Vodacom Group Limited - September 2016

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Vodacom

Group

Limited

September 2016

Vodacom Group Limited IR presentation | 5 September 2016

Disclaimer The following presentation is being made only to, and is only directed at, persons to whom such presentations may lawfully be communicated (‘relevant persons’). Any person who is not a relevant person should not act or rely on this presentation or any of its contents. Information in the following presentation relating to the price at which relevant investments have been bought or sold in the past or the yield on such investments cannot be relied upon as a guide to the future performance of such investments. This presentation does not constitute an offering of securities or otherwise constitute an invitation or inducement to any person to underwrite, subscribe for or otherwise acquire securities in any company within the Group. Promotional material used in this presentation that is based on pricing or service offering may no longer be applicable. This presentation contains certain non-GAAP financial information which has not been reviewed or reported on by the Group’s auditors. The Group’s management believes these measures provide valuable additional information in understanding the performance of the Group or the Group’s businesses because they provide measures used by the Group to assess performance. However, this additional information presented is not uniformly defined by all companies, including those in the Group’s industry. Accordingly, it may not be comparable with similarly titled measures and disclosures by other companies. Additionally, although these measures are important in the management of the business, they should not be viewed in isolation or as replacements for or alternatives to, but rather as complementary to, the comparable GAAP measures. This presentation also contains forward-looking statements which are subject to risks and uncertainties because they relate to future events. These forward-looking statements include, without limitation, statements in relation to the Group’s projected financial results. Some of the factors which may cause actual results to differ from these forward-looking statements are discussed on slide 23 of this presentation. Vodafone, the Vodafone logo, Vodafone Mobile Broadband, Vodafone WebBox, Vodafone WebBook, Vodafone Smart tab, Vodafone 858 Smartphone, Vodafone Passport, Vodafone live!, Power to You, Vodacom, Vodacom M-Pesa, Vodacom Millionaires, Vodacom 4 Less and Vodacom Change the World are trademarks of Vodafone Group Plc (or have applications pending). Other product and company names mentioned herein may be trademarks of their respective owners. Vodacom Group Limited IR presentation | 5 September 2016 2

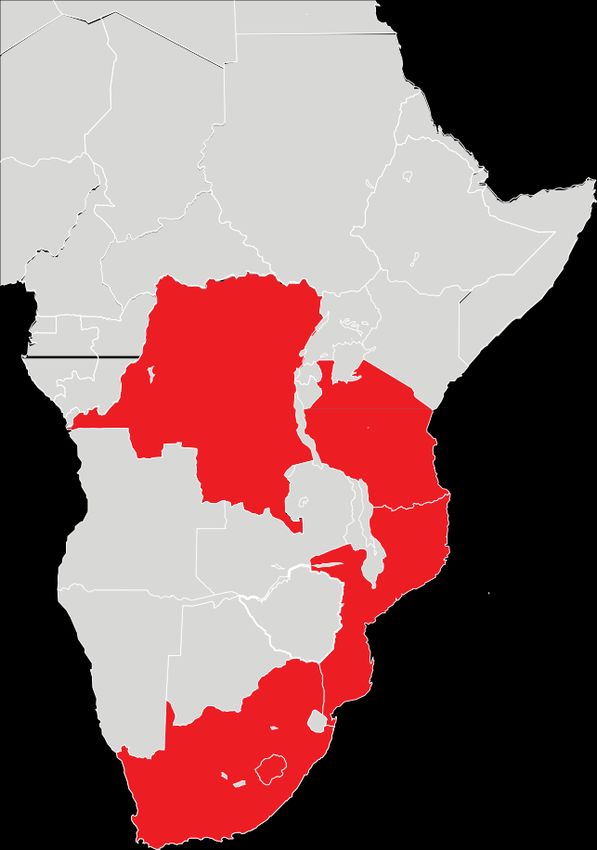

A leading African mobile communication company providing

a wide range of communication services including mobile

voice, messaging, data and converged services to over

61 million customers.

Vodacom DRC

Licenced 2002

Population 71 million Vodacom Tanzania Vodacom is majority owned by Vodafone Plc (65%) and we

Licenced 1999

are listed on the JSE Limited.

