ARGENTINA UNSHACKLED - INVESTORINTEL

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Argentina Unshackled Observers from outside Argentina have gone on a frenzied romp of self-congratulation hailing the change in the Argentine Presidency in last week’s elections as something akin to a Revolution. Once again though we find that simplistic formulas are being used and the nuances of what has happened being ignored. The situation still has the potential to be a wild ride for investors.

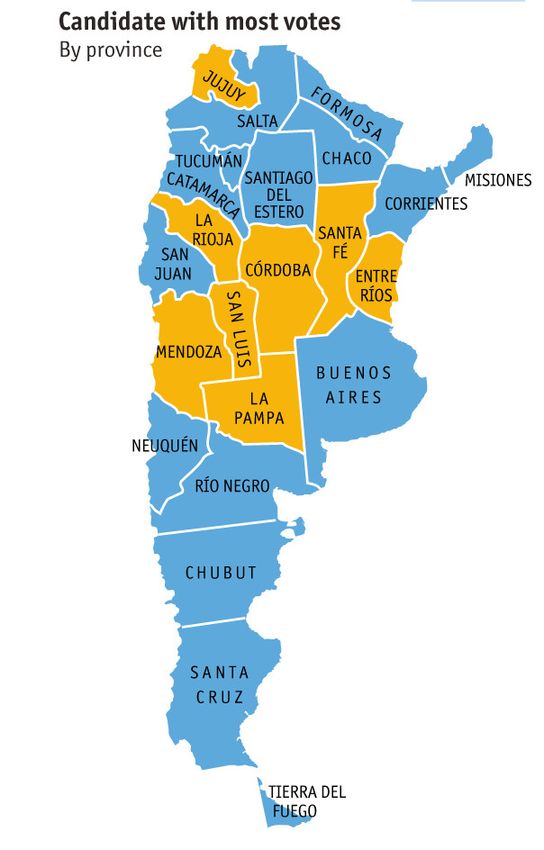

For a start the victory of Mauricio Macri is being hailed as a “right-wing” victory. To put that in context, firstly he leads a Rainbow Coalition that stretches from the Left across to the Right and the party he beat, the Frente Para la Victoria, is in fact the old Peronist Party, which was a fascist/corporatist construct in its original roots. So to claim that a wealthy businessman (in fact I would venture one of the five wealthiest in the country) that leads a Coalition including the Left is a “Right-wing” victory is stretching it a bit. Secondly we would note that the victory was surprisingly narrow. While the first votes in showed a 9% lead for Macri, as the night wore on the margin slipped and it ended up being 51.4% for Macri and 48.6% for his Kirchnerite opponent, Daniel Scioli. It should also be noted that the first round of elections last month delivered stinging losses to the Kirchnerites but they just barely hung onto control of the Senate meaning that, if they stay cohesive, they still have potential to block reforms. That said, with their patroness gone, the rats tend to disperse into the woodwork to regroup. We may end up seeing the phenomenon apparent under the De La Rua government in the late 1990s of Bribes for Votes when a hostile majority in the Senate had to be paid off, literally. The New Lay of the Land As we have repeated endlessly mining is controlled in Argentina by the provinces, in much the same way as it is in Canada or Australia. The national government in Argentina has NO approval or denial power over mining projects. So everything you have heard of “Cristina Kirchner blocked our project” is a load of codswallop. In all cases blockages occurred because of ornery provincial governments. It is interesting therefore to look at the map of the electoral results. The blue areas are provinces that voted for the Kirchnerite candidate. The yellow are those that voted for

the winning Macri-led ticket. Oops, for those who know the only province with mining of note (Silver Standrad’s Pirquitas mine) that voted for Macri was Jujuy. La Rioja has been an on- again, off-again mining favorable area and La Pampa and Mendoza have been graveyards for miners.

