Top players in the European AV industry - Ownership and concentration 2021 Edition - Coe

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Top players in the European AV industry

Ownership and concentration

2021 Edition

Laura Ene (Author)

Agnes Schneeberger (Contributor)

January 2022

A publication of the European Audiovisual Observatory

Table of Contents Key insights Methodology Key indicators Operating revenues structure for top 100 AV groups in Europe Pay TV market structure by subscriptions in Europe SVOD market structure by subscriptions in Europe Pay AV services market structure by subscriptions in Europe Broadcast service market structure by number of TV channels in Europe On-demand service market structure by number of platforms in Europe AV services market structure by number of TV channels and ODAS in Europe TV market structure by audiences in Europe TV fiction market structure by number of titles produced in Europe Cinema market structure by number of screens in Europe Additional Methodological Notes

Key insights

The top 100 audiovisual companies in Europe showed some resilience to the COVID-19 pandemic

which has been accelerating pre-existing market trends. Their cumulated operating AV services

revenues grew slightly more (+7.7% over 2016 at the end of 2020) than average inflation and the

overall market. This was due to several factors:

Not all market segments have been equally impacted. Players whose business models are

primarily based on pay TV and public funding proved more resilient. Those relying on

advertising were more severely affected.

The SVOD market has been thriving, significantly boosting the revenues of SVOD players

across the board. Cumulated revenues of the pure SVOD players (Netflix, Amazon and DAZN)*

among the top 100 audiovisual companies quadrupled over the five-year period, comprising

7% of cumulated revenues for the top 100 at the end of 2020.

*No separate data on European operations was available for Apple TV+

Key insights

The top 100 developed against a very dynamic backdrop of M&A and divestment activities pushed up

by the streaming wars and the pandemic crisis.

Consolidations helped bolster the top 100 companies’ revenues

These consolidations followed different rationales: obtaining more, premium content at

competitive prices, seeking to pair that content with strong distribution, or just eyeing

access to new markets. The players moved horizontally (i.e. acquisition of TVN by Discovery

in the takeover of Scripps Network Interactive, acquisition of Fox International Channels and

NGC Europe by Disney in the takeover of 21st Century Fox, acquisition of Sanoma’s Dutch

unit by DPG Media), and vertically (i.e. acquisition of TV4 Media by Telia, acquisition of CEME

by PPF Group), as well as in the direction of market extensions (i.e. acquisition of TDC

Norway by Telia, acquisition of DNA by Telenor, acquisition of Forthnet and Vivacom by

United Group) in a quest to strengthen market positions.

At times these consolidations impacted the audiovisual sector indirectly since they were

primarily telco-driven (i.e. acquisition of UPC operations in Europe from Liberty Global by

Vodafone). These were more generally moves designed to build strong convergent telco

offers or to feed content into platforms or simply to expand to new territories.

Conversely, a series of divestments were also registered between 2016 and 2020, with several

actors refocusing on their strongholds, be these core businesses or key territories (i.e. MTG

transformation into a global digital entertainment company, Kinnevik turning to their primary

telco business, Grupo Prisa accelerating the digital transformation, Sanoma transforming into a

learning and cross-media company).

Key insights

Moreover, the structure of the top 100 audiovisual groups in Europe by operating AV revenues

experienced several significant evolutions between 2016 and 2020:

Public players saw their weight in revenues diminish between 2016 and 2020 (down by 3% to

31%). Although not too strongly affected by COVID-19, PSB revenues decreased over the same

period by 0.4% in real terms. Also, these players were not part of the consolidation game.

Overall, the revenues of the traditional players have more or less stagnated, while the growth of

the top 100 players was largely driven by the new SVOD players. Traditional telco players kept

their share of the top 100 revenues stable over the five-year period (around 16%), while

traditional broadcasters lost 5% in weight (down to 77% at the end of 2020). By contrast, pure

SVOD players namely Netflix, Amazon and DAZN, accounted cumulatively for more than 75% of

the revenue growth registered between 2016 and 2020 at the top 100 level.

