Meeting the Challenge of Air Filter Supplies A Panel Discussion

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Meeting the Challenge of Air Filter Supplies

A Panel Discussion

Moderated by: Jim Rosenthal, CAFS, CEO, TEX-AIR Filters/Air

Relief Technologies

Panelists:

• Hunter Dinsmore, National Sales Manger, Tailored Chemical Products, Inc

• Greg Guy, CAFS, Vice President, Expanded Technologies, Inc.

• Chad Karl, CAFS, Graphic Packaging International, Inc.

• Rob Castor, Senior Director of Sales North America, Lydall Performance

Materials Inc.

NAFA 2021 Technical Seminar | Phoenix-Scottsdale, AZ | May 11-12

GLUE SHORTAGE OF 2021

Presented by: Hunter Dinsmore

INDUSTRY CHALLENGES PRIOR TO WINTER STORM URI • The adhesive industry was already imbalanced prior to Winter Storm Uri • COVID-19 – labor shortages for adhesive manufacturers and their suppliers • Overseas Transportation – Container Shortages on inbound materials from Asia & India • Domestic transportation issues – lack of drivers, trucks, and capacity. • Butyl Acrylate, Acetone, Propylene were some of the most impacted raw materials prior to Winter Storm Uri, which only made the situation worse…

FEBRUARY 13TH, 2021 – WINTER STORM URI

FEBRUARY 13TH, 2021 – WINTER STORM URI CONT. • Winter Storm Uri resulted in the immediate closer of all raw material manufacturing facilities generally associated with adhesive production. • VAM (Vinyl Acetate Monomer) became the immediate primary pinch point of all PVA/VAE polymer producers in the United States. • Pinch Points were not limited to VAM. Butyl Acrylate, PVOH, tank wagons, rail cars, totes, plasticizer, and other key component production was non-existent for up to 8 weeks in some cases.

No Issues

Tight

Short

VAM Feedstock Path

Crude Oil

(Heavy)

Oil Refinery

- Naphtha

- Gas Oil

Heavy and Light cracker

Ethylene

Feedstocks

Vinyl Acetate

VAM was short prior to Winter

Natural Gas Synthesis Gas

Methane Methanol Acetic Acid Storm Uri, which caused all NA

(Light) (CO, CO2, H2 ) VAM producers offline. With 3 of

4 producers still nor producing as

Gas Processing of 3/9. The 3 merchant producers

Acetic acid was tight prior to of VAM are working through

- Ethane

Winter Storm Uri due to restarting underlying assets to

- Propane

Clear Lake Acetic Acid asset bring VAM units back online. It is

- Butane

being down. The storm has expected that production may

further shortened the resume mid-March.

market.

Feedstocks - Map 1

4/21/2005

Coal Tar Naphthalene

Fischer-

Coal Tropsch Fischer-Tropsch wax Formaldehyde

Synthesis gas Synthesis

(CO, CO2, H2 )

Methanol Acetic

Coke CalciumCarbide Carbon monoxide Acid

Acetylene

Hydrogen

Natural gas Methane Steam

Cracker Carbon dioxide

Ethylene

Ethane

Propane Propylene

2 butene MEK

n-Butane Butylenes

LPG 1 butene

Butadiene

Maleic

i-Butane Isobutylene anhydride

i-Pentane

Isoprene

C5s Pygas Phthalic

Piperylene, C5 anhydride

n-Pentane

Hexanes

DCPD/CDC

Light Naphtha

Benzene

Naphtha

Gasoline Toluene o-Xylene

C7 – C9

Oil Xylenes

Distillate Fuels m-Xylene

Light Gas oils

C10 – C12

C8 -C9 aromatics

Refined oils p-Xylene

C10 - C17 n-Paraffin

Heavy Gas oils Base oils Micro Wax

Alpha Olefins

Paraffin Wax

Distillation residues Cat Cracker Carbon Black oil Carbon Black

CHALLENGES STILL BEING FACED TODAY

• The Logistical Shuffle

• Immediate rush of tank trucks due to need of immediate raw materials, customers couldn’t wait on rail cars.

Totes also became short do to lack of raw materials and an influx of tote needs due to short shipments of typical

tanker or rail car materials.

• Once raw materials facilities were running, and rail cars were able to be filled they all departed together. A

logistical dance is still ongoing, and it will take months for this to settle out.

• VAM allocations

• VAM producers are way behind on orders and still have customers on allocations due to continued Acetic Acid

issues, due to carbon monoxide issues.

• There remains a huge backlog of VAM needs in multiple sectors, allocations will not allow anyone to dig out of a

hole and make it extremely difficult for adhesive manufacturers to get our customers all the product they desire.

• VAM allocations are anticipated to remain in effect thru 2021.