The provinces where mining is currently active are Catamarca,

Santa Cruz (the Kirchnerite province par excellence now run by the outgoing president’s daughter), Salta and San Juan. If there is anything to be read from this map it is that the marginalized distant provinces with the smallest populations (excepting Buenos Aires which was only won marginally by Scioli and that was because of the sprawling urban slums voting for him) supported the Kirchnerite program which gave them a greater share of the goodies. The provinces that trended for Macri where those with the largest populations (and strong agricultural export economies) that were actively persecuted and discriminated against for the last 12 years. Implications for Mining Having said that mine approvals are in provincial hands, some matters are still in the Federal purview. Amongst these that have relevance are foreign exchange allocations. Miners have been griping for years now that they could not bring in the capex items they wanted in an unrestricted way due to import restrictions and could not remit profits or dividends as and when they wished. These restrictions were part of the increasingly draconian and bizarre forex rules that the Kirchnerite regime was imposing as Argentines tried to head for the exits and buy dollars to protect themselves against the rapidly deflating peso. Moreover to say the forex regime was complex was an understatement. Here is the table of exchange rates for today for a leading Buenos Aires newspaper, La Nacion: So on the left we have the official rate, on the far right is

the so-called Dolar Blue which is the back-alley rate. In the

middle are various official rates administered by the Central

Bank for different purposes. Dolar Ahorro is a savings rate,

Dolar Tarjeta/Turista is the rate that locals can use credit

cards for (when travelling abroad) and that bona fide tourists

within the country can use to change money. The Dolar Soja is

the very prohibitive rate forced upon farmers selling their

crops (effectively a 30% tax on the official rate and a 150%

tax on the unofficial rate). Finally the Dolar Bolsa is a

conversion rate for transactions in the Stock Exchange.

Byzantine is obviously not too strong a word to describe this

bizarre system. Miners will be hoping that this system loosens

up, though the new government will be wary of letting this go

too soon or there will be a dollar buying spree that will

decimate Central Bank reserves. One suspects that Dolar

Turista and Dolar Soja will be the first to go. The government

will then aim to draw the Dolar Blue and the official rate

together somewhere in the middle. Who knows? Maybe the

wonderful Convertibility regime of the 1990s might be

revived.. Certainly Argentina had never experienced such good

times since the 1920s as under that arrangement.

Despite the mining provinces largely being of the Kirchnerite

ilk, they are the provinces that have shown themselves to be

most pro-mining. With less subsidies coming from the Federal

government more of the provinces will have to look to mining

to keep their local economies buoyant.

If one wants to muse with some names in Argentine mining those

to consider are:

Patagonia Gold Plc (AIM: PGD)

Hochschild Mining (LON: HOC)

McEwen Mining Inc. (NYSE: MUX | TSX: MUX)

U3O8 Corp. (TSX: UWE | OTCQX: UWEFF)

Pan American Silver Corp. (NASDAQ: PAAS | TSX: PAA)

Silver Standard Resources Inc. (TSE: SSO)Yamana Gold Inc. (TSX: YRI | NYSE: AUY)

Argentex Mining Corporation (TSXV: ATX | OTCQB: AGXMF)

Orocobre Limited (ASX: ORE | TSX: ORL)

Western Lithium USA Corporation (TSX: WLC | OTCQX:

WLCDF)

Galaxy Resources Limited (ASX: GXY)

One might also see those who have downplayed their Argentine

prospects dusting them off or racing back to restake them.

What Next

After exchange rates there are a vast swathes of regulations

constraining all aspects of economic life that could be cast

into the dustbin of history. Some of these measures being

rescinded should help miners. One that might not though is the

bizarre fuel subsidies. These were introduced after the

collapse of 2000/1 and the spike in inflation. To “protect the

poor” massive subsidies were introduced which have bled the

Treasury dry. They have been reduced and some have been made

to pay world parity prices for oil but many have not. This

could be the big budget winner but also a tough policy to bite

on first.

One could see a strong inflow of FDI though and this might

actually reverse the exchange rate so delays in freeing

remittances might actually work out better for miners when

they are eventually freed.

The whole construct of Kirchnerism was so bizarre and

distortive that untangling it is akin to unraveling the

Gordian Knot. Like Alexander the Great, sometimes it’s better

to just draw one’s sword and chop the knot in one fell swoop

than spend years testing one’s Boy Scout skills trying to

untie it..

