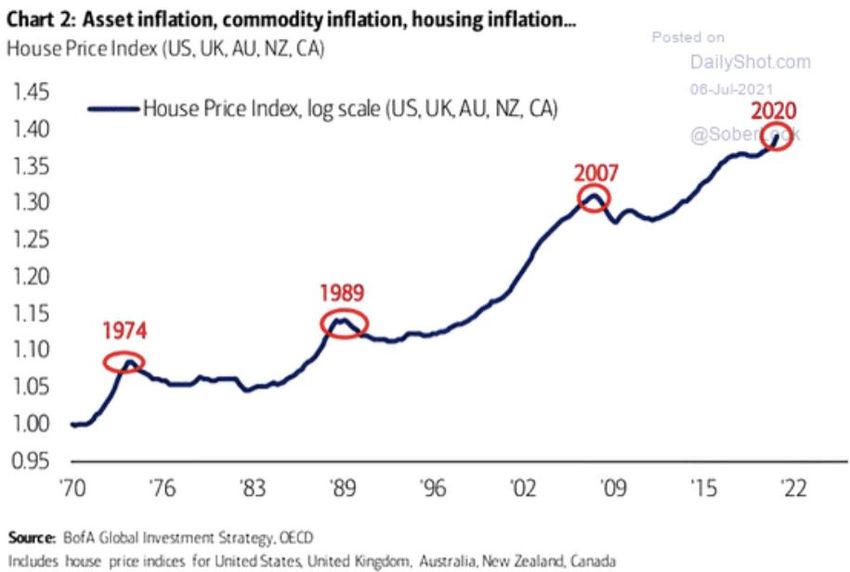

v. As shown in the accompanying chart — depicting house price increases in the United States, the

United Kingdom, Australia, New Zealand, and Canada — record house price inflation could produce

increased inflationary expectations and inflationary pricing behavior.

Factors indicating that inflation rates are likely to be declining and transitory include:

i. Recent high inflation data in large part reflect year-over-year base effects, supply-side bottlenecks,

commodity shortages, and inventory management shortfalls, all of which are expected to diminish with

the passage of time;

ii. The trimmed mean Personal Consumption Expenditures price deflator (which removes extreme price

gains, as well as extreme price declines) has not been exhibiting any sharp acceleration;

iii. The Federal Reserve has indicated that it will begin tightening monetary policy to bring inflation under

control if price pressures exhibit signs of becoming permanently embedded rather than transitory;

Past and projected performance

4

does not guarantee future results.

MARKET COMMENTARY - JULY 2021

iv. Whatever final form the proposed physical infrastructure bill takes, it is much smaller than the Covid

Relief and Economic Security payments, and is targeted to be spread over 5 to 8 years rather than

being immediately injected into the economy;

v. The significant degree of labor market slack could take several years to work off and help keep wage

price inflation contained;

vi. Among other materials, copper and lumber prices have begun declining from their recent peaks;

vii. Clamping down on rising domestic prices, the Chinese government in late May expressed “zero

tolerance” for “abnormal transactions and malicious speculation” in commodities markets;

viii. Rising short-term interest rates relative to intermediate- and long-term interest rates (known as a

flatter U.S. Treasury yield curve) generally indicates slower economic growth;

ix. Recent strength in the U.S. dollar currency index tends to exert downward pressure on the price of

imported goods;

x. Although the May University of Michigan Consumer Sentiment Survey reported one-year Inflationary

Expectations at +3.7%, the Survey’s five-year Inflationary Expectations registered +2.8% — indicating

