Natural Gas & LNG Trends in Asia - LNG Solutions in Prime Play - Global LNG Hub

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

85

SECTOR BRIEFING

DBS Asian Insights

DBS Group Research • November 2019

Natural Gas &

LNG Trends in Asia

LNG Solutions in Prime Play

DBS Asian Insights SECTOR BRIEFING 85 02 Natural Gas & LNG Trends in Asia LNG Solutions in Prime Play Pei Hwa HO peihwa@dbs.com Suvro Sarkar suvro@dbs.com Jason SUM jasonsum@dbs.com Jinmyung Choi NH Investment & Securities Produced by: Asian Insights Office • DBS Group Research go.dbs.com/research @dbsinsights asianinsights@dbs.com Wen Nan Tan Editor Martin Tacchi Art Director

DBS Asian Insights

SECTOR BRIEFING 85

03

04 Executive Summary

09 LNG Value Chain Demand Supply Analysis

LNG Value Chain Overview

LNG Demand and Regas Forecast

LNG supply and Liquefaction Forecasts

31 Key LNG Asset Classes

LNG Liquefaction Terminals

LNG Receiving Assets

LNG Carriers

45 Beneficiary of Booming Demand for Gas

Solutions

Korea’s Winning Formula

DBS Asian Insights

SECTOR BRIEFING 85

04

Executive Summary

Snapshot of the LNG value chain and relevant asset classes

LNG LNG LNG

upstream midstream downstream

Onshore

Onshore gas Onshore LNG Trucking regasification

production liquefaction

Storage Transmission

and distribution

Offshore gas Offshore LNG Shipping

production liquefaction Offshore

regasification

Floating, liquefied natural Floating, storage

LNG Carrier (LNGC)

gas units (FLNG) regasification units (FSRU)

Source: DBS Bank

LNG investment cycle As the global LNG demand upcycle continues to play out, with various demand drivers firmly

to pick up steam in place, especially in Asia (read our previous report: “Natural Gas & LNG Trends in Asia – The

Volume Game is Strong”), we believe the LNG investment cycle could reach another inflexion

point soon as the market will likely turn from current oversupply situation into a supply deficit

situation beyond 2022, if no new liquefaction projects are sanctioned beyond what is already

in the pipeline.

In addition, despite some near-term hiccups owing to trade tensions and global growth

slowdown, LNG demand to 2025 is still projected to grow at 6% CAGR, the fastest growing

among fossil fuels. This will spur ongoing demand for LNG solutions in Asia – LNG carriers,

Floating Storage Regasification Units (FSRUs) and Floating LNG (FLNG) vessels. Consequently,

this will directly benefit the leading Asian shipyards.

DBS Asian Insights

SECTOR BRIEFING 85

05

LNG market could turn into supply deficit by 2030 if no new liquefication projects

are sanctioned

Source: International Gas Union (IGU), DBS Bank

Global LNG demand forecast till 2025

Source: IGU, Clarkson Research, DBS Bank

Global LNG We anticipate global LNG liquefaction (export) capacity to reach around 588mtpa in 2025

liquefaction capacity from 380mtpa in 2018 (55% growth). Of this, 110mtpa of capacity was under construction

expected to reach as at end-2018. In addition, we expect more liquefaction projects to reach final investment

around 588mtpa in decisions (FID) stage between now and 2021, to facilitate construction of another c.100mtpa

2025 of capacity by the end of our forecast horizon in 2025. Within the seven-year period between

2018 and 2025, most of the capacity growth will primarily be driven by the oil supermajors

and national oil companies (NOCs), owing to their better ability to adapt to rapidly evolving

industry dynamics. On a country level, those having favourable long-term marginal cost

LNG profiles like Qatar, Russia, and the United States will lead the charge. Newcomers like

Mozambique and Canada are also expected to make a big splash towards the end of our

forecast period (2024-25) and become solid contenders in the LNG supply market.

DBS Asian Insights

SECTOR BRIEFING 85

06

Do not discount We predict 17% or 25 of proposed LNG projects plan to adopt FLNGs in future. While natural

Floating LNG (FLNG) gas production will likely continue to be spearheaded by shale gas developers, we believe the

solutions for production FLNG market will also expand given that:

requirements

1. 67% of natural gas reserves (excluding those within shale formations) are located

underwater

2. 45% of underwater reserves are held in deep sea areas (where explorations are not

feasible without FLNGs)

Moreover, given that the inaugural batch of FLNGs have been in operation since 2018,

development/operational costs for gas field projects using FLNGs can now be evaluated and

analysed, and once these first batch of projects using FLNGs prove to be cost efficient, FLNG

adoption is likely to increase further.

LNG import capacity We expect global nominal LNG import capacity to increase to 1,085mtpa in 2025 from

will also soar, especially 823mtpa in 2018. Again, we expect an additional approximately c.140mtpa of projects to be

in Asia sanctioned and added till 2025, on top of what is already sanctioned. China will undoubtedly

remain the most critical driver of LNG demand, but other Asian countries like Thailand,

Pakistan, Vietnam and Bangladesh are expected to contribute in a big way as well, backed

by an upswing in gas-to-power projects and depleting indigenous gas production. India’s role

in the LNG growth story, while important, will be impeded to an extent by rising domestic

gas supply, domestic infrastructure bottlenecks, and lack of focus on gas in the power sector.

Smaller Asian countries of South and Southeast Asia will account for 26% of

incremental LNG regas capacity to 2025

Note: JKT refers to traditional Asian LNG markets of Japan, Korea Taiwan

Rest of Asia includes Thailand, Malaysia, Singapore, Pakistan, Bangladesh, Vietnam, Myanmar, Sri Lanka, Philippines, Hong Kong

Source: IGU, Clarkson Research, DBS Bank

DBS Asian Insights

SECTOR BRIEFING 85

07

We estimate around Onshore regasification unit costs have been trending up in recent years, as project developers

US$31bn of capital aim to bolster supply stability. On the other hand, offshore regasification unit costs have

investments in LNG remained steady as the controlled environment in shipyard construction promotes cost stability.

receiving terminals in Based on our earlier additional regasification capacity projections, we estimate there will be

Asia till 2025 around US$31bn of additional capital investment requirement in LNG receiving terminals in

Asia (excluding Japan, Korea, and Taiwan) between 2018-2025. China and India will account

for the lion’s share at around US$10bn and US$7bn respectively, while the remaining US$14bn

is split between other Asian countries like Pakistan, Bangladesh, Thailand, and Vietnam.

Floating Storage The impetus for choosing floating over land alternatives is multi-fold, but financing constraints

Regasification Units tend to be the most critical factor in developing countries. The capital outlay for a mid-scale

(FSRUs) preferred in (c.3mtpa) land terminal and other onshore infrastructure usually falls in the range of US$600-

new emerging LNG 750m, a substantial amount that necessitates foreign capital for project financing. However,

markets of Asia financing tends to be costly for emerging markets with elevated country and default risks.

Electing to use FSRUs can help developing countries circumvent financing challenges, since

FSRU projects require 30-50% less outlay than a land terminal with similar specifications.

Furthermore, chartering a FSRU, rather than an outright purchase, can reduce initial investment

costs even further, and mitigate potential cash flow mismatches, as the timing of revenue

inflows will be more consistent with operating costs (which forms most of the cash outflows).

