2022 ACH Rules Update - JESSICA LELII, AAP ASSISTANT DIRECTOR OF EDUCATION MACHA/PAR-EVERYTHING PAYMENTS, EVERYWHERE - MY CU ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2022 ACH Rules Update JESSICA LELII, AAP A S S I S TA N T D I R E C TO R O F E D U C AT I O N M A C H A / PA R - E V E R Y T H I N G PAY M E N T S , E V E R Y W H E R E JLELII@MACHA.ORG

Disclaimer (You Know the Drill)

Payments Associations are directly

engaged in the Nacha rulemaking

process, Accredited ACH © 2021 Macha/PAR

Professional (AAP) program and

the Accredited Payments Risk

All Rights Reserved

Professional (APRP) program.

The Accredited ACH No part of this material

Professional (AAP) and the

may be used without the

Accredited Payments Risk

Professional (APRP) are service prior written permission of

marks of Nacha. Macha/PAR

This document could include

This material is not intended to technical inaccuracies or

provide any warranties or legal typographical errors and

advice, and is intended for individual users are responsible

educational purposes only. for verifying any information

contained herein.

2

Agenda

Upcoming

Recap 2021 What’s the

Changes for Questions

Rule Changes Buzz?

2022

2021 Recap

Same Day ACH – March 19, 2021

Functionality Same Day ACH Processing

Transaction Eligibility

Credits and debits

($100,000 Limit, IAT not eligible)

10:30 AM ET

Same Day ACH Processing Deadlines 2:45 PM ET

4:45 PM ET

1:00 PM ET

Settlement Time(s) 5:00 PM ET

6:00 PM ET

1:30 PM RDFI local

ACH Credit Funds Availability 5:00 PM RDFI local

End of Day local

5

Reversals in the ACH

Effective June 30, 2021

◦ Explicitly state Reversals are only ALLOWED for defined reasons

◦ For example – explicitly not Allowed for non-settlement

◦ Add allowable reason – Wrong Date error

◦ Debit was earlier or Credit was later than intended

Reversal must match Original

Company Name If Reversal was Improper

SEC Consumer Claim – RDFI Permitted

Amount R11 – 60 days

Must have REVERSAL in R17 for Corporate – 2 days

Company Entry Description R17 - RDFI identifies – 2 days

6

Timeframe Limitation of Claims Based on Unauthorized

Entries – June 30, 2021

CONSUMER ACCOUNTS NON-CONSUMER ACCOUNTS

Two (2) years from Settlement One (1) year from Settlement Date

Date of Entry of Entry

And / Or

95 Calendar days from Settlement

Date of first Unauthorized Entry

(Regulation E compliance for RDFI)

New Rules limits the length of time in which an RDFI can make a

claim against the ODFI for its authorization warranty

7

Limitation– Consumer Account

Claim Date: Sept 8, 2021 Claim Date: Sept 8, 2021

Consumer reports 7 years' worth of Consumer reports 3 debits as

recurring debits as unauthorized unauthorized

RDFI likely able to return at least July 1, August 3, Sept 1

“2” entries – within the last 60 days

RDFI returns – Sept 1, August 3

RDFI can make claim for payments as unauthorized per the ACH

within the first 95 days – 1 – 4 Rules

entries

RDFI can make claim for July 1

RDFI can make claim for payments ◦ 2 years and/or

in the most recent 2 years – ◦ 95 days

October 2019 – July 2021

◦ Falls into either category

8

Consumer

Makes Claim

Request ODFI to Return Recent

accept Returns Entries

Not “Valid” or Contact ODFI for

Not Provided Proof

ODFI provides

Wait for ODFI

Proof

Process Does Not Change

9Summary – Warranty Limitations

Consumer Claims

Automatic Right to Return within last 60 days from Settlement Date

RDFI can still make a claim for Last 2 years worth of transactions

RDFI can make a claim for the First 95 days of entries from the original entry if it is older than 2

years

This change still maintains RDFIs compliance with Regulation E requirements

Most importantly we need to continue to remind account holders to monitor statements