that consumers view inflation as transitory rather than becoming structural; and

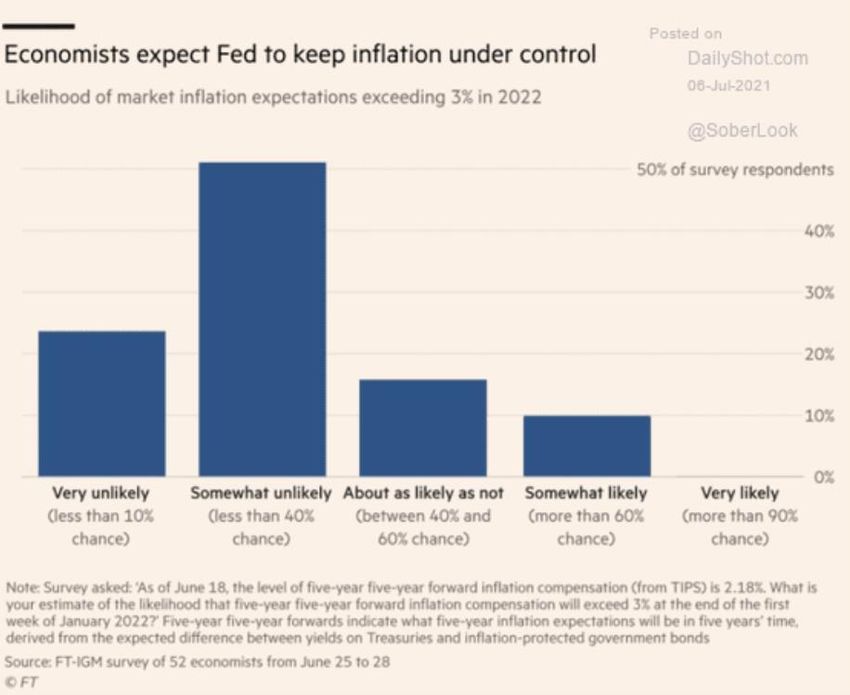

xi. As shown in the accompanying chart, a late June 2021 survey of 52 economists found that 70%

estimated that the likelihood of market inflation expectations exceeding +3% in 2022 was “somewhat

unlikely” or “very unlikely.”

In coming weeks and months, financial markets’ attempts to determine whether inflation is transitory or

enduring are likely to exert significant influence on asset prices. For example, cyclical sectors (such as

materials, financials, and industrials) that would be expected to do well (or poorly) in an inflationary

environment would be expected to appreciate (or decline). It is our view that inflation rates may peak and

come down from recent fairly high levels, yet we hasten to point out that such a slowdown is not equivalent

to disinflation and may in fact end up producing an average rate of increase in the general price level that is

higher than the pre-pandemic experience.

Past and projected performance

5

does not guarantee future results.

MARKET COMMENTARY - JULY 2021

Corporate Profits

As of July 2nd, according to FactSet, a record number of S&P 500 companies have issued positive revenue

and earnings guidance for 2Q21. Securities analysts were carrying the following forecasts for S&P 500

revenues and earnings, respectively: 1Q2021, +10.9% and +52.5%; 2Q2021, +19.6% and +63.6%; 3Q2021,

+12.3% and +23.6%; 4Q2021, +9.2% and +18.1%; and for the full 2021 calendar year, +12.4% and +35.5%.

Following the passage of Federal Reserve-administered stress tests, 23 of the nation’s largest banks are in

the process of announcing stock repurchase and dividend increases likely to reach up to $200 billion.

Corporate after-tax earnings could potentially be reduced by the early July agreement among 130 countries

to make significant changes to the international tax system (with the proposed rules, if passed, targeted to

be put in place in 2022 and implemented in 2023), including: (i) Pillar 1, which would grant countries the

right to tax large companies based on where they generate revenue; and (ii) Pillar 2, which would establish

a global minimum corporate tax rate of 15%.

Pillar 1 may have to be dealt with as a separate bill (and would need support from at least two-thirds of the

U.S. Senate), since it alters America’s agreements with other countries and means the United States must

change existing treaties or create new treaties. Pillar 2, which alters U.S. domestic legislation, could

potentially be passed using the so-called reconciliation process (which can be used by the U.S. Congress

once each fiscal year and bills passed by this route can clear the Senate with a simple majority). Passage of

these proposed tax changes is by no means certain, with numerous lawmakers having already expressed

opposition to a tax aimed primarily at U.S. companies and to a tax policy that in effect shifts to other

governments revenue which America might otherwise check claim for itself.

And as tabulated by Yardeni Research, Inc. at the end of 1Q2021, S&P 500 companies’ forward net profit

margins stood at a record high 12.8%. In our opinion, as 3Q21 and 4Q21 progress, and the economy

continues to reopen, analysts may slow down or halt their upward earnings revisions and these profit

margins may come under some degree of pressure owing to rising commodity prices, labor and other cost

pressures, supply chain issues, and especially, higher corporate taxes.

Another source of S&P 500 profit uncertainty is represented by potential regulatory, legislative, anti-trust,

and other state and federal legal challenges to the corporate sector, with particular emphasis on social

media and large-cap technology companies. Among other issues, the U.S. House of Representatives as of

early July is considering a package of bills that would severely limit the ability of tech megacap companies

to expand via acquisition, and could force them to sell some existing businesses.

While the currently wide profit margins and the cheerful revenue and earnings profit forecasts presented

above represent a tailwind for equities prices, we nevertheless continue to emphasize caution, quality, and

active security selection in the styles and sectors highlighted in “Equity Emphases and De-emphases,”

“Focus on Strength and Quality,” and “Balancing Growth and Value Sectors” In the Portfolio Positioning

Tactics section at the end of this Commentary.

