Understanding the Companies Act, 2013 - October 31, 2013

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Understanding the Companies Act, 2013 October 31, 2013

Housekeeping

• Place your phone on “mute”

• Use the question box

• #svcfindia

.

2

3

Agenda

1. Introduction

2. Kabir Kumar

3. Dr. Bhaskar Chatterjee

4. Pushpa Aman Singh

5. Q&A

4

Speakers

Kabir Kumar Dr. Bhaskar Chatterjee Pushpa Aman Singh

Silicon Valley Indian Institute of GuideStar India

Community Foundation Corporate Affairs

5

Evolution of Companies Act

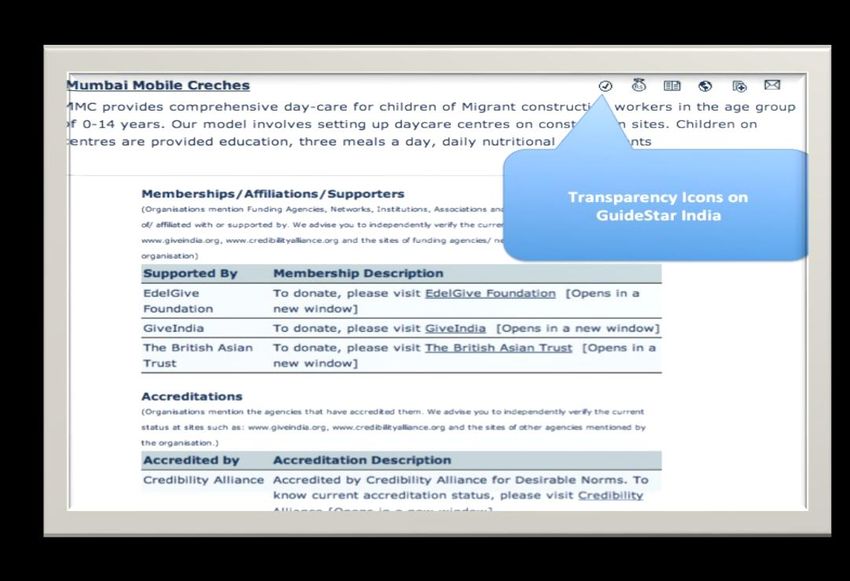

1956 2013

• Definition of public and • New types of companies

private company including one person

• Members and ownership company

• Definition of nonprofit • Increased guidance

company around governance

• Registration guidelines • New audit practices

• Emphasis on reporting

Section 25 company Section 8 company

6

Overview of CSR Section

• Eligible companies must spend 2% of average net

profits on CSR activities

• A committee must be formed to oversee these

mandated expenditures

• The committee develops a CSR policy which the

Board signs

• CSR activities must be monitored and reported on

7

Is My Company Eligible?

Net worth of Turnover of Rs. Net profit of Rs.

Rs. 500 crore 1,000 crore 5 crore

(US$81M) (US$162M) (US$1M)

Based on revenues generated in India

8

Role of the Committee

Policy Activities Monitor Report

9

Eligible Activities/Expenditures

10Reporting Requirements

Effective beginning

Annual CSR

FY14-15: Report Report

• CSR must be included

in annual report

materials

• Publish CSR policy

and report activities

online

11Indian Institute of Corporate Affairs Dr. Bhaskar Chatterjee

Dr. Bhaskar Chatterjee

DG&CEO

Indian Institute of Corporate AffairsHighlights of provisions of the Companies Bill Relating to CSR SECTION 135 1) Every company having a net worth of rupees five hundred crore or more (100 million $ or more),or a turnover of rupees one thousand crore or more (200 million $ or more) , or a net profit of rupees five crore or more (1 million $ or more) during any financial year shall constitute a Corporate Social Responsibility Committee of the Board consisting of three or more directors, out of which at least one director shall be an independent director; 2) The Board's report shall disclose the composition of14 the Corporate Social Responsibility Committee.

