Building Trust through Execution - March 2022 - Seeking Alpha

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Building Trust through Execution

March 2022

Cautionary Statement Regarding Forward-Looking Statements

and Important Disclosures

Forward-Looking Statements and Cautionary Statements

Certain statements in this presentation concerning future opportunities for Civitas, future financial performance and condition, guidance and any other statements regarding Civitas’ future expectations, beliefs, plans, objectives, financial conditions,

assumptions or future events or performance that are not historical facts are “forward-looking” statements based on assumptions currently believed to be valid. Forward-looking statements are all statements other than statements of historical facts.

The words “anticipate,” “believe,” “ensure,” “expect,” “if,” “intend,” “estimate,” “probable,” “project,” “forecasts,” “predict,” “outlook,” “aim,” “will,” “could,” “should,” “would,” “potential,” “may,” “might,” “anticipate,” “likely” “plan,”

“positioned,” “strategy,” and similar expressions or other words of similar meaning, and the negatives thereof, are intended to identify forward-looking statements. Specific forward-looking statements include statements regarding Civitas’ plans and

expectations with respect to the Transactions and the anticipated impact of the Transactions on Civitas’s results of operations, financial position, growth opportunities and competitive position. The forward-looking statements are intended to be

subject to the safe harbor provided by Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995.

These forward-looking statements involve significant risks and uncertainties that could cause actual results to differ materially from those anticipated, including, but not limited to, Civitas’ future financial condition, results of operations, strategy and

plans; the ability of Civitas to realize anticipated synergies in the timeframe expected or at all; changes in capital markets and the ability of Civitas to finance operations in the manner expected; the effects of commodity prices; and the risks of oil

and gas activities. Additionally, risks and uncertainties that could cause actual results to different materially from those anticipated also include general economic conditions, whether internationally, nationally or in the regional and local market

areas in which we do business; the effects of disruption of our operations or excess supply of oil and natural gas due to the COVID-19 pandemic and the actions by certain oil and natural gas producing countries; the scope, duration and severity of

the COVID-19 pandemic, including any recurrence, as well as the timing of the economic recovery following the pandemic; ability of our customers to meet their obligations to us; our ability to generate sufficient cash flow from operations,

borrowings, or other sources to enable us to fully develop our undeveloped acreage positions; the presence or recoverability of estimated oil and natural gas reserves and the actual future sales volume rates and associated costs; uncertainties

associated with estimates of proved oil and gas reserves; the assumptions underlying forecasts, the assumptions underlying forecasts, including forecasts of production, well costs, capital expenditures, rates of return, expenses, cash flow and cash

flow from purchases and sales of oil and gas; the possibility that the industry may be subject to future local, state, and federal regulatory or legislative actions (including additional taxes and changes in environmental regulation); environmental risks;

seasonal weather conditions; drilling and operating risks, including the risks associated with the employment of horizontal drilling and completion techniques; our ability to acquire adequate supplies of water for drilling and completion operations;

availability of oilfield equipment, services, and personnel; exploration and development risks; competition in the oil and natural gas industry; our ability to secure adequate processing capacity for natural gas we produce, to secure adequate

transportation for oil, natural gas, and natural gas liquids we produce, and to sell the oil, natural gas, and natural gas liquids at market prices; continued hostilities in the Middle East, South America, and other sustained military campaigns or acts of

terrorism or sabotage; and other economic, competitive, governmental, legislative, regulatory, geopolitical, and technological factors that may negatively impact our businesses, operations, or pricing. Expectations regarding business outlook,

including changes in revenue, pricing, capital expenditures, cash flow generation, strategies for our operations, oil and natural gas market conditions, legal, economic and regulatory conditions, and environmental matters are only forecasts

regarding these matters.

Additional information concerning other risk factors is also contained in Civitas’ most recently filed Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and other Securities and Exchange Commission (“SEC”)

filings.

All forward-looking statements speak only as of the date they are made and are based on information available at that time. Civitas does not assume any obligation to update forward-looking statements to reflect circumstances or events that

occur after the date the forward-looking statements were made or to reflect the occurrence of unanticipated events except as required by federal securities laws. As forward-looking statements involve significant risks and uncertainties, caution

should be exercised against placing undue reliance on such statements.

