Melville Douglas Focused Quarterly Commentary - 522 Origin ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Melville Douglas

Focused

Quarterly Commentary

/ Q1 2021

Staying the course

It has been just over a year since global equity markets reached their

lows on 23rd March 2020. A period when the outlook for not only

global growth but also humanity was extremely uncertain and difficult

to quantify. Companies around the world swiftly laid off employees in

the tens of millions as lockdown measures were enforced to contain

one of the worst humanitarian crises since the 1930s as COVID-19

became a global pandemic. Commodity prices collapsed whilst

companies’ capital expenditure programs were shelved as access to

funding at one stage became near impossible before central banks Bernard Drotschie

stepped in. Over this period companies had to rapidly adapt to a very / Chief Investment Officer

fast changing environment as consumers changed their spending

patterns and priorities and supply disruptions became the order of the

day. The burden of the health crisis has fallen unevenly across sectors,

with the non-tradable services sector most negatively affected –

tourism, hospitality and the high street bricks and mortar retail trade.

The impact on vulnerable income groups (women, the informal sector,

young workers, migrant workers and the less well-educated segment)

has also been significant as poverty levels have sadly increased.

The response by central banks and Governments has been a highly

effective coordinated effort of unconventional and unprecedented

monetary and fiscal support to stave off what was sure to be a

prolonged recession. The fiscal impetus alone has so far amounted to

more than 5% of Global GDP and more is on its way with the recently

approved $1.9 trillion support package in the US, which looks set to be

followed by Europe’s own fiscal stimulus program.

GLOBAL DEBT CONTINUES TO RISE SHARPLY

$ Trillion % of GDP, weighted avg.

290 360

280

350

270

260

340

250

Global debt (in USD)

240 330

% of GDP (rhs)

230

320

220

210

310

200

190 300

2013 2014 2015 2016 2017 2018 2019 2020

Source: IIF, BIS, IMF, National sources

In addition, the Biden administration has requested an additional $2 trillion which has been earmarked for

infrastructure projects over the next eight years. These are truly gigantic numbers, which combined with very

accommodative monetary (low interest rates) policies, the success of the inoculation programs globally,

pent up consumer demand and record high savings ratios should result in a very strong recovery in the global

economy, to a growth rate which has not been experienced since 2007. Over the longer term however, the

question of how governments plan to fund the increased levels of debt remains, and in time higher taxes or other

forms of austerity measures are a given. For now, policymakers have their foot on the economic accelerator

and are unlikely to ease off until economies are sustainably back on their feet and COVID-19 is under control.

VACCINE-POWERED STRENGTHENING

IMF NOW PROJECTS 2021 WILL BE THE BEST YEAR FOR GLOBAL GROWTH SINCE 2007

5%

4%

3%

2%

1% Annual GDP (YOY)

0%

Projections

-1%

-2%

-3%

1980 1986 1992 1998 2004 2010 2016 2022

Source: International Monetary Fund World Economic Outlook

Note: 2020 is an estimate

Investment markets have quickly turned their attention to the change in the growth and inflation outlook and many are

starting to be concerned that central banks might be behind the curve, meaning that interest rates and quantitative

easing programs are perhaps too loose and accommodative at this stage of the economic cycle. This debate is not

going to disappear any time soon; inflation is bound to increase significantly over the next few months partly due to

supply constraints / bottlenecks (COVID-19 restrictions and more recently the Suez Canal traffic jam), but mostly

due to base effects. From the lows reached a year ago, the price of oil has more than tripled and industrial commodity

prices have also reached new highs. Furthermore, the price of certain goods such as apparel, as well as non-tradable

services, are expected to bounce back to pre-crisis levels once mobility restrictions have been fully relaxed.

INFLATION EXPECTATIONS DERIVED FROM 5-YEAR BREAK-EVEN RATES

Source: Bloomberg

The key message from central banks however, is that these factors should be transitory in nature and that they will

allow inflation to overshoot targeted levels to make up for a sustained period of disinflation since the Global Financial

Crisis, when inflation consistently surprised on the downside. Capacity utilisation remains low whilst unemployment

is still well above pre-crisis levels which would indicate that there is still substantial slack in the system to prevent

inflation from spinning out of control on a sustained basis, thus reducing the need for a more restrictive monetary

policy over the next couple of years. For now at least, policy makers are adamant that more stimulus is required to

safeguard the economy from “a longer, more painful recession now – and long-term scarring of the economy later”.

