2021 MARKET UPDATE WEBINAR - WITH CHIEF INVESTMENT OFFICER JEREMY DEGROOT - LITMAN GREGORY ASSET MANAGEMENT

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2021 Market Update Webinar with Chief Investment Officer Jeremy DeGroot

Today’s Speakers

Gretchen Hollstein, CFP® Jeremy DeGroot, CFA®

Senior Advisor, Principal Chief Investment Officer, Principal

2

Topics We’ll Address Today

• Review of 2020; Market Performance & Portfolio Actions

• Apparent Disconnect of Wall Street vs. Main Street

• Market Trends Emerging in Late 2020

• Macro Economic Outlook for 2021

• Investment Opportunities in 2021 and Beyond

• Perception of Risks: Federal Debt/Deficits, Monetary Inflation, Dollar Debasement

• Interest in Speculative Investments

• Diversified Portfolio Management Strategy in this Environment

3

Market Review: Assets Class Performance in 2020

Bonds Stocks Alternatives

25.0%

20.0%

20.0%

18.2%

15.2%

15.0%

9.7%

10.0%

7.6% 7.3%

6.2% 6.3%

5.0%

3.1%

0.0%

Invest-Grade Floating-Rate High-Yield U.S. U.S. Developed Emerging Alternative Managed

(Interm-Trm) Loans Larger-Cap Smaller-Cap International Markets Strategies Futures

2020

4 Source: Morningstar Direct. Data as of 12/31/2020.

2020: A Tumultuous but Ultimately Positive Year

7.8%

U.S. Treasuries

0.2%

1/1/2020 - 3/23/2020

6.3%

U.S. Dollar

-12.2%

3/24/2020 - 12/31/2020

1.0%

U.S. Invest-Grade Core Bonds

6.4%

-20.1%

Floating-Rate Loans

29.0%

-20.6%

U.S. High Yield Bonds

33.6%

-30.4%

Larger-Cap U.S. Stocks

70.2%

-31.8%

Emerging Markets Stocks

73.5%

-33.2%

Developed International Stocks

61.4%

-39.7% 99.1%

Smaller-Cap U.S. Stocks

-40.0% -20.0% 0.0% 20.0% 40.0% 60.0% 80.0% 100.0%

5

LG Added to US Stocks in March 2020, which Gained 50% to Year-End

4000

3800

3600

3400

S&P 500 Closing Price

3200

3000

S&P 500 gained over 50% from mid-March

2800

2600 LG added

to U.S.

2400 equities in

mid-March

after ~30%

2200

decline

2000

6

LG Swapped Europe for Emerging Markets in May, Boosting 2020 Returns

20.0%

10.0%

0.0%

-10.0%

-20.0%

-30.0%

LG swapped Europe

for Emerging Markets

-40.0%

Emerging Markets Europe

7

Since the April Plunge, Economic Data Have Been Positively

Surprising, Boosting Financial Markets

8 Source: BCA Research; Citigroup Global Markets Inc.

The Market is Anticipatory: Reacts in Advance of GDP Decline and Rise

4,000 80.0%

Real GDP Growth (right scale)

S&P 500 (left scale)

