Valuation of: Holiday Inn Express, Llandarcy, Neath, Swansea, SA10 6GZ Prepared for

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Valuation of:

Holiday Inn Express, Llandarcy,

Neath, Swansea, SA10 6GZ

Prepared for

Morgan Stanley Bank N.A.

Valuation Date:

1 May 2019

1

Executive Summary

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Llandarcy, Neath,

Valuation Date: 1 May 2019 Swansea, SA10 6GZ

TABLE OF CONTENTS

Executive Summary ........................................................................................ 1

Property Record .............................................................................................. 3

1. Location ........................................................................................................................... 3

2. Description & Accommodation ........................................................................................ 4

3. Structural Condition and Repair ...................................................................................... 6

4. Statutory Enquiries .......................................................................................................... 6

5. Tenure ............................................................................................................................. 7

6. Operational Structure ...................................................................................................... 8

7. Local Hotel Market Analysis............................................................................................ 8

8. Business Analysis ........................................................................................................... 9

9. C&W Trading Projections .............................................................................................. 12

10. Principal Valuation Considerations ............................................................................... 15

Appendix A: Maps and Plans ........................................................................ 18

2

Executive Summary

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Llandarcy, Neath,

Valuation Date: 1 May 2019 Swansea, SA10 6GZ

EXECUTIVE SUMMARY

This summary is strictly confidential to you as the Addressee. It must not be copied, distributed or

considered in isolation from the full report.

Property Summary

Location The hotel lies adjacent to the M4 motorway, 7.5 miles east of

Swansea and 2.3 miles west of Neath.

Description The hotel comprises 91 guest bedrooms with ancillary Great Room

and three meeting rooms.

The Property was constructed in approximately 2003.

Condition Good

Tenure Long leasehold

Operating Structure Owner operator

Trading Performance

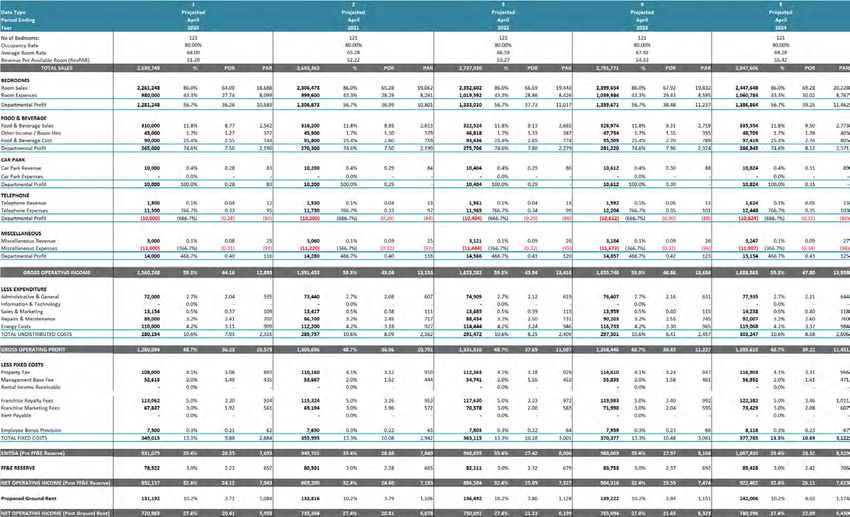

Year 2017 2018 2019 (2+10) forecast

Occupancy 75.53% 75.44% 74.92%

ADR £57.64 £58.87 £59.38

RevPAR £43.54 £44.41 £44.49

Total Revenue £1,609,721 £1,643,175 £1,638,345

NOI (post FF&E)* £443,883 £496,328 £358,737

Profit Margin 27.6% 30.2% 21.9%

*2019 figures include the proposed ground rent payable.

C&W Trading Projections

Year Year 1 Year 2 Year 3

Occupancy 75.00% 75.00% 75.00%

ADR £59.50 £60.69 £61.90

RevPAR £44.63 £45.52 £46.43

Total Revenue £1,641,249 £1,674,074 £1,707,556

NOI (post FF&E and £351,154 £358,177 £365,341

ground rent)

Profit Margin 21.4% 21.4% 21.4%

Market Value and Yields

Valuation Date 1 May 2019

Market Value £3,300,000

Capitalisation Rate 10.75% Discount Rate 12.75%

1

Executive Summary

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Llandarcy, Neath,

Valuation Date: 1 May 2019 Swansea, SA10 6GZ

Gross Initial Yield 10.75%

Capital expenditure None

deducted from gross

valuation

Loan security We consider the Property represents adequate security against a

loan over the proposed period.

Liquidity Reasonable subject to the comments in the property record and

the head report.

Key Investment / Market Considerations for Loan Security

Strengths / Opportunities

• Good connectivity to the M4 motorway;

• Good levels of hotel demand in local area, with relatively good corporate demand generators;

• Strong and stable management team.

• Relatively limited direct competition within the immediate locality.

Weaknesses / Risks

• Peripheral location on the outskirts of Swansea;

• Road noise from the M4 motorway, accentuated by lack of air conditioning in bedrooms;

• Poor customer feedback for adjacent Harvester restaurant, which is sometimes associated

with the hotel on web based customer reviews;

• Investment appetite for Swansea is likely to be more limited than for many of the other hotels

within the portfolio.

2

PROPERTY RECORD

Inspection

The Property was subject to an external inspection, from ground level and an internal inspection,

on 9 May 2019. The inspection was undertaken by Ian Thompson, MRICS.

1. Location

1.1. Location

General

Swansea is located on the south coast of Wales, within Swansea Bay, which opens on to the

Bristol Channel. Swansea lies approximately 40 miles west of Cardiff and 50 miles west of

Newport. Bristol is approximately 80 miles to the east, accessible via the Severn Bridge.

The hotel is reasonably well located within the context of the local market, lying directly adjacent

to Junction 43 of the M4 motorway. Swansea town centre is located approximately 6.5 miles to

the west, while the town of Neath lies approximately 2.3 miles to the east. Port Talbot is

approximately six miles south east of the hotel. Surrounding land uses include the M4 motorway

to the east, a David Lloyd leisure and fitness club to the south and a Harvester restaurant to the

west.