10Corporate Accounts –

Warranty Limitations

Business

RDFI ODFI RDFI

Accounts

• R29 • Past 2 Days • Contact • Warranty

• Two Days • Contact ODFI Information Claim – 1 year

• May Not be • Not much

Written really changes

Agreement for Corporate

Claims

11Proof of Authorization

September 17, 2021

RDFI Makes Request

for Authorization

ODFI written permission to RDFI to just

Return the Entry – no proof provided

RDFI still maintains right to request proof

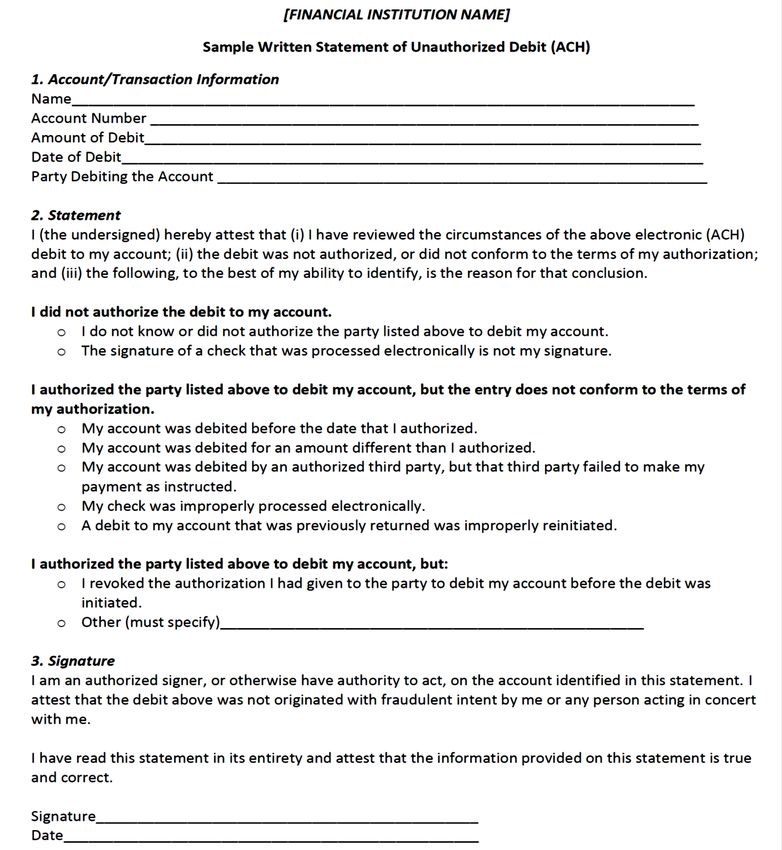

12Electronic or Oral WSUD

September 17, 2021

Clarifies that RDFI may obtain

Written Statements of Unauthorized Debits WSUD

Electronic Signatures or Oral

• Compliance with E-Sign

• Evidence of Identity & Assent to the Terms

13Oral or Electronic WSUD

RDFI

ODFI

Options

Prepared to receive requested

Wet Signature – like today WSUD

Electronic Signature In new acceptable formats

Oral

Electronic or Oral

Must comply with all existing

information requirements

Proof/Record

Ability to provide to ODFI

142021 Nacha Operating Rules

Page OG 342 or on Macha’s Member’s

Only page

R10

R11

R07

Just a Reminder – Never for “Happiness”

15Meaningful Modernization

Effective September 17, 2021

◦ Explicitly define & better enable use of Standing Authorizations & Subsequent

Entries for Consumer ACH debits

◦ Define & allow the use of oral authorizations of consumer ACH debits beyond

telephone calls

◦ Clarify & provide greater consistency of authorization standards for Consumer

ACH debits

16September 17, 2021

Authorization Standards

Grandfathered

applies to new

Minimum Requirements Authorizations

Consumer Debit Authorizations (2.3.2.2)