Concentration levels remain largely the same among the top 100 European AV groups by

operating revenues over the analysed period. Over the five-year period, the top 20 players

consistently accumulated between them around 70% of top 100 revenues. This percentage would

have risen to 85% were it not for the PSBs weakening concentration.

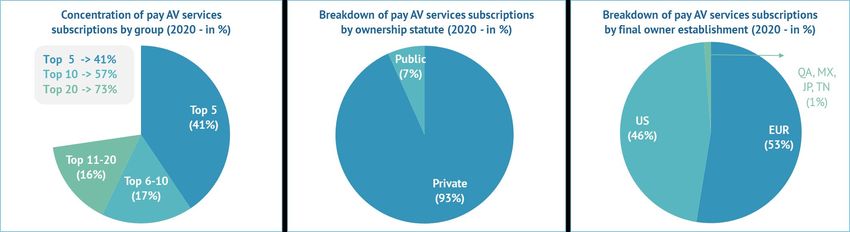

The private European AV sector tends however to be less concentrated than the US one. The top

five private European AV players account for 53% of top 20 revenues as opposed to 62% for

players on the US market.

Key insights

Significant changes have been also registered from a geoeconomics perspective:

The weight of US interests in top 100 revenues has increased (by +4% up to 31% in 2020) due to

the rise of the pure SVOD players. US-backed AV players in Europe particularly stand out in the

private sector where they comprised 44% of the main players’ revenues at the end of 2020. Two

thirds of the US share were accounted for by Sky, Netflix, Amazon and DAZN.

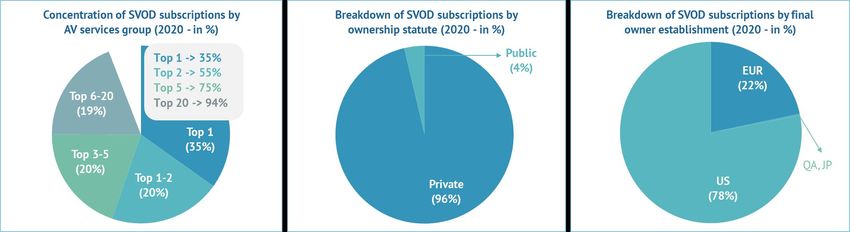

The share of US interests is by far the highest in the SVOD market, with around four in five

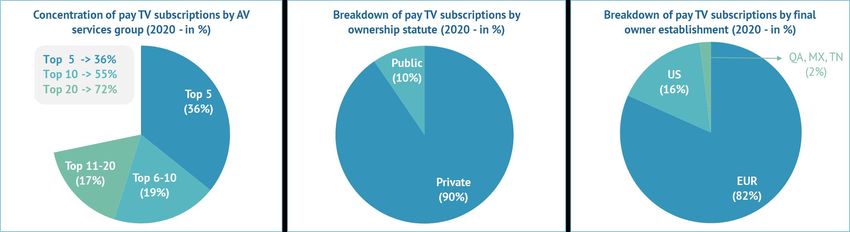

subscriptions signed off by a US-backed OTT platform. By contrast, pay TV remains largely a

European-driven business (US-backed companies account for only 16% of subscriptions).

US interests are less significant as regards TV audiences (only 11% of viewing time) as most of the

main national broadcasters are still controlled by European interests. However, US-backed

broadcasters are likely to claim a larger share of advertising as PSBs are bound to access only a

limited share.

Nevertheless, US groups have managed to roll-out a large range of thematic channels and

catalogues all over Europe, which is reflected in a comparatively higher share by number of TV

channels (19%) and on-demand services (25%) operated in Europe. Discovery, Sky, ViacomCBS and

Disney are the top four networks in Europe by number of TV channels, while Discovery and Disney

also rank among the top four groups by number of on-demand services.Key insights

Even if US-backed groups have started to increase their operative presence in Europe for TV

content production, their contribution as (executive) producers of European TV fiction titles is still

limited (only 6% of the total number of TV fiction titles produced in Europe between 2015-2019).