Swansea has a predominantly post-industrial service economy, with main employers including

3M, Bemis, 118 UK/Conduit, Admiral Group, Amazon and a number of public sector organisations

including the DVLA and HMRC. Public sector employment in Swansea is significantly above

average, at 11.1% of total employment compared to the average of 6.8% across Wales (ONS,

2016). According to the latest estimated in mid- 2017, Bath and North East Somerset count a

resident population of 245,480.

The hotel itself is located just within the border of Neath Port Talbot Council. This local authority

borders Swansea and has a population of 141,600 with a profile otherwise similar to Swansea in

terms of demography and employment.

Swansea also has a number of tourist attractions, with 4.59 million visitors in 2016 according to

the City and County of Swansea. Attractions include The Gower Peninsula, which received the

European designation of Area of Natural Beauty in 1956, and numerous beaches along the

coastline.

3

Site Boundary

The plan above is shown for indication purposes only and may not accord strictly with the title

plan.

2. Description & Accommodation

Summary

The hotel comprises 91 guest bedrooms with ancillary Great Room and three meeting rooms.

The Property was constructed in approximately 2003 and is arranged over ground, first and

second floor. The building is of brick construction underneath a pitched tiled roof.

4

Guestrooms

The following table summarises the Property's guestroom facilities, based on information provided

by Atlas Hotels.

Category Unit Count

Twin 25

Double 60

Accessible 6

Total 91

There are three room types – twin, accessible and double rooms (which can accommodate up to

three guests). There are 25 twin bedrooms and 60 double bedrooms. In addition, there are six

accessible bedrooms which have an interconnecting door. The style of the bedrooms is Fourth

Generation, having been refurbished in 2015. The bedrooms are not fitted with air conditioning

units.

Food & Beverage

The primary dining area is The Great Room, a seated open plan restaurant offering 60 covers. A

breakfast buffet servery lies adjacent to the Great Room. The bar and lobby area extend from the

Great Room adjoining the reception, and offer more casual soft seating. There is air conditioning

to the ground floor public areas.

5

Meeting Rooms

There are three meeting rooms, one of which is significantly larger with a capacity of 25 theatre

style, while the smaller two each have a capacity of 12. All meeting rooms have natural light.

Additional food and beverage packages are on offer alongside meeting room hire.

There is air conditioning to the meeting rooms.

Car Parking

There are approximately 130 car parking spaces, which are offered free of charge to guests. The

car park is shared with the adjacent Harvester restaurant.

Back of House Accommodation

There is appropriate storage provision and back of house accommodation. The staff room is able

to accommodate eight covers.

3. Structural Condition and Repair

The Property has been well maintained and was found to be in good condition. Following

construction in 2003, the hotel was further extended in 2006 with the addition of 18 bedrooms.

The hotel has undergone various refurbishments since construction; in 2012 The Great Room

and meeting rooms received a soft refurbishment, which included new fitted carpets and painting.

In 2015 the bedrooms were refurbished to Generation Four standards. This refurbishment

included the redecorating of wall coverings, the replacement of desk with a moveable work

surface and an iconic red chair, and the upscaling of the headboards to include charging sockets.

We have been provided with a schedule of the capital expenditure plan, which confirms the

following:

2018 2019 Forecast

£28,538 £51,378

3.1. Indication of Reinstatement Cost

Our informal guide to the Day One Cost is £7,800,000 (exclusive of VAT)

This guide figure envisages clearance and reinstatement using modern methods and materials,

which may not necessarily be appropriate or permitted. It does not reflect any additional costs

attributable to conservation area status or listed building status (or similar – for example proximity

to listed buildings)

You should not rely on this guide for any purpose before it has been confirmed by a formal

assessment carried out by a building surveyor or other person with sufficient current experience

of replacement costs.

4. Statutory Enquiries

We have been provided with an Argyll Environmental report dated 29 May 2019, which we have

had regard to in undertaking our valuation.

Ground Conditions

Potential liabilities have been identified under the relevant contaminated land legislation. We

recommend further investigation prior to drawdown of the loan. For further comments please refer

to the head report.

6

Flooding Risk

The property falls within Flood Zone 1, with a low probability of flooding.

Environmental Considerations

Please refer to head report.

Planning

The planning policy for the subject Property is determined by Neath Port Talbot Borough Council.

We are not aware of any outstanding or unimplemented planning applications.

Conservation Area and Listed Building Status

The Property is not listed and nor is it located within a conservation area.

Business Rates

Demise Description Rateable Values

Holiday Inn Express, Swansea Hotel & Premises 139,500

In Wales the Non-Domestic rating multiplier for the fiscal year 2019/2020 has been set at 52.6

pence in the pound.

5. Tenure

Title

We have been provided with a Certificate of Title prepared by Reed Smith LLP dated 3 November

2017 and based on this we summarise our understanding of the title below.

The Property is held freehold although the proposal is to sell the freehold interest and

simultaneously be granted a ground lease back. The terms of the ground lease are set out in the

head report.

Overview

Type of tenure Proposed long leasehold

Title no(s) Unknown

Lease Term 125 years

Rent £74,449 pa to be reviewed annually in line with the

RPI subject to a cap and collar of 0% and 5%.

Any material encumbrances or unduly None other than disclosed in the draft certificate.

onerous / unusual easements, restrictions,

outgoings or conditions?

Any title characteristics likely to have an None.

adverse impact on value, either now or over

the proposed loan term?

Full details of the proposed leasehold interest are detailed in the head report.

7

6. Operational Structure

Please refer to the head report for operational structure, franchise agreement and information

relating to the IHG/Holiday inn Express brand.

7. Local Hotel Market Analysis

7.1. Existing Market Supply

According to AM:PM Hotels, there are 37 hotels and 1,540 bedrooms in the area of Swansea, all

of which are located further than a mile away from the subject Property. The market is dominated

by the budget segment with 577 rooms, followed by four-star hotels with 525 rooms. This

compares to a national trend characterised by less than 30% of total rooms in the four-star

category and approximately 25% of total rooms in the budget sector. Of this supply, over 60% is

branded, with Ibis, Premier Inn, Travelodge and the subject in the budget sector.

7.2. Competitor Trading Analysis

Smith Travel Research (STR) is an independent research firm that is recognised by the hotel

industry as the standard source of reliable data, providing operating statistics on the local market

as a whole.

