Coles Group Property Developments Pty Ltd - Beerwah Homemaker Centre Economic Need and Impact Assessment 9 October 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

p Coles Group Property Developments Pty Ltd Beerwah Homemaker Centre Economic Need and Impact Assessment 9 October 2019

Table of Contents

Table of Contents

Section 1 Introduction ............................................................................................................................................. 1

1.1 Report Structure................................................................................................................................................. 3

Section 2 Trade Area Overview ................................................................................................................................ 4

2.1 Trade Area Definition ......................................................................................................................................... 4

2.2 Socio‐Economic Overview of Trade Areas ......................................................................................................... 6

2.3 Population and Household Projections .............................................................................................................. 9

2.3.1 Scenario One Population and Household Projections .......................................................................................................... 9

2.3.2 Scenario Two Population Projections ................................................................................................................................. 10

2.4 Implications for Retail Demand........................................................................................................................ 11

Section 3 Centres Network .....................................................................................................................................12

3.1 Centres Hierarchy............................................................................................................................................. 12

3.1.1 Planning Scheme Centres Zones ......................................................................................................................................... 12

3.2 Existing Centres ................................................................................................................................................ 13

3.2.1 Major Centres ..................................................................................................................................................................... 14

3.2.2 District Centres ................................................................................................................................................................... 14

3.2.3 Local Centres ...................................................................................................................................................................... 14

3.2.4 Specialised Centres ............................................................................................................................................................. 16

3.2.5 Township Zone ................................................................................................................................................................... 16

3.2.6 Other Centres ..................................................................................................................................................................... 16

3.3 Approved and Designated Centres .................................................................................................................. 16

3.3.1 Beerwah Shopping Complex ............................................................................................................................................... 16

3.3.2 Mooloolah Valley IGA Expansion ........................................................................................................................................ 17

3.3.3 Potential Beerwah East Centres ......................................................................................................................................... 17

Section 4 Retail Expenditure Analysis......................................................................................................................18

4.1 Weekly Household Retail Expenditure ............................................................................................................. 18

4.2 Annual Available Expenditure .......................................................................................................................... 19

4.3 Market Share Analysis and Centre Performance‐Supermarket & Related Uses and Fast Food Pads .............. 21

4.3.1 Supermarket Analysis ......................................................................................................................................................... 21

4.3.2 Retail Showroom Analysis .................................................................................................................................................. 22

4.3.3 Fast Food Pad Sites ............................................................................................................................................................. 23

4.3.4 Centre Performance ........................................................................................................................................................... 24

4.4 Floor Space Demand for Bulky Goods and Retail Showrooms on Balance Land.............................................. 25

Section 5 Impact Assessment ..................................................................................................................................28

5.1 Impact Defined ................................................................................................................................................. 28

5.2 Impact of Supermarket & Related Uses and Fast Food Pad Sites Components of the Development ............. 29

ii

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docx

Figures

Section 6 Sequential Site Test .................................................................................................................................31

Section 7 Need and Other Benefits .........................................................................................................................38

7.1 Economic Need ................................................................................................................................................ 38

7.2 Community Need ............................................................................................................................................. 38

7.3 Planning Need .................................................................................................................................................. 39

7.4 Employment Related Impacts .......................................................................................................................... 39

Appendix A – Alternative Available Expenditure and Supportable Floor Space Estimates ........................................41

Scenario Two Estimates .................................................................................................................................................... 41

Figures

Figure 1‐1 Concept Masterplan for Beerwah Homemaker Centre .................................................................................................. 2

Figure 2‐1 Geographic Definition of the Trade Areas and Location of Centres ............................................................................... 5

Figure 6‐1 Vacant Land and Houses within Peachester Local Centre Zone ................................................................................... 33

Figure 6‐2 Vacant Land and Houses within Mooloolah Valley Local Centre Zone ......................................................................... 34

Figure 6‐3 Vacant Land and Houses within Landsborough Local Centre Zone and Landsborough Specialised Centre Zone ........ 35

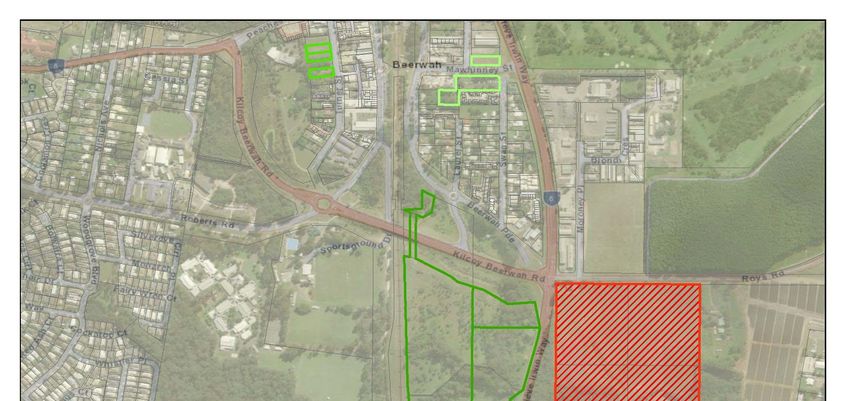

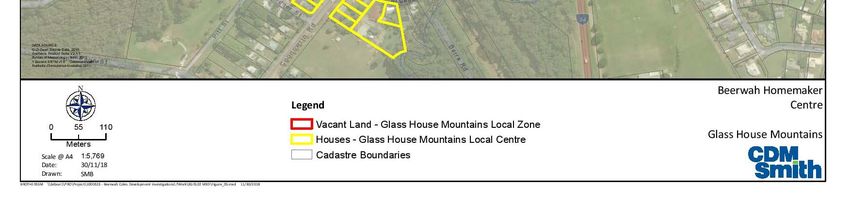

Figure 6‐4 Vacant Land and Houses within Glass House Mountains Local Centre Zone ............................................................... 36

Figure 6‐5 Vacant Land and Houses within Beerwah Centres Zones............................................................................................. 37

Tables

Table 2‐1 Socio‐economic profile, PTA, STA North, STA South, Sunshine Coast LGA and Queensland, 2016 Census .................... 7

Table 2‐2 Scenario One population and household projections, PTA, STA North, STA South, Sunshine Coast LGA and

Queensland 2018 to 2031 ............................................................................................................................................ 10

Table 2‐3 Scenario Two population and household projections, PTA, STA North, STA South, Sunshine Coast LGA and

Queensland, 2018 to 2031 ........................................................................................................................................... 11

Table 3‐1 Retail floor space in trade areas by centre type, anchor tenants and distance from subject site................................ 13

Table 4‐1 Available weekly household expenditure ($ per household, 2018 dollars) by trade area, 2018‐2031 ........................ 18