Investor Exuberance and Liquidity

Entering the second half of the year, it is worth keeping in mind that summer equity and bond trading

volumes tend to be lighter than average and as a result, thin trading activity can on occasion exacerbate

volatility and price movements, as numerous investors remain on the sidelines. Among the key questions

Past and projected performance

6

does not guarantee future results.

MARKET COMMENTARY - JULY 2021

investors are pondering at the turn of the second half of the year are: (i) how much good news is already

reflected in market prices; (ii) will financial asset prices be able to cope with and digest the next

pronouncements and policy actions by the Federal Reserve — whether they delay, or accelerate, reducing

monetary policy stimulus; and (iii) what fresh catalysts — earnings, taxation, legislative, public health,

and/or geopolitical — can produce a meaningful move in equity prices and interest rates.

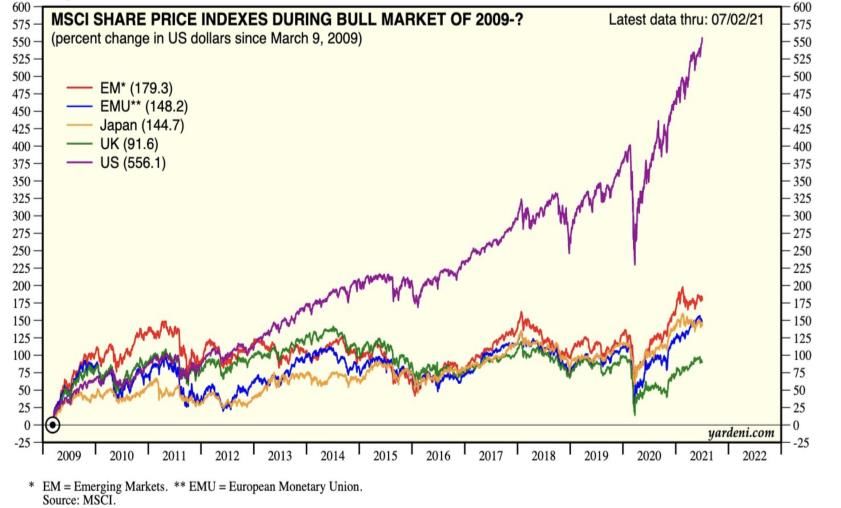

As depicted in the accompanying chart, since the bottom of the Global Financial Crisis on March 9 th, 2009,

U.S. equities (as measured by the MSCI U.S. share price index) have risen by a significant amount — both in

absolute terms (+556.1%), and relative to Emerging Markets, European, Japanese, and U.K. equities.

And over the past year, as shown in the nearby chart of the VIX volatility index, despite episodic instances of

high volatility in certain stocks and industry groups, on an aggregate basis, overall equity market volatility — as

measured by the VIX index — has traced essentially a downward pattern since spiking to a level above 80 at the

beginning of the pandemic-induced economic lockdowns. As goes the time-honored saying in the futures

trading pits in Chicago and globally, “When the VIX is high, it’s time to buy, and when the VIX is low, it’s time to

go slow.” Recent low levels of the VIX volatility index reflect a preternatural (from the Latin for “beyond nature”)

degree of investor calm, complacency, and nonchalance. Such conditions call for an extra degree of investor

caution and vigilance.

Past and projected performance

7

does not guarantee future results.

MARKET COMMENTARY - JULY 2021And with U.S. equities having generated stellar price performance over the past 12 months and VIX volatility

at low levels, it is not surprising to note how popular stocks have become among the household sector. The

accompanying chart shows that U.S. households’ equity allocation as a percentage of total financial assets

has reached a record-high 36.5% in 1Q2021, well above previous secular bull market peaks of 29.7% in

4Q1968 and 32.5% in 1Q2000. These percentages should strike an admonitory note while seeming to

confirm one of the precepts of the legendary Merrill Lynch Investment Strategist Bob Farrell: “The public

buys the most at the top and the least at the bottom.”

In an acronym-laden investment environment (e.g., YOLO = You Only Live Once; FOMO = Fear Of Missing

Out; and TINA = There Is No Alternative), it is also worth keeping in mind the built-up spending power and

potential investing flows represented by the absolute level ($17.16 trillion) and 18-month growth (+$3.5

trillion) of liquid assets on consumers’ balance sheets.

Past and projected performance

8

does not guarantee future results.

MARKET COMMENTARY - JULY 2021Over several cyclical and secular asset pricing movements, we have maintained that the principal drivers of

asset prices are: (i) fundamentals; (ii) valuations; and (iii) psychological/technical/liquidity factors.