Demand for LNG Bullish LNG market conditions bode well for related shipping players and builders. Amid rising

Carriers (LNGCs) to pick LNG shipping demand, vessel supply appears to be still insufficient. Global marine LNG trade

up in line with greater volume is set to expand at a CAGR of 9.5% over 2018 to 2019. Owing to the US-China trade

LNG use dispute, LNG trade volume between the two countries over 2018c. 2019 is likely to tumble

by 66% compared to before the dispute broke out. Despite this, global LNG trade volume

remains on the rise, suggesting that issues such as the US-China trade dispute will not affect

the changing global energy mix trend.

LNG Carrier supply We note that there are only a few orders for LNGCs scheduled to be delivered after 2022.

beyond 2022 appears To meet demand, LNGC orders placed in the coming years for delivery after 2022 could

insufficient in our view potentially expand 33.7% (shipping capacity basis) compared to the 2017~2018 average.

Such an increase in newbuilding orders will benefit the shipbuilding market.

Surge in US LNG Since the US began exporting LNG, approximately 1.8 ships have been needed for each

cargoes to increase 1mtpa of supply, which is considerably greater than the global average shipping multiplier

demand for LNG of 1.3x. According to S&P Platts, the average distance covered by a laden LNG ship from

Carriers the US stood at 9,268nm in 2018, compared to 3,936nm and 5,602nm for Australia and

Qatar respectively, highlighting the vast distance between the US and central demand points.

Hence, we expect the global average shipping multiplier to continue trending up as the US

powers ahead in supply, which should further propel the demand outlook on LNGCs.

DBS Asian Insights

SECTOR BRIEFING 85

08

No. of LNGCs required for each mtpa of US LNG has been increasing amid growing exports to Asia

Source: Gaslog Ltd, NH I&S Research Center

Shipping route changes Demand for LNGCs is expected to pick up, and the market penetration of super-sized LNGCs

to spark demand for is set to strengthen. At present, LNG shipping players mainly use shipping routes passing

super-sized LNGCs through the Panama Canal and Suez Canal. Thus, the global LNGC fleet is now mainly

composed of 160c. 174k cubic metre (CBM) Panamax vessels that can pass through the

canals. However, expected changes in shipping routes should lead to greater demand for

super-sized LNGCs (larger than Panamax ships).

Korean yards dominate Korean yards have been dominating the LNG carrier market, which is widely recognised for

the LNG solutions its high technical barriers of entry owing to the inherent characteristics of transporting a

space highly flammable fuel that needs to be stored at super low temperatures at below -160°C

with low specific gravity. However, leading Singapore and Chinese shipyards will also enjoy

some spillover effects of the demand uptrend for LNG solutions like Floating LNG (FLNG) and

LNG carriers, as they continue building their track record. Those companies providing LNG

containment systems and insulation systems also stand to benefit from this trend.DBS Asian Insights

SECTOR BRIEFING 85

09

LNG Value Chain Demand

Supply Analysis

LNG Value Chain Overview

The liquefied natural gas (LNG) value chain begins at the upstream stage, where natural

gas is discovered and extracted and then piped to a liquefaction facility, either an onshore

liquefaction terminal, or a floating liquefied natural gas vessel (FLNG).

After impurities and liquids are removed from the natural gas at the processing facility at the

liquefaction terminal, the gas is then cooled to -160ºC, where it is converted to a liquid state

(as its volume reduces by 600 times from its gaseous state) and then loaded on super-cooled

storage tanks aboard LNG carriers to be transported to import terminals (commonly referred to

as regasification terminals). At that stage, LNG is first stored in special cryogenic storage tanks,

subsequently regasified with LNG vaporisers, and finally odourised before being transported

via natural gas pipelines to gas fired power plants, industrial and petrochemical facilities or

commercial and residential users.DBS Asian Insights

SECTOR BRIEFING 85

10

Comprehensive overview of the LNG value chain

Source: IGU, DBS Bank

LNG Demand and Regas Forecasts

What is the present LNG demand situation?

China, the global gas The past few years marked the rise of China as a global gas superpower, as the Chinese titan

superpower overtook South Korea as the world’s second largest LNG importer in 2017, while accounting

for nearly 50% of global LNG demand growth between 2015 to 2018. LNG consumption in

the rest of Asia during the same period saw incredible momentum as well, representing 40%

of global LNG demand growth with a 28.4mt increase in net imports.

Unsurprisingly, the slowdown in Asia’s LNG demand growth this year reverberated throughout

the market. With the region’s demand for LNG failing to keep pace with breakneck supply

growth, the spread between Asian and European spot LNG prices have shrank to the point

where Asia no longer commands an adequate gas premium for LNG exporters, which led to

a diversion of spot LNG to Europe.DBS Asian Insights

SECTOR BRIEFING 85

11

Though Europe has traditionally been a dumping ground for LNG, the region has been

particularly instrumental in soaking up new cargoes this year, with global exports to the region

swelling to 51 tonnes (+130% y-o-y) in the first six months of 2019. However, absorption of

excess supply by Europe may soon come to an end as the region’s storage capacity approaches

its limits.

Historical LNG net imports (2011-2018)

Source: IGU, DBS Bank

Historical LNG imports (including re-imports) 2019 YTD

Source: Poten & Partners, DBS BankDBS Asian Insights

SECTOR BRIEFING 85

12

US exports shifted to Europe amid spread compression

Source: Bloomberg Finance L.P., DBS Bank

Europe’s gas storage is filling up at an incredibly fast pace

Source: Gas Infrastructure Europe, DBS BankDBS Asian Insights

SECTOR BRIEFING 85

13

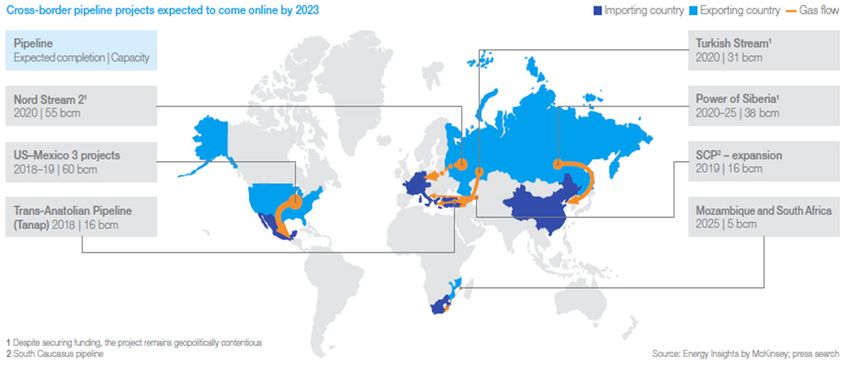

Will cross-border pipeline gas pose a threat to LNG demand

growth?

Pipeline gas exports Despite the proliferation of LNG, there are still many countries that are heavily dependent on

play an important role pipeline gas today. In Europe, Russian and Norwegian pipeline exports constitute the majority of

in Europe, China and gas supply in countries like Germany, France, Italy and Turkey, while in North America, US pipeline

Mexico gas makes up the bulk of Mexico’s gas supply. In central Asia, pipeline gas from Turkmenistan,

Uzbekistan and Kazakhstan have been crucial in facilitating China’s transition away from coal.

Over the next five years, we anticipate cross-border pipeline capacity additions of around

120bcm, 80bcm and 45bcm in Europe (Russia and Azerbaijan to Europe), North America (US

to Mexico), and North Asia (Russia to China) respectively.