TYPES OF FILTER ADHESIVES & BINDERS IMPACTED

• ALL OF THEM!

• The immediate pain point for all filter and media manufacturers was likely on waterbased

adhesives (shorter shelf life, lower inventory levels for manufacturers) but this is not all

that has been / will be impacted:

• Urethanes – Isocyanate shortages, Polyol Shortages, MDI shortages, logistical challenges

• Hotmelt Adhesives – Polyethylene shortages, EVA shortages, logistical challenges

What happened? Steel capacity 81% prior to pandemic 4-6 week lead times Steel capacity 55.4% 2020 production shut down 6-8 week lead times Steel capacity 78% 04/2021 demand is up 10-15 week lead time Truck shortage

• Average mill utilization last week grew to 78.0%.

What is the CRU Index? The CRU Index is the most established and trusted price benchmark in North America for U.S. Midwest Domestic Hot-Rolled Coil Steel (HRC). Ultimately, the CRU index helps those across the entire steel supply chain, from global investors and analysts to mills and service centers, manage their businesses by having a trusted price benchmark to use when purchasing and selling steel.

Pricing is based on the CRU Index. Steel mill contract. Comes out every week, but price is set on the 2nd Wednesday of month. Price for May will be set on 5/12. Determines price we pay for June steel shipments. $0.50/# 2020 now $1.00/# 2021 No spot market steel available.

Steel supplies remain excruciatingly tight, forcing suppliers to perform a balancing act in parceling out tons to customers.

Good News/Bad News The good news still outweighs the bad news in the construction/HVAC market, report wholesalers of galvanized steel products. HARDI said demand is strong across the country and has not been diminished by the record high steel prices, at least so far. Most expect steel prices to remain at record levels well into the second half of this year and possibly beyond. Lead times for spot orders of galvanized from the mills have extended to nearly 11 weeks, putting further strain on the already limited supplies. “The mills have not started to catch up yet. We are keeping all customers on allocation; they can only get what they have been using, not what they may need to grow,” said one wholesaler on the call.

I don’t know! Steel Dynamic president says pricing could last into 2022. HARDI says steel price high through 4th quarter of 2021. Steel prices will continue to rise in the near-term as demand steadily rises from pandemic levels and supply lags behind.

P aperboard M arket O verview for N A FA May 11, 2021 Inspired Packaging. A World of Difference.

FO O D ,B EV ER A G E,FO O D SER V IC E & C O N SU M ER

P R O D U C TS

P A P ER B O A R D P A C K A G IN G LEA D ER

2020 SALES MARKETS

$6.6B 39%

Food

20%

Foodservice

86%

Americas

12%

Europe

2% ROW

21% 20%

8

Paperboard Mills

73

Converting

3.9MTons Beverage

2%

Filter Frame

Other Consumer

Plants Produced

©2021 Graphic Packaging International 115SU STA IN ED M A R K ET

LEA D ER SH IP Big Player in #1 CRB Producer

Filter Frame

market

49%

2.1M ton U.S. market

40% 30%

of all folding cartons

in North America

of all paper cups in the U.S.

#1 CUK Producer

60%

2.7M ton U.S. market

#2 SBS Producer

22%

5.5M ton U.S. market

Source: PPC, AF&PA, RISI, GPI estimates

11

©2021 Graphic Packaging International 6Key factors contributing to board shortages in 2021

SUPPLY DEMAND

• Began 2020 with a flat plan – low inventory levels • COVID Effect– increasing demand for paperboard

• Early COVID – anticipated lean year and adjusted • 2020 full-year grocery sales increased 11.2%

• COVID – decreased efficiency from suppliers • Declining market for folding cartons increased 5-7%

• COVID – shortages of labor at plants • Filter Frame market segment increased … 10% ...?

• Planned Maintenance & adjusted timing for COVID

• Use of higher filtration level SKUs increased

• Cyber Attacks impacted some paper mills

• Are some customers & consumers “panic buying”?

• Winter Storm Uri in Feb – Impacted latex in coating

• Sustainability-driven plastic replacement initiatives

• Presently sitting at historically low levels of inventory

• Paperboard supply is a global challenge and not specific to GPI or USA.D EM A N D -H istoricalU SA industry folding

carton production

(000,short tons)

• Declining market for folding cartons increased 5-7%

262,000 tons

Filter Frame market

estimated 100,000 tons

Source: PPC, Company estimates

©2021 Graphic Packaging International 118DEMAND - Continue to experience a significant increase in orders

• Are some customers

and consumers

“panic buying”?