Table 4‐2 Annual available expenditure by retail category ($m), 2018‐2031 (2018 dollars) ....................................................... 20

Table 4‐3 Available supermarket expenditure, 2018‐2031 .......................................................................................................... 21

Table 4‐4 Supermarket market share analysis, 2021‐2031 ($M) ................................................................................................. 22

Table 4‐5 Available showroom and bulky goods related expenditure, 2018‐2031 ($M) ............................................................. 23

Table 4‐6 Retail showroom market share analysis, 2021‐2031 ($M) ........................................................................................... 23

Table 4‐7 Available dining and take‐away food expenditure, 2018 to 2031 ($M) ....................................................................... 24

Table 4‐8 Fast food pad site market share analysis, 2021 to 2031 .............................................................................................. 24

Table 4‐9 Supermarket & Related Uses and Fast Food Pad Sites‐Centre Performance, 2021 to 2031 ($M) ............................... 25

Table 4‐10 Estimated Bulky Goods Expenditure ($m, 2018 dollars) and Supportable Bulky Goods Floor Space (sqm), Main Trade

Area, 2018‐2031 ........................................................................................................................................................... 27

Table 5‐1 Trading impacts of the proposed Supermarket & Related Uses and Fast Food Pad Sites, 2021 .................................. 30

Table 6‐1 Outcomes Sequential Site Test, Summary of Results ................................................................................................... 31

iii

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docx

Tables

Printed: 17 October 2019

Last Saved: 17 October 2019

File Name: CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVF 091019

Author: Shelley McCormack

Project Manager: Marcus Brown

Client: Coles Group Property Developments Pty Ltd

Document Title: Beerwah Homemaker Centre Economic Need and Impact Assessment

Document Version: Rev G

Project Number: 1000323

iv

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docx

Introduction

Section 1 Introduction

CDM Smith was engaged by Coles Group Property Developments Ltd to prepare an economic need and impact

assessment associated with multiple applications over land at 8 Roys Road, Beerwah. Ultimately the development

would be known as the Beerwah Homemaker Centre. The applications include a variation application over the entire

site to override the planning scheme and designate the land as Specialised Centre. The variation application will be

accompanied by applications for two development permits, including:

Coles supermarket (3,768 sqm) and Showroom (600 sqm)‐described herein as supermarket and related uses;

Fast food pad sites (2)(combined GFA of 588sqm); and

Service station (co‐located with one of the fast food pad sites).

The remaining land outside of the supermarket and related uses and the fast food pad sites that are subject to the

applications for development permits, is anticipated to accommodate predominantly bulky goods and retail

showrooms with complementary and ancillary uses. It is envisaged that the balance of the site would be developed

over a number of stages.

Shaping SEQ identifies Beerwah as a Major Activity Centre. Under the regional plan, Major Activity Centres are,

among other things, intended to fulfil higher order retail functions. Despite this, Beerwah’s highest order retailer is a

full line Woolworths supermarket. The Beerwah Major Activity Centre currently does not fulfil its intended role and

function. A key reason for this is the constrained nature of Beerwah centre zones, with there being limited

opportunities for new development within centre zones, particularly those of a scale that would contribute to

Beerwah meeting its Major Activity Centre role and function. The addition of a Coles supermarket and additional

retail showrooms within Beerwah would contribute to moving Beerwah towards achieving its intended role and

function.

CDM Smith’s brief was limited to assessing the economic need and impact for the Coles supermarket, showroom and

fast food pad sites on the subject site. Additionally, our brief was to consider the future demand for retail showrooms

on the balance of the land covered by the variation application.

Figure 1‐1 provides an outline of the concept masterplan for the Beerwah Homemaker Centre.

1

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docx

Introduction

Figure 1‐1 Concept Masterplan for Beerwah Homemaker Centre

2

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docx

Introduction

1.1 Report Structure

This report is structured as follows:

Section 1 – Introduction: This section provides an overview of the structure of the report and a summary of the

purpose of the study;

Section 2 – Trade Area Overview: This section provides an assessment of the defined trade areas for the

proposed Coles based component of the development and bulky goods retail development, including an analysis

of the demographic and socio‐economic characteristics of the defined trade area(s) and population projections

under three alternative scenarios;

Section 3 – Centres Network: The purpose of this chapter is to identify the existing, approved and designated

centres network servicing the identified trade areas for the Beerwah Homemaker Centre;

Section 4 – Retail Expenditure Analysis: This section reports the results of the retail expenditure modelling

undertaken to estimate the available retail expenditure within the trade area(s). The chapter also provides a high

level assessment of the potential supportable floor space on the subject site;

Section 5 – Impact Assessment: This section estimates the anticipated trading impacts of the proposed

development on the centres network;

Section 5 – Sequential Site Testing: This section provides an overview of potential alternative zoned sites within

the trade area(s) that could potentially accommodate a development of a similar scale to the Beerwah

Homemaker Centre; and

Section 6 – Need and Other Benefits: This section provides an assessment of the need for the proposed

development and other relevant benefits.

3

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docx

Trade Area Overview

Section 2 Trade Area Overview

2.1 Trade Area Definition

The trade area(s) for the Beerwah Homemaker Centre have been defined having regard to the following key factors:

Existing retail centres network, including existing, approved and designated centres;

Layout of the proposed development and relationship to site access;

Existing road network and accessibility of the site to the surrounding area;

Co‐location with or proximity to any other core attractors;

Location, role and function of surrounding centres, including existing, approved and designated centres;

Physical or psychological barriers that might impede custom, such as potential severance created by the Bruce

Highway; and

Australian Bureau of Statistics geographic boundaries, for which Census data is available.

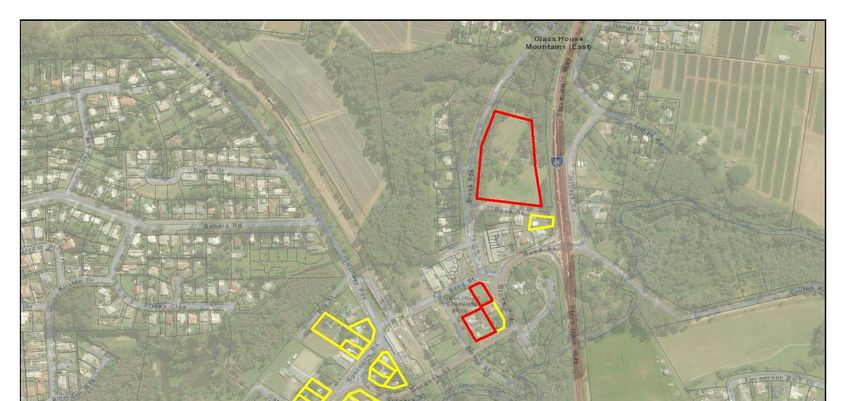

There have been three trade areas defined for the Beerwah Homemaker Centre, these being the Primary Trade Area

(PTA), Secondary Trade Area North (STA North) and Secondary Trade Area South (STA South), with the combined

three trade areas referred to as the main trade area.

