Fresno County Employees' Retirement Association (FCERA) - May 2021 - County of ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Fresno County Employees’ Retirement Association (FCERA)

May 2021

www.aksia.com

Aksia Presenting Team

Jim Vos

Partner, CEO

Patrick Adelsbach

Partner, Head of Credit Strategies

Tim Nest, CFA

Managing Director, Head of Private Credit Research

Lynn O’Connell, CAIA

Portfolio Advisor

2

Aksia – At A Glance

$240bn+ 316

of AUA1 Professionals2

Client Centric

Business

Model

90+ >3,000

Institutional Clients1 Integrated Due Diligence Reports3

Founded in

2006 Front-to-Back

Approach

$10bn+ 3.1

of AUM1 Staff to Client Ratio1

100% Employee 7 Offices

Owned Globally

All references to Aksia herein refer to Aksia LLC, together with its wholly owned subsidiaries (collectively, “Aksia”)

1As February 28, 2021. Total AUA (inclusive of AUM) is defined as NAV plus unfunded commitments. Represents investments currently tracked and

monitored by Aksia’s Client Operations team. AUM includes fully discretionary accounts or accounts where the client retains veto authority

2As of March 31, 2021

3As of December 31, 2020 3

Our Professionals

Team Size Aksia Professionals' Average Industry Experience (Years)

ODD & Risk

35

Investment

76

Research,

Investment Research1 Senior, 17.5 professionals

Total, 7.3

Operational Due

55 23

Advisory &

Operations

Diligence1

Portfolio

Senior, 20.2

Client

professionals

Total, 8.1

Risk Management 26

Legal, IT, &

Senior, 15.0 12

Admin

professionals

Total, 10.1

Portfolio Advisory 43

0.0 5.0 10.0 15.0 20.0

Client Operations 64

Headcount by Function Type

Legal & Compliance 10

Information Technology 19 34% 16% 50%

Administration 23 Legal, IT, Investment Research,

Portfolio Advisory

& Client Operations & Admin ODD & Risk

316

As of March 31, 2021

1Of the 76 Investment Research professionals, 23 spend some or all of their time covering Private Credit strategies as well as 3 members of the relevant

investment committee or the investment research team specialized in niche strategies that can be expressed through Private Credit vehicles.

Operational Due Diligence professionals are generalists and cover all asset classes

4

Private Credit Team Resources

26 Investment Research Professionals

Patrick Adelsbach, Partner Tim Nest, Managing Director

Head of Credit Strategies Head of Private Credit Research

23+ years of experience 21+ years of experience Supporting Resources

Mike Krems, Partner Simon Fludgate, Partner

Dan Krivinskas, Partner1

Head of Co-Investments Head of Operational Due Diligence

Head of Real Estate Research

18+ years of experience 18+ years of experience Kara King, Partner

Head of Client Operations & Risk Management

Joshua Hemley, Managing Director Maiko Nanao, Managing Director

Co-Investments Investment Research, Asia Steve Beckett

12+ years of experience 21+ years of experience Head of Private Markets Risk

+

Brian Goldberg, Managing Director1 Leo Fletcher-Smith, Senior Vice President

Event Driven & Multi-Strategy European Private Credit Strategy Head ▪ 54 Operational Due Diligence

14+ years of experience 14+ years of experience ▪ 14 Risk Management

▪ 57 Client Operations

Kevin Hitchen, Senior Vice President1 Antonis Antypas, Global Head of Analytics

Head of Large Cap Buyouts 12+ years of experience

12+ years of experience

Ping Xu, Head of Hong Kong Office Filip Malaric, Vice President

17+ years of experience 7+ years of experience

Ilya Riskin, Vice President

15+ years of experience

5 Senior Associates | 4 Associates | 4 Analysts

As of March 31, 2021. Includes Investment Research, Risk Management and Client Operations professionals that spend some or all of their time

covering Private Credit strategies as well as members of the relevant investment committee or the investment research team specialized in niche

strategies that can be expressed through Private Credit vehicles (noted with “1”). Operational Due Diligence professionals are generalists and cover all

5

asset classes.