Non-GAAP Measures

To provide investors with additional information in connection with our results as determined in accordance with generally accepted accounting principles in the United States (“GAAP”), we disclose certain non-GAAP financial measures. The non-

GAAP financial measures include Net Debt, Adjusted EBITDAX, PV10, free cash flow and related calculations. We believe the non-GAAP financial measures provide users of our financial information with additional meaningful comparisons between

the current results and results of prior periods, as well as comparisons with peer companies. These non-GAAP financial measures are not measures of financial performance in accordance with GAAP and may exclude items that are significant in

understanding and assessing our financial results. Therefore, these measures should not be considered in isolation or as an alternative or superior to GAAP measures. You should be aware that our presentation of these measures may not be

comparable to similarly-titled measures used by other companies. Reconciliations of each non-GAAP financial measure to the applicable most comparable GAAP measure can be found in the Appendix section of this presentation.

1

Delivering on All Aspects of the New E&P Business Model

Pure Play DJ Basin Operator

High Quality Asset Base Delivers Low F&D Costs

✓ High-return, low-cost wells across DJ Basin asset base

Low-Cost Operations Enable Significant FCF Generation

✓ Sub-$4.00/boe LOE + cash G&A underpins over 20% FCF yield(1)

Fortress Balance Sheet and Operational Flexibility

✓ ~0.2x net leverage and minimal midstream commitments

Returning Capital to Shareholders

✓ Base dividend of $1.85/sh annually and significant variable dividend

Undergoing Opportunistic Consolidation

✓ Bison assets acquired at discount to PDP PV-12 and 1.6x 2022E EBITDA(2)

Leading-Edge Corporate Governance

✓ 100% of executive incentive compensation in stock, 75% based on share

price performance

Industry-Leading Commitment to Sustainability

✓ First carbon neutral E&P operator in Colorado

(1) Reflects unhedged free cash flow at $75/bbl (WTI) and $4.00/mmbtu (Henry Hub) pricing. See slide 6 for free cash flow yield definition.

(2) Based on February 25, 2022 NYMEX strip pricing. Bison acquisition closed on March 1, 2022.

2

High Quality Asset Base

Contiguous acreage position facilitates development optimization

Approximate Civitas Leasehold Positions

Development Area Geography

DJ Basin Net Acres(1)

Western 160,000 Suburban / Rural

Northern

Eastern 124,000 Rural

Southern 105,000 Suburban / Rural Western

Northern 128,000 Rural

Combined Q4 2021 Production Mix(2) (%)

26% Eastern

Oil

40% Southern

153.5

Gas

MBoe/d

NGL

33%

(1) Net acres as of December 31, 2021, adjusted to include ~35,000 net acres from Bison acquisition.

(2) Represents the combined Q4 2021 Civitas production from all predecessor companies - BCEI, XOG, and Crestone. Excludes Bison 2021 volumes.

3

High Quality Asset Base

High-return wells across acreage position

B-TAX Single Well IRRs at $55 WTI

100% Southern Western Eastern

90%

Undeveloped Locations by Area

80%

Area Total % of Total Weighted Avg. IRR

70% Southern 407 42% 43%

Western 301 31% 66%

60% Eastern 256 27% 29%

IRR (%)

Total 964 100% 46%

50%

40%

30%

20%

10%

0%

0 100 200 300 400 500 600 700 800 900

Gross Operated Future Locations

Robust, highly economic inventory of ~1,000 gross operated locations (1)(2)

Note: Single well economics valued at $55/bbl (WTI) / $2.75/mmbtu (Henry Hub) / NGL realizations of 40% of WTI. Average lateral length of ~8,900’.

(1) As of December 31, 2021. Includes 102 locations from the Bison acquisition.

(2) As of January 31, 2022 Civitas had 268 fully approved well permits. The Bison acquisition adds 38 permits.