March is updated through 3/15/21DEMAND - Consumer packaging volume has increased dramatically

Consumer Products Units Sold Volume YOY % Change Beverages Volume YOY % Change

0.9 TOTAL BREAKFAST FOODS 8.3 CARBONATED SOFT DRINKS

3.8 TOTAL CEREAL

21.4 TOTAL SPARKLING WATER

20.9 TOTAL PREPARED FOODS-DRY MIXES

15.1 DRY DINNERS-PASTA

60.2 TOTAL FMB/CIDER

17.3 TOTAL FROZEN - PIZZA

6.2 TOTAL BEER

12.5 TOTAL FROZEN - MAIN COURSE

24.5 TOTAL FROZEN - APPETIZERS

5.6 TOTAL BOTTLED WATER

5.9 TOTAL FROZEN - COMPLETE MEAL

0.0 10.0 20.0 30.0 40.0 50.0 60.0 70.0

11.2 TOTAL ICE CREAM

52 Wks

0.9 FACIAL TISSUE

0.0 5.0 10.0 15.0 20.0 25.0 30.0

• 2020 full-year grocery sales increased 11.2%

52 Wks

Nielsen 52 weeks through week ending 2/20/21

Includes All Outlet Channels (Walmart, Food, and Club)SUPPLY - Strong demand reduced paperboard inventory in 2020

• Presently sitting at historically low levels of inventory

Coated Recycled Boxboard Unbleached Kraft Boxboard & Gypsum

Inventory YoY % Change

Inventory YoY % Change Total GPI

Total GPI 24.5%

20.0% 17.3% 16.5%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 17.0%

5.7% 9.4% 11.0%

190.0% 151.8% 10.0% 6.6% 12.7%13.9%

12.4% 9.1% 1.2%

126.8%

140.0% 112.8% 0.0% 4.4%

2.2% 4.2% 3.5%

95.0% 80.0%

90.0% -10.0% -13.6%

61.6% -16.5%

84.4%78.3% -14.3% -14.6%

40.0% 63.3% 57.1% 4.2% -20.0%

38.5% -11.5% -21.2%

25.9% -37.4%-30.8% -22.6% -24.3%

-10.0% -38.0% -43.9%

-30.0%

3.5%

-15.7% Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

-60.0% -28.1%

-43.1% -46.2% -56.7% 2020 2020 2020 2020 2020 2020 2020 2020 2020 2020 2020 2020

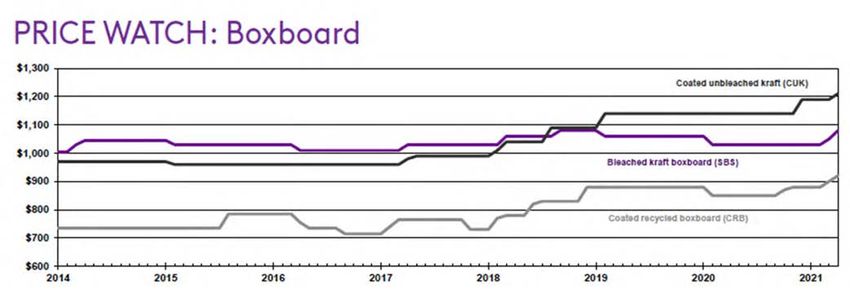

Source: AF&PAPRICING HISTORY of packaging grade paperboard

Tight

Steady Price Levels Multiple Increases

MarketWhat do we know about the board market? SUPPLY – is limited DEMAND – is growing INVENTORY – is low So what can be done about it?

Aggressive actions to improve supply on CRB and CUK

Coated Recycled Board (CRB) Coated Unbleached Kraft (CUK)

$100M investment in SBS mill to make

$600M investment in State of the Art it capable to “swing” to CUK

CRB paperboard machine in Creating 50k tons of incremental CUK

Kalamazoo, MI (January 2022) capacity (January 2021)

Secured 180k additional tons of supply Extending and increasing CUK to SBS

from NA CRB producers (January 2021) temporary moves to 90k tons (Jan2021)

Secured 25k tons of supply from NA Reducing exports by 40k tons of CUK

URB producers (January 2021) supply (February 2021)

Leveraging global purchases by 50k

Leverage integrated supply chain process improvements to drive 45k tons (Feb 2021)Leveraging the integrated supply chain requires customer involvement and support

• Forecasts and Forecast Accuracy is critical

• Longer term changes in forecast requires collaboration with supplier for planning and loading

• Any new changes should be communicated early in the process for planning & review

• Orders that exceed forecasts will be reviewed to ensure they are needed…timing & volume

• Reduced days of supply will result in smaller run sizes and more frequent runs

• Work with customers to address inventory on hand and aging before running similar orders

We appreciate your support as we work together to deliver outstanding serviceTH A N K YO U for the opportunity to be here and discuss paper Inspired Packaging. A World of Difference.

You can also read