Aksia Private Credit

Key Aksia Private Credit Statistics

$59bn in Total AUA Due Diligence on >600 PC 26 Investment Research 85+ PC

$5bn AUM1 Opportunities2 Professionals Sub-strategies

Client Investments in >55% Fund Size 200 Unique GPs1 >50% Global or Outside US2 Professionals Sourced LTM3

▪ Active in the Private Credit asset class since 2010

Seasoned Credit Team ▪ Deep credit research coverage and local presence across the global markets

▪ Synergies across public and private markets activities

▪ Proactive opportunistic idea generation

Thematic Approach ▪ Market and deal insights enhanced through broader platform relationships

▪ Global network of LPs, GPs, intermediaries

Deep Sourcing Channels ▪ Activities in PE, RA, RE and HF further complement credit sourcing efforts and market insights

▪ Proprietary tech platform houses information on over 2,900 private credit opportunities

▪ Anchor/seed deals, primaries, SMAs, dislocation vehicles, co-investments and secondaries

Flexible Capital Base

▪ Increasingly active managing credit-focused customized separate account mandates

1As of February 28, 2021

2As of December 31, 2020

3As of March 31, 2021. Based on initial communications with Managers. Includes deal flow from Aksia LLC and Aksia TorreyCove Capital Partners prior to the combination of

the businesses on March 31, 2020. Approximately $58mm has been invested in the last twelve months preceding September 30, 2020 6

Private Credit Coverage

DISTRESSED

DIRECT LENDING SPECIALTY FINANCE STRUCTURED CREDIT REAL ESTATE CREDIT REAL ASSETS CREDIT

& SPECIAL SITUATIONS

U.S. Direct Lending Corporate Distressed Consumer & SME Lending CLO U.S. CRE Core Lending Infrastructure Lending

Senior Stress / Distressed Trading Marketplace Finance CLO Debt U.S. CRE Core Lending Senior Focus

Opportunistic Influence / Control Lender/Platform Finance CLO Multi Sub-IG Focus

LMM (sponsored) Diversified Distressed Captive CLO Equity U.S. CRE Transitional Mezz Focus

LMM (non-sponsored) Factoring & Receivables 3rd Party CLO Equity Lending

Private BDCs Real Estate Distressed Factoring & Receivables Large Loan Energy Credit

Industry Focused Real Estate Distressed CRE Middle Market Energy Lending

Regulatory Capital Relief Non-Agency CRE B-Piece Small Balance Energy Mezzanine Lending

Revolvers

NPLs Regulatory Capital Relief Agency CRE B-Piece Opportunistic Opportunistic

European Direct Lending NPLs CMBS/CRE

Healthcare Royalties U.S. CRE Bridge Lending Trade Finance

Senior

Opportunistic Capital Solutions Healthcare Royalties RMBS Large Loan Trade Finance

Capital Solutions RMBS Middle Market

Lower Middle Market Music/Film/Media

Country-Specific Funds Small Balance Metals & Mining Finance

PC Special Situations Royalties Consumer ABS Metals & Mining Finance

Emerging Markets Lending PC Special Situations Music/Film/Media Consumer ABS European CRE Lending

Royalties Bridge Agricultural Credit

Asian

PE Special Situations Esoteric ABS Transitional Agricultural Credit

African

PE Special Situations Oil & Gas Minerals Esoteric ABS Core

CEE/Middle East Transportation

Latin American Royalties

Distressed-for-Control Oil & Gas Minerals Europe Structured Credit EM CRE Lending Aviation Lending

Pan-EM European Structured Credit Maritime Lending

Distressed-for-Control Royalties EM CRE Lending

Road & Rail Lending

Global Direct Lending Structured Credit Multi-

Global Metals Royalties Residential Mortgages Transportation Lending

Metals Royalties Sector Residential NPLs (Multi)

Structured Credit Multi- Single Family Rental

Healthcare Lending Sector Mortgage Servicing Rights

MEZZANINE Healthcare Lending Residential Origination

Venture Lending

U.S. Mezzanine Venture Lending

Upper Middle Market

Middle Market Insurance Linked Credit

Lower Middle Market Diversified

Life Insurance

European Mezzanine Non-Life Insurance

European Mezzanine

Litigation Finance

Structured Equity Litigation Finance

Structured Equity

Merger Appraisal Rights

Merger Appraisal Rights

PE Portfolio Finance

PE Portfolio Finance 7

Private Credit Coverage – Three Main Areas

DISTRESSED

DIRECT LENDING SPECIALTY FINANCE STRUCTURED CREDIT REAL ESTATE CREDIT REAL ASSETS CREDIT

& SPECIAL SITUATIONS

U.S. Direct Lending Corporate Distressed Consumer & SME Lending CLO U.S. CRE Core Lending Infrastructure Lending

Senior Stress / Distressed Trading Marketplace Finance CLO Debt U.S. CRE Core Lending Senior Focus

Opportunistic Influence / Control Lender/Platform Finance CLO Multi Sub-IG Focus

LMM (sponsored) Diversified Distressed Captive CLO Equity U.S. CRE Transitional Mezz Focus

LMM (non-sponsored) Factoring & Receivables 3rd Party CLO Equity Lending

Private BDCs Real Estate Distressed Factoring & Receivables Large Loan Energy Credit