Relevance of pipeline Even with more cross-border pipelines surfacing in Europe, we believe LNG will take market

gas in Europe should share away from pipeline gas in the region for several reasons:

fade gradually

1. LNG can help allay energy security concerns as many countries in Western Europe are overly

dependent on Russia for its gas supply (granting Moscow considerable political leverage

2. Expiry of around c.50bcm worth of long term pipeline contracts over the next seven

years, coupled with ample unutilised regasification capacity in the region suggests that

Europe could readily pivot towards LNG

3. Europe is well positioned to benefit from the favourable LNG price environment as

it is best suited to accommodate the incoming flood of US LNG due to its proximity

compared to Asia

4. Gas pipeline exports to Europe from Azerbaijan will require time to gain traction as the

country’s domestic gas production is not growing fast enough

Pipeline gas accounts for around 45% of Europe’s gas supply; Russian pipeline gas

makes up 35% of gas supply in Europe

Source: BP PLC, DBS BankDBS Asian Insights

SECTOR BRIEFING 85

14

LNG import terminals among European countries are relatively underutilised…

Source: IGU, DBS Bank

…allowing them to shift towards LNG as fixed pipeline contracts expire over the

next seven years

Source: EIA, DBS Bank

On the demand side, favourable government policies and more coal-to-gas switching will

increase the share of natural gas in China’s energy mix – the Government has set a target of

10% by 2020, and 15% by 2030, up from 7.4% in 2018. While domestic supply will grow at

a faster pace over the next few years with the government’s call for the national oil companies

to accelerate upstream activity, we still expect supply growth to trail demand growth due to

inherent challenges in the upstream sector.DBS Asian Insights

SECTOR BRIEFING 85

15

While China might yield decent results in boosting conventional and tight gas production,

more time is required to climb the steep learning curve to unlock its shale and coal bed

methane gas reserves in a more cost-effective manner without subsidies, according to

Woodmac. Testament to the difficulties in shale gas, BP, the last of the international oil majors

involved in China’s shale gas development, recently exited the country in April-2019 after

drilling eight to ten wells in Sichuan with disappointing results.

One major obstacle in China’s natural gas infrastructure is its severe lack of storage capacity

– the country’s total underground storage capacity available for peak shaving of 10bcm (as

at end-2018, excluding tank capacity at LNG receiving terminals) only accounted for a mere

3.5% of total gas consumption, which is drastically lower than the international average of

15%, according to IHS Markit. As storage bottlenecks are unlikely to be resolved in the near

to medium term, LNG is the only alternative to manage sharp supply deficits during winter

months, when gas demand can be double the average daily consumption.

CNPC – which accounts for around 69% of China’s gas production – might have set

an overly ambitious shale gas target

Source: PetroChina, DBS BankDBS Asian Insights

SECTOR BRIEFING 85

16

China’s import dependency trending up as production lags demand

Source: BP PLC, DBS Bank

While cross-border pipeline gas could adversely impact LNG demand in Europe and China,

we believe prospects in other parts of Asia are murky at best. Natural gas production within

Asia (excluding China) is gradually diminishing and is likely on a long-term structural decline,

discouraging the development of new intra-region pipeline gas connections. The Trans-ASEAN

gas pipeline project has made little progress in recent years due to a lack of stable feed gas

supply from Indonesia, according to S&P Platts, while the fate of the TAPI pipeline that was

meant to bring gas to India from Turkmenistan remains uncertain.

In addition, the significant distance between the top natural gas producers and prominent gas

demand centres like India, Thailand, Pakistan and Bangladesh renders pipeline connections

to not only be economically unfeasible, but extremely time consuming as well. Furthermore,

there are a host of other challenges with pipeline gas that can be overcome with LNG, such

as an acute lack of flexibility in end markets, complicated geopolitical issues (particularly if the

project involves a transit in another country), and narrow supply diversity.

Asia’s (excluding China) gas production remained flat from 2010

Source: BP PLC, DBS BankDBS Asian Insights

SECTOR BRIEFING 85

17

LNG is more competitive for transportation distances beyond 1,000km

(offshore) and 3,000km (onshore)

Source: Delft University of Technology, DBS Bank

New cross border pipeline projects are concentrated in North America and Europe

Cross-border pipeline projects expected to come online by 2023 Importing Country Exporting Country Gas Flow

Pipeline Turkish Stream1

Expected completion | Capacity 2020 | 31 bcm

Nord Stream 21 Power of Siberia1

2020 | 55 bcm 2020-25 | 38 bcm

US-Mexico 3 projects SCP2 - expansion

2018-19 | 60 bcm 2019 | 16 bcm

Trans-Anatolian Pipeline Mozambique & South Africa

(Tanap) 2018 | 16 bcm 2025 | 5 bcm

1: Despite securing funding, the project remains geopolitically contentious

2: South Caucassus pipeline

Source: McKinsey, DBS BankDBS Asian Insights

SECTOR BRIEFING 85

18

LNG regasification capacity and demand forecast till 2025

We expect global nominal LNG import capacity to soar to 1,085mtpa in 2025 from 823mtpa

in 2018, which is about 141mtpa higher than purely factoring in projects that are currently

under construction. However, we estimate global underlying LNG demand, or weather-neutral

demand, will grow at an even more rapid CAGR of 6.1% between 2018 to 2025, to 479mt

from 317mt in 2018, owing to structurally higher regasification utilisation in Europe and the

proliferation of LNG bunkering.

China will undoubtedly remain the most critical driver of LNG demand, and other Asian

countries like Thailand, Pakistan, Vietnam and Bangladesh are expected to contribute in a big

way as well, backed by an upswing in gas-to-power projects and depleting indigenous gas

production. India’s role in the LNG growth story, while important, will be impeded to an extent

by rising domestic gas supply, domestic infrastructure bottlenecks and intense competition

from coal in the power sector.

Global nominal regasification capacity forecast by geography

Source: IGU, DBS Bank

Global LNG demand forecast by geography

Source: IGU, DBS BankDBS Asian Insights

SECTOR BRIEFING 85

19

LNG project timeline and general trends

LNG import and export projects follow the same development phases, with the caveat that

export terminals are more costly on a ton-for-ton basis, due to the need for expensive massive

cooling and pressurisation equipment required for liquefaction. On an all-in basis, liquefaction

projects also necessitate greater capital expenditure as they are often larger in scale with a

relatively longer construction period. The sequence below describes the phases of an LNG

liquefaction/regasification project:

• Pre-Front End Engineering Design (Pre-FEED)

After a basic screening and evaluation process, a pre-FEED is performed to derive an initial

conceptual project design to prove its feasibility in technical and economic terms. This can

be a slow process for a greenfield project, but is likely much shorter for expansion, like the

addition of another train.

• Front End Engineering Design (FEED)

The FEED is used as the basis to better define the scope of the project to potential

EPC contract bidders, and to obtain a more comprehensive project cost estimate and

project schedule. Typically, the entire FEED (including pre-FEED) process takes around

18-24 months.

• Engineering, Procurement and Construction (EPC) bidding

Contractors receive the FEED package and submit bids based on their own internal

cost projections. If a bidder does not approve of the technical specifications in the FEED

package, they can propose changes and submit a bid and guarantees based on the

revised FEED package. This stage usually takes around 3-6 months.

• EPC Phase

The EPC phase begins after the project developers have made a final investment decision.

Depending on the scale and technical aspects of the project, construction usually takes

around 48-60 months for export terminals and 36-48 months for import terminals.

