COVID-19 COMPLIANCE UPDATE - Rochelle Alcon, CPA Hattie Mitchell, CPA, CFE The information provided herein is for informational purposes only and ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

COVID-19 COMPLIANCE UPDATE Rochelle Alcon, CPA

Hattie Mitchell, CPA, CFE

The information provided herein is for informational purposes only and should not be construed as financial, investment, tax, accounting or legal advice.

OVERVIEW

Background

Different types of COVID-19 funding through new or existing

programs

Updates to new COVID-19 related funding

Audit considerations

Resources

2

BACKGROUND

Five relief laws, including the CARES Act, have been enacted as of

January 31, 2021

As of January 31, 2021, of the $3.1 trillion appropriated by these five laws

for COVID-19 relief, the federal government had obligated a total of $2.2

trillion and expended $1.9 trillion, as reported by federal agencies

CARES Act includes a provision for GAO to report on its ongoing

monitoring and oversight efforts related to the COVID-19 pandemic

Sixth relief law in March 2021: American Rescue Plan Act of 2021

3

Excellence

BACKGROUND (CONT’D)

OMB issued guidance beginning in March 2020 that identified

temporary exceptions to grants management requirements Federal

agencies could make available to their grantees, as the agencies

deemed appropriate and to the extent permitted by law

OMB made most of these exceptions available for between 3 and 5

months; all have been rescinded or expired as of December 2020.

4

BACKGROUND (CONT’D)

OMB issued Promoting Public Trust in the Federal Government

through Effective Implementation of the American Rescue Plan

Act and Stewardship of the Taxpayer Resources, M-21-20

(Washington, D.C.: Mar. 19, 2021).

Appendices:

Management of Payment Integrity Risk

Achieving More Equity-Oriented Results

Disaster Relief Flexibilities to Reduce Burden

5COVID-19 FUNDING – (THROUGH FIRST 4

RELIEF BILLS)

2020 Compliance Supplement Addendum

Includes the 14 COVID-19 funded programs and one new non-COVID-19

program highlighted in yellow.

Part 2 matrix shows 8 new COVID-19 funded programs, 6 pre-existing

program supplements to which COVID-19 funding and compliance

requirements have been added, and 1 new non-COVID-19 program.

Part 4 coverage of new or existing programs with new compliance

requirements as a result of COVID-19 funding.

6COVID-19 FUNDING – LARGEST 4 NEW PROGRAMS

Payment Protection Program Provider Relief Fund

($>600B) ($175B)

Federal Agency: SBA Federal Agency: HHS

For-profits, NFPs For-profits, NFPs, Governmental Entities

Is NOT subject to Single Audit IS subject to Single Audit

CFDA No: 59.073 CFDA No: 93.498

Coronavirus Relief Fund Educational Stabilization Fund

($150B) ($>600B)

Federal Agency: Treasury Federal Agency: Education

Governmental Entities and Tribes States, Schools, IHE

IS subject to Single Audit IS subject to Single Audit

CFDA No: 21.019 CFDA No: 84.425CORONAVIRUS RELIEF FUND (CRF) – 21.019

Purpose of the Coronavirus Relief Fund (the Fund) is to provide

direct payments to state, territorial, tribal, and certain eligible

local governments to cover:

Necessary expenditures incurred due to the public health emergency

with respect to Coronavirus Disease 2019 (COVID–19);

Costs that were not accounted for in the government’s most recently

approved budget as of March 27, 2020; and

Costs that were incurred during the period that begins March 1, 2020.

8CORONAVIRUS RELIEF FUND (CRF) – 21.019

9CORONAVIRUS RELIEF FUND (CRF) – 21.019

Guidance started to level out with the last updates to the FAQs

dated 10.19.20

U.S. Treasury issued guidance on 11.20.20 to help clarify

beneficiary vs. sub-recipient, i.e., beneficiaries not subject to

single audit

U.S. Treasury issued guidance on 11.25.20 to help clarify

reporting and recording keeping (Grant Solutions)

1.15.21 – CRF Guidance, Q&A and updates from CAA 2021

published in the Federal Register

10PROVIDER RELIEF

FUND – 93.498

The Provider Relief Fund (PRF) is

administered by the Health Resources

and Services Administration (HRSA) and

provides relief funds to hospitals and

other healthcare providers, including

those on the front lines of the

coronavirus response. The funding

supports healthcare-related expenses or

lost revenue attributable to COVID-19

and ensures that uninsured Americans

can get treatment for COVID-19.

