Federal Tax Exemption for a Faith-Based Nonprofit - Phase Two NAPA LEGAL TOOLKIT 2021 - Webflow

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Federal Tax Exemption for

a Faith-Based Nonprofit

Phase Two

N A PA L E G A L TO O L K IT 2 02 1

501(C)(3) STATUS & A BRIEF GRAMMAR LESSON. . . . . . . . . . . . . . . . . . . . . . . . . 4

IS APPLYING FOR EXEMPTION RIGHT FOR EVERY ORGANIZATION?. . . . . . . . . 5

WHY WOULDN’T AN ORGANIZATION ASK THE IRS TO RECOGNIZE

THE ORGANIZATION AS EXEMPT FROM FEDERAL INCOME TAX?. . . . . . . . . . . . 4

A NOTE ON FISCAL SPONSORSHIPS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Table of

WHAT DOES THE IRS FORM 1023 APPLICATION LOOK LIKE? . . . . . . . . . . . . . . . 8

DO NOT SKIP THE INSTRUCTIONS!. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Contents

GETTING TO KNOW THE TWO VERSIONS OF THE IRS FORM 1023. . . . . . . . . . . 11

EMPLOYER IDENTIFICATION NUMBER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

PREPARING FOR CONSTRUCTION. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

BRUSH UP ON VOCABULARY. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

ORGANIZING DOCUMENT AND AMENDMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

DIRECTORS & OFFICERS INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

FAMILY AND BUSINESS CONNECTIONS WITH THE ORGANIZATION. . . . . . . . . . 16

BYLAWS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

CONFLICT OF INTEREST POLICY. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

INTERNATIONAL ACTIVITIES. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

GRANTS TO INDIVIDUALS OR ORGANIZATIONS. . . . . . . . . . . . . . . . . . . . . . . . . . 19

IRS FILINGS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

BALANCE SHEET & STATEMENT OF REVENUE AND EXPENSES . . . . . . . . . . . . . 20

POLITICAL ACTIVITY. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Legal Disclaimer: This resource contains general educational information related to legal concepts, but this

information does not constitute legal advice. Anyone seeking legal advice is strongly encouraged to consult ASSEMBLING THE APPLICATION. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

with a licensed attorney regarding any of the matters discussed herein. Although licensed attorneys work

THE ELEMENTS OF AN IRS DETERMINATION LETTER. . . . . . . . . . . . . . . . . . . . . . 22

with Napa Legal, Napa Legal is not a law firm and does not undertake legal representation on behalf of

any clients. Further, no licensed attorney working with or on behalf of Napa Legal agrees to undertake

legal representation on behalf of any client unless the terms of such representation are set forth in a separate,

written representation agreement.

4 Legal Creation of a Faith-Based Nonprofit • P H A S E T W O Legal Creation of a Faith-Based Nonprofit • P H A S E T W O 5

TOOLKIT

501(c)(3) Status & a Brief Grammar Lesson Is Applying for Exemption Right for

AS DISCUSSED IN OUR FIR ST TOOLK IT, understanding the vocabulary used to Every Organization?

describe tax exemption and nonprofit formation is very important. IF YOU FOLLOWED THE STEPS outlined in the first toolkit, your organization

To review, remember that: will have worked with an attorney to properly incorporate the entity. This attorney

presumably ensured that your Articles of Incorporation included a proper purpose

There are two key terms used in nonprofit law that are important to understand clearly from statement, dissolution clause, and other required language to qualify for federal income

the beginning. tax exemption.

The first term is “nonprofit corporation” or “not-for-profit corporation.” A nonprofit Now, you need to determine whether you should ask the IRS to recognize your

corporation is a type of legal entity. Each state has a law that defines what a nonprofit organization as exempt from federal income tax.

corporation is and how it must operate. Some states also use other additional descriptive

phrases, such as “nonstock” or “public benefit.” The defining characteristic of a nonprofit,

regardless of the state in which it was created, is that the organization does not exist to WHY WOULDN’T AN ORGANIZATION ASK THE IRS TO

maximize profit for shareholders. RECOGNIZE THE ORGANIZATION AS EXEMPT FROM

FEDERAL INCOME TAX?

