National Bank of Kuwait - Investor Presentation July 2021 - NBK

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

National Bank of Kuwait

Investor Presentation

July 2021

National Bank of Kuwait 1

Disclaimer

THE INFORMATION SET OUT IN THIS PRESENTATION AND PROVIDED IN THE DISCUSSION SUBSEQUENT THERETO DOES NOT

CONSTITUTE AN OFFER OR SOLICITATION OF AN OFFER TO BUY OR SELL SECURITIES. IT IS SOLELY FOR USE AT AN INVESTOR

PRESENTATION AND IS PROVIDED AS INFORMATION ONLY. THIS PRESENTATION DOES NOT CONTAIN ALL OF THE INFORMATION

THAT IS MATERIAL TO AN INVESTOR. This presentation has been prepared by (and is the sole responsibility of) National Bank of Kuwait

S.A.K.P. (the “Bank”).

The information herein may be amended and supplemented and may not as such be relied upon for the purposes of entering into any transaction. This

presentation may not be reproduced (in whole or in part), distributed or transmitted to any other person without the Bank's prior written consent.

The information in this presentation and the views reflected therein are those of the Bank and are subject to change without notice. All projections,

valuations and statistical analyses are provided to assist the recipient in the evaluation of the matters described herein. They may be based on

subjective assessments and assumptions and may use one among alternative methodologies that produce different results and, to the extent that they

are based on historical information, they should not be relied upon as an accurate prediction of future performance. These materials are not intended to

provide the basis for any recommendation that any investor should subscribe for or purchase any securities.

This presentation does not disclose all the risks and other significant issues related to an investment in any securities/transaction.

Past performance is not indicative of future results. National Bank of Kuwait is under no obligation to update or keep current the information contained

herein. No person shall have any right of action against the Bank or any other person in relation to the accuracy or completeness of the information

contained in this presentation. No person is authorised to give any information or to make any representation not contained in and not consistent with

this presentation, and, if given or made, such information or representation must not be relied upon as having been authorised by or on behalf of the

Bank.

This presentation does not constitute an offer or an agreement, or a solicitation of an offer or an agreement, to enter into any transaction (including for

the provision of any services). No assurance is given that any such transaction can or will be arranged or agreed.

Certain statements in this presentation may constitute forward-looking statements. These statements reflect the Bank’s expectations and are subject to

risks and uncertainties that may cause actual results to differ materially and may adversely affect the outcome and financial effects of the plans

described herein. You are cautioned not to rely on such forward-looking statements. The Bank does not assume any obligation to update its view of

such risks and uncertainties or to publicly announce the result of any revisions to the forward-looking statements made herein.

National Bank of Kuwait 2Contents

Section 1 Overview of NBK

Section 2 Strategy and Business Overview

Section 3 Operating Environment

Section 4 Financial Performance Highlights

Section 5 Appendix

National Bank of Kuwait 3NBK is Kuwait’s Leading Banking Group

Snapshot Financial snapshot

Established in1952 as the first local and home-grown GCC bank, and first USD million 2018 2019 2020

shareholding company in Kuwait

The leading banking group in Kuwait in terms of assets, customer deposits and

customer loans and advances Total Assets 90,447 96,524 97,996

Background

More than 30% market share of assets in Kuwait

Ranked amongst the 50 safest banks in the world by Global Finance, named the Loans, advances & Islamic financing 51,124 54,584 57,722

most valuable banking brand in Kuwait, and top 10 bank in the region by Brand

Finance

Customer Deposits 47,449 52,533 56,403

Established by a group of leading Kuwaiti merchants, NBK has retained the same Total Equity 12,205 14,045 13,656

core shareholder base since its inception

NBK’s shares are listed on the Kuwait Stock Exchange since 1984 with only one

Ownership Net Operating Income 2,913 2,953 2,778

shareholder holding owning more than 5% of the Bank’s share capital (PIFSS owns

5.60% as of December 2020)

NBK’s market capitalisation at 31 December 2020 was USD 19.0 bn. Net Profit attributable 1,222 1,323 812

Cost to Income (%) 31.3% 34.0% 37.0%

The Bank’s core businesses are (i) consumer and private banking, (ii) corporate

banking, (iii) Islamic banking and (iv) investment banking and asset management

Operations Net Interest Margin (%) 2.69% 2.56% 2.21%

The Bank operates across 14 countries with a predominant focus on the MENA

region.

NPL Ratio (%) 1.38% 1.10% 1.72%

Credit Ratings

Loan Loss Coverage Ratio (%) 228% 272% 220%

Rating Agency Long Term Rating Standalone Rating Outlook

Return on Average Equity (%) 12.0% 12.3% 7.0%

A1 a3 Stable

Tier 1 Ratio (%) 15.3% 15.9% 16.0%

A a- Stable

AA- a- Negative Capital Adequacy Ratio (%) 17.2% 17.8% 18.4%

Notes: Through out the investor presentation, the USD/KD exchange rate used is .30325 for year-end figures and .30105 for interim figures. The rates are based on the Central Bank of Kuwait’s closing exchange rates National Bank of Kuwait 4

as of 31/12/2020 and 30/06/2021.Regional and International Geographic Presence

Middle East

Europe Location - Year established/acquired Legal Structure - Branches

Location - Year established/acquired Legal Structure – Branches Kuwait – 1952 Parent – 68

