COVID-19 LANDSCAPE DETECTING AND COMBATTING FRAUD ACROSS

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

DETECTING AND COMBATTING FRAUD ACROSS THE

COVID-19 LANDSCAPE

NSAA 2021 Conference

June 8, 2021

GILA J. BRONNER, CPA, PRESIDENT AND CEO

BRONNER GROUP, LLC.

Chicago • Atlanta • Albany • Boston • Cleveland • Ft. Lauderdale • Indianapolis • New York • Los Angeles • Philadelphia • Washington, D.C.

AGENDA

▪ WHERE WE’VE BEEN: HISTORICAL PERSPECTIVE OF GOVERNMENT FRAUD

▪ COVID-19 FUNDING

▪ COVID-19 FRAUD: UNIQUE OPPORTUNITIES

▪ COVID-19 FRAUD: DETECTION AND PREVENTION

▪ 2021 AND BEYOND FOR STATE AUDIT

2

FRAUD IN GOVERNMENT IS NOTHING NEW

▪ William “Boss” Tweed

▪ NY State Senator (1868-1873) & political machine Boss

▪ Ran government corruption ring in NYC, convicted of stealing $45M

▪ Whiskey Ring of 1875

▪ Whiskey distillers bribed Treasury Department agents

▪ Hundreds of arrests, including the Supervisor of Internal Revenue

▪ The Crédit Mobilier Scandal of 1872

▪ Congressmen Oakes Ames and James Brooks were bribed by railway

companies to approve federal contracts

▪ Teapot Dome Scandal of 1921

▪ Secretary of the Interior Albert Fall

▪ Accepted bribes for favorable land leasing to oil companies

▪ Edwin Edwards – Governor of Louisiana

▪ Indicted in 1998

▪ Found guilty on 17 counts of extortion, fraud, and racketeering

3

FRAUD IN GOVERNMENT IS NOTHING NEW

▪ Spiro Agnew – Former Vice President

▪ Accepted bribes while governor of Maryland and Vice President

▪ Budd Dwyer – Pennsylvania State Representative

▪ Mail fraud, racketeering, and conspiracy to commit bribery

▪ George Ryan – Governor of Illinois

▪ Convicted of racketeering, fraud, and taking payoffs and gifts in

return for contracts

▪ City of Chicago Alderman

▪ Since 1972, 30 Chicago alderman have been convicted of, or pleaded

guilty to crimes relating to official duties

▪ Rod Blagojevich – Governor of Illinois

▪ Took bribes to fill a vacant US Senate seat, sentenced to 14 years in

federal prison

4

FRAUD IN GOVERNMENT IS NOTHING NEW

▪ Rita A. Crundwell, Comptroller and Treasurer of Dixon, IL

▪ Over $53 Million stolen from 1991 to 2012

▪ Average of $5 million per year

▪ More than half of Dixon’s operating budget

▪ More than the police and fire budgets combined

▪ Public Money financed her lavish lifestyle

▪ $2 million luxury motor home

▪ Over 400 prize winning horses worth millions

▪ People at City Hall trusted and respected Crundwell

▪ Rose through the ranks at City Hall

▪ Auditors did not notice lack of internal controls and

BEFORE AFTER segregation of duties

▪ Audits were sent to IL Comptroller, who compiled them,

but did not look carefully

5

COVID-19: A LOT OF THE SAME AND MORE

MAY 28, 2021 WASHINGTON, DC – Deputy Attorney General Convenes Inaugural Meeting of the COVID-19 Fraud

Enforcement Task Force. The DOJ has charged nearly 600 defendants to date with crimes related to COVID-19

fraud involving over $600 million in 56 federal districts.

MAY 28, 2021 MIAMI, FL – Florida Man Charged with Stealing Ventilators Intended for Critically Ill Covid-19

Patients in El Salvador Arrested in Texas.

MAY 6, 2021 NEW YORK CITY, NY – New York City Man Charged with Nearly $4 Million COVID-19 Relief Fraud

Scheme and Money Laundering.

MAY 4, 2021 CLEVELAND, OH – Six Charged with Fraudulently Seeking to Obtain $9 Million in COVID-Relief

Funding.

MARCH 8, 2021 PHOENIX, AZ – Fraud continues in Arizona's unemployment system a year into the COVID-19

pandemic.

APRIL 6, 2021 DAVENPORT, FL – Florida couple charged in $5.8 million COVID relief fraud.

MARCH 26, 2021 MIAMI, FL – 24 accused of COVID-19 relief fraud in South Florida, including ex-NFL receiver.