However, investment markets have become more concerned that excessive growth fueled by overly high levels of

monetary injections and fiscal support may at some stage lead to an inflation problem that needs to be addressed

by tighter monetary conditions (higher real interest rates) than expected - something markets haven’t really had

to contend with for quite some time. Evidence of how markets might react to a less supportive monetary policy

environment is clear and in line with previous cycles. Stocks that have run ahead of themselves and especially those

whose share prices have benefited from increased speculation on the back of cheap financing and easy access to

online trading and derivative platforms have experienced larger drawdowns than the rest of the market. The same

holds true for Emerging Market equities which have until recently benefitted from the “risk-on” cyclical trade, and

although these corrections are trivial compared to the gains over the past few years, they are starting to reconfirm a

familiar dynamic – central bank and, in particular, US Fed interest rate normalisation rarely unfolds without meaningful

asset price disruption somewhere.

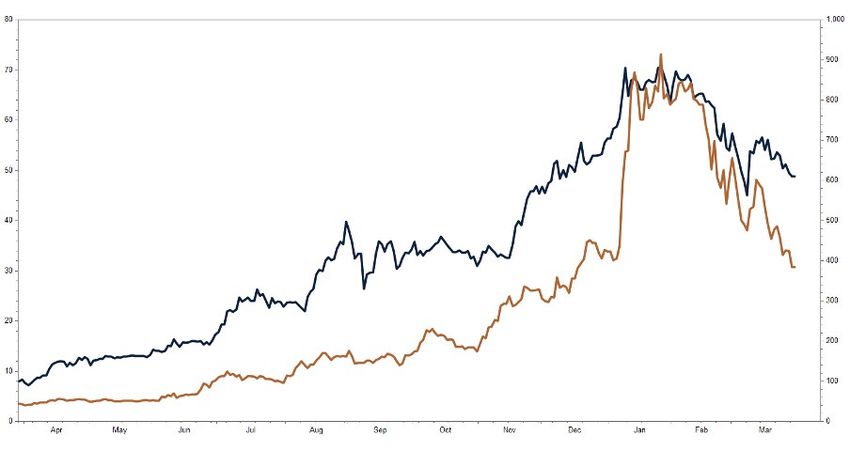

PLUG POWER AND TESLA’S SHARE PRICES

Tesla Inc - Price

Plug Power Inc. - Price

Source: Factset

The examples above are not unique but do highlight the potential for more volatility ahead as interest rates (cost of

money) normalise and, at the same time, serves as a good illustration of some of the unintended consequences of very

cheap money, which instead of being deployed in the real economy to create employment is finding its way into short

term speculative investment bets.

Higher bond yields a headwind

While risk assets such as equities have continued to gain ground this year, government bonds have been on the backfoot

for a change, with bond investors suffering losses. Bond yields have adjusted to a much-improved economic outlook

and higher inflation expectations and we would expect this normalisation in bond yields, alongside the steepening of

yield curves, to continue as the global economy transitions from recession to expansion.

US YIELD CURVE

3.0

2.5

2.0

Now

One Week Ago

1.5

One Month Ago

1.0 One Year Ago

0.5

0.0

-0.5

6M 1Y 2Y 3Y 5Y 10Y 15Y 20Y 30Y

Source: Bloomberg

Conclusion

The rebound in global economic activity is expected to be strong for 2021. A continuation of loose monetary

and fiscal policies will underpin growth and together with the re-opening of economies provide a backdrop

that is conducive for real (risk) assets. Inflation is sure to increase from recessionary lows and is expected

to overshoot in the near term, which is likely to result in some volatility along the way as investors reposition

their portfolios. Investors are concerned that increased inflation will result in higher interest rates and a

less supportive monetary environment. While this is possible, central banks have been communicating a

much more patient approach given the severity of, and uncertainties related to, last year’s pandemic crisis.

Higher global bond yields (discount rates) will be a headwind for equity valuations, but this is expected to

be more than offset by accelerating earnings growth.