Industry Focused Real Estate Distressed

Regulatory Capital Relief

Cash Flow

CRE

Non-Agency CRE B-Piece

Middle Market

Small Balance

Energy Lending

Energy Mezzanine Lending

Revolvers

NPLs Regulatory Capital Relief Agency CRE B-Piece Opportunistic Opportunistic

European Direct Lending NPLs CMBS/CRE

Healthcare Royalties

Senior

Distressed Healthcare Royalties RMBS

U.S. CRE Bridge Lending Trade Finance

Cash Flow

Opportunistic

Lower Middle Market

Capital Solutions

Capital Solutions

Music/Film/Media

RMBS

Large Loan

Asset-

Middle Market

Trade Finance

Asset-Based

Country-Specific Funds Small Balance Metals & Mining Finance

PC Special Situations Royalties Consumer ABS

Based

Metals & Mining Finance

Emerging Markets Lending PC Special Situations Music/Film/Media Consumer ABS European CRE Lending

Royalties Bridge Agricultural Credit

Asian

PE Special Situations Esoteric ABS Transitional Agricultural Credit

African

PE Special Situations Oil & Gas Minerals Esoteric ABS Core

CEE/Middle East

Latin American

Distressed-for-Control

Royalties Asset-Based

Europe Structured Credit EM CRE Lending

Transportation

Aviation Lending

Pan-EM Oil & Gas Minerals

Distressed-for-Control Royalties European Structured Credit EM CRE Lending Maritime Lending

Global Direct Lending Cash Flow

Metals Royalties Structured Credit Multi- Residential Mortgages

Road & Rail Lending

Transportation Lending

Global

Metals Royalties Sector Residential NPLs (Multi)

Structured Credit Multi- Single Family Rental

Healthcare Lending Sector Mortgage Servicing Rights

MEZZANINE Healthcare Lending Residential Origination

Venture Lending

U.S. Mezzanine Venture Lending ▪ Cash Flow – lending strategies that primarily rely on cash generation from

Upper Middle Market

Middle Market Insurance Linked Credit ongoing company operations as collateral

Lower Middle Market Diversified

▪ Asset-Based – lending strategies that primarily target hard assets as collateral

Cash Flow

European Mezzanine

Life Insurance

Non-Life Insurance

▪ Distressed – strategies focused on buying in the secondary markets at a discount

European Mezzanine

Litigation Finance to intrinsic value (i.e., investor returns driven by capital gains rather than yield)

Structured Equity Litigation Finance

Structured Equity

Merger Appraisal Rights

Merger Appraisal Rights

PE Portfolio Finance

PE Portfolio Finance 8

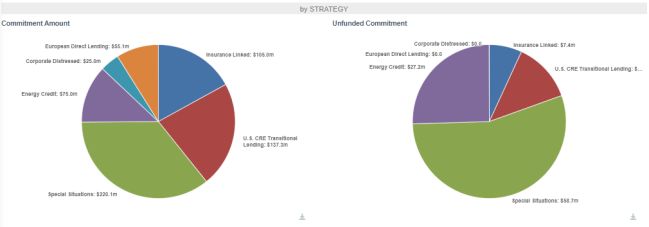

FCERA Private Credit Exposure

DISTRESSED

DIRECT LENDING SPECIALTY FINANCE STRUCTURED CREDIT REAL ESTATE CREDIT REAL ASSETS CREDIT

& SPECIAL SITUATIONS

U.S. Direct Lending Corporate Distressed Consumer & SME Lending CLO U.S. CRE Core Lending Infrastructure Lending

Senior Stress / Distressed Trading Marketplace Finance CLO Debt U.S. CRE Core Lending Senior Focus

Opportunistic Influence / Control Lender/Platform Finance CLO Multi Sub-IG Focus

LMM (sponsored) Diversified Distressed Captive CLO Equity U.S. CRE Transitional Mezz Focus

LMM (non-sponsored) Factoring & Receivables 3rd Party CLO Equity Lending

Private BDCs Real Estate Distressed Factoring & Receivables Large Loan Energy Credit

Industry Focused Real Estate Distressed CRE Middle Market Energy Lending

Regulatory Capital Relief Non-Agency CRE B-Piece Small Balance Energy Mezzanine Lending

Revolvers

NPLs Regulatory Capital Relief Agency CRE B-Piece Opportunistic Opportunistic

European Direct Lending NPLs CMBS/CRE

Healthcare Royalties U.S. CRE Bridge Lending Trade Finance

Senior

Opportunistic Capital Solutions Healthcare Royalties RMBS Large Loan Trade Finance