The second term is “tax-exempt organization.” This term is often used synonymously

with “501(c)(3) organization” to refer to organizations that are exempt from federal income Some organizations do not seek the IRS’s recognition of tax-exempt status because

tax under Section 501(c)(3) of the Internal Revenue Code. Federal income tax is the tax they determine either that the organization is automatically exempt or that there

the federal government imposes on a person or entity’s income or revenue. is some other alternative (such as application for inclusion in an existing group

ruling) to submitting an IRS Form 1023 requesting recognition of tax-exempt

Calling a lay apostolate a “nonprofit corporation” or a “501(c)(3) corporation” is like calling status. The available options should be discussed with an attorney or accountant, as

someone “a dark-haired person” or “a male person.” The noun is “person” and “dark-haired” there are strategic reasons why an organization may seek recognition from the IRS

and “male” are adjectives that describe characteristics of this person. “Corporation” is the even if the organization qualifies for the automatic exemption. For example, the

noun. “Nonprofit” is an adjective that describes a type of corporation organized primarily determination letter is often required for grants and certain state exemptions, such

for the execution of a mission. The term “501(c)(3)” describes a characteristic of an as property tax. Additionally, in California, organizations seeking exemption from

organization that has received exemption from federal income tax, either automatically or state franchise tax much submit the Form 3500 or the Form 3500A. Organizations

through an application process. with an IRS determination letter can submit the streamlined, two-page Form 3500A.

Organizations that do not have an exemption letter must use the Form 3500, which is

twenty-five pages and requires extensive supporting documentation.

You can still be an IRS Form 990 non-filers; even if you seek a determination letter

from the IRS (in that case, be sure to indicate the request for non-filing status on the

application).

You can speak with an attorney to determine if your organization is eligible to receive

federal tax exemption through inclusion in a group exemption. In a group exemption,

an organization applies to a parent organization, such as the USCCB, which has

H O M E WO RK

received IRS approve to grant exemption for subordinate organizations. Group

exemptions can help organizations reduce administrative costs and burdens, but group

Watch Part II of NLI’s “Steps to

exemptions also have certain technical requirements.

Success for Lay Apostolates” webinar.

6 Legal Creation of a Faith-Based Nonprofit • P H A S E T W O Legal Creation of a Faith-Based Nonprofit • P H A S E T W O 7

Working with an attorney will help you determine the best option for your organization.

Some other special exemption situations include:

A Note on Fiscal Sponsorships

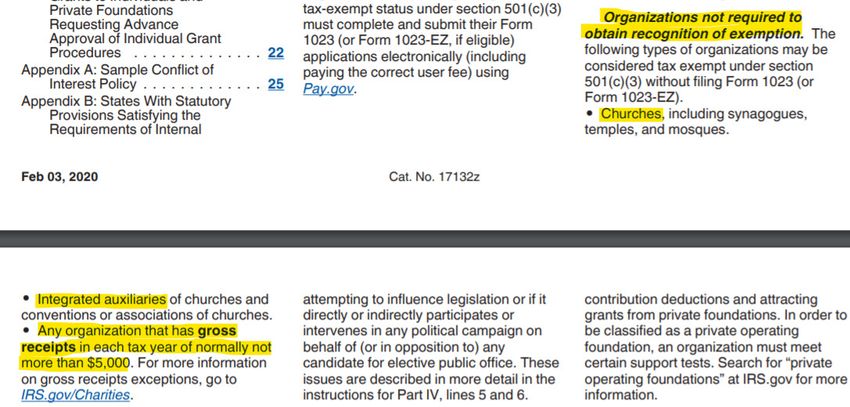

■ Churches AS DESCRIBED IN TOOLK IT: PHASE I, a fiscal sponsorship is an arrangement

■ Integrated Auxiliaries

through which an exempt sponsor organization provides financial support and

administrative oversight to a recipient organization.

■ Group Ruling

■ Fiscal Sponsorship

The fiscal sponsor can receive tax-deductible donations on behalf of the recipient

organization. The fiscal sponsor retains ultimate control over donated funds, as required

■ Organizations with less than $5,000 in revenue by tax law. The fiscal sponsor must oversee the recipient organization to ensure donated

funds are used for tax-exempt purposes.

The fiscal sponsor may also provide other forms of support to the recipient organization,

including handling certain administrative aspects of the recipient’s operations, providing

insurance coverage, and assisting with fundraising.