Population 55 million

Market capitalisation of R231.3 billion#.

Group revenue of R80.1 billion.

Vodacom Mozambique

Licenced 2003

Population 29 million Head office in Midrand, South Africa

Vodacom Lesotho

Vodacom South Africa Licenced 1995 History – consistent track record of innovation

Licenced 1993

Population 2 million

Population 55 million

1996 2004 2008 2009 2011 2012 2016

Vodacom

First to launch Vodacom LTE-Advanced

All information in presentation is as at 31 March 2016, unless otherwise stated. Vodacom Vodacom listed rebrands from First to launch

prepaid services launches a 3G launched

#Market capitalisation value as at 5 September 2016. Business on the JSE “Green and Blue” 4G in

in the world on IN HSDPA network

launches (18 May) to Vodafone South Africa

platforms in South Africa

RED

Vodacom Group Limited IR presentation | 5 September 2016 3

Share information

As at 5 September 2016 Institutional shareholding

JSE Ticker symbol VOD

ADR code VDMCY

PIC = 49.9%

Stock exchange JSE Limited 4%4%

7%

Shares in issue 1 487 954 000 South Africa

Freefloat 35% United States

52 week low and high R132 – R172 19% United Kingdom

Rest of Europe

Market capitalisation R231.3 billion

66% Rest of world

Debt rating Long term scaling zaAAA (S&P)

Transfer agent ComputerShare

FTSE/JSE Top 40 Index

Indices JSE Socially Responsible Index

Nedbank BGreen Exchange Traded Fund

Vodacom Group Limited IR presentation | 5 September 2016 4

Five reasons to own Vodacom shares

1 Market leadership

2 Focus areas of growth potential

3 Scale benefits driving efficiencies

4 Experienced, diverse management team

5 Track record of delivering shareholder returns

Vodacom Group Limited IR presentation | 5 September 2016 5

5

#1 | Market leadership

# 1 mobile operator in all markets

61.3 million customers in > 18 000 base stations, > 80% 3G

5 countries in Sub-Saharan Africa 1st to launch 4G in South Africa, Lesotho and

R14 billion enterprise revenue from Tanzania

30 countries in Africa

R13 billion

investment per annum to maintain our leading network quality

All information is as at 31 March 2016

Vodacom Group Limited IR presentation | 5 September 2016 6

#2 | Focus areas of growth potential

FY14: +33% FY14: +24%

FY15: +25% FY15: +10%

Data (32% of Group service revenue) FY16: +29%

International (27% of Group service revenue) FY16: +17%

• Group: 29 million active data customers; 57% of total base • 27% of Group service revenue

• SA: 14 million active smart devices; 37% of active • Data revenue growth +32%

customers • Active customers 27 million

• SA: 572MB per smart device growing 23% o Active customers now 44% of Group active customers

FY14: +37%

FY15: +13%

Enterprise (21% of Group service revenue) FY16: +19%

New services (SA) (4.2% of Group service revenue)

• Enterprise contributes 21% to Group service revenue • Insurance revenue +19%

• SA fixed and managed services revenue +27% o Expanding portfolio: life, funeral, device, cover

o Pan African MPLS network • Capture Internet of Things opportunity

o Fibre to the business/home • Fibre to home +25 000 homes and businesses passed

.

Vodacom Group Limited IR presentation | 5 September 2016 7

7

#3 | Scale benefits driving efficiencies

Focussed savings programmes – Fit 4 Growth

• Reduced transmission rentals through self-provisioning

• Cost optimisation through sharing, outsourcing and supply

chain management

• Improved return on investment in customer acquisition

spend

• Reduced support costs offsetting inflationary pressures

Benefits from being part of the Vodafone Group

• Global technology and product roadmap

• Better pricing through Vodafone Procurement Company

• Benefits from best practice sharing and benchmarking

• Talent and skills sharing

Vodacom Group Limited IR presentation | 5 September 2016 8

8

#4 | Experienced, diverse management team

4

CEO: Shameel Aziz Joosub (45) CFO: Till Streichert (41)

