Vattenfall Investor presentation - 10 May 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Vattenfall

Investor presentation

10 May 2021

IMPORTANT NOTICE

NOT FOR DISTRIBUTION TO ANY PERSON OR ADDRESS IN THE U.S.

IMPORTANT: You must read the following before continuing. The following applies to the presentation materials following this page, and you are therefore advised to read this carefully before reading, accessing or making any other use of the presentation

materials. In accessing the presentation, you agree to be bound by the following terms and conditions, including any modifications to them any time you receive any information from us as a result of such access.

This presentation (the “Presentation”) has been prepared by Vattenfall AB (publ) (the “Issuer” or, together with its direct and indirect subsidiaries, the “Group”) solely for the purpose of providing the recipients with information in connection with the

contemplated offering of subordinated floating rate and fixed rate green capital securities by the Issuer, expected to be issued in May 2021 (the “Capital Securities”), and may not be disclosed, reproduced or redistributed in whole or in part to any other person.

The Presentation and the information herein is strictly confidential and may not be disclosed or distributed to any other person unless expressly agreed by Citigroup Global Markets Limited, Danske Bank A/S, Nordea Bank Abp, Skandinaviska Enskilda Banken

AB (publ), Svenska Handelsbanken AB (publ. and Swedbank AB (publ) (the “Joint Bookrunners”), except to such of the recipient’s directors, employees and professional advisors as the recipients take full responsibility for. This Presentation and the

information herein may not be used or relied upon for any other purpose or by any other party. This presentation is accompanied by a preliminary prospectus dated 10 May 2021 (the “Preliminary Prospectus”). The Preliminary Prospectus is subject to

completion and amendment and is furnished on a confidential basis only for the use of the intended recipient. The Preliminary Prospectus shall not constitute an offer to sell or the solicitation of an offer to buy any Capital Securities. Prospective investors

should not subscribe for any Capital Securities except on the basis of information contained in the final form of the prospectus (including the information incorporated by reference therein) to be prepared in connection with the offering of the Capital Securities.

This Presentation is for information purposes only and does not in itself constitute an offer to sell or a solicitation of an offer to buy any of the Capital Securities, and it does not constitute any form of commitment or recommendation in

relation thereto. No representation or warranty (expressed or implied) is made as to, and no reliance should be placed on, the fairness, accuracy or completeness of the information in the Presentation. None of the Issuer or any of its affiliates,

advisers, representatives or any of the Joint Bookrunners or any of their respective affiliates, employees, directors or representatives shall have any liability or responsibility whatsoever (in negligence, tort, contract or otherwise) for any loss,

damage of any kind (including, without limitation, damages for misrepresentation under the Misrepresentation Act 1967) or other results howsoever arising, directly or indirectly, from any use of, or reliance on, this Presentation or its contents

or otherwise arising in connection with this Presentation. Each of the Joint Bookrunners therefore disclaims any and all liability or responsibility relating to this Presentation including without limitation any express or implied representations

or warranties for statements contained in, and omissions from, the information herein, including its fairness, accuracy or completeness or for any other statement made or purported to be made in connection with the Issuer and nothing in this

document or at this Presentation shall be relied upon as a promise or representation in this respect, whether as to the past or the future. The Joint Bookrunners are acting solely in the capacity of an arm’s length counterparty and not in the

capacity of financial adviser or fiduciary of the Issuer. By attending a meeting where this Presentation is presented, or by reading the Presentation slides, you agree to be bound by the terms, conditions and limitations stated herein.

The Joint Bookrunners are not giving and are not intending to give financial, investment, legal or tax advice to any potential investor, and this Presentation shall not be deemed to be financial, investment, legal or tax advice from the Joint Bookrunners to any

potential investor. Investors should not subscribe for or purchase any financial instruments or securities on the basis of the information provided herein and acknowledge that each investor will be solely responsible for and rely on its own assessment of the

market and the market position of the Group and that it will conduct its own analysis and be solely responsible for forming its own view of the potential future performance of the Group. Hence, investors are encouraged to seek advice from their own legal, tax

and financial advisors and to exercise an independent analysis and judgement of the merits of the Group, to ensure that they understand the transaction and have made an independent assessment of the appropriateness of the transaction in light of their own

objectives and circumstances, including the possible risks and benefits of entering into such a transaction.

The information contained in this Presentation has not been independently verified and no legal due diligence has been conducted in connection with the preparation of this Presentation. In particular, no information in this Presentation has been independently

verified by the Joint Bookrunners or their advisors and the Joint Bookrunners and their advisors assume no responsibility for, and no warranty (expressed or implied) or representation is made as to, the accuracy, completeness or verification of the information

contained in this Presentation. Neither the Group nor the Joint Bookrunners or any of their parent or subsidiary undertakings or any such person’s directors, officers, employees, advisors or representatives (collectively, the “Representatives”) make any

representations as to the correctness, accuracy or completeness of this Presentation or the information herein. Further, certain financial information contained in this Presentation has not been reviewed by the Group’s auditor or financial expert. Hence, such

financial information might not have been produced in accordance with applicable or recommended accounting principles and may furthermore contain errors and/or miscalculations. The inclusion of financial information in this Presentation should not be

regarded as a representation or warranty by the Group or the Joint Bookrunners, or any of their respective Representatives as to the accuracy or completeness of such information’s portrayal of the financial condition or results of operations of the Group. The

Group is the source of the information contained in this Presentation and neither the Joint Bookrunners nor any of their Representatives shall have any liability (in negligence or otherwise) for any inaccuracy of the information set forth in this Presentation.

The recipient is responsible for undertaking its own analysis and assessment of the Group and a potential transaction and the information relating to the Group does not constitute a complete overview of the Group and must be supplemented by the reader

wishing such completeness. This Presentation is not intended to contain any appraisals or advice, and no statements herein are to be construed as such. This Presentation may contain forward-looking statements that reflect the Group’s current expectations or

estimates with respect to certain future events and potential financial performance. Such statements are only forecasts which are based on a number of estimates and assumptions that are subject to significant business, economic and competitive uncertainties

and no guarantee can be given that such estimates and assumptions are correct. An investment involves a high level of risk and several factors could cause the actual results or performance of the Group to be different from what may be expressed or implied

by statements contained in this Presentation.

This Presentation speaks as to the date hereof and does not purport to contain all the information needed to evaluate a potential transaction involving the Group. Neither the Group, nor the Joint Bookrunners or their Representatives represent or warrant that

there has been no change in the affairs of the Group since such date and neither the Group, nor the Joint Bookrunners or their Representatives undertake any obligations to review, confirm, update or correct any information included in the Presentation. The

Presentation may however be changed, supplemented or corrected without notification. The Group and the Joint Bookrunners or any of their Representatives, as applicable, expressively disclaims all and any liability arising directly or indirectly from the use of

this Presentation and the information herein.

