GLOBAL SUMMARY TELECOMMUNICATIONS - Week Commencing 15th March MAR 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

MAR 2021 GLOBAL SUMMARY TELECOMMUNICATIONS Week Commencing 15th March

Global Summary Telecommunications | 20210315

Contents

Global ................................................................................................................................................................................................. 4

Premium-Centric Markets Show Fastest Post-Covid Recoveries On Telecoms Index...................................................................................... 4

Africa.................................................................................................................................................................................................. 7

Quick View: E-Services, Tech-Intensive Businesses To Benefit From Botswana Data Centre ....................................................................... 7

Europe ............................................................................................................................................................................................... 9

Quick View: Israel FTTH Market Gains Momentum With Bezeq Launch................................................................................................................. 9

Middle East ....................................................................................................................................................................................11

Quick View: Israel FTTH Market Gains Momentum With Bezeq Launch................................................................................................................. 9

Quick View: Connected Car Project To Boost STC's 4IR Momentum ....................................................................................................................13

North America ..............................................................................................................................................................................15

Quick View: Rogers-Shaw Merger A Boon For 5G/IoT But Costly For Consumers ...........................................................................................15

© 20

2021

21 Fit

Fitch

ch Solutions Gr

Group

oup Limit

Limited.

ed. All rights rreserv

eserved.

ed.

All information, analysis, forecasts and data provided by Fitch Solutions Group Limited is for the exclusive use of subscribing persons or organisations (including those

using the service on a trial basis). All such content is copyrighted in the name of Fitch Solutions Group Limited and as such no part of this content may be reproduced,

repackaged, copied or redistributed without the express consent of Fitch Solutions Group Limited.

All content, including forecasts, analysis and opinion, has been based on information and sources believed to be accurate and reliable at the time of publishing. Fitch

Solutions Group Limited makes no representation of warranty of any kind as to the accuracy or completeness of any information provided, and accepts no liability

whatsoever for any loss or damage resulting from opinion, errors, inaccuracies or omissions affecting any part of the content.

This report from Fitch Solutions Country Risk & Industry Research is a product of Fitch Solutions Group Ltd, UK Company registration number 08789939 (‘FSG’). FSG is an

affiliate of Fitch Ratings Inc. (‘Fitch Ratings’). FSG is solely responsible for the content of this report, without any input from Fitch Ratings. Copyright © 2021 Fitch Solutions

Group Limited.