Overall, the degree of internationalisation is following an upward trend regarding US interests.

However, US players are starting to prioritise expansion by investing in direct-to-consumer

business models (chiefly SVOD platforms) and producing locally as opposed to traditional indirect

investments.

The consolidation operations have not impacted the share of US players:

On the one hand, the largest mergers and acquisitions took place primarily between already-

US-backed companies or between companies controlled by European interests.

On the other hand, there were also registered divestments of European assets by US groups

(i.e. AT&T sale of WarnerMedia's stake in CEME to PPF Group).

To a lesser extent, emergent markets such as the CEE countries have registered a more rapid

increase in revenues compared to the other regions represented in the top 100. Their share of the

top 100 revenues grew from 4% in 2016 to 5% at the end of 2020. This is likely explained by

players taking advantage of relatively stronger economic growth as well as of the opportunities

afforded by divestments of US groups regarding investment and the strengthening of market

positions. This phenomenon was rather common among the telco-driven businesses.Key insights

The top 100 AV companies in Europe by operating AV revenues are heterogeneous in terms of their

portfolio of activities:

Even if top players tend to be active in several market segments, most appear to be driven by one

leading activity. Among them, the highest-ranking ones tend to also hold a strong position in at

least one additional activity.

For broadcasters and TV packagers, diversifying into TV production seems a common strategy as,

probably, an answer to the threat of on-demand over-the-top services.

High-ranking companies in terms of audiences are relatively better represented among the top

players by revenues as opposed to players topping other market segments. However, the higher

the position occupied by a player in terms of revenues, the greater the incidence of players

ranking highest on the SVOD or TV production market.Key insights

This diversity of portfolios among the top 100 companies determines different levels of concentration

in individual market segments, as well as different levels of involvement when it comes to PSBs:

SVOD and pay TV stand out as the most concentrated audiovisual market segments in Europe. A

total of 94% of SVOD subscriptions are cumulatively signed off to top 20 OTT platforms, while

72% of pay-TV subscriptions are cumulated by top 20 pay-TV operators.

At the other end of the spectrum, the operations of TV channels and ODAS (measured in number

of services) are least concentrated, with the top 20 players cumulating around one third of each

respective market segment. The private sector operates 91% of TV channels and 97% of ODAS.

Audiences tend to be more concentrated, with the leading 20 broadcasters accounting for 56% of

viewing consumption in Europe, followed by the TV production market (measured in number of TV

fiction titles) with the top 20 production companies cumulating up to 41% of titles.Key insights

This diversity of portfolios among the top 100 companies determines different levels of concentration

on individual market segments, as well different levels of involvement when it comes to PSBs:

Even if under-represented in terms of volumes (9% of TV channels and 3% of ODAS), PSBs

accounted for one third of global viewing consumption in Europe mainly thanks to strong

generalist channels that appeal to a larger public and with almost all of them offering at least

one on-demand service at the end of 2020. Also, they are relatively better represented in the TV

production business (accounting for 16% of the total number of TV fiction titles produced in

Europe between 2015 and 2019, a lower share than that commissioned, as private broadcasters

more often internalise production).