MARCH 26, 2021 SPRINGFIELD, MO – More Charges Against State Lawmaker for $900,000 COVID-19 Fraud

Scheme at Springfield Health Care Charity.

JAN. 25, 2021 SACRAMENTO, CA – California officials said Monday they have confirmed that $11.4 billion in

unemployment benefits paid during the COVID-19 pandemic involve fraud — about 10% of benefits paid.

6

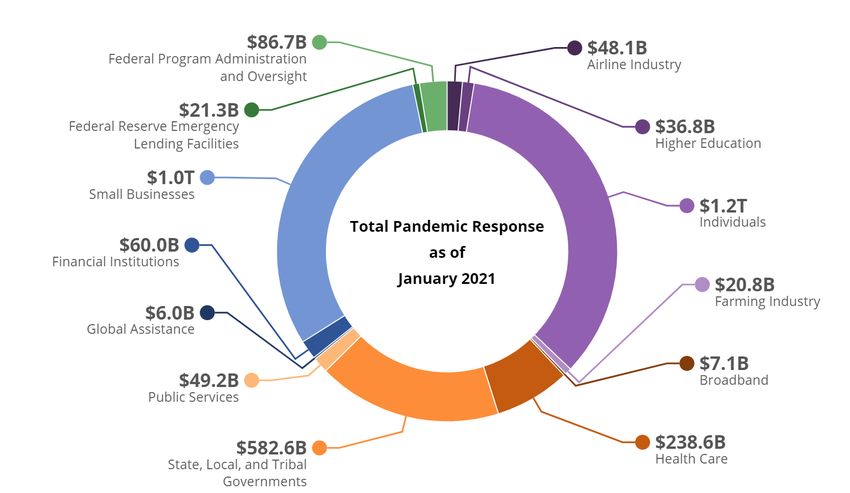

COVID-19 FUNDING: TIMELINE

$5T+ Total in COVID-19 Relief Funding

March 27, 2020 March 11, 2021

March 13 & 15, 2020

January 29, 2020 $2.1T Coronavirus Aid, $1.9T American

National Emergency

HHS declares Public Relief, and Economic Rescue Plan Act

declared

Health Emergency Security (CARES) Act (ARPA)

CDC guidelines

March 6, 2020 December 27, 2020

$7.8B The Coronavirus March 18, 2020

$900B Coronavirus

Preparedness and $15.4B Families First

Response and Relief

Response Coronavirus Response

Supplemental

Supplemental Act

Appropriations Act

Appropriations Act

7

COVID-19 FUNDING: CARES ACT FROM A FRAUD FOCUS

The CARES Act legislation included $2 trillion in funding, much of which was targeted to

or available for state and local governments to respond to COVID-19.

Coronavirus Relief Fund Education Stabilization Fund

Paycheck Protection Program

• $150 billion • $30.75 billion

• $350 billion ($300b later added)

• Direct funding to states and local • $14 billion to Higher education

• Grants to businesses to cover

governments with over 500k • $13 billion to K-12

payroll, critical operating expenses

population • $3 billion to Governors

Economic Stabilization Fund Housing & Urban Development Economic Development Admin.

• $454 billion • $17 billion • $1.5 billion

• Loans and loan guarantees to • CDBG, ESG, and HOPWA • Support local econ. development and

support state and local • Public Housing, Section 8 public works investment

governments • Elderly, disabled housing • State, local governments eligible

FEMA Disaster Relief Fund

Public Health Funding Election Assistance Grants

• $45 billion

• $1.5 billion for states (CDC) • $300 million

• Assistance to state and local

• $100 billion to healthcare providers • State and local election assistance

governments for reimbursement

• $1 billion to CSBG • Help America Vote Act formula

of emergency expenses

8COVID-19 FUNDING: CARES ACT FROM A FRAUD FOCUS

$3T+ Total

9COVID-19 FUNDING: AMERICAN RESCUE PLAN ACT (ARPA)

$1.9T Total

10COVID-19 FRAUD

WHY INCREASED FRAUD NOW?

1. Unprecedented amount of money spread across a variety of pots

2. Increased motivation, opportunity, rationalization, and capability

3. New funding streams going to governments without sufficient expertise and/or

adequate capacity

4. Large amount of people working remotely or unemployed

5. Increased time pressure to expend funds

6. Lack of timely/sufficiently clear guidance

11COVID-19 FRAUD

TYPICAL FRAUD SCHEMES RELATED TO THE COVID-19 PANDEMIC

▪ COVID-19 Assistance Grants and Loans (e.g., Small Business Grants) fraud

▪ Unemployment Insurance (UI) fraud

▪ Fake CDC or government emails

▪ Phishing Emails

▪ Charitable contributions

Auditors should consider potential fraud

▪ General financial relief

with respect to various funding streams

▪ Airline carrier refunds

▪ Fake cures and vaccines

▪ Fake testing kits

▪ Counterfeit Treatments or Equipment

▪ Identify theft

12COVID-19 FRAUD

WHAT TO LOOK FOR

Return to work but not notifying unemployment

Shell businesses; collusion between employee and employer with fake identifies.