The PTA is comprised of the suburbs of Beerwah and Peachester. The STA North comprises the state suburbs of

Landsborough, Mooloolah Valley and Mount Mellum. The STA South comprises the suburbs of Glass House

Mountains and Beerburrum. Figure 2‐1 illustrates the Primary Trade Area (PTA), Secondary Trade Area North (STA

North) and Secondary Trade Area South (STA South) as well as the location of the Beerwah Homemaker Centre and

existing centres servicing the trade areas.

The trade areas encompass land that is identified as part of the Beerwah East Identified Growth Area. Development

of this growth area would have implications for retail demand and potentially centres network planning in and around

Beerwah. The Beerwah East Identified Growth Area is not anticipated to see development commence until after

supermarket and related uses and fast food pad sites of the Beerwah Homemaker Centre are completed. However,

the potential growth associated with Beerwah East Identified Growth Area has implications for future development of

the remainder of the site subject to the variation application. Hence, this report includes a baseline scenario informed

by 2018 edition QGSO population projections and a ‘growth’ scenario that assumes the Beerwah East Identified

Growth Area sees development commence in 2023.

4

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docx

Trade Area Overview

Figure 2‐1 Geographic Definition of the Trade Areas and Location of Centres

5

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docx

Trade Area Overview

2.2 Socio‐Economic Overview of Trade Areas

The demographic and socio‐economic characteristics of the trade area populations as of the 2016 Census,

benchmarked to Sunshine Coast LGA and Queensland are summarised below:

As of the 2016 Census, the average age of residents within the trade area was lower than in the Sunshine Coast

LGA, but higher than in Queensland. Within the trade areas, the average age was lowest in the STA North (39.4

years) and highest in the STA South (41.2 years);

There was a significantly higher incidence of couple families with children in the PTA relative to both Sunshine

Coast LGA and Queensland, with couple families with children representing 44.6% of all households in the PTA

compared with 39.4% in the Sunshine Coast LGA and 42.5% in Queensland. The incidence of single parent

families in both the PTA and STA South was significantly lower than Sunshine Coast LGA and Queensland;

The average household size in all trade areas was 2.9 persons per household as of the 2016 Census, marginally

higher than the Sunshine Coast LGA and Queensland. Additionally, the average number of vehicles per

household in the trade areas was between 2.0 and 2.1 vehicles per household, higher than regional and state

averages;

In 2016, the incidence of households with a mortgage was significantly higher in all trade areas relative to the

Sunshine Coast and Queensland, and highest in the STA North at 44.9% of households. The incidence of rental

households in the STA North and STA South was significantly lower than in the Sunshine Coast LGA and

Queensland;

Average monthly housing loan and weekly rent payments were similar across all trade areas and lowest in the

STA North;

Average weekly household incomes were significantly lower in the PTA compared with Sunshine Coast LGA and

Queensland, at $1,495, $1,564 and $1,688 per week respectively;

In 2016, households within the PTA spent an average of 16.7% of their household income on housing costs,

compared to 16.2% in Sunshine Coast LGA and 15.5% in Queensland;

The incidence of household income spent on housing costs was lowest in the STA South at 14.8% and highest in

the PTA at 16.7% of total household income;

Average household incomes after adjusting for housing costs were higher in the STA North and STA South

relative to the Sunshine Coast LGA average;

As at the 2016 Census, the incidence of full time employment in the STA South was significantly higher than the

other trade areas and Sunshine Coast LGA;

The unemployment rate was similar in all trade areas analysed, and lowest within the PTA at 6.9%. The labour

force participation rate in the STA North was significantly higher than the other trade areas and Sunshine Coast

LGA but in line with the Queensland average;

The trade areas were characterised by a lower incidence of upper white collar workers1 and a higher incidence of

lower blue collar workers relative to the Sunshine Coast LGA and Queensland;

In 2016, the incidence of persons aged 15 years and over with a post school qualification was lower in all the

trade areas relative to Sunshine Coast LGA and Queensland, with a lower incidence of persons with a Bachelor or

higher qualification. On the other hand, the incidence of certificate holders was higher in all trade areas relative

to regional and state averages;

1 Upper white collar workers comprise the occupations of managers and professionals. Lower blue collar workers comprise the

occupations of machinery operators & drivers and labourers.

6

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docxTrade Area Overview

Residents in the trade areas were most likely to be employed within the health care and social assistance,

construction and retail trade sectors. The incidence of employment within the agriculture, forestry and fishing

sector in the PTA and STA South was significantly higher than in the STA North, Sunshine Coast LGA and

Queensland;

Table 2‐1 details the demographic and socio‐economic profile of the PTA, STA North and STA South benchmarked to

Sunshine Coast LGA and Queensland as of the 2016 Census.

Table 2‐1 Socio‐economic profile, PTA, STA North, STA South, Sunshine Coast LGA and Queensland, 2016 Census

PTA STA North STA South Sunshine Queensland

Coast LGA

Population 8,201 7,575 5,838 294,367 4,703,193

Age Distribution

0‐4 years 6.2% 6.1% 5.1% 5.3% 6.3%

5‐9 years 7.4% 6.8% 6.9% 6.4% 6.7%

10‐14 years 6.6% 6.8% 6.7% 6.4% 6.4%

15‐19 years 6.1% 6.4% 7.0% 6.0% 6.3%

20‐24 years 5.1% 5.4% 4.9% 5.2% 6.7%

25‐34 years 11.7% 10.3% 9.5% 10.6% 13.8%

35‐44 years 12.3% 14.2% 12.7% 12.6% 13.4%

45‐54 years 14.1% 14.8% 14.8% 14.0% 13.4%

55‐64 years 12.4% 14.2% 13.5% 13.1% 11.8%

65‐74 years 10.6% 9.7% 12.2% 11.5% 9.0%

75‐84 years 5.0% 3.9% 5.3% 6.2% 4.5%

85 years and over 2.2% 1.0% 1.3% 2.6% 1.8%

Average age (years) 40.2 39.4 41.2 42.1 38.8

Household Type (% of families)