The LNG sector is According to Wood Mackenzie, less than 10% of global LNG liquefaction projects were

notorious for lengthy constructed under budget, and 60% experienced delays to completion. Cost overruns in

project delays and the previous boom averaged 33%, led by Australian projects which averaged 40%. On the

substantial cost regasification side, our study of 18 projects that were under construction as at Dec-16 exhibits

overruns a similar trend, with 70% of projects completing behind schedule with an average delay

period of 1.5 years.DBS Asian Insights

SECTOR BRIEFING 85

20

Timeline of an LNG project varies widely between 48-108 months

Source: DBS Bank

Greenfield and Brownfield liquefaction projects delayed by 10 months and 6

months respectively, on average

Source: Wood Mackenzie, DBS BankDBS Asian Insights

SECTOR BRIEFING 85

21

Regasification projects are equally susceptible to interruptions and delays as well

Country Terminal name Target completion Actual completion Length of delay

date date (months)

China Yuedong LNG (Jieyang) Dec-16 May-17 5

China Rudong Jiangsu LNG Dec-15 Nov-16 11

Phase 2

China Beihai, Guangxi LNG Dec-15 Mar-16 3

Greece Revithoussa Dec-16 Dec-18 24

Philippines Pagbilao import terminal Mar-16 Uncompleted 43

Poland Swinoujscie Jun-14 Jun-16 24

China Dalian Phase 2 Dec-16 Nov-16 Completed in time

France Dunkirk LNG Dec-15 Jan-17 13

China Tianjin (Sinopec) Phase 1 Sep-17 Apr-18 7

China Tianjin (onshore) Dec-16 Oct-18 22

India Mundra LNG Dec-16 Uncompleted 34

India Dahej LNG (Phase 3-A1) Dec-16 Sep-16 Completed in time

Thailand Map Ta Phut Phase 2 Jun-17 Jun-17 Completed in time

China Shenzhen (Diefu) Dec-15 Aug-18 32

China Fujian (Zhangzhou) Dec-17 Uncompleted 22

China Zhoushan Dec-16 Oct-18 22

Korea Boryeong Dec-16 Jan-17 1

Japan Soma LNG Dec-18 Mar-18 Completed in time

Source: IGU, DBS Bank

What is the expected capital investment required for LNG

import terminals in Asia?

According to IHS Markit, the weighted average unit cost of new onshore and offshore LNG

import capacity was US$274/mtpa and U$129/mtpa respectively in 2017 (based on a three-

year moving average). Onshore regasification unit costs have been trending up in recent years,

as project developers are adding more storage capacity per unit of send-out capacity to bolster

supply stability. On the other hand, offshore regasification unit costs remained steady as the

controlled environment in shipyard construction promotes cost stability.

Based on our earlier capacity projections, we estimate there will be around US$31bn of capital

investments in LNG receiving terminals in Asia (excluding Japan, Korea, and Taiwan) betweenDBS Asian Insights

SECTOR BRIEFING 85

22

2018-2025. China and India will account for the lion’s share at around US$10bn and US$7bn

respectively, while the remaining US$14bn is split between other Asian countries like Pakistan,

Bangladesh, Thailand and Vietnam.

Onshore vs offshore capex comparison

Onshore

Source: IGU, DBS Bank

What other trends do we expect in LNG receiving capacity

build-up throughout 2025?

We foresee three trends in the build-up of LNG receiving capacity playing out in the medium

to long term.

• Floating regasification terminals should continue on its current growth trajectory to make

up around 17% of global regasification capacity by 2025. The inevitable shift towards

FSRUs should more than offset cost inflation and drive the blended unit cost of new

import capacity down.

• The composition of both LNG buyers and LNG regasification terminal owners is set to

become more fragmented amid market liberalisation in key Asian markets to allow third

party access to LNG import terminals and the advent of new LNG buyers other than the

traditional buyers in Northeast Asia.

Terminal owners will install more on-site infrastructure to allow for more value-added services.

LNG import terminals are gradually transiting towards a hub model, where LNG is not only

regasified and distributed via the conventional distribution pipeline network, but also through

other mediums like bunkering and truck loading. Other services that import terminals will

increasingly offer include LNG reloading and transhipment, and cold energy integration,

where waste cold energy released from LNG regasification is exploited for power production

and district cooling.DBS Asian Insights

SECTOR BRIEFING 85

23

Global regasification nominal capacity composition (by owner)

Source: IGU, DBS Bank

Global regasification nominal capacity composition (by sector)

Source: IGU, DBS BankDBS Asian Insights

SECTOR BRIEFING 85

24

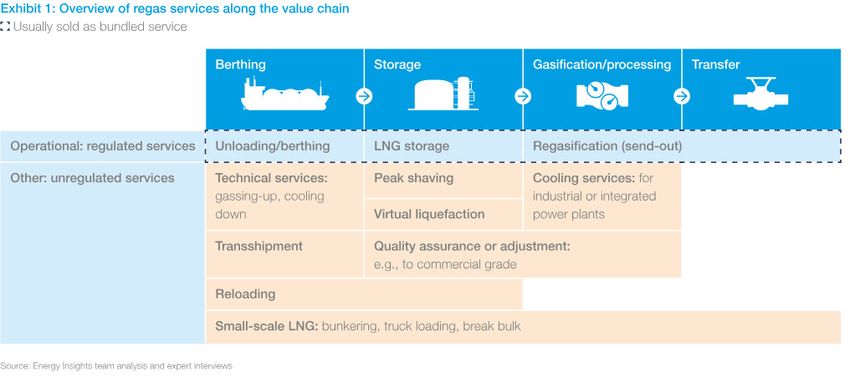

LNG import terminals are gradually shifting away from traditional business models and offering more value-

added services

Exhibit 1: Overview of regas services along the value chain

Usually sold as bundled service

Berthing Storage Gasification/processing Transfer

Operational: regulated services Unloading/berthing LNG storage Regasification (send-out)

Other: unregualted services Technical services: Peak shaving Cooling services:

gassing-up, cooling down for industrial or integrated

power plants

Virtual liquefaction

Transhipment Quality assurance or adjustment:

eg. , to commercial grade

Reloading

Small-scale LNG: bunkering, truck loading, break bulk

Source: McKinsey, DBS Bank

LNG supply and Liquefaction Forecasts

What is the present LNG supply situation?

The world is currently awash with LNG, following the tidal wave of liquefaction terminals

coming online from 2016. A grand net (additions less decommissioned) total of 85mtpa of

nominal liquefaction capacity entered the system in 2016-2018, underpinned by growth

in Australia (46.4mtpa), the United States (23.3mtpa) and Russia (11.0mtpa). The last time

the world witnessed such dramatic capacity growth was back in the period of 2008-2010,

when Qatar drastically expanded its nameplate liquefaction capacity to 69.2mtpa in 2010

from 30.2mtpa in 2008. To exacerbate the situation, several notable LNG export projects, like

Ichthys LNG in Australia and Yamal LNG in Russia are running ahead of schedule (faster than

expected project completion and capacity ramp-up), introducing more LNG supply while the

world struggles to digest the current supply.DBS Asian Insights

SECTOR BRIEFING 85

25

Historical nominal liquefaction capacity by geography

Source: IGU, DBS Bank

Global nominal liquefaction capacity composition (by owner)

Source: IGU, DBS Bank

When will the supply glut come to an end?