We have been provided STR data for the hotel and the following competitive set of hotels:

• The Dragon Hotel Swansea

• Mercure Swansea Hotel

• Holiday Inn Express Swansea East

• ibis Swansea

• Premier Inn Swansea City Centre

• Premier Inn Swansea North

• Travelodge Swansea Central Hotel

The direct competition to the subject hotel is relatively limited with few hotels located within the

same locality, given the hotels out of town location. Travelodge Swansea and Ibis are most likely

the most comparable in terms of their offering, but are located within Swansea town centre and

therefore target a different clientele.

8The table below sets out the hotels’ key performance indicators compared to the above

competitive set for the full years 2017 and 2018 and YTD March 2019*.

The hotel outperforms the competitive set in both occupancy and ADR and achieved an RGI of

116.2 in 2018. For the first three months of 2019, the hotel has increased its MPI and ARI rates.

7.3. Proposed Supply

There are currently 11 projects in the pipeline in Swansea, all in the three and four-star segments

and two unconfirmed. This would add just over 240 bedrooms to the market.

8. Business Analysis

Overview

The Holiday Inn Express is a purpose built limited service hotel, built in 2003. While the original

structure remains unmodified, there have been various refurbishments since, most significantly

in 2015 when the bedrooms were upgraded from Generation Two to Generation Four, in line with

Holiday Inn Express brand standards.

Swansea has a relatively healthy hotel market, supported both by the strong presence of business

in the area and the leisure and tourism industry. Following the decline of heavy industry, Swansea

has a predominantly post-industrial service economy, with main employers spread between the

service, manufacturing and public sectors. Businesses with a large presence in the area include

the DVLA, HMRC, Amazon, 3M and Admiral Group. Corporate business is a core component of

the Swansea hotel market.

In addition, Swansea has a prosperous leisure and tourism industry. Visitors are largely attracted

by the surrounding natural beauty; Swansea hosts over 30 Sites of Special Scientific Interest

(SSSI), while the Gower is designated an Area of Natural Beauty (AONB). The leisure and tourism

segments are particularly important to the hotel industry throughout the summer months, and

throughout the year on weekends, when the occupation rate of the corporate segment is

significantly lower.

Swansea also increasingly benefits from a strong events calendar, namely sporting and music

events. The Six Nations Rugby, hosted at the Principality Stadium in Cardiff, generates

consistently strong year-on-year business. Swansea, although located 40 miles west of the event,

is able to successfully capitalise on the overflow of visitors to Cardiff by offering a comparatively

lower rate. Swansea’s Liberty Stadium also hosts a number of events, although demand from the

football club has reduced since the team was relegated from the Premier League a couple of

years ago. The hotel experiences good levels of leisure occupancy predominantly through the

summer months and to a lesser extent throughout the remainder of the year due to events such

as those highlighted.

The hotel has moved away from low-rate leisure groups, and a focus on higher rate corporate

contracts including Scan Optics at 400 room nights per year (repeat business since 2003) and

Sterling Services at approximately 350 room nights per year. The agreed rate with Scan Optics

was previously £55 but currently stands at £65. Much of the corporate demand is transient rather

than contract led. Currently the segmentation comprises around 60% corporate and 40% leisure,

with corporate demand dominating on weekdays. The hotel achieved an occupancy rate of close

9to 90% during July and August 2017, as Swansea acts as the gateway to the Gower peninsula.

The hotel is now charging families a supplement.

To summarise, the hotel has shown resilience amidst a changing corporate base, and continues

to show strength in year-on-year growth on all key performance indicators. The hotel experiences

varying ratios of corporate to leisure segmentation, fluctuating throughout the year as would be

expected of a hotel in this location.

The hotel secures a good proportion of its business from IHG and also trying to convert as much

OTA business to direct. The hotel paid out around £1,500 in commission fees to booking.com last

year.

Trading Performance

The income and expense statements, illustrated in the table on the following page, were provided

by Atlas Hotels. The statements show the subject's operating history for the years ended

December 2016-2018, forecast for 2019 including 2 months actuals and trading projections for

2020, which includes the proposed ground rent.

10Cushman & Wakefield | Morgan Stanley Bank N.A. Property Record

Valuation Date: 1 May 2019 Valuation of: Holiday Inn Express, Llandarcy, Neath, Swansea, SA10 6GZ

11Property Record

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Llandarcy, Neath,

Valuation Date: 1 May 2019 Swansea, SA10 6GZ

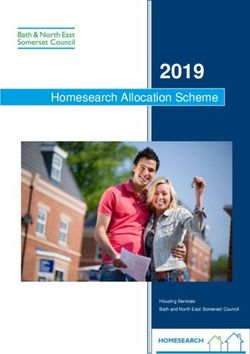

9. C&W Trading Projections

Trading Projections

The following chart depicts our summary profit and loss projections showing the hotels income

and expenses for the five years commencing May 2019. The statements are expressed in inflated

terms for each year.

12Cushman & Wakefield | Morgan Stanley Bank N.A. Property Record

Valuation Date: 1 May 2019 Valuation of: Holiday Inn Express, Llandarcy, Neath, Swansea, SA10 6GZ

13Property Record

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Llandarcy, Neath,

Valuation Date: 1 May 2019 Swansea, SA10 6GZ

Commentary on C&W Projections

The hotel is a stabilised business with occupancy levels extremely consistent ranging between

74-77% with the full year forecast for 2019 showing a similar level. We have adopted an

occupancy of 75% in each year of our projections.

The hotel achieved an ADR of £58.87 in 2018, similar to the previous year, although management

are forecasting a 1% increase in the current year to £59.38. For the purpose of our assessment

we have adopted a year one ADR of £59.50 to reflect our starting date of May 2019. We have

assumed inflationary increases thereafter taking into account the stabilised nature of the

operation.

There is limited other revenue generated from the hotel with rooms revenue accounting for around

90% of the total. Accordingly, we have adopted a similar business mix within our projections and

similar levels of food and beverage and other revenue to that currently being achieved.

The format of the accounts is not strictly in accordance with the Uniform System of Accounts for

the Lodging Industry with all payroll costs shown within the rooms expenses as opposed to being

allocated to individual departments given the nature of the operation. As a result, it is more difficult

to undertake full benchmarking of the departmental expenses.