Capital Solutions RMBS Middle Market

Lower Middle Market Music/Film/Media

Country-Specific Funds Small Balance Metals & Mining Finance

PC Special Situations Royalties Consumer ABS Metals & Mining Finance

Emerging Markets Lending PC Special Situations Music/Film/Media Consumer ABS European CRE Lending

Royalties Bridge Agricultural Credit

Asian

PE Special Situations Esoteric ABS Transitional Agricultural Credit

African

PE Special Situations Oil & Gas Minerals Esoteric ABS Core

CEE/Middle East Transportation

Latin American Royalties

Distressed-for-Control Oil & Gas Minerals Europe Structured Credit EM CRE Lending Aviation Lending

Pan-EM European Structured Credit Maritime Lending

Distressed-for-Control Royalties EM CRE Lending

Road & Rail Lending

Global Direct Lending Structured Credit Multi-

Global Metals Royalties Residential Mortgages Transportation Lending

Metals Royalties Sector Residential NPLs (Multi)

Structured Credit Multi- Single Family Rental

Healthcare Lending Sector Mortgage Servicing Rights

MEZZANINE Healthcare Lending Residential Origination

Venture Lending

U.S. Mezzanine Venture Lending

Upper Middle Market

Middle Market Insurance Linked Credit

Lower Middle Market Diversified

Life Insurance

European Mezzanine Non-Life Insurance

European Mezzanine

Litigation Finance [Black] Carlyle Accounts

Structured Equity Litigation Finance [Blue] Legacy Portfolio

Structured Equity

Merger Appraisal Rights

Merger Appraisal Rights

PE Portfolio Finance

PE Portfolio Finance 9

Target Returns Vary Considerably By Strategy

Sector Median Net Target Returns*

Low Medium High

Real Estate Direct Real Mezzanine Specialty Structured Distressed &

Credit Lending Assets Finance Credit Special Sits

Credit

Strategy Median Net Target Returns*

Median Target Net IRR

Metal & Mining Finance

Structured Credit Multi-Sector

Energy Credit CLO

European Mezzanine Factoring & Receivables Emerging Markets Lending

US CRE Transitional Lending Residential Mortgages Corporate Distressed

Infrastructure Lending US Mezzanine

Regulatory Capital Relief Royalties

US CRE Core Lending Venture Lending

CRE Structured Equity

European Direct Lending Special Situations

US CRE Bridge Lending RMBS

European CRE Lending Insurance Linked

US Direct Lending Litigation Finance

Global Direct Lending Real Estate Distressed

Consumer ABS PE Portfolio Finance

Transportation Healthcare Lending

Consumer & SME Lending

Low Medium High

*Data is sourced from Aksia’s internal database, as of December 31, 2020. Target Sector and Strategy returns are representative of information

provided by the managers of funds that are in Aksia’s database. Not all funds are included in the analysis due to insufficient amount of data. Target

returns are not indicative of future performance. 10Private Credit Manager Sourcing

Manager Selection Comprehensive Coverage

Real Estate Credit

11%

Real Assets Credit Direct Lending

28%

Preliminary Review 7%

By Sector

> 2,910 programs

Specialty Finance

12%

Mezzanine

2%

Further Review Structured Credit

8%

> 1,780 programs Distressed & Special Situations

32%

Due Diligence

> 640 programs

Americas

EMEA

By Geography

49%

17%

Asia Pacific

6%

8,000 60

7,000

50 Global

28%

6,000

40

5,000

$mm

Mega Micro

4,000 30 9% 6%

Small

By Fund Size

3,000 19% Micro: ≤ 200mm

20

Small: 200-500mm

2,000 Large Mid: 500mm-1bn

34%

10 Large: 1-3bn

1,000

Mega: > 3bn

0 0 Mid

2019 2020 32%

Client Commitments ($mm) Unique Programs

*Data is sourced from Aksia’s internal database, as of December 31, 2020, excluding legacy Aksia TorreyCove and Aksia Chicago’s private credit

coverage. Client commitments represent Aksia (Private Credit). Coverage by geography and fund size is representative of the universe of investment

programs (onshore & offshore count as one) on which Aksia has conducted due diligence (IDD, ODD, or Insights Report). 11Aksia Proposal

FCERA could consolidate the entire PC program, including legacy portfolio investments, within a Fund-of-One

FCERA Fund-of-One Proposal

(sole investor)

