Barclays 2018 High Yield Bond & Syndicated Loan Conference May 2018

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Barclays 2018 High Yield Bond & Syndicated Loan Conference May 2018

Safe Harbor

This presentation may contain “forward-looking” statements, as defined in federal securities laws including the Private Securities Litigation Reform Act of 1995, which are based on our current

expectations, estimates, forecasts and projections. Statements that are not historical facts, including statements about the beliefs, expectations and future plans and strategies of the Company, are

forward-looking statements. Actual results may differ materially from those expressed in any forward-looking statements. The following important factors, among other things, could cause or

contribute to actual results being materially and adversely different from those described or implied by such forward-looking statements including, but not limited to: those discussed in this release;

we operate in highly competitive industries, and customers may not continue to purchase products or services, which would result in reduced revenue and loss of market share; we may be unable to

grow our revenues and cash flows despite the initiatives we have implemented; failure to anticipate the need for and introduce new products and services or to compete with new technologies may

compromise our success in the telecommunications industry; our access lines, which generate a significant portion of our cash flows and profits, are decreasing in number and if we continue to

experience access line losses similar to the past several years, our revenues, earnings and cash flows from operations may be adversely impacted; our failure to meet performance standards under

our agreements could result in customers terminating their relationships with us or customers being entitled to receive financial compensation, which would lead to reduced revenues and/or

increased costs; we generate a substantial portion of our revenue by serving a limited geographic area; a large customer accounts for a significant portion of our revenues and accounts receivable

and the loss or significant reduction in business from this customer would cause operating revenues to decline and could negatively impact profitability and cash flows; maintaining our

telecommunications networks requires significant capital expenditures, and our inability or failure to maintain our telecommunications networks could have a material impact on our market share

and ability to generate revenue; increases in broadband usage may cause network capacity limitations, resulting in service disruptions or reduced capacity for customers; we may be liable for

material that content providers distribute on our networks; cyber attacks or other breaches of network or other information technology security could have an adverse effect on our business; natural

disasters, terrorists acts or acts of war could cause damage to our infrastructure and result in significant disruptions to our operations; the regulation of our businesses by federal and state

authorities may, among other things, place us at a competitive disadvantage, restrict our ability to price our products and services and threaten our operating licenses; we depend on a number of

third party providers, and the loss of, or problems with, one or more of these providers may impede our growth or cause us to lose customers; a failure of back-office information technology systems

could adversely affect our results of operations and financial condition; if we fail to extend or renegotiate our collective bargaining agreements with our labor union when they expire or if our

unionized employees were to engage in a strike or other work stoppage, our business and operating results could be materially harmed; the loss of any of the senior management team or attrition

among key sales associates could adversely affect our business, financial condition, results of operations and cash flows; our debt could limit our ability to fund operations, raise additional capital,

and fulfill our obligations, which, in turn, would have a material adverse effect on our businesses and prospects generally; our indebtedness imposes significant restrictions on us; we depend on our

loans and credit facilities to provide for our short-term financing requirements in excess of amounts generated by operations, and the availability of those funds may be reduced or limited; the

servicing of our indebtedness is dependent on our ability to generate cash, which could be impacted by many factors beyond our control; we depend on the receipt of dividends or other

intercompany transfers from our subsidiaries and investments; the trading price of our common shares may be volatile, and the value of an investment in our common shares may decline; the

uncertain economic environment, including uncertainty in the U.S. and world securities markets, could impact our business and financial condition; our future cash flows could be adversely affected

if it is unable to fully realize our deferred tax assets; adverse changes in the value of assets or obligations associated with our employee benefit plans could negatively impact shareowners’ deficit and

liquidity; third parties may claim that we are infringing upon their intellectual property, and we could suffer significant litigation or licensing expenses or be prevented from selling products; third

parties may infringe upon our intellectual property, and we may expend significant resources enforcing our rights or suffer competitive injury; we could be subject to a significant amount of litigation,

