Chicago CBD Office Insight Report - Q2 2021 - Avison Young

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Chicago CBD

Office Insight

Report

Q2 2021

1

Key takeaways

Economic conditions Recovery rate Office demand

− Reopening efforts and higher − The overall post-COVID rate of − Leasing activity has paused, decreasing

vaccination rates have allowed the recovery based on extrapolated cell by 59.5 percent compared with

Chicagoland unemployment rate to phone data is 35.7 percent. long-term historical averages.

rebound from a high of 16.5 percent to

7.5 percent. − Chicago office occupiers have − However, Memorial Day was a key

navigated their return-to-work turning point in assessed tenant

− Office-using job losses have totaled strategies differently, with banking demand as COVID-era renewals are set

4.1 percent compared with 11.0 and media firms returning more to expire.

percent for other industries’ job losses, quickly than tech and law firms. The

underscoring the disproportionate overall rate of recovery is a − The Class A segment accounts for a 60

impact the pandemic had on the comparatively low 19.7 percent, percent share of post-COVID

discretionary segments of the local though bellwether companies are sublease supply.

economy. beginning to mandate that their

employees return to the office.

2

01.

The deeper dive

Here we take a look at key return-to-

work metrics, including vaccination

rates, office occupation recovery rates

in Chicago and key markets, as well as

general market KPIs such as large

activity and sublease supply pipelines.

3

Vaccination rates

50.0

47.5

47.5%

45.0 46.1

40.0

35.0

Fully vaccinated %

Share of total Cook County 30.0

population that is fully vaccinated 25.0

20.0

Chicago-area proportionate vaccination rates have 15.0

remained in line with U.S. averages, an important metric 10.0

Cook County

that allowed the city to expedite reopening plans and 5.0 U.S.

loosen restrictions. 0.0

3/15/2021 3/30/2021 4/14/2021 4/29/2021 5/14/2021 5/29/2021 6/13/2021

Source: CDC, Includes Cook County only

4

Employment and unemployment rate

7.5%

20.0 Employment 5,000,000

18.0 4,500,000

16.0

4,000,000

Chicago MSA unemployment rate as 14.0

3,500,000

of April 2021, dipping below the 12.0

12.2 12.8

height of the financial crisis 10.0

3,000,000

8.7

2,500,000

Historically tightened labor market conditions were 8.0 7.2

7.5

2,000,000

halted by the pandemic with nearly 860 thousand job 6.0

losses from February into May 2020. Preparation for 4.0

1,500,000

4.5

4.1

reopening efforts allowed the economy to add 14.7% jobs 2.0 3.2 1,000,000

since May 2020. 0.0 500,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Note: Not seasonally adjusted data.

Source: Bureau of Labor Statistics

5

Office-using job gains and losses

Total change in Chicago MSA* job

-4.1%

Change in office-using employment

gains/(losses)

February 2020 to April 2021

Federal

Government

2.2%

State Government

during the pandemic -0.2%

Financial Activities

-0.7%

Chicago MSA job losses have declined by 6.5% since the start

Professional and Business

of the pandemic, though office-using jobs contracted by just Services

-3.8%

4.1%. This recession’s impact on the office-using labor market Local Government

-7.3%

has been less severe than the global financial crisis, when

Information

Professional and Business Services job losses totaled 12%. -11.0%

-15.0% -10.0% -5.0% 0.0% 5.0%

VIEW DASHBOARD

Note: Not seasonally adjusted data. Metropolitan statistical area.

