Extension of JobKeeper in the accommodation sector post COVID-19 - 4 JUNE 2020 2020

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2020 Extension of JobKeeper in the accommodation sector post COVID-19 4 JUNE 2020

Contents

1.0 About the Accommodation Association………………………………………………………………………...2

2.0 Accommodation industry recommendations on transitioning post JobKeeper

2.1 JobKeeper recommendations post-September 2020 to assist

accommodation businesses to transition……………………………………………………………..2

3.0 Economic Value of the Accommodation Sector……………………………………………………………….3

4.0 Economic Impact of COVID-19 on the Accommodation sector

4.1 HMSA Accommodation Industry State Performance 2020 year to April………………..4

4.2 HMSA Accommodation Capital City Performance 2020 year to April…………………….5

4.3 Forward Occupancy to mid-August 2020……………………………………………………….........5

5.0 Factors impacting Recovery of the accommodation sector performance post COVID-19

5.1 First and foremost, will be the closure of the international borders ……………………..6

5.2 Secondly the closure of the international borders may result in some

lift in domestic spend for holiday purposes…………………………………………………………..7

5.3 Thirdly the extent of domestic holiday spend will be impacted by labour

market outcomes and consumer confidence…………………………………………….............9

5.4 Fourthly the extent of domestic corporate spend will be impacted by

business confidence……………………………………………………………………………………………..9

5.5 Fifthly new health and guest safety regulations have the potential to

further impact operator/owner operating profitability………………………………...........9

6.0 The Importance of JobKeeper in retaining staff under current COVID-19 measures

6.1 Impact of JobKeeper in retaining employees ……………………………………………..........10

6.2 Primary reasons for hotels not accessing JobKeeper…………………………………………..11

7.0 The Importance of retaining JobKeeper post September 2020

7.1 Accommodation sector expectations on recovery ……………………………………………..11

7.2 Accommodation sector recovery impacts on employment……………………………......12

7.3 Anticipated impact of JobKeeper removal as of 30 September 2020…………………..13

8.0 Conclusion……………………………………………………………………………………………………………………….14

1

Accommodation Association | 401/105 Pitt Street Sydney NSW 2000| www.aaoa.com.au | 1300 304 397

1.0 About the Accommodation Association

The Accommodation Association is the peak body representing close to 1,000 accommodation

operators and over 100,000 rooms across Australia. Members of the Accommodation Association

include major hotels, resorts, motels, motor inns, serviced and holiday apartments, bed and

breakfasts and guesthouses that directly contribute $7 billion in GVA to the Australian economy.

Our members include AccorHotels (incorporating Mantra Group); Intercontinental Hotels Group

(IHG); Lancemore Group; Hilton; Toga Far East Hotels (TFE); Wyndham Hotel Group; Choice Hotels;

Meriton Suites; Best Western; Big 4 Holiday Parks and Quest Apartment Hotels.

The Association is committed to the future development and growth of a sustainable

accommodation industry within Australia’s dynamic tourism and hospitality sector.

2.0 Accommodation industry recommendations on transitioning post JobKeeper

Our submission below is in response to the discussions with Federal Government on the status of the

industry post September 2020 and outlines the continuing impact of COVID-19 measures on the

accommodation industry in Australia into 2021.

Our recommendations are based on the considerable evidence base in this submission, which show

that the below will have a significant impact on the performance of accommodation providers room

and food and beverage revenue to 2021

• continuing government restrictions on borders.

• consumer and business confidence.

• consumer spending capacity.

• and continuing restrictions on gatherings and events.

The modelling undertaken by several businesses shows that most hotels are keeping approximately

50% of their staff on the books with JobKeeper despite operating at occupancies below 10%. This

will have significant implications for the ability of accommodation businesses to recover.

Importantly the data from a wide cross-section of hotels indicates that the removal of

JobKeeper in September will result in an average of 30% or more of employees currently on

JobKeeper being made redundant.

Estimated Impact of JobKeeper on accommodation sector

120,000 150%

100,000 100%

80,000

50%

60,000

0%

40,000 56,750

20,000 -50%

113,500 33,382

0 -100%

Pre-COVID-19 JobKeeper End JobKeeper

Employment Revenue year on year

2

Accommodation Association | 401/105 Pitt Street Sydney NSW 2000| www.aaoa.com.au | 1300 304 397

2.1 JobKeeper recommendations post September 2020 to assist accommodation businesses to

transition

The biggest concern for accommodation providers is the deadline of 30th September as businesses

will not have recovered to the levels needed to bring all employees back to work and on the payroll.