which could require us to pay significant damages or settlements; we could incur significant costs resulting from complying with, or potential violations of, environmental, health and human safety

laws; the timing and likelihood of completing the merger with Hawaiian Telcom, including the timing, receipt and terms and conditions of any required governmental and regulatory approvals for the

proposed transaction that could reduce anticipated benefits or cause the parties to abandon the transaction; the possibility that competing offers or acquisition proposals for Hawaiian Telcom will be

made; the occurrence of any event, change or other circumstance that could give rise to the termination of the proposed transaction; the possibility that the expected synergies and value creation

from the proposed transaction involving Hawaiian Telcom will not be realized or will not be realized within the expected time period; the risk that the businesses of the Company and Hawaiian

Telcom and other acquired companies will not be integrated successfully; disruption from the proposed transaction involving Hawaiian Telcom making it more difficult to maintain business and

operational relationships; the risk that unexpected costs will be incurred; and the possibility that the proposed transaction involving Hawaiian Telcom does not close, including due to the failure to

satisfy the closing conditions and the other risks and uncertainties detailed in our filings with the SEC, including our Form 10-K report, Form 10-Q reports and Form 8-K reports, as well as Hawaiian

Telcom’s filings with the SEC, including its Form 10-K reports, Form 10-Q reports and Form 8-K reports.

These forward-looking statements are based on information, plans and estimates as of the date hereof and there may be other factors that may cause our actual results to differ materially from

these forward-looking statements. We assume no obligation to update the information contained in this release except as required by applicable law.

2

Non-GAAP Financial Measures

This presentation contains information about adjusted earnings before interest, taxes, depreciation and

amortization (Adjusted EBITDA), Adjusted EBITDA margin, net debt, net income (loss) applicable to common

shareholders excluding special items and free cash flow. These are non-GAAP financial measures used by

Cincinnati Bell management when evaluating results of operations and cash flow. Management believes these

measures also provide users of the financial statements with additional and useful comparisons of current results

of operations and cash flows with past and future periods. Non-GAAP financial measures should not be

construed as being more important than comparable GAAP measures. Detailed reconciliations of these non-

GAAP financial measures to comparable GAAP financial measures have been included in the tables distributed

with this release and are available in the Investor Relations section of www.cincinnatibell.com within the Investor

Relations section.

3

Cincinnati Bell’s Strategic

Transformation

Cincinnati Bell’s Strategic Transformation

Building Two Distinct, Complementary Lines of Business with Expanded Geographic Reach,

Customer Diversification and Increased Runway for Growth

Entertainment & Communications IT Services & Hardware

Fiber continues to differentiate Cincinnati Transform to become an international

Bell from traditional carriers hybrid cloud solutions provider

Focus on investing • Strong demand for our fiber suite of products • Strengthening North American platform

1 where we are

winning

• Fioptics revenue increased 13% year-over-year

• Growth in Fioptics internet subscribers more • Growing UCAAS sales funnel – with wins nationwide

than offset DSL declines

• IT services business, combined with our network

2 Why we win

• The more fiber, the greater the market

penetration

expertise, while being faster and more flexible than

the competition

• Continued investments in high speed, high • Enhanced scale and expanded portfolio of

3 How we win bandwidth fiber network creates future-

proof asset that has a high barrier to entry

complementary IT offerings to win larger, multi-

faceted deals

4 Significant market

opportunity

• Growth driven by IoT and 5G

infrastructure spend

• Growth driven by UCaaS, cloud, and security

5 Multiple upside • Network peers trading at ~8-11x • IT peers trading at ~8-10x

5

Page 5We Are Investing Where We Are Winning… Entertainment &

Communications

• Expanded our fiber network to reach 70% of the homes and businesses in Greater Cincinnati (53% FTTP)

• We are winning against national competitors where we have fiber, with 40% Fioptics penetration that is ~50% where we have