Source: Bureau of Labor Statistics

6

Chicago recovery index

35.7%

2,500K

COVID-19

lockdown

2,000K

Post-COVID rate of

1,500K

recovery based on

representative locations

through 6/13/2021 1,000K

The rate of recovery is most 500K

significant in healthcare, currently

63.1% of pre-COVID visitor volume, 0K

27-Oct-19

12-Apr-20

18-Oct-20

25-Apr-21

1-Mar-20

2-Jun-19

5-Jul-20

14-Mar-21

6-Jun-21

23-Jun-19

14-Jul-19

4-Aug-19

9-Feb-20

22-Mar-20

25-Aug-19

8-Dec-19

14-Jun-20

26-Jul-20

16-Aug-20

6-Sep-20

21-Feb-21

15-Sep-19

29-Dec-19

19-Jan-20

3-May-20

20-Dec-20

10-Jan-21

31-Jan-21

17-Nov-19

24-May-20

27-Sep-20

8-Nov-20

29-Nov-20

16-May-21

6-Oct-19

4-Apr-21

as elective procedure regulations

ease and vaccination rates increase. Transit Office Residential Hospitality, Recreation & Tourism Healthcare Government Education

Note: Representative areas of interest. Weekdays only.

Pre-COVID period measured as 12/1/2019 to 3/8/2020.

7 Source: Orbital Insights, AVANT by Avison Young

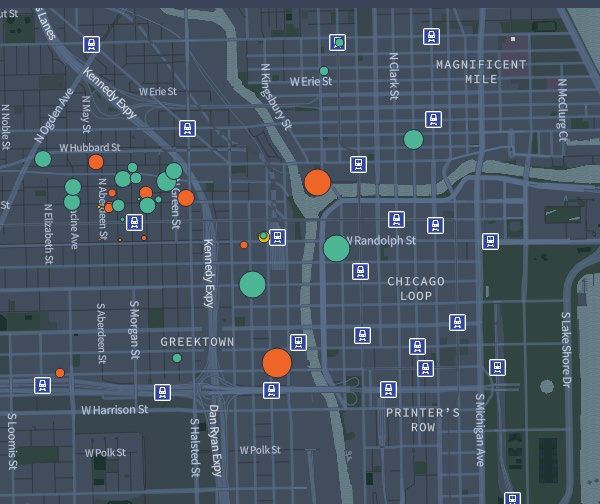

Office recoveries in gateway U.S. cities

Washington, DC 58.0%

43.9%

San Francisco 57.0%

Philadelphia 56.0%

New York 55.0%

Nashville 54.0%

Post-COVID rate of recovery for Miami 53.0%

representative Chicago office Los Angeles 52.0%

occupiers through 5/30/2021 Houston 51.0%

Dallas 50.0%

Chicago office employers are still solving return-to-work

Denver 44.9%

strategies as the city’s reopening plan continues. Transit

Chicago 43.9%

services have yet to see ridership recovery from office Boston 29.6%

commuters. Austin 22.3%

Atlanta 14.3%

Note: Select, representative occupiers only. Weekdays only.

Pre-COVID period measured as 12/1/2019 to 3/8/2020.

8 Source: Orbital Insights, AVANT by Avison Young

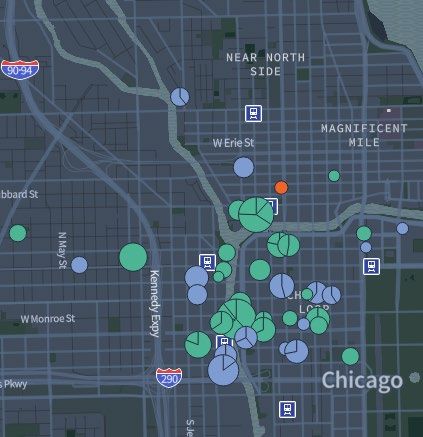

Chicago recovery index for select office

occupiers

21.9%

19.7%

20.2%

17.4%

Post-COVID rate of recovery for 12.4%

representative Chicago office

occupiers through 6/13/2021

Office employers have taken unique approaches in their

return-to-work efforts. While tech firms have adopted

remote working solutions, legal and financial services Law firms Banking, finance, Tech Food & beverage

insurance, real production

have returned to work most regularly. estate

Note: Select, major occupiers only. Weekdays only.

Pre-COVID period measured as 12/1/2019 to 3/8/2020.

