THE THREE NEEDS AND THREE RISKS FOR RETIREES CHAD PADOWITZ CFA - CIO TALARIA - FSITV

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The three needs and three risks for retirees

Chad Padowitz CFA – CIO Talaria

Contents

• Retirement investing is different

• How income is impacted by needs and risks

• A unique solution to the income problem

2Important information

Wholesale Clients Only. The information contained in this presentation is made available onlyfor persons who are wholesale clients or sophisticatedinvestors within the meaning

oftheCorporationsAct2001(Cth).Itmaynotbedistributedorreplicated in any form, to anyone who is not a wholesale client or sophisticated investor in Australia.

No Reliance. This document is produced by Talaria Asset Management Pty Limited (Talaria) ACN 130 534 342, AFS Licence No 333732 and based on information available at

the time of the presentation. The information herein is factualand believed to be accurate as at the time of the presentation.

Illustrative information only. This presentation is not, and is not intended to be, an offer or invitation for subscription or sale, or a recommendation, with respect to any

financial product discussed herein, nor is it to form the basis of any contract or commitment. Such an offer would only be made by distribution of an offering memorandum

relating to any such financial products offering recipients of this presentation should therefore place no reliance on the content of this presentation when making any

decision to invest. Any examples or information provided in this document are for illustrative and discussion purposes only and do not represent a recommendation or

Talaria’s view on future events and in no way bind Talaria. The presentation and this document do not purport to be a complete statement or summary. The Talaria Global

Equity strategy is available through the Talaria Global Equity Fund (Fund) Wholesale Units ARSN 132 393 705. The Fund is issued by Australian Unity Funds Management

Limited ABN 60 071 497 115 AFS Licence No. 234454. In deciding whether to acquire, hold or dispose of the product you should obtain a copy of the Fund’s Product Disclosure

Statement (PDS) and consider whether the product is appropriate. A copy of the PDS is available at the website australianunity.com.au or by calling the Client Services team

on 13 29 39.

This presentation is confidential and should not be distributed by the recipient in whole or in part to any other person without obtaining the prior written consent of Talaria

Asset Management Pty Limited.

© 2020 Talaria Asset Management Pty Limited

3Markets and economies have shifted

FAANMGs bigger than entire Japanese Stock Market

Apple’s market cap greater than FTSE100

US 10-year Treasury Rate 0.74% v long term average of 4.43%

Company dividends down 20-40%

Australian GDP – 7% for the June quarter

AU Gov’t Stimulus $289bn+ …

Sources: Bloomberg, Fairfax

4Retirement investing is different

Retirement investing is different

To achieve the 3 big retirement needs...

Retirement Needs

Income Growth Certainty

The 3 key risks need to be avoided

Income level risk Inflation risk Volatility risk

Longevity Above inflation growth Sequencing

6Adviser conundrum

• Advisers face a structural mismatch

Change In Importance of Investment Outcome Risk Over Time

• Clients seek income but industry

offers capital solutions

• Accumulation products vs.

Relative Importance

Retirement products

o As investors transition to

retirement capital protection

becomes more important

Accumulation Late Stage Accumulation Retirement

Age

Relative / Opportunity Cost Absolute

7Income adequacy

ASFA Standard Comfortable Annual Spending Needs

• Is the ASFA standard

enough? $80,000

Retirement Needs

$60,000

• What level of

savings do you need $40,000

to achieve it?

$20,000

$0

Single Couple

($20,000)

($40,000)

ASFA Standard Pension Shortfall

Sources: Google, ASFA, ATO

8Dividends (income) have played the key role in total returns

Retirement Needs

Source: Bloomberg

9So retirees require

▪ Capturing the market’s gains, less of its

declines

▪ Lower volatility – smoother journey

▪ Consistent income generation - a buffer

against loss

10How income is impacted by needs and risks

Risks: Inflation, concentration and duration

Retirement Needs

Source: Bloomberg, As at 25.9.20

12Valuation (duration) risk

Top 10 Index P/E

1 Year Performance - July 2020 Performers* Ratio

Retirement Needs Apple 35x

Amazon.com 71x

Top 10 Index Other 1,529 Index Total MSCI World TALARIA Microsoft 34x

Performers Members (ex Aus) Index MSCI VALUE (pre-fees)

10% Tesla 192x

6.4%

NVIDIA 55x

5% 3.4%

Alphabet 29x

0% Facebook 30x

-2.1%

-5% -2.9% PayPal Holdings 56x

-10% Shopify 547x

Adobe 48x

-12.3%

-15%

Avg. P/E Ratio 49x

Based on 12 month return to 31 July 2020. Source: Bloomberg,

*Index as at September 2020, Avg. P/E Ratio based on harmonic mean

13Traditional portfolio construction (60/40) is broken

Traditional income

sources are no longer

offering the same

returns…

There are more cuts to

come.

The result: Ongoing

uncertainty ahead!

Source: Bloomberg, Talaria

Talaria Yield based on 12-month Distribution Return as at 31 March 2020 for Talaria Global Equity Fund – Wholesale Units

15Lower returns ahead, new tools needed

The Dividend Swap Market shows an anticipated further decline in dividends is

being priced for 2021 v 2019 levels

0%

-10%

USA Europe

–20% –20% Australia

-30%

-20%

-30%

-40%

Source: Bloomberg, As at 25.9.2020How much do you need?

▪ Massive problem for

retirees today.

▪ US$1 million no longer

generates a US$50,000

income for

retirement.