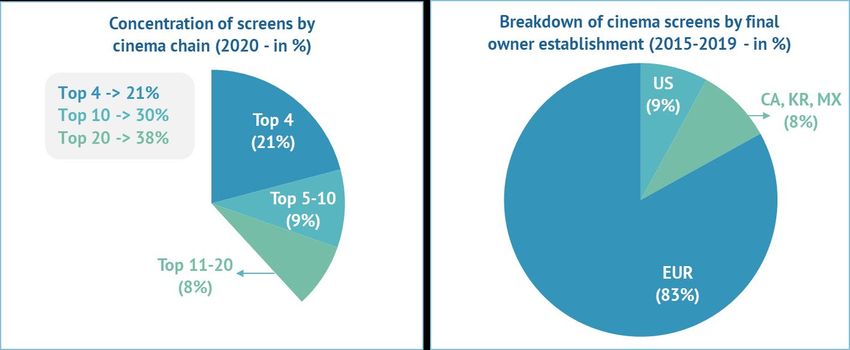

As regards cinema, the top 20 cinema chains account for 38% of cinema screens in Europe. It

remains a largely European-driven business with only 17% of cinema screens controlled by non-

European interests (of which 9% are US-backed).Methodology

Data providers

Based on the analysis of data collected by the European Audiovisual Observatory, and data from

the Observatory’s MAVISE database, as well as data provided by Ampere Analysis, Glance and

European Metadata Group.

Scope

The scope of analysis includes 40 European countries covered by the European Audiovisual

Observatory, provided that data was available.

Indicators and definitions

Figures in the report are presented at the European group level and reflect in general the

situation for the year 2020. Exceptions: for the number of TV fiction titles, figures are cumulated

for 2015-2019, to level out variations. For 10 out of the top 100 groups for which 2020 data was

not available, 2019 and 2018 revenues were used. To analyse revenues in evolution, 2016 data

was used as a benchmark.Methodology

Indicators and definitions

The indicators analysed at the European group level are: revenues, pay-TV subscriptions, over-the-

top SVOD subscriptions, number of TV channels, number of on-demand services (ODAS), audience

share, number of TV fiction titles and number of cinema screens.

The European Audiovisual Observatory collects on a yearly basis revenue data for the main

audiovisual players in Europe by relying on desk research, corporate annual reports, companies

houses, the Amadeus database for public and private companies across Europe and data from the

EBU’s Media Intelligence Service. Revenues presented in this report have been analysed for

European groups primarily active in the AV services sector and they derive mainly from the

exploitation of these AV services (including radio). Revenues of the groups in Europe were

estimated in several cases by cumulating the revenues of their main subsidiaries. They should not

be therefore considered as consolidated results in the proper sense, as subsidiaries may have

exchanges between themselves.

Ownership information about European and final owner groups reflects the situation at the end of

2020. There has been a best-effort assessment of ownership and alignment across the different

market segments by the EAO.Methodology

Indicators and definitions

For jointly owned assets, the indicators have been equally distributed between all parties.

Market shares, concentrations and breakdowns by establishment or statute of final owner are

calculated from the total sample available or total market; these calculated indicators are not

limited to the top 20 and/or 50 showcased in this report.

When several companies rank in the same position, those companies active in several market

segments have been prioritized for inclusion in the top listings.

Considering that the data samples used for analysis are neither exhaustive nor complete, the

figures presented in this report should be regarded as indicative and not exact.Key indicators Operating revenues structure for top 100 AV groups in Europe Pay TV market structure by subscriptions in Europe SVOD market structure by subscriptions in Europe Pay AV services market structure by subscriptions in Europe Broadcast service market structure by number of TV channels in Europe On-demand service market structure by number of platforms in Europe AV services market structure by number of TV channels and ODAS in Europe TV market structure by audiences in Europe TV fiction market structure by number of titles produced in Europe Cinema market structure by number of screens in Europe

Operating revenues structure for top 100 AV groups in Europe

Top 20 European AV groups by operating AV services revenues (2020 - in mEUR)

Market shares of AV group by (%)

