BACK ON TRACK Economy & Real Estate Report - Holiday Home and Hospitality Markets - Algean Property

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

BACK ON TRACK

Economy & Real Estate Report

Holiday Home and Hospitality Markets

Greece 2017

Greek Economy

Overview

A 4.2% of GDP, General Government Primary Surplus

has been achieved, far exceeding the target of 0.5%

set for 2016

The performance of the Greek increase in taxation on consumption For H1 2017, all the major economic

Economy throughout 2016 and the rise in energy prices. indices maintained a positive course.

remained almost neutral, implying Primary surplus was 15.7% higher

the end of the country’s crisis. A 4.2% of GDP, General during the same period last year

2017 is expected to be a year Government Primary Surplus has (H1 2017: €1.936mil), exceeding

of solid growth. The delay in been achieved, far exceeding the target set by the 3rd MoU for this

finalizing the second assessment the target of 0.5% set for 2016. year (€431mil.). Unemployment rate

of the 3rd MoU was a hindrance to Moreover, for the first time further decreased to 21.2% (June

the growth of the Greek economy in recent years, the General 2017), maintaining its momentum

in 2016, mitigating the projected Government balance had a positive over the last three years. In this

level of growth for 2017. margin, marking a €1.3bil. surplus climate, the domestic banking sector

or 0.7% of GDP. Greece’s test exit returned to positive results, while the

In 2016, GDP recorded a - 0.2 % to the markets in July 2017 with restructuring of their NPL’s portfolio

growth. For 2017 and 2018, the the issuance of a 5-year bond was is expected to facilitate gradual

economy is expected to experience another step towards the end of normalization of business access to

positive growth rates of 2.1% and the crisis and the return to stability, bank lending, giving new impetus to

2.5% respectively. Following the managing to raise €3bil. with a the country’s real economy.

positive performance of the previous 4,375% coupon and an interest

years, unemployment rates further rate of 4,625%. The Greek Economy still has many

declined to 23.6% in 2016 from open issues to face in order for

24.5% in 2015 and 26.5% in Despite the unfavorable economic growth to accelerate

2014. The projections for 2017 and circumstances occurring both locally including the debt relief and the

2018 refer to a further decline to and internationally (BREXIT, ongoing lifting of capital controls. For that,

22.8% and 21.6% respectively. The refugee crisis and terrorist activity), it is imperative to maintain a stable

Consumer Prices Index reached 0.0% the Greek economy, driven mainly political and economic climate

in 2016 for the first time after 3 by the tourism performance, kept a so that the Greek Economy can

years of deflation, mainly due to the steady course throughout the year. maintain a strong growth.

2

Greek Economy

3

Greek Economy

Tourism

For Greek International Tourist Arrivals and Tourism Receipts

Tourism to

further grow

over the

coming years,

it is imperative

to continue

attracting

large scale

investments

Despite the difficult conditions held back as a result of: Travel & Tourism investments

prevailing in 2016, Greek Tourism • Increase in taxation reached €3.2bil. or 15.7% of

continued its upward course over • Ongoing refugee crisis total investments made in the

the last years. Having maintained • BREXIT country, including among many

its dynamics at a very high level, • Increase in last minute the privatization of the 14 regional

tourism gave a great boost to the bookings airports, the privatization of Astir

Greek economy, both in terms of • Shorter vacation period Palace etc. As the culmination

profitability and employment. of these efforts, Greece reached

Preliminary data for H12017 are the 24th position in the Travel

For five years in a row, arrivals more encouraging; International & Tourism Competitive Index,

recorded a positive growth arrivals showed a +6.6% increase published by the World Economic

rate (+ 4.8%), reaching 24.8 compared to the respective period Forum for 2016, seven positions

million visitors, excluding cruise last year while tourist receipts ahead compared to 2015.

passengers, while expectations bounced back strongly, recording

for 2017 speak of further growth. a 7.1% increase, paving the way For Greek Tourism to continue