Couple families with children 44.6% 42.0% 42.0% 39.4% 42.5%

Couple families without children 40.8% 40.4% 44.4% 44.0% 39.4%

Single parent family 11.8% 16.2% 12.9% 15.5% 16.5%

Other 2.7% 1.0% 0.9% 1.1% 1.6%

Average household size 2.9 2.9 2.9 2.7 2.8

Average vehicle ownership 2.0 2.1 2.1 1.8 1.8

Household Finances

% of households fully owning home 30.7% 30.6% 36.1% 33.1% 28.5%

% of households purchasing home 38.1% 44.9% 43.3% 33.1% 33.7%

% of households renting 28.0% 21.4% 16.9% 29.6% 34.2%

Average weekly household income $1,495 $1,581 $1,617 $1,564 $1,688

Average monthly housing loan repayment $1,806 $1,806 $1,828 $1,886 $1,889

Average weekly rent payment $327 $324 $334 $372 $337

% of weekly income spent on housing costs 16.7% 16.2% 14.8% 16.2% 15.5%

7

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docxTrade Area Overview

PTA STA North STA South Sunshine Queensland

Coast LGA

Average weekly household income after housing costs $1,245 $1,324 $1,378 $1,310 $1,426

Labour Market

Full‐time employment (% labour force) 52.0% 52.3% 54.6% 52.5% 57.7%

Part‐time employment (% labour force) 34.6% 35.6% 32.6% 35.6% 29.9%

Unemployment rate 6.9% 7.3% 7.1% 7.2% 7.6%

Labour force participation rate (% of population > 58.0% 61.0% 58.8% 57.9% 61.0%

15 years)

Qualifications

% of persons with a post‐school qualification 45.0% 48.9% 47.8% 50.9% 48.3%

% of persons with Bachelor or higher 10.6% 12.7% 11.6% 16.9% 18.3%

% of persons with Diploma 8.5% 9.7% 9.4% 10.1% 8.7%

% of persons with Certificate 25.8% 26.5% 26.7% 23.9% 21.3%

Occupation

Upper White Collar

Managers 11.2% 9.6% 13.3% 11.7% 12.1%

Professionals 13.7% 14.5% 13.9% 19.1% 19.8%

Subtotal 24.8% 24.1% 27.2% 30.8% 31.9%

Lower White Collar

Clerical and Admin Workers 11.4% 12.4% 11.8% 12.9% 13.6%

Community & Personal Service Workers 10.3% 12.2% 11.2% 12.1% 11.3%

Sales Workers 10.1% 10.7% 10.2% 11.1% 9.7%

Subtotal 31.9% 35.3% 33.2% 36.1% 34.7%

Upper Blue Collar

Technicians & Trades Workers 17.6% 20.0% 16.3% 16.2% 14.3%

Subtotal 17.6% 20.0% 16.3% 16.2% 14.3%

Lower Blue Collar

Machinery Operators & Drivers 8.5% 7.6% 8.0% 5.0% 6.9%

Labourers 15.6% 12.2% 13.6% 10.3% 10.5%

Subtotal 24.1% 19.9% 21.6% 15.4% 17.5%

Employment by Industry (% of employees)

Agriculture, forestry & fishing 6.5% 2.4% 8.9% 1.8% 2.8%

Mining 1.7% 2.1% 2.1% 1.5% 2.3%

Manufacturing 5.6% 6.4% 4.8% 4.8% 6.0%

Electricity, gas, water & waste services 1.3% 1.2% 1.3% 1.0% 1.1%

Construction 12.4% 15.1% 12.3% 12.2% 9.0%

Wholesale trade 2.4% 1.8% 2.7% 2.1% 2.6%

Retail trade 10.1% 11.0% 9.3% 10.9% 9.9%

Accommodation & food services 6.4% 6.2% 5.3% 8.4% 7.3%

8

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docxTrade Area Overview

PTA STA North STA South Sunshine Queensland

Coast LGA

Transport, postal & warehousing 4.7% 3.8% 4.9% 3.4% 5.1%

Information media & telecommunications 0.9% 0.7% 1.0% 1.1% 1.2%

Financial & insurance services 1.6% 1.2% 1.8% 2.8% 2.5%

Rental, hiring & real estate services 1.2% 1.9% 1.8% 2.3% 2.0%

Professional, scientific & technical services 4.7% 4.9% 5.1% 5.6% 6.3%

Administrative & support services 3.9% 4.2% 3.0% 3.9% 3.5%

Public administration & safety 4.3% 4.5% 5.0% 4.2% 6.6%

Education & training 8.0% 8.5% 7.4% 9.0% 9.0%

Health care & social assistance 11.9% 13.4% 12.6% 15.0% 13.0%

Arts & recreation services 2.3% 1.6% 2.3% 1.9% 1.6%

Other services 2.3% 4.1% 4.2% 4.0% 3.9%

Source: ABS (2016) Census of Population and Housing

2.3 Population and Household Projections

As already mentioned, two separate population and household projection scenarios have been prepared for this

analysis considering historic rates of development, development yields, planning capacity within urban footprint areas

and the likely rollout of Beerwah East Identified Growth Area. The purpose of utilising two scenarios is to consider the

range of possible growth trends that could eventuate in the region and the consequent impacts on the timing of the

Beerwah Homemaker Centre.

A brief outline of each scenario is presented below:

Scenario One: Informed by the latest Queensland Government Statistician’s Office (QGSO) population

projections by SA2, with adjustments made to the projected growth rates to account for SA2 level growth that

falls outside of the trade areas. This represents the ‘main case’ scenario;

Scenario Two: Considers the impact of additional household growth within the Beerwah East Identified Growth

Area over and above the QGSO population projections.

This report utilises 2018 as a ‘current’ base year, because analysis is based on financial years and at the time of

preparing this report data to June 2019 was not available.

2.3.1 Scenario One Population and Household Projections

Scenario One population projections for the PTA, STA North and STA South, benchmarked to Sunshine Coast LGA and

Queensland have been prepared using the latest (2018 edition) Queensland Government Statisticians Office (QGSO)

medium series population projections. The population of the PTA is anticipated to increase from 9,065 persons in

2018 to 11,543 persons in 2031, representing average annual growth of 1.9% per annum. Within the main trade area,

population growth is anticipated to be highest in the STA North, increasing at an average annual rate of 5.4% per

annum to 16,682 persons by 2031.

Population growth and household formation in the main trade area is anticipated to exceed the Sunshine Coast LGA

and Queensland averages. As already mentioned this represents the ‘main case’ scenario.

Table 2‐2 below reports the projected population households within the PTA, STA North, STA South, Sunshine Coast

LGA and Queensland between 2018 and 2031 under Scenario One.