4

Midstream Ownership Civitas Midstream Infrastructure

Expands upstream returns Eastern

• Total book value of ~$300mm

• Infrastructure focused on operated production and results in lower differentials and

transportation expense

315 MMcf/d of gas gathering capacity

Eastern

280 miles of gas gathering, gas-lift, and sales lines

26 pipeline interconnects to 5 midstream gas processors

22 centralized compressor sites, 67,000 total centralized hp

Gas

Southern

Compressor stations - Pony 5,500hp & Mustang 5,600hp

Southern

Optional phase II expansion at Mustang of 30 MMcf/d Pony Compressor

Station

Mustang

Compressor

Oil line to NGL (Riverside), Taproot (Buckingham), Black Diamond Station

5 CPFs with total 77 Mbo/d capacity CIVI Leasehold

Oil

Compressor Station

35 miles of total oil gathering

Pipeline

Building new oil gathering system in Southern area in 2022 Oil

Oil – Under Construction

H2O

Gas

54 miles of water gathering/delivery connected to three 3rd party disposal wells

Water

5

Low-Cost Operations Enable Significant FCF Generation

Peer-Leading Operating Cost ($/Boe) (1)(2) Oil Price vs. Estimated 2022 FCF Yield (3)(4)

Operating Costs ($/Boe) % Oil $10.73 $1,500 35%

$10.28

Free Cash Flow ($MM)

Free Cash Flow Yield

30%

$8.29

$7.47 $7.62 $7.65 $1,000

25%

$6.40

$6.05

20%

$500

$3.85 $3.94

15%

80%

$0 10%

64% 65%

57% 55% 53% $65 WTI $75 WTI $85 WTI

45% 45% 44%

33%

Hedged Free Cash Flow Unhedged Free Cash Flow

CIVI Peer A Peer B Peer C Peer D Peer E Peer F Peer G Peer H Peer I

Hedged Free Cash Flow Yield Unhedged Free Cash Flow Yield

2022E

• Relentless focus on controllable cash operating costs • Attractive 2022E unhedged free cash flow yield of >20%

(lease operating expense and cash G&A expense at $75/bbl flat pricing

highlighted in chart)

• 2022E reinvestment rate is higher than target due to

• Low-cost structure and oily mix enhances recycle ratio continuing the Bison 2022 development program. Civitas

and corporate level returns expects to bring reinvestment rates in line with target in

2023, further increasing FCF yields

(1) Represents reported Q4 2021 lease operating expense and cash G&A for all peers except for Peer D and Peer F, which represent reported Q3 2021 metrics due to Q4 2021 metrics not yet reported.

(2) Oil-Weighted peers include CDEV, CPE, ESTE, MGY, MTDR, MUR, OAS, PDCE, and ROCC.

(3) Free cash flow yield represents 2022E operating cash flow before working capital changes less capital expenditures divided by CIVI’s market capitalization as of February 25, 2022, with 85 MM shares outstanding.

6

(4) Free cash flow metrics include Bison. Price decks assume $4.00/mmbtu (Henry Hub) and NGL realizations of 40% of WTI.

Fortress Balance Sheet

($ in millions)

Pro Forma Capitalization as of 3/1/22 PF For Bison Key Highlights:

Rev olv ing Credit Facility ($1bn BB; $800 ECA) $0 • PDP coverage of ~11x total debt

7.5% Senior Unsecured Notes due April 2026 100

5.0% Senior Unsecured notes due October 2026 400 • Financial policy and goals include:

Total Debt $500

(-) Cash (136) • Maintaining production with reduced reinvestment rates

Net Debt $364

• Operate at front end of cost curve

Pro Forma PDP PV-10

(1) • Maintain low leverage, with a target of 0.5x Debt to

PDP PV-10 ~$5,300

EBITDAX

Credit Statistics • Prioritize cash returns to shareholders

PDP PV-10 / Total Debt 10.6x

PDP PV-10 / Net Debt 14.6x

(2)

Net Debt / 2022E Hedged EBI TDAX 0.2x

(2)

Net Debt / 2022E Unhedged EBI TDAX 0.2x

(3)

Liquidity ($800 ECA) $924

Note: “BB” refers to “Borrowing Base” and “ECA” refers to “Elected Commitment Amount.”

(1) Reflects year-end 2021 PDP PV-10 with an effective date of December 31, 2021 at $75/bbl (WTI) / $4.00/mmbtu (Henry Hub) pricing.

(2) 2022E EBITDAX reflects $75/bbl (WTI) / $4.00/mmbtu (Henry Hub) pricing.

7

(3) Liquidity adjusted for ~$13 MM in letters of credit.