We recommend implementing a phased approach that would help support the transition for most

hotels. Our recommendations are as follows:

Phase 1 - Classification for eligibility is maintained for a minimum of 6 months from 1 October 2020

to 31 March 2021.

a) Further test of Eligibility - A further test at the end of September to demonstrate eligibility

for JobKeeper on an ongoing basis.

Phase 2 - Quarterly BAS reporting of wages to confirm eligibility during the 6-month period.

The parameters of JobKeeper to remain the same with some adjustments to update eligibility

requirements in line with the extended time.

1. JobKeeper to be expanded to casuals who are still engaged with the entity. The test to

remain the 12 months prior but to move to the new date of 30 September. As advised

above, 44.3%1 of employees in the accommodation sector are casuals with about 40% of

these who were with their employer for less than 12 months and thus were not eligible.

2. The ‘one in all in’ model is not fit for purpose as businesses adjust to a post COVID operating

model. Businesses will require some flexibility in adjusting employment requirements to a

new operating mode.

3. The $1,500 per fortnight remains the minimum payment per fortnight. This provides

businesses with the flexibility to pay staff for hours worked.

4. Extension of the HIGA provisions to enable employers to have flexibility in deploying their

staff. Specifically, around measures such as - direction to take leave; ability to direct a

reduction in part time and fulltime hours. These provisions to also override Enterprise or

Collective agreements for the period of the extension of JobKeeper.

3.0 Economic Value of the Accommodation Sector

In 2018–19, total tourist consumption was $152.0 billion2, which resulted in:

• $60.8 billion in GDP to the economy (3.1% of the national total)

• Employment of 666,000 persons (5.2% of the Australian workforce), and

• Exports of $39.1 billion from international visitors to Australia

The accommodation sector is a significant player in the tourism industry, directly contributing close

to $7billion in GVA, $14.3 billion in tourism consumption3 and directly employing 113,500 FTEs4, 17%

of total tourism employment.

1

Source: ABS, Characteristics of Employment, cat. no. 6333.0

2

2018-19 Tourism Satellite Accounts, TRA

3

2018-19 Tourism Satellite Accounts, TRA

4

2019 Accommodation Association Hotels Industry Survey

3

Accommodation Association | 401/105 Pitt Street Sydney NSW 2000| www.aaoa.com.au | 1300 304 397

In 2018-19 a total of 296,452 rooms and 5,535 properties made up the sector (50.6% hotels and

resorts; 21% motels, guest houses; 25% serviced apartments).

Rooms Rooms Properties Properties Revenue 2017-18

2017-18 2018-19 2017-18 2018-19

Hotels & Resorts 143,927 147,537 1677 1706 $7.85 billion

Motels/Private 60,006 61,455 2121 2221 $2.16 billion

Hotels/Guest Houses

Serviced Apartments 71,065 74,266 3574 1228 $3.57 billion

Holiday Parks 9,682 13,194 283 380 $0.27 billion

Source: Australian Accommodation Monitor, 2018-19

4.0 Economic Impact of COVID-19 on the Accommodation sector

Hotels, motels and serviced apartments across Australia have experienced a decline in revenue in the

order of 85% with self-isolation and essential services businesses the only activity.

The below tables demonstrate the impact of government measures which have:

• closed international borders.

• closed interstate borders (WA, SA, TAS, NT and QLD); and

• either limited the extent of regional travel (QLD – 150kms) or only permitted travel for

essential services (NSW).

• closed Conference/meeting rooms.