And in the time interval leading up to asset price zeniths (where investor psychology is highly optimistic and

euphoric) and leading down into asset price nadirs (where investor psychology is quite despondent and

despairing) by far the most important driver of asset prices is psychological/technical/liquidity factors.

We want to emphasize the importance of recognizing that buoyant investor psychology — evidenced by

such developments as crowd-sourced trading activity, enthrallment with meme and “story” stocks, elevated

initial public offering and options trading volume, fascination with Special Purpose Acquisition Companies

(”SPACs”), and highly unrealistic long-term equity returns expectations, among other aberrations — has

become an increasingly important influence on assets’ investment performance. Reflecting these sanguine

developments, and partly due to abundant global liquidity and massive monetary stimulus, in contrast to

the nine corrections of -5.0% or more during 1999 (itself quite a euphoric year, leading up to the dotcom

bust of early 2000) as of early July, the S&P 500 has not experienced even one -5.0% drawdown in the

previous eight months, representing the longest interval since early 2018.

***********************************************

Prior to this month’s discussion of Portfolio Positioning, the following two sections describe the essential

features, advantages, risks, and investment performance of: (i) Real Estate Investment Trusts; and (ii)

Inflation-Protected Securities.

Past and projected performance

9

does not guarantee future results.

MARKET COMMENTARY - JULY 2021REAL ESTATE INVESTMENT TRUSTS

Description

In its broadest sense, real estate refers to tangible property including land, buildings, oil and mineral rights,

and/or crops that give its owner the right of possession, enjoyment, lease/rental to another party, and

disposal. Real estate may be distinguished from moveable possessions and personal property such as

automobiles and livestock and encompasses a large, fragmented, diverse group of property types,

geographic locations, direct and non-direct ownership structures, and financial characteristics ranging from

highly predictable income-producing properties to speculative assets whose return is purely a function of

changes in capital value. Three related and sometimes imprecise methodologies for valuing real estate

include: (i) the predictability, amount, growth, and financial engineering potential of the cash flow a

property can generate, and the multiple that buyers are willing to pay for this cash flow (this method is

known as the Net Present Value Approach); (ii) reviewing prices for comparable property types; and (iii) the

cap rate, defined as a property’s net operating income before debt service and deprecation, divided by its

purchase price. Two important legislative acts affecting real estate include: (i) the Real Estate Investment

Trust Act of 1960, intended to foster public share ownership of real estate; and (ii) the Tax Reform Act of

1986, which eliminated a large number of real estate tax shelters.

Choices

Public securities markets exposure to real estate and other real assets is available through direct or mutual

fund investment in: (i) REITs dedicated to the apartment, office/industrial, hotel, retail, and other sectors in

the U.S., Europe, and Asia; (ii) non-REIT real estate operating companies; (iii) equities with significant real-

estate assets, in the lodging, gaming, and healthcare industries; and (iv) real estate-related companies such

as homebuilders, construction firms, and title insurers. The non-public markets for U.S. and non-U.S. real

estate and other real assets are many times larger than the public markets and include leveraged or

unleveraged exposure to: (i) owner-occupied residential homes, second homes, single-family rental

properties and smaller commercial assets; (ii) outright ownership of real estate properties, participation in

real estate opportunity funds, core funds, and other types of funds that focus on underperforming assets,

or co-investment with partnership sponsors; and (iii) farmland, forestry and timber, and oil and gas

properties.

Rationale for Investment

i. Due to their relatively straightforward pattern of income generation, several segments of the real-

estate asset class possess important defensive characteristics. The opportunity for cash flows to

increase over time may also allow real estate to prosper in favorable economic and demographic

environments. The returns of Real Estate Investment Trust (REITs) tend to exceed bond returns and at

times are competitive with equity returns.

ii. Due partly to the fact that their returns are largely driven by asset-specific supply and demand

influences, real estate assets generally have low correlations of returns with U.S. and developed non-

U.S. equity, and slightly negative correlations of returns with U.S. and non-U.S. bonds, high-yield bonds,

and emerging-markets equity; they thus may act as an effective diversifier within a portfolio. The

heterogeneity of real estate types and locations also allows diversification within and across real-estate

sectors.

iii. As a tangible, visible, and possibly aesthetically pleasing asset whose supply is reasonably fixed or

which may not be readily expandable due to zoning laws, development restrictions, or land

management and conservation policies, and whose income-generating ability and/or capital values

Past and projected performance

10

does not guarantee future results.