The oversupply situation will likely only end in 2022-2023, due to the culmination of

macroeconomic uncertainty putting a dampener on demand growth and another substantial

wave of LNG liquefaction terminals turning online in 2019 and 2020. Protracted trade tensions

between the two largest nations in the world, coupled with a broader macroeconomic

slowdown will likely translate into slower gas demand growth in the short run. Meanwhile onDBS Asian Insights

SECTOR BRIEFING 85

26

the supply front, a staggering 123mtpa (32% of global liquefaction capacity as at end-2018)

of liquefaction capacity will be added between 2018-2025, assuming that projects under

construction are completed according to schedule and no new projects are sanctioned during

the period. Yet, bulk of the new terminals (71mtpa) will be coming onstream in 2019 to 2020,

meaning the spurt in supply will likely exceed the increase in demand over the next two years

by a wide margin.

Projects under construction as at Dec-18

Source: IGU, DBS Bank

Global nominal liquefaction capacity composition (by sector)

Source: IGU, DBS BankDBS Asian Insights

SECTOR BRIEFING 85

27

Are LNG suppliers likely to throttle export utilisation to

manage excess supply?

Due to the high degree of fixed costs involved in liquefaction, LNG exporters will continue

sending out excess cargoes (supply that is not backed by long term contracts) or spot cargoes

as long as the spot price received covers all variable operating costs or the marginal cost of

production. The discussion here will be centred on US LNG, given that incremental global

LNG deliveries over the next two years will be largely driven by US LNG - US LNG liquefaction

capacity is projected to skyrocket to 71mtpa in 2020, from 23mtpa in 2018, and account for

c.65% of global liquefaction capacity additions during the period.

After months of surplus LNG in the market, spot LNG prices are fast approaching the short

run marginal cost (SRMC) of US LNG in both Asia and Europe after a brief dip below this level

during certain months. However, the temporary slide in spot prices below US SRMC has not

triggered a response from the US LNG plant owners, despite them incurring operating losses

from unrestrained exports. We believe that it will take either:

a. A sustained decline in European and Asian spot LNG prices to below their respective US

SRMC level beyond the start of winter this year, or

b. A decline in spot prices to below US SRMC less variable transportation costs (majority of

LNG carriers are on long term charters and have to be paid) before we see a negative

adjustment in US LNG deliveries

Of course, there are other factors in play - project owners will react differently depending

on their hedging strategy, cost competitiveness of their projects (projects that can secure

relatively cheaper feed gas will have a strong edge) and the extent of integration through the

LNG value chain (able to market spot cargoes across various markets with greater ease). On

the macro front, easing trade tensions between China and the US would stimulate demand

for more spot cargoes, especially if China removes the 25% tariff imposed on US LNG.DBS Asian Insights

SECTOR BRIEFING 85

28

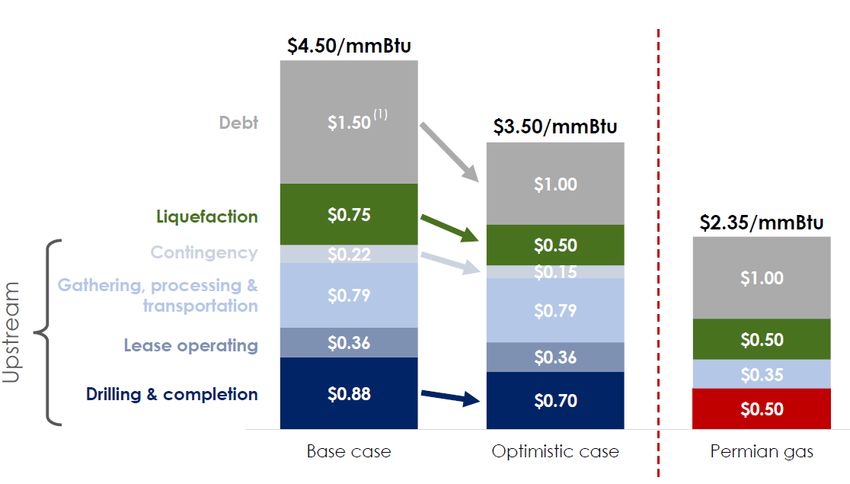

Tellurian can potentially deliver LNG FOB at US$1.35/mmbtu (excluding financing) by

tapping on cheap Permian gas

$4.50/mmBtu

Debt $1.50(1) $3.50/mmBtu

$1.00

Liquefaction $0.75 $2.35/mmBtu

$0.50

Contingency $0.22

$0.15 $1.00

Gathering, processing &

transportation $0.79

Upstream

$0.79

Lease operating $0.50

$0.36

$0.36

$0.35

Drilling & completion $0.88 $0.70

$0.50

Base case Opimistic case Permian gas

Source: Tellurian, DBS Bank

US exports will continue unabated as long as producers can cover variable costs

Source: Bloomberg Finance L.P., DBS BankDBS Asian Insights

SECTOR BRIEFING 85

29

Global nominal LNG liquefaction capacity and LNG supply

forecasts

We anticipate global nameplate LNG liquefaction capacity and global LNG exports to reach

around 588mtpa and 485m tons in 2025 respectively. More projects are expected to take final

investment decisions (FID) between now and 2021, and complete construction by the end of

our forecast horizon in 2025. This translates into an additional 100mtpa of capacity on top of

the 110mtpa of capacity currently under construction (as at end-2018).

Within the seven-year period between 2018 and 2025, most of the capacity growth will

primarily be driven by the oil supermajors and national oil companies (NOCs), owing to their

keen ability to adapt to rapidly evolving industry dynamics. On a country level, those having

favourable long run marginal cost LNG profiles like Qatar, Russia, and the United States will

lead the charge. Newcomers like Mozambique and Canada are also expected to make a big

splash towards the end of our forecast period (2024/25)IGU and become solid contenders in

the LNG market.

What are the key risks There are several factors that could delay or even constrain the development of global

to our projections? LNG export capacity. First and foremost, prolonged weakness in spot LNG prices below

the long run marginal cost (LRMC) of LNG projects, could prompt project owners to re-

evaluate their plans.

Most notably, proposed projects that we expect to come onstream during our forecast period

might fail to reach the FID stage, while projects under construction may not come online

in a timely manner for a number of reasons, including: i) inability to secure sufficient long

term offtake agreements with creditworthy counterparties could stifle access to financing,

ii) the sheer complexity of designing, building and commissioning LNG terminals (though

we have included a time buffer for each project as the LNG sector is notorious for extended

project delays), especially for greenfield projects and iii) other development risks like extensive

regulatory requirements.DBS Asian Insights

SECTOR BRIEFING 85

30

Global nominal liquefaction capacity forecast by geography

Source: IGU, DBS Bank

Global LNG supply forecasts by geography

Source: IGU, DBS BankDBS Asian Insights

SECTOR BRIEFING 85

31

Key LNG Asset Classes

LNG Liquefaction Terminals

FLNGs, or floating liquefied natural gas facilities, are offshore facilities used for natural gas

operations. Using subsea equipment, they extract natural gases from subsea gas fields before

liquefying, storing, and offloading them to LNG carriers. FLNGs are mainly used when it is not

feasible to install undersea pipelines to connect the gas fields to onshore terminals.

Benefits of FLNG facilities

First, they do not require platform jackets and minimise pipeline installations. FLNGs are also

frequently adopted when:

1. The ground surrounding the project field is insufficiently solid

2. The project is located in deep water fields or far away from land

In addition, given that FLNGs are built in shipyards before being deployed at project sites,

managing their construction process is easier compared to large-scale on-site facilities, which

is typically the case for land-based gas field projects. Moreover, given that FLNGs are floating

facilities, they can be moved or redeployed at other fields.