20 years industry experience 15 years industry experience

Previously CEO of Vodafone Spain Previously CFO of Vodafone Romania

IT Person of the year 2015 European and emerging market experience

Executive Committee (12 members)

Female

Intern-

17% ational

Black White 25%

58% 42% South

African

Male

75%

83%

Vodacom Group Limited IR presentation | 5 September 2016 9

#5 | Consistently delivering shareholder returns

Relative share price performance1 Dividend per share

Cents per share

825 795

775

430 400 400

TSR ZAR YTD (for 12 months ending 5 September 2016)

Vodacom 13.0%

395 375 395

Telkom 3.8%

Bharti -7.1% FY14 FY15 FY16

Millicom -18.1%

Interim dividend Final dividend

MTN -31.5%

-35.0% -25.0% -15.0% -5.0% 5.0% 15.0%

1. As at 5 September 2016.

Vodacom Group Limited IR presentation | 5 September 2016 10Targets | Group three-year targets

Low to mid single-digit

Service revenue growth

Mid to high single-digit

EBITDA growth

12% to 14%

Capex intensity

Vodacom Group Limited IR presentation | 5 September 2016 11

11Continuing to deliver returns

Best network Diversify Deliver cost Best talent Transform

--------------------- revenue to and process --------------------- society and

Best value deliver growth efficiency Best practice build

--------------------- stakeholder

Best service trust

Vodacom Group Limited IR presentation | 5 September 2016 12Customer | Best network, Best value, Best service

Best network Best value Best service

• Network customer satisfaction #1 in all • Personalised pricing and offers • Connectivity

markets but one • Driving pricing transformation • Always in control

• 4G coverage in SA at 58% • Reducing communication costs • Rewarding loyalty

• International sites +17% • Stimulating bundle adoption • Easy access

• SA dropped call rate @ 0.41%

• 1st in SA with commercial mobile LTE-A

Average download speeds in SA Total prepaid bundle sales in SA SA Consumer NPS points differentiation

Source: MyBroadband (March 2016) (Mbps) Million %

+6 ppts

+15 ppts

86 189

23 18 17 10 314 387 383 369

1H15 2H15 1H16 2H16 FY15 FY16

Vodacom SA Operator A Operator B Operator C Vodacom Competitor A Competitor B

Total prepaid bundle sales Just 4 You

Vodacom Group Limited IR presentation | 5 September 2016 13Growth | Diversifying revenue to deliver growth

Data contribution International contribution

FY16 • Growth +28.5% FY16 • Growth +17%

• Average usage per smart • EBITDA contribution

FY14 device - 572MB FY14

26.6% 17.7% (FY14: 15.6%)

31.9% • 2G to 3G; 3G to 4G

21.4% 24.6%

• M-Pesa revenue +19%

ARPU uplift +20%

Contribution to Group service revenue Contribution to Group service revenue

Enterprise contribution New services contribution (SA)

• Enterprise service FY16 • Device insurance

FY16 4.2%

revenue +20% policies +25%

• R3.2bn fixed-line & BMS FY14

FY14 20.5% 3.5% • IoT connections +28%

15.1% revenue

• Wholesale partnership

agreements for fibre

• GDSP platform delivery

Contribution to Group service revenue Contribution to SA service revenue

Vodacom Group Limited IR presentation | 5 September 2016 14

14Operations | Fit for growth SA

30.5% of SR 6.6% of SR

Number (FY15: 31.6%) (FY15: 6.7%)

of sites

+9% Direct expenses1 Staff expenses2

• Channel efficiencies • Hire in key growth areas

• Sophisticated IBRO • Attract and retain talent

management

Actively managing costs Energy • Credit management

inflation

• Sharing and outsourcing to realise scale +13%

• Incentives – volume vs revenue

• Digitisation – self care and empowering

customers Inflation 2.5% of SR 14.4% of SR

• Cost consciousness at an individual level +6% (FY15: 2.7%) (FY15: 14.1%)

