The Climate100 Index april 2021 - Tortoise Media

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

In partnership with The Climate100 Index april 2021

Contents

Introducing the Climate100 Index 3

Meet the FTSE 4

The Rankings 5

The Findings 6

Who’s leading in the Climate100 Index? 6

Who’s lagging behind? 6

Measuring emissions 6

Top Emitters – all direct and indirect emissions 8

Who’s decreased emissions? 10

Who’s increased emissions? 11

Emissions intensity 12

Energy 14

Water 15

Waste 15

The CDP 15

The path to net zero 15

Inside the Index 17

Guiding Principles 18

Talk vs Walk 18

Tortoise Media

22 Berners Street

Fitzrovia

London w1t 3lp

© Tortoise Media 2021. No part of this index

may be reproduced without permission. All

rights reserved

Report by the Tortoise Intelligence team.

Any queries, or suggestions about the

Climate100 Index, please contact

r100@tortoisemedia.com

Design: Oliver Bothwell, Nick Stone In partnership with

Cover illustration: Julia AllumIntroducing the Climate100 Index

Welcome to the Tortoise Climate100 Index, in partnership with Teneo. This special report

coincides with the bi-annual update of the Responsibility 100 Index, our ranking of the FTSE

100 companies on their commitment to key social, environmental and ethical objectives.

The Climate100 Index is a detailed assessment of the climate-related data drawn from the

Responsibility100 Index, and measures the gap between the words and actions of some of the

world’s biggest and most carbon-intensive companies.

A firm commitment to divestment, decarbonisation and sustainability has never been more

urgent for the FTSE 100. The welfare of the planet is a crucial factor in determining the well-

being of all life on Earth, and companies must act fast to ameliorate the many severe processes of

climate change that are already underway.

In this year of decisions, and in the run up to COP26, the companies of the FTSE 100 face an

emergency. Those that make and follow through on substantial commitments to alter their

course and address climate change deserve recognition. Those that do not must be held

accountable.

The Climate100 Index focuses on the factors that are important to this change, and presents a

comprehensive data set and ranking based on the climate-related aspects of the FTSE 100’s

actions.

We are delighted to present the 2021 index in partnership with Teneo, a global advisory firm that

provides strategic counsel to CEOs and senior executives of the world’s leading companies,

across their full range of key objectives and issues. As CEOs face an imperative to prioritise ESG

as a key aspect of value creation no company can ignore, silo, or treat as a supplementary

practice.

We hope you find the index and information contained in this report insightful and informative

as work in collaboration to accelerate the journey to net zero.

Alexandra Mousavizadeh

Editor & Partner, Tortoise Media

“2021 will be a pivotal year for the FTSE100. Leadership is rising to the climate

challenge and to the public’s desire for a fairer society. They are re-setting

ambitions to accelerate innovation and action. The Responsibility 100 is one

good way for all their stakeholders to track their progress.”

Fraser Hardie

Chairman, Teneo UK

In partnership with

3 of 19Meet the FTSE

The FTSE 100 are the largest group of companies on the London Stock Exchange, by market

capitalisation. These companies are often sector leaders, large employers and market innovators.

Their actions are an indicator of the current business environment and a standard for other

businesses around the world. The FTSE 100 have offices and subsidiaries all over the world,

meaning that smaller subsets of their operations span the entire globe and affect international

markets and supply chains.

In their most recent reporting year;

– the companies made a combined revenue of £1.59 trillion

– employed a total of 4.1 million people

Engineering Services Extraction Retail & Finance Travel Pharma

consumer

Aerospace Digital Energy Beverage Banking Travel Pharmaceuti-

Services cals

Chemicals Media Mining Consumer Financial

Goods Services

Construction Software Fashion Insurance

Engineering Support Packaging Real Estate

Services

Industrials Telecommuni- Supermarkets

cations

Utilities Tobacco

Where are the FTSE 100 headquartered?

United Kingdom

87

Luxembourg

1

Ireland Czechia

5 1

Netherlands

1

Mexico

1

Australia

South Africa 2

1

In partnership with

4 of 19The Rankings

Land Securities, a property development company, leads the inaugural rankings of the

Climate100 Index, updated as of 29 April 2021.