9 Source: Orbital Insights, AVANT by Avison YoungOffice leasing activity

-59.5%

15.0M sf

13.6

12.8

13.0M sf

11.7 11.8

11.2

11.0M sf 10.6

9.9 9.9

2020-pro-rated 2021 vs. 9.0M sf 8.7

9.1

9.6 9.5

9.0

prior 20-year annual 7.9

Millions, sf

7.5

7.0

average leasing activity 7.0M sf

5.6 5.7 5.5

5.1 4.8

5.0M sf

There is no modern precedent for

the post-COVID slowdown in leasing 3.0M sf

1.8

activity—not 2001 nor 2008—due to 1.0M sf

the sudden change in office

-1.0M sf

occupiers’ future workplace

strategies and the 2020 recession.

Source: AVANT by Avison Young

10Vacancy rate

Sublease vacancy rate Direct vacancy rate

18.0%

14.3%

16.0%

14.0%

12.0%

Record high Chicago CBD

vacancy as of Q1 2021 10.0%

8.0%

The Q1 2021 vacancy rate was recorded at 14.3%- up 170

6.0%

basis points (bps) from pre-pandemic level of 11.2%. This

4.0%

current spike in vacancy is higher then the all time high of

2.0%

12.6% in 2010.

0.0%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2Q21

Source: AVANT by Avison Young

11Vacant sublease space

Vacant sublease space % of total vacant space

5.4 msf

6.0M sf 18.0%

16.0%

5.0M sf

14.0%

4.0M sf 12.0%

Record levels of sublease

vacant space 3.0M sf

10.0%

8.0%

The share of sublease-to-total vacant space stands at 2.0M sf 6.0%

15.1% as subleases continue to drive supply across 4.0%

1.0M sf

Chicago CBD. 2.0%

0.0M sf 0.0%

Source: AVANT by Avison Young

12Sublease supply pipeline

Building classification Asking rent per square foot

Trophy $50-54 1

1 blocks

2%

$45-49 1

$40-44 3

64 blocks

Class B $35-39 3

3.1M sf

25 blocks

39%

Class A $30-34 8

38 blocks

59%

$25-29 4

$20-24 2

Source: AVANT by Avison Young

13Chicago’s aging inventory

10.0M sf

35 properties 9.0M sf

proposed or under 8.0M sf

construction

7.0M sf

12.9 msf 6.0M sf

proposed or under 5.0M sf

construction

4.0M sf

7.7% 3.0M sf

2.0M sf

share of office

inventory 1.0M sf

0.0M sf

1945 2016

2017

2018

2019

2020

2021

2022

2023

2024

average delivery date of Proposed

existing Chicago CBD offices

Source: AVANT by Avison Young

14Office investment dollar volume

Trophy Class A Class B Class C

$7B

$2.4B

$6B

$5B

Chicago CBD office dollar volume $4B

2020 to present $3B

Office sales activity has temporarily paused during the $2B

risk-pricing crisis, decreasing by an annualized rate of $1B

46.9% compared with the prior five-year average dollar

$0B

volume.

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

YTD 2021

Source: AVANT by Avison Young, RCA

1502.

Contact us today

With around-the-corner knowledge,

multi-national expert insights and data-

driven intelligence, our team is ready to

help you unlock economic, social, and

environmental value.

16Get in touch

Jeff Lindenmeyer Danny Nikitas

Principal Principal

Tenant Representation Landlord Representation

+1 312 273 4510 +1 312 940 8794

jeff.lindenmeyer@avisonyoung.com danny.nikitas@avisonyoung.com

Peter Kroner Tommy Maday

Central Region Manager, Insights Central Region Lead, Data

Innovation and Insight Advisory, U.S. Innovation and Insight

+1 312-273-1494 +1 773 945 5837

peter.kroner@avisonyoung.com tommy.maday@avisonyoung.com

17Let’s talk

© 2021 Avison Young Chicago, LLC. All rights reserved. E. & O.E.: The information contained herein

was obtained from sources which we deem reliable and, while thought to be correct, is not

18 guaranteed by Avison Young.You can also read