11PROVIDER RELIEF FUND – 93.498

12PROVIDER RELIEF FUND – 93.498

Generally, expenditures are reported on the SEFA when costs

(or lost revenue, as applicable) are incurred and an award is

determined to exist (except for PRF)

Impacts what is reported on the SEFA

Difference between accounting records and SEFA, reconcile with footnote

13SOME EXISTING PROGRAMS ALSO HAD COMPLIANCE

REQUIREMENT CHANGES DUE TO COVID-19

Student Financial Assistance Cluster (SFA)

USDA food programs

Certain HUD housing program

Assistance

2020 Compliance Supplement

14CAA FY 2021 – SIGNIFICANT RELIEF PROVISIONS

Summary of Tribal Related Provisions

Economic Assistance – CRF extension, Unemployment and

Small Business

Health Care

Agriculture and Nutrition

Housing

Education

Broadband

15AMERICAN RESCUE PLAN ACT (ARPA)

Signed into law March 11, 2021

$1.9 Trillion in federal relief/stimulus

$350 Billon allocated to states, local and tribal governments

$20 Billion to Tribal Governments

Funding more directly provided to local governments

16AMERICAN RESCUE PLAN ACT (ARPA)

Issued May 10, 2021

$20 billion reserved for Tribes will be allocated as follows:

Treasury will equally divide $1 billion among all eligible Tribal

Governments

Not using HUD IHBG numbers

Remaining $19 billion allocation will be based 1) Enrollment and

2)Employment data

17AMERICAN RESCUE PLAN ACT (ARPA)

Issued May 10, 2021 – Payment Schedule

Payment #1

Equal allocation of each Tribal government from the $1 billion

Tribal government’s pro rata share of the 65% of $19 billion ($12.35

billion) based on tribal enrollment

Payment #2

Tribal government’s pro rata share of the reaming 35% of the $19

billion ($6.65 billion) based on Tribal employment (2019 numbers)

18AMERICAN RESCUE PLAN ACT (ARPA)

Breaking News – issued May 10, 2021 – Due dates

Payment #1

The deadline to complete the first submission is June 21, 2021 at 11:59

PM PST (more of a request of recovery monies)

Payment #2

The deadline for confirming or amending a Tribal government’s 2019

employment numbers is July 9, 2021 at 11:59 PM PST. If a Tribal

government does not confirm or amend employment numbers by that

deadline, the Tribal government will not be eligible to receive a share

of the employment allocation.

19AMERICAN RESCUE PLAN ACT (ARPA)

U.S. Department of the Treasury will host an Information

Session on the Reporting and Compliance of $20 billion State

and Local Fiscal Recovery Funds to Tribal Governments – June

28, 2021 3:00- 4:00pm (Eastern Time)

20AMERICAN RESCUE PLAN ACT

Eligible Uses:

To respond to the public health emergency or its negative economic

impacts

To respond to workers performing essential work during the COVID-19

public health emergency by providing premium pay to eligible workers

For the provision of government services to the extent of the

reduction in revenue due to the COVID–19 public health emergency

relative to revenues collected in the most recent full fiscal year prior to

the emergency, and

To make necessary investments in water, sewer, or broadband

infrastructure

21AMERICAN RESCUE PLAN ACT

Ineligible Uses:

Cannot be spent on state or local pensions

State governments are prohibited from spending to replace revenue

declines resulting from tax cuts enacted since March 3, 2021

22AMERICAN RESCUE PLAN ACT

From the U.S. Treasury Interim Guidance

Costs incurred. A cost shall be considered to have been incurred for purposes

of paragraph (a) of this section if the recipient has incurred an obligation with

respect to such cost by December 31, 2024

Return of funds. A recipient must return any funds not obligated by

December 31, 2024, and any funds not expended to cover such obligations

by December 31, 2026.