The departmental expenses have however been relatively consistent as a percentage of

departmental revenue and on a Per Occupied Room (POR) basis and therefore we have had

regard to the actual expenses within our projections.

The miscellaneous expenses actually show a negative figure being the forecast cost savings

being implemented by management we have adopted these savings within our assessment.

The undistributed costs do not appear unreasonable based on other limited service hotels in the

market taking into account they do not include payroll costs. As a result, we have had regard to

current levels in preparing our assessment.

The majority of the sales and marketing expenses relate to the franchise sales and marketing

fees, which we have shown as a separate line item. We have allowed for increased sales and

marketing expenses to reflect that the hotel will be operated individually.

Property tax has regard to the hotels current rating assessment.

The accounts provided by management show the insurance charges within the administration

and general expenses. We have adopted the same approach for ease.

We have deducted franchise fees equivalent to a royalty fee of 5% of rooms revenue and a sales

and marketing of 3% of rooms revenue, which we consider would be the likely level paying

assuming the hotel was sold on an individual basis.

We have deducted an amount of 2% of total revenue to provide the services provided centrally

by management such as sales and marketing and revenue management as opposed to making

a separate allocation to each department as these costs would need to be provided whether

through another management company or at hotel level.

We have deducted an amount for an FF&E reserve equivalent to 3% of total revenue in each year

of our projection period.

Our resultant net operating profit post FF&E reserve is £425,603, which compares to the forecast

for the current year of £433,186. The hotel is forecast to achieve a net operating profit margin of

26.4% for the current year compared to 30.2% last year. Our projected net operating profit margin

is 25.9%.

After the deduction of the proposed ground rent of £74,449 per annum our adjusted net operating

profit is £351,154, which is equivalent to a profit margin of 21.4%.

14Property Record

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Llandarcy, Neath,

Valuation Date: 1 May 2019 Swansea, SA10 6GZ

10. Principal Valuation Considerations

Location / Situation and Competition

The Property is well located. The M4 motorway lies adjacent to the hotel, providing excellent

accessibility to the east and west. In addition, the A465, a main artery running north east to

Merthyr Tydfil and central Wales, lies just a few hundred metres from the hotel entrance.

Associated road noise is mitigated by a raised land bank to the north of the Property and

vegetation to the east, ensuring that the proximity to the roads is of benefit rather than detriment

to the business.

Building Design / Condition / Suitability

The hotel is in good condition having been well maintained over the years.

Tenure

The hotel will be held on long lease for a term of 125 years with a buy back option at year 60 for

£1.

There is limited comparable evidence of the sale of long leasehold as the structure is relatively

new within the hotel market. We would however expect there to be a narrower pool of purchasers

for the leasehold interest compared to the freehold interest, which will result in the interest

achieving a softer yield.

We consider the yield gap between a freehold interest and a ground lease interest will be

influenced by a number of factors including location, quality of the asset and rent cover. The yield

gap will also be influenced by whether the hotel is sold as part of the existing portfolio or as a

single asset. We consider that there is likely to be a wider yield gap if sold as a single asset as

the hotel will lose some of its appeal and economies of being operated as part of a larger platform.

The proposed rent payable will be £74,449 per annum subject to annual increases in line with

RPI with a cap and collar of 0% and 5%. The proposed rent represents 15% of the 2018 NOI.

We consider the proposed rent to fall within an acceptable range of NOI based on other

transactions that have occurred in the market providing sufficient rent cover in the short term.

Business & Income Security

The hotel is a stable business and well established in its local market being one of the strongest

performing hotels. The hotel has produced relatively consistent levels of revenue and net

operating profit with the profit margin being achieved good.

Whilst the profitability of the hotel has been good there is potential for the current margins to be

eroded by the proposed ground rent in the event that earnings do not keep pace with RPI.

Asset Management Opportunities

There is limited scope for additional growth through specific asset management. The hotel is

stabilised.

Saleability

Current Sale Prospects

What is the estimated period it would take to sell the Property at 6-9 months

Market Value?

Purchaser demand is likely to be Good

15Property Record

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Llandarcy, Neath,

Valuation Date: 1 May 2019 Swansea, SA10 6GZ

The market for hotels held on long ground leases such as that proposed has been largely untested

to date. Whilst this will result in a greater level of uncertainty in terms of purchaser appetite and

saleability, we are of the opinion that there would be fewer purchaser in the market than for the

equivalent freehold interest.

10.1. Market Value

Value Conclusion

In assessing the value of the hotel we have adopted a discounted cash flow (DCF) based on our

trading projections and rationale as set out above.

In arriving at our choice of capitalisation rate, we have had regard to the comparable evidence of

Holiday Inn Express hotels that have occurred generally as set out in our head report together

with other hotels in the surrounding area. There has been limited sales of hotels held on ground

leases and therefore we have made an appropriate adjustment to reflect the leasehold interest.

The yields for similar quality hotels held on a freehold basis have ranged between 7.5% and 9.5%.

Unfortunately, there have been no recent single asset transactions to have traded in Swansea or

indeed Cardiff.

We consider that the hotel would achieve similar yields to the Holiday Inn Express hotels

referenced in the head report of Tamworth and Ramsgate, which sold for between £35,000 per

key and £62,000 per key.

The yields for similar quality hotels held on a freehold basis have ranged between 7.5% and 9%.

Having regard to the comments above and the fundamentals of the Property including the location

of the hotel within the national and local context and quality of the asset, we are of the opinion

that the equivalent freehold interest would achieve a yield of 8.25%.

We have made an adjustment in our choice of capitalisation rate to reflect the proposed leasehold

interest having regard to the location of the hotel and the level of rent payable as detailed in the

head report. Based on these factors, we have adopted a capitalisation rate of 10.75%. We have

adopted a discount rate of 12.75%.

Our valuation is the net figure that would appear in a sale and purchase agreement with any

purchaser’s costs being paid in addition to the figure reported. We have not made any explicit

deduction for purchaser’s costs within our calculation rather implicitly reflecting this in our

capitalisation rate.

In summary, in arriving at our opinion of value we have adopted the following:

Market Value

Gross Initial Yield 10.75%

Capitalisation Rate 10.75%

Discount Rate 12.75%

Market Value £3,300,000

Capital value Per Bedroom £36,264

10.2. Market Rent

Our opinion of the Market Rent of the Property on the basis set out in the head report is £180,000

per annum.

