Central Bank Operations and their Current Challenges in Peru - Paul Castillo B. Central Reserve Bank of Peru

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Central Bank Operations and their Current Challenges in

Peru

Paul Castillo B.

Central Reserve Bank of Peru

XI Central Banking Operations (Digital) Meeting

June 2021

CEMLA

Central Bank Policy Response

Reduction of policy rate to historical minimum

01 Reduction of the policy rate between March and April 2020, from 2.25% to 0.25%, its historical minimum.

Forward guidance: The BCRP Board of Directors emphasized that it considers appropriate to maintain an expansionary

monetary stance as long as the negative effects of the pandemic on inflation and its determinants persist.

Easing of reserve requirements

02

Reduction of the reserve requirement in soles from 5% to 4% and of reserve requirement on FX external liabilities with terms below

two years from 50% to 9%.

Reduction of banks’ minimum current account requirement in soles with the BCRP from 1.0% to 0.75%.

Suspension of the additional reserve requirement associated with dollar loans.

Financial system liquidity

Repos up to 3 years (securities and FX).

03

Easing of portfolio repos (new scheme includes factoring, entities rated up to B +, reduction of minimum guarantee).

Discount window (elimination of limit on operations).

New liquidity facilities: (i) Repos under Government Loan Guarantee Program; (ii) Repos conditional on rescheduling of loan

portfolios; and (iii) liquidity facility under Government Loan Portfolio Guarantee.

Reduced volatility in long-term interest rates and the exchange rate

2

04 FX intervention through spot and derivatives operations.

The current stance of Monetary Policy

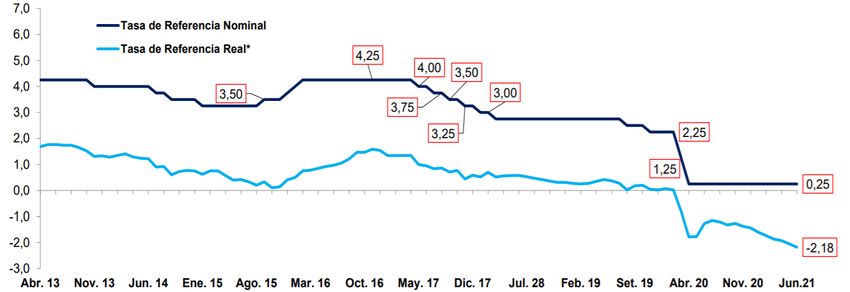

i) Low real interest rates

Monetary Policy rates

( In percentages)

Market expectations for the Monetary policy rate

Nominal rate

( In percentages)

Proyecciones de la TPM (%)

Nominal rate 3,00

Real rate Real rate

2,50

2,00

1,50

1,00

0,50

0,00

Q321 Q421 Q122 Q222 Q322 Q422 Q123 Q

Extranjeros

Foreigners(rango)

(range) Extranjeros

Foreigners(mediana)

(Median)

Local Banks CD Implied rate

Apr.13 Nov.13 Jun.14

Apr Jan.15 Aug.15 Mar.16 Oct.16 May.17

Jan.15 17 JulJul.18

DecDec.17 Apr 20

Set.19 Apr.20 Nov. 20 Jun.21

18

13

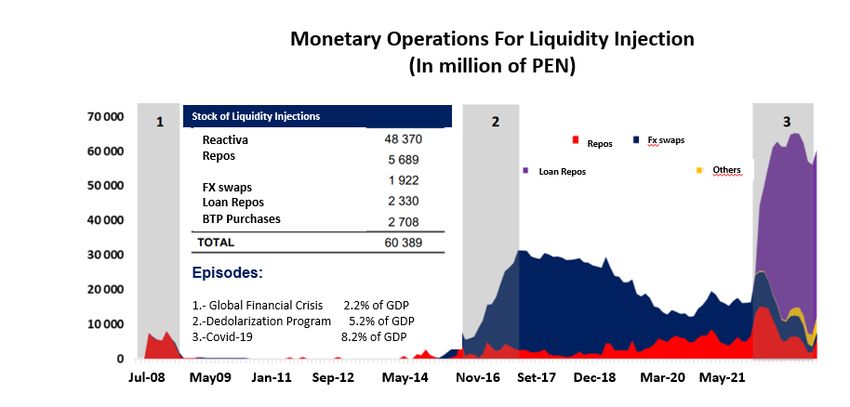

3ii) Large volumes of liquidity in the financial system

4Results

Peru’s GDP is expected to recover to pre-crisis levels by 2022, with a good performance among EMEs.

GDP Real GDP

Growth (Index 2000 = 100)

Average annual growth

(2001-2019)

Peru 4.9

255 Emerging

253 Peru

4.4 246

economies** 237 Emerging

235 World 3.7 228 economies**

215 Colombia 3.8 210 World

200

Chile 3.7

195

Latin America 2.4

175

Brazil 2.2 158

154 LatAm

155

Mexico 1.9

135

115

95

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020* 2021* 2022*

**Excludes China.

Source: IMF (World Economic Outlook Database, October 2020) and BCRP (Peru).