As it has not been long since FLNGs were first introduced, there are currently only three

shipbuilders in the world that boast FLNG construction track records - Samsung Heavy

Industries (SHI; three facilities), Daewoo Shipbuilding Marine Engineering (DSME; one facility),

and Keppel Corporation (two facilities).

Regasification projects are equally susceptible to interruptions and delays as well

Project name Operator Installation area Targeted Annual output Remarks

operation (mn tons)

Kribi FLNG Golar LNG Cameroon 2018 2.4 Remodeled existing LNGC

(Keppel Corporation)

PFLNG Satu Petronas Malaysia 2018 1.2 Built new ship (DSME)

Prelude FLNG Shell Australia 2018 3.6 Built new ship (SHI)

Rotan FLNG Petronas Malaysia 2020 1.5 To build new ship (SHI)

Coral South FLNG Eni Mozambique 2020 3.4 To build new ship (SHI)

Gimi FLNG Golar LNG Mauritania / 2022 2.5 To remodel existing LNGC

Senegal (Keppel Corporation)

Source: NH I&S Research CenterDBS Asian Insights

SECTOR BRIEFING 85

32

Expanding natural gas Amid rising natural gas consumption, we expect to see more natural gas exploration-related

consumption driving offshore development projects. According to International Energy Agency (IEA) statistics,

up deep sea gas field only 13% of the remaining crude oil reserves are located underwater. However, out of the

projects remaining natural gas reserves, 36% are underwater. Furthermore, out of remaining natural

gas reserves on land, 71% are trapped within shale formations. Accordingly, without offshore

gas field operations or shale gas projects, developers will likely secure only a limited amount

of natural gas.

Global crude oil reserves Crude oil reserve breakdown

Discovered Drilled Remaining Portion of

(bbl) (bbl) (bbl) remaining

reserves

Total 7,537 1,390 6147 81.6%

Onshore 2,247 885 1,362 60.6%

Nearshore 795 299 496 62.4%

Deep sea 302 28 274 90.7%

Shale 4,193 178 4,015 95.8%

formations/

others Note: bbl = billion barrels

Source: IGU, NH I&S Research Center

Global natural gas reserves Natural gas reserve breakdown

Discovered Drilled Remaining Portion of

(tcm) (tcm) (tcm) remaining

reserves

Total 920 122 798 86.7%

Onshore 234 86 148 63.2%

Nearshore 179 22 157 87.7%

Deep sea 132 4 128 97.0%

Shale 375 10 365 97.3%

formations/

others

Note: tcm = trillion cubic metres

Source: IGU, NH I&S Research CenterDBS Asian Insights

SECTOR BRIEFING 85

33

Natural gas production to be led mainly by shale gas developers, but the FLNG market is

also set to expand. While more offshore gas field projects using FLNGs are coming into the

limelight, they still lag shale gas projects in terms of natural gas production volume. We note

that around two-thirds of newly operating natural gas production/liquefaction facilities are in

North America. Also, about 46% of global natural gas reserves are held in shale formations,

which are mainly found in North America. According to Energy Information Administration

(EIA) statistics, US shale gas production climbed 18.8% y-o-y in 1H19, accounting for 61.1%

of US natural gas production.

17% of planned LNG development projects predicted to use FLNGs. While natural gas

production will likely continue to be spearheaded by shale gas developers, we believe the

FLNG market will also expand, given that: 1) 67% of natural gas reserves (excluding those

within shale formations) are located underwater; and 2) 45% of underwater reserves are held

in deep sea areas (where explorations are not feasible without FLNGs). In fact, 17% of new

LNG development projects are planning to employ FLNGs.

US natural gas production volume Global natural gas production volume

Source: EIA, BP Statistics, Clarkson, NH I&S Research Center

Proportion of projects planning to use FLNGs Expected FLNG installation breakdown by region

Source: IGU, NH I&S Research CenterDBS Asian Insights

SECTOR BRIEFING 85

34

We believe additional FLNG orders are likely to be placed. There are currently at least 25

projects in the proposed phase that are expected to adopt FLNGs. Given that the inaugural

FLNGs have been in operations since 2018, development/operational costs for gas field

projects using FLNGs are being evaluated and analysed. If these projects using FLNGs prove to

be cost efficient, FLNG adoption is likely to increase.

Planned FLNG orders Average project costs, by project type

Source: IGU, NH I&S Research Center

Projects planning to adopt FLNG

Project name Operator Installation area Targeted year Annual output

(mn tons/year)

Stewart Energy Stewart Energy Group Canada 2019 5.0

Kitsault Kitsault Energy Canada 2019 8.0

Orca Orca LNG Canada 2019 4.0

Cedar Haisla First Nation Canada 2020 6.4

Cambridge Energy Cambridge Energy US 2020 7.5

Delfin Fairwood LNG US 2020 12.0

Main Pass Energy Hub Freeport-McMoran Energy US 2020 24.0

Djibouti Poly-GCL Djibouti 2020 3.0

Fortuna Golar Equatorial Guinea 2020 3.0

Congn-Brazzaville New Age Democratic Republic of the Congo 2020 1.2

Scarborough ExxonMobil Australia 2021 6.5

Barca Barca LNG US 2021 12.0

Eos Eos LNG US 2021 12.0

Gorskaya Unannounced Russia 2021 1.3

Point Comfort Lloyds Energy Group US 2022 9.0

Avocet Fairwood LNG US Unannounced 3.3

Malahat Steelhead Group Canada Unannounced 6.0

Bonaparte ENGIE Australia Unannounced 2.0

Browse Woodside Australia Unannounced 4.5

Cash Maple PTTEP Australia Unannounced 2.0

Crux Shell Australia Unannounced 2.0

Poseidon ConocoPhillips Australia Unannounced 3.9

Sunrise Shell/Woodside Australia Unannounced 4.0

East Dara Black Platinum Energy Indonesia Unannounced 0.8

Pandora Cott Oil & Gas Papua New Guinea Unannounced 1.0

Source: IGU, NH I&S Research CenterDBS Asian Insights

SECTOR BRIEFING 85

35

LNG Receiving Assets

Like gas liquefaction, there are both onshore and floating solutions to regasify LNG, but the

key difference is that floating regasification technology is not only more established, but more

straightforward and better understood by market participants as well.

The LNG regasification process is generally similar across both land and offshore

configurations - LNG is firstly unloaded from LNG carriers into cryogenic storage tanks,

then pumped into a vaporiser unit where it is vaporised by heat exchange using seawater,

and finally metered and delivered to the gas distribution network. However, a land-based

concept could contain additional functions like LNG bunkering and reloading services and

typically has larger storage capacity.

Today, while land importing terminals still make up the lion’s share of global regasification

capacity, we are seeing good momentum in floating regasification units, primarily in emerging

markets like Pakistan, Turkey, and Bangladesh in recent years. This has propelled its market

share to around 12% in 2018, up substantially from 5% in 2010.