MARKET COMMENTARY - JULY 2021REAL ESTATE INVESTMENT TRUSTS

respond to such forces as employment trends, immigration, new-household formation, and long-term

changes in the general price level, many forms of real estate may function as a hedge against changes

in the general price level.

iv. Owing in part to the relative infrequency and subjectivity of the appraisal process for many property

types, the standard deviation of real-estate returns is generally lower than the standard deviation of

equity returns, and for REITs, may be higher than the standard deviation of the bond returns.

v. Because to some degree it is a relatively inefficient market, real-estate offers the opportunity for skilled

participants to identify and capture value through understanding the structure and potential of specific

properties, financial and operating expertise, market knowledge, and access to relationships.

Risks and Concerns

i. Real estate may not function well as an effective investment in disinflationary or deflationary global,

national, or local economic environments. Although operating income from property tends to lag

changes in the economy due to the nature and tenor of lease terms, during highly adverse times

lessors may cut back on their space commitments, possibly reducing or skipping their real-estate rental

payments without declaring default on their other outstanding debt.

ii. In response to cycles of expansion and contraction, shifting supply-demand conditions, interest rate

movements, borrowing and lending practices, capital gluts and capital vacuums, real estate may at

times be subject to feast-or-famine prices and returns, with substantial divergences between: (i)

property prices and replacement values; and (ii) (for REITs) share prices and per-share net asset values.

iii. Many real estate assets are not divisible and are characterized by illiquidity, high transactions costs,

lengthy time periods to effect the sale or purchase of a property, and significant price discounts

associated with distressed sales.

iv. Certain real-estate properties and forms of ownership may be expensive and/or complicated to locate,

research, value, finance, maintain, manage, lease out, pay taxes on, recapitalize, improve, transfer, and

calculate returns and identify sound exit strategies for.

v. Due to the single-asset, single-region, single-type nature of real estate, its virtual immovability, and

shifts in the relative popularity of certain property types and locations, real estate may be subject to a

number of special considerations, including: (i) bubble-like asset price movements, possibly followed

by sharp price declines; (ii) environmental laws and claims relating to the property itself or its building

materials; (iii) depreciation, depletion, or obsolescence; (iv) the quality of funds from operations (FFO);

(v) localized tax codes, zoning requirements, legal rights, and customs; (vi) exposure to uninsurable

losses stemming from acts of God, terrorism, cybersphere outages and other risks; (vii) the somewhat

shorter lease terms for hotels and apartments than for other properties; and (viii) the generation of

Unrelated Business Taxable Income for tax-exempt U.S. investors.

Past and projected performance

11

does not guarantee future results.

MARKET COMMENTARY - JULY 2021REAL ESTATE INVESTMENT TRUSTS

Source: YCharts and Morningstar

(1) Vanguard Real Estate ETF (VNQ). Seeks to track the performance of the MSCI US Investable

Market Real Estate 25/50 Index measuring the performance of publicly traded equity REITs and other

real estate-related investments. (2) Vanguard Global Ex-US Real Est EFT (VNQI). Seeks to track the

performance of the S&P Global ex-U.S. Property Index, a float-adjusted, market-capitalization-

weighted index measuring the equity market performance of international real estate stocks in

developed and emerging markets. (3) Real Estate Select Sector SPDR (XLRE). Seeks to track the

performance of publicly traded equity securities of companies in the Real Estate Select Sector Index.

(4) iShares Core US REIT EFT (USRT). Seeks to track the FTSE NAREIT Equity REITs Index. (5) Wilshire

US REIT Price Index (WUSREITP). Represents the performance of the Wilshire REIT index that does

not reinvest dividends.

Past and projected performance

12

does not guarantee future results.

MARKET COMMENTARY - JULY 2021INFLATION-PROTECTED SECURITIES

Description

Inflation-indexed securities refer to bonds whose principal and/or coupon payments are adjusted with the

general level of prices as measured by a commonly accepted price index. In January 1997, the U.S. Treasury

began auctioning capital-indexed bonds, known alternatively as Treasury Inflation Protection Securities

(TIPS) or Treasury Inflation Indexed Securities (TIIS). Originally issued with maturities of 5, 10, and 30 years,

TIPS generally pay semiannual fixed real coupons multiplied by a principal amount that is adjusted upward

monthly by an accretion amount paid to the investor at maturity and determined with a 3-month time lag

by the non-seasonally adjusted Consumer Price Index for All Urban Consumers (CPI-U). TIPS are usually

noncallable securities and often have fairly long durations relative to their maturities because a significant

portion of the total return is in the form of the inflation-adjusted principal amount paid at final maturity.

Any interim price deflation accruals are deducted from inflation accruals; in the arguably tumultuous and

highly unlikely event of cumulative deflation over the life of a TIPS security, its principal amount is

guaranteed to be repaid by the U.S. Treasury at its original face value.