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

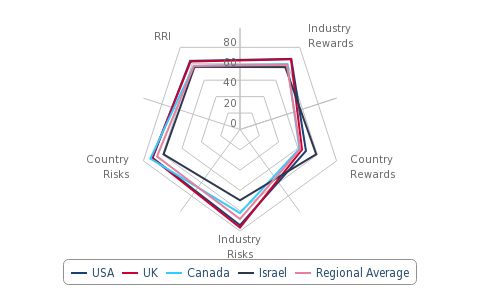

fitchsolutions.com 3Global Summary Telecommunications | 20210315 Global Premium-Centric Markets Show Fastest Post-Covid Recoveries On Telecoms Index Key View • The average score for the 10 Developed Markets we survey as part of our Risk/Reward Index improved by 0.2 points to 77.2 out of 100. • Fourth-quarter 2020 data had not been reported for all markets at the time the Index was refreshed, meaning that assessments continued to be weighed down by the Covid-19 pandemic on global supply chains and consumer spending attitudes. • All 10 of the markets surveyed were impacted most in the mobile and pay-TV segments, while fixed broadband also took a hit to a certain extent. Full-year data will likely show an improved outlook as physical retail channels re-opened and new flagship smartphones - such as Apple's first 5G devices - were launched, boosting mobile subscription growth rates. However, highly saturated markets such as Japan and markets where disposable incomes are likely to remain constrained due to high unemployment rates and slower economic recoveries amid third- and fourth-wave Covid-19 breakouts, will not improve to the same degree. It will be interesting, too, to see whether the traditional pay-TV business will rebound, as the loss of sporting coverage during the pandemic forced consumers onto alternative, streaming-based platforms, from which they may not return. This is an issue for all 10 of our Developed Markets, which have a high penetration rate of linear cable and satellite TV services. The United States has outperformed in this quarter's update, increasing its overall score by 1.2 points to reach 83.5 out of a potential 100 points. The country benefits from 1.1-point improvement in its Country Risks profile, with the transition to a Democrat-led government promising a more balanced approach to domestic and international politics and economic relations after the inward-looking and abrasive approach favoured by the departing Republican regime. The new government does have its work cut out, however, dealing with very high unemployment rates and a still-growing Covid-19 infection rate that the new range of vaccinations will not be able to curb in the short term. There is also little sign, so far, of the new administration easing off on the economic pressure being applied on China, a country that remains at the centre of the global technology supply chain, so further improvements to the Country Risks score are likely to be less pronounced in the coming quarters. The US also sees a 2.2-point increase to its Industry Rewards score, to 85.9 points, as Q3 and preliminary Q4 data showed a strong resurgence on mobile subscriptions, mostly in the postpaid/contract arena. Some of that growth will have been driven by iPhone upgrades, but we believe many consumers and businesses that had relied on low-cost prepaid plans are now shifting to postpaid given the need for more robust data packages in a work-from-home environment that is unlikely to disappear post-Covid. Canada is the other outperformer, seeing its overall RRI score improve by 0.7 points to 77.5. There is a 0.7-point increase to its Country Risks score, linked to a marked thawing in its political and economic relations with the US, its closest neighbour and principal trading partner, again linked to the change in government in the US. More significant, however, is the 1.5-point improvement in Canada's Industry Rewards score, with Q3 data showing a marked recovery in subscriber growth after the initial wave of Covid-19-driven lockdowns and supply chain disruptions. The availability of the new iPhones in Q4 will ensure that this upward momentum continues. In Canada and the US, while pay-TV-dependent telcos were hit by customer migration from their linear TV services, they at least benefited from increased traffic flowing over their networks and greater usage of broadband services in general, particularly for entertainment and productivity purposes, and this has helped push fibre connection uptake rates to faster than those previously envisaged. THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research. fitchsolutions.com 4

Global Summary Telecommunications | 20210315

Most Mature Markets Recovering Quickly

Selected Developed Markets Telecoms RRIs, Q221

Note: Scores out of 100, with high scores denoting low risk. Source: Fitch Solutions

Canada overtakes Germany to become the fifth most attractive Developed Market, its improved scores easing it just ahead of the

European industrial powerhouse, which itself sees no notable score changes this quarter. This is not to say that Germany has

performed poorly; rather, it is the case that the country moved in the directions and at the pace we had been expecting and the

relatively slow vaccine distribution programme will likely hold the country back in the short to medium term.

Israel, by contrast, has outperformed in terms of its vaccination drive, with one of the highest inoculation rates in the world at the

time of writing. This will help the country's economic recovery, relative to its peers, as it is a tech innovation hub in the Middle East

but depends highly on uninterrupted trade and distribution flows for success. Its telecoms market, however, is a different matter

altogether: power is concentrated among three key providers, all of whom compete aggressively for control over a very small

addressable market, with price competition exacerbated by the presence of a large number of sub-brand, discount and specialised

players.

Israel's Rewards profile is not much changed since last quarter, with the short-term boost in broadband usage providing a small

degree of uplift in this quarter's update. There is, however, a one-point increase to Israel's Country Risks score as lines of

communication between Israel and some of its neighbours reopened in light of a Trump government-brokered accord. That

agreement is based on a very tenuous understanding concerning economic stability, but the political risks remain elevated and the

accord may not prove to be long-lasting. The long-term outcome will not have much impact on the relatively unattractive nature of

the Israeli telecoms market and there are few opportunities for new and/or foreign investors in this relatively closed ecosystem.

DEVELOPED MARKETS TELECOMMUNICATIONS RISK/REWARD INDEX, Q2 2021

Industry Country Industry Country Regional Global

REWARDS RISKS RRI

Rewards Rewards Risks Risks Rank Rank

USA 85.9 68.3 79.7 94.2 90.5 92.3 83.5 1 1

UK 85.4 64.2 77.9 96.6 91.0 93.8 82.7 2 2

France 81.2 63.3 75.0 91.6 86.2 88.9 79.1 3 5

Australia 74.3 68.7 72.3 92.1 87.5 89.8 77.6 4 7

Canada 79.5 61.5 73.2 82.3 92.8 87.6 77.5 5 8

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 5Global Summary Telecommunications | 20210315