Our approach is to continue backing quality companies with secular and structural growth drivers,

supported by strong balance sheets, while ensuring that we do not overpay for them. In addition, these

companies tend to have pricing power given the uniqueness of their offering, something that will become

very important once higher costs start to surface or in the (unexpected) event of an economic downswing.

Many other companies do not have the same ability to weather the storm from higher inflation (and interest

rates) and will thus find it difficult to maintain their profit margins and dividend growth.

We cannot be exactly sure when interest rates will normalise given that the US Federal Reserve (FOMC),

along with many other central banks, are adamant that monetary conditions will remain ‘ultra-loose’ for

the foreseeable future, but we do expect lower investment returns and perhaps more volatility in future for

multi-asset mandates and have positioned portfolios accordingly.

Light at the end of the tunnel

The South African economy is slowly recovering from a devastating 2020 during which the economy shrunk by 7%.

This was the second-largest annual contraction since 1920, when real GDP fell by 11.9% and was also about five times

larger than the contraction of 1.5% that followed the Global Financial Crisis (GFC) in 2009. Despite all the despair and

uncertainty, investment markets have more than recovered their losses over the period and the outlook for investors

remains positive given the strong recovery in earnings expected this year and undemanding valuations.

SA ASSET CLASS PERFORMANCE

TOTAL RETURN, YEAR-TO-DATE

Cash

All Share Index

MSCI World in ZAR

All Bond Index

COVID-19 remains a risk, but companies and individuals have successfully adapted to the new environment.

The impact of the second wave on the economy was much smaller than the original outbreak and we would expect

an even smaller impact should a third wave of infections materialise post the April public holidays. Technology has

played an important part in making this transition possible. Furthermore, the intervention by government and the SA

Reserve Bank has been equally important. Lower interest rates together with significant liquidity injections and tax

breaks have allowed many households and companies to survive. Unfortunately, there were casualties along the way,

with the travel and leisure industries worst affected. The full extent of the crisis will only be revealed in time as many

smaller companies simply do not have the liquidity or ability to service the higher debt levels incurred over the period .

Although many of us still work from home, activity levels in the economy have picked up a gear and this will continue

as vaccines are rolled out, paving the way for a more “normalised” environment. The mining industry has benefitted

hugely from higher metal prices, which have been brought about from supply disruptions and strong demand out

of China. Similarly, a strong rainfall season had a positive effect on agriculture. Other sectors/companies have also

benefitted from the stay-at-home theme, such as DIY/Hardware sales as individuals have either been renovating their

homes or added rooms to earn an extra source of income during the crisis. These benefits may well not be sustainable,

but for now many companies will be making hay while the sun shines. For the rest of the economy, continued support

from government intervention policies and improved service delivery will remain of utmost importance.

In this regard, there are more signs of government slowly getting its mojo back after it had to deal with one of the worst

crises in history. Even though government was found wanting in so many respects, there is no doubt that President

Cyril Ramaphosa has gained more support from within the party. This is an important development that should open

the door for improved execution and implementation of the government’s growth and recovery initiatives, which

primarily relate to improved infrastructure, service delivery, reducing the costs of doing business and eradicating

corruption. The task at hand is immense given the lack of capacity and experience within government and so therefore

closer collaboration with the private sector is of the utmost importance.

The recently awarded contracts announced by the Minister of Mineral Resources and Energy to supply 2,000

megawatts of emergency power to address the gap in electricity generating capacity is a step in the right direction and

illustrates what can be achieved. The power will be produced from a range of sources including solar, wind, liquified

natural gas and battery storage. Government has also released a request for proposals for the procurement of a

further 2,600 megawatts of renewable energy from independent power producers. Over the next 12 months, four

more requests for proposals for new power generation projects in renewable energy, gas, coal and battery storage

respectively will be released.

The base that the economy comes from is low after years of mismanagement and elevated corruption that have

resulted in hardship, unemployment and social unrest, but therein lies the opportunity. An improvement in confidence

is essential to lift the declining investment cycle and will go a long way to get the economy on its feet again and end

the continued outflow of capital by foreign investors. It’s now up to all stakeholders in the economy to pull together in

a concerted effort to change its growth trajectory.