Conclusion

After 12 years of Kirchnerite “policies” (more like populistbootstrapping) the Argentine economy is emerging from a long

dark tunnel into the glare of daylight. Frankly it’s better

out of the tunnel rather than being in it and foreign miners

for better or worse face a brave new world. We can say with

confidence that the rules will NOT be more onerous and the

forex regime WILL be more flexible. Growth should kick up and

frankly Argentina looks like a better bet than the deeply

troubled Brazil these days.

As a New Yorker would say “What’s not to like?”

When the going gets tough,

the technology metals get

going

Oil prices are going

to stay low until

2020, warns the

International Energy

Agency this week. The

base metals are in a

swoon. Wheat, corn

and oilseed prices

are seeing sharp

price drops. And the

U.S. Federal Reserve

is limbering up to

raise interest rates,

with no one quite

sure what the global

economic impact willbe. So, while most of the commodity sector struggles and suffers, there are still strong signs of life in the technology metals sector. First, Lithium Australia (ASX:LIT) is expanding when many other exploration companies are counting their money and calculating how long they can survive. It already has alliances with European Metals (ASX:EMH) with its Cinovec tin and lithium deposit in the Czech Republic, Pilbara Minerals (ASX:PLS), the owner of the Pilgangoora lithium and tantalum project in Western Australia, along with with two other West Australian operations, Focus Minerals (ASX:FML) with targets near the mining centre of Coolgardie and Tungsten Mining (ASX:TGN). Lithium Australia has carved a distinctive niche for itself, targeting the lithium micas which it regards as the forgotten lithium resource. Now it has its eyes on Mexico and a new under-rated source of lithium. Lithium Australia has teamed up with Alix Resources Corp (TSX.V:AIX) to advance the latter’s lithium concessions covering 22,625 hectares in Sonora, a state abutting the U.S. border. There has been a meeting of minds: both companies believe that a combination of low-grade material and the application of energy intensive processing systems have historically hindered lithium clay deposits from being commercialized. The Australians plan to bring to the Mexican project their low-energy technology to extract lithium from micas. It is thought that some of the materials previously tested by the Australian company may have similar mineral chemistry to what is found at the Sonora project, For Lithium Australia, this is clearly not just another deposit. It is a foothold in North America, which it sees as the future lithium business powerhouse, Gigafactory and all. The project adjoins the big Sonora lithium project operated by Bacanora Minerals (TSX.V:BCN), which has caught the attention

of Tesla. Aggressive expansion is not an option for too many exploration companies. But the key here is that Lithium Australia is just not another exploration company. It has developed its own technology, and that separates it from the herd. As it does for Neometals (ASX:NMT) which has announced that it and Mineral Resources (ASX:MIN) have begun a definitive feasibility study on their Eli process, to produce 20,000 tonnes a year of battery-grade lithium hydroxide directly from lithium oxide concentrates. NMT points out that this development coincides with the announcement by one of the world’s leading lithium producers that it has hiked its lithium compounds prices by 15%, thanks to the demand from renewable energy storage end electric/hybrid vehicle manufacture. And Peak Resources (ASX:PEK) is pressing on with its bankable feasibility study on its Ngualla rare earth project in Tanzania. Last month it completed important field drilling programs needed to underpin the BFS, with two additional areas firmed up as containing high grade mineralization. Managing director Darren Townsend sees it as another milestone establishing Ngualla as a low cost, long term supplier of magnet metals. All three of these developments out in the past few days confirm one thing: that quality technology metals projects can survive what is a challenging commodities environment.