2

The Joint Bookrunners and their Representatives may hold securities of the Group and may, as principal or agent, buy or sell such securities and have, or may in the future, engage in financing transaction and other transactions with the Group. Accordingly,

conflicts of interest may exist or may arise as a result of the Joint Bookrunners having previously engaged, or will in the future engage, in financing and other transactions with the Group and/or the Issuer. The Joint Bookrunners will be paid a fee by the Issuer

in respect of the placement of the Capital Securities.

The Presentation is not, and should not be considered, a prospectus for the purposes of Regulation (EU) 2017/1129 and has not been prepared in accordance therewith or in accordance with any other Swedish or foreign law or regulation. Accordingly, the

Presentation has not been, and will not be, examined, approved or registered by any supervisory authority. However, a prospectus relating to the admission to trading of the Capital Securities may be prepared and approved and will, in such case, be published

and available at the Swedish Financial Supervisory Authority’s website and at the Issuer’s website.

The information in this Presentation is not for release, publication or distribution, directly or indirectly, in or into the United States or any other jurisdiction in which such distribution would be unlawful or would require registration or other measures. No securities

referred to in this Presentation have been or will be registered by the Group under the U.S. Securities Act of 1933, as amended (the “Securities Act”) or the securities laws of any state of the United States. This Presentation may not be distributed into or in the

United States or to any “US person” (as defined in Rule 902 of Regulation S under the Securities Act) absent registration or pursuant to an applicable exemption from, or in transaction not subject to, the registration requirements of the Securities Act and in

compliance with any applicable securities laws of any state or other jurisdiction of the United Sates. In so far this Presentation is made or would cause any effect in the United Kingdom, this Presentation is only addressed to and directed at persons in the

United Kingdom who (i) are persons who have professional experience in matters relating to investments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”), (ii) are persons who are high

net worth entities falling within Article 49(2)(a) to (d) of the Order, or (iii) are other persons to whom this Presentation may otherwise lawfully be communicated (all such persons together being referred to as “Relevant Persons”). This Presentation must not be

acted on or relied on in the United Kingdom by persons who are not Relevant Persons. Any investment or investment activity to which this presentation relates is available only to Relevant Persons in the United Kingdom and will be engaged in only with such

persons. Further, the distribution of this Presentation and any purchase of or application/subscription for securities may be restricted by law in certain jurisdictions, and persons into whose possession this Presentation comes should inform themselves about,

and observe, any such restriction. Any failure to comply with such restrictions may constitute a violation of the applicable securities laws of any such jurisdiction.

The distribution of this Presentation and the placement of the Capital Securities in certain jurisdictions may be restricted by law. No action has been or will be taken to permit a public offering in any jurisdiction. Persons into whose possession this Presentation

comes are required to inform themselves about, and to observe, such restrictions. Any failure to comply with such restrictions may constitute a violation of the applicable securities laws of any such jurisdiction. The Group and the Joint Bookrunners disclaim any

responsibility or liability for the violations of any such restriction by any person.

MiFID II PRODUCT GOVERNANCE / PROFESSIONAL INVESTORS AND ECPs ONLY TARGET MARKET – Solely for the purposes of each manufacturer’s product approval process, the target market assessment in respect of the Capital Securities has led

to the conclusion that: (i) the target market for the Capital Securities is eligible counterparties and professional clients only, each as defined in Directive 2014/65/EU (as amended, “MiFID II”); and (ii) all channels for distribution of the Capital Securities to eligible

counterparties and professional clients are appropriate. Any person subsequently offering, selling or recommending the Capital Securities (a “distributor”) should take into consideration the manufacturers’ target market assessment; however, a distributor

subject to MiFID II is responsible for undertaking its own target market assessment in respect of the Capital Securities (by either adopting or refining the manufacturers’ target market assessment) and determining appropriate distribution channels.

UK MiFIR PRODUCT GOVERNANCE / PROFESSIONAL INVESTORS AND ECPS ONLY TARGET MARKET – Solely for the purposes of each manufacturer’s product approval process, the target market assessment in respect of the Capital Securities has

led to the conclusion that: (i) the target market for the Capital Securities is only eligible counterparties, as defined in the FCA Handbook Conduct of Business Sourcebook, and professional clients, as defined in Regulation (EU) No 600/2014 as it forms part of

domestic law by virtue of the European Union (Withdrawal) Act 2018; and (ii) all channels for distribution of the Capital Securities to eligible counterparties and professional clients are appropriate. Any distributor should take into consideration the

manufacturers’ target market assessment; however, a distributor subject to the FCA Handbook Product Intervention and Product Governance Sourcebook is responsible for undertaking its own target market assessment in respect of the Capital Securities (by

either adopting or refining the manufacturers’ target market assessment) and determining appropriate distribution channels.

PROHIBITION OF SALES TO EEA RETAIL INVESTORS – The Capital Securities are not intended to be offered, sold or otherwise made available to and should not be offered, sold or otherwise made available to any retail investor in the European Economic

Area (“EEA”). For these purposes, a retail investor means a person who is one (or more) of: (i) a retail client as defined in point (11) of Article 4(1) of MiFID II; or (ii) a customer within the meaning of Directive (EU) 2016/97, where that customer would not qualify

as a professional client as defined in point (10) of Article 4(1) of MiFID II.

Consequently no key information document required by Regulation (EU) No 1286/2014 (the “PRIIPs Regulation”) for offering or selling the Capital Securities or otherwise making them available to retail investors in the EEA has been prepared and therefore

offering or selling the Capital Securities or otherwise making them available to any retail investor in the EEA may be unlawful under the PRIIPs Regulation.

PROHIBITION OF SALES TO UK RETAIL INVESTORS – The Capital Securities are not intended to be offered, sold or otherwise made available to and should not be offered, sold or otherwise made available to any retail investor in the United Kingdom

(“UK”). For these purposes, a retail investor means a person who is one (or more) of: (i) a retail client, as defined in point (8) of Article 2 of Regulation (EU) No 2017/565 as it forms part of domestic law by virtue of the European Union (Withdrawal) Act 2018

(“EUWA”); or (ii) a customer within the meaning of the provisions of the Financial Services and Markets Act 2000 (the “FSMA”) and any rules or regulations made under the FSMA to implement IDD, where that customer would not qualify as a professional

client, as defined in point (8) of Article 2(1) of Regulation (EU) No 600/2014 as it forms part of domestic law by virtue of the EUWA.

Consequently no key information document required by the PRIIPs Regulation as it forms part of domestic law by virtue of the EUWA (the “UK PRIIPs Regulation”) for offering or selling the Capital Securities or otherwise making them available to retail

investors in the UK has been prepared and therefore offering or selling the Capital Securities or otherwise making them available to any retail investor in the UK may be unlawful under the UK PRIIPs Regulation.