Written documentation of the terms of the fiscal sponsorship is important to set the

expectations of both parties and protect both parties’ interests. The fiscal sponsorship

agreement should address the conditions of funding, the accounting of funds donated

for the benefit of the recipient, the duration of the agreement, marketing, branding, and

cross-promotion arrangements, religious identity and commitments, the ownership of

intellectual property, and, of course, applicable fees to be paid to the fiscal sponsor.

Fiscal sponsorships are particularly appropriate for the following types of organizations:

■ Volunteer-Run Organizations

■ Start-up Organizations

■ Event-based Organizations (for example, an annual march or conference)

■ Organizations whose leaders are new to operating exempt organizations and

nonprofits

■ Organizations without stable sources of revenue

■ Overseas organizations with few or no U.S. operations

With the assistance of an attorney, almost any tax-exempt organization may become a

fiscal sponsor. Some organizations specialize in providing fiscal sponsorships, serving as a

nonprofit counterpart to the popular start-up incubators. The nonprofit organization San

Francisco Study Center Inc. provides a directory of fiscal sponsors.

To protect their religious identities, faith-based organizations should seriously consider

HOMEWORK working with a fiscal sponsor whose religious commitments align with the potential

recipient’s mission. An example of a Catholic organization that offers a fiscal sponsorship

Review the Table of Contents and program is the Knights of Columbus Charitable Fund.

Introduction for IRS Publication

557: Tax-Exempt Status for Your

Organization

8 Legal Creation of a Faith-Based Nonprofit • P H A S E T W O Legal Creation of a Faith-Based Nonprofit • P H A S E T W O 9

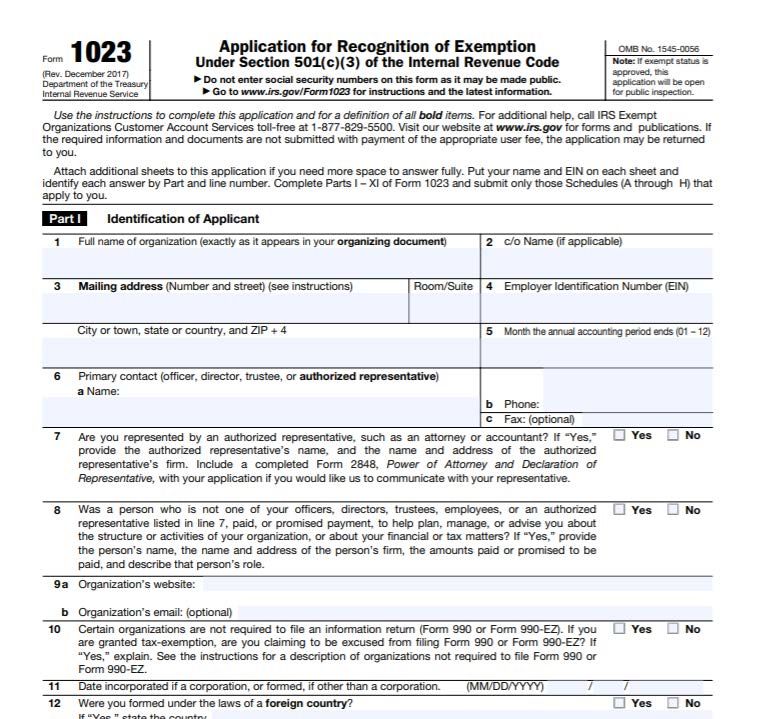

What Does the IRS Form 1023

Application Look Like?

THE IR S FOR M 1023 LOOK S similar to other IRS forms, such as the IRS Form 1040,

which most individual U.S. taxpayers file every year. The IRS Form 1023 comes in two

versions, each of which will be described in the next section of the toolkit.

As of January 2020, both forms of the IRS Form 1023 must be submitted online. However,

rather than drafting the form online, a best practice is to print the PDF of the application

and complete and finalize a hard-copy draft before submitting the online version. Be sure

to review the hard copy side by side with the appropriate set of instructions. As described

in the previous section, the instructions are more than simply practical guidelines; they

are a tutorial on the background of each question and the factors the IRS considers when

reviewing an application.

In content and structure, the

application looks like a simple,

fill-in-the-blank test. Despite this

appearance, however; the application

In content and structure, has several “traps for the unwary.”