London – 1983 Subsidiary – 2 Egypt – 2007 Subsidiary – 52

Geneva – 1984 Subsidiary – 1 Iraq – 2005 Subsidiary – 5

Paris – 1987 Subsidiary – 1 Lebanon – 1996 Subsidiary – 2

Jordan – 2004 Branch – 1

Bahrain – 1987 Branch – 2

UAE – 2008 Branch – 2

Saudi Arabia - 2006 Branch – 3

US

Location - Year established/acquired Legal Structure – Branches

New York – 1984 Branch – 1

Asia

Location - Year established/acquired Legal Structure - Branches

Shanghai – 2005 Branch – 1

Singapore - 1984 Branch – 1

National Bank of Kuwait 5Key Strengths

High credit ratings and among the Largest banking group in Kuwait with

top brand values regionally dominant market position

As at 31 December 2020, the Bank was the largest bank in

NBK has one of the highest credit ratings in the MENA region Kuwait in terms of total assets, loans and customer deposits. In

Ranked amongst the 50 safest banks in the world by Global addition, the Bank enjoys a dominant market share across its

Finance, named most valuable banking brand in Kuwait and business segments

among the top 10 in the Middle East by Brand Finance NBK also has one of the largest and most diversified distribution

networks

Sound and consistent Only banking group in Kuwait to provide

financial performance both conventional and Islamic banking

Following its consolidation of Boubyan Bank in 2012, NBK

Long history of profitability, even throughout the global financial became the only banking group in Kuwait to offer both

crisis conventional and Islamic banking services

Excellent asset quality with an NPL ratio standing at 1.72% at This has allowed the Bank to leverage off the opportunities across

end-2020 both markets, particularly given the growing importance of Islamic

Strong liquidity serving as a buffer in times of need Finance in Kuwait

Stable shareholder base and A strong regional and

strong management team international network

Established in 1952 by a group of leading Kuwaiti merchants and Operations in 14 countries, 8 of which are in the MENA region.

has retained the same core shareholder base since The Bank continues to explore opportunities to expand

NBK’s stable shareholder base is complemented by a strong and geographically with a primary focus on further strengthening

stable Board of Directors and a long-serving executive team with operations in MENA region

in-depth experience

Strong investment banking capability

NBK conducts its investment banking and asset management

business through its subsidiary, Watani Investment Company

K.S.C.C. (Known as NBK Capital)

National Bank of Kuwait 6Contents

Section 1 Overview of NBK

Section 2 Strategy and Business Overview

Section 3 Operating Environment

Section 4 Financial Performance Highlights

Section 5 Appendix

National Bank of Kuwait 7NBK’s Strategy

The Group’s strategy, which is based on two main pillars, focuses on defending and growing its leadership position in Kuwait whilst also

diversifying its business

The Bank aims to (i) remain the primary banker for the leading local companies whilst continuing to be active in the

Corporate mid-market sector;(ii) remain the bank of choice for foreign companies and continuing to serve at least 75% of those

Banking companies and (iii) maintain its current market share in trade finance (over 30%). To achieve the above, NBK will

Defend and Grow leverage off its different services, expand its coverage and broaden the range of products and services offered.

Digital Leadership Position

transformation in Kuwait NBK intends to expand its consumer customer base by focusing on profitable consumer segments (such as the

of the core Consumer affluent and mass affluent segments) and by attracting new clients such as the SMEs.

Maintain excellence and Through the above, the Bank aims to maintain its leadership position, maintain its focus on delivery of superior

market leadership position, Banking

customer service experience and achieve the lowest cost of funds among Kuwaiti conventional banks.

to expand market shares

and to maintain discipline in

managing both risks and Within the private banking sector, NBK aims to continue to provide a unique proposition to high net worth clients in

costs collaboration with its investment arm. NBK also aims to provide superior customer service through its highly

Private Banking experienced bankers. The Bank also aims to leverage off its existing brand and experience (particularly in

Switzerland) to provide access to leading funds and broaden its product portfolio.

The Bank’s geographic diversification strategy is to leverage its fundamental strengths and capabilities, including its

Expand Regional international reach and strong regional relationships, to build a regional platform and support growth in key markets.

Business NBK focuses on markets with long-term potential through a combination of high growth economies, sound

Presence

diversification Geographical, and demographic trends and opportunities aligned with the Bank’s competitive advantages.

leveraging product and service

digital diversification

The Bank’s strategy, in relation to its Islamic subsidiary, is to differentiate it from other domestic Islamic banks

disruption through a clear focus on high net worth and affluent clients and large and mid-market corporate customers.

Includes expanding Establish an

regional presence, Islamic Franchise

establishing an Islamic

banking franchise and

building a leading regional NBK looks to establish its business as a leading regional investment banking, asset management, brokerage and

Build Regional

investment bank. research operation and to leverage the Group’s strong regional position to cross sell these products across the

powerhouse in

Wealth MENA region.