Returning Capital to Our Shareholders

Stockholder Return Philosophy 2022E Dividend Yield(1)

• Quarterly base dividend: $0.4625/share to be paid on 3/30 to 10.2%

Base Variable

9.9%

shareholders of record on 3/18 9.4%

7.2%

6.6% 6.5%

• Peer-leading 3.9% base yield(1) 6.3%

7.2% 7.1%

3.7%

6.1%

• Potential to increase based on synergies from future 5.2%

1.9% 1.8% 1.8% 1.8% 1.8%

consolidation 3.9%

2.6% 2.3% 2.8% 0.4% 0.1%

1.2% 1.4%

CIVI CTRA CHK DVN PXD EOG MGY OAS MUR FANG PDCE MTDR SM

• First quarterly variable dividend: $0.75/share to be paid on

3/30 to shareholders of record on 3/18:

Dividend History

• 50% of Civitas’ 2021 combined 12-month average

Base Variable $1.2125

quarterly free cash flow

• See appendix for additional calculation detail $0.7500

$0.4625 $0.4625

$0.3500 $0.3500

2Q21 3Q21 4Q21 1Q22

Source: Market data per Eikon as of February 25, 2022.

Note: All figures are pro forma for any acquisitions or transactions, where applicable.

(1) Based on 2022E fixed and variable distributions per share and share prices as of February 25, 2022.

8

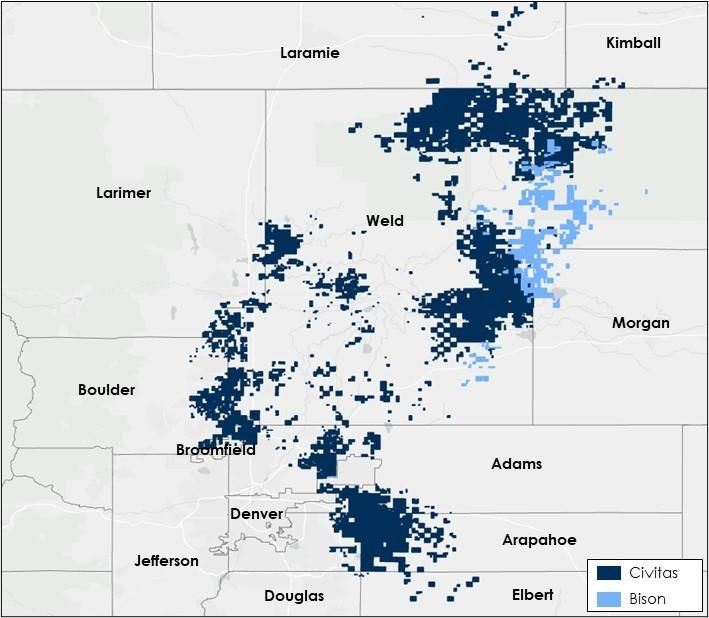

Firm Believers in Opportunistic Consolidation

• Civitas will continue to be a disciplined transaction partner DJ Basin Acreage Summary

Laramie Kimball

• Focus on value creation and accretion

• Increase efficiencies with economies of scale

• Operating expertise across the basin Weld

Larimer

• Maintain low pro forma leverage with a through cycle target of 0.5x

• Focus on offsetting acreage and operatorship

• Bison acquisition case study

Morgan

• Total consideration of 1.6x 2022E EBITDA is a discount to PDP PV-12 Boulder

with no consideration given to 102 undeveloped locations

• 38 drill-ready permits Broomfield Civitas (1)

Bayswater

• Accretive to NAV, 2022E production, EBITDA and FCF Adams

Confluence

Jefferson Denver

• No incremental G&A Arapahoe Mallard

PDC (2)

• Pro forma leverage of 0.2x Douglas Elbert Verdad

Source: Enverus.

(1) Includes leasehold from Bison acquisition.

(2) Pro forma acreage for PDC Energy’s announced acquisition of Great Western Petroleum.

9Reducing Operational Emissions

“Through our

Civitas is committed to driving down operational emissions through the use of commitment to highly

innovative best management practices and implementation of new technologies(1) responsible operations,

we will work to produce

energy in a way that is

safe, efficient, and

environmentally

sustainable while

meeting the world’s

Zero routine flaring in Electric rigs, Tier IV Closed-loop 70% liquids produced

all new developments and eFrac Tank Gauging at facilities with non- energy demands.”

completion fleets emitting pneumatics

- Ben Dell, Chairman

Use pipelines where Utilize NextGen Facilities designed to Monthly LDAR

feasible (transport oil flowback to pipeline mitigate maintenance and daily visual

and water) infrastructure emissions inspections

(1) Emissions reduction mitigation measures implemented where technologically, economically and practicably feasible.