9

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docxTrade Area Overview

Table 2‐2 Scenario One population and household projections, PTA, STA North, STA South, Sunshine Coast LGA

and Queensland 2018 to 2031

2018 2021 2026 2031 Ave. annual

change

Population

PTA 9,065 10,172 11,268 11,543 1.9%

STA North 8,470 9,939 12,886 16,682 5.4%

STA South 6,294 6,885 7,338 7,499 1.4%

Main Trade Area 23,829 26,997 31,492 35,723 3.2%

Sunshine Coast LGA 306,719 327,352 366,932 409,596 2.2%

Queensland 5,009,919 5,261,567 5,722,780 6,206,566 1.7%

Households

PTA 3,156 3,562 3,984 4,122 2.1%

STA North 2,944 3,471 4,534 5,916 5.5%

STA South 2,179 2,395 2,573 2,650 1.5%

Main Trade Area 8,279 9,428 11,091 12,688 3.3%

Sunshine Coast LGA 113,597 121,969 138,103 155,740 2.5%

Queensland 1,771,429 1,870,816 2,053,956 2,248,756 1.9%

Source: QGSO (2018) Medium Series Population Projections, ABS (2016) Census of Population and Housing, ABS Estimated Resident

Population Estimates by SA1

2.3.2 Scenario Two Population Projections

Scenario Two population projections assume that the rate of population growth and household formation will be

higher in the PTA resulting from residential development within the Beerwah East Identified Growth area. Advice from

Project Urban has indicated that residential allotments within Beerwah East would be available within the next five

years. Our assessment has assumed that 150 lots will be taken up in Beerwah East in 2023, increasing to 350 lots

taken up in 2031, translating to ~2,250 lots taken up in the 2023‐31 period.

Based on the above assumptions, the population of the PTA is projected to increase from 9,065 persons in 2018,

increasing to 17,843 persons in 2031, or by 5.3% per annum.

The rate of population growth and household formation in the main trade area is anticipated to exceed the Sunshine

Coast LGA and Queensland averages, and be higher than under Scenario One and Scenario Two.

Table 2‐4 reports the projected population households within the PTA, STA North, STA South, Sunshine Coast LGA and

Queensland between 2018 and 2031 under Scenario Three.

10

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docxTrade Area Overview

Table 2‐3 Scenario Two population and household projections, PTA, STA North, STA South, Sunshine Coast LGA

and Queensland, 2018 to 2031

2018 2021 2026 2031 Ave. annual

change

Population

PTA 9,065 10,172 13,403 17,843 5.3%

STA North 8,470 9,939 12,886 16,682 5.4%

STA South 6,294 6,885 7,338 7,499 1.4%

Main Trade Area 23,829 26,997 33,627 42,023 4.5%

Sunshine Coast LGA 306,719 327,352 366,932 409,596 2.2%

Queensland 5,009,919 5,261,567 5,722,780 6,206,566 1.7%

Households

PTA 3,156 3,562 4,739 6,372 5.6%

STA North 2,944 3,471 4,534 5,916 5.5%

STA South 2,179 2,395 2,573 2,650 1.5%

Main Trade Area 8,279 9,428 11,846 14,938 4.6%

Sunshine Coast LGA 113,597 121,969 138,103 155,740 2.5%

Queensland 1,771,429 1,870,816 2,053,956 2,248,756 1.9%

Source: QGSO (2018) Medium Series Population Projections, ABS (2016) Census of Population and Housing, ABS Estimated Resident

Population Estimates by SA1, CDM Smith estimates based on advice from Project Urban

2.4 Implications for Retail Demand

Average household incomes after adjusting for housing costs within the main trade area were highest in the STA South

and lowest in the PTA as of the 2016 Census. Both the STA North and STA South recorded higher household incomes

after adjusting for housing costs relative to the Sunshine Coast, suggesting higher levels of disposable income

available to spend on retail.

The average household size in all trade areas was higher than Sunshine Coast LGA and Queensland averages,

suggesting that retail expenditure on essential items such as groceries may potentially exceed regional and state

averages.

The rate of retail expenditure growth in the PTA and STA North is anticipated to exceed regional and state averages,

particularly if the roll out of the Beerwah East Identified Growth Area commences prior to 2031.

11

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docxCentres Network

Section 3 Centres Network

The purpose of this chapter is to identify the existing, approved and designated centres servicing the identified trade

areas for the Beerwah Homemaker Centre.

3.1 Centres Hierarchy

3.1.1 Planning Scheme Centres Zones

The Sunshine Coast Planning Scheme 2014 identifies five centres zones relevant to the subject proposal, these being:

Principal centre zone: Principal centres provide for the widest range and highest order retail, commercial,

residential and community facilities to be accommodated. The only land currently zoned for principal centre use

it the Maroochydore Principal Regional Activity Centre in an arrangement that produces mixed land use

outcomes, supports public and active transport modes and creates a large number of jobs in a wide array of

creative and successful enterprise;

Major centre zone: The purpose of the Major centre zone code is to provide for Beerwah Town Centre,

Caloundra Town Centre, Nambour Town Centre and Sippy Downs Town Centre to

– (a) be developed as major regional activity centres for the Sunshine Coast, servicing a part of the sub‐region

and complementing the role of Maroochydore as the principal regional activity centre for the Sunshine

Coast;

– (b) accommodate a range of higher order business activities, entertainment activities, multiunit residential

activities and community activities in an active and vibrant mixed‐use environment; and

– (c) have a scale and intensity of development that is commensurate with the role and function of a major

regional activity centre as specified in the Sunshine Coast activity centre network and the applicable local

plan code.

District centre zone: The purpose of the District centre zone code is to provide for a range of activities that

complement, but do not compete with, the role and function of higher order activity centres by serving the

convenience needs of district catchments in centres that are highly accessible and well connected to the

catchment areas that they serve. District centres are developed as well‐designed, safe and visually attractive

business, community and employment centres, predominantly in a low‐rise building format;

Local centre zone: The purpose of the Local centre zone code is to provide for a range of activities that

complement, but do not compete with, the role and function of higher order activity centres by meeting the

convenience service needs of individual rural towns and villages or coastal urban neighbourhoods and providing

local employment opportunities. Local centres are developed as well designed, safe and visually attractive local

convenience centres, predominantly in a low‐rise building format, where significant off‐site impacts are avoided;

and

Specialised centre zone: The purpose of the Specialised centre zone is to accommodate showrooms, garden

centres, hardware and trade supplies and outdoor sales, with each tenancy to have a minimum gross leasable

floor area of 300m². In addition, the Specialised centre zone code states that higher order and other retail

facilities better suited to establishing within an activity centre, including supermarkets, department stores and

discount department stores are not to be established within the Specialised centre zone.