Africa the key to feeding the world (and itself) A critical meeting is now underway at Dakar, Senegal. It is about food, but it is also about much more than that: it is about fertilizer (potash and phosphate) and about the stability of two continents, Africa and Europe. It is the African Development Bank’s (AfDB) conference on food for Africa, held Wednesday through Friday this week. As the bank puts it, Africa has 65% of all the arable land left in the world and, by 2050, that land will be vital to meeting the food needs of nine billion people living on the planet by that year. Yet, Africa imports $35 billion worth of food annually. Africa’s food needs are set to double by 2050. How can Africa feed itself and the world? Sub-Saharan Africa has the highest prevalence of under-nourishment in the world. One in every four people in Sub-Saharan Africa is under-nourished with 39% of children being malnourished. According to one study, Uganda alone spends around $254 million year treating cases of diarrhoea, anaemia and respiratory infections linked to malnutrition. But the AfDB president, Nigeria’s Akinwumi Adesina, sheets home the food issue as one of the causes of a problem that is headline news in Europe right now. “Migration out of rural areas is rising rapidly, and thousands of young people now jump on boats to the Mediterranean looking for new opportunities in Europe,” he says. “That is why we make the claim that we can diminish the migrant crisis in Europe by supporting agricultural transformation in Africa.” Alliance for a Green Revolution, based in Nairobi, Kenya, has recently warned that Africa will not alleviate its chronic

food shortages unless more youth get involved in farming. Yet a survey in Ethiopia found only 9% of youth there planned to work in agriculture. By 2050 the world will probably not be in a position to supply food to Africa; everyone will need to feed their own, ever growing populations. The AfDB notes that by 2030 (only 15 years away, folks) the value of the food and agribusiness market is estimated to reach $1 trillion. Rather than importing food, Africa will need to be a net exporter within decades if there is going to be enough food to go around. This is an enormous task, and opportunity (for the fertilizer feedstock miners particularly). In early 2014 I reported on InvestorIntel that sub-Saharan Africa consumes only about 750,000 tonnes a year of potash. But it could easily absorb 6 million tonnes if the money was there to pay for it and the infrastructure to get it to the farmers. Over the past 50 years, cereal productivity for Sub-Saharan Africa has stagnated at 1 tonne a hectare compared to 4 tonnes a hectare in developed countries. Average fertilizer use in Africa is 8kg/hectare compared with the global average of 107kg/ha. We have been disappointed many times before by promises made by and for Africa, only to see hopes dashed in the longer term. But Akinwumi Adesina puts his finger on the key point: how will Africa turn agriculture from a sector that now manages poverry to one that creates wealth. “How will we move away from exporting primary commodities to the point where we sell processed cocoa not cocoa beans, processed coffee not coffee beans, and textile instead of cotton?” he adds. Good question. *******

The problem is that African farmers have usually been on the wrong end of any deal, with decades of possible progress squandered in the colonial era. My recently published book, Fighting on Empty: How Hitler and Hirohito Lost the Economic War, contains details of one shameful fact about how Britain treated farmers in its African colonies during the Second World War who faced a loss of their European markets as Germany invaded those markets, and reduction in exports to Britain due to shortages of merchant ships. It is an episode that should be better known: The colonies which relied on agricultural products were faced with sudden contractions in the market for their produce; coffee growers in east Africa suffered, as did copra producers in the Pacific islands, banana growers in Jamaica and cocoa and palm oil plantation operators in West Africa. London made a good deal of the fact that it bought the whole cocoa crop of 1940 in the Gold Coast (now Ghana) and Nigeria at prices higher than had obtained in 1939, but this was small comfort to the growers as their receipts were still lower than they had been in 1931 before the worst of the Great Depression was felt. In fact, Britain did not buy the entire output of cocoa: the mid-crop had no taker and was destroyed, and then in 1941 London sliced twenty per cent off what it paid for that year’s crop at the same time as raising the price of the cocoa to wholesalers within Britain by £10 per ton, the extra margin accruing to the government. When it came to palm oil, Britain did not need the entire output from Sierra Leone and Nigeria. Those farmers in Nigeria who grew oil palms as part of a diversified operation (and therefore did not rely solely on this crop) were told their output would not be needed, so they should switch to other crops (cassava was one suggested, as Britain needed 10,000 tons of that). The Economist estimated that palm oil growers who could not sell their palm oil lost, in total, about half a million pounds. As for cocoa crops, African officials had

recommended to London that some extra payment be made to

compensate for the fact that growers no longer had an open

market. This fell on deaf ears at the Colonial Office, the

price being set at £16 10s a ton when growers could not make a

viable living at much less than £25. The London response was

that, with Germany’s market closed off and American demand

declining, the growers had no option other than to take what

London was offering.

