How Germany Benefits from the Euro in Economic Terms

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

How Germany Benefits

Policy Brief # 2013/01

from the Euro in Economic

Terms

There can be no doubt about the fact that Germany bene-

fits from the euro in a significant number of ways. For ex-

ample, monetary union membership helps to reduce the

cost of international trade, and provides protection against

excessive exchange rate volatility. This means that even if

Germany had to write off a large percentage of the loans

that it has made available to the heavily indebted states of

southern Europe as part of the various euro rescue meas-

ures, the economic advantages of its membership of the

Dr. Thieß Petersen monetary union would continue to predominate. Reverting

Program

Shaping Sustainable to the deutschmark would thus be disadvantageous even in

Economies

purely economic terms.

Phone:

+49 5241 81-81218

Email:

thiess.petersen@

bertelsmann-

stiftung.de

Focus

Dr. Michael

Böhmer

Prognos AG Without the euro, that is, if Germany had a

separate currency, the annual increase in

Phone: real gross domestic product (GDP) would

+49 89 954 1586-

701 be about 0.5 percentage points lower. If

Email: one adds up the advantages of eurozone

michael.boehmer@

prognos.com membership between 2013 and 2025 in

terms of greater growth, the benefits as far

Henning vom as Germany is concerned amount to

Stein

Program Europe’s almost € 1.2 trillion.

Future

Phone:

+49 5241 81-81398

Email:

henning.vomstein@

bertelsmann-

stiftung.de

Future Social Market Economy Policy Brief # 2013/01

Since the advent of the European sover- model provided by Prognos AG (see

eign debt crisis German citizens have Bertelsmann Stiftung 2012a, p. 8). In or-

voiced mounting criticism of the European der to calculate what the real economic

Monetary Union and of the euro. In a rep- consequences are likely to be, the model

resentative opinion poll on the “Value of simulates the economic performance – i.e.

Europe” conducted in the summer of 2012 the real gross domestic product (GDP) – in

by the Bertelsmann Stiftung, 65 percent of the 42 countries covered by the VIEW

German respondents said that they model up to the year 2025 if Germany de-

thought they would now be better off if the cides to introduce a separate currency in

deutschmark were still in existence (see 2013. Only the results which show the

Bertelsmann Stiftung 2012a, p. 3). A real economic consequences on Germany

number of politicians and academics have are taken into consideration. The projec-

also joined in the chorus of criticism. tions relating to the size of real GDP in

Hans-Olaf Henkel, who used to be in fa- Germany (and the associated development

vour of the euro, has now become a bitter of the labour market) that emanate from

opponent, and in a book published in this scenario are compared with the eco-

2012 he included a telling subtitle, “How nomic developments described in “World

the Euro fraud threatens our prosperity” Report 2012,” which assumes the survival

(Henkel 2010). In the “Bogenberg Declara- of the eurozone (“basic forecast”). Its pre-

tion,” which was released at the end of dictions relating to global economic devel-

2011, the signatories, who included Ro- opment were also made with the help of

land Berger, Georg Milbradt and Hans- the VIEW projection model. The “World

Werner Sinn, subscribe to the idea that Report 2012,” which was compiled in the

“Germany does not benefit from the euro” summer of 2012, predicts a noticeable de-

(Bogenberger Erklärung 2011, p. 3). How- cline in global economic growth as a result

ever, the following model projections of the much-needed consolidation of pub-

demonstrate that German economic lic budgets throughout the world until

growth and indeed the German labour 2016/2017. The difference between the

market both benefit to a considerable ex- real economic development depicted in

tent from the euro. the two scenarios describes the advan-

tages that Germany derives from its

membership of the eurozone.

1. What the Projections Subsequently we look at a number of

Can Do other scenarios in which we assume that

the states which have assisted the Euro-

pean countries hit by the crisis by provid-

The goal of the model projections pre- ing loans and guarantees will have to re-

sented below is to assess the impact of nounce some of their claims. These sce-

Germany’s membership of the eurozone narios – the “euro survival plus debt writ-

on growth, income and the labour market. ten off scenarios” or, to put it even more

For this purpose there will be a scenario in succinctly, the “write-off scenarios” – take

which Germany has a separate currency: into account the fact that in order to stabi-

the “deutschmark scenario.” The real eco- lize the common currency the countries

nomic consequences associated with this which are trying to rescue the euro will

scenario are assessed with the help of the have to provide the appropriate financial

VIEW global macroeconomic projection resources.