Monetary support to continue amid fiscal restraint

In a unanimous decision, the Monetary Policy Committee members left the repo rate unchanged during their March

meeting. The outlook for inflation remains subdued and although the impact of a higher oil price, electricity prices and

other administrative prices will result in higher headline inflation, the expectation is that the second-round effects on

core inflation will be temporary and contained in nature, given the underlying weakness in final demand. Furthermore,

governor Lesetja Kganyago also reiterated that the Reserve Bank stands ready to inject additional liquidity as and

when required. This is crucially important to keep the funding lines open for companies in need.

SA INFLATION: HEADLINE AND CORE

CPI, Headline

CPI, Core

The support from the Reserve Bank is important at this juncture of the country’s economic cycle given that National

Treasury will be focused on rebuilding fiscal buffers through countercyclical fiscal tightening after years of unnecessary

countercyclical fiscal expansion. Government’s finances are dire and although the National Budget Speech delivered

a positive surprise in term of government’s debt trajectory over the next few years, compared to what was expected

at the Medium-Term Budget Policy Statement in October last year, execution risks remain high as the bulk of the

proposed savings are expected to come from the public sector wage bill over the medium term. Government cannot

afford to loosen the reins at this stage as any evidence of further deterioration is sure to result in further downgrades

by the international credit rating agencies. In such an event, South Africa will be rated as highly speculative (from

speculative), which will immediately result in an even higher cost of capital for the country. It is alarming to think that

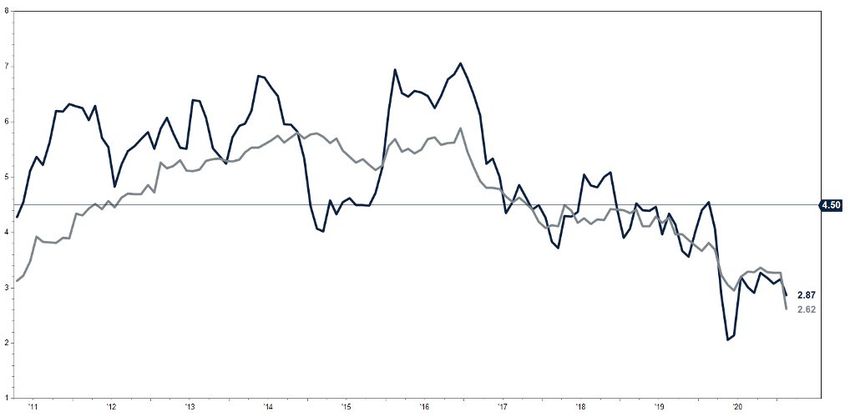

the yield differentiation between a South African and an American 10-year bond is nearly 8% - an illustration of the

country’s debt predicament.

SOUTH AFRICA’S SOVEREIGN CREDIT RATING

5

4

Levels above Investment Grade

3

2

1

S&P

0

Fitch

-1 Moody’s

-2

Levels below Investment Grade

-3

-4

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Under the difficult circumstances, Minister of Finance Tito Mboweni delivered a reasonable budget. The reallocation

of spending from public sector compensation while staying committed towards infrastructure spend is encouraging.

An improvement in basic service deliveries such as water and electricity, improved road and railway, port and

telecommunication infrastructure, student housing and upgrading of ports will provide the necessary infrastructure

that will allow domestic companies to grow and compete internationally.

Another key feature of this budget was the determination by government to contain spending and optimise revenue

collection by adopting tax efficient ways of doing so. It was therefore encouraging that government has decided to opt

for growth and fiscal consolidation through putting a lid on public sector wages, instead of putting additional pressure

on households and corporates, after one of the deepest recessions in history. The minister pledged to reduce the

corporate tax rate to 27% for companies with years of assessment commencing on or after 1 April 2022. In our view,

this is a good move on the part of government as one of the objectives for government is to lower the cost of doing

business and to make South African companies more competitive. With that in mind, this will certainly assist and

should be a step in the right direction. In time and when business confidence improves, this reduction in tax rate

should afford companies the opportunity to invest and potentially employ more people.