12

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docxCentres Network

3.2 Existing Centres

CDM Smith personnel undertook comprehensive site inspections to centres zoned land within and servicing the main

trade areas, as well as along the main travel routes between each centre. These site inspections provided on‐the‐

ground information about the size, tenant composition, layout and accessibility of existing centres, as well as scoping

the role and function of each centre. The centres network assessment focussed on centres located to the west of the

Bruce Highway, but also included those centres located on both sides of the Bruce Highway corridor.

The site inspections also identified and quantified vacant tenancies within each centre. Details relating to vacant land

and remnant housing within each centre zone within the main trade area is outlined in Section 5 of the report.

Table 3‐1 provides a summary of the centres both within and servicing the main trade area located either on the

Bruce Highway or to the west of the Bruce Highway, including details on total floor space, retail floor space, anchor

tenants and distance from the subject site.

Table 3‐1 Retail floor space in trade areas by centre type, anchor tenants and distance from subject site

Within Main Total Retail Anchor tenants Distance from

Trade Area Floor Floor subject site

Space Space (km)

(sqm) (sqm)

Major centres

Beerwah 3 (PTA) 18,079 12,981 Aldi, Woolworths, Fresh & 1.4

Save, Target

District centres

Maleny 2 32,019 22,279 Woolworths, IGA 20.7

Local centres

Beerwah 3 (PTA) 2,975 2,595 ‐ 1.0

Glass House Mountains 3 (STAS) 2,609 2,103 IGA 4.3

(train station)

Glass House Mountains 3 (STAS) 210 210 ‐ 5.1

(Bowen Road / Steve Irwin Way

intersection)

Landsborough 3 (STAN) 6,305 4,611 IGA 6.7

Peachester 3 (PTA) 250 250 ‐ 9.7

Beerburrum 3 (STAS) 336 298 ‐ 10.9

Mooloolah Valley 3 (STAN) 3,243 2,370 IGA 14.5

Bald Knob 2 1,000 1,000 ‐ 15.7

Eudlo 2 390 310 ‐ 24.4

Palmwoods 2 7,495 5,747 IGA 28.5

Specialised centres

Beerwah 3 (PTA) 1,500 1,330 ‐ 0.7

Landsborough 3 (STAN) 200 ‐ ‐ 6.4

Township Zone

Woodford* 2 14,116 12,574 Woolworths, IGA 31.8

Other centres

Glass House Mountains 3 (STAS) 1,980 1,980 ‐ 4.6

13

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docxCentres Network

Within Main Total Retail Anchor tenants Distance from

Trade Area Floor Floor subject site

Space Space (km)

(sqm) (sqm)

Glenview 2 750 550 ‐ 17.8

Palmview 2 1,210 1,030 ‐ 18.6

Elimbah* 2 2,257 1,681 ‐ 23.0

Note: Woodford and Elimbah are contained within Moreton Bay LGA

Source: CDM Smith site inspections

3.2.1 Major Centres

3.2.1.1 Beerwah

Beerwah was the only major centre identified within the main trade area, with anchor tenants including Aldi,

Woolworths, Fresh & Save and Target. There was an estimated 18,079m2 of floor space identified at the Beerwah

major centre, including 12,981m2 of retail floor space. An estimated 1,138m2 of vacant tenancies were identified

within the Beerwah major centre zone, representing a vacancy rate of 6.2%.

3.2.1.2 Sippy Downs

The Sippy Downs major centre zone represents the alternative comparison shopping destination for residents within

the STA North and the location of the closest Coles to the proposed subject site (~23 kilometres between Coles Sippy

Downs and the proposed Beerwah Coles). The Sippy Downs major centre zone is located immediately south of the

Sunshine Motorway, to the north of the University of the Sunshine Coast. However, the Sippy Downs major centre has

not been comprehensively floor spaced due to its location on the eastern side of the Bruce Highway and its distance

from the subject site.

Development within the Sippy Downs major centre zone has occurred within the last few years, with major tenants

including a Coles, Liquorland and Chipmunks (indoor children’s play centre). A Woolworths anchored centre is also

located within Sippy Downs on local centre zoned land off Chancellor Village Boulevard.

3.2.2 District Centres

3.2.2.1 Maleny

Maleny has evolved since the 1980’s as a retail tourism destination known for its artistic temperament and small‐scale

enterprises. The main stretch of Maple Street is anchored by the ~ 1,500m2 IGA, with the ~3,000m2 Woolworths

somewhat isolated on the east side of Obi Obi Creek. Maleny includes various local food product, arts and crafts

stores and notable franchises include Mitre 10, Bridgestone Tyres, Ray White, ANZ and CJ’s Bakery.

The Maleny district centre zone had a total of 32,019m2 of floor space, comprising 22,279m2 of retail floor space,

7,697m2 of commercial office floor space and 2,043m2 of vacant tenancies.

3.2.3 Local Centres

3.2.3.1 Beerwah

The local centre zoned land on the western side of the rail line in Beerwah was largely utilised by industrial businesses

such as food distributors and upholsterers. At the time of site inspections, industrial sheds were under construction on

Free Street, despite the land being zoned for centre uses.

Major retail tenancies within the Beerwah local centre zone included the Beerwah Hotel (~1,200m2 over two storeys)

and the Pump House (store selling pump and irrigation systems (~770m2)).

14

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docxCentres Network

3.2.3.2 Glass House Mountains

Within the Glass House Mountains local centre zone surrounding the train station, there was an estimated 2,609m2 of

floor space, comprising 2,103m2 of retail floor space and 506m2 of commercial floor space. There were no vacant

tenancies identified in the Glass House Mountains local centre zone. The site inspections identified the absence of any

clothing, footwear and apparel businesses, core bulky goods businesses or ancillary bulky goods businesses.

Glass House Mountains local centre is anchored by a ~300m2 IGA, and other notable tenants include Bottlemart, QML,

CJ’s Bakery, Mitre 10 and Golden Casket. The main section surrounding the roundabout is easily accessible and

inviting. However, the Mitre 10 and surrounding tenancies on the other side of the rail line are somewhat fragmented

from the main part of town.

Additionally, there was a parcel of local centres zoned land identified at the corner of Steve Irwin Way and Bowen

Road, south of the main local centre precinct, occupied by a Puma service station, café and greengrocer.

3.2.3.3 Landsborough

The site inspections identified a total of 6,305m2 of floor space within Landsborough, anchored by a ~450m2 IGA. The

site inspections identified a significant quantum of floor space occupied by dining and take‐away food businesses,

amounting to 2,407m2 or 38.2% of total floor space. An estimated 586m2 of tenancies within the Landsborough local

centre zone were vacant, representing 9.3% of total floor space.