02

Future Social Market Economy Policy Brief # 2013/01

In this context it is important to remember rency, interest rates would be lower than

that the following model projections are those in the eurozone. Falling interest

not designed to tell us what the conse- rates reduce manufacturing costs, and act

quences would be if Germany decided to as an incentive when it comes to making

leave the eurozone. If Germany left the investments. Thus a separate currency

European Monetary Union, the net result can have an impact in a number of differ-

would almost certainly be the sudden de- ent ways. Of the four listed above, the first

mise of the entire system. And this would three can have a negative effect on eco-

go hand in hand with a major global eco- nomic growth and the labour market,

nomic crisis, the consequences of which whereas lower interest rates can stimulate

would be completely unpredictable. growth. These effects are incorporated into

the model projections as follows:

With regard to the increase in transac-

2.Projections Based on tion costs, it is assumed that the euro

saves annual transaction costs amount-

Certain Assumptions ing to 0.5 percent of GDP. In 2013

these savings will come to about €12

billion. This means that in the model

The “deutschmark scenario” starts out projections import prices for goods and

from the assumption that from 2013 on- services, when compared with the ba-

wards Germany will go back to having a sic forecast, will increase by 1.1 per-

separate currency. This has four major ef- cent from 2013 onwards.

fects. First, having a separate currency The lower level of price transparency

will lead to higher transaction costs. Thus forms part of the “deutschmark sce-

German companies will have to protect nario” because companies have more

themselves against deutschmark ex- pricing flexibility. This leads to greater

change rate fluctuations. Furthermore, price increases, which augment the

people will have to pay for currency con- rate of inflation during the projection

version, for bank transfers between differ- period by an average of 0.13 percent-

ent currency areas, and for currency man- age points, and reduces the real in-

agement in banks and companies. Sec- come of private households.

ondly, after the reintroduction of the The assumed deutschmark exchange

deutschmark price transparency will be rate is based on the development of

lower than would have been the case if real exchange rates after 1999. After

Germany had remained in the eurozone. the advent of the euro the real ex-

The higher price transparency of the euro change rate fell by 23 percent in Ger-

is advantageous in that it stimulates cross- many, whereas the real exchange rate

border trade and enhances price competi- in the rest of the eurozone rose by 7

tion. The latter leads to significant price- percent. That is why, in the simulated

cutting and thus to an increase in interna- projections, the introduction of a sepa-

tional competitiveness. Third, it should be rate currency leads to a revaluation of

taken for granted that a separate currency the deutschmark by 23 percent and to

will lead to a great deal of pressure to re- a 7 percent devaluation of the euro.

value the deutschmark. Since this will Finally, the lower interest rates are de-

make German goods and services more termined with the help of what is

expensive in other countries, it will have a known as the “Taylor interest rate” (for

negative impact on German exports. more information on this point see

Fourth, if Germany had a separate cur- Deutsche Bundesbank 1999). The ap- 03Future Social Market Economy Policy Brief # 2013/01

plication of the Taylor rule means that

between 2013 and 2025 German inter-

3.Principal Results

est rates will on average be about 0.5

percentage points lower than in what A VIEW model projection based on the as-

remains of the eurozone. sumption that from 2013 onwards Ger-

many once again has a separate currency,

The “write-off scenarios” are based on the that is, that it has left the eurozone, will be

assumption that the eurozone will con- compiled in order to assess the economic

tinue to exist unchanged. However, they development of Germany in the

also assume that the four European states “deutschmark scenario.” In this model

hit by the crisis cannot repay in full the projection Germany’s separate currency

financial assistance that they have re- initially has the effect of promoting

ceived. As in the preceding study (see growth. Thus in 2013 the positive aspects

Bertelsmann Stiftung 2012b, and in par- of a strong deutschmark still outweigh the

ticular pp. 21-23) the assumption is that negative ones. For example, they include

there is going to be a debt haircut amount- lower import prices, which have the effect

ing to 60 percent of the claims on (up to) of reducing inflation, or lower interest