Answering thoughtfully and precisely

the application can mean the difference between

receiving recognition of tax-exempt

status or not.

looks like a simple, Many of the application questions

fill-in-the-blank test. are worded in plain English, but

are actually technical tax and

legal questions. These technical

Despite this appearance, questions require precise and specific

explanations to clearly demonstrate

however; the application to the IRS that the organization

is both organized and operated

has several “traps for

exclusively for exempt purposes.

Working with an experienced

professional, such as an attorney or

the unwary.” accountant, is key to making sure

the answers respond to the issues

underlying the questions.

10 Legal Creation of a Faith-Based Nonprofit • P H A S E T W O Legal Creation of a Faith-Based Nonprofit • P H A S E T W O 11

Do Not Skip the Instructions! Getting to Know the Two Versions

B OTH THE IR S FOR M 1023 and the IRS Form 1023-EZ have extensive

“instruction” sheets that are line-by-line tutorials that provide both guidance and

of the IRS Form 1023

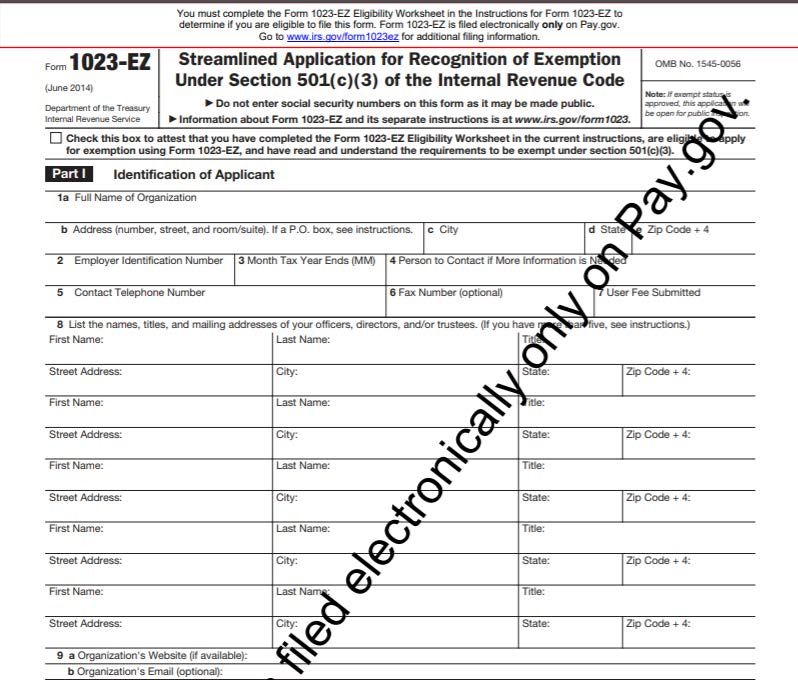

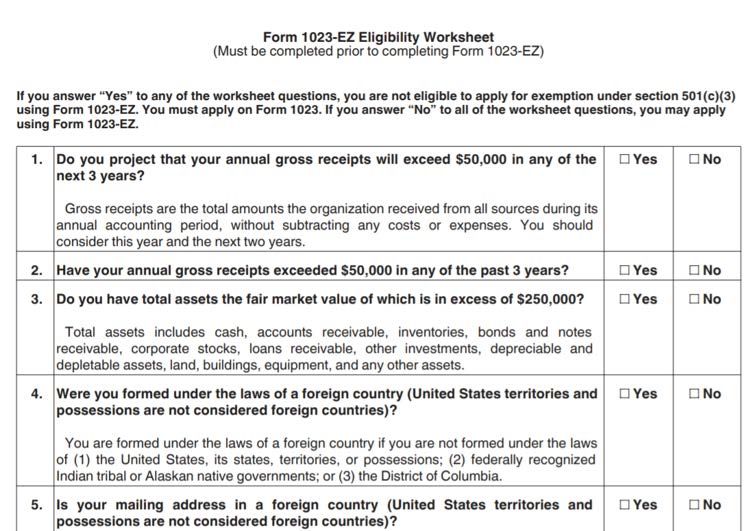

background information regarding each of the questions. AS DISCUSSED IN THE PRIOR section, the IRS Form 1023 is available

in two versions.