4.1 HMSA Accommodation Industry State Performance 2020 year to April

January February March April May

State % Revenue % Revenue % Revenue % Revenue % Revenue

year on year year on year year on year year on year year on year

NSW -4.9% -12.9% -47.6% -85.1% -86.0%

Victoria -1.2% -12.5% -46.9% -75.0% -77.0%

Tasmania 4.7% -10.5% -36.4% -85.0% -86.0%

WA 1.6% -2.2% -33.8% -71.0% -72.0%

NT -9.8% -0.7% -28.4% -70.5% -72.0%

Queensland 7.0% -1.2% -39.9% -85.0% -86.0%

ACT -18.1% -4.5% -36.7% -86.9% -87.0%

South 6.5% 6.6% -37.7% -81.7% -83.0%

Australia

Source: STR Global

4

Accommodation Association | 401/105 Pitt Street Sydney NSW 2000| www.aaoa.com.au | 1300 304 3974.2 HMSA Accommodation Capital City Performance 2020 year to April

Capital City January February March April May

% Revenue % Revenue % Revenue % Revenue % Revenue

year on year year on year year on year year on year year on year

Adelaide 4.6% 4.3% -40.6% -83.5% -85.0%

Brisbane 9.4% 2.1% -43.1% -78.3% -80.5%

Cairns 4.8% -25.5% -55.3% -87.4% -88.0%

ACT & Canberra -18.1% -4.5% -36.7% -88.2% -89.0%

Melbourne -2.4% -14.9% -48.8% -76.6% -78.6%

Perth 1.3% -3.4% -36.6% -65.8% -66.0%

Sydney -5.5% -15.3% -51.1% -83.6% -85.3%

Gold Coast 4.6% 2.4% -40.0% -93.3% -94.0%

Darwin -12.4% 0.7% -31.0% -73.9% -75.0%

Hobart 2.9% -14.2% -41.0% -82.3% -83.4%

Source: STR Global

4.3 Forward Performance of the Accommodation sector to mid-August 2020

The announcements on easing from the 15 May have had a small impact on forward bookings (+2%)

but the reality is that there are a number of factors that negatively impact the performance of the

accommodation market even as restrictions ease.

5

Accommodation Association | 401/105 Pitt Street Sydney NSW 2000| www.aaoa.com.au | 1300 304 3975.0 Factors impacting Recovery of the accommodation sector performance post COVID-19

5.1 First and foremost, will be the closure of the international borders

Hotel, motel, and serviced apartments (HMSA) in capital city markets are hugely reliant on

international travel as demonstrated in the graph below. International visitor nights represent

42.4% of HMSA visitor nights in Sydney; 34% in Melbourne; 30.5% in Perth and 25.6% in Brisbane-

Gold Coast 25.6%.

Visitor Nights in HMSA

25000

20000

15000

10000

5000

0

Domestic Visitor Nights "000 International Visitor Nights '000

Source: IVS and NVS, TRA YE Dec 2019

International visitors have been a key segment for Australian HMSA. In full year 2019 international

visitors spent $31.4 billion in Australia. This compares to $80.7 billion in domestic overnight

expenditure.

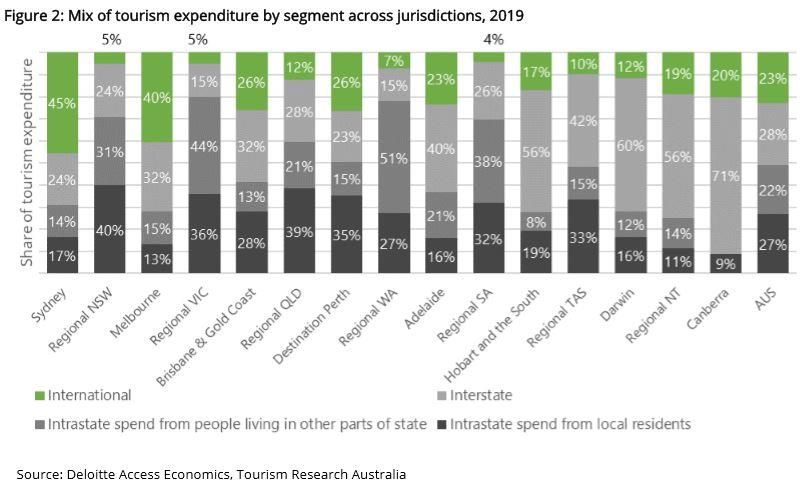

The Deloitte graph below highlights the breakdown of expenditure across the cities and regions,

once again highlighting the concentration of international business in capital cities.