16Property Record

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Llandarcy, Neath,

Valuation Date: 1 May 2019 Swansea, SA10 6GZ

10.3. Market Value with Vacant Possession

For the purpose of our valuation with vacant possession we have adopted our trading assessment

as set out above. In arriving at our opinion of value on this basis, we have adopted our Market

Value.

17Appendix A: Maps and Plans

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Llandarcy, Neath,

Valuation Date: 1 May 2019 Swansea, SA10 6GZ

APPENDIX A: MAPS AND PLANS

18Holiday Inn Express, Llandarcy, Neath,

Swansea, SA10 6GZ

Ordnance Survey © Crown Copyright 2017. All rights reserved.

Licence number 100022432. Plotted Scale - 1:700000

This plan is published for convenience of identification.

Any site boundaries shown are indicative only and

should be checked against Title Deeds.Holiday Inn Express, Llandarcy, Neath,

Swansea, SA10 6GZ

Ordnance Survey © Crown Copyright 2017. All rights reserved.

Licence number 100022432. Plotted Scale - 1:7500

This plan is published for convenience of identification.

Any site boundaries shown are indicative only and

should be checked against Title Deeds.Holiday Inn Express, Llandarcy, Neath,

Swansea, SA10 6GZ

Shelter

M4

M4

Mast

Dra

in

0m 25m 50m 75m

Ordnance Survey © Crown Copyright 2017. All rights reserved. Licence number 100022432. Plotted Scale - 1:1250

This plan is published for convenience of identification.

Any site boundaries shown are indicative only and

should be checked against Title Deeds.About Cushman & Wakefield Cushman & Wakefield is a leading global real estate services firm that helps clients transform the way people work, shop and live. The firm's 43,000 employees in more than 60 countries provide deep local and global insights that create significant value for our clients. Cushman & Wakefield is among the largest commercial real estate services firms, with core services of agency leasing, asset services, capital markets, facility services, global occupier services, investment & asset management (DTZ Investors), project & development services, tenant representation and valuation & advisory. To learn more, visit www.cushmanwakefield.com or follow @CushWake on Twitter. © Cushman & Wakefield 2017

Valuation of:

Holiday Inn Express, Frankland

Road, Blagrove, Swindon, SN5

8UD

Prepared for

Morgan Stanley Bank N.A.

Valuation Date:

1 May 2019

1Executive Summary

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Frankland Road,

Valuation Date: 1 May 2019 Blagrove, Swindon, SN5 8UD

TABLE OF CONTENTS

Executive Summary ........................................................................................ 3

Property Record .............................................................................................. 5

1. Location ........................................................................................................................... 5

2. Description & Accommodation ........................................................................................ 6

3. Structural Condition and Repair ...................................................................................... 8

4. Statutory Enquiries .......................................................................................................... 9

5. Tenure ............................................................................................................................. 9

6. Operational Structure .................................................................................................... 10

7. Local Hotel Market Analysis.......................................................................................... 10

8. Business Analysis ......................................................................................................... 11

9. C&W Trading Projections .............................................................................................. 14

10. Principal Valuation Considerations ............................................................................... 17

Appendix A: Maps and Plans ........................................................................ 20

2Executive Summary

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Frankland Road,

Valuation Date: 1 May 2019 Blagrove, Swindon, SN5 8UD

EXECUTIVE SUMMARY

This summary is strictly confidential to you as the Addressee. It must not be copied, distributed or

considered in isolation from the full report.

Property Summary

Location The hotel is well located within close proximity to the M4, allowing

excellent accessibility. Swindon town centre is approximately four

miles north of the Property.

Description The hotel comprises 121 bedrooms with Great Room and four

meeting rooms.

Condition Good

Tenure Long leasehold

Operating Structure Owner operator

Trading Performance

Year 2017 2018 2019 (2+10) forecast

Occupancy 76.32% 79.20% 80.12%

ADR £62.66 £61.55 £63.82

RevPAR £47.82 £48.75 £51.14

Total Revenue £2,457,880 £2,500,688 £2,625,387

NOI (post FF&E)* £868,941 £874,612 £785,047

Profit Margin 35.4% 35.0% 29.9%

*2019 figures include the proposed ground rent payable.

C&W Trading Projections

Year Year 1 Year 2 Year 3

Occupancy 80.00% 80.00% 80.00%

ADR £64.00 £65.28 £66.59

RevPAR £51.20 £52.22 £53.27

Total Revenue £2,630,748 £2,683,363 £2,737,030

NOI (post FF&E and £720,965 £735,384 £750,092

ground rent)

Profit Margin 27.4% 27.4% 27.4%

Market Value and Yields

Valuation Date 1 May 2019

Market Value £7,000,000

Capitalisation Rate 10.25% Discount Rate 12.25%

3Executive Summary

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Frankland Road,

Valuation Date: 1 May 2019 Blagrove, Swindon, SN5 8UD

Gross Initial Yield 10.25%

Capital expenditure None

deducted from gross

valuation

Loan security We consider the Property represents adequate security against a

loan over the proposed period.

Liquidity Reasonable subject to the comments in the property record and

the head report.

Key Investment / Market Considerations for Loan Security

Strengths / Opportunities

• Accessible location adjacent to the M4;

• Strong hotel demand in local area.

Weaknesses / Risks

• Located outside of the town centre, some distance from Swindon train station.

• Large telegraph mast located on site.

4Property Record

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Frankland Road,

Valuation Date: 1 May 2019 Blagrove, Swindon, SN5 8UD

PROPERTY RECORD

Inspection

The Property was subject to an external inspection, from ground level and an internal inspection,

on 9 May 2019. The inspection was undertaken by Ian Thompson.

1. Location

1.1. Location

General

The Holiday Inn Express Swindon West is located on the north side of junction 15 of the M4

motorway, approximately four miles to the west of Swindon town centre.

According to the latest estimated in mid- 2017, Swindon count a resident population of 220,363

(ONS,2017). Major businesses in Swindon include Honda, Dolby Labs and Zurich, while

Nationwide, W H Smith and Intel are amongst those with headquarters in the town.