This Presentation and any non-contractual obligations arising out of or in connection with it shall be governed by the substantive law of Sweden, without regard to its principles and rules on conflicts of laws. Any dispute, controversy or claim arising out of or in

connection with this Presentation is subject to the exclusive jurisdiction of Swedish courts, with the District Court of Stockholm (Stockholms tingsrätt) as court of first instance.

3

Vattenfall Investor Presentation

Agenda Speakers

1. Group overview Johan Gyllenhoff

Head of Finance and Group

2. Sustainability is fully integrated in our strategy Treasurer

3. Green financing

4. Financial highlights and hybrid offering

Annika Ramsköld

5. Appendix Head of Sustainability

4

Group overview

This is Vattenfall Activities in the Value Chain Active Inactive

Upstream Production Transmission Distribution Trading Retail Services

Main markets CO2 emissions & Renewable

In Brief 6.8 Million • Sweden capacity

Electricity customers 90 4 000

• Vattenfall is a leading European • Germany

3 500

energy company • Netherlands 3 000

1.8 Million 60

Mtonnes

• We want to make fossil-free living Heat customers • Denmark 2 500

MW

• United Kingdom 2 000

possible within one generation 30 1 500

3.3 Million 1 000

• We are driving the transition to a more Electricity 500

sustainable energy system through growth grid customers 0 0

in renewable production and climate

smart energy solutions for our customers 2.3 Million

Gas customers Installed renewable capacity (MW)

• 100 per cent owned by the Swedish CO2 emissions (Mtonnes)

State 19,859 Electricity generation EBITDA breakdown by

Employees

• Our long-term credit ratings are BBB+ breakdown by technology, 2020 segment, 2020

stable outlook by S&P and A3 negative Wind Customers & Solutions

Distribution

outlook by Moody’s 6%

10% 19%

Nuclear

Fossil 35% Heat 6%

20% SEK

112.8

46.5 bn

TWh 49%

20%

Wind

35%

Hydro Power Generation

6

Vattenfall’s value chain

Production Electricity distribution Sales of electricity, District heating Energy services and

heat and gas decentralised generation

Production from • Guarantees secure supply • Sells electricity, heat and • Drives the transformation Offers energy services

• Hydro via well-functioning gas to consumers and towards fossil-free heating • Heat pumps

distribution networks and business customers and cooling solutions

• Nuclear smart network solutions together with cities • Solar panels

• Focuses on various price

• Coal • Enables customers to feed and service models, and and regions • Charging solutions for

• Natural gas self-generated electricity gives customers the • One of Europe’s electric vehicles

into the grid (“prosumers”) opportunity to reduce their largest producers • Battery storage

• Wind

environmental impact and distributors of

• Solar • Network services

district heating

• Biomass • Smart meters

• Waste Provides marketplaces and

access to marketplaces

Actively phasing out where customers can buy

fossil-based production and sell electricity

7

Significant shift in production portfolio over the past 5 years

The shift has accelerated with large investments in renewables and phase out of fossil production

CAPEX by technology Electricity production mix CO2 emissions

SEK 30.8 bn SEK 33.9 bn 173.0 TWh 112.8 TWh

5.5% 83,8

20.1%

39.6% 48.6% 9.6%

71.7%

3.4% 35.2%

30.5%

22.8%

10.4% 12,1

5.7% 41.2%

19.5% 16.6% 25.3%

2015-16 2021-22 2015 2020 2015 3 2020 4

1 2

Other Hydro Wind Fossil Other11 Hydro Wind Fossil 2

CO2 emissions (Mtonnes)

CO2 emissions (Mtonnes)

Major investments in renewable projects Share of fossil production has been reduced …and with this our CO2 emissions

• Around SEK 23 billion of investments are planned dramatically… We sold the lignite business in 2016, which reduced

for new wind farms, both onshore and offshore • Strong wind growth: 3.5 GW installed capacity; our CO2 footprint dramatically

• Recent milestones: ~ 3 GW under construction and >4 GW in • We continue to identify further actions such as

• Final investment decision for Hollandse Kust development retiring coal fired power plants earlier than

Zuid 1-4 offshore wind farm in the • Increased focus on decentralised production, planned (such as Hemweg-8 in the Netherlands

Netherlands, the world’s largest offshore wind storage and EV charging

farm when commissioned in 2023 and Moorburg in Germany)

• Coal-fired production has been phased out such • We are also phasing out coal from all of our

• Major onshore projects in the Nordics and the as Reuter C in Berlin, Moorburg in Hamburg and

UK (Blakliden & Fäbodberget, South Kyle) operations by 2030, at latest

Hemweg-8 in the Netherlands

• Proof of concept in solar & batteries ready for

scaling up and innovative solutions such as

co-location with wind farms (Haringvliet,

Battery at Pen y Cymoedd)

1 Other includes nuclear, solar & batteries (CAPEX only) & biomass

2 Includes hard coal and gas

4 Pro rata values, corresponding to Vattenfall’s share of ownership

3 Consolidated values for 2015. Consolidated emissions are approximately 0.5% higher 8

than pro rata emissions, corresponding to Vattenfall’s share of ownership

Our milestones towards fossil-free living

within one generation

2023 2024 2025 2026 2030 2035

We provide electric 750 MW of We reduce CO2 Our HYBRIT We reduce CO2 We are not done,

charging for 1 billion additional, flexible intensity by >40% partnership intensity by nearly more to come…

fossil-free kilometers hydro capacity from 2017 produces fossil-free 70% from 2017

annually enables more steel

renewable We generate fossil- We have completely

generation free electricity to phased out coal

power 30 million

homes We operate a bio-

energy carbon

We provide 7 TWh of capture and storage

renewable energy plant

through corporate

PPAs.

9Sustainability is fully

integrated in our strategy

Enable fossil-free living within one generationEurope continues to be a highly attractive growth market

Despite significant ramp-up in renewables, much more growth is expected in the coming decade

Increasing demand and phase-out of coal Double-digit growth across renewable technologies until 20301

gives plenty of room for growth in Europe Europe ROW2

Offshore wind (GW) Onshore wind (GW) Solar (GW)

Increased demand

250 974 2077

driven by 1000 2100

Investment need electrification trend 194

200

750 664

56% 1400 1239

150

79%

91 500 58%

Expected lifetime 100 348

~20-25 years 79%

700

448

250 62%

50 44%

Significant 22

42% 74%

phasing-out 21%

39% 21%

0 0 0 26%

Today ~25 year horizon 2018 2025 2030 2018 2025 2030 2018 2025 2030

Europe 17 GW 46 GW 97 GW 136 GW 279 GW 367 GW 115 GW 255 GW 379 GW

ROW 5 GW 45 GW 97 GW 212 GW 405 GW 588 GW 333 GW 1057 GW 1,555 GW

1 Source: Bloomberg NEF

2 ROW excludes China 11Energy transition to spur dramatic growth in electricity

demand in Sweden

Electrification, growth in renewable production capacity and ageing assets call for large grid investments