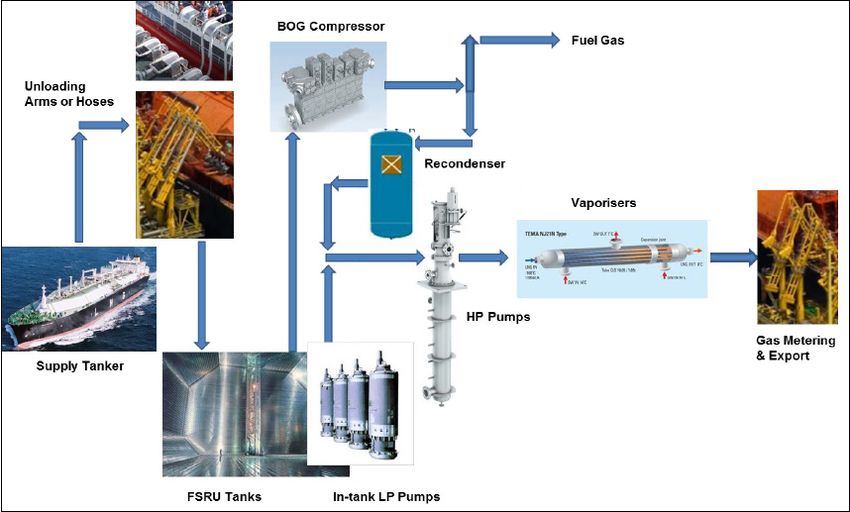

Typical FSRU flow scheme

BOG Compressor

Fuel gas

Unloading

Arms or Hoses

Recondenser

Vaporisers

HP Pumps

Gas Metering

& Export

Supply Tanker

FSRU Tanks In-tank LP Pumps

Source: The Oxford Institute for Energy Studies, DBS BankDBS Asian Insights

SECTOR BRIEFING 85

36

Comparison between land terminals and FSRUs

Land-based terminals FSRUs

Greater storage and regasification capacity – Crucial when Shorter project lead times – FSRUs are typically constructed

storage and send-out capacities are of strategic importance within 24-36 months, while conversion usually takes

to the market, or when the terminal is used to serve a around 12-18 months. With redeployment, the world’s

large market. fastest FSRU project was implemented in a span of 5

months from project inception to first gas.

Lower operating costs – More economical in the long-run, Significantly lower capital investment – FSRUs can be

despite a substantial initial capital outlay. Land-based completed at a significantly lower cost (30-50% less) than

terminals tend to be more economically viable for projects land-based alternatives. Additionally, vessels can be leased

lasting beyond 12-15 years. and redeployed or even function as an LNG carrier.

High local content value – Job creation via operation of Less regulatory constraints – Offshore permits for FSRUs

the regasification terminal can be a compelling reason for are easier to obtain, as it does not require a massive land

governments to support the project area unlike its onshore counterparts

Ease of expansion – To meet rising gas demand, subject to Shipyard construction – Enables better project

land availability management and cost control, given that construction is

performed in a controlled environment

Less susceptible to supply disruptions – Less affected by

inclement weather, and large storage capacity ensures

stable supply

Source: DBS Bank

Historical onshore and floating regasification capacity Historical and expected FSRU delivery schedule

Source: IGU, Clarksons, DBS Bank

Breakdown of new LNG importing countries (2010-2018) – Shaded names represent those with FSRUs

2010 2011 2012 2013 2014 2015 2016 2017 2018

UAE Thailand Indonesia Malaysia Lithuania Pakistan Poland Malta Bangladesh

Netherlands Singapore Jordan Jamaica Panama

Israel Egypt Colombia

Source: IGU, DBS BankDBS Asian Insights

SECTOR BRIEFING 85

37

Global FSRU owner (left) and builder market share (right) as at Sep-2019 by count

Source: Clarksons, DBS Bank

Why are FSRUs preferred in new emerging markets?

The impetus for choosing floating over land alternatives is multi-fold, but financing constraints

tend to be the most critical factor in developing countries. The immediate capital outlay for

a mid-scale (c.3mtpa) land terminal and other onshore infrastructure usually falls in the

range of US$600-750m, a substantial amount that necessitates foreign capital for project

financing. However, financing tends to be costly for emerging markets with elevated country

and default risks. Electing to use FSRUs can help developing countries circumvent financing

challenges, since FSRU projects require 30-50% less outlay than a land terminal with similar

specifications. Furthermore, chartering a FSRU, rather than an outright purchase, can reduce

investment costs even further, and also mitigate potential cash flow mismatches, as the timing

of revenue inflows will be more consistent with operating costs (which forms the majority of

cash outflows).

Economic analysis of regasification concepts

Project feasibility aside (factors like minimum required send-out or storage capacity/land

availability/regulatory constraints), the economic viability of the project is the most crucial factor

in the selection process. On this basis, we anticipate FSRUs to continue to be the preferred

option by markets seeking quick and short-term access to natural gas. This is substantiated

by our project finance analysis which suggests that FSRUs are more cost-efficient for projects

(assuming similar send-out and storage capacities) not exceeding 12 to 15 years, a moderately

higher duration than IGU’s estimated breakeven period of 8 to 10 years, which was based on

a simplistic undiscounted payback period analysis that assumes all capex would be incurred in

year 0 and excludes all financing costs.DBS Asian Insights

SECTOR BRIEFING 85

38

Total cost comparison between land-based and floating terminals

Summit LNG FSRU cost component breakdown (figures in US$m)

Source: Excelerate Energy, DBS BankDBS Asian Insights

SECTOR BRIEFING 85

39

Outlook for FSRUs

As at June-2019, there was 28.4mtpa of offshore capacity in the construction phase, while

proposed FSRU projects that have yet to reach the FEED stage totalled about 132mtpa. Despite

a pause in FSRU newbuild contracts in 2019 thus far, we maintain a sanguine outlook on the

development of FSRUs globally, and expect floating terminals to account for around 17% of

total regasification capacity by 2025, from 11% in 2018. Future FSRU capacity could surpass

our estimates as unsanctioned projects may start up during our forecast period due to the

relatively short construction timeframe of FSRUs.

Source: IGU, DBS Bank

LNG Carriers

Demand for LNGCs to pick up in line with greater LNG use. Bullish LNG market conditions

bode well for related shipping players and builders.

European ship

owners typically take Owning 45% of the overall global LNGC fleet, European shipping companies currently take

conservative stance up 60% of global LNGC orders. As these companies are mostly owned by individuals or

on technologies and families, they tend to take a conservative stance towards technologies and markets, and

markets hence there is typically less impact from optimism that continues to haunt other commercial

shipping markets.

While spot contracts are increasing, long-term contracts still represent the lion’s share of

the LNG shipping market. Long-term contracts suit the tastes of the conservative shipping

companies, reducing the possibility of excessive LNGC order placement.DBS Asian Insights

SECTOR BRIEFING 85

40

LNGC with membrane-based containment system LNG fleet by shipping company (existing + on order)

Source: Clarkson Research, NH I&S Research Center

Breakdown of LNGC owners by nationality LNG shipping contracts by long term vs spot/ short term

Source: Clarkson Research, NH I&S Research CenterDBS Asian Insights

SECTOR BRIEFING 85

41

Global marine LNG trade volume is set to expand at a CAGR of 9.5% over 2018 to 2019.

Amid rising LNG Owing to the US-China trade dispute, LNG trade volume between the two countries over

shipping demand, ship 2018c. 2019 is likely to tumble by 66% compared to before the dispute broke out. Despite

supply appears to be this, global LNG trade volume remains on the rise, suggesting that issues such as the US-China

still insufficient trade dispute will not affect the changing global energy mix trend.