four south European states. A debt haircut rates, which act as an investment incen-

of this kind will be applied to both public tive. The revaluation of the deutschmark,

budgets and the private sector. As far as which has an adverse effect on exports,

public budgets are concerned, these losses sets in at a later stage. In other words, the

will have to be written off in full. Such level of exports and the level of imports

costs are clearly definable in auditing both react with some delay. However,

terms, so that the budget deficits in the from 2014 onwards the changes in the ba-

states which have provided direct or indi- sic framework start to have a dramatic

rect guarantees for the countries hit by the impact on the pace of German growth. The

crisis will increase in size. This means shock waves which are part and parcel of

that in the states concerned government the introduction of a separate currency

debt will increase, and so will the debt continue to reverberate rather noticeably

servicing requirements. For this reason until about 2020. After this the annual dif-

governments will be compelled to intro- ferences in growth between the basic fore-

duce consolidation measures elsewhere. cast and the exit model prediction begin to

In other words, they will either have to re- stabilize (see Fig. 1).

duce the level of expenditure, or they will

have to raise taxes and contributions. Both When one attempts to interpret these re-

of these things will lead to a decline in the sults it is important to bear in mind the

demand for goods and services, and this in purpose of the model predictions de-

turn will lead to a decline in manufactur- scribed at the beginning of this study. The

ing and employment. The private write- goal is not to assess the economic conse-

offs lead to a reduction in net wealth, and quences and what will happen if and

in the final analysis this has an impact on when Germany leaves the European

private households. These losses mean Monetary Union. The question is in fact

that there is a decline in private consumer about the advantages that Germany de-

expenditure and in investment in new rives from its membership of the euro-

housing construction. zone. In this context the long-term conse-

quences of the abrupt introduction of a

new currency are of crucial significance,

04Future Social Market Economy Policy Brief # 2013/01

between 2013 and

2025 in the

“deutschmark sce-

nario,” the total

comes to almost

€1.2 trillion. If this

sum is divided by

the total number of

German citizens, it

signifies an accu-

mulated loss in in-

come amounting to

more than €14,000

per inhabitant.

Slower economic

growth also means

that fewer people

are gainfully em-

ployed. The num-

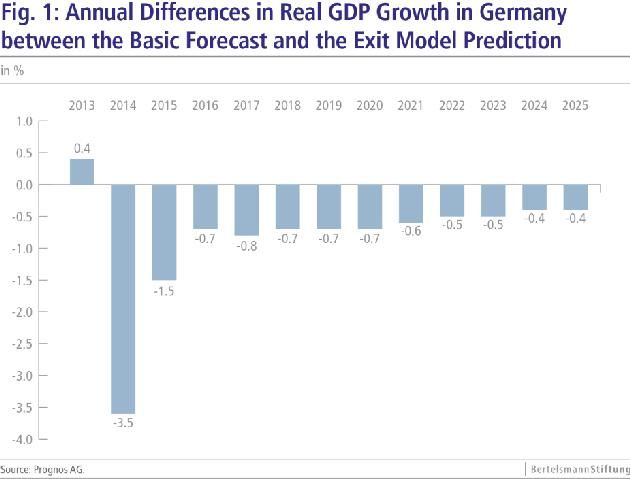

and not the direct impact or the short-term ber of people out of work increases by

fluctuations. Thus the long-term and rela- about 200,000, and as a result the un-

tively constant differences in growth, employment rate rises. For example, in

which become apparent from 2021 on- 2013 the unemployment rate in the

wards, are of decisive importance. “deutschmark scenario” is 7.4 percent,

whereas in the basic forecast it is

The long-term growth which derives from merely 6.9 percent.

Germany’s membership of the eurozone

becomes apparent at the end of the projec- All in all this means that Germany’s

tion period. It oscillates between 0.4 and membership of the eurozone has a posi-

0.6 percent. Thus in order to calculate how tive effect on real GDP, income, and the

German economic performance might de- labour market. Membership of the euro-

velop in an imaginary scenario in which zone would also make sense for Germany

Germany has a separate currency, the even if it had to write off many of its loans

long-term difference in growth of about to the four countries hit most by the crisis.

