Housing Market and Policy Backdrop - Lucian Cook Emily Williams

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Housing Market and Policy Backdrop

Lucian Cook

Emily Williams

1

Annual House Price Growth at +12.1% to the end of April…..

……meaning prices have risen by 23.7% since June 2020 (Nationwide)

110,990 housing transactions in March….

….continuing at +12% above the pre pandemic norm for the month (HMRC)

2nd hand stock levels a third lower in March 2022 than March 2019 (20CI)

And continued (if less generous support) from Help to Buy

2

A strong land market despite cost pressures

EPCs granted for new dwellings (England)

Band A Band B

+9.3% Band C Band D

Band E, F & G As a % of all housing tranactions

growth in

80,000 30%

greenfield land

values

(above 2008 peak in Despite a 70,000

25%

SE England)

+19.5% 60,000

cost increase 50,000

20%

in materials

(and +7.0% 40,000 15%

underlying rate of

+7.2% inflation) 30,000

10%

growth in 20,000

brownfield land 5%

values 10,000

0 0%

Year to March 2022

Source: DLUHC, HMRC, Savills 3

successive

interest votes for a

rate rises 0.50%

increase

votes for a

0.25% increase further rate

at the last MPC rises pencilled

in for this year

4

What that does to affordability?

The average household buying the average house

Interest payments Capital repayments Mortgage payments (stress tested)

40%

35%

30%

25%

20%

15%

10%

5%

0%

Q4 2007

Q4 2015

Q4 2002

Q4 2003

Q4 2004

Q4 2005

Q4 2006

Q4 2008

Q4 2009

Q4 2010

Q4 2011

Q4 2012

Q4 2013

Q4 2014

Q4 2016

Q4 2017

Q4 2018

Q4 2019

Q4 2020

Q4 2021

Q4 2022

Source: Savills using numerous sources 5

From a housing market perspective

Supply-demand but that will be

imbalance will tempered by and a squeeze

drive further pressure on on affordability

short-term price household at point of

growth incomes mortgage

…dependent on New build will

which will the extent to be better placed

curtail capacity which mortgage to meet lenders’

for price growth regulation is future EPC

from 2023.. relaxed demands

6

The role of mortgage regulation

SVR has

become

disconnected

from market

rates

Loan Income Responsible Mandatory

Don’t expect

Cap Lending Rules stress

an opening tests of

the mortgage

No more than 15% of Borrower affordability Affordability stress

credit

lending at over 4.5 x tested having regard to tested at 3% over SVR

Loan to Income market-expectations floodgates

unless the borrower has

over 5 years or +1.00% fixed for 5+ years More

borrowers

have locked

into 5-year

money

7

Price growth, pressure on household incomes & higher interest rates will have

the greatest impact on first time buyers

Challenges exacerbated by Help to Buy coming to an end (despite initiatives

such as First Homes and schemes such as Deposit unlock)

Some of that slack will be taken up by expanded shared ownership (provided

there remains an effective route to delivery)

But the ability to sell into an expanding and maturing Build to Rent market will

take on heightened importance for housebuilders

8

Help to Buy and what fills the gap

Help to Buy activity v average for month Low Cost Home Ownership

2017 - 2019 Help to Buy

Old Scheme New Scheme (FTBs & Value Caps) Deposit Unlock

200% First Homes

9,835

Shared Ownership (grant funded)

180%

185%

183%

Shared Ownership (Section 106)

160% 156% 8,788

140%

140%

7,422

135%

133%

129%

120%

121%

18,000

109%

100%

107%

105%

60%

92%

80%

5,124

57%

53,154

70%

60%

64%

61%

60%

40%

42%

41%

39%

35%

24,451

20%

21%

0%

Jul-20

Jul-21

Feb-20

Feb-21

Oct-20

Apr-20

Apr-21

Nov-20

Dec-20

May-20

Aug-20

Sep-20

May-21

Aug-21

Sep-21

Jun-20

Jan-20

Mar-20

Jan-21

Mar-21

Jun-21

3yrs to 2021 3yrs to 2026

(actual) (forecast)