3,500 60.0%

3,000 40.0%

Q3: 33.4%

2,500 20.0%

Q4: 6.0%

2,000 0.0%

Q1: -5.0%

1,500 -20.0%

Q2: -31.4%

1,000 -40.0%

Jan-20 Apr-20 Jul-20 Oct-20

9 Source: U.S. Bureau of Economic Analysis, Federal Reserve Bank of Atlanta, Yahoo! Finance. Data as of 12/31/20.

Labor Market Recovering Rapidly — But Still Far From Recovered

Permanent Unemployment vs. Other Downturns

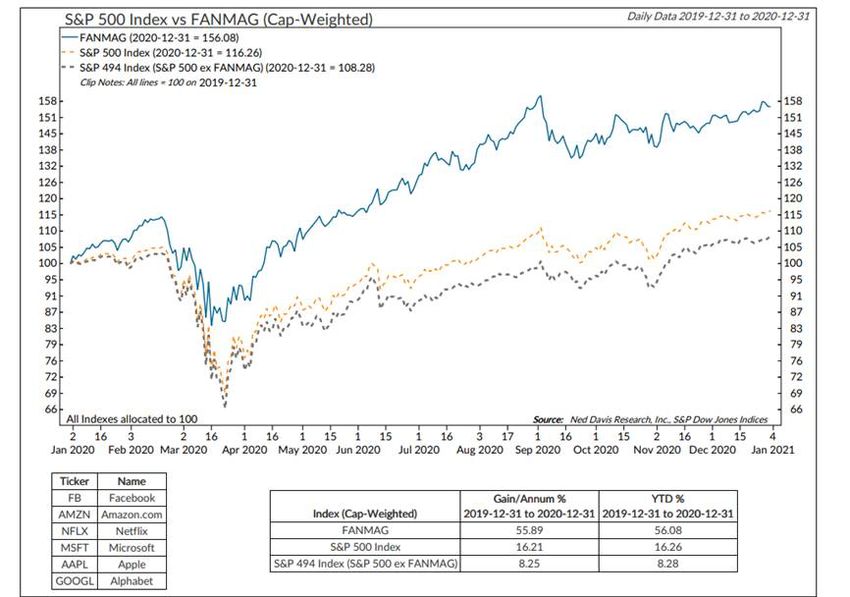

10 Source: U.S. Bureau of Labor Statistics. Chart concept courtesy of Guggenheim Investments. Data as of 11/30/20S&P 500 “Under the Hood”: FANMAG stocks vs. the S&P “494”

FANMAG

Stocks

S&P 500

Index

S&P 494

Index

(without

FANMAG)

11 Source: Ned Davis Research, Inc.Market Review: Asset Class Performance October–December 2020

Bonds Stocks Alternatives

35.0%

31.3%

30.0%

25.0%

20.0%

16.3% 16.5% 16.6%

15.0%

11.4%

10.0%

6.5%

5.8% 5.9%

5.0%

0.6%

0.0%

Invest-Grade High-Yield U.S. Larger Cap U.S. Larger Cap U.S. Developed Emerging Alternative Managed

(Interm-Trm) Value Growth Smaller-Cap International Markets Strategies Futures

Q4 2020

12 Source: Morningstar Direct. Data as of 12/31/2020.COVID Mobility Trackers: Real Time Measures of Activity,

Recovered in the Summer but Weakened into January 2021

* Mobility trackers are real time requests of web browser services for data on retail, recreation, and

workplace visits, use of public transportation, and drivers' routing requests. They provide real time

data reflecting changes in economic activity.

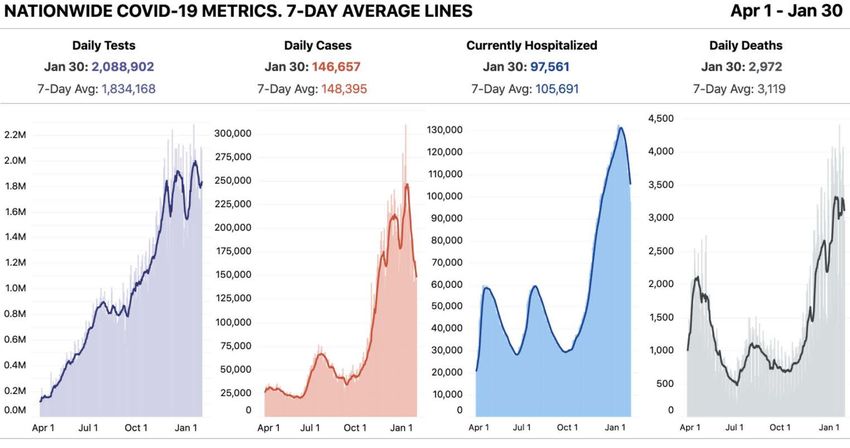

13 Source: Google, Apple, Moovit, Capital EconomicsU.S. COVID-19 Statistics: Key Risk in Near-Term Economic Outlook 14 Source: The COVID Tracking Project