• Customized to FCERA’s objectives

• Access niche strategies & unique

“Yosemite” Aksia exposures more efficiently

Fund-of-One (appointed GP) • Full back-office operations & accounting

support on new & legacy investments

• Aksia leverages our scale when

negotiating fund terms on behalf of

Legacy Legacy New New New New

FCERA

Funds Funds Fund Fund Fund Fund

• Fee transparency: Aksia does not earn

any fees from the underlying funds & we

have no products to place clients in

Simplicity: Fund-of-One would be one line

item for performance & reporting purposes

12Benefits of Aksia Proposal

Aksia Investment Management Expertise

Actively manage $5bn in discretionary Private Credit portfolios

Flexible Direct Fund Simplify Operations Legal & Structuring

Governance Ownership & Reporting Support

Client chooses desired Fo1 owns underlying Consolidate legacy & Experienced legal team

level of involvement in positions and capacity future PC investments that negotiates on

the investment process into one portfolio and FCERA’s behalf

overall line item

Customization Transparency Fee Discounts High Conviction Co-investments

Managers

Sole investor in Fo1; Transparency into Leverage the size of Leverage Aksia’s Invest selectively in

portfolio tailored to underlying Aksia’s broader client extensive research no/low fee co-

specific objectives investments & base to negotiate and advisory investment

and constraints position-level lower fees resources opportunities

exposures*

*Subject to GP cooperation 13Aksia’s Private Credit Performance

As of September 30, 2020 (USD Billions)

Total Gains

Total Invested Total Distributions (realized and unrealized)

$15.6 billion $4.9 billion $2.1 billion

Initial Gross Net Gross Net

Asset Class Invested Distributed Unrealized Total Value

Investment TVPI TVPI IRR IRR

Private Credit Jun-10 $15.6 $4.9 $12.7 $17.7 1.13x 1.13x 8.9% 8.5%

Please refer to page 25 for a description of methodology and the end of these materials for important information. These pro-forma performance

returns are being presented to illustrate the performance as if all investments were in a single portfolio and are not necessarily indicative of future

results. Investors may lose all or part of their invested capital. 14Private Credit Fee Discounts

• Aksia has a structured program for actively negotiating fee discounts generally based on aggregating advisory clients’

investments

• All fee discounts flow 100% to clients

• Fee discounts are generally made available to eligible clients to view via Aksia’s investor portal

Currently negotiated deals by:

Sector AUM

Micro

Mega 2%

9%

16% Small

4%

11%

30%

11%

Mid

22%

9%

Large

49%

37%

Direct Lending & Mezzanine Distressed & Special Situations Micro: ≤ 200 million Small: 200-500 million

Mid: 500-1 billion Large: 1-3 billion

Real Estate Credit Specialty Finance

Mega: > 3 billion

Real Assets Credit Structured Credit

*Aksia’s active negotiated private credit fee deals as of December 31, 2020. Fee deals are only available to advisory clients who subscribe to our

client operations and accounting support services. Sector and AUM breakout is by program. “Program” = onshore and offshore count as one

program. 15Questions?

Thank you!

16Appendix

17Private Credit Co-Investment Sourcing

Last 12 months as of March 31, 2021

• Approximately $3.1 billion in total private credit co-investment deal flow shown to Aksia

• 101 unique private credit co-investments sourced over this same time period

• 71 distinct managers showed Aksia private credit co-investment opportunities

Private Credit Co-Investment Sourcing by Sector Co-Investment Sourcing by Geography

2% 1%

9%

13%

16%

6%

44%

20% 74%

12%

3%

North America Europe Global Not Defined

Credit - Corporate Credit - Real Assets

Credit - Real Estate Specialty Finance

Structured Credit Distressed & Special Situations

Not Defined

Based on initial communications with Managers. Includes deal flow from Aksia LLC and Aksia TorreyCove Capital Partners prior to the combination of

the businesses on March 31, 2020. There is no guarantee that an investor can participate in any identified co-investment. 18Private Markets Client Operations

The Client Operations Team serves as an extension of client’s staff allowing clients to focus on investments rather

than administrative functions

• Investment Activity

PORTFOLIO ACCOUNTING IN MAX

• Workflows

• Checks and Balances

• Analytics

• Attribution

• Sector/Structure

• Strategy

• Vintage Year

• Geography

• Cash Flows

• Valuation

• Performance

• Exposures

• Documents

• Benchmarks

PERFORMANCE REPORTING

• Onboarding1

TRANSACTIONS SUMMARY

*For Illustrative purposes only

1May be at an additional cost if clean data is unavailable and Aksia is required to reconstruct the portfolio’s history 19Risk Analytics

Private Market Alternatives

Risk

exposures in

Company- the context of Investment-

specific risk the portfolio specific risk

Risk Profile

Return Attribution, Outlier and Trend Analysis1

Contexts Financials

Vintage Industry Revenue Leverage

Holding Period Asset Class EBITDA Valuation Bridges

Geography Deal-type Capital Structure Covenants

Aggregated Portfolio Risk Reporting

▪ Position Level Exposures

▪ Asset Class / Region / Industry

▪ Net / Gross Exposure

Available to Advisory clients and subject to the GP’s cooperation and provision of such data to Aksia.