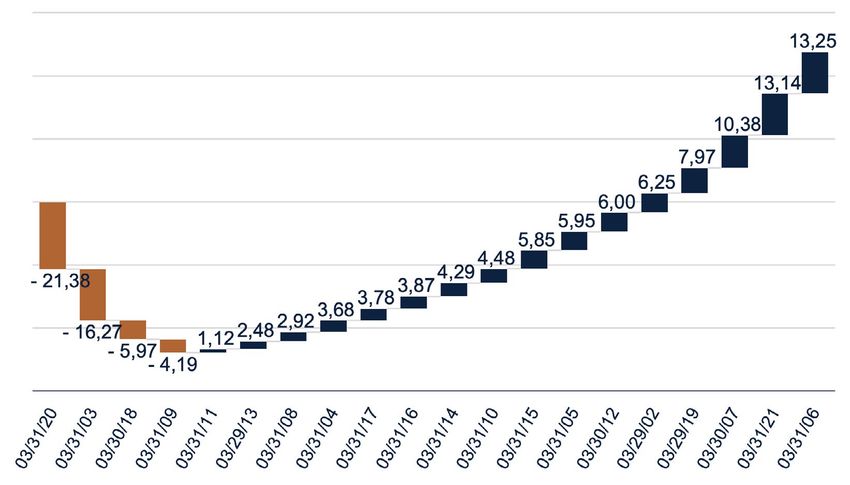

The JSE delivers the best Q1 performance in 15 years

Q1 PERFORMANCE

The domestic equity market has de-rated relative to emerging

markets and is currently trading at the lower end of its historical

range – an attractive entry point for patient investors

The JSE All Share Index produced its best Q1 performance in 15 years by

returning 13% and is one of the best performing equity markets this year. A

good result given the economic backdrop but does speak to the underlying

value in locally listed equities. Although the returns were reasonably broad

based, domestic financials continued to lag the rest of the market on the back

of poor results and weak guidance from management. Platinum group metals

(PGMs) in particular had another strong quarter and some of the stocks that

were under significant pressure a year ago in the leisure, retail and chemical

industries have rebounded sharply. Naspers, which makes up more than

20% of the index, contributed positively as its share price forged ahead.

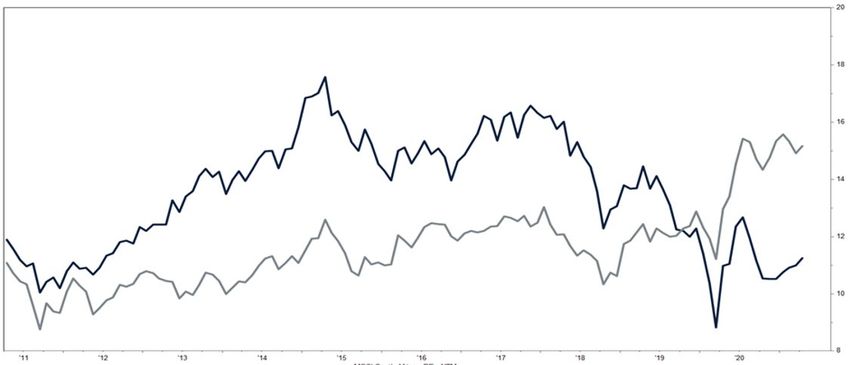

SOUTH AFRICA VS EM FORWARD P/E

MSCI South Africa

MSCI EM

While returns have been positive, the domestic equity market has de-rated

relative to emerging markets and is currently trading at the lower end of its

historical range – an attractive entry point for patient investors. The derating

can be explained by the surge in earnings growth (+50%) expected this year.

What is perhaps most surprising is that earnings increased by 5% during

2020. However, this is not a true reflection of how domestic companies

performed last year. Strong earnings growth from materials (resources),

which benefited from the windfall of higher commodity prices, combined

with another strong performance in profits from Naspers (Tencent), explains

the positive outcome. Domestic orientated companies that are reliant on

South Africa’s economic developments have experienced a much tougher

environment as illustrated in the table below, which provides a summary of

last year’s earnings growth and the consensus forecasts over the medium

term.