Publicity expenses Other operating expenses3

• Consolidated agency spend • Reduced network cost per site

Innovate Wage

• Improved production cost • Improved digitisation and App

efficiency penetration

inflation

• Increased digital/social

+6% • Leverage scale through

platform spend

sharing and outsourcing

• Increased share of voice

1. Excluding equipment expenses.

2. Excluding BEE charge.

3. Excluding trading foreign exchange.

Vodacom Group Limited IR presentation | 5 September 2016 15

15People | Attracting and retaining the best talent

Driving people transformation through

Enhancing diversity Growing talent Developing skills

• 73% black and 39% female • 123 graduates in 2015 • R103 million spent on skills

staff Graduate programme development

• 55% of EXCO black • International Graduate • Capability build and

• Vodacom Women in Red programme in all our succession programmes

Awards markets

• International assignee

programme

Vodacom Group Limited IR presentation | 5 September 2016 16Reputation | Mobile for good

R106m +600k Vodacom

spent by TZN eSchool

Vodacom subscribers: free education

Foundation on Healthy portal 105k

CSI projects pregnancy registered

Healthy baby learners

20 24 hour 3 087

volunteers for call center for schools

annual Change victims of connected -

the World gender-based Universal

programme violence Service

obligations

Vodacom Group Limited IR presentation | 5 September 2016 17

17Reputation | BEE Level 2 contributor

R841m R218m R112m

spent on spent on spent on skills

developing uplifting development

SMME ICT communities

businesses

98.25

Most empowered

telco in 18

South Africa

R7.2bn R5bn R26bn

to >51% black- to >30% black weighted spend

owned women-owned on BEE-status

suppliers suppliers suppliers

Vodacom Group Limited IR presentation | 5 September 2016 18Additional

information

Vodacom Group Limited IR presentation | 5 September 2016Country data

South Africa Tanzania DRC Mozambique Lesotho

PopulationŦ (million) 55 55 71 29 2

GDP per capitaŦ (USD) 4 770 855 495 456 887

GDP growth estimateŦ 2016 (%) 0.7 6.5 5.0 4.8 2.0

Ownership (%) 93.75# 82.2 51 85 80

License expiry period 2029 2031 2028/2032µ 2018/2026µ 2036

Active customers (thousand) 35 112 12 060 8 486 4 817 1 359

ARPU (rand per month) 109 40 58 56 62

ARPU (local currency per month) 109 5 876 3.9 207 62

Minutes of use per month 134 158 50 109 79

Key indicators for the quarter ended 30 June 2016.

Ŧ The Economist Intelligence Unit.

# 6.25% held indirectly through special purpose entities which are consolidated in terms of SIC 12: Consolidation – Special Purpose Entities as part of the broad-based black economic empowerment transaction.

µ 2028/2018 relates to the 2G license and 2032/2026 relates to the 3G licence.

20

Vodacom Group Limited IR presentation | 5 September 2016 20Latest results | Q1 results for the quarter ended 30 June 2016

Sustained robust service revenue growth R million Jun 2016 Jun 2015 YoY % Δ

• Group service revenue up 7.3% (4.6%*) Group

• SA service revenue growth of 5.6% to R12 426 million Service revenue 16 806 15 660 7.3

• SA added just under 1 million customers in the quarter Revenue 19 902 18 806 5.8

Data revenue 5 786 4 846 19.4

Customers (m) 61 834 63 502 (3.3)

Strong demand for data services

South Africa

• Group data revenue up 19.4%, 34.4% of service revenue

Service revenue 12 426 11 762 5.6

• SA active data customers up 6.1% to 18.8 million Revenue 15 443 14 845 4.0

• 3.1 million LTE/4G customers in South Africa Data revenue 4 691 3 975 18.0

Customers (m) 35 112 33 309 5.4

International impacted by customer registration International

• Service revenue up 13.5% (2.8%*); contributed 26.7% to Service revenue 4 479 3 945 13.5

Group service revenue Revenue 4 620 4 095 12.8

• M-Pesa revenue +47.5%; 10.6 million active customers Data revenue 1 095 871 25.7

Customers (m) 26 722 30 193 (11.5)

* Normalised growth adjusted at a constant currency using current year as the base.