The Impact of the Liberal

Majority on Canada’s

Marijuana Industry

We’ve previously looked at

the possible impact of

various electoral outcomes

on Canada’s cannabis

industry. On Oct 19 the

Liberal Party cruised home

to a majority of seats in

the House of Commons, meaning their agenda will be implemented

with little real opposition over the next four years.

The Liberal Position on marijuana is very clear: “If we pass

smart laws that tax and strictly regulate marijuana, we can

better protect our kids, while preventing millions of dollars

from going into the pockets of criminal organizations and

street gangs.”

Watch for legislation to be introduced that amends the

Criminal Code and the Controlled Drugs and Substances Act to

allow for decriminalization and licencing, much like alcoholand tobacco. On the medical side, expect further licences to be granted to MMPR applicants, and expect the range of medical products to be expanded (see our analysis on the Smith decision from the Supreme Court of Canada.) This will generate additional tax revenue to the feds and the provinces (see our prior tax analysis here). Full-time jobs will be created. There will also be less government money spent on street level policing for marijuana, and a clearing of the backlog in the criminal justice system. Financially, all of that is good for Canadians and the dollar. On a more micro basis, there is less risk associated today with the marijuana stocks so expect them to rally. Share prices will fluctuate in accordance with the usual factors but over the long run the market is in a far better position than it would have been under the Conservatives. The next two drivers of value in the cannabis industry will be the Allard decision from the Federal Court of Appeal (our historic analysis is here, and remains accurate) and the exact terms of the legislation to be introduced by the Liberals when Parliament is formed. The grey market in MMPR applicants continues to grow with valuations decreasing as more capital is consumed pending the application process being completed. We are at the end of Marijuana Prohibition. The Allard decision will go a long way to determining who the winners will be, but the Liberal majority ensures that there will be winners.

Aurora Cannabis’ Terry Booth on the impact of the Allard decision and the election on the Marihuana Industry September 22, 2015 — In a special InvestorIntel interview, Publisher Tracy Weslosky, speaks with Terry Booth, President, CEO and Director of Aurora Cannabis Inc. (CSE: ACB | OTCQB: ACBFF) on the two new Board members and securing the former executive director of the CMCIA for the Aurora management team. They also discuss how Aurora is positioned as rising leaders in the marihuana sector and what the Allard decision and elections will mean to the overall industry. Tracy Weslosky: Terry I noticed you had a big corporate update, but I also noticed that you keep attracting some of the leaders in the industry, a new brand manager, a couple of new board members. Can you tell us just a little bit more about this? Terry Booth: Adam Szweras joins us, Chuck Rifici, ex-CEO of Tweed and Neil Belot, he was an executive director of the CMCIA, association of LPs in Canada. Quite happy with the team we’re assembling. Tracy Weslosky: Well, I think there’s a lot of other companies looking at you because you seem to be attracting all the best and brightest. Could that be your personality or does it have to do with the actual story, which I’m assuming it does? Terry Booth: I’d like to say it’s the personality, but it’s not. It’s the team we’ve assembled, it’s the facility that we’ve built and I think it’s the corporate vision that we have.