Tourism receipts on the other hand for a new record year for tourism growing over the coming years, it

indicated a slowdown (-6.8%), in Greece. is imperative to continue attracting

reaching €12.8bil. Greek large scale investments. A €3.5bil

tourism’s main markets for 2016 In recent years, Greece has been investment per year is necessary

were Germany, UK, France, USA consistently investing in tourism, for the industry to be able to take a

and Italy, accounting for 39.4% exploiting its strategic advantages step further.

of total arrivals, 47.8% of total in order to further improve its

overnight stays and 50.3% of total attractiveness for foreign travellers.

tourist receipts. More specifically, for 2016 and

according to WTTC (World Travel

Tourism revenues in 2016 were & Tourism Council), Greece

4

Greek Real Estate Market

Building Activity

Building activity showed signs cumulatively since 2007, there and the high number of construction

of decline for another year, has been a decrease of 84.1%. projects announced to begin in the

confirming the sector’s struggle The stabilization of the number of upcoming years, are expected to

since the beginning of the financial issued building permits per year boost the country’s building activity,

crisis in Greece in 2008. More close to 13,000 in the last three giving life to an industry which was

specifically, in 2016 12,641 years (2014: 13,434, 2015: once characterized as the “steam

building permits were issued, the 13,350, 2016: 12,641) is showing engine” of the Greek economy.

lowest number achieved over the that the sector has reached the Provisional data for H12017

last ten years. Compared to 2015 bottom and a grow period is already show a 13.1% increase

(13,350 permits issued), building expected. The settlement of the in issued permits compared to the

activity declined by 5.3%, while Banks’ non-performing loans (NPL’s) respective period in 2016.

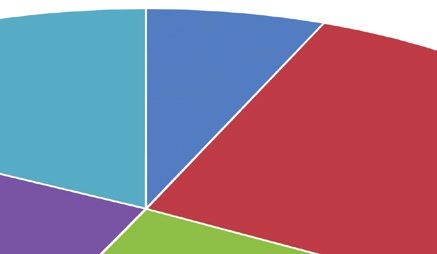

Market Watch

The real estate industry showed was also observed in the logistics Average Prime

signs of stabilization during sector, with return ranging between Yields per Sector

2016, albeit with a low volume 10.5-11.5%. Nonetheless, the

of transactions. No significant overall activity recorded was very

developments in the office and low. The industry is expected to

retail sector took place due to move upwards in the future, mainly

diminished demand and low due to COSCO’s intense activity

liquidity as a result of the limited at the Piraeus port and to the

access to bank lending. Also, in construction of the Logistics Center

an effort to reduce operational in Thriassio Pedio by the Goldair-

costs, many companies tried to ETVA consortium.

renegotiate their existing rents

or searched for a new space by For H1 2017, the commercial

achieving a combination of size, and the office sector maintained

location and inveteracy which, in a steady course without recording

return, increased the supply stock any significant changes. The the domestic real estate market.

in old age commercial spaces logistics sector confirmed its The ability to record transactions

(retail, office). increased dynamics and growth as will help normalize market prices,

there was a strong demand from improve the quality of service

Office space yield ranged between retail, e-commerce and 3PL’s. provided by professionals as well

8-9%, due to the limited supply of as allow private and institutional

class-A office spaces. In the retail The real estate sector in Greece investors to keep track of the

sector, yield ranged between 7-8%, still faces many structural problems market and identify opportunities

with an increase being recorded including increased bureaucracy, where they can be found.

in high commercial streets and multiplicity of laws and lack of

shopping malls. The market is transparency. The Property Transfer

expected to grow further as a Registry, recently launched by

result of large commercial chains the Ministry of Finance, consists

entering the Greek market. Stability in a very important progress for

5

Greek Real Estate Market

Domestic Residential Market

Key markets of Attica Basin displayed remarkable

stability during this difficult economic climate

The residential property sector onwards. In addition, a very debilitating position in which the

continued its downward trend important step toward further industry has been put in during

in 2016, with property prices improvement is the equation of tax these years.

recording an overall fall of 2.1%, assessed values with commercial

marking the eighth consecutive year values. However, this measure is Nevertheless, key markets of Attica

of recession in the sector, with little not expected to be implemented Basin, such as the Northern and

auspicious prospect of growth. A before 1/1/2018, although it Southern suburbs, as well as the

further decline was recorded in was a prerequisite for the second historic center of Athens (Plaka,