EPS GROWTH (%)

2020 2021E 2022E 2023E

MSCI SA 5.0 56.0 11.9 7.4

Consumer Discretionary 21.1 37.7 30.2 11.8

Retailing 21.1 37.7 30.2 11.8

Multiline Retail -54.4 65.6 19.1 15.8

Internet & Direct Marketing Retail -4.9 26.0 37.5 32.2

Speciality Retail -8.3 19.0 9.4 8.5

Consumer Staples -19.2 23.4 18.9 9.6

Food, Beverage & Tobacco -29.2 52.2 12.5 14.8

Food & Staples Retailing -17.6 19.3 20.1 8.7

Energy 0.4 28.6 -19.0 2.2

Oil, Gas & Consumer Fuels 0.4 28.6 -19.0 2.2

Financials -34.4 39.3 23.9 17.7

Banks -50.5 60.1 27.3 16.9

Insurance -23.0 26.0 20.4 15.6

Diversified Financials -13.8 26.9 21.8 21.0

Health Care -10.3 -5.6 14.1 8.2

Pharmaceuticals -10.3 -5.6 14.1 8.2

Industrials -23.7 18.0 16.9 9.2

Capital Goods -23.7 18.0 16.9 9.2

Materials 96.7 109.7 -2.3 -3.5

Metals & Mining 285.2 78.7 -4.4 -7.6

Communication Services 37.7 7.3 11.3 16.5

Real Estate -37.0 52.7 10.4 8.2

SA equity valuations are attractive and as economic momentum gathers; domestic orientated stocks are well

positioned to outperform. Resources have delivered exceptional returns over the past few years, but with profits

expected to peak this year, returns may well be more challenging in the future.

Conclusion

Investors will be pleased with the rebound in investment markets over the past 12 months. Returns from

South African assets (equities, bonds and the domestic currency) have outperformed global assets

handsomely over the same period – base effects did play an important role, but it does illustrate the

importance of focusing on absolute and relative valuations even when the chips are down.

The global economy is on the mend with strong growth expected over the next two years. South Africa

will benefit from the upswing as global trade accelerates. An improved global backdrop coupled with low

inventory levels and a very accommodative monetary policy bode well for South Africa’s recovery once

confidence returns. Now that the worst of the pandemic, with all of its uncertainties, is behind us, companies

will shift their focus from survival mode to growing profits again. Similarly, government will also be in a

better position to execute on its growth and recovery plan, which if successfully implemented, will assist in

improving the country’s long-term growth outlook.

South African assets offer good value. Government bonds are offering real income yields in excess of 6%

and the equity market is trading at depressed levels. Not unexpected given the enormous challenges faced

by the fiscus and domestic economy. But a turn in global confidence combined with a strong earnings

recovery are expected to underpin returns this year.

Domestic Asset Allocation

inflation. South African bonds were not spared and followed

Domestic Equity Overweight

suit. This development, aside from the risk of potential

Domestic Cash Neutral further credit downgrades, poses the largest near-term

risk to the asset class. Income yields are attractive relative

Domestic Bonds Neutral to cash and long-term expected inflation. We would expect

that returns from current levels will predominantly be

Global Equities Underweight derived from the income (coupons) earned. The outlook for

South Africa’s government debt profile remains a concern,

Offshore Bonds Underweight

but government remains steadfast in its objective of

keeping costs under control. In addition, an improvement in

tax collections bodes well for the coming year as economic

Domestic Equities – Overweight. Domestic equities growth improves.

delivered a very strong return during the first quarter of

the year. Expected returns from both a bottom up and Cash – Neutral.

a top down perspective remain attractive with double

digit returns expected over the next 12 months. This is a Offshore Fixed Income – Underweight. Even after the

function of attractive valuations and a rebound in earnings recent sell-off in developed market bonds, income yields

from depressed levels, which will further be supported by remain unattractive in both absolute and inflation adjusted

an improving economic backdrop. Any tangible signs of terms and we would expect yields to continue to normalise

reforms in South Africa or an improvement in the domestic to higher levels as inflation increases and the global

growth outlook will unlock significant value for investors. A economy recovers.

return to dividend payments by many domestic companies

will also be welcomed as cash earnings improve.

Offshore Equities – Underweight. Although we expect

positive returns from offshore equities over the next 12

months, we find domestic equities at current valuations

more attractive. Elevated valuations in offshore listed

equities are however expected to be supported by low

interest rates in developed markets. Strong and positive

earnings growth will continue to underpin returns, but

this should to some extent be hampered by the fairly rich

starting valuations. In other words, a de-rating in valuations

is our base case.

