NSIF Stock Pitch BUY Recommendation

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Recommendation:

BUY

NSIF Stock Pitch

Group 5: Marcus, Andrew, Zhi You

Agenda

Industry and company overview

Investment thesis

Financials

Industry Overview

● Singapore’s telecommunications sector is competitive, but not the fibre

network sector

○ 4 telco operators (Singtel, Starhub, M1, TPG) with several MVNO partners

○ Main fibre infrastructure provider in Singapore: Netlink Trust

● Main business segments for telco operators:

○ Mobile, Pay-TV, Broadband

● High capital expenditure for telco & fibre network operators to maintain &

develop physical infrastructure

● Industry developments

○ Smart Nation Initiative 2015: government initiative to harness technologies and networks

for enhanced connectivity

○ Roll-out of 5G technology in Singapore & planned release of 2 full-fledged licences by IMDA

What is Netlink NBN Trust (CJLU)?

Porter’s 5 Forces Analysis

Low bargaining ● Many suppliers for materials procurement & many

power of suppliers contractors/developers for services outsourcing

Moderate bargaining ● Three major internet service providers (Singtel, M1,

power of buyers Starhub) with other smaller players

● Regulated pricing model by IMDA

Low-moderate threat ● Fibre optics is currently the main technology underlying

of substitutes broadband connections

● Netlink is poised to benefit from 5G rollout in Singapore

Low-moderate threat ● High barriers to entry due to 1) government regulation;

of new entrants 2) high capital startup costs

● Existing telcos & utility companies may contemplate

entering the fibre industry

Low industry rivalry ● Due to IMDA’s appointment, Netlink is effectively a

Industry Attractiveness monopoly operating Singapore’s fibre network

0.910 CJLU.SI Market cap: 3.51B Shares outstanding: 3.897B PE: 44.33 PB: 1.1948 ROE: 2.5%

1. Well positioned for 5G roll-out ● Singapore is set to introduce 5G in 2020, with 50% coverage by 2023 ● IMDA specifies 5G based on standalone network infrastructure, focusing on network sharing ● 5G capital expenditure estimated 2 -3x more than 4G and reach up to $1.5 billion by telcos

1. Well positioned for 5G roll-out

● Fibre network necessary for 5G base stations backhaul

connections

● Future revenue for Netlink expected to increase

○ Netlink is the sole operator of Singapore’s fibre

infrastructure

○ Fairer pricing as Netlink’s prices are regulated2. Growth of residential segment ● Residential units are expected to grow at an annual rate of 2.3% between 2016 and 2021 ● This translates to approximately 170,000 new residential premises in the market

2. Growth of residential segment

2. Growth of non-residential segment

● Singapore’s emphasis on being an international business and technology

hub

● Future urban transformation projects up to 2023 which would require

Netlink’s fibre capabilities once completed, eg., Punggol Digital District and

Jurong Innovation District are potential clients

● Reduce reliance on residential segment as bulk of revenue and increase the

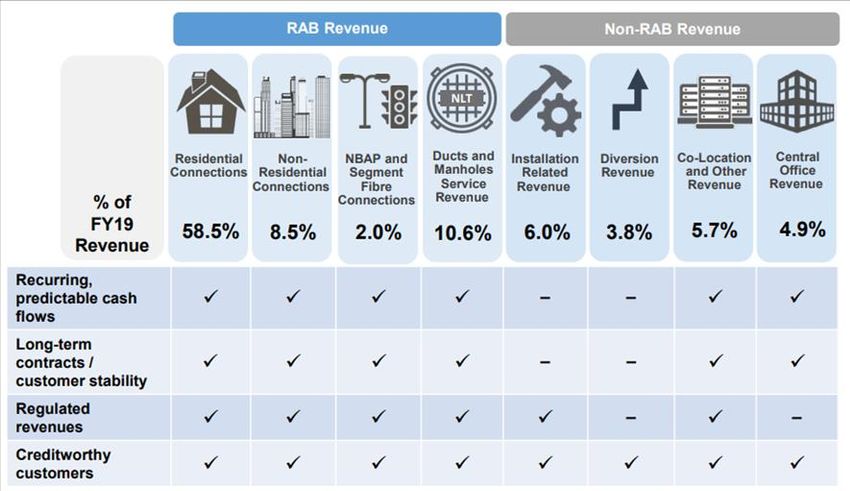

proportion of revenue in non-residential and NBAP segments3. Resilient Business Model ● IMDA’s Regulated Asset Base model allows Netlink to earn 80% of its revenue at a guaranteed, regulated rate of return ● For 2017 to 2022, IMDA sets fibre connection prices such that Netlink earns a 7% pre-tax return on capital investments ● A further 10% of its revenue comes from long-term contracts → 90% of revenue either regulated or contractual

3. Resilient Business Model

Sustainable Distribution Yield

● FY2019 distribution (dividend) yield of 6.0%

● Projected to sustain distribution yield at around 5.0 -

6.0% up till FY2022 due to:

○ Monopolistic status

○ Strong growth potential

○ Resilient business model

● In the short to medium term, good defensive stock

that can perform well in a potential recession as a

dividend playFinancial Projections

Absolute Valuation - DCF Analysis

CAPM Inputs Source

Risk-free rate 1.75% SG 10Y Government Bond (October)

Market risk premium 7.75% Bloomberg WACC

Beta 0.342 Bloomberg Historical Beta

Cost of equity 4.40%

Implied Enterprise Value SGD 5,820 M

WACC = 84.2% x 4.40% + 15.8% x 2.30%

= 4.10%

Implied Equity Value SGD 5,260 M

PV of Cumulative FCFF SGD 800 M Shares Outstanding 3,897 M

PV of Terminal Cash Flow SGD 5,020 M Intrinsic Value per Share SGD 1.35Relative Valuation - P/E Analysis

● High PE Ratio : 44.3 compared to the Telecom industry

average (17.5) and the Singapore market (13.4).

● From our investment theses, high expected growth rate

might justify its high PE ratio

● Effect of Depreciation & Amortisation on EPS & hence

PE ratio

● Difficulty in finding truly comparable companies

○ Bharat Broadband Network of India

○ Hong Kong Broadband Network PE ratio of 87.5Conclusion

● Good medium-term prospects due to sustainable

distribution yield at 6.0%

● Robust and resilient business model in an attractive industry

● Strong projected long-term growth from tailwinds &

catalysts; backed by financials and valuation analysis

○ 50% potential upside in capital appreciationYou can also read