Industry Country Industry Country Regional Global

REWARDS RISKS RRI

Rewards Rewards Risks Risks Rank Rank

Germany 78.1 55.9 70.3 91.6 93.1 92.4 76.9 6 12

Israel 75.9 78.9 77.0 69.7 79.1 74.4 76.2 7 14

Spain 83.1 55.1 73.3 85.8 76.7 81.3 75.7 8 15

Japan 74.7 59.3 69.3 85.8 87.7 86.8 74.6 9 20

Italy 67.7 49.6 61.3 91.6 74.0 82.8 67.8 10 36

Regional

78.6 62.5 72.9 88.1 85.9 87.0 77.2 - -

Aver

erage

age

Global A

Avver

erage

age 50.0 50.0 50.0 50.0 50.0 50.0 50.0 - -

Note: Scores out of 100; higher score = lower risk. Source: Fitch Solutions' Telecommunications Risk/Reward Index

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 6Global Summary Telecommunications | 20210315 Africa Quick View: E-Services, Tech-Intensive Businesses To Benefit From Botswana Data Centre The Latest: State-owned Botswana Fibre Networks (BoFiNet) is building a Tier III+ data centre in the capital Gaborone. Set for completion in late 2021, it will host at least 400 racks in 1,000 square metres of white space, making it the country’s largest data centre. Implications: BoFiNet is investing to meet growing demand for enterprise and consumer cloud services and applications, areas where only private players - including SEACOM and Liquid Telecom - have been investing so far. To date, the state has invested mainly in the development of backbone infrastructure, including international cable systems, including access to the East and West Africa Cable Systems. The wholesale fibre service provider will leverage its 9,200km fibre footprint to augment its data hosting offering. The government will be a key beneficiary of the data centre as it pursues its 11th National Development Plan 2017-2023, focused on increasing capital spending on key projects including boosting technology infrastructure deployment and ICT services adoption. Under the plan the government has committed resources for the implementation of e-Government, e-Health, e-Education and e- Commerce services. We anticipate an acceleration in cloud migration in order to generate efficiencies in public service delivery and operations, as well as to underpin new e-government services. Within the plan, the Smart Botswana initiative targets the use of disruptive technologies to improve transportation, logistics and security. However, deeper opportunities exist for the integration of technologies such the Internet of Things, Artificial Intelligence and even 5G-powered applications targeting more efficient use of resources such as water, electricity and urban spaces. The country's first smart city, Kgale Lake City (construction of which began in 2018), will serve as a key testbed for these technologies. Meanwhile, in the private sector, increased cloud migration from large enterprises is also a lucrative proposition for BoFiNet. We believe prospects are strongest in more technologically intensive verticals such as financial services, ICT, manufacturing and logistics. THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research. fitchsolutions.com 7

Global Summary Telecommunications | 20210315

BoFiNet Seeking A Larger Slice Of The Market

Middle East And Africa: Cloud Spending (USDmn), 2020-2024

e/f = Fitch Solutions estimate/forecast. Source: Fitch Solutions

Upsides for stronger uptake of IT solutions and services from this base are posed by the country’s strong economic outlook, and

Botswana’s growing appeal as a business-friendly investment destination. Our Country Risk team expects that Botswana's GDP will

recover by 5.1% in real terms in 2021 after an estimated 8% contraction in 2020. That said, we anticipate limited adoption of cloud

solutions among small firms in the short to medium term, as many businesses currently have very low utilisation of technology

beyond basic services and applications.

What’s Next: Through the launch of its data centre, BoFiNet will look to market its data hosting capabilities to more firms in the

region to boost its revenues. Fitch Solutions believes the Middle East and Sub-Saharan African cloud computing market will be

worth USD2.42bn in 2021, rising to USD6.46bn by 2024.

However, the operator will face strong competition from neighbouring South Africa which has long been the region’s data centre

hub, hosting a range of local, regional and global players. In 2019 Microsoft and Amazon Web Services built data centres in the

country to serve both local data demand as well as the wider region. We believe that over the near term, relatively expensive

Internet costs and deep power deficits may dim the appeal of BoFiNet’s offering.

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 8Global Summary Telecommunications | 20210315

Europe

Quick View: Israel FTTH Market Gains Momentum With Bezeq Launch

The Latest: Israel’s incumbent telecoms operator, Bezeq, has launched its Fibre-to-the-Home (FTTH) service. Bezeq aims to

cover 40% of households nationwide by the end of 2021 and calls its offering as ‘Israel’s largest infrastructure project’. Bezeq's move

to commercialisation of FTTH is particularly significant after years of disagreement with the Ministry of Communications (MoC)

over coverage terms.