SECTION 135 {CONTD.}

3) The Corporate Social Responsibility Committee

shall,

a. formulate and recommend to the Board, a

Corporate Social Responsibility Policy which

shall indicate the activities to be undertaken by

the company as specified in Schedule VII;

b. recommend the amount of expenditure to be

incurred on the activities referred to in clause

(a); and

c. monitor the Corporate Social Responsibility

Policy of the company from time to time. 15SECTION 135 {CONTD.}

4) The Board of every company referred to in sub-section

(1) shall,

a) After taking into account the recommendations

made by the Corporate Social Responsibility

Committee, approve the Corporate Social

Responsibility Policy for the company and

disclose the contents of such Policy in its report

and also place it on the company's website, if

any, in such manner as may be prescribed; and

b) ensure that the activities as are included in

Corporate Social Responsibility Policy of the

company are undertaken by the company. 16

.SECTION 135 {CONTD.}

5) The Board of every company referred to in sub-

section (1), shall ensure that the company spends,

in every financial year, at least two per cent of the

average net profits of the company made during the

three immediately preceding financial years, in

pursuance of its Corporate Social Responsibility

Policy.

17SECTION 135 {CONTD.}

Provided that the company shall give preference to

the local area and areas around it where it operates,

for spending the amount earmarked for Corporate

Social Responsibility activities;

Provided that if the company fails to spend such

amount, the Board shall, in its report made under

clause (o) of sub-section (3) of section 134, specify

the reasons for not spending the amount.

18Sub Section (8) of Section 134

If a company contravenes the provisions of this

section, the company shall be punishable with

fine which shall not be less than fifty thousand

rupees but which may extend to twenty-five lakh

rupees and every officer of the company who is

in default shall be punishable with

imprisonment for a term which may extend to

three years or with fine which shall not be less

than fifty thousand rupees but which may extend

to five lakh rupees, or with both.

19What is CSR and what is not?

What is CSR? What is not CSR?

It should be rupee measurable; That which is not rupee measurable is

not a CSR activity;

It must bring direct benefits to If it does not benefits the poor &

marginalized , disadvantaged, poor or backward section of the community it is

deprived section of the community/ies; not a CSR activity;

It should not pre-dominantly benefit Employee benefits will not count as

employees of the company; CSR;

20What is CSR and what is not?

What is CSR? What is not CSR?

It can be related to the core business or It must not be part of the core business

the business model. It can thus deliver of the company;

shared value;

The quantum of value in monitoring The total value of the project itself

terms which the target group will derive cannot be shown as CSR;

must be shown and clearly identified;

It must be a sustained activity over a One-of or intermittent activities will not

period of time; count as CSR;

21What is CSR and what is not?

What is CSR? What is not CSR?

CSR activities must be in the form of Pure philanthropy or mere donations

projects/programmes. Thus CSR will not count as CSR

activities should be projectivized ;

Components of a project are as

follows:

•Need Based Assessment/Baseline

Survey/Study

•Clearly identified time frame

•Specific annual financial allocation

•Clearly identified milestones

•Clearly identified & measurable

objectives /goals

22

•Robust & periodic review &

monitoringWhat is CSR and what is not?

What is CSR? What is not CSR?

Programmes/projects must be within Programmes/projects undertaken

India; outside India will not count as CSR;

It should be independent of Activities which are in compliance

compliances with any regulation or with any regulation or law will not

law; count as CSR;

Projects/programmes can be taken Projects from CSR activities should

up as social business projects. not be shown as

commercial/business projects.

23GuideStar India Pushpa Aman Singh

Are there enough NGOs in India

• 3.17 million NGOs counted by the

Central Statistical Organisation

• Traced 694,000

• 55,000 unverified NGO records

with the Planning Commission

• 22,735 NGOs filed returns for

foreign contributions

• 4,200 registered on GuideStar

India

25How to identify NGOs partners

*No single registrar/ administrator of charities

*No common accounting standards, reporting guidelines

• Organization Assessment

• Financial & legal compliance

• Transparency in public domain

• Accountability to public

• Good governance practices

• Program Assessment

• Track record (milestones accomplished)