1Analysis is tailored to the asset class. The metrics listed are a subset of the metrics we request, and they are relevant in a variety of the asset classes

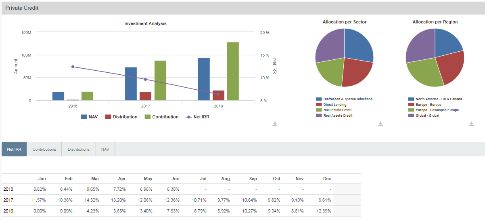

covered under this process. 20“MAX” – Investor Portal

• View performance and various statistics at the aggregated portfolio level

Holdings Shadow Accounting • Dissect performance and exposure by sector/strategy sleeves or vintage

• Portfolio pacing by investment/harvest period

Aggregated Portfolio Analysis

Fund Profiles

Due Diligence

Risk Analysis Reports

Fund & Portfolio

Fund Screener

Customizable Reports

*Provided for illustration purposes only

21Short-Term Private Credit Capital Markets Assumptions

Expected

Sector N ormalized

N et R etu rn

Volatility

Direct Lending 8.9% 7.5%

Mezzanine 8.1% 12.3%

Distressed &

12.5% 15.1%

Private Credit

Special Sits

Specialty Finance 10.9% 13.1%

Structured Credit 8.8% 12.1%

Real Estate Credit 14.2% 13.8%

Real Assets Credit 8.6% 7.6%

Investment Grade 1.4% 5.3%

Public Credit

Hig h Yield 2.4% 11.6%

Syndicated Bank

2.6% 4.1%

Loans

Emerg ing Markets

4.6% 11.6%

Debt

Distressed & Event

3.6% 5.7%

Credit

Hedge

Driven

Fund

Long /Short Credit 5.6% 7.1%

Please see page 26 for a description of methodologies.

NO RELIANCE ON FORECASTS: Any projections, forecasts or market outlooks provided herein should not be relied upon as events which will occur and no assurances

can be given that a particular strategy will perform in a manner consistent with its historical characteristics, or that forecasts, expected volatility or market impact

projections will be accurate. Use of this reference material does not assure any level of performance or guarantee against loss of capital. Neither Aksia nor any of its

representatives make any representation or warranty, express or implied, as to the accuracy or completeness of the information provided herein. Neither Aksia nor any of

its representatives shall have any liability relating to or resulting from the use of this reference material or any errors therein. 22Aksia Presenting Team Biographies

Jim Vos is CEO of Aksia and has over 35 years of alternative investments, research and derivatives experience. He is responsible for the overall

management of Aksia as well as the design of the firm’s research and advisory processes.

Prior to joining Aksia, Jim was a Managing Director and headed Credit Suisse’s Hedge Fund Investment Group from its inception through

December 2005, which grew to over $8 billion AUM. His 20-year career at Credit Suisse also included working in the Portfolio Strategies

group, running a research desk in Tokyo, managing the firm’s FLP trading desk and working within the Credit Suisse Financial Products

derivatives trading boutique.

Jim graduated from the University of Pennsylvania with a BS in Economics. In 2009 and 2010, he was recognized as Hedge Fund Consultant of

the Year by Institutional Investor. In 2016, he was recognized as Consultant of The Year by Chief Investment Officer.

Patrick Adelsbach is Head of Credit Strategies and has over 23 years of financial markets experience including 20 years focused on research

and investment management. He oversees private and public credit strategies, and works with clients to integrate credit strategies within their

portfolios. Patrick led the creation of Aksia’s private credit business and has worked with the institutional investor community to help transition

private credit as an institutional asset class.

Prior to joining Aksia, he was a Director and Head of the Event Driven and Fixed Income Emerging Markets sector team at Credit Suisse and

began his career in 1997 at Capital One Financial Corporation.

Patrick graduated cum laude from the Jerome Fisher Program in Management and Technology at the University of Pennsylvania,

contemporaneously earning a BS in Economics from the Wharton School and a BAS in Systems Engineering from the School of Engineering and

Applied Science.

23Aksia Presenting Team Biographies

Tim Nest is a Managing Director on the Investment Research team and has over 21 years of experience in alternative investments with a

primary focus in private markets. He manages the global private credit investment research professionals responsible for sourcing, conducting

due diligence, evaluating and monitoring of these strategies.