Implications: Bezeq becomes the latest operator in Israel to offer FTTH services: rival operators began deploying fibre networks in

order to compete with the incumbent’s monopoly on traditional fixed line infrastructure, but seem to have made little progress

while their mobile broadband services remain competitively priced. However, Bezeq is responding to strengthening competition in

the fibre market from the Israel Broadband Company (IBC) and Partner. In January 2021, the MoC approved Hot Telecom's

investment in the IBC, in which it joined Cellcom with a 23.3% stake in the consortium.

Partner took the opportunity of Bezeq's announcement to report it was already providing FTTH services to 150,000 customers. This

is the first time it has disclosed actual customer numbers and this reinforces our view that the pace of its rollout has been slow,

hence its decision to seek an investor to buy a 20% stake in its fibre business.

As of Q320, Bezeq supplied 1.5mn customers with broadband services over its traditional copper network, meaning that it has a

sizeable user base to persuade to upgrade to faster fibre. However, Bezeq notes that its FTTH prices would be higher than those of

its competitors and that it would charge installation fees, in contrast to Partner and Cellcom. This could lead to Bezeq’s offering

being disregarded by many customers, but may also drive up average revenue per-user (ARPU) levels as the other operators may

take the opportunity to increase their prices.

Bezeq's Monopoly Still Evident

Wireline Market Shares, Q220 (%)

Regulator, Operators, Fitch Solutions

Israel’s adoption of high-speed internet access has been very slow, so far, largely hindered by Bezeq's monopoly on the sector

stalling development and competition, but not helped by the low cost of mobile data and broadband services. Disagreements

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 9Global Summary Telecommunications | 20210315

between Bezeq and the MoC over the scale of fibre rollout have also hampered progress; as the incumbent, Bezeq has coverage

and service quality obligations that its mobile-first rivals do not.

On the upside, the Covid-19 pandemic has added urgency to the deployment of high-speed internet capability after a massive

surge in demand precipitated by remote work and education. Thus, Israel’s MoC has made fibre development a priority. We suspect

that that Bezeq's offering, as well as HOT's acquisition of a stake in IBC will provide much-needed competition to Israel's fibre

segment, finally providing a catalyst for mass uptake.

What’s Next: As a result of growing momentum in Israel's fibre broadband market, we have revised upwards our forecast for the

fixed broadband market over the medium term. However, we believe that Israel will continue to lag behind its neighbours in terms of

fibre offering, particularly due to the advent of 5G offering even faster mobile broadband connectivity whilst still being cheaper than

a fibre internet package. Deployment of fibre is massively capital intensive, and incumbent operator Bezeq has already been in

disagreement with the government over its ability to meet the rollout demands of the MoC, claiming it is not financially suitable to

do so. Opening up to external investors - as its rivals have done - is an option, but there are no other independent players in the

market at present and the closed nature of that market will deter foreign investors.

Wireline Forecasts

Israel - Wireline Voice & Broadband Subscriptions (2020-2030)

e/f = Fitch Solutions estimate/forecast. Source: Operators, Fitch Solutions

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 10Global Summary Telecommunications | 20210315

Middle East

Quick View: Israel FTTH Market Gains Momentum With Bezeq Launch

The Latest: Israel’s incumbent telecoms operator, Bezeq, has launched its Fibre-to-the-Home (FTTH) service. Bezeq aims to

cover 40% of households nationwide by the end of 2021 and calls its offering as ‘Israel’s largest infrastructure project’. Bezeq's move

to commercialisation of FTTH is particularly significant after years of disagreement with the Ministry of Communications (MoC)

over coverage terms.

Implications: Bezeq becomes the latest operator in Israel to offer FTTH services: rival operators began deploying fibre networks in

order to compete with the incumbent’s monopoly on traditional fixed line infrastructure, but seem to have made little progress

while their mobile broadband services remain competitively priced. However, Bezeq is responding to strengthening competition in

the fibre market from the Israel Broadband Company (IBC) and Partner. In January 2021, the MoC approved Hot Telecom's

investment in the IBC, in which it joined Cellcom with a 23.3% stake in the consortium.

Partner took the opportunity of Bezeq's announcement to report it was already providing FTTH services to 150,000 customers. This

is the first time it has disclosed actual customer numbers and this reinforces our view that the pace of its rollout has been slow,

hence its decision to seek an investor to buy a 20% stake in its fibre business.

As of Q320, Bezeq supplied 1.5mn customers with broadband services over its traditional copper network, meaning that it has a

sizeable user base to persuade to upgrade to faster fibre. However, Bezeq notes that its FTTH prices would be higher than those of

its competitors and that it would charge installation fees, in contrast to Partner and Cellcom. This could lead to Bezeq’s offering

being disregarded by many customers, but may also drive up average revenue per-user (ARPU) levels as the other operators may

take the opportunity to increase their prices.