Reading through the full instructions is time-consuming, but a worthwhile

investment. If an organization has less than $50,000 in annual revenue and less than $250,000

in assets, the organization might be eligible for a short-form IRS Form 1023, called

Set aside an hour or so each day to read through the instructions with a highlighter the 1023-EZ. The IRS Form 1023-EZ is easier to complete and is processed within

and pen. Mark questions and areas of uncertainty for discussion with your attorney ninety (90) days of submission.

or accountant.

The IRS has issued a simple questionnaire that can help determine eligibility for the

Below are examples of helpful tips and educational information included in the short-form IRS Form 1023-EZ. The questionnaire is available on page 13 of the IRS

IRS Form 1023 Instructions. Form 1023-EZ Instructions.

HOMEWORK

Homework: Read through the

Life Cycle of a Public Charity*

12 Legal Creation of a Faith-Based Nonprofit • P H A S E T W O Legal Creation of a Faith-Based Nonprofit • P H A S E T W O 13

Employer Identification Number You will need the following information:

1. Employer Identification Number

AN EMPLOYER IDENTIFICATION NUMBER (“EIN”) is to an organization

something like what a social security number is to an individual. The EIN is referenced 2. Point of Contact for the application

in all communications and reports to the IRS and is also often used by state and local

3. Mailing Address (best if this is not a home address; it can be a PO Box)

government agencies for reporting and taxing purposes. If an organization doesn’t have an

EIN, or if you aren’t sure whether or not an organization has one, go back to Toolkit Phase I for 4. Fiscal Year End (usually in bylaws or initial board resolutions)

instructions.

5. List of Directors

Preparing for Construction 6. Articles of Incorporation

GATHERING THE REFERENCES, EQUIPMENT, and tools you will need to 7. Bylaws

work with your attorney in advance of preparing the application can help you work more 8. Budget

efficiently and can reduce the stress involved in the process of preparing the application.

9. Revenue and Expense Statement(s)

You will need the following materials:

■ Computer ■ Printed Copy of the IRS Form 10. If applicable:

■ Printer 1023 or 1023 EZ a. Statements of Stocks and Investment Holdings

■ Highlighter ■ Printed Copy of the IRS Form b. Real Estate Holdings

■ Pen

1023 or 1023 EZ Instructions

■ Printed Copy of IRS Publication

■ Notepad 557: Tax Exempt Status for Your

c. Other property (including large equipment)

■ Optional: Post it notes or flags Organization

11. Marketing Material or Screenshots from Website or Flyers from Events

HOMEWORK

For more information on EIN,

watch Part I of our webinar

“Steps to Success for Lay

Apostolates.” You may also wish

to review the applicable section

of the Toolkit Part I.

14 Legal Creation of a Faith-Based Nonprofit • P H A S E T W O Legal Creation of a Faith-Based Nonprofit • P H A S E T W O 15