Vodacom Group Limited IR presentation | 5 September 2016 21Annual results for the year ending 31 March 2016

Improved revenue growth and margins R million Mar 2016 Mar 2015 YoY % Δ

• Group service revenue up 7.4% (5.8%*) Service revenue 66 763 62 167 7.4

• Group EBITDA up 12.8% (10.2%*) Revenue 80 077 74 500 7.5

• Headline earnings per share up 2.7% EBITDA 30 345 26 905 12.8

Operating profit 21 059 19 516 9.5

• 400 cents final dividend per share

Operating free cash flow 17 054 14 003 21.8

Free cash flow 9 807 7 763 26.3

Strong demand for data services Capital expenditure 12 875 13 305 (3.2)

• Group data revenue up 28.5%. 31.9% of service Net debt 21 287 16 760 27.0

revenue Headline earnings per share

883 860 2.7

• Group active data customers up 8.6% to 28.8 million (cents)

Dividend per share (cents) 795 775 2.6

• 14 million active smart devices in South Africa

EBITDA margin (%) 37.9 .36.1 1.8 ppts

Effective tax rate (%) 31.5 29.9 1.6 ppts

Excellent International performance Net debt/EBITDA (times) 0.7 0.6 0.1 times

• Service revenue up 16.2% (9.6%*), contributed 26.6% to Capex intensity (%) 16.1 17.9 (1.8 ppts)

Group service revenue

• M-Pesa revenue +19.3%; 9.2 million active customers

* Normalised growth adjusted for trading foreign exchange gains/losses and at a constant currency using current year as base (collectively ‘foreign exchange’).

Vodacom Group Limited IR presentation | 5 September 2016 22Five-year financials for the year ended 31 March R million 2016 2015 2014 2013 2012 16/15 % Δ 5-year CAGR Service revenue 66 763 62 617 62 047 59 261 58 125 7.4 3.8 Revenue 80 077 74 500 73 219 67 781 65 700 7.5 5.1 EBITDA 30 345 26 905 27 314 25 253 22 763 12.8 7.5 Operating profit 21 059 19 235 20 394 18 897 16 617 9.5 6.1 Operating free cash flow 17 054 14 003 19 410 18 158 16 934 21.8 0.2 Free cash flow 9 807 7 763 13 185 12 136 10 921 26.3 (2.7) Capital expenditure 12 875 13 305 10 779 9 456 8 662 (3.2) 10.4 Net debt 21 287 16 760 8 052 8 007 7 667 27.0 15.4 Headline earnings per share (cents) 883 860 896 872 709 2.7 7.0 Dividend per share (cents) 795 775 825 785 710 2.6 13.9 EBITDA margin (%) 37.9 36.1 37.3 37.3 34.6 Effective tax rate (%) 31.5 29.9 30.2 28.3 36.0 Net debt/EBITDA (times) 0.7 0.6 0.3 0.3 0.3 Capex intensity (%) 16.1 17.9 14.7 14.0 13.2 Return on capital employed (%) 48.2 50.1 62.1 62.8 63.2 Vodacom Group Limited IR presentation | 5 September 2016 23