Q22017 (-1.2%) which is expected evaluation of the 3rd MoU. Kolonaki) maintained their prices

to continue for the rest of the year. in 2016 demostrating remarkable

The two major urban centres of The housing market in Greece stability during this difficult

the country, Athens & Thessaloniki, became a ‘buyers’ market over economic climate, while some

suffered the most during the crisis the crisis years, with increased individual markets even recorded

years, where, the overall decline in tax on real estate coupled with a small increase in demand. More

prices exceeded 40%. the downfall in household income specifically, the southern suburbs

and the rising unemployment rate, attracted many buyers from the

Nevertheless, the price correction leading to many homeowners Middle East, Israel and especially

over the past two years is incentivized to put their property Turkey, where, due to the political

declining, indicating a stabilization for sale, increasing real estate turmoil which prevailed in the

of the housing market, which, stock, the majority of which being country, saw in Athens as closest

coupled with the forthcoming old constructions. At the same time, and safest destination in securing

regulation of the banks’ red loans the number of transactions declined and diversifying their capital. The

(NPL’s), leaves a small margin significantly, recording a 72% fall ‘Golden Visa’ scheme is expected to

of expected growth from 2018 since 2008 and demonstrating the further assist the market’s recovery.

Greek Residential Prices Rate

Source: Bank of Greece

6

Holiday Home Market

Overview

The holiday home market is expected to continue

growing rapidly over the coming years

The Greek holiday home market The holiday home market grew With the positive momentum

remains the most dynamic part of greatly in recent years. 2016 was created by the stable economy and

the domestic real estate market a milestone year for the Greek the ever-increasing dynamics of

in the years of the crisis and one holiday home market as the signs tourism, the holiday home market

of the most promising sectors of of recovery were clearly positive, is expected to continue growing

the Greek economy along with both in terms of transaction as well rapidly over the coming years.

Tourism. as of new development.

Supply

Holiday home capacity in Greece terms of asking prices and quality of include the construction of holiday

remained almost unchanged in construction. homes within their premises,

recent years due to limited building increasing and renewing the

activity as well as the small number The majority of holiday homes existing stock in tourist resorts with

of transactions. in Greece are private houses, over 3,000 properties over the next

as holiday homes in residential 5 years.

The Greek holiday home remains complexes have only recently

faithful to the style and form found developed in the last few years. Already, luxury hotel resorts

in each region, without sparing However, due to the development provide the option of buying a

any comforts and amenities, while boom of tourism in recent years, holiday home within their premises,

remaining competitive with holiday a great number of complex tourist contributing to the improvement of

homes in neighboring areas in resort projects in the pipeline, will holiday home stock.

Demand

The dynamics of the holiday home Due to the tension prevailing in golden visa and a clear preference

market in Greece remained high in the Middle East, buyers from these for Athens; out of a total of 2,014

2016 with tourism being a decisive countries saw the opportunity of residence permits issued by the end

factor in maintain a positive further diversifying their investment of September 2017, 850 regarded

momentum. portfolio by taking advantage Chinese nationals. Estimates show

of the high returns offered in that, since the beginning of the

Apart from markets that Greece the Greek holiday home sector, ‘Golden Visa’ scheme in mid-2013,

traditionally attracts (UK, showing particular interest for the a total of €1.1bil. has been invested

Italy, France, Germany, and Athenian Riviera as well as for high in the Greek real estate sector.