Electricity demand set to grow due to Installed wind capacity continues to Existing grid assets are increasingly in

electrification and new electricity grow need of reinvestments

intensive businesses • More and more capacity will be • There was a large build out of grid assets

• Electrification of industry and transports to intermittent and decentralised in 1970-1990. These assets are now

increase total electricity demand • Wind production is set to continue the reaching the age when they need to be

growth in Sweden, mainly in the North and reinvested in

• New businesses such as data centres and

battery factories are also likely to have a off the coast in Southern Sweden which • This is on top of the need to make new

significant impact increases the need for grid capacity investments in the grid to accommodate

more renewable energy and electrification

• Efficiency improvements in the residential

sector only have a small mitigating effect

on total demand

Forecast – Change in electricity demand (Sweden)1 Forecast – wind power generation (Sweden)2 Asset age structure – Vattenfall Eldistribution3

50 140 4 10 years 20 years 30 years

40 120 40 years 50 years

100 3

30

BSEK

TWh

TWh

80

20 2

60

10 40

1

0 20

2020 2025 2030 2035 2040 2045

-10 0 0

2020 2030 2040

Housing Datacenter etc Industry Transportation 1930 1940 1950 1960 1970 1980 1990 2000 2010

1 Source: Nepp, Färdplan för fossilfri el, Aug 2019

2 Source: Svensk vindenergi, Färdplan 2040, Dec 2020

3 Asset 12

base per 2020-01-01A strategy based on an “integrated utility logic”

To enable our goal of fossil-free living within one generation

We believe being active in the whole value chain is strategically important:

It increases our competitive advantage in eg. wind auctions, by

enabling stable revenues through Corporate PPAs with our customers

Access to renewable volumes on the customer side differentiates us

from competitors as fossil-free electricity becomes more scarce

The ability to optimise dispatch across both customer loads and

supply brings optimal value of a total portfolio

Diversifying and reducing total portfolio risk means lower cost of

capital and an ability to take on more debt

13To enable fossil-free living sets a focus on the full value chain

CO2 emissions 2020

Suppliers Own operations Customers

5

Mtonnes

12

Mtonnes

12

Mtonnes

Reducing emissions Climate smart

Supplier dialogues

in line with scientific solutions for homes

and requirements

limits and cities

Lifecycle Growth in renewables City

Assessments partnerships

Reducing emissions

Industry Environmental

from employee

collaborations product offerings

travelling

14Vattenfall’s 2030 emissions targets have been approved by

the Science Based Target initiative (SBTi)

Projected Vattenfall Scope 1 & 2 CO2 intensity vs. SBT scenarios Vattenfall Total 2017 Scope 3 Emissions

16

14

150 2017 2030 target set at 20% reduction by 2030

93 gCO2e, a 38% 12

130 reduction 30% reduction

153 10

MtCO2e

gCO2e / kWh

110 50% reduction in business

8 by 2030 travel by 2030

90 6

70 67 4

50 2

30 0

2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 Use of sold Fuel- and Waste Capital goods Upstream Other

products energy- generated in transport and

Vattenfall SBT 2° SBT 1.5° SBTi Paris related operations distribution

activities

• Target set for 38% reduction from 2017-2030; more ambitious target • Science-based target set for 20% reduction of emissions from use of

under discussion sold products; more ambitious target under discussion

• New 2025 CO2 intensity KPI set for 86 gCO2e/kWh, in line with • Programmes are in place to reduce emissions in other categories but

1.5°trajectory we have not included them in the target for the sake of simplicity.

• Based on planned coal phase out by 2030 and expansion in wind + • We will focus on further expanding non-fossil heating solutions such as

solar heat pumps, solar thermal, non-fossil gas, and others

• Requires continued successful execution of major projects

15Committed to electrification of society

All sectors need to contribute to the transition and electrification will be a key abatement option for reaching the

national and EU targets by 2030

Total green house gas emissions Transports

Sweden1 (2018) 52 MtCO2e MtCO2e

3 2 1 16

10

7

5 Cars Heavy Trucks Other Road Air,

Transports Railroad,

7 Shipping

16 Industry

64% of total MtCO2e

Emissions 17

5

3

6 3

17

Iron & Steel Cement Refineries Other

Ambitious EU and national targets are forcing emission trajectories downwards. This will accelerate the energy transition and

electrification will be a key abatement option for reaching 2030 targets in transport, industry and heat sectors. In turn, these sectors

drive demand for fossil-free electricity & heat, grid capacity and flexible solutions.

1 Source: Swedish Environmental Protection Agency 16Electricity - from a power source to a source of innovation

Together with our partners, we pave the way for a new generation of transports, industries and materials

Research project for Cooperation in large Feasibility study on Electrification of Co-operation for e-

a carbon dioxide- scale bio-diesel electrified mines and smelters mobility

free steel industry production cement production

Green guaranteed Support of a major Northern Europe’s Powering Storage projects at a

energy delivery enterprise for largest charging sustainable number of wind parks

large customers, battery production network for e- datacenters

e.g. in Sweden vehicles

17Green financing

Future investments focused on renewables

Total capex Growth capex per Growth capex per country

2021-2022 technology 2021-2022 2021-2022

6% 10%

18% 9%

11% 29%

57bn 14% 32bn 32bn

SEK SEK SEK

57%

25%

22%

71%

28%

Growth, 32 bn SEK Wind power, 23 bn SEK Netherlands, 9 bn SEK

Maintenance, 14 bn SEK Electricity distribution, 4bn SEK Denmark, 9 bn SEK

Heat supply, 3 bn SEK UK, 7 bn SEK

Replacement, 10 bn SEK

Other 1, 2 bn SEK Sweden, 4 bn SEK

Empty Empty Germany, 3 bn SEK

Empty

1 Mainly charging solutions, solar and battery projects, decentralised solutions and the

19

Hybrit projectVattenfall’s green bond framework

Use of proceeds - eligible categories with examples of technologies

Renewable energy and related infrastructure Energy efficiency

• Wind energy • Hydro power

• Solar energy • Smart grids/meters

• Biomass • Fossil-free1 district heating and cooling

• Geothermal • Energy recovery

• Hydrogen

Electrification of transport and electrification of heating Industry projects

• Infrastructure for electric vehicles • Activities enabling the transformation to fossil-free1 production

• Power to Heat

1Fossil-free: not depending on fossil fuels for its own operations (e.g. for Vattenfall

20

no fossil fuels for energy generation and no fossil products to customers)Recent investment projects

Kriegers Flak Princess Ariane Hollandse Kust Zuid 1-4 HYBRIT

• Will be Denmark’s largest • Largest onshore wind farm in • Will be the world's largest • Pilot project in collaboration

offshore wind farm the Netherlands offshore wind farm once with SSAB and LKAB for