Bernard Drotschie

Domestic Fixed Income – Neutral. Global bonds have sold / Chief Investment Officer

off this year on an improved global backdrop and higherDomestic Equity

peers measured in US Dollars over the quarter as

Basic material Underweight

valuations catch up to the rest of the world. The JSE

Industrials Underweight capped swix returned 12.0% in USD over the quarter

whereas the MSCI AC World Index and the MSCI

Consumer goods Overweight Emerging Market Index returned 4.6% and 2.3% in

US Dollars respectively. Globally, macro-economic

Healthcare Neutral

factors continue to be supportive of risk assets, with

Consumer services Underweight unprecedented monetary and fiscal policy in place. This

should be supportive of South African equities in the near

Telcos Neutral term given that our equities look relatively cheap when

compared to global peers. We do however need to be

Financials Overweight

cognisant of global yields reversing off very low levels.

Technology Overweight This was evidenced in the first quarter of 2021 where

we witnessed some short sharp sell offs as the threat of

rising yields emerged.

South African equity continued its strong momentum from Crucially, South Africa needs to execute on the vaccine

the fourth quarter of 2020 into the first quarter of 2021, rollout and manage the fiscal situation which has

with the JSE capped swix delivering a first quarter return of deteriorated dramatically as GDP slumped and the

12.6%, bringing the rolling twelve month return to 54.2%, required sovereign borrowings increased in 2020. Longer

admittedly off a low base given where the trough of the term the country requires investment to stimulate growth

market was on 23rd March 2020. and job creation. The current GDP forecasts will not be

enough to meaningfully reduce the unemployment rate,

Most sectors showed very strong performances for the crucial to company earnings growth and sustainable

quarter, with telecommunications leading the way and equity returns.

basic materials not far behind as the strong performance

from 2020 continues into 2021 for the cyclical sector. Other Many listed South African companies have, however,

notable sectors were the technology, industrials, consumer managed their way through a very difficult 2020 and the

services and healthcare sectors which are all benefitting balance sheets for the most part appear to be resilient,

from a better economic outlook than initially anticipated. despite falling earnings. These strong balance sheets

Some of the sectors that lagged the overall performance should allow companies to recover and many who cut

in the first quarter include financials and property, where or did not pay dividends in 2020 should resume the

greater uncertainty exists in terms of the earnings recovery distributions in 2021.

into 2021 and beyond.

We expect more volatility for the rest of 2021.The opening

Despite the second wave of COVID-19 cases, which started of the economy and capacity utilisation are of utmost

in December 2020 with the full effects coming through in importance. Many share prices have recovered strongly

January and February 2021, equities appear to be looking in anticipation of the earnings recovery. Earnings misses

through the near-term virus impacts. South African could therefore have a significantly negative impact off the

government imposed restrictions to curb the spread of the current valuations. Now, more than ever, stock selection

virus are less restrictive on the economy than the lockdowns and diversification are paramount.

imposed in 2020. Unfortunately, the social and economic

impact will have long-lasting effects on the country and

many of the companies’ earnings will not recover to the 2019

base for several years.

Despite an improvement coming off record lows, business

confidence has improved, however, not to the required level

to promote investment and job creation given the ongoing

policy uncertainty and lack of reliable electricity. We should

however, experience a positive effect from short term

inventory restocking as most companies drew down on

inventory in 2020 to conserve cash.

Paolo Senatore

Despite these factors, South African equities significantly

/ Head: Domestic Equity Strategy

outperformed global equities and our emerging marketDomestic Fixed Income

Early this quarter, the country, just like the rest of the globe

Government Neutral

began the ambitious programme to inoculate its population

Inflation Linked Overweight to combat the spread of COVID-19. The R100 billion

reduction in the tax deficit estimates that were announced

State Owned Enterprise Underweight in the budget will go a long way in funding this programme

without stretching the fiscus further.