The hotel has excellent visibility from the motorway in both directions. Access is via the A3102

Great Western Way. Vehicular traffic leaving the motorway cannot turn right towards the hotel

and so must travel 100 metres east along the A3102 before doubling back at the roundabout

junction of the A3102 and the B534 Whitehill Way.

There are a number of occupiers clustered around the motorway junction, including Johnson

Matthey Fuel Cells, a Volkswagen dealership, Hilton Hotel and Arval UK. Just to the north is

Windmill Hill Business Park, where there is a variety of tenant occupiers.

We consider the location to be good and although it is not in the town centre, this is probably an

advantage given that Swindon does not have a particularly attractive central area.

5Property Record

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Frankland Road,

Valuation Date: 1 May 2019 Blagrove, Swindon, SN5 8UD

Site Boundary

The plan above is shown for indication purposes only and may not accord strictly with the title

plan which we have reviewed.

2. Description & Accommodation

Summary

The hotel comprises 121 bedrooms with Great Room and four meeting rooms.

The Property was constructed in approximately 2001 and comprises ground and three upper

floors of brick construction underneath a pitched tiled roof. The fenestration comprises UPVC

framed double glazed units.

6Property Record

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Frankland Road,

Valuation Date: 1 May 2019 Blagrove, Swindon, SN5 8UD

Guestrooms

The following table summarises the Property's guestroom facilities, based on information provided

by Atlas Hotels.

Category Unit Count

Twin 27

Double 88

Accessible 6

Total 121

There are three room types, namely twin, accessible and double rooms. All rooms were

refurbished from mid-2016 until around October 2016, to fourth generation, the current brand

standard. As such, they present well.

Typical room facilities include tea and coffee making facilities, land line telephone, desk, flat

screen TV, internet access and bathroom.

All guest bedrooms are served by air conditioning.

Food & Beverage

The primary dining area is The Great Room, a large open plan restaurant offering 70 covers. A

breakfast buffet servery lies adjacent to the Great Room. The bar and lobby area extend from the

Great Room to reception and offer more casual soft seating.

The Great Room is relatively large for a Holiday Inn Express and we are advised that the hotel

has a strong food & beverage business, with a 70% midweek capture rate. This success is likely

due to the out of town location of the hotel, with limited alternative dining choices for guests.

7Property Record

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Frankland Road,

Valuation Date: 1 May 2019 Blagrove, Swindon, SN5 8UD

Meeting Rooms

There are four meeting rooms, all of which are located on the ground floor and benefit from natural

light. We are advised by the General Manager that the day delegate rate for these rooms is

approximately £200, which does not include any food or beverages. This can be added at the

extra expense of £7 per person.

Car Parking

There are approximately 100 car parking spaces, which are offered free of charge to guests. The

hotel has a longstanding agreement with the neighbouring Volkswagen Garage, who hire

approximately 5-10 car parking spaces from the hotel.

Back of House Accommodation

There is appropriate storage and back of house accommodation. The staff room is able to

accommodate 6-8 covers.

3. Structural Condition and Repair

The Property has been well maintained and was found to be in good condition. There have been

no additions to the structure since construction.

The hotel has undergone numerous refurbishments since opening. In 2006 The Great Room and

public areas received a soft refurbishment and remain in good condition. The bedrooms were

refurbished from a Generation Two to Generation Four standard at the end of 2016. This

refurbishment most notably included the redecorating of wall coverings, the replacement of the

desk with a moveable work surface and an iconic red chair, and the upscaling of the headboards

to include charging sockets.

We have been provided with a schedule of the capital expenditure plan, which confirms the

following:

2018 2019 Forecast

£18,004 £39,754

3.1. Indication of Reinstatement Cost

Our informal guide to the Day One Cost is £10,300,000 (exclusive of VAT)

This guide figure envisages clearance and reinstatement using modern methods and materials,

which may not necessarily be appropriate or permitted. It does not reflect any additional costs

8Property Record

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Frankland Road,

Valuation Date: 1 May 2019 Blagrove, Swindon, SN5 8UD

attributable to conservation area status or listed building status (or similar – for example proximity

to listed buildings)

You should not rely on this guide for any purpose before it has been confirmed by a formal

assessment carried out by a building surveyor or other person with sufficient current experience

of replacement costs.

4. Statutory Enquiries

We have been provided with an Argyll Environmental report dated 29 May 2019, which we have

had regard to in undertaking our valuation.

Ground Conditions

Please refer to head report.

Flooding Risk

The property falls within Flood Zone 1, with a low probability of flooding.

Environmental Considerations

Please refer to head report.

Planning

The planning policy for the subject Property is determined by Swindon Borough Council.

We are not aware of any outstanding or unimplemented planning applications.

Conservation Area and Listed Building Status

The Property is not listed and nor is it located within a conservation area.

Business Rates

Demise Description Rateable Values

Holiday inn Express,

Hotel & Premises £108,360

Swindon

In England, the Non-Domestic Rating Multiplier for the fiscal year 2019/2020 has been set at 50.4

pence.

5. Tenure

Title

We have been provided with a Certificate of Title prepared by Reed Smith LLP dated 3 November

2017 and based on this we summarise our understanding of the title below.

The Property is held freehold (Title Number: WT195205) although the proposal is to sell the

freehold interest and simultaneously be granted a ground lease back. The terms of the ground

lease are set out in the head report.

Overview

Type of tenure Proposed long leasehold

9Property Record

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Frankland Road,

Valuation Date: 1 May 2019 Blagrove, Swindon, SN5 8UD

Overview

Title no(s) Unknown

Lease Term 125 years

Rent £131,192 pa to be reviewed annually in line with the

RPI subject to a cap and collar of 0% and 5%.

Any material encumbrances or unduly None other than disclosed in the draft certificate.

onerous / unusual easements, restrictions,

outgoings or conditions?

Any title characteristics likely to have an None.

adverse impact on value, either now or over

the proposed loan term?

Full details of the proposed leasehold interest are detailed in the head report.

6. Operational Structure

Please refer to the head report for operational structure, franchise agreement and information

relating to the IHG/Holiday inn Express brand.