Management

National Bank of Kuwait 8Kuwait Operations

NBK is a universal bank and the industry leader in all key business segments in Kuwait with an average market share of 30%

Overview and strategy

Corporate Banking Consumer Banking Private Banking

Remain the primary banker for most of the local blue-chip Maintain undisputed leadership in retail banking with Continue to provide a unique proposition to HNW clientele

companies, and an active player in the mid-market leading market share and the highest customer in collaboration with NBK Capital and the bank’s

Remain bank of choice among foreign corporations and penetration among conventional banks international network

continue serving 75% of them active in the Kuwaiti market Maintain focus on customer service Provide access to best of breed international funds

Maintain current market share in excess of 30% in trade Expand client base with focus on profitable consumer leveraging NBK Banque Privee’s wealth management

finance in Kuwait segments such as affluent and mass affluent, and aim to expertise

Offer differentiated services to large corporate clients attract new bankable clients such as SMEs Provide the best service with a dedicated team of over 30

leveraging other NBK units Achieve lowest cost of funds among Kuwaiti commercial well qualified and experienced private bankers

Increase market share in medium corporate segment banks Leverage NBK’s strong brand to acquire new clients and

through focused teams and relationship management Pioneer innovative multi-channel solutions including state retain onshore relationships

Focus on Government mega projects benefiting from of the art internet, mobile banking and call center Broaden the product portfolio to accommodate growing

NBK’s large capital base services needs

Maintain asset quality with emphasis on credit control and Focus on the evolution to segment of one by providing

risk management tailor-made propositions aiming at better cross-sell,

increased product penetration, proactive attrition

management utilizing the latest tools and technologies

NBK is a full-service bank that offers a broad suite of financial services and products

to clients, meeting their ever growing and evolving demands

National Bank of Kuwait 9International Operations

Established or

NBK’s international operations has been traditionally contributing up to circa 30% of the Group’s Branches Legal structure

acquired

bottom line with the Bank aspiring to increase this contribution.

The Bank generally aims to maintain a majority stake in its subsidiaries or at least maintain a decision International

making role.

NBK’s international presence is a differentiating factor for the Bank and an extension of the MENA London 1983 2 Subsidiary

franchise enabling better service and strengthening client relationships.

Specifically within the MENA region, the Bank is focused on growing its business in existing and new New York 1984 1 Branch

markets through attracting increased corporate and private customers.

Meanwhile, across the international locations, the Bank’s focus is on servicing its private and corporate Geneva 1984 1 Subsidiary

customers who are active internationally and growing its business with international companies that

are active in the MENA region. Singapore 1984 1 Branch

Within its international network, NBK is focused on managing risks and costs to improve efficiency and

achieve long-term cost savings and productivity gains. Paris 1987 1 Subsidiary

Shanghai 2005 1 Branch

Overview of Performance MENA region

Revenue Trends (USD mn) Balance Sheet Trends (USD mn) Bahrain 1987 2 Branch

Net Operating Income Net Profit Segment Assets Lebanon 1996 2 Subsidiary

36,601

728

690 680

Jordan 2004 1 Branch

Iraq 2005 5 Subsidiary

372 33,467

370

32,227 Saudi Arabia 2006 3 Branch

165

Egypt 2007 52 Subsidiary

2018 2019 2020 UAE 2008 2 Branch

2018 2019 2020

National Bank of Kuwait 10Boubyan Bank (59.9% owned subsidiary)

Market share of Total Assets(%) Highlights

Islamic banking has been gaining ground in the Kuwaiti market, representing

more than 40% of assets and deposits at year-end 2020.

7.6% After a series of gradual share acquisitions since 2009, NBK’s stake in Boubyan

6.5% bank reached 58.4% in 2012. Through Boubyan, NBK aims at diversifying its

5.5% 5.7%

5.1%

income stream, complementing its product offering as well as targeting a new

segment of clients.

The size and market share development of Boubyan relative to other Islamic

2016 2017 2018 2019 2020

banks leaves significant room for repositioning the bank and acquiring market

share.

Market share of Total Deposits (%) As the largest single shareholder, NBK is committed to the future growth and

transformation of Boubyan Bank and establishing a strong presence in the

growing Islamic banking segment.

Leading international consulting firms have assisted Boubyan in developing a

new strategy aiming to differentiate the bank from other players with a clear

focus on HNWI, affluent and mid/large companies.

The Bank’s transformation and strategy implementation is led by a highly

9.6%

7.9% 8.5% 8.9% proficient management team with extensive regional banking experience, with

7.4%

key positions filled by NBK veterans aligned with the NBK culture.

2016 2017 2018 2019 2020

Notes: Market share data based on the consolidated data of all banks operating in Kuwait. National Bank of Kuwait 11Maintaining Course with Our Sustainability Directions

NBK Sustainability Pillars

Respecting

Contributing Giving Back Caring for

Serving Leading in and

to Economic to Our Our

Customers Governance Developing

Development Community Environment

People

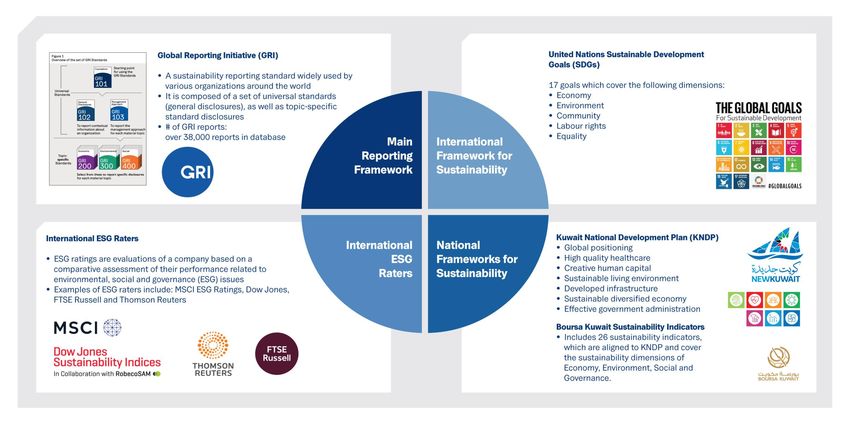

National Bank of Kuwait 12Close Alignment With International Frameworks and ESG Raters

National Bank of Kuwait 13NBK’s 2020 ESG Highlights

Environmental Social Governance

With leadership in business and

Caring for our environment is a Wellbeing of external and internal

governance among our sustainability

priority as we actively measure and stakeholders is of critical importance

priorities, NBK continues to strive to

assess the environmental impacts of as we remain committed to show our

integrate sustainable practices into

our business and operations. values to our people.

its corporate governance practices.