6

Accommodation Association | 401/105 Pitt Street Sydney NSW 2000| www.aaoa.com.au | 1300 304 397Separate from the above, city hotels with major airport hubs and cruise terminals rely on airline staff

and crew to provide base business and with the closure of international borders both these types of

businesses have disappeared.

Oxford Economics5 advise that the economic ramifications of the current crisis, together with

negative sentiment towards international travel, point to a prolonged recovery period. International

visitor arrivals in cities are expected to return to 2019 peak levels by 2023.

5.2 Secondly the closure of the international borders may result in some lift in domestic spend for

holiday purposes

Deloitte and Dransfield have pointed to the opportunity for states and territories to ‘redirect’ and

‘retain’ some of the expenditure that would otherwise be spent overseas.

In 2019 Australians spent a total of $65 billion overseas. Converting this intent to travel will be a

function of both pent-up demand, consumer confidence and consumer spending capacity.

Intention to Travel - Consumers

An early May survey of 2,225 people by Vox Pop Labs in collaboration with the ABC6 has found that

only about one in eight Australians would attend a large event even if they could, fewer than one in

five would get on a plane, and only 40 per cent would go to a bar or restaurant.

Tourism Australia in their latest Domestic survey in April asked Australians how people’s holiday

behaviour may change once travel restrictions are lifted. The consensus is that consumers will be

quite cautious, subject to the hygiene measures put in place. Please refer below.

Even when domestic travel is planned, 30% say it will be in the next 6 – 12 months. This points to

some delay in travel returning to pre-COVID levels until 2021. This is supported in Oxford Economics

forecasts.

5

Travel & Tourism | Cities COVID-19: pandemic impacts on Asia Pacific city tourism, May 7

6

https://mobile.abc.net.au/news/2020-05-06/australians-hesitant-to-head-out-coronavirus-restrictions-

lifted/12217102

7

Accommodation Association | 401/105 Pitt Street Sydney NSW 2000| www.aaoa.com.au | 1300 304 397An important factor to recognise is that the extent of the recovery will depend on the customer

experience. With the easing of restrictions, difficulties in booking into restaurants, cafes, and

limitations in accessing destination experiences will impact consumer intentional to travel

domestically.

McKinsey and Company Australian Consumer Sentiment Survey, May 8 -11

The McKinsey survey demonstrated a net decline of 6% in intent for domestic travel but 26% in net

decline in intent for international travel post COVID-19.

8

Accommodation Association | 401/105 Pitt Street Sydney NSW 2000| www.aaoa.com.au | 1300 304 3975.3 Thirdly the extent of domestic holiday spend will be impacted by labour market outcomes and

consumer confidence

The hit to the labour market has largely been softened by government stimulus measures such as

JobKeeper and JobSeeker. ABS Labour force figures for April show that compared to a year ago,

there were 123,000 less people employed full-time and 272,000 less people employed part-time.7

Those employees who are on JobKeeper are classified as employed. The extent to which

employment is impacted post-September will impact consumer and travel demand.

ANZ-Roy Morgan Consumer Confidence as of 26 May 2020, gained for the eighth straight week and

is up 42% from its low point of 65.3 in March, when fears about the pandemic were at the most

extreme.

Now 23% (down 1ppt) of Australians say their families are ‘better off’ financially than this time last

year and 36% (unchanged) say their families are ‘worse off’ financially. The extent to which this

positively changes as current measures are lifted will impact consumer spending on discretionary

items.

The McKinsey and Company Consumer Survey from 8-11 May pointed to a third of Australians

advising of a decline in income and savings in the period.

5.4 Fourthly the extent of domestic corporate spend will be impacted by business confidence

The April NAB Business Survey noted business confidence remains “well below the trough of the

1990s” recession. Overall, the NAB survey noted that confidence rose 19 points to -46 index points

over the whole month. This was led by improvements in retail, construction, and mining.

Business conditions, meanwhile, continued to fall in April, declining by 12 points to -34 index points.

The NAB Group Chief Economist, Alan Oster, pointed to the fact that “the hit to confidence will have

some ongoing impacts to hiring and capex, which could see a drag on growth for some time”.

The NAB employment index was near its lowest level on record at -35 index points.

5.5 Fifthly new health and guest safety regulations have the potential to further impact

operator/owner operating profitability

The extent of new health and safety regulations, in particular physical distancing measures, also has

future financial implications for owners and impacts both the capacity and profitability of opening

facilities within accommodation hotels.