Scandinavia) whose preference lies end tourist destinations.

mostly in the Cyclades, the Ionian

Sea and Crete, a keen interest was The interest from the Chinese

recently recorded by investors from market remained high, with buyers

the Middle East and Turkey. primarily interested in obtaining the

7

Holiday Home Market

Prices - Transactions

destinations in the Mediterranean Greece, net capital inflows from

The positive (Nice: 4.2%, Ibiza: 3.8%,), while abroad for the real estate market

other regions in Greece also had in Greece for H12017 show an

impact of good performance with an average increase of 63.4% compared to the

of 4.5% respective period in 2016.

tourism

performance in The positive market climate

was eloquently represented by

Despite the overall positive climate

in the holiday home sector, however,

certain areas inflows of foreign capital for the

purchase of real estate going

the total number of purchases is still

much lower than in the pre-crisis

favored in many up 45.3% (€270mil.) compared

to 2015 (€186mil.). In fact, the

years and the real potential of the

market. The most popular Greek

cases the local actual amount is estimated to be

even higher as a large number of

destinations such as Mykonos,

Santorini, Paros and Corfu recorded

holiday home transactions were made outside

the Greek banking system. The

an upward trend, which is expected

to continue in 2017.

market signs for 2017 are more than

encouraging as, according to the

latest figures from the Bank of

Holiday home prices remained

almost stable in 2016. The positive

impact of tourism performance in

certain areas favored the local

holiday home market.

In 2016 holiday home yields in

Greece increased for a second

year in a row, a trend which

continued into 2017. More

specifically, according to Algean

Property’s latest report “Yields

Report 2017: High End Holiday

Homes in the Mediterranean“,

yields in popular destinations

such as Mykonos recorded 8.4%

while Santorini and Paros reached

6.4%, being far above competitive

Outlook

The positive performance of tourism for property purchases in Greece political stability the last two years,

and its ever-increasing prospects increased significantly, while a further increase in the number of

have had an auspicious impact on preliminary data show a further transaction and building activity is

the holiday home market. increase being recorded for 2017. expected in the coming years.

In 2016, investment climate shifted, Greatly assisted by the economy’s

as the amount of foreign capital positive performance and the

8

Hospitality Market

Overview

The outperformance of tourism was a decisive factor for

the industry’s further development, attracting the interest

of investors and hotel management companies

In 2016 the hospitality sector kept management companies. 2016 which, along with the

a steady upwards pace recording ongoing developments that began

positive numbers in occupancy, The continued growth of Greek over the last few years, paved the

revenues and quality of services tourism as well as the ever- way for a new era of growth for

provided. increasing rate of international the hospitality sector in Greece.

arrivals in the country led to overall

The outperformance of tourism was improvements within the industry.

a decisive factor for the industry’s

further development, attracting A series of new developments

the interest of investors and hotel and acquisitions took place within

Supply

In 2016, according to the latest

data from Greek Hotel Chamber, the Allocation of Hotel Beds per Category in Greece

hotel capacity in Greece amounted

to 9,730 hotel units, with 407,146

rooms and 788,553 beds.

The biggest increase was recorded

in the upper category hotel units,

hence the increase in the number +6.2%

of total rooms and beds. More y-o-y

specifically, in the 5-star category,

there was a +6.2% growth or 8,538

beds in only one year.

Despite the increase in new 5-star

and 4-star units in recent years

(+ 5.6% and 5.1%, respectively

only for 2016), there is still space

for further development, since only The ever increasing number of upgrading of the country’s hotel

4.6% of the country’s hotel capacity foreign visitors each year as well capacity imperative.

or 17.4% of the beds’ capacity is as the growing need for high-end

listed in the upper class category. services, makes the need for further

9

Hospitality Market

Perspectives – Key Performance

The hospitality sector recorded

Hotel Units: Key Performance Indicators, 2016

positive growth in all key

performance indicators in 2016.

The average occupancy rate

ranged between 55%-65% on

an annual basis while seasonal

numbers reached over 70%.

Average daily rate (ADR) ranged

between €90-€180. Revenues

per available room (ReVPAR)

amounted to €50-€160, recording

a significant increase compared

to last year, especially in resorts

(+9.6% ytd). Total income

averaged close to €20,000 per

available room. The visitors’

satisfaction index (GRI Index) Greece: Hospitality Sector – Performance

increased to 85.4%, higher than

its immediate competitors in the Annually Occupancy Rate 55% - 65%

Mediterranean (82.6%), and

confirming the country’s aptitude Average Duration of Stay 6.7 days

for quality in services.