Source: DLUHC, Savills 9

Build to Rent

Build to Rent

Average Annual Rolling Starts

size of 20,000

schemes 18,000

16,000

243 units

under 14,000

construction

+66% 12,000

Q on Q 10,000

140 units growth in

operational completed 8,000

single family

6,000

units

308 units 4,000

in planning 2,000

0

Q1 2015

Q1 2016

Q 2 2016

Q1 2017

Q1 2018

Q1 2019

Q1 2020

Q1 2021

Q1 2022

Q 2 2015

Q 2 2017

Q 2 2018

Q 2 2019

Q 2 2020

Q3 2020

Q 2 2021

Q3 2015

Q4 2015

Q3 2016

Q4 2016

Q3 2017

Q4 2017

Q3 2018

Q4 2018

Q3 2019

Q4 2019

Q4 2020

Q3 2021

Q4 2021

London Regions

Source: Savills Q1 2022 10A “challenging” policy environment

Increasing

Planning environmental

Levelling up & uncertainty & standards &

impact on local plan development

housing targets adoption constraints

section

Design codes,

build standards

and energy

efficiency

106

Delivery of

infrastructure &

affordable

housing

£ Financial

responsibility for

cladding

remediation

11The lost art of letter writing……

12A new broom sweeps through…..

13Levelling up focus… Source: Glenigan, DLUHC 14

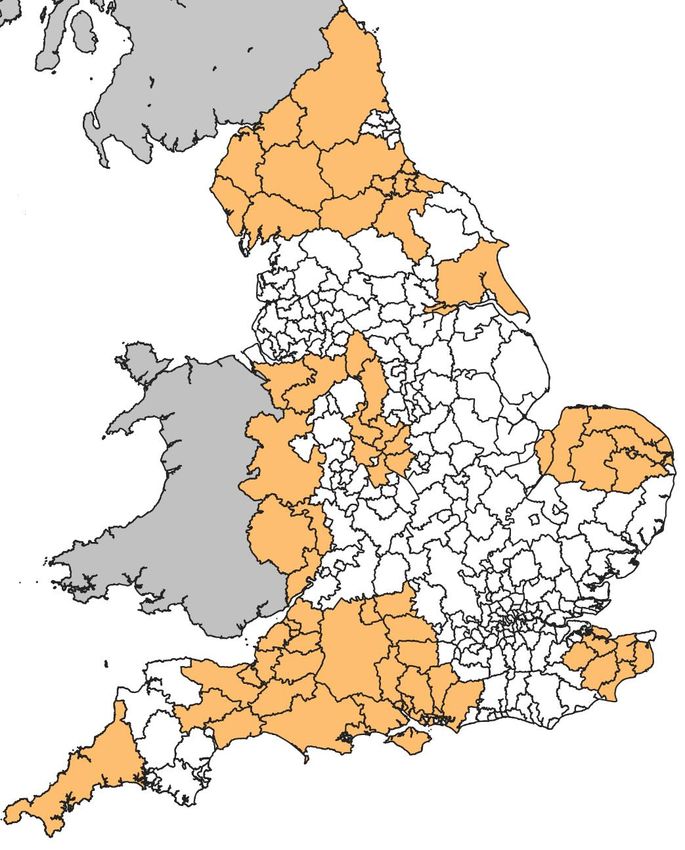

… leading to planning uncertainty

5-year land supply Local Plan Status

12 Local Plans

stalled in the

last 9 months

9LPAs cited lack of

national policy

clarity as reason to

pause

Source: Savills Research, DLUPHC 15First Homes: who will they work for?

Housebuilders Housing Residents

Weakened cashflow associations Higher deposit and income

Lower GDV Greater competition for S106 requirements

Greater difficulty competing More demand for land-led Lower monthly housing costs?

with logistics delivery Less choice overall

16Nutrient neutrality

74 LPAs

currently affected across the country

50% - 70% homes planned in these areas

could be at risk based on analysis in the south

17Build cost Future

annual Homes

inflation Standard

19.5% from 2025

+ £4,000 10% BNG

uplift from

per unit

2023

30%

beyond + £3,000-

£2,000 per

existing Part £5,000 per unit

L regulations unit

from 2022

18Developer tax: two taxes…

Paid when All

Building seeking residential Raising

Safety Levy planning

permission

development

activity

£3bn

For

Residential companies For UK res

Property Raising

with dev activities

Developer

Tax (RPDT) >£25m including £3bn

BTR

profit

Source: Savills Research 19Lack of planning policy clarity

Reduced Govt support for new build sales

Increased requirements for developers

Slower house price growth over the next 5 years

Leaving a less certain environment for housing future delivery

20Months in Office

0

10

20

30

40

50

60

70

Source: DHLUC

Pickles

All change?

Clark

Javid

Brokenshire

Jenrick

Gove

21Thank you

© Savills 2022

22You can also read