Unliquidated financial obligations means, for financial reports prepared on a cash

basis, financial obligations incurred by the non-Federal entity that have not been paid

(liquidated). For reports prepared on an accrual expenditure basis, these are financial

obligations incurred by the non-Federal entity for which an expenditure has not been

recorded (Section 200.1 of Uniform Guidance)

23AMERICAN RESCUE PLAN ACT

Reporting Requirements

Subject to the provisions of the Uniform Administrative Requirements,

Cost Principles, and Audit Requirements for Federal Awards (2 CFR

200) (the Uniform Guidance)

Certain regular reporting requirements (depending on the use)

Additional Guidance from Treasury

Increased oversight (OIG office and/or new Office)

Final Regulations still pending

24AMERICAN RESCUE PLAN ACT – OTHER

Look at community needs

ARPA funding is temporary, so its use should be focused on

non-recurring expenditures

Consider an investment plan for the funding

Expect and prepare for change in guidance

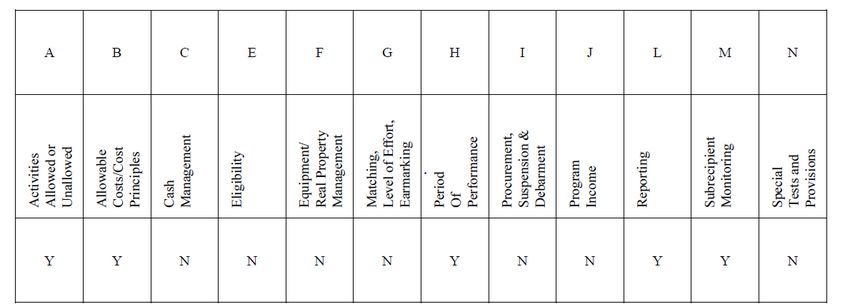

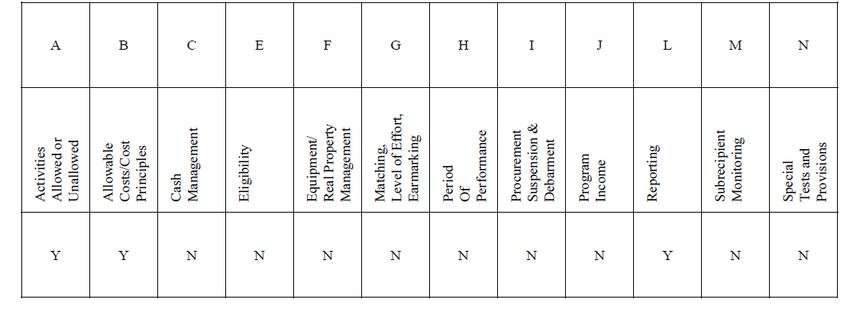

25AUDIT CONSIDERATIONS

What COVID-19 funding has the Tribe received?

Through existing awards or new awards

What COVID-19 funding is subject to Single Audit?

Nontraditional awards, such as the Coronavirus Relief Fund, Provider Relief

Fund and Educational Stabilization Fund are subject to Single Audit

However, the Payment Protection Program Loan is not subject to Single Audit

Is COVID-19 funding recorded in separate funds and/or programs?

This is important so the Tribe can keep track of which funding belongs to

which nontraditional or traditional awards

Ensures the Tribe is not double-dipping

26AUDIT CONSIDERATIONS (CONT’D)

SEFA Preparation – separately identify funding sources specifically

related to COVID-19 by Assistance Listing Number and Title

What documentation is available to determine program

requirements?

Treasury FAQs, OMB Memos, Supplemental Fact Sheets, Guidance

Documents, Federal Agency Websites, GASB Technical Bulletins, etc.

Can the audit continue to be performed remotely due to COVID-19

restrictions?

Creatively, audits often can be done remotely!

27OTHER CONSIDERATIONS …

Treasury continues to update and issue guidance.

OMB has issued the 2021 Compliance Supplement.

Know what your reporting requirements are

Ensure written justification documentation.

Implement/revise policies and procedures to support

costs/expenditures charged to each program

Know how the expenditures tie into the pandemic

28Resources

RESOURCES

AICPA – Governmental Audit Quality Center (GAQC)

Treasury and Treasury OIG Resources (website)

OMB Compliance Supplement/Addendum and related guidance

CFRs and actual legislation signed by the President

Treasury’s OIG Resources (Reporting)

GASB Technical Bulletin No. 2020-1

Department of Treasury Interim Final Rule (ARPA)

2 CFR Revised FAQ (www.cfo.gov/financial-assistance/)

29Hattie Mitchell, CPA, CFE Rochelle Alcon, CPA

Senior Manager, Principal

Tribal Consultant ralcon@redw.com

hattie.mitchell@redw.com 505.998.3486

623.469.0058

QUESTIONS? Ask us!

30You can also read