10Demonstrating Climate Leadership

Colorado’s first carbon neutral energy producer (Scope 1 & 2 basis) 2020 GHG Intensity (mt CO2e/MBOE)

• Eliminate operational emissions as first priority 29.5

• Offset remaining Scope 1 emissions using only certified offset credits 24.9

• All credits sourced from largest and most credible registries: Gold

Standard, Verra, ACR, CAR

14.1

• Offset Scope 2 emissions using only Green-e certified RECs 12.9

• All RECs sourced to date from the Rockies sub-grid region as a best

6.7

practice

• Move Scope1 emissions to Scope 2 wherever possible, consistent with

energy transition goals

Peer 1 Peer 2 Peer 3 Civitas Peer 4

Source: 2020 EPA Subpart W Data.

11Valuing Community Engagement

Civitas Community Fund Plugging Colorado’s Orphaned Wells

• Civitas is focused on remaining a trusted, engaged partner in our Civitas committed to plugging all orphaned wells in

communities the Greater Denver Area and Northern Front Range of

• The Civitas Community Fund will source revenue from specific Colorado

developments that will provide community project grants and

scholarships with special dispensation for community members Abandoned by former operators whose clean-up

located closest to our operations would otherwise be the responsibility of the state of

Colorado

Developing Community Solar Investing in EV Transition

• Civitas is forming a • Civitas has committed to When wells are left unplugged, they can emit

partnership to develop installation of electric vehicle greenhouse gases such as methane and carbon

community solar gardens charging stations in the dioxide, which amplify the effects of climate change

throughout Colorado’s Front communities where we

Range operate

“We are proud to eliminate these wells for the benefit of the

• These initiatives will reduce • We have begun converting communities where we live and work”

utility costs for neighboring our own work fleet to EV

subscribers and help hybrid utility vehicles and EVs,

Colorado meet its renewable saving emissions and costs

energy goals

12Leading-Edge Corporate Governance

• Director service compensated in stock • Diversity of gender, race and industry experience

and held through duration of service

• Annual board elections • Dedicated ESG Board Committee

Brian Steck Howard Willard III

Ben Dell Carrie Fox Independent Director Independent Director

Chairman of the Board Independent Director Chair, Nomination & Chair, Compensation

Governance Committee Committee

Morris Clark Carrie Hudak James Trimble Jeffrey Wojahn

Independent Director Independent Director

Independent Director Independent Director

Chair, Audit Committee Chair, ESG Committee

132022 Guidance

Production • D&C program reflects ~3.5 rigs / ~3 frac crews

Total Production (MBoed) 156 – 167

• Expected oil price differential of -$6.00/Bbl relative to WTI

Oil Production (MBbld) 69 – 75

• CIVI does not expect to pay cash income tax in 2022 at

% Liquids 68 – 70% $75/Bbl WTI oil and $4.00/MMBtu Henry Hub gas prices

Unit Costs ($/Boe, unless stated) • Guidance includes Bison acquisition which closed on March

1, 2022

Lease Operating Expense $2.50 – 2.75

Gathering, Transportation & Processing $3.25 – 3.50 2022E Operated Development Schedule

Midstream Operating Expense $0.50 – 0.60 Gross Horizontal Wells Drilled 190-210

Recurring Cash G&A ($ in millions) $70 – 75 Average WI% / Lateral Length 82% / 2.1 miles

Production Taxes (% of revenue) 8 – 9% Gross Horizontal Wells Completed 165-175

Capital Expenditures ($ in millions) Average WI% / Lateral Length 83% / 2.2 miles

Drilling & Completion $825 – 950 Gross Horizontal Wells Brought Online 155-165

Land, Midstream and Other $70 – 90 Average WI% / Lateral Length 85% / 2.0 miles

Note: Guidance assumes $75/bbl (WTI) and $4.00/mmbtu (Henry Hub) pricing.