• Scheduled to be operational • Electricity generated by the completed in 2023 development of a hydrogen-

by end of 2021 wind farm is used to power a • Project without subsidies in the based process for fossil-free

nearby data centre Netherlands steel production

• The wind farm is estimated to

reduce CO2 emissions by 325 • Saving approximately 350 • Renewable output equivalent • If implemented at full scale,

ktonnes per year ktonnes of CO2 emissions per to the annual consumption of HYBRIT has the potential to

year over two million Dutch reduce Sweden’s C02

• Capacity: 605 MW emissions by 10% and

• Completed in 2020 households

• Total investment: 7,600 MDKK Finland’s by 7%

• Capacity: 301 MW • Capacity: 1,500 MW

• Total investment: 858 MSEK

• Total investment: 394 MEUR • Total investment: 2,600 MEUR

Note: See Appendix for more information on the projects 21A leader in the European renewables transition

Strong position within offshore wind and extensive European pipeline ahead

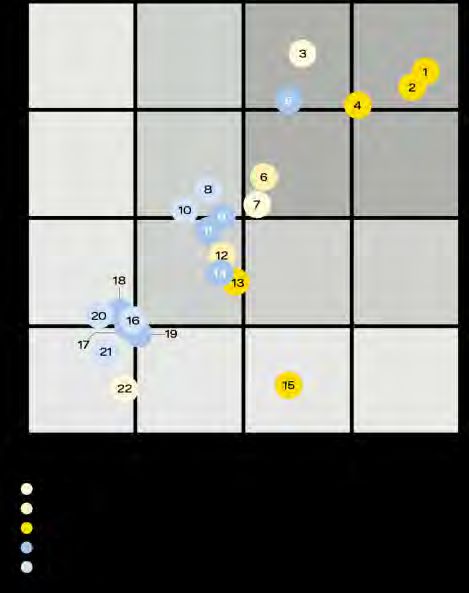

Geographical overview – we develop, construct and operate Competitive landscape – Offshore capacity involved (GW)²

wind and solar farms in our core European markets1

0,0 5,0 10,0 15,0 20,0 25,0 30,0

Sweden

In operation: 328 MW RWE 5,0 13,4 0,9

Under construction: 353 MW Orsted 8,0 9,2 10,3

UK Denmark In development: 193 MW SSE 0,5 11,9 0,0

In operation: 1,083 MW In operation: 802 MW Vattenfall 2,1 8,8 0,0

Under construction: 240 MW Under construction: 605 MW Equinor 1,2 7,6 10,1

In development: 3 600 MW In development: 344 MW 5 Iberdrola 1,5 4,6 14,2

12 EDF 0,7 4,7 2,4

Aberdeen Bay EnBW 0,9 3,9 2,1

Vesterhav Macquarie 0,7 3,9 7,5

Horns Rev 3 Shell 0,8 1,0 7,0

Lillgrund

Sandbank Horns Rev 1

Ormonde Danish Kriegers Flak Operational Pipeline (Europe) Pipeline (Non-Europe)

7 Dan Tysk

² Minority shares included as 100%, sorting based on operational projects and European pipeline

Norfolk Boreas

Alpha Ventus Netherlands Source: 4C Offshore Wind Farm Database

15 In operation: 723 MW

Norfolk Vanguard

Under construction: 1,699 MW Under construction and pipeline1

In development: 57 MW

Kentish Flats

Kentish Flats Extension

Thanet

2 ~ 3 GW > 4 GW ~ 1 GW ~ 200 MW

Offshore wind project Hollandse Kust Germany

in operation Zuid 1-4

In operation: 658 MW Wind projects

Offshore wind project in Wind projects Solar projects Batteries

under

construction/development NoordzeeWind in development in development pipeline

construction

Number of onshore wind

farms country-wide

22

1 As of December 2020Financial highlights and

hybrid offeringFinancial targets

Targets over a business

Financial targets cycle1 FY 2020 FY 2019 Comment

Return on capital employed decreased to 5.8%,

Return on capital employed: which is below the target of 8%, mainly owing to

Profitability 5.8% 8.5%

≥8%2 impairment losses related to the Moorburg power

plant in Hamburg

FFO/adjusted FFO/adjusted net debt increased to 28.8% in 2020,

Capital structure net debt: 28.8% 26.5% mainly owing to lower adjusted net debt resulting

22%–27% from higher cash flow from operations

The Annual General Meeting decided on a dividend

Dividend:

of SEK 4 billion equivalent to 62% of profit for the

Dividend policy 40%–70% of the year’s profit SEK 4.0 bn SEK 3.6 bn

year attributable to the owner of the parent

after tax

company for 2020

1 5–7 years

2 The key ratio is based on average capital employed 24Credit ratings overview

Long term rating: A31 Long term rating: BBB+1

Short term rating: P-2 Short term rating: A-2

Outlook: Negative Outlook: Stable

Latest publication: 4 February 2021 Latest publication: 4 February 2021

• “Most of Vattenfall’s operating segments were overall stable and the • “Vattenfall managed to keep its operating performance relatively

company showed a high degree of resiliency throughout 2020. “ unchanged in 2020 compared with 2019, despite record low power

• “The company's overall solid credit metrics were supported by a prices, which we view as a support for the current rating.”

combination of (1) resiliency in its EBITDA generation (2) the • “Profitability continues to be underpinned by its diversified earnings

company's decision to halve its dividend payment last year (3) a very base, with increased contributions from the heat business divisions

favorable movement in margins calls affecting working capital, which partly offsetting the lower contribution from its power generation

subsequently improved the company's reported net debt figure (inflow segment, which was also supported by hedges in place.”

of SEK 12.6 billion during last year, whereas 2019 saw an outflow of

• “We anticipate that Vattenfall will gradually benefit from a recovery of

SEK 20.7 billion).”

Nord pool system spot prices in the Nordic region.”

• “We expect Vattenfall's credit metrics to weaken in 2021 as power • “Although a continued stronger-than-expected financial risk profile

prices remain at low levels and with the company having locked in could lead to upside rating pressure, we believe that Vattenfall's credit

69% of its Nordic output for the year at €28/ MWh (against achieved ratios will soften over 2021-2022. This is because investments are set

prices of €31/ MWh during 2020). In addition, Vattenfall's heavy to increase to about SEK 57 billion over 2021 and 2022, up from SEK

capital expenditure programme - amounting to net expenditures of 23.6 billion in 2020.”

SEK 57 billion over 2021 and 2022 - will weaken free cash flows in

the current year.”