Top 50 companies Bottom 50 companies

lk

lk

p

p

lk

lk

Wa

Wa

Ga

Ga

Ta

Ta

Land Securities 1 1 0 Antofagasta 51 74 23

British Land 2 6 4 St. James’s Place plc 52 59 7

Burberry 3 5 2 Imperial Brands 53 26 -27

Unilever 4 10 6 Sage Group 54 88 34

BT Group 5 2 -3 Legal & General 55 32 -23

RELX 6 9 3 Prudential plc 56 60 4

Natwest Group 7 8 1 Spirax-Sarco Engineering 57 57 0

United Utilities 8 31 23 B&M 58 98 40

Berkeley Group Holdings 9 19 10 Segro 59 71 12

London Stock Exchange Group 10 38 28 Ferguson plc 60 77 17

Lloyds Banking Group 11 35 24 Smiths Group 61 67 6

Severn Trent 12 29 17 Experian 62 74 12

Barclays 13 44 31 Bunzl 63 79 16

RSA Insurance Group 14 43 29 Smurfit Kappa 64 42 -22

Coca-Cola HBC 15 25 10 Rio Tinto Group 65 53 -12

Taylor Wimpey 16 45 29 Standard Chartered 66 22 -44

Barratt Developments 17 20 3 Intermediate Capital Holdings 67 82 15

Phoenix Group 18 49 31 Melrose Industries 68 97 29

Mondi 19 18 -1 Aviva 69 33 -36

Diageo 20 16 -4 Croda International 70 37 -33

3i 21 88 67 Weir Group 71 77 6

Next plc 22 47 25 Intertek 72 63 -9

Informa 23 24 1 National Grid plc 73 17 -56

Renishaw 24 79 55 Entain 74 82 8

Kingfisher 25 21 -4 DS Smith 75 56 -19

Vodafone Group 26 11 -15 Polymetal International PLC 76 52 -24

Tesco 27 7 -20 Anglo American plc 77 51 -26

GlaxoSmithKline 28 4 -24 InterContinental Hotels Group 78 30 -48

Associated British Foods 29 87 58 Ocado 79 82 3

Persimmon plc 30 71 41 Royal Dutch Shell 80 41 -39

Schroders 31 28 -3 Halma 81 71 -10

Pearson plc 32 12 -20 SSE plc 82 13 -69

HSBC 33 15 -18 Auto Trader Group 83 88 5

Hargreaves Lansdown 34 88 54 Fresnillo plc 84 64 -20

Smith & Nephew 35 67 32 Aveva 85 85 0

BAE Systems 36 79 43 Rentokil Initial 86 70 -16

Reckitt 37 23 -14 Compass Group 87 39 -48

British American Tobacco 38 40 2 Hikma Pharmaceuticals 88 64 -24

AstraZeneca 39 3 -36 Rolls-Royce Holdings 89 62 -27

Standard Life Aberdeen 40 36 -4 Flutter Entertainment 90 88 -2

WPP plc 41 14 -27 BHP 91 58 -33

M&G 42 60 18 Avast 92 88 -4

Admiral Group 43 88 45 DCC plc 93 88 -5

Whitbread 44 74 30 Glencore 94 66 -28

JD Sports 45 46 1 Ashtead Group 95 88 -7

Johnson Matthey 46 67 21 Evraz 96 55 -41

Sainsbury’s 47 27 -20 Homeserve 97 85 -12

International Airlines Group 48 34 -14 BP 98 54 -44

Rightmove 49 48 -1 Just Eat Takeaway.com 99 98 -1

CRH plc 50 50 0 Scottish Mortgage Investment Trust 100 98 -2

In partnership with

5 of 19The Findings

Who’s leading in the Climate100 Index?

Our Index leader, Land Securities, is one of only 14 FTSE 100 companies to receive an “A” rating

from the CDP as its Climate Score; this suggests that its performance and reporting against the

CDP’s comprehensive measures are both solid. Three other companies in the Top 5 – Burberry,

Unilever and BT Group – also receive an “A” rating from the CDP.

Land Securities and Burberry also achieved their targets to limit the amount of waste sent to

landfill, with their recycling rates standing at 73 and 75 per cent respectively.

BT Group makes use of renewable energy for 89.9 per cent of its total consumption, well above

the FTSE 100 average of 38 per cent for those companies that also report. Burberry and British

Land – also in the Top Five of the Climate100 Index – exceed the average at 83 and 77 per cent

respectively.

All five companies decreased their total year-on-year energy consumption, with Burberry making

the largest percentage reduction at nearly 10 per cent.

Our Index leaders practice what they preach; four of the Top Five companies also rank well in

our “Talk” pillar. In other words, they set plenty of clear, measurable climate-related targets and

they outperform their peers when it comes to our “Walk” indicators.

Who’s lagging behind?