Prior to joining Aksia in 2015, Tim spent several years as a Vice President at Frontier Capital Advisors, a secondary investment firm. Before that,

Tim worked for GSC Group, focusing on two credit-based funds including the firm's distressed corporate credit and structured credit strategies.

Tim began his career as an Analyst in PwC's Corporate Finance practice.

Tim graduated from Boston College with a BS in Finance and Information Systems (dual degree). He holds an MBA in Corporate Finance and

Law and Business from the Leonard N. Stern School of Business at New York University with specializations in Corporate Finance and Law and

Business. He is a CFA charterholder.

Lynn O’Connell is a Portfolio Advisor primarily responsible for supporting clients based in North America in the management of their

alternative investment programs. She also supports the Portfolio Advisory team in various client and business development projects.

Prior to her current role, Lynn was a Senior Analyst on the Operational Due Diligence team focusing on assessing the operational, business,

regulatory and fraud risks of alternative investment funds. While on the Operational Due Diligence team she worked with clients during the due

diligence process, educating and advising them on operational risk considerations.

Prior to joining Aksia in 2012, Lynn was as an Operations Associate at ICON Investments, an alternative investment manager, where she

supported the legal, accounting, technology and investment departments.

Lynn graduated from Binghamton University with a BS in Financial Economics. She has earned the CAIA designation.

She is a member of 100 Women in Finance and was recognized as a Rising Star of Hedge Funds by Institutional Investor Magazine in 2017.

24Aksia Private Credit Performance Methodology

METHODOLOGY: Includes the performance of Aksia LLC’s, together with its wholly owned subsidiaries’ (collectively, “Aksia”) recommended private

credit investments made by some discretionary and predominantly advisory clients as of September 30, 2020. Performance statistics are calculated

through pooled cash flows of qualifying client investments; foreign-denominated investments are converted to USD using a constant FX rate defined at the

commitment date of each individual investment. Cash flows and valuations for terminated relationships are included through the termination date and, if

available, thereafter for so long as cash flow and valuation data are received by Aksia. The track record includes 294 client investments, representing 219

unique programs (where onshore and offshore count as one). Of the 294 investments, Aksia does not have any cash flow information for 15 investments or

5% of commitments, which have not been included. Upon request, Aksia can provide, the performance results of Aksia’s complete track record covering

all alternative asset classes.

PERFORMANCE NOTES:

“Invested” includes the gross capital invested plus fees and expenses.

“Distributed” represents total cash proceeds received.

“Unrealized” equals the fair value of each respective Asset. There can be no assurance that the investments will be realized at these fair values and actual

results may differ significantly.

“Total Value” equals the sum of Distributed and Unrealized.

“TVPI” is the quotient of Total Value over Invested.

“Gross IRR” and “Gross TVPI” are presented net of expenses, management fees and carried interest charged by the underlying managers but does not

include Aksia’s fees or performance compensation.

“Net IRR” and “Net TVPI” are net of management fees, expenses and carried interest charged by the underlying managers, and net of an assumed Aksia

management fee of 40 bps.

PAST PERFORMANCE: Past performance is not indicative of future results and should not be taken as an indication or guarantee of any future

performance or prediction. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown herein,

which are being shown for illustrative purposes and have not been experienced by any specific individual client account. The performance of a specific

individual client account may vary substantially from the track record performance. In addition, certain assumptions have been made by Aksia in

presenting the performance results herein. Therefore, no prospective client should assume that future performance will be profitable or equal either to the

track record performance results.

25Short-term Private Credit Capital Markets Assumptions Methodologies

• The credit universe: We divide the credit universe into three groups (private, public and hedge fund credit). For the purposes of this analysis we concentrate on a

subset of strategies within each sector as a proxy for the broader sector.

• Net return calculation: There are five components that comprise the net return values for the private and public sectors, as detailed below. Although the

Distressed and Special Situations sector typically does not invest in performing loans, we still approximate its returns using the same methodology as other credit

strategies; we assume a riskier mix of component indices to reflect the sector’s risk relative to performing credit sectors. Returns for hedge fund credit sectors use

an alternative methodology based on a trailing 120-month average total return on a representative HFRI index.

• Risk free rate: Wherever floating rate instruments are most prevalent, a 5-year average of the forward 3-month LIBOR curve is used. For fixed rate

instruments, a 5-year treasury rate is used. Risk free rates are as of July 29th, 2020.

• Spread: For private credit sectors, we use a hierarchy of sources (Aksia’s proprietary databases, managers-reported returns and indices) to represent the

current market spread (where applicable, upfront fees and OID are amortized and included in the spread). We use a public market index or a custom

index based on credit rating, issuer size and geography in cases where they offer a better representation of the underlying asset class.