This is further exacerbated by cashflow constraints emerging from 6 or more months of declining

demand. To understand the impact of COVID-19 on hotel operations, the Association together with

AHS Advisory and Horwath HTL conducted a survey of close to 400 properties in mid-May. The

results were:

• 80% of accommodation properties described their current operations as ‘Cash Flow

Negative’ – 72% capital city properties and 82% regional properties.

• 74% of properties listed ‘improving hygiene standards’ as a top 3 initiative. This was the only

initiative flagged as increasing costs to the operation.

7

6202.0 - Labour Force, Australia, April 2020

9

Accommodation Association | 401/105 Pitt Street Sydney NSW 2000| www.aaoa.com.au | 1300 304 3976.0 The Importance of JobKeeper in retaining staff under current COVID-19 measures

The Accommodation Association/AHS Advisory and Horwath Hotel Sentiment Survey in mid-May

showed that of the 35,834 rooms surveyed approximately 41% were operational with 59% closed.

As a result, 50% of accommodation properties across Australia are currently operating at staffing

levels between 0-25% of pre-COVID levels.

6.1 Impact of JobKeeper in retaining employees

The survey results show that 91% of all participating properties utilised JobKeeper to maintain a

connection to staff.

Participants in the Hotel Sentiment Survey advised that JobKeeper had resulted in:

• 77% of hotels bringing back workers from Stand Down.

• 42% of hotels using as an opportunity to multi-skill workers.

• 40% advised that it resulted in a rationalisation of their workforce.

• 29% advising that visa employees were not retained.

This demonstrates that JobKeeper has been successful in retaining employees at a time when the

industry is operating with revenues of negative 85%.

10

Accommodation Association | 401/105 Pitt Street Sydney NSW 2000| www.aaoa.com.au | 1300 304 3976.2 Primary reasons for hotels not accessing JobKeeper

While most hotels sought to access JobKeeper, there were issues with accessing this benefit where

staff and properties fell outside eligibility criteria.

• Casual employees of less than 12 months. 44.3%8 of employees in the accommodation

sector are casuals with about 40% of these with their employer for less than 12 months and

were not eligible for JobKeeper.

• Employees on visas represent about 24% of all employees and were not eligible for

JobKeeper.

• Where the hotel is a wholly owned entity of a body politic of a foreign country or foreign

government agency regardless of their Australian tax residency.

• Insufficient cashflow to make payments given the requirement to pay in arrears.

7.0 The Importance of retaining JobKeeper post September 2020

7.1 Accommodation sector expectations on recovery

As a result of the factors outlined in section 2 – opening of international borders; consumer and

business confidence; intention to travel and hygiene and physical distancing measures – the

accommodation industry expectations on recovery are subdued.

The AHS Advisory/Horwath HTL Hotel

Industry Sentiment Survey results

showed that:

40% of hotels anticipated recovery

would take longer than 12 months.

21% of hotels anticipated recovery

would take 9-12 months.

The Dransfield Hotel Futures 2020 advises that ‘demand will now be materially adversely affected,

for a likely period of 9-18 months (which began in Feb 2020), initially to a much higher degree as

border and social controls limit both International and Domestic movement’. Their analysis of the

Melbourne market points to 30-45% reduction in RevPAR (revenue per available room) over the next

12-24 months and 30-50% reduction in RevPAR in Sydney over the same time period.

8

Source: ABS, Characteristics of Employment, cat. no. 6333.0

11

Accommodation Association | 401/105 Pitt Street Sydney NSW 2000| www.aaoa.com.au | 1300 304 397The AHS Advisory/Horwath HTL Hotel Sentiment Survey supported the above. Respondents

anticipated Q3 occupancy of 21% and Q4 occupancy of 31% with RevPAR (revenue)declines in the

order of 37%.

7.2 Accommodation sector recovery impacts on employment

Over the past month owners and operators in the accommodation sector have been undertaking an

analysis of the likely employment impacts post September, given the continued impact on travel

demand expectations of hygiene measures. The AHS Advisory/Horwath HTL Survey pointed to a

rationalisation of staff.