Dividend policy and payment history Current dividend payout is 90% of headline earnings per share The Company intends to pay out as much of its after tax profits as will be available after retaining such sums and repaying s uch borrowings owing to third parties as shall be necessary to meet the requirements reflected in the budget and business plan, t aking into account monies required for investment opportunities. There is no fixed date on which entitlement to dividends, arises and th e date of payment will be determined by the Board or shareholders at the time of declaration, subject to the JSE Listings Requirements. Dividend number Ex-dividend date Payment date Cents per share Policy payout (%) Actual payout (%) Interim dividend number 1 30 Nov 2009 7 Dec 2009 110 40 50 Final dividend number 2 28 Jun 2010 5 Jul 2010 175 40 60 Interim dividend number 3 29 Nov 2010 6 Dec 2010 180 60 60 Final dividend number 4 27 Jun 2011 4 Jul 2011 280 70 79 Interim dividend number 5 28 Nov 2011 5 Dec 2011 260 70 80 Final dividend number 6 18 Jun 2012 25 Jun 2012 450 90 117 Interim dividend number 7 26 Nov 2012 3 Dec 2012 355 90 90 Final dividend number 8 24 Jun 2013 1 Jul 2013 430 90 90 Interim dividend number 9 25 Nov 2013 2 Dec 2013 395 90 90 Final dividend number 10 23 Jun 2014 30 Jun 2014 430 90 94 Interim dividend number 11 24 Nov 2014 1 Dec 2014 375 90 90 Final dividend number 12 22 Jun 2015 29 Jun 2015 400 90 90 Interim dividend number 13 30 Nov 2015 7 Dec 2015 395 90 90 Final dividend number 14 20 Jun 2016 27 Jun 2016 400 90 90 Vodacom Group Limited IR presentation | 5 September 2016 24

Investor relations | 2016 Calendar

Reporting dates Roadshows/conferences

Date Event Location Date Event Location

14 November H1 2017 results released Vodacom/ 26-27 September RMB Big 5 conference Cape Town

Website

10 October UBS TMT conference Johannesburg

Mid-November Interims 2017 roadshow JHB/CT/UK/USA

Vodacom Group Limited IR presentation | 5 September 2016 25Thank you Vodacom Group Limited IR presentation | 5 September 2016

Definitions

Active customers Active customers are based on the total number of mobile customers using any service during the last three months. This includes

customers paying a monthly fee that entitles them to use the service even if they do not actually use the service and those customers who

are active whilst roaming.

Active data customers Number of unique users generating billable data traffic during the month. Also included are users on integrated tariff plans, or who have

access to corporate APNs, and users who have been allocated a revenue generating data bundle during the month. A user is defined as

being active if they are paying a contractual monthly fee for this service or have used the service during the reported month.

ARPU Total ARPU is calculated by dividing the average monthly service revenue by the average monthly active customers during the period.

Contribution margin Revenue less direct expenses as a percentage of revenue.

EBITDA Earnings before interest, taxation, depreciation and amortisation, impairment losses, profit/loss on disposal of investments, property, plant

and equipment, and intangible assets, profit/loss from associate and joint venture, restructuring cost and BEE income/charge.

Free cash flow Cash generated from operations less additions to property, plant and equipment and intangible assets, proceeds on disposal of property,

plant and equipment and intangible assets, tax paid, net finance charges paid and net dividends received/paid to minority shareholders.

HEPS Headline earnings per share.

International International comprises the segment information relating to the non-South African-based cellular networks in Tanzania, the Democratic

Republic of Congo, Mozambique and Lesotho as well as the operations of Vodacom International Limited and Vodacom Business Africa

Group (Pty) Limited and its subsidiaries.

MOU Minutes of use per month is calculated by dividing the average monthly minutes (traffic) during the period by the average monthly active

customers during the period.

Normalised growth (*) Adjusted for trading foreign exchange gains/losses and at a constant currency (using current year as base) (collectively ‘foreign exchange’).

Operating free cash flow Cash generated from operations less additions to property, plant and equipment and intangible assets other than licence and spectrum

payments and purchases of customer bases, net of proceeds on disposal of property, plant and equipment and intangible assets, other than

license and spectrum payments and disposals of customer bases.

South Africa Vodacom (Pty) Limited, a private limited liability company duly incorporated in accordance with the laws of South Africa and its subsidiaries,

joint ventures and SPV’s.

Traffic Traffic comprises total traffic registered on Vodacom’s mobile network, including bundled minutes, promotional minutes and outgoing

international roaming calls, but excluding national roaming calls, incoming international roaming calls and calls to free services.

Vodacom Group Limited IR presentation | 5 September 2016 27More information

Visit our website for more information

Follow us on social media

@vodacom

Facebook.com/vodacom

Contact us

VodacomIR@vodacom.co.za

+27 11 653 5055

http://www.vodacom.com/about-us/investors/investors-home

Vodacom Group Limited IR presentation | 5 September 2016You can also read