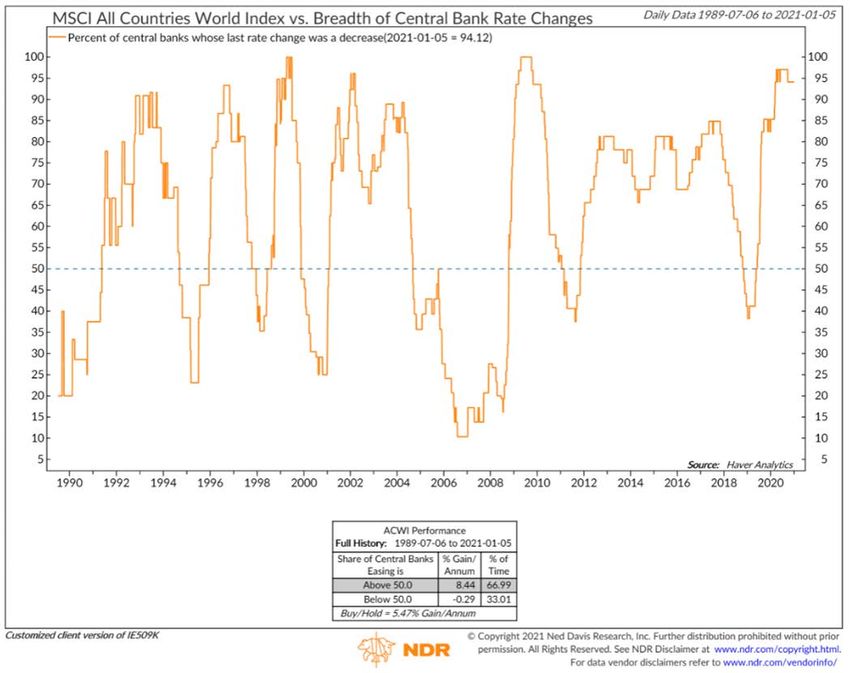

Accommodative Monetary and Fiscal Policy Should Support the

Economy and Financial Markets Over the Near-Term

15 Source: Ned Davis Research.The Fed Has Again Hugely Expanded Its Balance Sheet via

Quantitative Easing (QE) …

The Fed’s Balance Sheet in Perspective

16 Source: BCA Research… As Have Other Major Global Central Banks

Global Central Bank: Balance Sheet

* Sum of the BOE, ECB, FED and BoJ

17

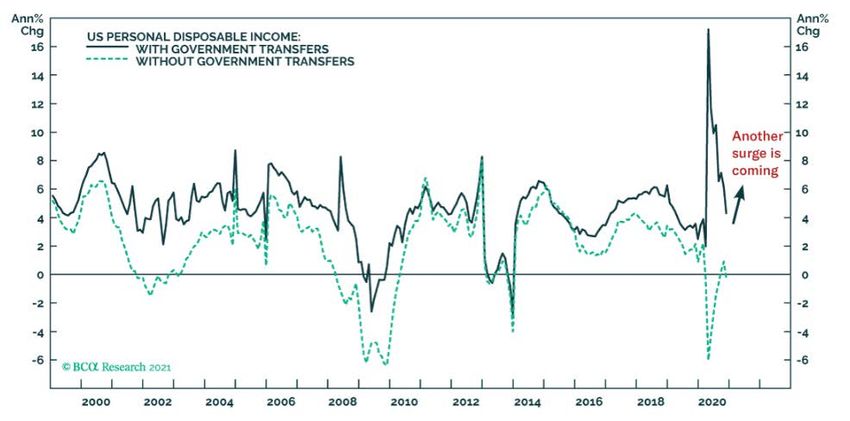

Source: BCA ResearchFiscal Policy/CARES Act Had a Huge Positive Impact on

Personal Disposable Income, Offsetting the Shutdown

18 Source: BCA Research 2021U.S. Stocks Are Expensive But Still Attractive Relative to Bonds

US CYCLICALLY-ADJUSTED P/E GLOBAL EXCLUDING US CYCLICALLY-ADJUSTED P/E

50 50

• U.S. stock valuations, as

40 40 measured by the Shiller CAPE

(cyclically-adjusted price-to-

30 30 earnings) ratio, are at a level

not seen since the dot-com

20 20 bubble.

2000 2020

• However, in this environment

of extremely low bond yields,

U.S. stocks still look relatively

US EQUITY RISK PREMIUM GLOBAL EXCLUDING US EQUITY RISK PREMIUM

attractive compared to core

600 600

bonds or Treasury bonds. This

is evident by looking at the

400 400

“equity risk premium,” which is

historically high (a higher ERP

BPs

BPs

200 200

implies stocks are cheaper

versus bonds).

0 0

-200 -200

2000 2020

.

19 Source: BCA Research.Outlook for Emerging Markets vs. U.S. Stocks Is Very Attractive

Rolling 5-year Return Difference: EM Stocks Minus US Stocks

30%

25%

20% EM stocks

15% outperforming Litman Gregory Base-Case

U.S. stocks Five-Year Return Difference

10%

5%

0%

-5%

-10%

-15%

-20%

U.S. stocks

-25%

outperforming EM stocks

-30%

-35%

-40%

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021 2023 2025

20 Source: Morningstar Direct. Data as of 12/31/2020.A Weaker Dollar Should Also Benefit Foreign Stock Returns

U.S. Stocks / Non-U.S. Stocks (left scale)

350 Real Trade Weighted U.S. Dollar Index (right scale)

130

• The direction of the

U.S. dollar is important

300

for foreign markets

U.S. Outperforming Non-U.S.