FTTP, and significant Fioptics contribution to revenue growth

Wireline Capex Last 3 Years Fiber Availability Fioptics Growth

as % of Revenue

+25 Mbps1

($ in mm) 2017 Y/Y Q4 2017 Y/Y

FTTH / 1 Gbps Revenue $310 +22% $80 +17%

32.1% 70.0%

% of E&C Revenue 39% 41%

Internet Subs (000s) 226.6 +15%

17.0%

% Penetration 40%

54.0%

50.0% Video Subs (000s) 146.5 +6%

% Penetration 26%

42.0%

39.0%

17.0%

15.5% 15.4%

53.0%

39.0% 32.0%

13.7% 20.0%

1 Gbps $310

24.0%

$254

22.0%

$191

18.0% 1 Gbps $142

15.0% +100 Mbps 15.0% $101

$68

$28 $47

+75 Mbps +100 Mbps

1 2 3 4 5

1 2 3 3 4 5 5,6 2010 2011 2012 2013 2014 2015 2016 2017

Fioptics Revenue

Source: Company filings and Capital IQ (as of Dec 31, 2017)

[1] Excludes Level 3 and adjusted for data centers

[2] Pro forma for FairPoint

[3] Historicals reflect actuals and are not adjusted to pro forma Verizon CTF, ELNK or Broadview

[4] CBB reflects 50 Mbps or more; CTL reflects 40 Mbps or more as of Q2 2016 6

[5] Not pro forma for Level 3 or EarthLink

[6] Expects 20% of homes with GPON / 1 Gbps by 2019…Which Creates Competitive Advantages And Future Entertainment &

Communications

Growth Opportunities

Not a matter of “IF” high bandwidth is necessary but a matter of when not having it makes you irrelevant

Growth in Network Capacity and Speed Demands 5G and Small Cell Opportunity

Forecast Global Data Traffic (PB/Month)1

• Market opportunity for 5G acceleration

– Verizon plans to deploy 8k to 10k small cells in

278,108

228,411 Boston, investing $300 million over six years

186,454

150,910 – AT&T plans to launch mobile 5G in 12 U.S. markets

121,694 this year

• UBS research estimates 500x increase in small cell sites to

support 5G densification in NYC, based on mmWave

2017 2018 2019 2020 2021 spectrum and 100 meter propagation distance

Fixed internet Managed IP Mobile data

Speed Capability (Mbps) Small Cells (000s) 4

455

1,000 1,000 1,000 FTTN

350

260

186

150 125

~200 - 300 50 -

74

300 25

- 300 100

3 - 25 3 - 12

2 3

2016 2017 2018 2019 2020 2021 2022

FTTH Cable (DOCSIS 5G Wireless Cable (DOCSIS G. Fast VDSL DSL 4G LTE

3.1) 3.0)

Cincinnati Bell is Well-Positioned to Capitalize on IoT and wireless 5G Opportunities

Source: Nokia, Wall Street research and news articles

[1] Cisco VNI Forecast as of 6/6/17

[2] G. Fast is “Fast access to subscriber terminals” and is a standard to offer fiber-like speeds over copper wires

[3] VDSL stands for “very high bit rate digital subscriber line” and is digital subscriber line technology that provides data transmission faster than asymmetric data subscriber lines