Scottish Mortgage Investment Trust ranks bottom of the Climate100. The investment group has

no offices or employees and therefore does not report its emissions or other key climate data,

including mandatory Scope 1 and 2 reporting

Second-to-last is food delivery company Just Eat Takeaway.com. Alongside Scottish Mortgage

Investment Trust, they are one of just two companies not to report their Scope 1 and 2 emissions

data, as well as most other environmental reporting.

A lack of transparency overwhelmingly contributed to poor performance in our Index. For

example, of the bottom five companies, only BP reports its Scope 3 emissions – i.e. greenhouse

gas emissions that occur along the company’s value chain.

Other “bottom five”companies include oil and gas giant BP and home improvements business

Homeserve. Both received an “F” rating from the CDP. This suggests that the companies have

weak reporting on climate-related metrics – from emissions to waste.

Extraction giants Evraz and BP reported some of the highest overall emissions across our Index

– at 8th and 3rd respectively.

Measuring emissions

Most companies listed in the UK are required by law to disclose their emissions data, making it

possible to monitor their progress on targets relating to both their direct and indirect emissions.

These disclosures provide a useful picture of the emissions footprint of the FTSE 100 and allow

the Climate100 Index to show the biggest laggards.

In partnership with

6 of 19There are three ways for companies to measure and report on their greenhouse gas emissions, or

CO2 equivalent (CO2e):

– Scope 1 emissions are “direct” emissions produced by the company. These must physically

occur at sites owned or rented by the company, for example emissions from company vehicles

or combustion in the company’s boilers.

– Scope 2 emissions are “indirect” emissions produced by the company. These occur from

electricity consumed by the company.

– Scope 3 emissions are additional “indirect” emissions that occur along the company’s value

chain. Scope 3 therefore includes any emissions resulting from:

• goods and services delivered by outside providers

• product distribution

• product waste disposal

• investments

• employee travel and commuting – for many companies, this is one of the biggest sources of

Scope 3 emissions.

It is important to note that there are significant holes in the way that emissions data is reported.

It is not a legal requirement to publish Scope 3 emissions – those that arise indirectly from a

company’s value chain.

This year, 32 companies chose not to calculate or disclose a Scope 3 emissions figure.

Another area where we’re yet to see consistent reporting is on Scope 2 emissions, where we find

that like-for-like comparisons aren’t possible due to differences in the methodologies used. Some

companies choose to publish data on Scope 2 emissions for the region-wide grids on which their

company facilities are located – known as “location-based” methodology. Others published this

same data according to a “market-based” methodology, which takes into account the energy

decisions they make, such as whether they buy renewable electricity.

The UK’s Environmental Reporting guidelines suggest it is best practice to report using both

methodologies, yet we found that in practice just 49 companies provided both. Furthermore, we

found that in many cases it was unclear which of the two methodologies was used to arrive at the

figure provided. This marks a significant lack of transparency given that the difference between

the two methodologies is often substantial. In total, we counted 36 companies that did not

specify either way.

Faced with this inconsistency, we chose to use the market-based figure where available in order

to encourage companies to pursue energy contracts with low-carbon providers. When the

market-based figure was not available, we used the location-based figure.

Beyond the issue of methodological inconsistencies, there remain two companies in the FTSE

100 that do not disclose their emissions at all. They are:

– Just Eat Takeaway.com, the online food delivery service

– The Scottish Mortgage and Investment Trust, which focuses on investment

The context of Covid-19

Over the course of the past year, many of the FTSE 100 companies saw their offices close, with

remote working taking centre stage. Many, such as those in the travel industry, also had a

significant slump in demand.

Estimates from the Global Carbon Project suggest that global emissions fell by 7 per cent – or

2.4 billion tonnes of CO2e – in 2020, the largest absolute fall ever. The UK’s national greenhouse

gas output fell almost nine per cent when national and then regional lockdowns shut down or

transformed large sectors of the economy. These movements are reflected in data from the

Climate100.

In partnership with

7 of 19Top Emitters – all direct and indirect emissions

Despite having the largest absolute year-on-year reduction in emissions, Royal Dutch Shell

continues to produce the most absolute Scope 1 and 2 emissions – at 72 million tonnes CO2e

– and the most Scope 3 emissions, at 1.3 billion tonnes CO2e.

Top 9 overall emitters

Absolute Scope 1, 2 and 3 emissions (tonnes CO2e), where known

1 2 3 4 5

Royal Dutch Shell Rio Tinto Group BP Plc Glencore Anglo American

1,377,000,000 550,900,000 373,100,000 295,300,000 242,100,000

6 7 8 9

Unilever CRH plc Evraz National Grid plc

61,167,269 45,900,000 43,570,000* 36,300,000

Scope 1 & 2 Emissions (tonnes of CO2e)

Scope 3 Emissions (tonnes of CO2e)

*Evraz do not publish Scope 3 emissions figures.