Country of Revenues Top 100

Rank AV group Country Statute Final owner

final owner (EUR million) PayTV SVOD # TV # VOD TV TV fiction

AV group

subs. subs. channels services audiences titles

revenues

1 Sky GB Private Comcast US 16 279 13.3% 9.7% 1.3% 3.2% 1.6% 1.4% 0.1%

2 ARD DE Public State of DE DE 6 527 5.3% 0.3% 0.1% 3.0% 7.3%

3 Netflix (Europe) NL Private Netflix US 6 152 5.0% 34.9% 1.5%

4 RTL Group LU Private Bertelsmann DE 6 017 4.9% 1.3% 1.2% 1.1% 4.5% 3.7%

5 BBC GB Public State of GB GB 5 674 4.6% 1.3% 0.4% 2.6% 2.3%

6 Groupe Canal Plus FR Private Vivendi FR 5 498 4.5% 3.8% 0.8% 1.2% 1.9% 0.8% 1.1%

7 ProSiebenSat.1 Media DE Private ProSiebenSat.1 Media DE 4 047 3.3% 0.3% 0.5% 0.3% 1.9% 0.1%

8 The Walt Disney Company (Europe) EUR Private The Walt Disney Company US 3 876 3.2% 8.2% 2.7% 2.4% 2.1%Pay TV market structure by subscriptions in Europe

Top 20 European AV groups by number of pay TV subscriptions (2020 - in thousands)

Market shares of AV group by (%)

Country of Subs. Top 100

Rank AV Group Country Statute Final owner

final owner (thousand) PayTV SVOD # TV # VOD TV TV fiction

group

subs. subs. channels services audiences titles

revenues

1 Vodafone GB Private Vodafone GB 20 989 10.0% 0.1% 0.5% 2.2%

2 Sky GB Private Comcast US 20 384 9.7% 1.3% 3.2% 1.6% 1.4% 0.1% 13.3%

3 Tricolor TV RU Private Tricolor TV RU 12 257 5.9% 0.3% 0.1% 0.2%

4 Rostelecom RU Public State of RU RU 10 823 5.2% 2.3% 0.1%SVOD market structure by subscriptions in Europe

Top 20 European AV groups by number of SVOD subscriptions (2020 - in thousands)

Market shares of AV group by (%)

Country of Subs. Top 100

Rank AV Group Country Statute Final owner

final owner (thousand) SVOD Pay TV # TV # VOD TV TV fiction

group

subs. subs. channels services audiences titles

revenues

1 Netflix (Europe) NL Private Netflix US 62 470 34.9% 1.5% 5.0%

2 Amazon Prime Video (Europe) EUR Private Amazon Inc US 36 507 20.4% 0.1% 1.6% 1.4%

3 Apple (Europe) EUR Private Apple Inc US 15 097 8.4% 2.2%

4 The Walt Disney Company (Europe) EUR Private The Walt Disney Company US 14 637 8.2% 2.7% 2.4% 2.1%Pay AV services market structure by subscriptions in Europe

Top 20 European AV groups by number of subscriptions to pay AV services (2020 - in thousands)

Market shares of AV group by (%)

Subs.

Country of Pay TV & Top 100

Rank AV Group Country Statute Final owner

final owner SVOD PayTV SVOD # TV # VOD TV TV fiction

group

(thousand) subs. subs. channels services audiences titles

revenues

1 Netflix (Europe) NL Private Netflix US 62 470 34.9% 1.5% 5.0%

2 Amazon Prime Video (Europe) EUR Private Amazon Inc US 36 507 20.4% 0.1% 1.6% 1.4%

3 Sky GB Private Comcast US 22 727 9.7% 1.3% 3.2% 1.6% 1.4% 0.1% 13.3%

4 Vodafone GB Private Vodafone GB 20 989 10.0% 0.1% 0.5% 2.2%

5 Apple (Europe) EUR Private Apple Inc US 15 097 8.4% 2.2%

6 Rostelecom RU Public State of RU RU 14 907 5.2% 2.3% 0.1%Broadcast service market structure by number of TV channels in Europe

Top 20 European AV groups by number of TV channels (2020)

Market shares of AV group by (%)