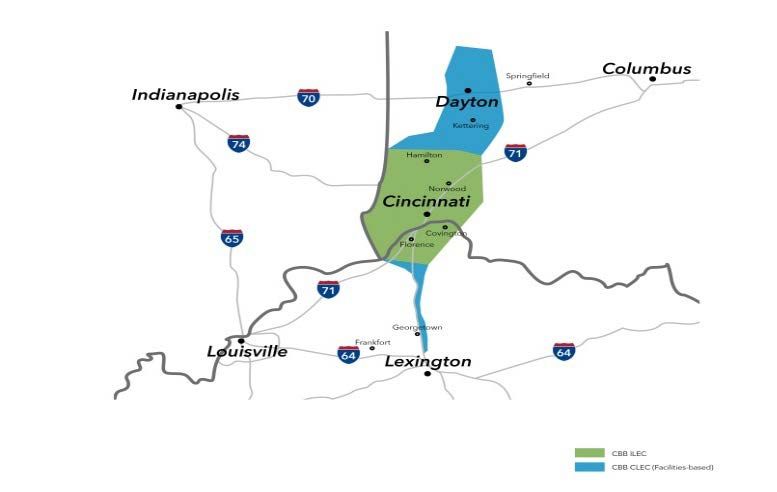

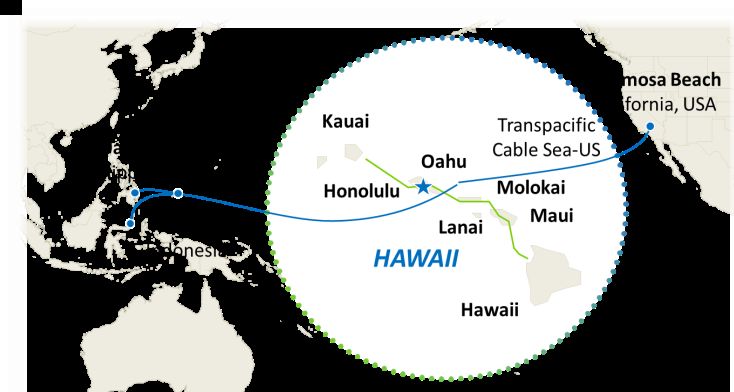

[4] SNL Small Cell and Tower Projections as of 8/30/17 7Merger with Hawaiian Telcom Represents Opportunity to Scale Entertainment &

Communications

Cincinnati Bell’s Fiber Success in Another Attractive Market

Combined Network business with over 14k fiber route miles

Cincinnati Bell Network Map

• Hawaii’s fiber-centric technology leader providing voice, video,

Business broadband, data center and cloud solutions

Description • Incumbent position with leading market share and strong

brand equity

• Adds operational scale and expands the Company’s fiber-

significant footprint and commercial opportunity to Hawaii

Growth • MDU growth opportunity and strategic subset a Trans-Pacific

cable asset

Opportunity

• Opportunity to continue fiber investment in Hawaii – currently

65% FTTH in Oahu, with opportunity to continue Oahu build

and invest in other islands where ROI makes sense Hawaiian Telcom Network Map

Expected • Network: ~$11mm annually

Cost *To be realized within two years post-close, and excluding

Synergies* potential revenue synergies from cross-selling opportunities

• Approved by Hawaiian Telcom shareholders

• Cleared the HSR review period

Approval • Received approval from Hawaii DCCA Cable Television Division

Process & and Public Utilities Commission

Closing • Pending approval from FCC

• Closing expected in H2 2018

8Acquisition of OnX, Creating A Leading North American IT Services &

Hardware

IT Services Provider…

Combined IT Services business with a diversified customer base and increased geographic footprint

• OnX provides industry-leading technology services

Business and solutions to enterprise customers in the U.S.,

20+ 2,000+

Description Offices Customers

Canada and the U.K.

• Expansion of geographic footprint and addressable

market beyond Cincinnati to accelerate momentum

Growth in IT services

Opportunity

• Attractive enterprise customer base adding Offices

diversification and cross-selling opportunities

• ~$10mm annually

Expected

*To be realized within two years post-close, and excluding

Cost Synergies* potential revenue synergies from cross-selling opportunities

• Closed on October 2, 2017 Key Technology Partners / Certifications

Closing • 1Q18 Contribution:

and 4Q17 − $45mm in revenue

Contribution

9

9…which Positions Cincinnati Bell to Tap Into a IT Services &

Hardware

Fragmented and Growing IT Services Market…

Fragmented IT Services Market1 Growing Markets

$402bn Market

2017 2015-2020

Top Provider

Market2

Market Size3 CAGR

4%

Cloud-Based Unified Communications4 $109 13%

IaaS (Cloud) 18 32%

Next Top 10 Providers

25% Enterprise Security Services 22 10%

Tech Consulting & Implementation 120 3%

Other Service Providers

71% Q1 ’18 Service Revenue Mix

Infrastructure

Solutions

Consulting

Scaling to Create Strategic Flexibility 21%

30%

Goal of $100mm Adj. EBITDA to create scale

Communications

31% Cloud

18%

[1] Based on Gartner research; Market defined as 2016A North America IT Services market