This rationalisation is likely to create significant redundancies post September for a minimum of 6

months until accommodation properties across Australia have achieved improved operating

performances and there is more certainty around the opening of the borders and hygiene and

physical distancing requirements.

12

Accommodation Association | 401/105 Pitt Street Sydney NSW 2000| www.aaoa.com.au | 1300 304 3977.3 Anticipated impact of JobKeeper removal from 30 September 2020

The analysis conducted by employers in the accommodation sector demonstrates the impact on

employment across a range of different types of hotels if:

1. JobKeeper and Fair Work enabling stand down conditions cease.

2. International borders remain closed.

3. Airlines are not operating at full capacity domestically.

4. Occupancies are between 25-35% meaning most rooms remain closed; and

5. Physical hygiene measures remain restrictive not permitting restaurants and

conference/meeting rooms to operate at close to full capacity.

Rooms Type of Hotel BAU Staffing prior Current Staff Staff employed at end of

COVID who qualify for JobKeeper

JobKeeper

209 Upper Upscale 83 43 21

suburban + housekeeping + housekeeping

hotel

138 Upscale 88 47 33

Regional hotel + housekeeping +housekeeping

238 Upscale 91 47 23

City hotel + housekeeping + housekeeping

545 Upper Upscale / 232 126 62

Upscale + + housekeeping + housekeeping

Economy

Suburban hotel

286 Upscale 89 42 26

City hotel + housekeeping + housekeeping

146 Midscale 55 29 23

Serviced + housekeeping + housekeeping

apartment

72 Premium 55 43 25

Serviced + housekeeping + housekeeping

apartment

210 Upscale 90 55 42

+ housekeeping + housekeeping

Note: 3rd party Housekeeping staff utilised

The above modelling undertaken by several businesses shows that most hotels are keeping

approximately 50% of their staff on the books because of JobKeeper, despite operating at

occupancies below 10%.

Post September most hotels are forecasting 30% occupancy. It is likely that without JobKeeper, on

average 70% of those staff who qualified for JobKeeper will be retained, with 30% made redundant

as restrictions on demand continue to impact performance.

The above modelling undertaken by a number of businesses indicates that the removal of

JobKeeper at the end of September will result in approximately 30% of employees currently on

JobKeeper being made redundant because industry performance does not support the

retention of employees without a wage subsidy.

13

Accommodation Association | 401/105 Pitt Street Sydney NSW 2000| www.aaoa.com.au | 1300 304 397The biggest concern for accommodation providers is the deadline of 30th September, as businesses

will not have recovered to even half the levels needed to bring employees back to work and on the

payroll.

We recommend implementing a phased approach for the continuiation of JobKeeper:

Phase 1 - Classification for eligibility is maintained for a minimum of 6 months from 1 October 2020

to 31 March 2021.

a) Further test of Eligibility - A further test at the end of September to demonstrate

eligibility for JobKeeper on an ongoing basis.

Phase 2 - Quarterly BAS reporting of wages to confirm eligibility during the 6-month period.

This phased approach will be essential in helping support the transition for most hotels at the end of

September and recommends the retention of JobKeeper and Fair Work Enabling Stand Down

conditions for a 6-month period post September 2020.

8.0 Conclusion

Our submission clearly outlines the impact of Government measures on the performance of the

industry with most hotels advising that by December they expect occupancies of approximately 30%

and revenue declines of approximately 45%.

The continuation of international border closures, reduced flight capacity, reduced consumer

spending and confidence and reduced business confidence, coupled with physical distancing

restrictions, means that the industry is unlikely to return to pre-COVID levels until 2023.

The industry is seeking support in the 6 months post September period to enable hotels to retain

employees whilst building demand. This connection to employees will be critical in enabling

businesses to bounce back in a timelier way in 2021 and beyond.

Equally important in the retention of JobKeeper will be payment only to those employees who are

connected to the business and able to be deployed. Given the reduced demand, this will also require

a continuation in the flexibility of Fair Work Enabling Stand Down Directions, to enable employers to

direct staff to work for specific periods; to take leave; and to direct a reduction in part time and full

time hours.

Without the above measures many operators will be unable to continue as a going concern.

14

Accommodation Association | 401/105 Pitt Street Sydney NSW 2000| www.aaoa.com.au | 1300 304 397You can also read