3.2.3.4 Peachester

The Peachester local centre zone had an estimated 250m2 of retail floor space, occupied by a café and general store.

3.2.3.5 Beerburrum

The Beerburrum local centre zone had an estimated 336m2 of floor space, with tenancies including a café, general

store and post office.

3.2.3.6 Mooloolah Valley

There was an estimated 2,370m2 of retail floor space within the Mooloolah Valley local centre zone, anchored by a

~911m2 IGA and a ~250m2 Mitre 10.

3.2.3.7 Bald Knob

The Bald Knob local centre zone was occupied by an estimated 1,000m2 of retail floor space, predominately occupied

by dining and take‐away food tenancies (~900m2).

3.2.3.8 Eudlo

The Eudlo local centre zone had an estimated 390m2 of floor space, including a café, general store and post office.

3.2.3.9 Palmwoods

Total floor space identified within the Palmwoods local centre was estimated at 7,495m2, comprising 5,747m2 of retail

floor space and 1,658m2 commercial office floor space. The major tenant within the Palmwoods local centre was a

~300m2 IGA. Dining and take away food tenancies accounted for a significant proportion of total floor space at the

centre, occupying an estimated 3,155m2.

15

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docxCentres Network

3.2.4 Specialised Centres

3.2.4.1 Beerwah

The Beerwah specialised centre zone had an estimated 1,500m2 of tenancies located on Beerwah Parade, with major

tenants including a mower store and a tyre and battery store. Land within the Beerwah specialised centre zone

immediately to the west of Steve Irwin Way was identified as vacant.

Property searches have identified that vacant land within the Beerwah specialised centre zone is owned by the

Queensland Department of Transport and Main Roads. Approaches to the Department have indicated this land is not

surplus to their requirements, hence will not be available for purchase. Therefore, it is considered the prospect of

developing this land for special centre uses is low.

3.2.4.2 Landsborough

The majority of land within the Landsborough specialised centre zone was either vacant or occupied by houses. A

veterinary surgery was identified within the Landsborough specialised centre zone.

3.2.5 Township Zone

3.2.5.1 Woodford

There was an estimated 14,116m2 of floor space identified within the Woodford township zone. The Woodford centre

was anchored by a Woolworths supermarket (~3,000m2) and an IGA (~2,250m2). Dining and take‐away food tenancies

also accounted for a significant quantum of floor space within the Woodford township zone, occupying ~3,332m2 of

floor space.

3.2.6 Other Centres

Retail activity outside of centres zoned land was identified at Glass House Mountains, Glenview, Palmview and

Elimbah.

A significant quantum of retail floor space at Glass House Mountains was identified on the Bruce Highway on the

southbound side, with tenancies including McDonald’s, Hungry Jack’s, Beefy’s and Subway. Retail activity within

Palmview was identified immediately adjacent to Aussie World, with a range of specialty tenancies including Subway,

Beefy’s and Cellabrations. Retail activity within Glenview was at the corner of Ballantine Court and Glenview Road

and included a café, saddlery and opal store.

A relatively new centre has been established at 459 Pumicestone Road, Elimbah, co‐located with the Big Fish Tavern.

Tenancies include a Caltex service station, the Foodary and drive thru Red Rooster. It is understood that the site has a

development approval for a Woolworths and specialty tenancies, yet construction had yet to commence at the time of

site inspections. Retail activity was also identified at an older style centre at 866‐870 Beerburrum Road, Elimbah

(Elimbah Village) with tenancies including a hairdresser and newsagent.

3.3 Approved and Designated Centres

A review of development applications identified two applications, these being the Beerwah Shopping Complex

(approved) and the Mooloolah Valley IGA expansion (under application).

3.3.1 Beerwah Shopping Complex

As mentioned above, at the time of site inspections, the Beerwah Shopping Complex had just been completed 26

Simpson Street (corner Pine Camp Road). The approved development comprises an additional 1,046m2 of gross floor

area (GFA) across two buildings. Our assessment has conservatively assumed that all additional floor space would be

occupied by specialty retail tenants.

16

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docxCentres Network

3.3.2 Mooloolah Valley IGA Expansion

It is understood that a development application has been lodged to expand the IGA within the Mooloolah Valley local

centre zone from 911m2 to 1,522m2, representing a floor space increase of 611m2. However, Sunshine Coast Regional

Council considers this expansion impact assessable, as the expanded supermarket will exceed 1,000m2 in size.

Sunshine Coast Regional Council is yet to decide the outcome of this application.

3.3.3 Potential Beerwah East Centres

The Beerwah East Identified Growth Area would likely include a number of centres. At the time of preparing this

report, there was no guidance available as to the status of any structure or master planning over Beerwah East

Identified Growth Area.

17

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docxRetail Expenditure Analysis

Section 4 Retail Expenditure Analysis

This section of the report provides an overview of retail expenditure patterns of main trade area households,

estimates the level of expenditure likely to be captured by the proposed scale of development at the subject site and

converts these estimates to supportable floor space for the sub‐categories of supermarket, specialty retail and bulky

goods, utilising the household projections presented in Section 2.3.1 of the report (Scenario One).

The outcomes of the assessment under alternative household growth scenarios (Scenario Two) are presented in

Appendix A.

Retail expenditure patterns are estimated based on the CDM Smith retail expenditure model which generates small

area retail expenditure estimates based on a simulation utilising a range of small area demographic data sourced from

the Census and ATO; regional level data from the ABS Household Expenditure Survey; and broader state and national

level data from state and national accounts.

4.1 Weekly Household Retail Expenditure

Weekly household retail expenditure estimates are presented in 2018 dollars and assume real expenditure growth of

1.0% per annum.

Average weekly household expenditure across the main trade area is expected to increase from:

$695.63 per week in 2018 to $791.69 per week in 2031 within the PTA;

$760.33 per week in 2018 to $865.33 per week in 2031 within the STA North; and

$805.75 per week in 2018 to $917.02 per week in 2031 within the STA South.

Strong expenditure outcomes for the STA South relative to the other two trade areas is driven by comparatively higher

incomes, but comparatively lower housing costs resulting in comparatively high discretionary income.

Table 4‐1 reports the average weekly household expenditure by retail category for each of the trade areas between

2018 and 2031.