• Losses: Calculated as an expected default rate multiplied by 1 minus the recovery rate.

• Defaults: We typically stress a historical default rate for each sector to reflect our subjective outlook on the credit market during the projected

period. For some sectors where default data is not readily available or we believe is not an accurate representation of default risk, we use

public market data and adjust based on our view of the relative risk profile of the underlying assets.

• Recovery: We typically stress a historical recovery rate to reflect our subjective outlook on the credit market during the projected period. For

some sectors where recovery data is not readily available or we believe is not an accurate representation of the recovery risk, we use public

market data and adjust based on our view of the relative risk profile of the underlying assets.

• Fees: Private credit fees are calculated using Aksia’s proprietary databases of representative funds’ fee structures from recent vintages and account for the

investment period management fee, hurdle and carry. Fees for managing public credit portfolios are estimated based on expected implementation costs.

• Leverage: Applied where we believe fund-level leverage is usually employed and at typical market rates.

• Normalized volatility calculation: Normalized to approximate the volatility of a liquid investment with similar credit risk and adjusted to account for Aksia’s

outlook for the credit markets during the projected period. There are three components that comprise normalized volatility, as detailed below.

• Proxy index: The historical annualized standard deviation over a lookback period of 9 to 12 years of a public market index that we believe most closely

approximates the risk of each relevant credit sector.

• Factor: A multiplier to adjust for our view of (1) the relative risk between the proxy index and the sector, (2) illiquidity, (3) lookback periods that do not

include a market cycle and (4) our outlook of how risk will differ between the lookback and projected period.

• Leverage: Wherever leverage is used the volatility is increased (i.e., 1:1 D/E doubles volatility).

26Disclaimers

THIS PRESENTATION IS PROVIDED PURSUANT TO FCERA’S REQUEST. CERTAIN INFORMATION IN THIS PRESENTATION REQUIRES

FURTHER EXPLANATION AND SHOULD BE DISCUSSED WITH AKSIA. ACCORDINGLY, SUCH INFORMATION SHOULD NOT BE RELIED ON ABSENT

SUCH DISCUSSIONS

NO OFFERING: These materials do not in any way constitute an offer or a solicitation of an offer to buy or sell funds, private investments or other securities

mentioned herein. These materials are provided only in contemplation of Aksia’s research and/or advisory services. These materials shall not constitute advice

or an obligation to provide such services.

RELIANCE ON TOOLS AND THIRD-PARTY DATA: Certain materials utilized within this presentation reflect and rely upon information provided by fund

managers and other third parties which Aksia reasonably believes to be accurate and reliable. Such information may be used by Aksia without independent

verification of accuracy or completeness, and Aksia makes no representations as to its accuracy and completeness. Any use of the tools included herein for

analyzing funds is at your sole risk. In addition, there is no assurance that any fund identified or analyzed using these tools will perform in a manner consistent

with its historical characteristics, or that forecasts, expected volatility or market impact projections will be accurate.

NOT TAX, LEGAL OR REGULATORY ADVICE: The Intended Recipient is responsible for performing his, her or its own reviews of any private investment fund

it may invest in including, but not limited to, a thorough review and understanding of each fund’s offering materials. The Intended Recipient is advised to

consult his, her or its tax, legal and compliance professionals to assist in such reviews. Aksia does not provide tax advice or advice concerning the tax

treatments of a private investment fund’s holdings of assets or an investor’s allocations to such private investment fund. Tax treatment depends on the individual

circumstances of each client and may be subject to change in the future.

PRIVATE INVESTMENT FUND DISCLOSURE: Investments in private investment funds involve a high degree of risk and investors could lose all or substantially

all of their investment. Any person or institution investing in private investment funds must fully understand and be willing to assume the risks involved. Some

private investment funds may not be suitable for all investors. Private investment funds may use leverage, hold illiquid positions, suspend redemptions

indefinitely, modify investment strategy and documentation without notice, short sell securities, incur high fees and contain conflicts of interests. Private

investment funds may also have limited operating history, lack transparency, manage concentrated portfolios, exhibit high volatility, depend on a concentrated

group or individual for investment management or portfolio management and lack any regulatory oversight. Past performance is not indicative of future results.

RECOMMENDATIONS: Any Aksia recommendation or opinion contained in these materials is a statement of opinion provided in good faith by Aksia and based

upon information which Aksia reasonably believes to be true. Recommendations or opinions expressed in these materials reflect Aksia’s judgment as of the

date shown and are subject to change without notice. Except as otherwise agreed between Aksia and the Intended Recipient, Aksia is under no future

obligation to review, revise or update its recommendations or opinions.

27You can also read