0.5 percent is used as a yardstick. The A series of four additional scenarios eluci-

economic consequences may be summa- date what the real economic consequences

rized as follows: for Germany will be if it waives 60 percent

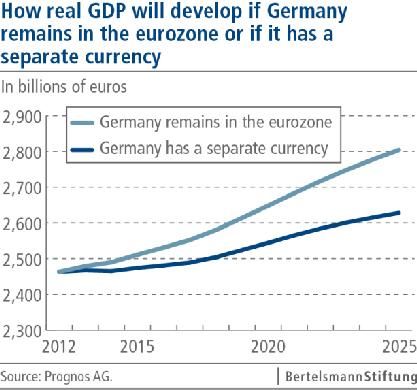

In 2025 German GDP in the “deutsch- of its claims in Greece (“G write-off” sce-

mark scenario” will amount to about nario), or 60 percent of its claims in

€2,630 billion, whereas if Germany Greece and Portugal (“GP write-off” sce-

continued to be a member of the Mone- nario), or indeed is confronted with a

tary Union it would amount to about situation in which it has to waive 60 per-

€2,800 billion (see Focus diagram on p. cent of what it is owed by all the four

1). For every German citizen in 2025 countries hit by the crisis (“GPSI write-off”

this signifies an average loss in real in- scenario).

come of about €2,200.

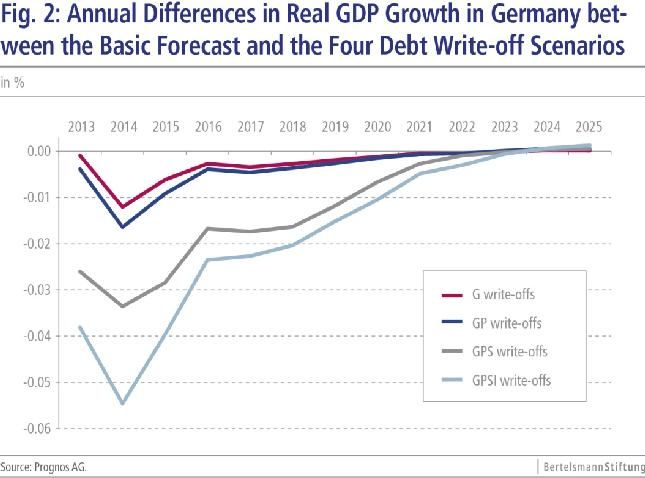

If one compares the data with the basic As fig. 2 demonstrates, as far as Germany

forecast and adds up the lost growth is concerned these bad debts lead to a de- 05Future Social Market Economy Policy Brief # 2013/01

cline in growth that is hardly perceptible. work provided by the common European

Even if there were a 60 percent debt hair- currency, the German economy grows

cut in all of the four countries hit by the more robustly than it would do in an

crisis, this would merely lead to a short- imaginary environment and with a sepa-

term and in fact minimal decline in the rate currency. It is true, of course, that a

real GDP growth rate of 0.05 percentage comprehensive debt haircut for Greece or

points. There are two significant reasons perhaps other members of the eurozone

why a debt haircut has such a relatively would increase the level of sovereign debt

small impact. On the one hand, a haircut in Germany. However, such an event

merely increases the indebtedness of the would do very little to inhibit growth.

euro rescuers, though without – as in the

preceding study – provoking major eco-

nomic upheavals in the debtor country,

e.g. state insolvency, a different currency,

4. Political Consequences

etc. (See Bertelsmann Stiftung 2012b, p.

20). On the other hand, as far as a debtor The projections on which this policy brief

country is concerned, a haircut leads to a is based show that Germany derives im-

lower level of indebtedness. This increases portant benefits from the euro. Member-

the government’s room for manoeuvre in ship of the common European currency

the area of fiscal policy, and has a positive leads to a growth trajectory that is always

impact on the economy. An exporting na- higher than what is achieved in the case of

tion such as Germany benefits from this a separate currency. Without the euro the

more favourable economic state of affairs annual German GDP growth rate would be

because it can boost its level of exports. about 0.5 percent lower. Even if Germany

and the other creditor countries have to

The net result of all this is that, even if it write off a significant part of the loans

has to write off sizeable losses, Germany which they have given to the highly in-

continues to benefit from its membership debted countries in southern Europe in

of the eurozone. As a result of the frame- the context of the various euro rescue

measures, the

advantages of the

Monetary Union,

at least as far as

Germany is con-

cerned, outweigh

the disadvan-

tages.