7. Local Hotel Market Analysis

7.1. Existing Market Supply

According to AM:PM Hotels, there are 56 hotels and 2,545 rooms in Swindon, two of which, a

Doubletree and a Premier Inn, are located less than a mile from the subject Property. The market

is dominated by the three-star segment with 970 rooms, followed by budget and four-star hotels.

This compares to a national trend characterised by less than 30% of total rooms in the four-star

category and approximately 25% of total rooms in the budget sector. Of this pipeline, over 75%

is branded, with Holiday Inn Express, Travelodge and Premier Inn accounting for most of the

budget sector.

10Property Record

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Frankland Road,

Valuation Date: 1 May 2019 Blagrove, Swindon, SN5 8UD

7.2. Competitor Trading Analysis

Smith Travel Research (STR) is an independent research firm that is recognised by the hotel

industry as the standard source of reliable data, providing operating statistics on the local market

as a whole.

We have been provided STR data for the hotel and the following competitive set of hotels:

• Village Hotel Swindon

• Campanile Swindon

• Holiday Inn Swindon

• DoubleTree By Hilton Hotel Swindon

• Holiday Inn Express Swindon West

• Holiday Inn Express Swindon City Centre

• Travelodge Swindon Central Hotel

• Jurys Inn Swindon

The Premier Inn Swindon West and DoubleTree by Hilton are located within close proximity. The

Campanile Swindon is located in the town centre while the Holiday Inn Swindon is similarly

located on the fringes of the town centre, albeit not within such close proximity to the M4.

The table below sets out the hotels’ key performance indicators compared to the above

competitive set for the full years 2017 and 2018 and YTD March 2019*.

The hotel has performed lower than that within the competitors set in terms of ADR, however, has

outperformed with regards to occupancy levels and achieved an RGI of 103.7 in 2018. For the

first three months of 2019, the hotel has increased its MPI and ARI has rates.

7.3. Proposed Supply

There are 12 projects in the pipeline in Swindon, five of which are currently in construction and

due to open in 2019. The ibis Budget Swindon will comprise 73 rooms and is due to open in 2019,

approximately three miles from the subject, and an independent budget hotel of 180 rooms, North

star Oasis Leisure, is in its final planning and should be located by the ibis Budget.

8. Business Analysis

Overview

Holiday Inn Express Swindon is a purpose built limited service hotel constructed in 2001. The

original structure remains unchanged, although the hotel benefited from refurbishment of the

public areas in 2006 and of the bedrooms in late 2016. This refurbishment upgraded the rooms

from Generation two to Generation four standard, such that it complies with the latest Holiday Inn

Express brand standards.

Swindon benefits from its location at the nexus between Reading, Bristol, London and Cardiff.

The construction of the M4 in the 1970s brought with it significant interest from businesses looking

11Property Record

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Frankland Road,

Valuation Date: 1 May 2019 Blagrove, Swindon, SN5 8UD

to capitalise on the strategic location. Honda, Dolby Labs and Zurich all have a presence in the

area, while Nationwide, W H Smith and Intel are amongst those with headquarters in the town.

The strong presence of businesses in the area coupled with the location, particularly in relation

to a number of regional airports, drives strong demand for hotels. Moreover, the location of the

hotel on the edge of the town acts as a further benefit, allowing ease of access by car.

Swindon does not have a particularly strong leisure business, and correspondingly the hotel

largely focusses on the corporate sector. However, the location of the hotel on the periphery of

Swindon allows the hotel to attract guests visiting neighbouring attractions, such as Bath

Christmas Market approximately 40 miles to the south west. The summer months are more

heavily represented by this leisure business that uses Swindon as a base, while the remainder of

the year is dominated by the corporate segment.

The hotel holds a healthy variety of corporate contracts and is not over reliant on any one contract.

Main accounts that provide more than 200 room nights per year include UK training venue

provider Develop and Nationwide. The corporate rate for key clients like Nationwide is around

£70 - £75. On Tuesday and Wednesday nights, the rate can increase to as much as £140. BP

had previously taken around 150 room nights per year, but this contract has been lost due to

relocation. This demonstrates spreading of risk by hotel management, mitigating against the

fragility that would otherwise ensue following the loss of large business accounts.

The corporate / leisure split is around 65% in favour of corporate. Approximately 35% of bookings

are made through Online Travel Agencies (OTAs). ADR growth has in part been aided by the

extensive soft refurbishment in 2016. As a result, the occupancy rate has remained static,

although demand appears to be on an upward trajectory. The balance achieved between

corporate and leisure occupancy mitigates against seasonality, although Q1 remains the weakest

across all segments. May and June tend to be the busiest months, even though the corporate

segmentation starts to decrease, leading into the summer months. Significant annual events

which draw custom to the locality include the Fairford Air Festival and the Bath Christmas Market.

In terms of setting the rate, hotel management tend to be about £10 lower than the Holiday Inn at

Junction 15.

The hotel tends to generate around 30 to 35 covers per night within the Great room, mostly used

by their corporate guests with a meal allowance.

Trading Performance

The income and expense statements, illustrated in the table on the following page, were provided

by Atlas Hotels. The statements show the subject's operating history for the years ended

December 2016-2018, forecast for 2019 including 2 months actuals and trading projections for

2020, which includes the proposed ground rent.

12Cushman & Wakefield | Morgan Stanley Bank N.A. Property Record

Valuation Date: 1 May 2019 Valuation of: Holiday Inn Express, Frankland Road, Blagrove, Swindon, SN5 8UD

13Property Record

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Frankland Road,

Valuation Date: 1 May 2019 Blagrove, Swindon, SN5 8UD

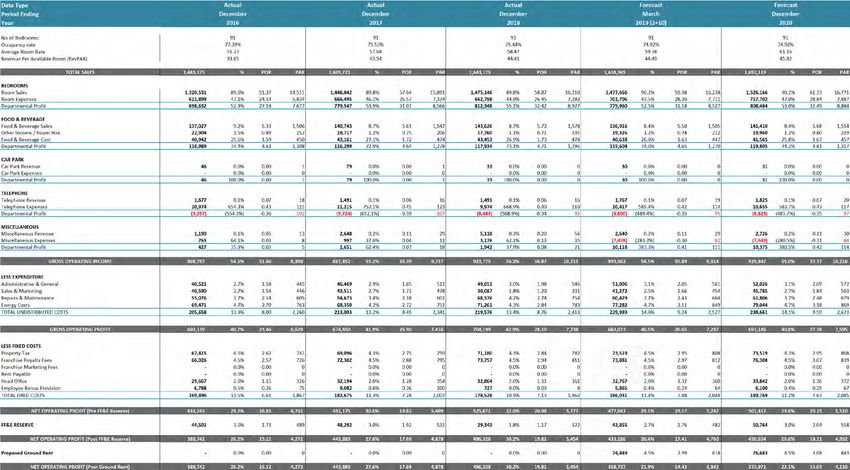

9. C&W Trading Projections

Trading Projections

The following chart depicts our summary profit and loss projections showing the hotels income

and expenses for the five years commencing May 2019. The statements are expressed in inflated

terms for each year.