Bezeq's Monopoly Still Evident

Wireline Market Shares, Q220 (%)

Regulator, Operators, Fitch Solutions

Israel’s adoption of high-speed internet access has been very slow, so far, largely hindered by Bezeq's monopoly on the sector

stalling development and competition, but not helped by the low cost of mobile data and broadband services. Disagreements

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 11Global Summary Telecommunications | 20210315

between Bezeq and the MoC over the scale of fibre rollout have also hampered progress; as the incumbent, Bezeq has coverage

and service quality obligations that its mobile-first rivals do not.

On the upside, the Covid-19 pandemic has added urgency to the deployment of high-speed internet capability after a massive

surge in demand precipitated by remote work and education. Thus, Israel’s MoC has made fibre development a priority. We suspect

that that Bezeq's offering, as well as HOT's acquisition of a stake in IBC will provide much-needed competition to Israel's fibre

segment, finally providing a catalyst for mass uptake.

What’s Next: As a result of growing momentum in Israel's fibre broadband market, we have revised upwards our forecast for the

fixed broadband market over the medium term. However, we believe that Israel will continue to lag behind its neighbours in terms of

fibre offering, particularly due to the advent of 5G offering even faster mobile broadband connectivity whilst still being cheaper than

a fibre internet package. Deployment of fibre is massively capital intensive, and incumbent operator Bezeq has already been in

disagreement with the government over its ability to meet the rollout demands of the MoC, claiming it is not financially suitable to

do so. Opening up to external investors - as its rivals have done - is an option, but there are no other independent players in the

market at present and the closed nature of that market will deter foreign investors.

Wireline Forecasts

Israel - Wireline Voice & Broadband Subscriptions (2020-2030)

e/f = Fitch Solutions estimate/forecast. Source: Operators, Fitch Solutions

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 12Global Summary Telecommunications | 20210315

Quick View: Connected Car Project To Boost STC's 4IR Momentum

The Latest: Saudi Telecommunications Company (STC) has announced a partnership with Cubic Telecom, a leading

provider of connected vehicle software.

Implications: STC and Cubic Telecom aim to make connected cars a mass-market proposition in Saudi Arabia. Cubic Telecom’s

software can be installed at the point of manufacture and can be pre-configured to meet the regulatory

requirements of the region, reducing time-to-market for any car manufacturer aiming to extract additional value

from the country's massive autos market. The project aligns with the Saudi Vision 2030, which aims to digitalise and

diversify the economy away from the hydrocarbon sector and pioneer emerging Industry 4.0 technologies.

Notably, the Saudi Vision 2030 focuses on ‘people safety’, intending to reduce the number of road traffic accidents in the Kingdom.

One of the services being worked on by the partnership is an ‘emergency call’ button, which would automatically call emergency

services in the event of an accident. Artificial intelligence (AI) technology and advanced data analytics provided by STC can be used

to assess driver behaviour, alerting the driver to potential dangers.

The venture also meets the requirements of STC's own digitalisation strategy, DARE, particularly its second phase directed towards

facilitating digital transformation in sectors other than telecommunications.

Connected cars would become part of a wider Internet of Things (IoT) ecosystem by leveraging STC’s extensive mobile network,

as well as its new digital operations control centre, opened in March 2021 and tasked with supporting STC's growing digital projects

business. As Saudi Arabia plans to create the Middle East’s largest 5G network - utilising around 10,000 base stations to give 5G

access to 71 cities - the partnership has commercial as well as societal upsides.

5G Capabilities Drive Capex Spending

Capex By Operator (SARbn) 2017-2020

Source: Operators, Fitch Solutions

Investing in projects such as this serves to diversify STC’s revenues, meaning the operator can rely less on low-margin traditional

mobile services and tap into greater revenue streams such as advanced data services.

What’s Next: Continual deployment of telecoms infrastructure and projects such as this one with Cubic Telecom are capital

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 13Global Summary Telecommunications | 20210315

intensive and require sustained proficiency, particularly in providing efficient security. The IoT poses significant cybersecurity risks: at

the heart of our long-term view for digital ecosystems is the notable risk that anything connected can be hacked. Therefore,

operators will need to invest in robust cybersecurity infrastructure that promises business continuity and user safety.