Tracy Weslosky: And, of course, all of you out there who may not be familiar with Aurora Cannabis, can you just step back and give us an overview as you were one of the first facilities in Canada? Terry Booth: Yes. We’re one of 26, I believe, licensed producers in the country out of 1,400 applicants. The facility itself is over 55,000 square feet. It’s in a very tax friendly jurisdiction in Alberta. We’re the very first facility in Canada built brand new from the ground up. We’re ready to roll. We’ve got a license to produce. We’ve pulled over seven harvests in to our vault and looking forward to the sales. Tracy Weslosky: It’s my understanding that you have some competitive advantages to this processing facility. Would you mind telling us what those are? Terry Booth: Sure. Well, building brand new, the flow of the facility itself is built for growing cannabis. There’s tax advantages in Alberta with its corporate tax rates. We hope that remains the same. We’re in a rural location in Alberta. We don’t pay for our water, its mountain fed. There’s farm tax credits in Alberta that a lot of provinces don’t have and our power rates are the second lowest in the country and the lowest in the country when we get our discounts for deregulation. Tracy Weslosky: Of course, there’s a lot happening in the marijuana sector in Canada right now. We have a major election and we also have the Allard decision. Can you give us some insight into both of these events? Terry Booth: On the election front both the opposing candidates have said they’ll either decriminalize or legalize it. Either way the existing government is who we’re answering to now. If it changes then it will only be good for us and we’re poised to take on any increase in market. With respect to the Allard decision…to access the rest of the interview,

click here

Disclaimer: Aurora Cannabis Inc. is an advertorial member of

InvestorIntel

Commodities cycle: Is the

worst of the pain behind us?

Call

it

“All

Quiet

on the

Commod

ities

Front”

.

Which is not a bad thing; as this is being written before the

Federal Reserve makes its decision on whether to lift interest

rates, this feeling of calm is probably a good thing. A lack

of volatility – one hopes – means that the Fed won’t scare the

commodity horses (in either direction).

And there’s even good news on the rare earth front with

Reuters reporting that China’s demand for these elements “is

likely to soar more than 50% over the next five years”. Chen

Zhanheng, vice-secretary general of the Association of China

Rare Earth Industry, told a conference in Shanghai this weekthat domestic consumption was expected to rise nearly 9% this year to 97,700 tonnes, and would end the decade at nearly 150,000 tonnes, up from 90,000 tonnes in 2014. If this is the case, it will certainly encourage non-China REE hopefuls to press on, holding out the hope that China might have to curb exports further to satisfy domestic manufacturing demand (and possibly even look to imports for heavy rare earths). On the broader front, the metals markets seems to be stabilizing; we have a few days without any sudden, heart- stopping movements. Is it over, then? (The downward plunge in the commodity cycle, I mean.) Well, Peter Strachan who runs the commodity analysis business StockAnalysis in Perth, Western Australia, says he thinks “the Australian resource sector is now either very close to its maximum point of pain or it is 85% of the way to that point.” The slight weakness in the U.S. dollar this week (at least against some currencies) has probably helped stabilize the metals ship of state. Prices may fall again, possibly across all the minerals, oil and soft commodities, but you get the feeling that it will be a gentle slide at worst. After all, they’ve all pretty well taken their licks, so Strachan might be right in saying the pain has reached its maximum point. The team at Capital Economics in London has compiled an overview. Their conclusion: “After the mid-Summer volatility in global financial markets, commodity indices have had a period of relative calm since mid-August”. The S&P energy index did worst among the commodity indices, while the industrial metals index actually rose 1% month on month. However, they point out that a number of commodities have seen a large decline in investor interest over the past month, highlighted by a 25% fall in the number of open-interest

contracts for palladium, and a 13% and 15% decline respectively for corn and wheat. What is most encouraging – and here I am reading between the lines of this report – is that the futures curves for industrial metals indicate some changes, but no great volatility. Copper, further out, looks like getting a little more colour in its cheeks, but zinc may be losing some ground in terms of investor expectations. On the soft commodities front, Capital reports that investors have sharply cut the number of short positions on sugar, and cocoa is also now net-long. Corn prices might be helped by forecasts that the next harvest total may not be so good. And a very interesting piece of news on the gold front: Randgold Resources is considering a spend of up to $1 billion to help AngloGold Ashanti revive its huge Obuasi mine in Ghana. It is estimated there are still 5 million ounces to be extracted. Randgold has not made a discovery since 2009 and has no new mines in development. Does that company see a gold squeeze ahead? It is getting harder and harder for the major producers to replace the ounces they are mining. And people still want to buy gold. (And when was the last time there was a gold surplus, with bars of metal lying around unsold? Answer: probably never.) Cancana Resources –

Production Trumps Inaction

When we have written about Manganese in the past it has been

in the context of steel alloys or of exotic new types of

batteries. The conversation has keep to these topics rather

than the alternative use as fertilizer because for Manganese

to be fertilizer grade it needs to be in excess of 48% Mn

grade. While Manganese mining does tend to focus on the high-

grade Direct Shipping Ore (DSO) material it is rare that it

reaches the grade that satisfies fertilizer demand. In fact of

all the major manganese mines in Brazil, only that of Cancana

Resources Corp. (TSXV: CNY) broaches the required level. I

thought that this merited highlighting so I have done a review

of the company’s activities and shall discuss these here.