▪ Today, it is just

US$6,900 p.aHow much do you need?

▪ Need closer

to US$

8millionA unique solution to the income problem

What are the other income sources?

Genuinely uncorrelated, persistent proven income

• Banking / Shadow banking

• Catastrophe insurance

• Equity insurance

20Getting paid for taking risk – An Insurance Mindset

A different approach to buying shares

Typical insurance premiums

Turn ‘theoretical’ return into ‘real’

return

Life

o

Insurance

Consumers pay to protect

homes, lives, cars

0.1% p.a .

o Insurers receive the premium for 0.3% p.a .

accepting risk

So, what about investors?

2.5% p.a . Sha res???

Insurance premium costs based on estimates provided by insurers. Share market insurance defined as annualized return on near the money American put options.

Past performance is not a reliable indicator of future performance.Getting paid for taking risk – An Insurance Mindset

A different approach to buying shares

Investors pay 15-20%+ p.a. to protect Typical insurance premiums

shares.

Life

o Generates income Insurance

o Diversifies sources of return

0.1% p.a . 0.3% p.a .

o Creates buffer against loss

Selling Put Options = Selling Insurance on

Shares

2.5% p.a . 15-20% p.a.

Insurance premium costs based on estimates provided by insurers. Share market insurance defined as annualized return on near the money American put options.

Past performance is not a reliable indicator of future performance.EQUITY INSURANCE EXAMPLE

Trade on offer: Sell August 2020 Put

Available Trades:

Maturity date Oct 2020

Date: August 2020

Share Price ($): 68.13

Strike Price ($): 62.50

Source: Talaria, Bloomberg

For illustrative purposes only and not a recommendation to buy or sell a particular stock

23EQUITY INSURANCE EXAMPLE

Trade on offer: Sell August 2020 Put

Available Trades:

Maturity date Oct 2020

Date: August 2020

Share Price ($): 68.13

Strike Price ($): 62.50

Option Price (Premium $): 2.17

Annualised Option Premium Return: 22.17%

Source: Talaria, Bloomberg

For illustrative purposes only and not a recommendation to buy or sell a particular stock

24EQUITY INSURANCE EXAMPLE

Trade on offer: Sell August 2020 Put

Available Trade:

Maturity date Oct 2020

Date: August 2020

Share Price ($): 68.13

Strike Price ($): 62.50

Option Price (Premium $): 2.17

Annualised Option Premium Return: 22.17%

Total Buffer To Loss ($): 7.80

Total Buffer To Loss (%): 11.5%

Dividend Yield: 6.20%

Price / Earnings Ratio: 5.7

Source: Talaria, Bloomberg

For illustrative purposes only and not a recommendation to buy or sell a particular stock

25Consistent income from diversified sources

We generate consistent income as part of the total fund return.

This comes from a variety of sources creating more stable returns to investors.

16.0%

14.0%

12.0%

10.0%

8.0%

6.0%

4.0%

2.0%

0.0%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

-2.0%

Option Premium Interest Dividends Annualised

Source: Talaria, 2020 reflects calendar year to September 2020

Option premium generated is on capital account and is therefore not always distributable.

26Consistent income from diversified sources

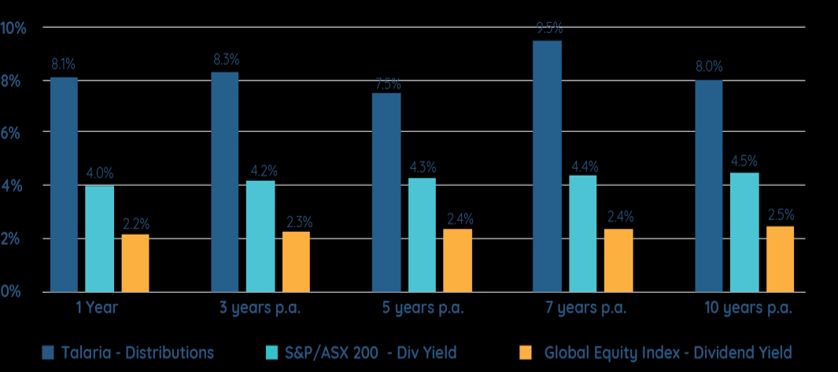

Historically higher distributions than both domestic and foreign industries.

Talaria Global Equity Fund distribution calculations based on the distributions paid in each financial year, using financial year starting values to determine annual distribution yield to June 2020

S&P/ASX 200 and MSCI World (ex Aus) Index (MXWO) Dividend Yields = 12mth DY. Source: Bloomberg

Sources: Bloomberg, FactSet,Talaria

Numbers may not sum due to geometric compounding and rounding. Past performance is not an indicator of future performance

27Consistent income from diversified sources

Enjoy a smoother ride to the end result, less volatility is always better

Standard Deviation

(Rolling 3 year, annualised quarterly returns)

14%

12%

10%

Structurally lower

8% volatility than

broader market

6%

4%

Benchmark Talaria

2%

0%

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18 Jan-19 Jul-19 Jan-20 Jul-20

Source: Talaria, Bloomberg

Based on quarterly returns of Talaria Global Equity Strategy (Foundation Units) (pre-fees) January 2015 – July 2020

Past performance is not an indicator of futureperformance

28So retirees require

Retirees need an alternative and more stable source of income

generation now.

Retirees need less volatility to enjoy their retirement.

Retirees need to diversify their sources of return.

There is a solution that creates greater retirement certainty.

1

2You can also read