Choices

In addition to TIPS, other capital-indexed bonds (and in a more limited number of cases, interest-only

indexed bonds and indexed-annuity bonds) have been issued on a limited basis in a variety of maturities

and structures by federal agencies, corporations, and municipalities, and sometimes in meaningful

quantities by non-U.S. issuers in more than 20 foreign capital markets. Several inflation-protection mutual

funds seek to add value in excess of annual management fees through sector, issuer, and maturity selection

and other tactics aimed at benefitting from supply-demand imbalances, seasonal factors, yield-curve

movements, and changing expectations for the general price level. Some investors monitor the equivalent

maturity, preferring TIPS if the actual inflation rate is expected to be above the breakeven spread, and

conventional U.S. Treasury bonds if the actual inflation rate is expected to be below the breakeven spread.

Subject to annual per-person limitations on new purchases, Series I inflation-indexed accrual security U.S.

savings bonds have a number of TIPS-like features.

Rationale for Investment

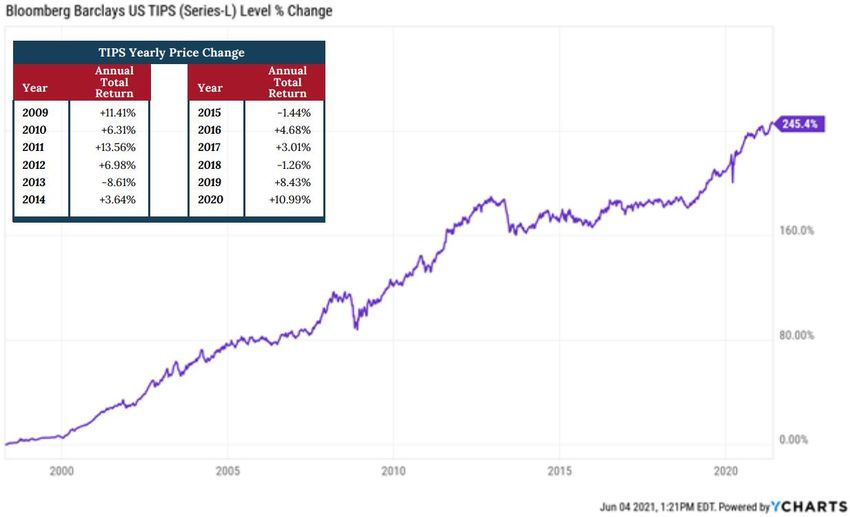

i. TIPS offer an effective hedge against inflation through a reliable stream of real income payments and

adjustments to principal that can keep pace with the price increases in a market basket of consumer-

oriented goods and services.

ii. Due to their high degree of correlation with unanticipated inflation episodes over the course of

multidecade economic and financial cycles, TIPS have tended to exhibit very low or meaningfully

negative correlations of 1- to 10-year returns with U.S. and non-U.S. equities, similar-duration

conventional U.S. bonds, and alternative asset classes, and moderate to high correlations of 1- to 10-

year returns with cash instruments.

iii. Because of the relative stability of real interest rates, which have tended to be approximately one-third

to one-half as volatile as nominal interest rates, TIPS generally behave as low-volatility assets, with

standard deviations of annual returns that tend to be one-fourth to one-fifth those of equities and

similar-duration bonds.

iv. Owing to their low standard deviations of annual returns, their low or negative correlations of 1- to 10-

year returns with most asset classes, and their frequently favorable real-yield comparisons versus the

real yields of conventional bonds, TIPS may reduce the overall long-term risk level of a portfolio of

assets.

Past and projected performance

13

does not guarantee future results.

MARKET COMMENTARY - JULY 2021INFLATION-PROTECTED SECURITIES

v. As a result of their different degree of price responsiveness compared to other asset classes in varying

financial environments, and their positive return characteristics in periods of stable-to-falling real

interest rates coupled with rising inflation, in appropriate circumstances, TIPS can serve as an effective

diversifying substitute for conventional bond-like asset classes, in some cases allowing potentially

greater emphasis on equity-like and/or alternative asset classes.