Budgeting in South Africa has proven to be a difficult The central bank in its two meetings this quarter has kept

juggling act for the Finance Ministry over the last few years interest rates on hold and, significantly in the last meeting

due to the deteriorating fiscal metrices of the country. held in mid-March, all five members of the MPC voted

This coupled with the onset of the COVID-19 pandemic, unanimously to keep rates on hold. This is significant as

from the beginning of last year, have compounded the it may be signalling that members of the monetary policy

economic and financial problems faced by South Africa. committee are now in agreement that the interest rate

As a result of these economic and financial difficulties, all cutting cycle has bottomed.

three rating agencies eventually downgraded the country’s

sovereign rating to non-investment grade. It was against Conclusion

this backdrop that the FY2021/22 budget was delivered at

the end of February. / We believe that the interest rate cutting cycle by the

central bank has bottomed, however, there is a very long

In the budget speech Minister Tito Mboweni minister way to go before interest rates are adjusted higher.

succeeded in delivering a more realistic and achievable Risk to the interest rate trajectory remains tilted to the

debt and fiscal consolidation trajectory, revising the downside

matrices slightly down from the October forecasts.

/ Mboweni’s budget was well received by the market and

rating agencies have taken a cautious approach awaiting

In the budget implementation of the ambitious plans in the budget

/ Estimated peak for total debt was reduced to 88.9% of / We are concerned that in the budget implementation risks

GDP in 2025-26 compared with the 95.3% forecast in remain as the bulk of the proposed savings will still come

October’s mid-term budget from the wage bill

/ Consolidated fiscal deficit was seen at 14% of GDP vs. / At current levels, bond yields are attractive and offer us

15.7% in the MTBPS an opportunity to increase the duration of the fund

/ The deficit is now expected to narrow to 9.3% in the

fiscal year through March 2022 and to 6.3% of GDP by

2023-24

/ Tax brackets were adjusted by more than inflation and

as a result giving back to taxpayers about R2.2 billion in

relief

/ Determination by government to contain spending and

optimise revenue collection by adopting tax efficient

means to do so

Mzimasi Mabece

/ Head of Fixed IncomeDomestic Market Performance / as at 31 March 2021 EQUITY MARCH QTR 12M All Share Index 1.6 13.1 54.0 Capped SWIX Index 3.7 12.6 54.2 Resources 1.2 18.7 92.5 Financials 0.8 2.5 37.6 Industrials 1.9 13.0 38.2 All Bond Index -2.5 -1.7 17.0 MSCI US 1.1 5.9 31.1 MSCI UK 0.0 7.1 15.3 MSCI Emerging -4.0 2.8 31.0 MSCI AC World 0.1 5.1 27.8 US DOLLAR RETURNS MARCH QTR 12M MSCI US 3.7 5.4 58.6 MSCI UK 2.6 6.5 39.4 MSCI Japan 1.1 1.6 39.7 MSCI Emerging -1.5 2.3 58.4 MSCI AC World 2.7 4.6 54.6 Citigroup WGB Index -2.1 -5.7 1.8 CURRENCY VS. US DOLLAR MARCH QTR 12M Rand 2.3 -0.5 20.7 Euro -2.9 -4.0 6.3 Yen -3.8 -6.7 -2.9 Sterling -1.1 0.8 11.0

Melville Douglas

Melville Douglas Investment Management (Pty) Ltd is a subsidiary of Standard Bank Group Limited.

Melville Douglas Investment Management (Pty) Ltd (Reg. No. 1962/000738/06) is an Authorised Financial Services Provider. (FSP number 595).

This summary brochure has been prepared for information purposes only and is not an offer (or solicitation of an offer) to buy or sell the product. This document and the information in

it may not be reproduced in whole or in part for any purpose without the express consent of Melville Douglas.

All information in this document is subject to change after publication without notice. While every care has been taken in preparing this document, no representation, warranty or

undertaking, express or implied, is given and no responsibility or liability is accepted by Melville Douglas as to the accuracy or completeness of the information or representations in this

document. Melville Douglas is not liable for any claims, liability, damages (whether direct or indirect, actual or consequential), loss, penalty, expense or cost of any nature, which you

may incur as a result of your entering into any proposed transaction/s or acting on any information set out in this document.

Some transactions described in this document may give rise to substantial risk and are not suitable for all investors and may not be suitable in jurisdictions outside the Republic of South

Africa. You should contact Melville Douglas before acting on any information in this document, as Melville Douglas makes no representation or warranty about the suitability of a product

for a particular client or circumstance. You should take particular care to consider the implications of entering into any transaction, including tax implications, either on your own or with

the assistance of an investment professional and should consider having a financial needs analysis done to assess the appropriateness of the product, investment or structure to your

particular circumstances. Past performance is not an indicator of future performance

Q1 2021 | 2021-031You can also read