14Appendix

Q1-2022 Dividend Calculation

• Quarterly base dividend of $0.4625/share Q1 2022 Total Dividend Calculation ($MM)

(1)

• Quarterly variable dividend framework

(2)

Av erage Quarterly Free Cash Flows Ov er Prior 12 Months $167

• 50% of FCF (before changes in working capital

and after base dividend) Less: Quarterly Base Div idend ($39)

• Based on average quarterly FCF over prior 12

months Av erage Quarterly Free Cash Flow After Base Div idend $128

• To be paid in combination with base dividend, Variable Div idend: 50% Payout $64

commencing March 2022

Variable Dividend / Share $0.7500

• Total first quarter dividend of $1.2125/share

• To be paid on March 30th to shareholders of record as (+) Base Dividend / Share $0.4625

of March 18th

(=) Total Dividend / Share $1.2125

(1) Per share calculations based on 85 MM shares outstanding.

(2) Free cash flow is calculated as operating cash flow before working capital changes less capital expenditures.

16Year-End 2021 CIVI Proved Reserves

Net Oil Net Gas Net NGL Net BOE SEC PV-10(1) $75/bbl PV-10(2)

Reserve Category

(MMBBL) (BCF) (MMBBL) (MMBOE) ($MM) ($MM)

PDP 98 714 85 302 $4,302 $4,859

PDN 6 35 4 16 $162 $201

PUD 40 140 17 80 $864 $1,090

Total Proved 144 888 106 398 $5,327 $6,150

Proved Reserves by Commodity Proved Reserves by Category PV-10 by Category

PUD reserves reflect a conservative booking policy of 234 gross operated locations, which is less than two years of activity at our current rig pace

Note: Excludes Bison acquisition.

(1) SEC Pricing Assumptions: $66.56/bbl (WTI), $3.598/mmbtu (Henry Hub); PV-10 graph above reflects SEC PV-10.

(2) Assumes $75/bbl (WTI) and $4.00/mmbtu (Henry Hub). Excludes ~$390 MM in PDP PV-10 value for the Bison assets.

17Oil Hedge Positions Summary

Civitas Oil Hedges (Bbl/d)

35,000

32,740

30,000

24,717

25,000 $44.15 - $59.56

21,045

20,000 18,669

$41.52 - $64.00

$42.35 - $66.22

15,000

$42.39 - $67.38

10,000

$47.36

5,000 $49.56 $47.00 $46.84 3,231

1,884 1,675 1,527

$45.77 - $64.05 795 1,005 692

$48.10 - $57.69 $47.91 - $57.48 $49.04 - $56.49 $45.00 - $56.25 $51.81 $56.50

– $45.42 $46.29 $46.79 $46.75 $55.65

Q1 2022 Q2 2022 Q3 2022 Q4 2022 Q1 2023 Q2 2023 Q3 2023 Q4 2023 Q1 2024 Q2 2024 Q3 2024

Oil Swaps Oil Collars

Note: Hedge positions as of Feb 28, 2022, pro forma for closed Bison acquisition.

18Gas Hedge Positions Summary

Civitas Gas Hedges (MMBtu/d)

175,000

NGL OPIS Swaps

157,162 2022: 4,000 Bbl/d OPIS swaps at $20.22/Bbl

148,879 146,105

150,000 144,058

$2.18 - $2.78

125,000

$2.42 - $3.31 $2.59 - $3.67 $2.60 - $3.68

100,000

75,000

$2.84

55,098

50,000 $2.07 - $3.23 45,979 45,767 45,613

$2.28 - $2.91 $2.34 - $2.96 $2.38 - $2.96

31,702 31,587 31,468

$2.66 $2.67 $2.67 $2.50 - $3.37 $2.21 - $2.90 $2.50 - $3.16

25,000 $2.51 $2.51 $2.51 $2.51

$2.57 $2.57 $2.57

–

Q1 2022 Q2 2022 Q3 2022 Q4 2022 Q1 2023 Q2 2023 Q3 2023 Q4 2023 Q1 2024 Q2 2024 Q3 2024

Gas Swaps Gas Collars

Note: Hedge positions as of Feb 28, 2022, pro forma for closed Bison acquisition.

19Adjusted EBITDAX Reconciliation

Source: Company disclosure. $ in thousands.

20You can also read