1 Rating factors in a one notch uplift given that Vattenfall is 100% owned by the Swedish state 25Transaction rationale

Supports commitment to solid investment grade rating. Replacement of existing SEK 6bn

NC2022 hybrid securities and further strengthening of the balance sheet

Issuance under our Green Bond Framework reinforces sustainability commitment connected

to funding activities

Provides cost efficient non-dilutive equity-like capital to support our fossil-free living within

one generation strategy

26Green Hybrid Structural Overview

Issuer ▪ Vattenfall AB (publ)

Issuer Ratings* ▪ A3 (Negative) by Moody’s / BBB+ (Stable) by S&P

Expected Instrument Ratings* ▪ Baa2 by Moody’s / BB+ by S&P

Ranking ▪ Direct, unsecured and subordinated, ranking senior to any share capital and pari passu with Vattenfall’s outstanding hybrids

Expected Equity Credit ▪ 50% with Moody’s (Basket C) until Year [52] / 50% with S&P (Intermediate) until Year [7]

Currency / Size ▪ SEK benchmark

Maturity Date ▪ [●] 20[83]([62] years) / [7] NC [●] 20[28]

First Reset Date ▪ [●] 20[28] (Year [7])

Tranche FRN FXD

▪ On any date in the 6-month period prior to and including the 20[28] Call Date ([●] May 20[28]) and ▪ On any date in the 6-month period prior to and including the First Reset Date ([●] May 20[28]) and

Optional Redemption every quarterly Interest Payment Date thereafter, at par, together with any Arrears of Interest and any every annual Interest Payment Date thereafter, at par, together with any Arrears of Interest and any

other accrued and unpaid interest other accrued and unpaid interest

▪ 3mSTIBOR + Margin (initial credit spread + any relevant step-up(s)) ▪ [•]% fixed rate until the First Reset Date, payable annually in arrear on [●] May in each year

Coupon ▪ Coupons payable quarterly in arrear on [●] February, [●] May, [●] August and [●] November in each ▪ Reset on the First Reset Date and every 5 years thereafter to the then prevailing 5 Year SEK Mid-

year Swap Rate + Margin (initial credit spread + any relevant step-up(s))

▪ 25bps on [●] May 20[33] (Year [12]) (the “20[33] Step-up Date”)

Coupon Step-up Dates

▪ Additional 75bps on [●] May 20[48] (Year [27]) (the “20[48] Step-up Date”)

▪ At the Issuer’s sole discretion at any time

▪ Arrears of Interest will be cumulative and compounding

▪ Arrears of Interest may be paid (in whole or in part) at any time but will be mandatorily payable (in whole only) (i) on any Interest Payment Date in respect of which the Issuer does not elect to defer, (ii) on the date on

which the Capital Securities are redeemed or repaid; and (iii) upon any of the following events (subject to customary carve-outs):

Optional Interest Deferral a. Declaration or payment of any distribution or dividend or any other payment made by the Issuer on its share capital or any other obligation of the Issuer which ranks or is expressed by its terms to rank

junior to the Capital Securities or by the Issuer or any subsidiary of the Issuer, as the case may be, on any Parity Securities;

b. Redemption, repurchase, repayment, cancellation, reduction or other acquisition by the Issuer or any subsidiary of the Issuer of any shares of the Issuer or any other obligation of the Issuer which ranks

or is expressed by its terms to rank junior to the Capital Securities; and/or

c. Redemption, repurchase, repayment, cancellation, reduction or other acquisition by the Issuer or any subsidiary of the Issuer of any Parity Securities,

▪ Vattenfall will have the right to redeem all of the Capital Securities at any time upon the following events:

a. Tax Deductibility Event / Rating Methodology Event - at 101% until 6 months prior to the 20[28] Call Date (FRN tranche) / 6 months prior to the First Reset Date (FXD tranche), at par thereafter

Special Redemption Events

b. Substantial Repurchase Event (≥75%) / Withholding Tax Event – at par

c. Make-whole – at the make-whole redemption amount

▪ Subject to applicable law, no Holder may exercise, claim or plead any right of set-off, compensation or retention in respect of any amount owed to it by the Issuer in respect of, or arising under or in connection with,

No Set-Off

▪ the Capital Securities and each Holder shall, by virtue of its holding, be deemed to have waived all such rights of set-off, compensation or retention

Substitution & Variation ▪ Yes, in lieu of redemptions upon a Tax Deductibility Event, Rating Methodology Event or Withholding Tax Event; subject to certain preconditions (including terms not materially less favourable to Holders)

Replacement Language ▪ Intention-based (non-binding), subject to customary carve-outs

Denominations ▪ SEK 2,000,000 + SEK 1,000,000

Governing Law ▪ Swedish law

▪ The Issuer intends to allocate an amount equal to the net proceeds of the issue of the Capital Securities to the financing or refinancing of a portfolio of new or existing Eligible Green Projects that meet the

Use of Proceeds

requirements of the Issuer’s Green Bond Framework available on its website, as applicable from time to time

Listing ▪ Nasdaq Stockholm

* Rating at the time of issuance. A security rating is not a recommendation to buy, sell or hold securities and should be evaluated

independently of any other rating. The rating is subject to revision or withdrawal at any time by the assigning 27

rating organization. Please refer to the Prospectus for full Terms & ConditionsDebt repurchase / Tender Offering

▪ SEK 3bn Fixed Rate Reset ▪ SEK 3bn Floating Rate Reset

Description

Capital Securities due 2077 Capital Securities due 2077

Summary

ISIN ▪ XS1205627547 ▪ XS1205625251

▪ Interest Payment Date falling in

Vattenfall has invited holders of its

First Call Date ▪ 19 March 2022 outstanding SEK Fixed and Floating Rate

March 2022 (21 March 2022)

Outstanding Principal Reset Capital Securities to tender such Notes

▪ SEK 3,000,000,000 ▪ SEK 3,000,000,000

Amount for cash

Purchase Price ▪ 102.16% ▪ 101.52%

• The rationale of the tender offer, and the

Amount subject to the

▪ Any and all intended new notes, is to optimise Vattenfall’s

Offer

cost of debt and balance sheet structure and

▪ If 80% or more of the principal amount of the notes has been repurchased enable investors to free up cash to invest in

Clean-up and cancelled, Vattenfall may redeem all of the remaining notes at their the New Capital Securities

principal amount with accrued and unpaid interest.