Country of No. of Top 100

Rank AV Group Country Statute Final owner

final owner TV channels # TV # VOD PayTV SVOD TV TV fiction

group

channels services subs. subs. audiences titles

revenues

1 Discovery Inc (Europe) EUR Private Discovery US 353 6.4% 3.9% 1.3% 3.0% 1.3% 2.6%

2 Sky GB Private Comcast US 175 3.2% 1.6% 9.7% 1.3% 1.4% 0.1% 13.3%

3 ViacomCBS (Europe) EUR Private ViacomCBS Inc US 162 2.9% 1.3% 1.6%On-demand service market structure by number of platforms in Europe

Top 20 European AV groups by number of on-demand services (2020)

Market shares of AV group by (%)

No. of

Country of Top 100

Rank AV Group Country Statute Final owner on-demand

final owner # VOD # TV PayTV SVOD TV TV fiction

services group

services channels subs. subs. audiences titles

revenues

1 Discovery Inc (Europe) EUR Private Discovery US 106 3.9% 6.4% 1.3% 3.0% 1.3% 2.6%

2 Google (Europe) EUR Private Alphabet US 90 3.3%

3 Rakuten Europe ES Private Rakuten Inc JP 74 2.7% 0.1%

4 The Walt Disney Company (Europe) EUR Private The Walt Disney Company US 67 2.4% 2.7% 8.2% 2.1%AV services market structure by number of TV channels and ODAS in Europe

Top 20 European AV groups by number of TV channels and on-demand services (2020)

Market shares of AV group by (%)

Sum of

Country of Top 100

Rank AV group Country Statute Final owner TV channels

final owner # TV # VOD PayTV SVOD TV TV fiction

and ODAS group

channels services subs. subs. audiences titles

revenues

1 Discovery Inc (Europe) EUR Private Discovery US 459 6.4% 3.9% 1.3% 3.0% 1.3% 2.6%

2 Sky GB Private Comcast US 220 3.2% 1.6% 9.7% 1.3% 1.4% 0.1% 13.3%

3 The Walt Disney Company (Europe) EUR Private The Walt Disney Company US 218 2.7% 2.4% 8.2% 2.1%TV market structure by audiences in Europe

Top 20 European AV groups by TV audience (2020 - in million hours)

Market shares of AV group by (%)

Daily total

Country of hours of Top 100

Rank AV group Country Statute Final owner

final owner viewing time TV PayTV SVOD # TV # VOD TV fiction

group

(million) audiences subs. subs. channels services titles

revenues

1 Channel One - Perviy Kanal RU Public State of RU RU 180 5.9% 0.2% 0.1% 0.2%

2 Gazprom Media RU Public State of RU RU 150 4.9% 0.4% 0.4% 0.6% 0.1% 0.4%

3 RTL Group LU Private Bertelsmann DE 137 4.5% 1.3% 1.2% 1.1% 3.7% 4.9%

4 Gruppo Mediaset IT Private Gruppo Mediaset IT 131 4.3% 0.8% 0.6% 0.2% 0.7% 2.2%

5 National Media Group RU Private National Media Group RU 120 4.0% 0.3% 0.1% 0.4%

6 RAI IT Public State of IT IT 96 3.2% 0.3%TV fiction market structure by number of titles produced in Europe

Top 20 European AV groups by number of TV fiction titles produced (2015-2019)

Market shares of AV group by (%)

No. of titles

Country of Top 100

Rank AV Group Country Statute Final owner (2015-2019

final owner TV fiction Pay TV SVOD # TV # VOD TV

cummulated) group

titles subs. subs. channels services audiences

revenues

1 ARD DE Public State of DE DE 369 7.3% 0.3% 0.1% 3.0% 5.3%

2 Banijay Group (Europe) EUR Private Banijay Group FR 236 4.7%

3 RTL Group LU Private Bertelsmann DE 186 3.7% 1.3% 1.2% 1.1% 4.5% 4.9%

4 Mediawan FR Private Mediawan FR 167 3.3% 0.3% 0.4% 0.1%

5 ITV GB Private ITV GB 140 2.8% 0.5% 0.3% 0.4% 1.8% 2.5%

6 ZDF DE Public State of DE DE 131 2.6% 0.1%Cinema market structure by number of screens in Europe

Top 20 European cinema chains by number of screens (2020)