Completion of our new LEED Gold 45.8% Female employee Ratio Reformation of Board Risk Committee

Headquarters to Board Risk and Compliance

72.7% Kuwaitization

Committee

Inclusion in Refinitiv AFE Low Carbon 51.9 k Employee training hours

Select Index MENA

77% Local Procurement Appointment of two independent Board

840 Kgs Plastic collected and recycled of Directors (March 2021)

Supporting nationalization programs in

from branches

Kuwait including NBK Academy

Updated and published various policies

98 tons of paper recycled Provided training center facilities for 110 and statements including:

participants in LOYAC

Total GHG emissions of 5,152 MT

Human rights statement

CO2e Organized training courses for 141

candidates (Ministry of Justice)

Advertising Code policy

Sponsoring TAMKAN graduate training

scheme (32 fresh graduates) Brand protection policy

National Bank of Kuwait 14Contents

Section 1 Overview of NBK

Section 2 Strategy and Business Overview

Section 3 Operating Environment

Section 4 Financial Performance Highlights

Section 5 Appendix

National Bank of Kuwait 15Overview of Kuwait

Overview Fiscal breakeven oil price

The State of Kuwait is a sovereign state on the coast of the

90 90

Arabian Gulf with a population of 4.7 million 84

85 Excl inv inc Incl inv inc 85

80 80

Kuwait is a constitutional monarchy, headed by His Highness the 73

75 75

Emir, Sheikh Nawaf Al-Ahmad Al-Jaber Al-Sabah 72

70 70

68 66

65 65

Kuwait enjoys an open economy, dominated by the government 60

61

60

62 62

sector. Its economy is primarily dependent on the oil industry, but 55

57 54 54 55

54

has witnessed growing contribution from non-oil sectors 50 48 50

46

45 45 45

Kuwait has one of the lowest industry breakeven oil prices in the 40

45

40

13/14 14/15 15/16 16/17 17/18 18/19 19/20 20/21

world and a fiscal breakeven lower than some other GCC

countries, making it more resilient to low oil prices. It has one of

the world’s largest sovereign wealth funds and very low debt, Key economic indicators

which underpins the investment grade sovereign credit rating

Key Indicators 2020 2021F

Kuwait has a long-term policy vision under the banner of

Sovereign Ratings A1 / AA- / AA (M / S / F)

“Kuwait Vision 2035”. It encompasses six strategic aims:

increasing GDP growth; encouraging the private sector; Current Account $33.5 bn $28.8 bn

supporting human and social development; promoting Gov Revenues* (% GDP) 32% 39%

demographic policies; enhancing and improving the

Public Debt* (% GDP) 12% 17%

effectiveness of government administration and consolidating the

* Financial year. Debt projections assume debt law is approved in FY21/22

country’s Islamic and Arab identity

Sources: Central Bank of Kuwait, Central Statistical Bureau, Ministry of Finance, NBK estimates National Bank of Kuwait 16Kuwait’s Economy

Recent Developments Real GDP (% y/y)

GDP declined by 8.8% in 2020 due to sharply lower oil production as Kuwait

Total Non-oil

adhered to OPEC+ cuts and reduced non-oil activity resulting from the

coronavirus pandemic. Headline growth could rebound to 0.5% in 2021 as 10 10

5.7 4.2

GDP Growth these cuts are partially reversed. 3.0

5 3.2 2.5 2.6 5

1.1 1.3

Non-oil GDP contracted 8.8% in 2020 after mobility restrictions were imposed 0.5 0.6 0.0

to contain the pandemic. Growth could rebound 3.0% in 2021 as private 0

2.4

0

consumption recovers. 2.9 -0.6 0.5

-5 -5

-4.7 -8.8

After cutting spending in FY20/21 to address the fiscal deficit, the FY21/22

budget outlined a 7% rise in outlays, including a targeted 20% rise in capex. If -10 -8.9 -10

Public 2013 2014 2015 2016 2017 2018 2019 2020 2021f

implemented, this would help spur the recovery in economic growth.

Finance and

Inflation Inflation accelerated to 2.1% in 2020, mainly on higher food prices, and is

expected to average 2.5% in 2021; there is some downside risk from potential Private credit (change, %y/y)

softness in residential real estate rents.

10 10

Month end 12 month average

Consumer spending took a major hit during the lockdown months, but has 8 8

bounced back appreciably. Total spending (POS/ATM) was up 49% y/y in June

Consumer 2021, albeit boosted by weakness at the same time last year. 6 6

Sector

Loan payment deferrals, the number of nationals in stable public sector jobs 4 4

and reduced overseas travel have supported spending.