• Vattenfall intends to cancel any notes

▪ When considering allocations in the new notes, Vattenfall may give

preference to holders of the SEK Subordinated Capital Securities who have

purchased pursuant to the offer

Priority Allocations

validly tendered or given a firm intention to tender their holdings pursuant to

the tender offer • The tender offer commences on 10 May 2021

▪ Lucid Issuer Services Limited

and will expire on 20 May 2021, with

Tender Agent ▪ Tel: +44 20 7704 0880 settlement expected on 26 May 2021

▪ Email: vattenfall@lucid-is.com

Dealer Managers ▪ Citi, SEB and Swedbank

28Vattenfall key highlights

BBB+ stable outlook

by S&P and A3 100% Owned by

negative outlook by Swedish State

Moody’s

A leading European Stable and predictable

energy company with cash flow from

activities across the electricity distribution

value chain and district heating

Experienced player in

Leading towards renewables and one

sustainable production of the leaders in wind

power generation

Significant growth in

A significant

renewable production

transformation has

and climate smart

already happened

energy solutions

29Appendix

Financial overview

Vattenfall Q1 Results 2021

Financial highlights

Key data Key developments

SEK bn Q1 2021 Q1 2020

Net Sales 45.9 48.2 • Net sales decreased by SEK 2.2 bn to SEK 45.9 bn

mainly due to negative currency effects (-1.8 bn).

EBITDA 17.7 16.9 Lower sales volumes in the Netherlands and the

Underlying operating profit (EBIT) 12.1 10.2 B2B segment in France had an additional impact

EBIT 13.4 12.3

• Underlying EBIT increased by SEK 1.9 bn mainly

due to higher achieved prices, higher hydro power

Profit for the period 10.4 6.9 generation and higher realised trading result.

Funds from Operations (FFO) 14.0 12.2

Higher contribution from Heat also had a positive

impact, mainly due to the closure of Moorburg

Cash flow operating activities 11.1 -8.5

• Profit for the period increased to SEK 10.4 bn. The

Net debt 43.9 81.6 increase stems in addition to the increase in

underlying operating profit, from higher returns from

Adjusted net debt 112.2 148.3

the Nuclear Waste Fund

Adjusted net debt/EBITDA1 (times) 2.4 3.2

• ROCE was 5.9% mainly due to impairments made

Financial targets in 2020

ROCE1 (≥8%) 5.9 9.4 • FFO/Adjusted net debt (AND) increased to

32.8%, driven primarily by a decrease in AND. The

FFO/adjusted net debt1 (22-27%) 32.8 25.2 decrease mainly stems from positive cash flow after

investments which was supported by SEK 25 bn in

positive working capital flows (mainly margin calls)

1 Last 12-month values 32Development of underlying EBIT Q1 2021

Increase from Power Generation, Heat and Customers & Solutions

Change in Q1 2021 vs. Q1 2020 Breakdown per operating segment Highlights

SEK bn SEK bn

• Customers & Solutions: More customers in

Underlying EBIT 2020 10.2 12.1 Germany and lower temperatures in the

1.2

Nordics

Customers & Solutions 0.2

10.2 • Power Generation: higher achieved prices,

Customers & Solutions 1.0 higher hydro generation and higher realised

earnings from trading. Partly countered by

Power Generation 1.8 lower nuclear power generation due to

6.3 closure of Ringhals 1

Wind -0.4 Power Generation 4.6 • Wind: low wind speeds and more

maintenance work

Heat 0.5 • Heat: lower opex and depreciation due to

closure of Moorburg and higher heat sales

Wind 2.1 1.8 because of lower temperatures and a

Distribution -0.3 growing customer base. New plant Marzahn

Heat 0.9 1.4 and Lichterfelde fully in operation also

Net other effects 0.1 contributed

Distribution 2.1 1.8 • Distribution: lower margin in the Swedish

Underling EBIT 2021 12.1 -0.5 -0.4 operations due to lower prices in the local

Other

Q1 2020 Q1 2021

network

33Cash flow development Q1 2021

Higher working capital mainly due to seasonal effects within Customers & Solutions and Heat

SEK bn

17.7 -1.1

-1.2

0.1 -1.6

14.0 -2.9

11.1 -2.3

8.8 -3.1

-0.1 5.7

EBITDA Tax paid Interest Capital Other1 FFO Change Cash Maintenance Free Growth Divestments, Cash flow

paid/received, gains/ in WC flow from and cash flow investments net before

net losses, net operating replacement financing

activities investments activities

Main effects

• Change in working capital mainly driven by change in operating receivables and operating liabilities attributable to seasonal effects in the Customers &

Solutions and Heat operating segments (SEK -5.4 bn), changes related to CO2 emission allowances (SEK -2.6 bn) and an increase in inventories (SEK -

0.4 bn). Partly countered by the net change in margin calls (SEK 4.9 billion)

• Growth investments mainly related to wind power

1 ”Other” includes non-cash items included in EBITDA, mainly changes in fair value of

34

commodity derivativesDebt maturity profile1

SEK bn 31 Mar. 31 Dec.

2021 2020

20,5

Duration (years) 4.7 3.8

Average time to maturity (years) 6.5 5.1

Average interest rate (%) 2.8 3.4

Net debt (SEK bn) 43.9 48.2

Available group liquidity (MSEK) 43.3 50.8

10,2 Undrawn committed credit facilities

9,0 20.5 23.1

(MSEK)

7,0

6,0 6,1

5,2 5,2 5,2 5,5

3,8

Cumulative maturities excl. undrawn back-up facilities

1,0

0,2 0,3 0,0 0,0 2021- 2024- From

2023 2026 2027

2021 2023 2025 2027 2029 2031 2033 2035 2037 2039 2041

Debt incl. hybrid capital 17.3 15.5 31.9

Hybrid capital (first call date) Debt (excl. hybrid cap) Undrawn back-up facilities % of total 27% 24% 49%

1 Short term debt (Repo’s and Commercial paper: 8.9), loans from associated companies,

minority owners, margin calls received (CSA) and valuation at fair value are excluded. Currency

35

derivatives for hedging debt in foreign currency are included.Price hedging

Vattenfall continuously hedges its future electricity generation through sales in the forward and futures markets. Spot prices

therefore have only a limited impact on Vattenfall’s earnings in the near term

Estimated Nordic1 hedge ratio (%) and indicative prices Achieved prices2 - Nordic portfolio

69% Q1 2021 Q1 2020 FY 2020

33 27 31

56%

Sensitivity analysis – Continental3 portfolio

Market +/- 10% price impact on future profit

25% quoted before tax, MSEK4

Observed yearly

2021 2022 2023

volatility

Electricity +/- 251 +/- 417 +/- 1,574 20% - 27%

2021 2022 2023 Coal -/+ 42 -/+ 30 -/+ 14 19% - 21%

Average Gas -/+ 39 -/+ 106 -/+ 774 19% - 28%

indicative Nordic 28 28 26

hedge prices in CO2 -/+ 33 -/+ 55 -/+ 396 50% - 51%

EUR/MWh

1Nordic: SE, DK, FI 3Continental: DE, NL, UK.