Country of No. of cinema Market

Rank Cinema chain Country Statute Final owner

final owner screens share (%)

1 AMC Theatres (Europe) GB Private AMC Entertainment Holdings US 2 938 7.1%

2 Cineworld Group (Europe) GB Private Cineworld Group GB 2 300 5.6%

3 VUE International GB Private OPE/AIMCo CA 2 052 5.0%

5 Pathé Cinemas FR Private Pathé FR 1 360 3.3%

4 Mars Entertainment Group TR Private CJ-CGV KR 850 2.1%

6 CGR Cinémas FR Private CGR Cinémas FR 686 1.7%

7 United Cinemas RU Private United Cinemas RU 640 1.5%

8 Kinepolis Group BE Private Kinepolis Group BE 586 1.4%

9 UGC Ciné Cité FR Private UGC FR 584 1.4%

10 Cineplex DE Private Cineplex DE 560 1.4%

11 Premier Zal (Magna Tech) RU Private Magna Tech US 505 1.2%

12 Cinestar DE Private Greater Union Filmpalast DE 449 1.1%

13 Yelmo Films ES Private Cinepolis MX 400 1.0%

14 Cineplexx AT Private Constantin Film Foundation AT 347 0.8%

15 Helios PL Private Agora PL 281 0.7%

16 Showcase Cinemas (Europe) GB Private National Amusements US 275 0.7%

17 Kinomax RU Private State of RU RU 268 0.6%

18 Karo Film Management RU Private Concern Karo RU 248 0.6%

19 Nordisk Film Cinemas DK Private Egmont Fonden DK 237 0.6%

20 Omniplex IE Private Omniplex IE 231 0.6%

Download

Top 20 cinema chains

by number of screensAdditional Methodological Notes

Scope

The scope of analysis for each data set includes 40 European countries covered by the European

Audiovisual Observatory, provided that data was available.

Data sets

Revenues

European Audiovisual Observatory analysis of data collected on a yearly basis for the main

audiovisual players in Europe by relying on desk research, corporate annual reports,

companies houses, the Amadeus database for public and private companies across Europe

and data from the EBU’s Media Intelligence Service.

The analysis covers consolidated operating revenues derived mainly from the exploitation of

AV services (including radio) by the top 100 European groups for which the AV services

business is the leading activity as assessed by the European Audiovisual Observatory. Groups

not included: 1) groups mainly providing telecommunication services without details on

video revenues; 2) subsidiaries of US groups with no separate data on European operations

available; 3) groups mainly active in production and distribution of audiovisual works; 4)

cinema chains.Additional Methodological Notes

Revenues of the groups in Europe were estimated in several cases by cumulating the revenues of

their main subsidiaries. They should not be therefore considered as consolidated results in the

proper sense, as subsidiaries may have exchanges between themselves.

The figures represent revenues in EUR million, at the current rate for the year 2020. There are

several groups for which 2020 data was not available and instead 2019 data was used: The Walt

Disney Company (Europe), Discovery Inc (Europe), ViacomCBS (Europe), BeIn Media (Europe), DAZN

Group, Bauer Media, Global Media & Entertainment, NOS (NL), COPE and Warner Media.

Conversion from local currencies to EUR is based on the actual dates of the companies' fiscal year.