Risks and Concerns

i. For taxable investors, the semiannual real interest payments on TIPS are taxed each year as ordinary

income, even though the monthly inflation adjustments to principal are not received until the final

maturity of the bond; the amount of this “phantom income” is also fully taxable each year. In

sufficiently high tax brackets and at moderately high CPI inflation rates, TIPS may very well generate

negative current cash flow. As a result, taxable investors may need to hold TIPS in tax-deferred

accounts and/or to consider instead tax-exempt inflation protection securities (TEIPS).

ii. Depending upon the duration of the TIPS and the magnitude of the real interest rate rise, higher real

interest rates may cause capital losses on TIPS. The level of real interest rates is generally influenced by

fluctuations in capital supply-demand factors such as real economic growth rates, federal budget

and/or balance of payments surpluses or deficits, and monetary policy.

iii. For a series of holding periods of one year of less, TIPS may lose some of their beneficial diversification

features due to moderate or high correlations of returns with conventional bonds caused by short-term

common movements in real and nominal yields, flight-to-quality effects, and other factors.

iv. During periods of declining inflation expectations, falling inflation rates, or outright deflation, TIPS may

underperform conventional bonds of the same maturity or duration.

v. TIPS possess certain potentially complicating features associated with: (i) their post 1997 status as a

relatively new, untested, not widely understood, and somewhat lower liquidity instrument sometimes

featuring wider bid-asked trading spreads; (ii) the behavior of, and interaction among, expected

inflation, inflation risk premiums, nominal interest rates, and real interest rates; (iii) the risk that a

decline in the external purchasing power of the U.S. dollar may exceed its domestic adjustment for

inflation; and (iv) the efficacy of various index contingencies available to the U.S. Treasury in the event

that the applicable Consumer Price Index is discontinued or fundamentally altered in a manner

materially adverse to TIPS investors.

Past and projected performance

14

does not guarantee future results.

MARKET COMMENTARY - JULY 2021INFLATION-PROTECTED SECURITIES

Source: YCharts & Morningstar

(1) Seeks to track the investment results of the Bloomberg Barclays U.S. Treasury Inflation Protected

Securities (TIPS) Index (Series-L) which is composed of inflation-protected U.S. Treasury bonds. (2)

Seeks to track the total return of the Bloomberg Barclays U.S. Treasury Inflation-Linked Bond Index

(Series-L) SM. (3) Seeks to track the performance of the Bloomberg Barclays U.S. Treasury Inflation-

Protected Securities (TIPS) 0-5 Year Index. (4) Seeks to track the price and yield performance of the

Bloomberg Barclays U.S. Government Inflation-Linked Bond Index. (5) Seeks to track the investment

results of the Bloomberg Barclays U.S. Treasury Inflation-Protected Securities (TIPS) 0-5 Years Index

(Series-L). (6) Seeks to track the price and yield performance of the FTSE International Inflation-

Linked Securities Select Index.

Past and projected performance

15

does not guarantee future results.

MARKET COMMENTARY - JULY 2021PORTFOLIO POSITIONING

Portfolio Positioning Strategies:

In the current moderately slowing economic expansion and somewhat softer yields environment, we

believe that careful thought, planning, and attention needs to be devoted to the investor’s most

appropriate forms and vehicles for implementing the fundamental elements of Asset Allocation and

Investment Strategy, which include:

i. Diversification: which means having sustainably low- and negatively-correlated investment exposures

that truly counterbalance price movements in other assets, particularly during times of great financial

stress and/or market volatility;

ii. Rebalancing: which encompasses using concepts of reversion to the mean to trim exposures to assets

that have grown to represent too large a portion of the overall portfolio, while at the same time,

adding exposure to high-quality assets that have fallen out of investor favor and suffered significant,

though deemed not permanent, price declines vs. intrinsic value;

iii. Risk Management: which involves recognizing when markets become consumed by meme securities,

momentum plays, “story stocks,” and information overload — a situation that has pertained in recent

months to more than a few companies in the technology space — and understanding the degree of

liquidity, the true pricing realism, and the appropriate roles of short-term liquid securities, real assets,

financial assets, and alternative assets in decades-long (or longer) regimes of inflation, stagflation,

deflation, monetary disruptions, and currency resets;

iv. Reinvestment: which encompasses knowing when to emphasize and trade off income versus capital

growth, all the while keeping in mind the critical importance of discipline, equanimity, patience, tax

awareness, and longevity in capturing and compounding dividend, coupon, rental and other income

flows; and

v. Asset Protection and Husbandry: which encompass considerations of income and capital gains

taxation at the state, local, federal, and possibly international level; estate planning; relevant insurance

design and structuring; cybersecurity shielding; portfolio monitoring and reporting; administrative

costs; forms, frequency, and means of access; and custody.