Language that entry is single, multiple, recurring entry

Amount or method of amount determination All Authorizations

Timing, number or frequency Readily identifiable

Receiver’s name/identity Clear and readily

Account to be debited understandable terms

Date of Authorization

Revocation language (how & when)

Originators need to

be incompliance

17Standing Authorizations

/Subsequent Entries

Flexibility Clearer

Authorization &

accommodates understanding of

Initiation across

Originator's systems “wholesome

business models

and practices authorization”

Framework for

Originators to offer

new payment

initiation options

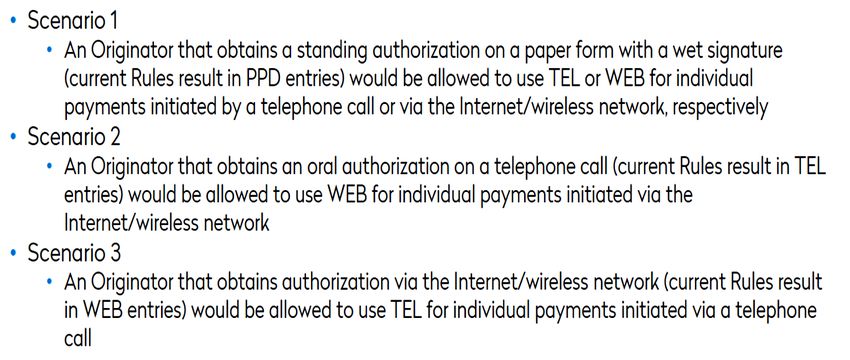

18Standing Authorization

Source: Nacha

19Standing Authorizations

Method of Receiver’s Affirmative Action

Via the Internet/Wireless

Written Via a

Network (Alexa, Skype,

Request Telephone Call

website, text msg., app)

In Writing PPD PPD or TEL PPD or WEB

Telephone

Form of the TEL TEL TEL or WEB

Auth.

Standing

Authorization

Internet or

Wireless

WEB WEB or TEL WEB

Network

Auth.

20“Speaking” Authorization – Debate

Settled

Oral Authorization / Oral Authorization /

Subsequent Entries Subsequent Entries

Oral Authorization Rules

Unsecure Electronic Consumer uses a Language Updated

Network Originator uses telephone Originator

WEB entry uses TEL entry

21Meaningful Modernization Guidelines

Update

Supplement #2-2021

Nacha issued

Significant revisions to • To address all the changes from Meaningful Modernization

the Guidelines • Will be incorporated in 2022 Nacha Operating Rules

Available on Macha – • Under “ACH & Check Rules Updates”

Member’s Only site

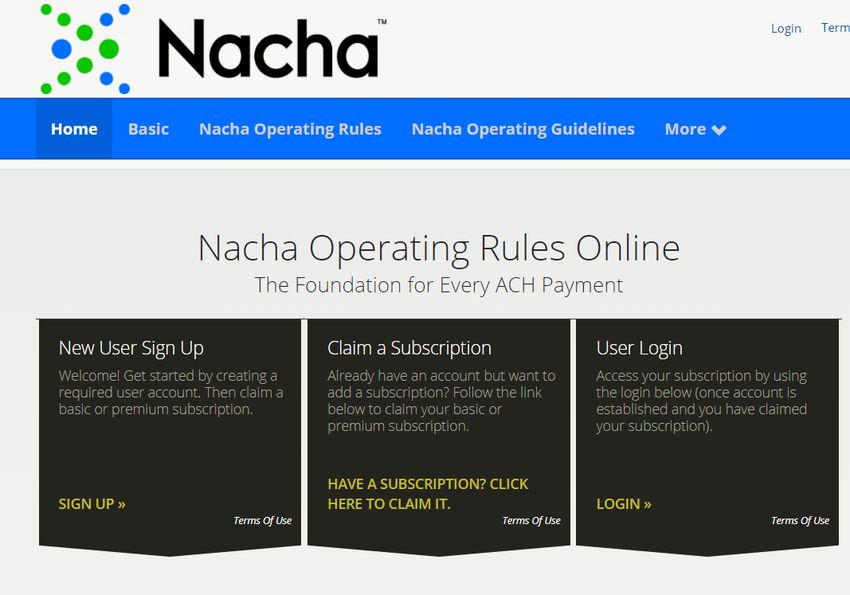

22What’s Coming in 2022?