120

and the global

economy; it tends to

250

appreciate and

Real Trade Weighted U.S. Dollar Index

depreciate in the

S&P 500 / MSCI World ex USA

110

200 opposite direction of

the global business

cycle.

USD 100

150 Falling

90 • A rebound in the

100

global economy

should be a negative

80 for the dollar relative

50

to other currencies

0 70

1973 1978 1983 1988 1993 1998 2003 2008 2013 2018

21 Source: Board of Governors of the Federal Reserve System. Data as of 12/31/2020.China: Large and Growing Importance in World Economy

and Emerging Markets

Share of World GDP in $USD

USA, 24.4%

Rest of World,

30.4%

Share of MSCI ACWI “All World” Equity Index

Canada, 2.0%

EU, 17.8%

India, 3.3% Other, 24.9%

Japan, 5.8%

China, 16.3%

USA, 56.3%

Canada, 2.8%

UK, 4.1%

China, 4.7%

Japan, 7.3%

USA Japan China UK Canada Other

22Given the Slack in the Economy, Inflation Unlikely a Near Term Risk

• Inflation is unlikely to

move substantially higher,

absent an external shock,

as long as there remains

high unemployment and

excess economic capacity.

• Currently the Fed is

forecasting a 5.0%

unemployment rate for

2021 and 4.2% for 2022.

And core inflation of 1.8%

in 2021 and 1.9% in 2022.

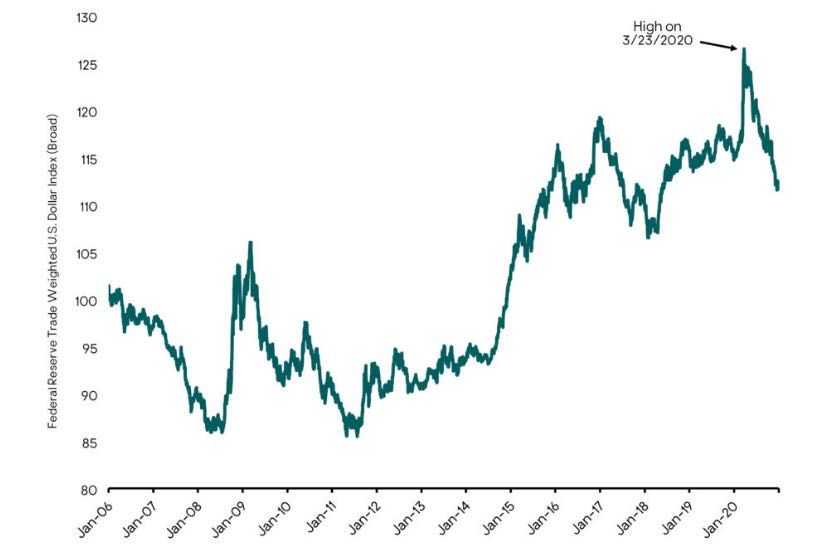

23 Source: Ned Davis Research.Trade-Weighted Dollar Index: US Dollar vs. Other Currencies,

More Room to Fall

The U.S. Dollar Has Fallen More than 10% Since Late March

24 Source: Litman Gregory Analytics, LLC; Data from Board of Governors of the Federal Reserve System as of 12/31/2020.Bitcoin’s Price is Extremely Volatile! 25 Source: Bloomberg, Goldman Sachs Global Investment Research.

Bitcoin Performed Poorly During Last Year’s Equity Bear Market 26 Source: Goldman Sachs Asset Management, Bloomberg; Data as of 4/3/2020.

The Stratospheric Rise of Bitcoin vs. Other Speculative Situations 27 Source: BofA Global Investment Strategy, Bloomberg, Financial Times.

Portfolio Opportunities Across Different Environments

Our portfolios are designed to provide exposure to a mix of investments that offer different return and risk profiles

across a variety of economic environments and financial market scenarios.

Mid-High Growth – Low Inflation Mid-High Growth – High Inflation

EM EQUITIES ALL EQUITIES

FLOATING RATE LOANS EM CURRENCIES

INTERNATIONAL EQUITIES

HIGH YIELD BONDS

US EQUITIES NATURAL RESOURCES

Growth

ALTERNATIVE

STRATEGIES

Growth Slows / Shrinks – Low Inflation Growth Slows – High Inflation

(Recession / Deflation) (Stagflation)

SHORT-TERM BONDS

TIPS

INTERMEDIATE-TERM BONDS

COMMODITIES

TIPS

MANAGED

FUTURES

GOVERNMENT BONDS

Inflation

EM: Emerging Markets

28 TIPS: Treasury Inflation-Protected SecuritiesOur Portfolios Are Built to be Balanced, Resilient and Opportunistic

Global Balanced Portfolio Components

Hybrid Investments (Return

+ Risk Management)