But over and

above the eco-

nomic advantages

one is also

prompted to ask a

rather basic ques-

tion, especially in

view of the re-

vived debate

06Future Social Market Economy Policy Brief # 2013/01

about whether we need more or less inte-

gration in the European Union. “What

5.References

would have happened if the euro had

never materialized?” That also happens to • Bertelsmann Stiftung, Der Wert Euro-

be a scenario that cannot simply be dis- pas: Repräsentative Bevölkerungsumfrage

missed as if it were of no importance. in Deutschland, Frankreich und Polen, Gü-

Plans for a European monetary union were tersloh 2012a.

mooted in the 1970s, but there were a • Bertelsmann Stiftung (Hrsg.), Wachs-

number of delays, most of which were tumswirkungen eines Euro-Ausstiegs, Gü-

caused by external shocks (e.g. the oil cri- tersloh 2012b.

ses). Right at the start the European • Bogenberger Erklärung, in: ifo Schnell-

Monetary Union had to weather the storm dienst, 64. Jg., Ausgabe 23/2011, S. 3 –

when the dot.com bubble burst in 2000. 11.

Will the euro once be seen as a golden op- • Deutsche Bundesbank, Taylor-Zins und

portunity that was seized just in time? Monetary Conditions Index, in: Monatsbe-

richt April 1999, S. 47 – 63.

It is becoming apparent that the European • Henkel, Hans-Olaf, Rettet unser Geld!

integration process has given our policy- Deutschland wird ausverkauft. Wie der

makers more room for manoeuvre in the Euro-Betrug unseren Wohlstand gefähr-

global context. It has never been possible det, München 2010.

to confine upheavals in the European

monetary system and the various ways in

which they impinge on the national

economies to the sphere of monetary pol-

icy. They have always led to a more or less

major political crisis in the EU. Without

the impending threat of the wholly unpre-

dictable collapse of their common cur-

rency the countries of the European Union

would not have been able to agree on the

measures that were needed in order to

rescue their banking system. However,

the fact that an independent European

Central Bank was a viable institution that

operated in a global context significantly

changed the policymaking framework. Af-

ter a severe financial crisis the euro is still

in use in all of the original 17 countries.

This, if nothing else, demonstrates the

learning ability of policymakers in an in-

tegrated Europe.

07Policy Brief 2012/06: Euro-exit in Southern Europe

Future Social Market Economy Policy Brief # 2013/01

While Greece defaulting on its sovereign debt and leav-

ing the European Monetary Union would have relatively

little effect on the world economy, such a move could

lead to contagion in Portugal, Spain and Italy, thus

evoking not only a sovereign default in those states as

well, but also a severe worldwide recession. Economic

growth would be reduced by a total of 17.2 trillion Eu-

ros in the world’s 42 largest economies in the lead-up

to 2020. Hence, political actors are well advised to pre-

vent Greece from leaving the euro, and the domino ef-

fect that this event could induce.

Policy Brief 2012/07: Sustainability and solidarity –

basic ideas of new financial structures

Federal financial structures which include fiscal equaliza-

tion between the German states remain indispensable

for leveling out significant regional economic differences

and for ensuring sufficient funding for the responsibili-

ties of the public sector across the nation. The necessary

revisions of financial structures beginning in 2020 pro-

vide an opportunity for a substantial overhaul. The ob-

jective is to consolidate in the long term the budgets of

federal, state and municipal governments and to safe-

guard a modern welfare state.

Bertelsmann Stiftung Upcoming releases:

Carl-Bertelsmann-Straße 256

D-33311 Gütersloh • Green and Fair Economy

www.bertelsmann-stiftung.de

Dr. Thieß Petersen • Better Employment Opportunities for

Phone: +49 5241 81-81218

thiess.petersen@bertelsmann-stiftung.de Older Workers

Eric Thode

Phone: +49 5241 81-81581

eric.thode@bertelsmann-stiftung.de

08 ISSN-Nummer: 2191-2467You can also read