• Who are current supporters

• Reference checks

26How you could engage NGOs

*Giving money is great, give it for high impact

*Give your in-kind resources & expertise: infrastructure, IT, managerial, mentoring,

employee volunteering

• Use intermediaries or co-fund

• Use existing data and credibility information

• Participate in NGO India conference &

exhibition

• Uplift Non profit practice

• Review quarterly/ six monthly

• Demand factual, verifiable public reporting

• Challenge status quo

• Bring your best practices

• Report on challenges and not just highlight

success stories

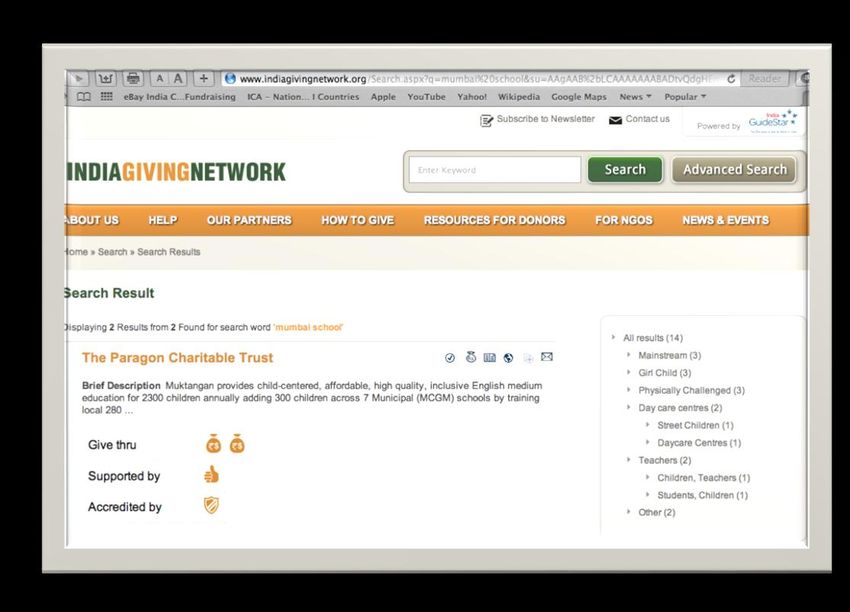

27Existing Resources

28What NGOs want

*308 NGOs responded to our mailer to give feedback on rules to the Act

*They attend every seminar on CSR to make sense of the “tamasha”

• We have been working with the community

all these years…

• Are we going to get any real support

• Every one wants projects,

who will support organisation development

for greater effectiveness

• Why is our cause not important

• Care for the disabled, elderly

• Every one wants a famous NGO,

near the airport!

• We seek partnerships not vendor contracts

• Please do not waste our time!

• Giving can be cool … enjoy the heat & dust!

29What you could do for great impact

*Giving money is great, give it for high impact

*Give your in-kind resources & expertise: infrastructure, IT, managerial, mentoring,

employee volunteering

• Look for high impact projects

• Catering to underserved areas

• Leveraging government programs

• Invest in the plumbing

• Capacity building of the sector

• Invest in philanthropy infrastructure

• Capacity building of grantees

• Get Involved!

30Thank you!

Pushpa Aman Singh (pushpa@guidestarindia.org)

Founder & CEO

GuideStar India

Call +91-22-26856900 /98/ 99

Visit http://www.guidestarindia.org

Read http://guidestarindia.blogspot.com

Follow http://twitter.com/GuideStarIndia

Like http://www.facebook.com/guidestarindia

Also, visit our portal on giving to

India: http://www.indiagivingnetwork.org

31Q&A

Kabir Kumar Dr. Bhaskar Chatterjee Pushpa Aman Singh

Silicon Valley Indian Institute of GuideStar India

Community Foundation Corporate Affairs

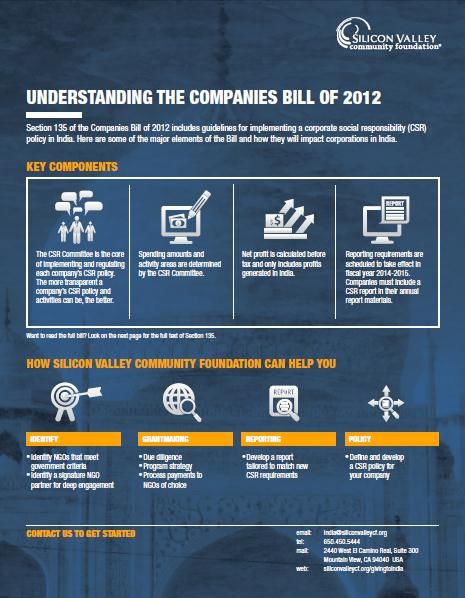

32How SVCF Can Help You

33Resources

34Contact Us

India@siliconvalleycf.org

+1.650.450.5444

siliconvalleycf.org/givingtoindia

35You can also read