Falsified payroll documentation

Fictitious entities

Created fake tax documents

Illicit restoration of defunct entities

Stolen Identities

Falsified ownership of legitimate businesses

Paying fictitious vendors

Ghost employees

Ghost students

Misappropriation of funds

13COVID-19 FRAUD: DETECTION AND PREVENTION

Key focus for State Auditors: Identifying changes in risks and controls; building the

necessary information sharing relationships and frameworks to detect and prevent

fraud; and, identifying changes in policies and systems

Measures to mitigate and detect fraud are vital to ensure that COVID-19 pandemic relief

efforts are effective and benefit the most negatively impacted and vulnerable:

▪ Fraud prevention efforts must consider the importance of speed in an emergency

▪ Governments can implement longer term assurance mechanisms targeted to new

programs and activities

▪ It is critical that governments share information as fraudsters often target multiple

programs and use common methodologies

▪ Identifying and testing vulnerabilities at both the control and program level

14COVID-19 FRAUD: DETECTION AND PREVENTION

ADDRESSING COVID-19 PANDEMIC-RELATED FRAUD

Adjust fraud detection and prevention

Identify fraud risks

▪ Apply a COVID-19 lens

strategies and approaches

▪ Consider available fraud and compliance

▪ What processes and controls are new or

resources

changed?

▪ Be aware of the shift from detection measures

▪ Target new processes

for emergency (short-term) relief vs longer

▪ What emergency decisions were made?

term

Educate staff on threats

▪ Ensure staff are aware of new and evolving Look at vendors and contractors

threat areas ▪ Are they able to manage their own fraud risks

▪ Increase focus on cyber threats ▪ Possible risks of vendor account takeovers,

▪ Educate staff on how to detect and respond supplying substandard goods, access to assets

▪ Ensure audit teams are well versed in relevant and sensitive information

compliance and other requirements

15COVID-19 FRAUD: DETECTION AND PREVENTION

QUESTIONS FOR CONSIDERATION

1. Do the entities you audit have risk management programs in place to identify and

address existing risks, including any new fraud risks arising from the additional

funding received from federal and other sources?

2. Are the risk management programs currently in place entity-wide and effective in

complying with federal Green Book requirements?

3. Are auditors performing audits of these risk management programs and providing

feedback to management and governing bodies?

4. Do the auditors have risk assessment processes in place to identify and report on

the risks impacting an audited entity, including those arising from the additional

funding received from federal and other sources?

5. How has the rapid pace of this new funding impacted critical control systems,

including staffing, procurement, and expenditure processing?

6. Do the entities you audit have risk management programs in place to identify and

address risks at the subrecipient level, including new fraud risks arising from the

additional funding received from federal and other sources?

16COVID-19 FRAUD: DETECTION AND PREVENTION

QUESTIONS FOR CONSIDERATION (CONT.)

7. Do the auditors have risk assessment processes in place to identify and address

fraud risks at the subrecipient level whenever the subrecipients are financially

material to the entity being audited?

8. Do the entities you audit have processes in place to ensure all subrecipients are

submitting federal Single Audit reports whenever required? [NOTE that the

additional federal funding being received by smaller entities is expected to cause a

major increase in the number of entities subject to Single Audit requirements]

9. Do the entities you audit have processes in place to ensure all subrecipient federal

Single Audit reports are reviewed and corrective action is tracked until audit

findings have been resolved?

10. Do the state auditors have adequate procedures in place over the receipt and

review of federal Single Audit reports for financially significant subrecipients?

11. How should the audited entities (and the state auditors) address fraud risks for

subrecipients that fall below the Single Audit threshold?

12. Given all of the above, how should each state auditor modify its approach to risk in

general, and with respect to individual audit engagements?

172021 AND BEYOND FOR STATE AUDIT

WHAT’S NEXT? ▪ New/changing federal relief

▪ Continuing workforce disruption programs/requirements

▪ Remote/hybrid workplace and audit ▪ Rising demands for transparency and

process dynamics accountability

▪ Adjusting to a new normal ▪ Heightened presence of federal auditors

▪ Increasing relevance of the fraud triangle

18THANK YOU!

You can also read