STC has demonstrated early commitment and success in offering cybersecurity, both with the creation of the 'Advanced

Technology and Cybersecurity Company' under the STC Solutions arm of the business and in providing cybersecurity protection

during the G20 Riyadh Summit in 2020. STC is considering an Initial Public Offering (IPO) that would list shares of its Solutions arm

on the Saudi Stock Exchange. An IPO would give Solutions access to a large pool of investment capital to continue enhancing its

Industry 4.0 offerings, while increased transparency and regulatory oversight from a listing would encourage more partners to work

with the company.

Growing IT Market Drives Demand For Cybersecurity Solutions

Saudi Arabia IT Market Forecast (2019-2025)

e/f = Fitch Solutions estimate/forecast. Source: Fitch Solutions

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 14Global Summary Telecommunications | 20210315 North America Quick View: Rogers-Shaw Merger A Boon For 5G/IoT But Costly For Consumers The Latest: Rogers Communications has agreed to buy Shaw Communications in a deal valued at CAD26bn (USD20.8bn). Implications: Concentration of power in the fixed broadband and mobile services markets, plus the loss of a distinctive budget mobile brand will be the main regulatory arguments against the transaction, but faster 5G/IoT rollout, increased rural commitments and lower costs to consumers could secure approval. Rogers would invest CAD2.5bn to deploy 5G infrastructure across Western Canada over a five-year period, targeting more cities and rural areas than it or Shaw would have been able to commit to servicing independently, and sooner. A further CAD1bn would be spent on improving Internet connectivity in rural areas and locations hosting indigenous communities, a key target for regulators, while CAD3bn would be spent on 'additional networks, services and technology' needs of consumers and businesses, such as IoT. There is also a commitment to preserving jobs, upskilling some segments of the workforce and creating new jobs. Industry and competition regulators would, however, need to weigh the promises made by Rogers against the impact of increased market power the enlarged Rogers would enjoy. The main issue would be in the mobile arena, where Shaw's Freedom Mobile and Shaw Mobile businesses would become part of the Rogers Mobile portfolio. Freedom would add 5% of the national market to give Rogers a clear lead with a 36% share, leaving Telus and BCE with just under 30% apiece, so the arguments against the deal would not necessarily focus on market share, but rather the impact on pricing and consumer choice. Significantly, the move would draw a line under long-standing efforts to improve consumer choice and drive down prices: in its previous incarnation as WIND, Freedom had succeeded in forcing Rogers, Telus and BCE to become more price competitive and innovative. Some impetus was lost after WIND - the sole survivor of a quartet of new players - was sold to Shaw, and despite Rogers' insistence that it will not alter pricing plans for three years, it is likely that the brand would eventually be de-emphasised, given Rogers' focus on premium TV- and broadband-centric service packages. Spectrum ownership could also be an issue, as Freedom's rights in the 700MHz, 1700MHz and 2600MHz band would complement Rogers' holdings in those same bands, potentially giving it greater capacity than its rivals. Excess spectrum could be clawed back and given to a new entrant, but that seems unlikely given the failure of the mobile market expansion drive; giving excess spectrum to Telus and BCE is another possibility, but the overall impact would merely concentrate all three players' power. Shaw's fixed broadband business leverages its cable TV infrastructure in British Columbia and Alberta, where it trails slightly behind market leader Telus. As Rogers has a limited presence in Western Canada, market positions would not alter significantly, but merger costs and infrastructure upgrades could drive up basic costs to consumers, while a more aggressive multi-play drive by Rogers could see prices increase over the longer term. THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research. fitchsolutions.com 15

Global Summary Telecommunications | 20210315

ARPUs Still Rising, Driven By Data Usage

Canada Mobile Usage Metrics, 2014-2019

Source: CRTC

What's Next: The deal will need to be scrutinised by several regulatory agencies, including the Canadian Radio-Television

Commission (CRTC), the Competition Bureau and Innovation, Science & Economic Development Canada (ISED). Rogers has set a

mid-2022 completion date for the merger.

While we believe the merger will go through, strict conditions will be set on coverage, quality of service, price freezes/reductions

and asset redistribution, as outlined above. In the medium term, we believe duplicated passive infrastructure carve-outs (towers,

data centres, wireline networks) will be attempted, creating some investment opportunities for niche players, while longer-term

possibilities include the creation of dedicated IoT connectivity and services businesses that could go on to become standalone

entities. That said, the Canadian telecoms sector lags Europe and Asia with regards to the industry's ongoing transition to an

Operator-as-a-Service business paradigm, so those opportunities are likely to remain distant for the foreseeable future.

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 16You can also read