Expenditure per Overnight Stay € 67

Seasonality was the main setback

for Greek tourism. Improvement

Average Daily Rate (ADR) € 90 - € 180

was evident, especially in Q4

2016, international arrivals

Revenue per Available Room (RevPAR) € 50 - € 160

recording significant growth

(Dodecanese +26.7%, Crete

+33.3%, Ionian Islands +38.7%, Total Income per Available Room up to € 20,000

Cyclades +43.8% and Kalamata

+46.0). Preliminary results for EBITDA Multiplier 10x - 15x

2017 show further improvement

compared to last year. However, GRI Visitor Satisfaction Index 85.4%

we still have a long way to go.

In an effort to further stimulate the Beach, Religious, Cultural, City parties in the hospitality sector is

market, the Ministry of Tourism Break, Sports, Medical, MICE). essential for this road map to have

presented a strategic plan for the However, a concerted effort and immediate and tangible results.

development of individual tourism systematic promotion of alternative

categories (Thematic Sun and forms of tourism from all concerned

10Hospitality Market

Transactions - Investments

In 2016 there was intense activity in Koutras for €30mil. and the purchase overnight stay fee varying

terms of new hotel unit developments of Athena Ledra Hotel from Hines for from €0.5 to €4/overnight

and acquisition of existing ones. €33mil. Furthermore, Dolphin Capital stay depending on the hotel

Investors announced their agreement category, thus increasing their

The hospitality sector is one of the with Kenzer International Holdings operating costs.

most dynamic investment sectors in Limited to build the 5 star hotel

Greece, offering very high returns. complex “One & Only Kea Island“ in Moreover, the high borrowing of

Athens offers one of the highest hotel Kea. The total cost of the investment hotel businesses is a drawback

yields in Europe (8.0%) compared is estimated at €150mil. to potential acquisition. More

to major European capitals such as specifically, out of €7.6bil, the total

London (5.5%), Paris (5.5%), Rome Despite the strong activity, the lending of the tourist enterprises,

(6.25%) and Madrid (6.25%). obstacles future investors are facing €2bil. are non-performing

remain significant. exposures (NPEs).

During 2016, a number of

acquisitions, relaunching and More specifically: A special purpose vehicle was

redevelopments were carried out • In 2015, VAT on accommodation created by Grivalia REIT (Grivalia

upgrading the hospitality sector in services increased by 100%, Hospitality) aiming to invest in

Greece. The positive course in the reaching 13% from 6.5%, the domestic and international

hotel industry continued in 2017 • VAT in the wider hospitality hospitality industry. The company

with a large number of acquisitions sector increased from 13% to has signed a binding pre-agreement

and management takeovers taking 23% and then to 24%. to acquire 80% of Nafsika S.A., to

place. The cases that stood out in • High corporate taxation (29%) commercially exploit “Asteria“ Resort

the first half of 2017 concerned the • From 1/1/2018, all hotel in Glyfada in the Athenian Riviera,

purchase of Capsis Rhodes by Nikos units will be charged with an which was in operation until 1990.

2016 Milestones

Project Seller Investor Type of Investment Amount

National Bank of Greece Jermyn Street Real

Astir Vouliagmenis Acquisition € 444 mil.

(NBG) & HRADF (TAIPED) Estate Fund IV LP

Miraggio Thermal Spa Resort - Med Sea Health S.A. Hospitality Development € 120 mil.

Corfu Chandris & Ikos Resorts &

Chandris Group SANI Group Acquisition € 110 mil.

Dassia Chandris

Plot in Kassiopi, Corfu HRADF (TAIPED) NCH Capital Acquisition € 100 mil.

Leto Hotel, Mykonos HRADF (TAIPED) Douzoglou Group Acquisition € 17 mil.

Imperial Athens Hotel Grecotel Wyndham Group Hotel Management -

Dogus Group -

Hilton Athens Alpha Bank Acquisition € 142 mil.

TEMES S.A.