[2] Based on Gartner research

[3] Market size in billions, figures represent North America estimates

[4] Includes cloud-based conferencing, telephony and messaging

10

10…Focused on Growing Higher Margin, Recurring IT Services &

Hardware

IT Services

Recent Strategic Initiatives Growing Higher Margin Recurring Services

• Launched nationwide SD-WAN and NaaS ($ mm) Total Services Revenue1

products $205

$225 $232

$168

• Reorganized segment adding CLEC commercial $135 $143

operations to highlight strength of growing

UCaaS business

• Continued demand for Communications 2012 2013 2014 2015 2016 2017

1

services– recent wins:

Diversifying Customer Mix

• SD-WAN and UCaaS deal provides service GE Revenue % of IT Services & Hardware Revenue

to 3,500 retail locations (4Q17)

33%

• UCaaS contract hosts 32,000 profiles

across 96 locations (1Q18)Transformation Has Created A Unique Scalable IT IT Services &

Hardware

Services Platform

1,500+ 2,800+ 2,400+

Employees Technology Certifications Customers

25 Locations Broad Solution Practices Blue Chip Customer Base

Communications Cloud

Consulting

Services Infrastructure

Note: Figures shown as of 12/31/17

12

12Execution of Strategy Has Continued to Yield Results…

Disciplined Capital Allocation Strategy Reorganizing to Facilitate Growth and Cost Management

• Investments in fiber and IT solutions create • Completed internal reorganization leading to

platforms for long-term value

two distinct business units, with the

• Monetized CyrusOne and wireless assets – appropriate scale, structure and leadership

improved leverage profile from ~6x in 2013 to ~4x committed to driving their respective brands

in 2017

forward

• Ability to fund fiber investments through cash flow • Reporting changes beginning 1Q’18 to improve

Strategic Revenue Growth

investors’ ability to appropriately value these

services independently

($ in mm)

$727 – Entertainment and Communications segment is

$649

reported in the following three categories:

$331 Fioptics, Enterprise Fiber and Legacy

$317

86

78

– IT Services and Hardware segment is reported in

254 310

the following practices: Communications, Cloud,

2016 2017 Consulting and Infrastructure Solutions

Fioptics Revenue Enterprise Other Revenue IT Services Revenue (previously referred to as Telecom and IT

% of Total Revenue Hardware sales)

64% 68%

13

13Strong Performance Through

TransformationFirst Quarter 2018 Highlights

Key Financial Metrics

Total Revenue Adjusted EBITDA

($ in mm) ($ in mm) $79

$296 $73

$12

$7

$250

$128

$81

$68 $70

$175 $174

-$6 -$6 -$2 -$3

1Q17 1Q18 1Q17 1Q18

Entertainment & Communications IT Services & Hardware Intersegment Entertainment & Communications IT Services & Hardware Corporate

Entertainment & Communications IT Services & Hardware

Fioptics Communications Cloud Services

Revenue of Revenue of Revenue of

580,800

$83mm addresses $41mm $23mm

+13% y/y +7% y/y +11% y/y +8% y/y

15

Page 15Continued Success with Fioptics

Total Fioptics Subscribers Fioptics Addresses Fioptics Penetration (y/y)

(in thousands) (in thousands)

Video 25%

581

545 Internet 40%

233

Voice 18% =

207 441

141 146

404

Fioptics Monthly ARPU

100 107

141 140 Video $89 +4% y/y

Internet $50 +3% y/y

1Q17 1Q18 1Q17 1Q18

Internet Video Voice

FTTP

(1)

FTTN (2)