4 The denotation +/- entails that a higher price affects operating profit favorably, and -/+ vice 36

2Achieved prices from the spot market and hedges. Includes Nordic (SE, DK, FI) hydro,

nuclear and wind power generation versaLiquidity position

Facility size,

Group liquidity SEK bn Committed credit facilities EUR bn SEK bn

Cash and cash equivalents 18.2 RCF (maturity Nov 2023) 2.0 20.5

Short term investments 29.3 Total undrawn 20.5

Reported cash, cash equivalents & short 47.5

term investments

Debt maturities2 SEK bn

Unavailable liquidity1 -4.2 Within 90 days 0

Available liquidity 43.3 Within 180 days 2.0

1 German nuclear ”Solidarvereinbarung” 1.2 SEK bn, Margin calls paid (CSA) 2.1 SEK bn,

Insurance “Provisions for claims outstanding” 0.8 SEK bn

2 Excluding loans from minority owners and associated companies 37Breakdown of gross debt

Total debt: SEK 91.8 bn (EUR 9.0 bn)

External market debt: SEK 80.1 bn (EUR 7.8 bn)

Debt issuing programmes Size (EUR bn) Utilization (EUR bn)

EMTN 42% EUR 10bn Euro MTN 10.0 3.4

EUR 4bn Euro CP 4.0 1.0

Hybrid capital 21%

Total 14.0 4.4

Loans from minority shareholders 12%

Commercial paper / Repo 10%

Lease 7%

• All public debt is issued by Vattenfall AB

Margin calls (CSA) 4% • The main part of debt portfolio has no currency exposure that

has an impact on the income statement. Debt in foreign

Bank loans 2% currency is either swapped to SEK or booked as hedge against

net foreign investments.

Other liabilities 1% • No structural subordination

Loans from associated companies 0%

1 EMTN= Euro Medium Term Notes 38Reported and adjusted net debt

Reported net debt 31 Mar. 31 Dec. Adjusted net debt 31 Mar. 31 Dec.

(SEK bn) 2021 2020 (SEK bn) 2021 2020

Hybrid capital -19.7 -19.3 Total interest-bearing liabilities -91.8 -104.8

Bond issues and liabilities to credit institutions -40.8 -49.6 50% of Hybrid capital 9.9 9.7

Commercial papers and Repos -8.9 -13.3 Present value of pension obligations -40.4 -43.8

Liabilities to associated companies -1.0 -0.7 Wind & other environmental provisions -10.9 -10.6

Liabilities to minority shareholders -10.8 -10.9 Provisions for nuclear power (net) -36.4 -37.8

Lease liabilities -6.4 -6.0 Margin calls received 3.3 4.1

Other liabilities -4.2 -4.9 Liabilities to minority owners due to consortium

10.8 10.9

agreements

Total interest-bearing liabilities -91.8 -104.8

= Adjusted gross debt -155.5 -172.3

Reported cash, cash equivalents & short-term

47.5 56.2

investments Reported cash, cash equivalents

47.5 56.2

& short-term investments

Loans to minority owners of foreign subsidiaries 0.4 0.4

Unavailable liquidity -4.2 -5.4

Net debt -43.9 -48.2

= Adjusted cash, cash equivalents & short-term

43.3 50.8

investments

= Adjusted net debt -112.2 -121.5

39Operating segment overview FY 2020

Operating segments Customers & Solutions Power generation

We report our operations broken down by the Responsible for sales of electricity, gas and Responsible for Vattenfall’s hydro and nuclear

Group’s operating segments: Customers & energy services in all of Vattenfall’s markets power operations, maintenance services

Solutions, Power Generation, Wind, Heat, and • A market leader in Sweden with nearly 900,000 business, and optimisation and trading

Distribution. The operating segments reflect our electricity contracts operations, including certain large business

Business Area organisational structure except for • A market leader in the Netherlands with 3.8 customers

the Power Generation segment, which is divided million electricity and gas contracts • Operates a portfolio with 5.5 GW4 nuclear

into the Generation and Markets Business Areas • Leading position as electricity supplier in Berlin capacity and 11.5 GW hydro power capacity

and Hamburg across Sweden, Finland and Germany

• Challenger position in sales of electricity in • One of Europe’s largest providers of fossil-free

Number of Employees as of 31 Denmark, Finland and France and in France also electricity, with 39.7 TWh from hydro power and

December 20201 of gas 39.3 TWh from nuclear power

• Operates 22,400 EV charging points in Sweden, • Provides professional asset optimisation services

Germany and the Netherlands and market access, and a leading player in PPA

Customers and Solutions 2,971 markets in northwest Europe

Power Generation 7,474

Wind 1,104

Underlying Operating Profit3: SEK 2,146 mn Underlying Operating Profit: SEK 14,670 mn

Heat 3,213 (8% of total) (54% of total)

External Net Sales: SEK 84,661 mn External Net Sales: SEK 36,597 mn

Distribution 2,366 (53% of total) (23% of total)

EBITDA: SEK 2,832 mn EBITDA: SEK 23,144 mn

(6% of total) (49% of total)

Other2 2,731

1 Full-time equivalents

2 Pertains mainly to Staff Functions and Shared Service Centres

3 Numbers reflect FY 2020 40

4 Excluding Ringhals 1 nuclear reactor that was closed at the end of 2020Operating segment overview FY 2020 (Cont’d)

Wind Heat Distribution

Responsible for development and operation of Responsible for Vattenfall’s heat operations Responsible for Vattenfall’s electricity

Vattenfall’s wind farms as well as large-scale including sales, decentralised solutions and distribution operations in Sweden, Germany

and decentralised solar power and batteries gas-fired condensing (Berlin) and the UK

• One of the largest producers of offshore wind • One of Europe’s leading providers of district • Leading operator of regional electricity

power in the world heating in large metropolitan areas with distribution grids and top-3 position in local grids

• One of the largest producers of onshore wind approximately 1.8 million end customers in Sweden

power in Denmark and the Netherlands • Strong partnerships with cities for realisation of • Approximately 3.3 million business and

• Strong wind power pipeline with 3 GW under their carbon reduction plans, supported by a track household customers in Sweden and Berlin,

construction and over 4 GW in development record of fulfilling previous reduction targets Germany

• Front-runner in innovative solutions in solar & • Heat production and distribution systems used as • Unit for operation and ownership of new grids in

batteries, such as colocation with wind farms and platforms to integrate other energy solutions, e.g. the UK established in 2017 has now been

shared infrastructure cooling, EV charging solutions, wind and solar awarded its first three contracts.

Underlying Operating Profit1: SEK 3,970 mn Underlying Operating Profit: SEK 978 mn Underlying Operating Profit: SEK 5,325 mn

(15% of total) (4% of total) (20% of total)

External Net Sales: SEK 6,901 mn External Net Sales: SEK 13,538 mn External Net Sales: SEK 16,970 mn

(4% of total) (9% of total) (11% of total)

EBITDA: SEK 9,482 mn EBITDA: SEK 2,644 mn EBITDA: SEK 8,713 mn

(20% of total) (6% of total) (19% of total)

1 Numbers reflect FY 2020

41You can also read