Assets

Cancana Resources Corp. is focused on

exploring and developing the BMC

manganese project in the far western

state of Rondônia in Brazil. This

state borders Bolivia. The assets

consist of concessions that the

company accumulated itself and then

the plant and deposits of two other

producers that the BMC Joint Venture

(in which Cancana is partnered by a

leading resources hedge fund) bolted

on in 2014 to take the step up to

being a producer.

The Joint Venture holds a large land position extending to

nearly 37,000 hectares in very prospective terrain. In its

2015 NI43-101 report the consultants noted that very little

exploration had been performed to date and that Cancana needed

to initiate regional exploration programs aimed at identifying

manganese occurrences with follow up leading to resource andreserve calculations. That report was based upon exploration over an area of a mere 4.4 hectares, containing an inferred resource of 35,000 tonnes of mineralization with an average grade of 54% Mn. The geology of the area consists of Proterozoic aged granitic plutons underlying several high-grade manganese occurrences. The mineralization occurs as close-packed, rounded to angular clasts of Pyrolusite / Manganite within a saprolitic soil. The clasts range in size from sand particles to boulders greater than 1m on a side. Prior to Cancana’s arrival on the scene this type of mineralisation was already in production by Rio Madeira and Eletroligas, two companies operating in the area, of this more anon. Manganese (Mn) – the Known Unknown Fertiliser Manganese is a chemical element with symbol Mn and atomic number 25. It is not found as a free element in nature; it is often found in combination with iron, and in many minerals. Manganese is a metal with important industrial metal alloy uses, particularly in stainless steels. So while Manganese is primarily used in the production of steel, the high-grade and high-purity nature of the material produced at BMC qualifies as ‘agricultural-grade’ manganese and can be sold at a premium. Manganese is an important plant micronutrient and is required by plants in the second greatest quantity compared to iron. Manganese is a major contributor to various biological systems including photosynthesis, respiration, and nitrogen assimilation. Manganese is also involved in pollen germination, pollen tube growth, root cell elongation and resistance to root pathogens. Manganese deficiency in plants is evidenced by symptoms which often look like those of iron deficiency. Deficiency can occur from low fertilizer application rates, use of general purpose fertilizers (which typically have reduced micronutrient

contents), excessive leaching or applying too many iron chelate drenches. Manganese is the world’s twelfth most prevalent mineral and is mined in South Africa, Australia, China, Brazil, Gabon, Ukraine, India and Ghana and Kazakhstan. It is the fourth most traded metal with annual production (in 2011) amounting to an estimated 14 million tonnes. As a direct shipping ore (DSO) it has become in recent years almost the exclusive preserve of mega-producers, and smaller players have disappeared. One of the largest players has been BHP-Billiton (with mines in Australia and South Africa) while the largest player in North America is probably Grupo Autlan in Mexico. The BHP Manganese assets (amongst others) were recently spun- out via the South32 demerger operation. The goal here though is not for the product from Cancana’s venture to go to the export market but rather to go for domestic fertilizer usage in the soybean industry in particular. Brasil Manganese Corporation In 2014, the producing assets of the two miners operating in the vicinity of Cancana’s concession in Rondonia came under the ownership of Brasil Manganese Corporation (BMC), Cancana’s joint venture partnership with Ferrometals (which is a special purpose investment vehicle for The Sentient Group). Sentient is a resource-focused private equity fund with approximately $2.7Bn in assets under management, and a 15-year track record for advancing resource projects from early stage to pre- feasibility and development. We have come across Sentient before, principally in the context of the Rincon Lithium asset in Argentina. The backstory to the two companies acquired is that Manganese was first explored for by Rio Madeira Mineracao in 2005. The partners in that firm recognized an opportunity to create a niche market for high-grade, high-value manganese cobbles. These cobble fields were known from road cuts and discussions