2 2

0 0

Private credit growth has slowed so far this year, up 2.9% y/y in April 2021. But Apr-17 Apr-18 Apr-19 Apr-20 Apr-21

household borrowing is strong and business credit should benefit from the

economy returning to a more normal footing. The policy interest rate is at 1.5%.

Credit Growth Real estate sales 12m average (KD mn)

Deposits were down 1.2% y/y in April, but the reinstatement of loan repayment

deferrals should be positive; government deposit growth (-7.5% y/y) should get

200 200

a boost from higher oil prices this year, helping liquidity. Commercial Residential Investment

150 150

Property sales have returned to pre-Covid levels having been hard-hit in 2020.

Recent strength is mostly from the residential sector which could hold up well 100 100

Real Estate given the solid demand base and potentially get a further boost if the mortgage

Activity law is approved. 50 50

0 0

May-17 May-18 May-19 May-20 May-21

Sources: Central Bank of Kuwait, Central Statistical Bureau, Ministry of Finance, Refinitiv, NBK estimates National Bank of Kuwait 17Kuwait’s Banking Sector

Snapshot

The Kuwaiti banking sector comprises 23 banks, including 11 domestic banks (five conventional, five Shariah-compliant and one specialized), and branches of 12 international banks

(11 conventional and one Islamic).

The sector is well regulated by the Central Bank of Kuwait (“CBK”) with a number of regulations and supervisory norms to ensure the safety of the banking sector including through

strict supervision and imposition of prudential ratios, such as lending limits and concentrations, investment limits, liquidity and capital adequacy.

The banking sector has demonstrated strong resilience and elevated levels of financial soundness over the past 10 years. In fact, the sector is very well capitalized, with an

average Capital Adequacy Ratio of 19.0% in 4Q20, 8.5% higher than the required minimum of 10.5%. Non-performing loans to total loans stood at 2.0% in 4Q20.

Key indicators (USD bn, end year) 1 Development of the Discount rate (%, end year2)

Loans Deposits

122.1 122.0 126.6 129.9 3.5 3.5

119.4 121.9

110.7 108.0 114.2 110.8 109.8 113.6 113.0 116.6 116.7

102.1 3.0 3.0

2.5 2.5

2.0 2.0

1.5 1.5

1.0 1.0

2013 2014 2015 2016 2017 2018 2019 2020 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Sources: Central Bank of Kuwait / Refinitiv

National Bank of Kuwait 18

1Loans refers to total credit facilities to residents and deposits refer to private resident deposits, all as reported by the Central Bank of Kuwait. 2 Latest figure is for end-June 2021Dominant Kuwaiti Franchise

NBK is the leading banking group in Kuwait with a market leading position across its business segments

Total Assets (USD million) Customer Deposits (USD million)

National Bank of Kuwait 97,996 National Bank of Kuwait 56,403

Kuwait Finance House 70,906 Kuwait Finance House 50,511

Burgan Bank 23,433 Boubyan Bank 16,843

Gulf Bank 21,227 Burgan Bank 13,492

Boubyan Bank 20,157 Gulf Bank 13,302

Al-Ahli Bank of Kuwait 16,002 Al-Ahli Bank of Kuwait 11,494

Commercial Bank of Kuwait 14,472 Ahli United Bank 9,920

Ahli United Bank 14,411 Commercial Bank of Kuwait 7,812

Warba Bank 11,460 Warba Bank 7,761

Kuwait International Bank 9,239 Kuwait International Bank 5,424

0 20,000 40,000 60,000 80,000 100,000 120,000 0 10,000 20,000 30,000 40,000 50,000 60,000

Customer Loans & Advances (USD million) Net Profit attributable (USD million)

National Bank of Kuwait 57,722 National Bank of Kuwait 812

Kuwait Finance House 35,441 Kuwait Finance House 489

Boubyan Bank 15,905 Boubyan Bank 114

Burgan Bank 14,328 Burgan Bank 111

Gulf Bank 14,208 Ahli United Bank 98

Al-Ahli Bank of Kuwait 10,279 Gulf Bank 95

Ahli United Bank 10,268 Warba Bank 19

Warba Bank 8,235 Kuwait International Bank 0

Commercial Bank of Kuwait 7,515 Commercial Bank of Kuwait -

Kuwait International Bank 6,526 Al-Ahli Bank of Kuwait (230)

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 -250 -50 150 350 550 750 950

Sources: Bank’s annual reports. All data as of 31 December 2020 for Balance Sheet items and Income Statement Items.

Note: Kuwait Finance House, Boubyan Bank, AUB, KIB and Warba Bank are Islamic banks while Burgan Bank, CBK, Gulf Bank, Al-Ahli Bank of Kuwait are conventional banks.