While LNGC orders upped over 2017c. 1H19, the rise was not excessive in light of the outlook

for trade volume growth. Most of the recent LNGC orders are expected to be delivered by

2022. Over 2018c. 2022, LNG shipping capacity is predicted to climb 31.4%, on par with the

projected LNG export growth of 28.4% over the same period.

We note that there are only a few orders for LNGCs scheduled to be delivered after 2022.

Based on the average construction time for LNGCs, we believe LNGC orders between 2019-

2022 will likely expand by 33.7% (shipping capacity basis) compared to the 2018-2019

average to meet demand in 2023-2025. Such an increase in newbuilding orders will benefit

the shipbuilding market.

Global LNGC supply-demand dynamics

2017 2018 2019E 2020F 2021F 2022F 2023F 2024F 2025F

Export volume (mt) 288 317 358 387 402 409 421 443 485

New demand (mt) 25.2 28.2 41.9 28.6 14.9 7.1 11.8 22.2 41.9

Shipping demand growth 9.1 9.8 13.2 8.0 3.9 1.8 2.9 5.3 9.5

(%) - A

Global fleet at beginning of 64.3 69.2 73.7 82.0 88.5 96.9 98.2 97.8 97.2

year (mn m3)

Newbuilding (mn m3) 5.2 5.0 8.8 7.0 9.0 1.9 0.2 0 0

Demolition (mn m3) -0.3 -0.5 -0.5 -0.5 -0.6 -0.6 -0.6 -0.6 -0.7

Global fleet at yearend (mn 69.2 73.7 82.0 88.5 96.9 98.2 97.8 97.2 96.5

m3)

Shipping capacity growth 7.6 6.5 11.3 7.9 9.5 1.3 -0.4 -0.6 -0.7

(%) – B

Supply-demand balance (%) 1.5 3.3 1.9 0.1 -5.6 0.5 3.3 5.9 10.2

- (A-B)

Source: Clarkson Research, NH I&S Research CenterDBS Asian Insights

SECTOR BRIEFING 85

42

Global LNG export volume Global LNGC supply forecasts (based on order backlog)

Source: Clarkson Research, NH I&S Research Center

US LNG export volume US LNG exports to China

Source: Cheniere Energy, NH I&S Research Center

Surge in US LNG Since the US began exporting LNG, approximately 1.8 ships have been needed for each

cargoes to propel 1mtpa of supply, which is considerably greater than the global average shipping multiplier

demand for LNGCs of 1.3x. According to S&P Platts, the average distance covered by a laden LNG ship from

the US stood at 9,268nm in 2018, compared to 3,936nm and 5,602nm for Australia and

Qatar respectively, highlighting the vast distance between the US and central demand points.

Hence, we expect the global average shipping multiplier to continue trending up as the US

powers ahead in supply, which should further propel the demand outlook on LNGCs.DBS Asian Insights

SECTOR BRIEFING 85

43

Shipping route changes Demand for LNGCs is expected to pick up, and the market penetration of super-sized LNGCs

to spark demand for is set to strengthen. At present, LNG shipping players mainly use shipping routes passing

super-sized LNGCs through the Panama Canal and Suez Canal. Thus, the global LNGC fleet is now mainly

composed of 160c. 174kCBM Panamax vessels that are able to pass through the canals.

However, expected changes in shipping routes should lead to greater demand for super-sized

LNGCs (larger than Panamax ships).

Once more natural gas pipelines in the US are developed, LNG will be able to be exported from

ports in the US West Coast, a development which would lower the need for LNG carriers to

pass through the Panama Canal. Australia-Asia trade routes will also likely generate demand

for bigger LNGCs.

No. of LNGCs required for each mtpa of US LNG has been increasing amid growing exports to Asia

Source: Gaslog Ltd, NH I&S Research Center

Rising LNGC orders With the anticipated rise in global LNGC orders highlighting the importance of LNG carriers’

will also spur demand containment systems, the holders of proprietary technologies in the area of LNG storage

for LNG containment systems are drawing strong market attention. Given the high entry barrier to the LNG

systems containment system market, players equipped with accumulated technological knowhow

and boasting solid track records are to enjoy the benefits of the reviving global LNGC market

for the long haul.DBS Asian Insights

SECTOR BRIEFING 85

44

LNG containment system technology comparison

GTT (France) Moss (Norway) SPB (Japan) KC-1 (Korea)

Technology Membrane1 Spherical tank Tank Membrane

Construction costs Requires less steel Higher costs (versus Higher costs (versus Similar to GTT

and aluminum than GTT) GTT)

tanks for a given

LNG capacity

Operating costs More efficient use Australia 2018 3.6

of space

LNGCs 453 130 4 2

Other factors Value added services High center of Huge losses and Little experience at

gravity; harder to delays on vessels sea

navigate in order book;

no significant

experience

Note 1: Membrane: In the shipbuilding sector, ‘membrane’ refers to a design technology that installs insulation between the tank and the hull

Note 2: BOR stands for boil off rate, the amount of liquid that is evaporating from a cargo due to heat leakage and is expressed in % of total liquid volume per unit time; the

lower the BOR, the greater the superiority of the containment system

Source: GTT, NH I&S Research CenterDBS Asian Insights

SECTOR BRIEFING 85

45

Beneficiary of Booming

Demand for Gas Solutions

Korean shipyards set to The Korean shipbuilding industry will be a primary beneficiary of the anticipated increase in

be prime beneficiary global LNG carrier demand. In 2018, Korean shipbuilders bagged more than 90% of global

LNGC orders, and in 1H19, their share in the global LNGC market reached roughly 80%. We

note that:

1. Almost all 1H19 LNGC orders (excluding those from China and Japan) were awarded to

Korean shipbuilders

2. New large-scale LNGC orders are all expected to come from countries other than China

and Japan

Korean yards have been dominating the LNG carrier market, which is widely recognised for

its high technical barriers owing to characteristics of highly flammable LNG that needs to be

stored at super low temperatures at below -160°C with low specific gravity (0.43 to 0.50).

Korean-built LNG carriers (>40k cbm) account for c. 71% of the existing global fleet and their

dominance has continued to climb over the past 10 years. Korean yards’ market share has

expanded to 83% based on deliveries in 2015-2019 and further increases to a whopping c.

90% based on the current orderbook for LNG carriers.

On the other hand, Japanese yards’ market share of the LNG carrier newbuild market has

plunged from c. 20% based on the existing LNG carrier fleet to a mere c. 2% by current

orderbook. In general, Japanese yards have been losing cost competitiveness in shipbuilding

as the nation struggles with an aging population and labour shortages, particularly for the

shipbuilding industry, leading to yard closures and shrinking capacity. Japanese yards are

now partnering with Chinese yards to lower cost. In view of the intensifying competition,

Japanese shipyards are focusing on higher added-value tonnage and technological R&D as

well as shifting production to China through JVs with Chinese shipyards to streamline cost.

Leading Chinese and A handful of established Chinese yards are also emerging in the LNG carrier shipbuilding

Singapore shipyards set market. Initially, they were beneficiaries of LNG carriers ordered by Chinese shipping company

to enjoy some spillover - China LNG Shipping International (CLNG) but have since then diversified their customer base

effects to include other global LNG fleet owners.

Qatar Petroleum may consider giving some orders to non-Korean yards for its newbuild LNG

carrier campaign. In April 2019, Qatar Petroleum, the world’s largest LNG producer, had issuedYou can also read