2022 Rule Book

www.nachaoperatingrulesonline.org

◦ January 1, 2022

◦ Access to Rules supplements

◦ Printing , bookmark

Revisions Section

◦ New Rules

◦ Reminder – highlighted text

◦ New or revised Ruleswww.nachaoperatingrulesonline.org

25More Changes to SDA

Dollar Limit $1,000,000 March

per entry 18, 2022

• RDFI Impact to Clearing Accounts

• Especially the 6:00 pm settlement

• ODFI Risk Management

26Non-FI Originators, Third-Party Service Providers, Third-Party Senders

This rule DOES NOT APPLY DIRECTLY TO Financial Institutions

June 30, 2022

/

Protect account numbers by making them unreadable when stored electronically

• 2020 volume exceeds 2 million entries, by June 30, 2022

Rules requirement is neutral on method/technology

• Encryption, truncation, tokenization, etc

Account Information Security RequirementNested Third-Party Senders

Recently ◦ Defines

Approved ◦ Requirements of Origination Agreements to address

Nested TPS (going forward)

◦ ODFI required to attest in Risk Management Portal if

Third-Party Sender Roles &

Nested relationships exist

Responsibilities

◦ ODFI warranties for chain of Nested TPS

Effective:

Explicit requirement:

September 30, 2022 ◦ Third-Party Senders must complete a Risk Assessment of

their ACH Activity

Compliance by:

Only applies if you are an Originating

March 31, 2023 Depository Financial Institution and you

have Third-Party Sender Relationships

28Risk Assessments for Third-Party Senders??

No Standard

CDD, Exposure

Limits, PCI, TPPP

Credit, ODFI Guidance

Originator industry

Operational, Requirements issued by

Authorization groups, FFIEC

Fraud, – Article One financial

process, data & Third-Party

Compliance, & Two of institution

security, ACH Payment

Reputational Rules regulators

entry specific Processors

Rule

29What’s the Buzz?

Coming Soon Nacha is considering a ballot on a rule to define and standardize practices and formatting of micro-entries, which are used by some ACH Originators as a method of account validation This Rule is proposed to become effective in two phases •Phase 1-June 30, 2022 •Micro-Entries will be defined, and Originators will be required to use the standard Entry description and follow other origination practices •Phase 2 -March 17, 2023 •Originators of Micro-Entries will be required to use commercially reasonable fraud detection, including the monitoring of Micro-Entry forward and return volumes •RDFIs will be required to treat credit and debit Micro-Entries consistently

What’s a Micro-Entry? Micro-entries are a generally accepted method in the marketplace for an ACH Originator to test the validity of a Receiver’s account Due to several incidents of mis-use of micro-entries, Nacha issued two ACH Operations Bulletins in 2021 on Risk Management and Monitoring of Micro-Entries (May 18 and Sept. 7, 2021) •Nacha’s Risk Management Advisory Group also published a paper on the Use and Monitoring of Micro-Transactions on the ACH Network (Sept. 8, 2021)

SM FedNow News

Continuing Education

Credits

2022 ACH Rules Update

November 18, 2021

This session is worth 1.8 credits

36Payments – Its What We Do

Macha/PAR- Everything Payments, Everywhere

HELP DESK

Phone: Toll Free: Fax:

262-345-1245 info@macha.org

800-453-1843 262-345-1246

410-859-0090

37You can also read