Alternative Strategies

Flexible Bond Funds

Long-Term Return Generators

Floating Rate Loans

U.S. Equities

Developed International Equities

Emerging Markets Equities

Risk Mitigators Private Real Estate

Private Equity

Core Investment Grade Bonds

Treasury Bonds

29The Market’s “Mood” Cycles Between Fear and Greed,

Successful Long-Term Investors “Stay the Course”

30 Source: CNN Business, December 2020Markets Have Been Resilient Over Time, Despite There Always Being

a Myriad of Things to Worry About

Subprime Mortgage Crisis

Lehman Brothers Collapse

Housing Crisis

Great Financial Crisis

$640,000 Asian Financial Crisis 2007-2009 Recession

Russian Ruble Crisis 2009 Flu Pandemic

Cumulative Growth of $10,000 Invested in the S&P 500 Index

Clinton Impeachment MERS Outbreak

Y2K European Debt Crisis

$320,000 U.S. Debt Downgraded by S&P

Tech Bubble Busts

9/11 Terrorist Attacks U.S. Gov't Shutdown

2001 Recession

$160,000 Afghanistan War

Black Monday Crash

Gulf War

1990-1991 Recession

$80,000

Los Angeles Riots

World Trade Center Bombing Ebola Epidemic

Bond Market Crisis Taper Tantrum

$40,000 Oil Crisis

Zika Virus

Brexit

Iraq War U.S. Gov't Shutdown

Avian Flu Quantitative Tightening

$20,000

SARS Outbreak U.S.-China Trade War

Hurricane Katrina Coronavirus

$10,000

$5,000

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

31 Source: Morningstar Direct. Data as of 12/31/2020.Closing Thoughts

• As always, it is paramount to stay disciplined and recognize when emotion rears its head in

investment decision making.

• Maintain a focus on long-term financial goals and objectives, with an eye to near-term risks.

• Avoid the temptation to time the market — it is a fool’s errand.

• There is always uncertainty, but as an investor it has paid to maintain a long-term,

rationally optimistic view of human progress, adaptation and recovery.

o A recent quote* we liked: “Save like a pessimist and invest like an optimist.”

• We understand that each individual client has unique circumstances. Please contact your

advisor directly to discuss any of today’s comments in the context of your portfolio.

• Most importantly, we sincerely hope you and yours are able to remain healthy and manage

well through this extraordinary period.

32 *quote from Morgan HouselThank you for joining us today!

For further questions, please contact your advisor directly, or the

Litman Gregory Client Services team at:

415.526.4380

information@lgam.com

www.lgam.com

33Disclosure

This writing is provided by Litman Gregory Asset Management, LLC (“LGAM”) for informational purposes only and may contain information that is not suitable

for all investors. No portion of this commentary is to be construed as a solicitation or recommendation to buy or sell a security, or the provision of

personalized investment advice, tax or legal advice. Past performance may not be indicative of future results and may have been impacted by market events

and economic conditions that will not prevail in the future. There can be no assurance that any particular investment or strategy will prove profitable and the

views, opinions and projections expressed herein may not come to pass. A complete list of portfolio holdings and specific securities transactions for the

preceding 12 months is available upon request. All information is subject to change without notice. Any direct or indirect reference to a market index is

included for illustrative purposes only, as an index is not a security in which an investment can be made. Indices are benchmarks that serve as market or

sector indicators and do not account for the deduction of management fees, transaction costs and other expenses associated with investable products. LGAM

does not make any representations as to the accuracy, timeliness, suitability, completeness or relevance of an information prepared by any unaffiliated third

party and takes no responsibility therefore. Any projections provided regarding the likelihood of various investment outcomes are hypothetical in nature, do

not reflect actual investment results and are not guarantees of future results. Investing involves risk, including the potential loss of principal, and investors

should be guided accordingly.

The graphs, charts and other visual aids are provided for informational purposes only. None of these graphs, charts or visual aids can of themselves be used

to make investment decisions. No representation is made that these will assist any person in making investment decisions and no graph, chart or other visual

aid can capture all factors and variables required in making such decisions.

LGAM is an independent investment adviser registered with the U.S. Securities and Exchange Commission (SEC). For additional information about LGAM,

please consult its Form ADV disclosure documents, the most recent versions of which are available on the SEC’s Investment Adviser Public Disclosure website

at www.adviserinfo.sec.gov.

34You can also read