National Bank of Kuwait 19Contents

Section 1 Overview of NBK

Section 2 Strategy and Business Overview

Section 3 Operating Environment

Section 4 Financial Performance Highlights

Section 5 Appendix

National Bank of Kuwait 20Operating Performance & Profitability

Profitability (USD mn) Operating Income Composition (USD mn)

Net Operating Income Net Profit

NII & NI from Islamic financing Non-interest income

2,953

2,778 2,953

2,778

23%

25%

1,503 1,503

1,323 1,377 1,377

23% 26%

812 77% 75%

534

369 74%

77%

2019 2020 1H 2020 1H 2021 2019 2020 1H 2020 1H 2021

Return on average assets (%) Return on average equity (%)

1.42% 12.3%

1.05% 9.2%

0.82% 7.0%

0.75% 6.3%

2019 2020 1H 2020 1H 2021 2019 2020 1H 2020 1H 2021

National Bank of Kuwait 21Operating Performance & Profitability (cont’d)

1H 2021 Op. income by type (%) 1H 2021 Op. income by business line (%) Cost to income (%)

Others, 5% Consumer

FX, 3% & Private

Banking, Corporate,

16% 37.0% 37.2% 37.6%

33%

Fees, 18%

34.0%

Inv Bkg &

AM, 4%

Others,

1%

Net Interest Islamic

Income, Banking,

74% Intern'l,

21%

25%

2019 2020 1H 2020 1H 2021

Net Interest Margin (%) Net Interest Margin Drivers

2.56%

2.21% 2.25% 2.28% -0.37% +0.82%

2.25% 2.28%

-0.42%

2019 2020 1H 2020 1H 2021 1H 2020 Loans Others Deposits 1H 2021

National Bank of Kuwait 22Balance Sheet Parameters

Net loan portfolio (USD bn) Loans to assets (USD bn)

Net Loans Net loan growth YoY (%) Total Assets Loans/Assets

61.5 104.9

57.7 58.4

54.6 98.0 98.6

96.5

56.5% 58.9% 59.2% 58.6%

8.4%

6.8%

5.7% 5.3%

Dec-19 Dec-20 Jun-20 Jun-21 Dec-19 Dec-20 Jun-20 Jun-21

Loan exposure by sector (%) (as at 30 June 2021) Low loan concentrations (as at 30 June 2021) Assets by Type (as at 30 June 2021)

Crude Oil & Goodwill and

Gases, 7% other Other, 2% Cash and ST

Manufacturing, Other, 12% Top 20 Customers intangible funds, 14%

8% assets, 2%

Others CBK Bonds

Inv. and Kuwait

Financial ,

16% securities, Tbills, 4%

7% Real Estate,

15%

20% Deposits with

Trade & banks, 4%

Commerce, Construction,

7% 3% 84%

Purchase of

Securities, Loans,

Personal, 4% advances

33% and Islamic

financing to

customers,

59%

National Bank of Kuwait 23Funding and Liquidity Positions

Customer Deposits (USD bn) Funding Mix (Total Liabilities)

Due to banks and other Fis Customer Deposits

Certificates of deposit Other borrowed funds

56.4 58.3 57.8

52.5

64% 68% 64%

67%

30% 23% 25% 26%

Dec-19 Dec-20 Jun-20 Jun-21 Dec-19 Dec-20 Jun-20 Jun-21

Overview of Investment Securities1 – USD 15.6 bn

As at 31 December 2020

Other, 5% Amortized Cost

FVPL

18%

Equities, 1% 5%

Non-Gov't Debt,

38% Gov't Debt (non

Kuwait), 56% FVOCI

77%

Notes:1Excludes investments in Central Bank of Kuwait Bonds and Kuwait Government Treasury Bonds National Bank of Kuwait 24Capitalization and Asset Quality

Total Equity1 Breakdown (USD mn) Prudent capitalization (%)

Share capital Statutory reserves Tier 1 Tier 2

Retained Earnings Other Reserves & Treasury Shares

18.4% 18.2%

17.8%

16.8%

11,323 10,915 11,107 1.9% 2.4% 2.5%

10,229 1.9%

3,382 3,134 2,719

2,229

4,715 4,392 4,641 4,861 15.9% 16.0% 14.9% 15.7%

1,076 1,129 1,084 1,138

2,151 2,259 2,275 2,389

Dec-19 Dec-20 Jun-20 Jun-21 Dec-19 Dec-20 Jun-20 Jun-21

Prudent Provisioning (USD mn) Provisions and Impairments (USD mn) Asset Quality Ratios (%)

Specific Provisions General Provisions Provisions for Credit Losses Other Impairment Losses Loan Loss Coverage Ratio NPL Ratio

813

2,266

95

1,668 1,678

1,702 428 421

24 272% 186% 2.45%

718 91 323

1,269 1,309

10 220%

404 1.77% 152%

330 313 1.72%

564 1.10%

398 368

2018 2019 2020 2019 2020 1H 2020 1H 2021 Dec-19 Dec-20 Jun-20 Jun-21

Notes:1Equity here refers to total equity attributable to the shareholders of National Bank of Kuwait S.A.K.P. National Bank of Kuwait 25Expected Credit Losses (ECL) 1H 2021

Financial Statements ECL Disclosure (USD mn) Total Gross Loans (USD bn)

Stage 1 Stage 2 Stage 3

30 June 2021 Stage1 Stage 2 Stage 3 Total

60.3 60.0 63.8

2% 2% 3%

Loans, advances and Islamic 7% 10% 9%

financing to customers 56,449 5,791 1,603 63,843

91% 88%

88%

Contingent liabilities 12,078 2,554 107 14,740

ECL allowance for credit

facilities 443 525 1,128 2,096

Jun-20 Dec-20 Jun-21

ECL Allowance for Credit Facilities CBK Credit Provisions vs IFRS 9 ECL (USD mn)