Voice $29 +6% y/y

• Internet subscriber net adds totaled 2,200 in 1Q18 – Fioptics Internet growth offset legacy DSL

declines

CBB continues to win with

• Goal is to construct Fioptics to 35,000 new addresses during 2018 – passed 8,600 new homes and

businesses during in 1Q18 fiber in a very competitive

• Capital expenditures for Fioptics expected to be between $95mm to $110mm during 2018

environment

1. FTTP: fiber-to-the-premise 2. FTTN: fiber-to-the-node

16

Page 16IT Services &

Hardware

Strong Revenue Growth across Each Practice

($ in mm) 1Q18 Y/Y Communications Metrics (q/q)

Consulting $38 n/m NaaS 564

Cloud 23 8% Locations

Communications 41 11% SD-WAN Momentum in

117 Communications

locations

Infrastructure Solutions 26 n/m

Hosted UCaaS 178,457

Total $128 58%

Profiles

Trusted provider of Voice services for more than 100 years

17

Page 17Capital Structure and Free Cash Flow Performance

($ in mm)

Free Cash Flow Net Debt

Q1 Y/Y

2018 Change 4.1x 4.1x

Net Leverage(1) Net Leverage(1)

Adjusted EBITDA (Non-GAAP) $79 $6

Interest Payments (27) (8)

Pension and OPEB Payments (3) -

Stock-based Compensation 1 (2)

Restructuring & Severance related payments (7) 6 $1,351 $1,333

Transaction and Integration Costs (2) (2)

Working Capital and Other 18 5

Cash Provided by Operating Activities (GAAP) $59 $5

Capital expenditures (33) 22 4Q17 1Q18

Restructuring & severance related payments 7 (6)

Preferred stock dividends (3) -

Transaction and Integration Costs 2 2

Other 1 - Selected 2018 Free Cash Flow Items

Free Cash Flow (Non-GAAP) $33 $23

Capital Expenditures $190mm – $210mm

• Strong FCF performance primarily due to timing interest Interest payments $115mm – $125mm

payments and capital expenditures

Pension and OPEB payments $15mm – $20mm

• On track to generate positive FCF during 2018

1. Calculated as net debt divided by 2018 Adjusted EBITDA Guidance (mid-point)

18

Page 18Capital Structure and Maturity Towers

Term Loan B repricing in April 2018

($ in mm) 3/31/18 Maturity Rating

Cash & Cash Equivalents $ 32 - B2/B

saves $3mm annually

-------------------------------------------

Revolving Credit Facility - 10/2/2022 Ba3/BB-

Receivables Facility - 5/10/2021 AR Facility expanded to $250mm

Term Loan B 600 10/2/2024 Ba3/BB- and extended to May 2021

Capital Leases and Other Debt 80 Various

6.3% CBT Notes 88 12/1/2028 Ba2/BB-

7.25% CBI Senior Secured Notes 22 6/15/2023 Ba3/BB-

Senior Secured Debt $ 790

7% Senior Notes Due 2024 625 7/15/2024 B3/B- $600

8% Senior Notes Due 2025 350 10/15/2025 B3/B-

Total Debt $ 1,765

Weighted Average Cost of Debt 6.73%

$625

Cash shown net of restricted cash

$250 $200 $350

$22 $88

$ in mms

Bonds Term Loan B Revolving Debt

192018 Outlook

• Effective January 1, 2018, revenue guidance

Reaffirms 2018 Guidance reflects adoption of new revenue recognition

standard

Revenue $1,200mm – $1,275mm

• Infrastructure Solutions sales recognized

net of product cost

Adjusted EBITDA $320mm – $330mm

• For reference, had the revenue standard

not been effective– the revenue guidance

range would have been $1.7bn to

$1.775bn

Impact of New Revenue Standard

($ in mm) 2018 (Guidance) • Guidance does not include contribution from

the pending merger with Hawaiian Telcom

As previously presented $1,700 – $1,775

Impact of new revenue recognition ($500)

As currently presented $1,200 – $1,275

20

Page 20You can also read