Outlook

The significant progress of the of the sector’s growth, creating new developments took place.

hospitality sector during 2016 positive expectations for its further Furthermore, many more projects

was the result of the exceptional development. are in the pipeline in the coming

course of Greek tourism in recent years, certifying the investor’s trust

years. Its positive growth in key Despite the challenging economic in the ever increasing prospects of

performance indices throughout environment in 2016, a great Greek tourism.

the year came as a confirmation number of acquisitions and

11Market Snapshot

Economy

Macroeconomic Data

Economic Indicators 2009 2010 2011 2012 2013 2014 2015 2016 2017f 2018f

Population (mil.) 11.2 11.2 11.1 11.0 11.0 10.9 10.8 10.7 10.7 10.7

GDP Growth (%) (3.1) (4.9) (7.1) (7.0) (3.9) 0.7 (0.2) (0.2) 2.1 2.5

Inflation (%) 1.3 4.7 3.3 1.5 (0.9) (1.4) (1.3) 0.0 1.2 1.1

Unemployment Rate (%) 9.6 12.7 17.9 24.4 27.5 26.5 24.5 23.6 22.8 21.6

FDI (net inflows in mil. €) 1,753.8 249.2 822.3 1,354.3 2,122.1 2,022.5 1,143.0 2,819.5

Spreads (10 year bond) 238.7 950.9 3,313.4 1,058.4 649.0 906.0 771.0 710.0 514.0*

Athens Stock Exchange 2,196.2 1,413.9 680.4 907.9 1,162.7 826.2 631.4 643.6 744.0*

Sources: Eurostat, European Commission, IMF, OECD, Bank of Greece, Alpha Bank

*Reference Date: 27/10/17

Real Estate

Market Trends

Price Demand Supply

Residential Market ↘ → →

Holiday Home Market → ↗ ↗

Hospitality Market → ↗ ↗

12Our Latest Reports

Yields Report 2017:

High End Holiday Homes in the Mediterranean

FLASH REAL ESTATE REPORT 2016

To uris m Trends , Ho liday Ho me

& Ho s pitality Markets

1

George Eliades Konstantinos Sideris

Managing Partner of Algean Group Senior Analyst

Skype: george.elias.eliades Skype: ksideris.algeanproperty

george.eliades@algeangroup.com konstantinos.sideris@algeanproperty.com

Fani Dritsa Giannikos Giannakos

Senior Property Advisor Property Advisor

Skype: fdritsa.algeanproperty Skype: ggiannakos.algeanproperty

fani.dritsa@algeanproperty.com giannikos.giannakos@algeanproperty.com

Athens London

78,Kifisias Avenue, Marousi 19,Portland Place

15125, Athens, Greece W1B1PX, London, UK

T : +30 210 6833 304 T : +44 (0)20 3608 6917

www.algeanproperty.com welcome@algeanproperty.com

Sources: Bank of Greece, European Commission, International Monetary Fund (IMF), Eurostat, Hellenic Statistical Authority (ELSTAT),

OECD, Association of Greek Tourism Enterprises (SETE), Hellenic Chamber of Hotels, Foundation for Economic & Industrial Research

(IOBE), Global Review, Ministry of Finance, Ministry of Economy, Development and Tourism, Hellenic Republic Asset Development Fund,

CBRE, GBR, HotelCompset Database and Algean Property Research.

This report has been produced by Algean Property for general information purposes only and nothing contained in the material constitutes a

recommendation for the purchase or sale of any property, any project or investments related thereto. Information on this report is not intended

to provide investment, financial, legal, accounting, medical or tax advice and should not be relied upon in that regard. The intention of this

report is not a complete description of the markets or developments to which it refers. Although the report uses information obtained from

sources that Algean Property considers reliable, Algean Property does not guarantee their accuracy and any such information may be incom-

plete or condensed and Algean Property is under no obligation to issue a correction or clarification should this be the case. Any information

of special interest should be obtained through independent verification. Views are subject to change without notice on the basis of additional

or new research, new facts or developments. All expressions of opinion herein are subject to change without notice. Algean Property accepts

no responsibility or liability for any loss or damage resultant from any use of, reliance on or reference to the contents of this document. The

prior written consent of Algean Property is required before this report can be reproduced/ distributed or otherwise referred to in whole or in

part. Algean Property, All Rights Reserved.You can also read