CBK Provision ECL* Excess over ECL

2,504

2,387

2,080

Stage 1 Stage 1 Stage 1 408

21% 392

25% 21%

337

Stage 3

Stage 2 47%

Stage 3 Stage 2 Stage 3 Stage 2

54% 21% 25%

32% 54%

1,995 2,096

1,743

June-20 (USD 1,743 mn) Dec-20 (USD 1,995 mn) June-21 (USD 2,096 mn)

Jun-20 Dec-20 Jun-21

* ECLs as per CBK guidelines

National Bank of Kuwait 26Contents

Section 1 Overview of NBK

Section 2 Strategy and Business Overview

Section 3 Operating Environment

Section 4 Financial Performance Highlights

Section 5 Appendix

National Bank of Kuwait 27Kuwait Selected Mega Projects

Project Sector Value (KD bn) Scope Status

Underway: The infrastructure works have progressed up to 93% on Plots N2 & N3 and up to 67% on Plots N1 & N4. Roads

South Al Mutlaa City Housing 2.33 30,000 residential units, schools and other facilities construction has progressed up to 52% and is scheduled to be completed by Mar-2023. Likewise, construction works have

commenced on water distribution network.

Housing Underway: Infrastructure works completed. Project was in the execution stage as per latest update in May-2020 and scheduled to

Jahra & Sulaibiya Low Cost Housing City 0.6 Low cost housing project north of Kuwait City; 824 Hectares

complete in 2030.

New Refinery Project Underway: Construction works are complete on P-1 to P-5. The project is to operate by end-2021 from June-2021. Final

Oil & gas 3.90 New 615,000 bpd refinery by KNPC

(NRP) consultancy contract yet to be awarded.

Clean Fuels Project Specification upgrade and expansion of 2 existing refineries to produce Complete: Overall progress 100%. Construction works completed. The project is currently under operation and the time for its

Oil & gas 3.70

(CFP) 800,000 b/d. shutdown mechanical maintenance is still unknown.

Jurassic Non Associated Oil & Gas Reserves Production of 120,000 b/d of wet crude and more than 300 million cubic Underway: Construction activities completed on West and East Raudhatain field, Sabriyah and Umm Niqa and commissioning is

Oil & gas 1.22

Expansion: Phase 2 feet a day (cf/d) of sour gas underway. JPF-4 & 5 bids submitted. The invitation to bid for JPF-6 and 7 are not yet issued and tendency towards cancellation.

Planning: FEED works completed. Project Engineering and Management Services for 6 years contract has been awarded. ITB

Petrochemical Facility at Al-Zour Oil & gas 2.0 Petrochemical plant to be integrated with Al-Zour refinery.

expected by 4Q2021 for 7 qualified bidders.

4 full containment LNG tanks each with a working capacity of 225,500 Underway: Progress at 97%. Dredging works have been completed and undertaken while construction works are still progressing

LNG Import and Regasification Terminal Oil & gas 0.80 3

m and a regasification plant with capacity of 1500 BBTU/day and expected to be completed by 2022.

Complete/Planning: Overall progress 55%. P-1 is complete. KAPP obtained approval to award the Transaction Advisory Services

1800 MW of power generation capacity and 464,100m3 /day of

Al-Zour North (IWPP) – P2 to P5 Power & water 0.5 contract for P-2 & P-3. P-4 & P-5 are under study.

desalination capacity

Net capacity of a min 1,500 MW of power and a min 125 MIGD of Bidding/Planning: KAPP obtained approval to award the Transaction Advisory Services contract . P-2 & P-3 are still in the study

Al-Khairan Power & Desalination Plant (IWPP) Power & water 0.51

desalinated water phase.

3

Initial treatment capacity of 500,000 m /d. Plant may replace Riqqa Underway: KAPP signed final agreements and financial closure has been achieved for the project. Construction works commenced

Umm Al Hayman Waste Water (PPP) Power & water 0.47

WWTP in future and set to be completed by Jan-2024.

Waste to energy facility; 50% of all the municipal solid waste produced

Kabd Municipal Solid Waste Project Power & water 0.3 On Hold: The project has been put on hold and the client is likely to cancel the project.

in Kuwait will be processed at the facility

Planning: Feasibility study for the project has been completed stating the PPP models is more economically viable than the

Kuwait Metropolitan Rapid Transit Transport 5.4 165 km transit line running across Kuwait.

traditional tendered approach.

To increase the annual handling capacity of the airport to 20 million Underway/Planning: Overall progress at 41%. Construction works ongoing on Terminal. P-2 contract for landside works is yet to be

Airport Expansion (New Passenger Building) Transport 1.90 passengers and new runways and infrastructure expansion awarded. Crossroads contract bid submission deadline ended Jun-2021. The main contract tender is yet to be issued on P-1 of

Package 1. The Cargo City (Package 4B) is still in its initial stage of development.