5Results

Countercyclical expansion of credit to the private sector

Credit to non-financial firms: as of January 2020

(Annual growth rate)

23.1 22.1

12.9 11.8

8.9 8.5

6.2

4.2

0.7 0.4

-0.2

Peru

Brazil

New Zealand*

United States

Germany*

China

Chile

Russia

France

Mexico*

Australia

Note: for China, includes credit to the public and private sector.

* As of December 2020.

Source: Central banks

6Results

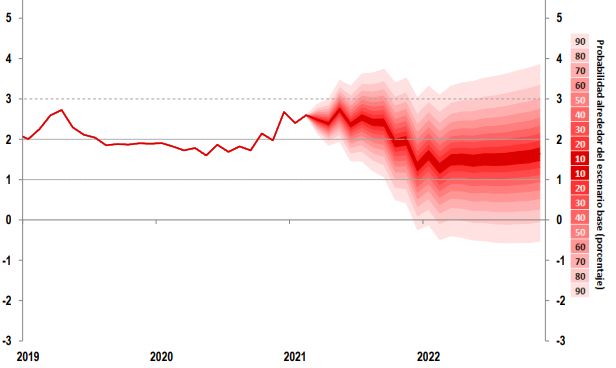

Inflation subdued and within the Central Bank target range

Inflation Forecast: 2021-2022

(Last 12-month % change)

7New challenges for BCRP Monetary Operations

• Mitigate Volatility in financial markets.

– Fears of sooner than anticipated FED´s monetary policy reversal are generating

volatility in capital flows.

– The uncertainty about the direction of macroeconomic policies under a new

government in Peru has triggered an increase in the demand for foreign assets.

– Congress has pass a new Pension Fund withdrawal, which also is generating

volatility in long-term interest rates

• Contain pressures in foreign currency liquidity.

– Demand for deposits in foreign currency has increased recently in response to

higher uncertainty.

8Targeted Liquidity Provision

Repos to inject FX

To reduce pressure on FX liquidity

Repos with bank loans

guarantee by the National

Government Stabilize Financial

To provide liquidity to small

financial institution.

Targeted Markets

liquidity

Repos to provide liquidity to Pension

Funds: provision Support

-To reduce volatility in long-term monetary policy

interest rates

Fx Intervention

transmission

9Banks faced large FX net demand from local clients

Net offer flows in the spot market

3

2

1

USD Billion

0

-1

-2

-3

-4

Jun.-20 Ago.-20 Oct.-20 Dic.-20 Feb.-21 Abr.-21 Jun.-21

Comercial, Food, Refineries, Telecom and Electric Mining and Energy

Retail Customers Non-residents

Pension Funds Others

Total

10In May-June, local banks lost USD 1.5 billion and USD 572 million in term and demand deposits,

respectively, which put pressure on USD liquidity in the local interbank market. As a result, the USD O/N

interbank rate increased from 0.25% to 0.80%.

USD Repo Outstanding Interbank ON Loans

(USD million)

(USD million and %)

4 000

400 0,90

3 500

350 0,80

3 000

300 0,70

2 500 0,60

250

2 000 0,50

200

1 500

0,40

150

0,30

1 000 100 0,20

500 50 0,10

0 0 0,00

03-May. 08-May. 13-May. 18-May. 23-May. 28-May. 02-Jun. 07-Jun. 12-Jun. 2021-Ene. 2021-Feb. 2021-Mar. 2021-Abr. 2021-May. 2021-Jun.

Size Rate

11Non-resident investors reduced their BTPs holdings from 52% to 45% during 2021. Pension Fund

Managers (AFPs) and the BCRP bought BTPs. BCRP has open a Repo facility to AFP to provide liquidity to

this market.

Latam 5: GBI-EM Index (Local Currency) Cumulative change in BTP nominal holdings by group

31Dec20 = 100 8

105

6

4

100 2

PEN billions

0

-2

95

-4

-6

90

-8

-10

Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21

85

04-Jan 25-Jan 15-Feb 08-Mar 29-Mar 19-Apr 10-May 31-May Non residents Pension Funds Private Banks

Sources: BCRP based on data from CAVALI and SBS

Peru Brazil Colombia Chile Mexico

Source: Bloomberg

12Non-residents escalated their demand for hedging and residents increased their preference for dollar-

denominated deposits. The BCRP has continued to use FX intervention through spot and swap operations

to mitigate FX volatility.

Historical Volatility PEN

Intraday Volatility in pip Annualized standard deviations

13Challenges Ahead

1. Use effectively monetary policy instruments to smooth volatility in financial

markets.

2. Support the stance of monetary policy with the appropriated combination of

OMO.

3. Provide timely foreign currency liquidity in order to mitigate the impact of

higher volatility on credit and money markets.

4. Targeted strategy to inject liquidity to smaller financial institutions, mutual

and pension funds.

14You can also read