14Cushman & Wakefield | Morgan Stanley Bank N.A. Property Record

Valuation Date: 1 May 2019 Valuation of: Holiday Inn Express, Frankland Road, Blagrove, Swindon, SN5 8UD

15Property Record

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Frankland Road,

Valuation Date: 1 May 2019 Blagrove, Swindon, SN5 8UD

Commentary on C&W Projections

The hotel is a stabilised business with occupancy levels extremely consistent ranging between

75-80% with the full year forecast for 2019 showing a similar level. We have adopted an

occupancy of 80% in each year of our projections.

The hotel achieved an ADR of £61.55 in 2018, similar to the previous year, although management

are forecasting a 4% increase in the current year to £63.82. For the purpose of our assessment

we have adopted a year one ADR of £64 to reflect our starting date of May 2019. We have

assumed inflationary increases thereafter taking into account the stabilised nature of the

operation.

There is limited other revenue generated from the hotel with rooms revenue accounting for around

86% of the total. Accordingly, we have adopted a similar business mix within our projections and

similar levels of food and beverage and other revenue to that currently being achieved.

The format of the accounts is not strictly in accordance with the Uniform System of Accounts for

the Lodging Industry with all payroll costs shown within the rooms expenses as opposed to being

allocated to individual departments given the nature of the operation. As a result, it is more difficult

to undertake full benchmarking of the departmental expenses.

The departmental expenses have however been relatively consistent as a percentage of

departmental revenue and on a Per Occupied Room (POR) basis and therefore we have had

regard to the actual expenses within our projections.

The miscellaneous expenses actually show a negative figure being the forecast cost savings

being implemented by management we have adopted these savings within our assessment.

The undistributed costs do not appear unreasonable based on other limited service hotels in the

market taking into account they do not include payroll costs. As a result, we have had regard to

current levels in preparing our assessment.

The majority of the sales and marketing expenses relate to the franchise sales and marketing

fees, which we have shown as a separate line item. We have allowed for increased sales and

marketing expenses to reflect that the hotel will be operated individually.

Property tax has regard to the hotels current rating assessment.

The accounts provided by management show the insurance charges within the administration

and general expenses. We have adopted the same approach for ease.

We have deducted franchise fees equivalent to a royalty fee of 5% of rooms revenue and a sales

and marketing of 3% of rooms revenue, which we consider would be the likely level paying

assuming the hotel was sold on an individual basis.

We have deducted an amount of 2% of total revenue to provide the services provided centrally

by management such as sales and marketing and revenue management as opposed to making

a separate allocation to each department as these costs would need to be provided whether

through another management company or at hotel level.

We have deducted an amount for an FF&E reserve equivalent to 3% of total revenue in each year

of our projection period.

Our resultant net operating profit post FF&E reserve is £852,157, which compares to the forecast

for the current year of £916,238. The hotel is forecast to achieve a net operating profit margin of

34.9% for the current year compared to 35.0% last year. Our projected net operating profit margin

is 32.4%.

After the deduction of the proposed ground rent of £131,192 per annum our adjusted net operating

profit is £720,965, which is equivalent to a profit margin of 27.4%.

16Property Record

Cushman & Wakefield | Morgan Stanley Bank N.A. Valuation of: Holiday Inn Express, Frankland Road,

Valuation Date: 1 May 2019 Blagrove, Swindon, SN5 8UD

10. Principal Valuation Considerations

Location / Situation and Competition

The hotel is well located within close proximity to the M4, allowing excellent accessibility. Swindon

town centre is easily accessible by car approximately four miles north of the Property. While a

town centre location would allow for improved rail connectivity and proximity to business and

amenities, the location of the hotel benefits from the unparalleled access to the M4 and associated

business.

From an investment perspective Swindon would be viewed as a secondary hotel market.

Building Design / Condition / Suitability

The hotel is in good condition having been well maintained over the years and recently

refurbished. The design of the building is functional and fit for purpose.

Tenure

The hotel will be held on long lease for a term of 125 years with a buy back option at year 60 for

£1.

There is limited comparable evidence of the sale of long leasehold as the structure is relatively

new within the hotel market. We would however expect there to be a narrower pool of purchasers

for the leasehold interest compared to the freehold interest, which will result in the interest

achieving a softer yield.

We consider the yield gap between a freehold interest and a ground lease interest will be

influenced by a number of factors including location, quality of the asset and rent cover. The yield

gap will also be influenced by whether the hotel is sold as part of the existing portfolio or as a

single asset. We consider that there is likely to be a wider yield gap if sold as a single asset as

the hotel will lose some of its appeal and economies of being operated as part of a larger platform.

The proposed rent payable will be £131,192 per annum subject to annual increases in line with

RPI with a cap and collar of 0% and 5%. The proposed rent represents 15% of the 2018 NOI.

We consider the proposed rent to fall within an acceptable range of NOI based on other

transactions that have occurred in the market providing sufficient rent cover in the short term.

Business & Income Security

The hotel is a stable business and well established in its local market being one of the strongest

performing hotels. The hotel has produced relatively consistent levels of revenue and net

operating profit with the profit margin being achieved good.

Whilst the profitability of the hotel has been good there is potential for the current margins to be

eroded by the proposed ground rent in the event that earnings do not keep pace with RPI.

Asset Management Opportunities

There is limited scope for additional growth through specific asset management. The hotel is

essentially at a stabilised trading position.

Saleability

Current Sale Prospects

What is the estimated period it would take to sell the Property at 6-9 months

Market Value?

Purchaser demand is likely to be Good

17You can also read