with local farmers. The black cobbles were visible in roadbeds, especially after a rain. Minimal exploration uncovered several occurrences of these “boulder patches”. The company built a processing plant, which became operable during 2008. Operations BMC’s first actions after ownership transfer were to bring the safety features into line with modern practices. The mining is open cut, indeed it is somewhat akin to scraping the surface as the weathered boulders are the main material sought after. The picture below tells a thousand words as the heavily weathered red earth so frequently found in the tropics is the source of the boulders and other Manganese ore. The Rio Madeira plant is a basic affair consisting of common gravel washing and sorting plants. The raw material from the field is fed through a hopper and jaw crusher if needed, to

the first wash station – vibrating screens. The majority of soil is removed with the soil / water slurry being pumped to settling ponds. The remaining clasts are fed through a trommel for a second wash before being sorted by size with vibrating screens. The sorting places the material into 3 piles – a coarse, medium and fine fraction that is now available for sale as the final product. Further beneficiation can be done to separate manganese clasts from gangue by jigging the fine and medium material producing a cleaner, enriched material for the end client, depending on their need. During 2011, a second company, Eletroligas, optioned the properties known as Jaburi and set up a similar plant based on Rio Madeira’s plant. They produced material for themselves, as they are a ferro-manganese producer and needed a source of high-grade manganese. Their plant was designed to produce product for the ferro-manganese market only, which means they can tolerate higher minor elements in their final product then can material destined for the fertilizer market. Increased silica (quartz) and iron minerals are detriments to fertilizer producers but not ferro-manganese producers. The Eletroligas plant (renamed the Jaburi Plant) was improved to provide feed for the fertilizer market. The washing cycle and particle separating jigs were improved. The trommel feed and rotation were adjusted. New water pumps were installed. Both facilities needed extensive safety features such as re- wiring of overhead electrical infrastructure, hand rails, cat walks, chain guards, upgraded trommels, water pumps, tailing / settling ponds. Both plants follow similar circuits to produce finished product from raw materials. The raw material, which is a mixture of soil and clasts of all sizes, is brought to the plant by 20 tonne capacity trucks and stored near the plant. The clasts within the soil are heterogeneous in nature, made from manganese bearing materials, granitic, mafic and vein

quartz bearing clasts. Communications were improved by installing a radio network between all vehicles and base stations at each plant capable of reaching Espigao, over 40 km away. Production is still relatively small scale. BMC produced 2,143 tonnes of manganese product during the June quarter from colluvial sources, bringing stockpiles to 7,056 tonnes (net of sales) at the end of June. BMC then went on to produce 2,045 tonnes of manganese in the month of July 2015, being record production levels for the Rio Madeira plant. Most product seems to be accumulated into these stockpiles as BMC recorded second quarter sales of 338 tonnes. However what it did sell it managed to achieve prices averaging more than a 30% premium on current CIF prices. CIF Tianjin pricing for 44% manganese was US$2.98 per dmtu as of June 26th, 2015 Conclusion As I often repeat, Production is King and Cancana have short- circuited the expensive and tedious route of endless consultant’s reports by acquiring two producing properties to get the product flowing. We suspect that this shall be the trend for wannabe miners across a swathe of metals in coming years as the old paradigm fades in the face of brutal financing conditions. The Joint Venture partners, Cancana and Ferrometals, are employing a two-pronged strategy at BMC. The primary objective is to advance BMC to an initial resource and onward to pre- feasibility, while also expanding current small-scale production to support those exploration activities. This matches the strategy we have seen a number of other more innovative miners have pursued with the small scale operations funding the eventual bigger project. We can find nothing to fault in that and Cancana have gained a serious endorser of that strategy by attracting the very choosy Sentient people to

join with them in the venture.

You can also read