Additional notes for specific groups for which revenues required compilation:

The Walt Disney Company (Europe) = combined 2019 revenues of The Walt Disney Company Limited, NGC

Europe and Fox International Channels. Includes film production and distribution activities and therefore

cannot be compared to the revenues of other US studios in Europe

Discovery Inc (Europe) = combined 2019 revenues of Discovery Communications Europe, TVN SA, Eurosport

and 50% All3 Media

Vodafone = combined 2020 revenues of network video services and 25% of Sport TV Portugal

Bouygues = combined 2020 revenues of TF1 and network video services

Liberty Global = combined 2020 revenues of network video services and 50% of All3Media

Warner Media (Europe) = combined 2019 revenues of Turner Broadcasting System Europe Limited and HBO

(Europe). HBO revenues estimated by combining last available revenues of subsidiaries in the Czech

Republic, Poland, the Nordic countries, Romania, Bulgaria and Hungary.Additional Methodological Notes

NENT = combined 2020 revenues of Nent and 50% of Allente

ViacomCBS (Europe) = combined 2019 revenues of Viacom International Networks in Belgium, the Nordic

countries, Hungary, Italy and the UK, and of Nickelodeon UK, Nickelodeon International and Channel 5 UK,

and the 2018 revenues of Viacom International Networks in Germany

Altice Europe = combined 2020 revenues of network video services, Next Radio TV and 25% Sport TV

Portugal

BeIn Media (Europe) = combined 2019 revenues of BeIn Media IP, Digiturk and BeIn Connect

Telia = combined 2020 revenues of network video services and TV4 Media

Telenor = combined 2020 revenues of network video services and 50% of Allente

PPF Group = combined 2020 revenues of O2 Czech Republic and Central European Media Enterprises (as of

2020)

Gazprom Media = combined 2020 revenues of Telekompaniya NTV, Natsionalnyi Sportivnyi Telekanal, Red

Media and NTV-Plus

NOS (PT) = combined 2020 revenues of network video revenues and 25% of Sport TV PortugalAdditional Methodological Notes

PayTV

European Audiovisual Observatory analysis based on 2020 pay-TV subscription data

provided by Ampere Analysis.

SVOD

European Audiovisual Observatory analysis based on 2020 over-the-top SVOD subscription

data provided by Ampere Analysis.

TV channels and on-demand services (ODAS)

European Audiovisual Observatory analysis based on 2020 figures from the MAVISE

database.

Data is presented in number of TV channels and on-demand services, each cumulated at

European group level.Additional Methodological Notes

Audiences

European Audiovisual Observatory analysis based on 2020 audience data provided by

Glance.

The figures represent a calculated European audience market share that is comparable

across different national markets. The European audience market share per audiovisual

group corresponds to the sum of daily hours of TV channels belonging to one group divided

by total daily hours in Europe, multiplied by 100. Total viewing time in Europe corresponds

to the average daily television viewing time per person per country multiplied by the total

population per country (source EUROSTAT).

Data for Bosnia and Herzegovina is based on 2019 figures for daily audience shares and

Eurostat population numbers, and 2016 data for daily viewing time.

The data sample includes TV channels with a daily market share of at least 0.1%. The same

TV channel can be available in several national markets.Additional Methodological Notes

Production of TV fiction

European Audiovisual Observatory analysis based on European Metadata Group data on TV

fiction titles by main production company.

The figures represent TV fiction titles broadcasted between 2015-2019 and cumulated at

European production group level for the given period to level out variations for this

indicator. One “title” refers to either a TV film or a TV season. Each different TV season of a

TV series is counted as one title.

The ownership information reflects the market realities at the end of 2020.

Cinema screens

European Audiovisual Observatory data collection and analysis of estimated number of

screens by selected exhibitors in Europe at the end of 2020.

The figures represent number of cinema screens at exhibitor level in Europe.

Breakdown of number of screens by final owner establishment was calculated based on the

assumption that half of the screens for which ownership data was not available were owned

in 2020 by European exhibitors.More information: www.obs.coe.int

You can also read