Brush Up on Vocabulary Organizing Document and Amendments

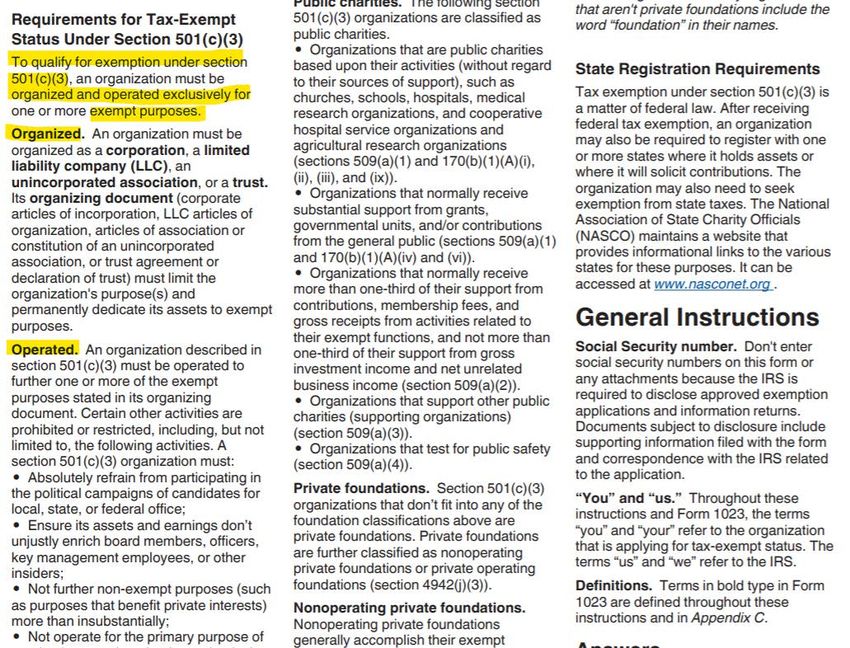

VOCABUL ARY IS AN IMP ORTANT FUNDAMENTAL to building an EVERY ORGANIZ ATION APPLYING FOR EXEMPT status must submit to the

understanding the IRS Form 1023. As discussed in previous sections, the IRS Form 1023 IRS a copy of the entity’s “organizing document.”

uses common, plain-English words and phrases, that can be misleading because they are

often actually technical terms that refer to legal and tax concepts. If your organization has legally changed its name or purpose, or otherwise amended its

original articles of incorporation, be sure to include copies of the amendment filings in the

For example, a “substantial contributor” in plain English would logically mean anyone application.

who contributes in a meaningful way to an organization. In the tax context, however,

“substantial contributor” is a technical term referring specifically to persons who contribute

more than $5,000 to an organization in a single fiscal year. TIP

Remember to be precise in using the organization’s legal name throughout the application,

To assist users in recognizing these technical terms, the IRS Form 1023 uses bold font to

even if the organization uses an acronym or nickname in marketing, fundraising, and

highlight the terms. The IRS provides a helpful glossary of the bolded terms in Appendix C

conversation. Using the wrong name could result in an incorrect determination letter.

on page 29 of the IRS Form 1023 instructions.

Excerpts from IRS Form 1023 and the glossary entry for the bolded term are below:

IRS REQUIRED LANGUAGE

Although the organizing document is primarily based on state law, the IRS requires certain

language to be included before the IRS will grant tax-exempt status to the applicant. Below

are four key areas in which the IRS has specific language requirements. (See Day Fifteen of

Toolkit Phase I)

1. Purpose – Part III, Line 1 of the Form 1023 explains the IRS requirement that an

exempt organization have a purpose statement that limits the organization to activities

that are recognized as exempt under the tax code. If your organization’s articles do not

already include this language, you should work with an attorney to amend them before

submitting the application. Note: the purpose statement in the articles should match

the purpose statement in the bylaws. To avoid contradictions, some organizations’

bylaws simply reference the purpose statement in the articles.

2. Dissolution – Part III, Line 2 will ask about your organization’s dissolution clause, to

ensure the assets of the organization are permanently dedicated to exempt purposes.

If your organization’s dissolution clause does not specifically indicate that assets go to

another charitable and exempt organization, work with an attorney to amend this prior

to submitting the IRS Form 1023.

3. Political Activity – The IRS also recommends that an exempt organization’s organizing

document specifically prohibit more than an insubstantial amount of political activity.

4. Private Benefit and Private Inurement – Finally, the organizing document should limit

the organization exclusively to its exempt purposes. Accordingly, including an express

prohibition on impermissible private benefit and private inurement is a best practice.

16 Legal Creation of a Faith-Based Nonprofit • P H A S E T W O

Directors & Officers Information

PART V ASK S A SERIES of questions about the relationships among the organization,

its directors, its vendors and contractors, and its employees.

These questions are used to help the IRS decide whether the organization meets the

Like people, most

requirement of operating primarily for exempt purposes and not for the private benefit of

an individual.

organizations

When answering these questions, the organization must demonstrate that no improper

private benefit is occurring and that safeguards are in place to prevent such improper private

benefit. For example, stating that the board is “independent,” meaning not conflicted by

the directors’ own business interests, and demonstrating that reasonable compensation is

set according to objective standards are two ways to indicate the organization is eligible for

exemption.

– even “exempt”

organizations –

Part V, Line 1a requires a list of current directors and officers.

If your organization has a board of directors that regularly meets, this task will be simple. If

your organization’s board does not meet regularly or has not yet appointed officers, take the

time to bring the board up to date. Check to make sure director and officer terms have not

expired.

are required to

submit an annual

If possible, use a business address for all directors. The IRS Form 1023 is a public

document, so using people’s home addresses might be intrusive and even dangerous in some

circumstances.