Portfolio Positioning Principles:

We continue to allocate to a considered and considerable exposure to equities, with judicious shifts

between styles, sectors, geographies, and — where appropriate from a cost, timing, tax, liquidity, and size

standpoint — public versus private markets. Expressed below are a number of themes that we believe

should be taken into consideration over the next few years in selecting asset categories, asset classes, asset

managers, sectors, companies, and security types:

i. Paying Attention to the Value of Money: Taking advantage of (rather than being taken advantage of

by) the likelihood of money printing, internal and external currency debasement, government debt

monetization, and the ‘Modern Monetary Theory’ approach that to some degree in the pandemic-

response era has been pursued by the Authorities — within shifting money and credit cycles — to

service America’s massive explicit government and corporate indebtedness and the enormous implicit

obligations of pension and healthcare promises;

Past and projected performance

16

does not guarantee future results.

MARKET COMMENTARY - JULY 2021PORTFOLIO POSITIONING

ii. Concentrating on “All-Weather” Sectors and Companies: Seeking investments with balance and

flexibility, that are able to thrive regardless of: which political persuasion informs the thinking and

policies of the White House and/or Congress; evolving Environmental, Social, and Governance (ESG)

priorities and values; wealth distribution initiatives and public health conditions; and wider

socioeconomic trends;

iii. Distinguishing Between Temporary and Permanent Change: Focusing on the commercial and financial

implications of new social and political power structures, alliances, and geopolitical relationships; new

energy sources and resources; new trade patterns; new on- and offshoring channels; new “WFH” and

“WFA” (Work From Home and Work From Anywhere) employment modalities; and new business

models, pathways, digitalizations, and forms of person-to-person and business-to-business work,

leisure, learning, and wellness activity;

iv. Taking Advantage of Demographic Tailwinds: Through U.S. and select non-U.S. companies, gaining

exposure to, and meeting the rising needs, aspirations, and spending power of, the rapidly expanding

global middle class, especially in Asia;

v. Comprehending and Verifying Past Success: Emphasizing companies and sectors that have

demonstrated successful track records and past experience in: capital allocation; balance sheet

strength; risk management; sustainably defendable business models; and the ability to generate and

sustain high multiyear returns on equity (derived from revenue growth and favorable margin

preservation, rather than through overly high levels of leverage) meaningfully above the companies’

and sectors’ weighted average cost of capital; and

vi. Identifying Innovative and Disruptive Technology Hegemons: Focusing on technology enablers,

disrupters, and dominators in biotechnology, diagnostics and therapeutics based on CRISPR (Clustered

Regularly Interspaced Short Palindromic Repeats) public health, artificial intelligence, data analytics,

machine learning, 5G cellular network technology, the Internet of Things, infrastructure, robotics,

quantum computing, battery inventions, alternative energy, electric vehicles, and cybersecurity, while

not least, also taking account of the Environmental, Social, and Governance (ESG) characteristics of

companies in these and other fields.

Past and projected performance

17

does not guarantee future results.

MARKET COMMENTARY - JULY 2021Important disclaimers and disclosures

Unique Wealth (“Unique”) is a registered investment adviser with the Securities and Exchange

Commission. Any reference to the terms “registered investment adviser” or “registered” does not imply

that Unique or any person associated with Unique has achieved a certain level of skill or training. A copy of

Unique Wealth’s current written disclosure statements discussing our advisory services and fees is

available for your review upon request.

This message is intended for the exclusive use of clients or prospective clients of Unique Wealth. It should

not be construed as an attempt to sell or solicit any products or services of Unique or any investment

strategy, nor should it be construed as legal, accounting, tax or other professional advice. Different types

of investments involve varying degrees of risk, and there can be no assurance that any specific investment

will either be suitable or profitable for a client or prospective client’s investment portfolio.

This material is proprietary and may not be reproduced, transferred, modified or distributed in any form

without prior written permission from Unique. Unique reserves the right, at any time and without notice,

to amend, or cease publication of the information contained herein. Certain of the information contained

herein has been obtained from third-party sources and has not been independently verified. It is made

available on an "as is" basis without warranty. The content of this communication is provided solely for

your personal use and shall not be deemed to provide access to any particular transaction or investment

opportunity. Unique does not intend the information in this Presentation to be investment advice, and the

information presented in this communication should not be relied upon to make an investment decision.

The views expressed in the referenced materials are subject to change based on market and other

conditions. This document contains certain statements that may be deemed forward‐looking statements.

Please note that any such statements are not guarantees of any future performance; actual results or

developments may differ materially from those projected. Any projections, market outlooks, or estimates

are based upon certain assumptions and should not be construed as indicative of actual events that will

occur.

Historical performance results for investment indices and/or product benchmarks have been provided for

general comparison purposes only, and do not include the charges that might be incurred in an actual

portfolio, such as transaction and/or custodial charges, investment management fees, or the impact of

taxes, the incurrence of which would have the effect of decreasing historical performance results.

Past and projected performance

18

does not guarantee future results.

MARKET COMMENTARY - JULY 2021You can also read