Table 4‐1 Available weekly household expenditure ($ per household, 2018 dollars) by trade area, 2018‐2031

2018 2021 2026 2031

PTA

Groceries & take‐home food $261.55 $269.47 $283.22 $297.67

Dining & take away food $120.01 $123.64 $129.95 $136.58

Clothing, footwear & apparel $68.68 $70.76 $74.37 $78.16

Personal & other goods $93.47 $96.30 $101.21 $106.38

Core bulky goods $45.60 $46.98 $49.38 $51.90

Ancillary bulky goods $58.19 $59.95 $63.01 $66.23

Hardware $23.22 $23.92 $25.14 $26.42

Takeaway liquor $24.91 $25.67 $26.98 $28.35

Total Grocery & Specialty $568.62 $585.85 $615.73 $647.14

Total Bulky Goods $127.01 $130.86 $137.53 $144.55

Total $695.63 $716.70 $753.26 $791.69

18

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docxRetail Expenditure Analysis

2018 2021 2026 2031

STA North

Groceries & take‐home food $316.78 $326.38 $343.03 $360.52

Dining & take away food $122.79 $126.51 $132.96 $139.75

Clothing, footwear & apparel $69.96 $72.08 $75.76 $79.62

Personal & other goods $95.75 $98.65 $103.68 $108.97

Core bulky goods $47.25 $48.68 $51.16 $53.77

Ancillary bulky goods $59.17 $60.97 $64.08 $67.34

Hardware $23.54 $24.25 $25.49 $26.79

Takeaway liquor $25.09 $25.85 $27.17 $28.56

Total Grocery & Specialty $630.37 $649.47 $682.60 $717.42

Total Bulky Goods $129.96 $133.90 $140.73 $147.91

Total $760.33 $783.37 $823.33 $865.33

STA South

Groceries & take‐home food $332.72 $342.80 $360.29 $378.67

Dining & take away food $133.19 $137.22 $144.22 $151.58

Clothing, footwear & apparel $74.47 $76.73 $80.64 $84.76

Personal & other goods $102.52 $105.62 $111.01 $116.68

Core bulky goods $50.77 $52.31 $54.98 $57.78

Ancillary bulky goods $62.08 $63.96 $67.22 $70.65

Hardware $24.38 $25.12 $26.40 $27.75

Takeaway liquor $25.63 $26.40 $27.75 $29.17

Total Grocery & Specialty $668.52 $688.78 $723.92 $760.84

Total Bulky Goods $137.23 $141.39 $148.60 $156.18

Total $805.75 $830.17 $872.52 $917.02

Source: Derived from ABS (2018) Retail Trade publication and ABS (2018) Household Expenditure Survey

4.2 Annual Available Expenditure

To convert average weekly household estimates to annual available expenditure estimates, the assessment has

utilised the Scenario One household projections reported in Section 2.3.1. Annual available expenditure estimates

under Scenario Two household projections are presented in Appendix A.

Available annual retail expenditure within the main trade area is anticipated to increase from $321.86 million in 2018

to $562.24 million in 2031, or by 4.4% per annum. In 2018, the PTA is anticipated to account for 35.5% of annual

available expenditure in the main trade area, decreasing to 30.2% of annual available expenditure by 2031. On the

other hand, the STA North is anticipated to account for an increasing share of retail expenditure in the main trade

area, increasing from 36.2% of available expenditure in 2018 to 47.3% of available expenditure in 2031.

Table 4‐2 reports on the total annual available expenditure within each trade area by retail category between 2018

and 2031 (2018 dollars).

19

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docxRetail Expenditure Analysis

Table 4‐2 Annual available expenditure by retail category ($m), 2018‐2031 (2018 dollars)

2018 2021 2026 2031

PTA

Groceries & take‐home food $42.92 $49.91 $58.68 $63.81

Dining & take away food $19.69 $22.90 $26.92 $29.28

Clothing, footwear & apparel $11.27 $13.11 $15.41 $16.76

Personal & other goods $15.34 $17.84 $20.97 $22.80

Core bulky goods $7.48 $8.70 $10.23 $11.13

Ancillary bulky goods $9.55 $11.10 $13.06 $14.20

Hardware $3.81 $4.43 $5.21 $5.66

Takeaway liquor $4.09 $4.75 $5.59 $6.08

Total Grocery & Specialty $93.31 $108.52 $127.57 $138.72

Total Bulky Goods $20.84 $24.24 $28.50 $30.99

Total $114.16 $132.75 $156.07 $169.71

STA North

Groceries & take‐home food $48.50 $58.90 $80.88 $110.90

Dining & take away food $18.80 $22.83 $31.35 $42.99

Clothing, footwear & apparel $10.71 $13.01 $17.86 $24.49

Personal & other goods $14.66 $17.80 $24.45 $33.52

Core bulky goods $7.23 $8.79 $12.06 $16.54

Ancillary bulky goods $9.06 $11.00 $15.11 $20.72

Hardware $3.60 $4.38 $6.01 $8.24

Takeaway liquor $3.84 $4.67 $6.41 $8.78

Total Grocery & Specialty $96.50 $117.21 $160.95 $220.69

Total Bulky Goods $19.90 $24.17 $33.18 $45.50

Total $116.40 $141.38 $194.13 $266.19

STA South

Groceries & take‐home food $37.70 $42.69 $48.20 $52.17

Dining & take away food $15.09 $17.09 $19.29 $20.88

Clothing, footwear & apparel $8.44 $9.56 $10.79 $11.68

Personal & other goods $11.62 $13.15 $14.85 $16.08

Core bulky goods $5.75 $6.51 $7.35 $7.96

Ancillary bulky goods $7.03 $7.97 $8.99 $9.73

Hardware $2.76 $3.13 $3.53 $3.82

Takeaway liquor $2.90 $3.29 $3.71 $4.02

Total Grocery & Specialty $75.75 $85.78 $96.84 $104.83

Total Bulky Goods $15.55 $17.61 $19.88 $21.52

Total $91.30 $103.39 $116.72 $126.35

Main Trade Area

Groceries & take‐home food $129.12 $151.51 $187.76 $226.88

Dining & take away food $53.58 $62.82 $77.57 $93.15

Clothing, footwear & apparel $30.42 $35.67 $44.06 $52.93

Personal & other goods $41.61 $48.80 $60.27 $72.40

Core bulky goods $20.47 $24.00 $29.65 $35.63

Ancillary bulky goods $25.64 $30.07 $37.16 $44.65

Hardware $10.18 $11.94 $14.75 $17.73

Takeaway liquor $10.83 $12.71 $15.71 $18.88

Total Grocery & Specialty $265.57 $311.51 $385.37 $464.24

Total Bulky Goods $56.29 $66.01 $81.56 $98.00

Total $321.86 $377.52 $466.92 $562.24

Source: Derived from ABS (2018) Retail Trade publication, ABS (2018) Household Expenditure Survey and QGSO (2018) medium

series population projections

20

CDM Smith‐1000323‐RPT Beerwah Coles Economic Need and Impact Assessment REVG 171019.docxYou can also read