Family and Business Connections with the filing to the IRS.

Organization IRS FILINGS, PG 20

LINE 2 ASK S AB OUT THE family and business connections among the organization’s

directors and offers.

The question behind the question here is whether the organization is operating primarily

for exempt purposes, or whether private individuals are benefitting improperly from the

organization’s activities. For more information about private benefit, please review NLI

President and General Counsel John Peiffer II’s blog post, “Three Observations from

Recent Media Coverage of Liberty University,” and whitepaper series.

18 Legal Creation of a Faith-Based Nonprofit • P H A S E T W O Legal Creation of a Faith-Based Nonprofit • P H A S E T W O 19

Bylaws Grants to Individuals or Organizations

PART II, LINE 5 WILL ask if your organization has bylaws. As discussed in Toolkit Part BECAUSE INTERNAL REVENUE CODE SECTION 501(c)(3) prohibits exempt

I, having bylaws is a best practice under state and federal law. Additionally, for a faith-based organizations from operating for the benefit of a private individuals or organization, any

nonprofit, bylaws are an important tool through which to demonstrate the organization’s grants to individuals must be made on an objective basis and cannot be earmarked for any one

religious identity. person. For example, starting an organization called “Aid for Larry”, which fundraised to cover

Larry Lightfoot’s medical bills, would not be eligible for exemption under Section 501(c)(3).

The bylaws should include a signature page signed by a corporate officer indicating that the Many GoFundMe pages are examples of causes that benefit a specific individual, rather than a

bylaws have been approved by the board and as of what effective date. charitable class; thus, they would not be eligible for tax exemption.

If an exempt organization wishes to grant funds to other organizations, the exempt organization

must demonstrate that the funds will be used in furtherance of the exempt purposes. An exempt

Conflict of Interest Policy organization is not prohibited from granting funds to a commercial organization, but the

exempt organization must be very cautious. For example, an exempt organization that sought to

PART V, LINE 5 ASK S whether the organization has adopted a conflict of interest policy. promote interest in classical music conducted a number of programs to encourage listeners to

The IRS does not require a conflict of interest policy, but adopting one is a best practice tune in to a for-profit radio station. The IRS found that this promotion of the for-profit station

(and not adopting one is a red flag). Further, state laws also affect the manner in which was taking up too much of the exempt organization’s resources and was actually causing the

conflicts of interest are handled by the organization, and, therefore, should be taken into organization to operate for the benefit of a private entity. The organization was not eligible for

account in your conflict of interest policy. recognition as 501(c)(3) tax-exempt organization.

NLI has created template documents that can be tailored by an attorney to adopt a conflict

of interest policy for your organization. Appendix A of the IRS Form 1023 Instructions

also includes a boilerplate conflict of interest that can be tailored for your organization. IRS Filings

All directors, officers, and key employees should complete an annual statement disclosing LIK E PEOPLE, MOST ORGANIZ ATIONS – even “exempt” organizations – are required

any conflicts of interest and acknowledging that the individuals have reviewed and agreed to submit an annual filing to the IRS.

to the policy.

People and for-profit companies submit an annual income tax return, along with a payment of their

federal income tax.

International Activities Organizations that are exempt from federal income tax do not submit taxes, but they do submit an

annual report to the IRS through which the organization demonstrates that it still deserves to be

ORGANIZ ATIONS THAT M AY SEND GR ANTS outside the United States have recognized as exempt from federal income tax.

special legal responsibilities. Certain religious organizations, which are churches or are “integrated auxiliaries” of churches, are

From a tax perspective, all funds must be used for exempt purposes, not the benefit of exempt BOTH from paying taxes and from sending an annual report about their activities to the

private individuals. Organizations that send grant money cannot delegate this responsibility IRS. The reason these organizations are exempt both from taxes and from even just “checking

to the grant recipients; rather, the exempt organization must continue to oversee the use of in” with the IRS is that the IRS does not want to become entangled with religion because such

the funds to ensure no private individuals are benefiting improperly. involvement would put the agency at risk of violating the First Amendment to the Constitution.

Your accountant or attorney can help you determine whether your organization fits within one of

these special categories.