National Bank of Kuwait 28Consolidated financials 1H 2021 (USD million)

YoY Growth YoY Growth

Income Statement (USD million) 1H-2020 1H-2021 Balance sheet (USD million) June-2020 June-2021

(%) (%)

Interest Income 1,391 1,083 (22%) Cash and short term funds 12,527 14,476 16%

Interest Expense 558 247 (56%) Central Bank of Kuwait bonds 2,757 2,757 0%

Net Interest Income 833 836 0% Kuwait Government Treasury bonds 1,927 1,488 (23%)

Deposits with banks 3,698 4,282 16%

Murabaha and other Islamic financing income 379 374 (1%)

Loans, advances and Islamic financing to customers 58,366 61,461 5%

Distribution to depositors and Murabaha costs 154 102 (34%)

Investment securities 14,963 15,726 5%

Net Income from Islamic financing 225 272 21% Investment in associates 21 14 (34%)

NII and NI from Islamic financing 1,058 1,108 5% Land, premises and equipment 1,488 1,461 (2%)

Net fees and commissions 238 270 14% Goodwill and other intangible assets 1,936 1,929 0%

Other assets 907 1,300 43%

Net investment income (9) 60 NM

Total Assets 98,589 104,895 6%

Net gains from dealing in foreign currencies 85 53 (38%) Due to banks and other financial institutions 21,049 23,144 10%

Other operating income 6 12 NM Customer deposits 58,342 57,798 (1%)

Non-interest income 319 395 24% Certificates of deposit issued 1,667 4,655 NM

Net Operating Income 1,377 1,503 9% Other borrowed funds 1,977 2,724 38%

Other liabilities 2,597 2,422 (7%)

Staff expenses 282 314 11%

Total Liabilities 85,631 90,744 6%

Other administrative expenses 173 192 11%

Share capital 2,275 2,389 5%

Depreciation of premises and equipment 55 56 2% Proposed bonus shares - - NM

Amortisation of intangible assets 3 3 0% Statutory reserve 1,084 1,138 5%

Operating Expenses 513 565 10% Share premium account 2,667 2,667 0%

Treasury shares (130) - NM

Pre-provision profits (and impairments) 865 938 9%

Treasury share reserve 83 116 39%

Provision charge for credit losses and impairment losses 421 323 (23%) Other reserves 4,250 4,796 13%

Equity attributable to shareholders 10,229 11,107 9%

Operating profit before taxation 444 615 39%

Perpetual Tier 1 Capital Securities 1,456 1,458 0%

Taxation 51 55 6%

Non-controlling interests 1,272 1,586 25%

Non-controlling interest 24 27 13% Total equity 12,958 14,151 9%

Profit attributable to shareholders of the Bank 369 534 45% Total liabilities and equity 98,589 104,895 6%

National Bank of Kuwait 29Consolidated Statement Of Income (USD million)

USD million 2018 2019 2020

Interest Income 2,959 3,253 2,496

Interest Expense 1,091 1,390 880

Net Interest Income 1,868 1,863 1,617

Murabaha and other Islamic financing income 614 697 742

Finance cost and Distribution to depositors 204 287 270

Net Income from Islamic financing 409 410 472

Net interest income and net income from Islamic financing 2,277 2,273 2,089

Net fees and commissions 495 518 481

Net investment income 7 28 7

Net gains from dealing in foreign currencies 129 130 126

Other operating income 5 5 75

Non-interest income 636 680 689

Net Operating Income 2,913 2,953 2,778

Staff expenses 528 579 575

Other administrative expenses 325 326 337

Depreciation of premises and equipment 48 87 110

Amortisation of intangible assets 10 11 5

Operating Expenses 911 1,003 1,027

Op. profit before provision for credit losses and impairment losses 2,001 1,950 1,751

Provision charge for credit losses 558 404 718

Impairment losses 34 24 95

Operating profit before taxation 1,409 1,522 938

Taxation 110 117 85

Non-controlling interest 77 81 41

Profit attributable to shareholders of the Bank 1,222 1,323 812

National Bank of Kuwait 30Consolidated Statement Of Financial Position (USD million)

USD million 2018 2019 2020

Cash and short term funds 9,783 12,489 12,782

Central Bank of Kuwait bonds 2,671 2,715 2,738

Kuwait Government treasury bonds 2,876 2,184 1,527

Deposits with banks 7,796 6,295 3,388

Loans, advances and Islamic financing to customers 51,124 54,584 57,722

Investment securities 12,129 13,898 15,594

Investment in associates 104 116 17

Land, premises and equipment 1,196 1,430 1,408

Goodwill and other intangible assets 1,909 1,922 1,919

Other assets 859 891 812

Total Assets 90,447 96,524 97,996

Due to banks and other financial institutions 26,679 25,002 19,725

Customer deposits 47,449 52,533 56,403

Certificates of deposit issued 1,488 1,776 3,030

Other borrowed funds 1,137 1,161 2,667

Other liabilities 1,488 2,007 2,516

Total Liabilities 78,241 82,478 84,341

Share capital 2,049 2,151 2,259

Proposed bonus shares 102 108 113

Statutory reserve 1,024 1,076 1,129

Share premium account 2,648 2,648 2,648

Treasury shares (216) (129) -

Treasury share reserve 46 83 115

Other reserves 4,777 5,387 4,650

Equity attributable to shareholders of the bank 10,431 11,323 10,915

Perpetual Tier 1 Capital Securities 695 1,446 1,446

Non-controlling interests 1,079 1,276 1,295

Total equity 12,205 14,045 13,656

Total liabilities and equity 90,447 96,524 97,996

National Bank of Kuwait 31Contact

Contact Investor Relations Useful information

E: Investor-Relations@nbk.com

Download copies of NBK’s:

National Bank of Kuwait (NBK)

PO Box 95, 13001 Safat Kuwait • Financial statements

Al Shuhada Street, Block 7, Sharq • Earnings release

State of Kuwait • Annual report

National Bank of Kuwait 32National Bank of Kuwait

Investor Presentation

July 2021

National Bank of Kuwait 33You can also read