Parish churches and religious orders are often exempt both from paying taxes and from the annual

“check-in.” Lay-run apostolates are generally not exempt from reporting, even though they are

exempt from paying taxes.20 Legal Creation of a Faith-Based Nonprofit • P H A S E T W O Legal Creation of a Faith-Based Nonprofit • P H A S E T W O 21

Balance Sheet & Statement Assembling the Application

of Revenue and Expenses PUT THE ORGANIZ ATION’S NAME AND EIN on each page of your supplemental

response and identify the part and line number to which the information relates.

THE IR S INCLUDES A SECTION requesting a copy of the organization’s budget

and statement of revenue and expenses. The IRS requests this financial information to Combine your attachments in the following order:

determine whether the organization will in fact be operated as an exempt organization. 1. Organizing document (required).

Properly characterizing revenue and expenses in these statements is critical. An accountant

or attorney will help you ensure the organization is precise and accurate in developing these 2. Amendments to your organizing document in chronological order

reports. (required if applicable).

The financial information should be consistent with the information provided elsewhere in 3. Bylaws or other rules of operation and amendments (if adopted).

the application. For example, if the application states that the organization’s funding comes

4. Form 2848, Power of Attorney and Declaration of Representative (if applicable).

primarily from tickets to educational lectures, make sure the revenue statement properly

includes and identifies this. 5. Form 8821, Tax Information Authorization (if applicable).

6. Expedite request (optional).

Political Activity 7. IRS Form 1023 or Form 1023-EZ

8. Supplemental responses (if your response won’t fit in the provided text field) and any

UNDER STANDING THE B OUNDARIES OF PER MISSIBLE educational issue

additional information you want to provide to support your request (optional).

advocacy and impermissible political activity is important to protecting your organization’s

exempt status.

As the IRS states in Publication 557: “If any of the activities (whether or not substantial)

of your organization consist of participating in, or intervening in, any political campaign

on behalf of (or in opposition to) any candidate for public office, your organization won’t

qualify for tax-exempt status under section 501(c)(3). Such participation or intervention

includes the publishing or distributing of statements.”

HOMEWORK

Read the USCCB’s “Political

Activity and Lobby Guidelines

for Catholic Organizations.”22 Legal Creation of a Faith-Based Nonprofit • P H A S E T W O Legal Creation of a Faith-Based Nonprofit • P H A S E T W O 23

The Elements of an IRS The blue indicates the NLI qualified for exemption from federal income tax under Section

501(c)(3) of the Internal Revenue Code.

Determination Letter The pink refers to NLI’s responsibility to file annual reports to the IRS.

AF TER THE IRS Form 1023 is submitted, the IRS will review the application. The typical The green indicates which subcategory of 501(c)(3) organizations NLI falls into based on

processing and review time is about two to four weeks, for the IRS Form 1023-EZ, and six NLI’s sources of revenue.

months for the full IRS Form 1023.

The yellow is NLI’s Employer Identification Number, or EIN, which is similar to a social

The IRS may contact the organization with additional questions if any aspect of the security number. The EIN is referenced in all communications and reports to the IRS and is

application is unclear. also often used by state and local government agencies for reporting and taxing purposes.

If the application is successful, the organization will receive an “IRS Determination Letter” The orange indicates the effective date of NLI’s exemption. (See page 6 of IRS Publication

similar to the following. Keeping a copy of the determination letter in the organization’s 557 for more information about effective dates.) In this case, the effective date is the same

records is very important. date NLI was incorporated, in other words, NLI’s legal birthday. For most organizations,

the effective date should be the date of incorporation. Exceptions occur if an organization

is seeking exemption after being included on a group ruling or if an organization did not

receive recognition of exemption within 27 months of its incorporation. An attorney

can assist to make sure your organization receives the correct effective date. An incorrect

effective date might lead to extra taxes or penalties.

LEGAL DISCLAIMER

This resource contains general educational information related to legal concepts, but this

information does not constitute legal advice. Anyone seeking legal advice is strongly encouraged

to consult with a licensed attorney regarding any of the matters discussed herein. Although

licensed attorneys work with NLI, NLI is not a law firm and does not undertake legal

representation on behalf of any clients. Further, no licensed attorney working with or on behalf

of NLI agrees to undertake legal representation on behalf of any client unless the terms of such

representation are set forth in a separate, written representation agreement.You can also read