Our analysis also shows that, while reporting on Scope 3 emissions is not required by law, this

reporting is crucial to gaining an understanding of a company’s environmental impact. Shell’s

Scope 3 figures represent 90 per cent of its emissions. This figure is particularly striking when

you consider that Shell is also the biggest emitter of Scope 1 and 2 CO2e across all the FTSEs.

Overall, the top emitters are overwhelmingly in the extraction – that is, energy and mining –

industries. They emitted 253 million tonnes of Scope 1 & 2 CO2e in the last reporting year. Not

all of them reported their Scope 3 emissions, but those that did reported emissions of 2.6 billion

tonnes CO2e. That represents 95 per cent of all reported CO2 emissions.

Extraction companies emitted 253 million tonnes of Scope 1 & 2 CO2e between them

The Scope 3 figures we know about are even higher, at 2.6 billion

Scope 1 & 2 Emissions Scope 3 Emissions

Royal Dutch Shell

Rio Tinto Group

BP

Glencore

Anglo American plc

Evraz

BHP

Antofagasta

Polymetal

Fresnillo plc

0 200 400 600 800 1,000 1,200 1,400

Emissions (million tonnes CO2e)

Antofagasta, BHP, Evraz and Fresnillo do not report their Scope 3 emissions In partnership with

8 of 19Evraz stands out at the 8th largest overall emitter in our data set, despite not reporting its Scope

3 emissions. The company is responsible for 43.4 million tonnes of Scope 1 and 2 CO2e

emissions each year. The total figure, including Scope 3, could be even higher. According to

Evraz, its increase in emissions is largely down to the company removing more methane, a

colourless, odourless and dangerously flammable greenhouse gas, from mines.

Top 10 emitters

Scope 1 and 2 greenhouse gas emissions (tonnes CO2e)

Royal Dutch Shell BP International Airlines Group Evraz

80,000,000 54,400,000 52,480,000 43,350,000

CRH plc Rio Tinto Group Glencore Anglo American plc

36,500,000 31,500,000 29,300,000 17,700,000

BHP SSE plc Everyone else

15,800,000 9,530,000 41,259,320.48

The picture does not change dramatically even when measuring emissions relative to the number

of employees at the company. When looking at the data in this way, International Airlines Group

has the highest figure– even after a 60 per cent year-on-year decrease in emissions. However,

extraction companies overwise remain the most damaging.

Top 10 emitters per employee

Average Scope 1 and 2 greenhouse gas emissions (tonnes CO2e) per employee

International Airlines Group Royal Dutch Shell BP SSE plc

1,516 920 855 816

Rio Tinto Group Evraz BHP CRH plc

664 623 500 473

Antofagasta Glencore Everyone else

433 334 1,870

In partnership with

9 of 19Who’s decreased emissions?

During the last reporting year, Scope 1 and 2 emissions across the FTSE fell by 61.5 million

tonnes of CO2e, representing an average drop of 14 per cent per company year-on-year. The

drop was not consistent across the board, however. The travel company International Airlines

Group -– which owns airlines British Airways and Iberia – saw a 60 per cent drop in Scope 1 and

2 emissions, representing 31.5 million tonnes of CO2e.

International Airlines Group saw the steepest decline in emissions

Absolute emissions (tonnes CO2e)

Previous reporting year Most recent reporting year

International Airlines Group 52,480,000

21,020,000

Other companies that saw a big drop in Scope 1 and 2 emissions were fashion company Burberry

at 64 per cent (9,400 tonnes CO2e) and publishing company Informa, at 61 per cent (6,800

tonnes CO2e).

Companies with the largest relative reduction in emissions

0

YOY change in emissions (%)

-10

-20

-30

-40

-50

-60

LX

c

n

e

s

p

s

ro s

a

y

em

er

G line

rr

pl

ov

rm

e

u

up

de

RE

ro

be

od

tm

n

fo

st

ir

tG

o

er

r

hr

In

Sy

lA

rs

gh

Bu

Ab

es

Sc

a

na

Ri

E

Pe

tw

BA

fe

io

Na

Li

at

rd

rn

da

te

In

an

St

In partnership with

10 of 19It is likely that sharp decreases in emissions are a temporary result of pandemic lockdowns and

Covid-19 measures, and that we will see a steady increase in these figures as the situation eases.

A green recovery is crucial to keep emissions low and avoid numbers rising above pre-pandemic

levels.

Who’s increased emissions?

Despite the pandemic, 14 companies saw their direct and indirect Scope 1 and 2 emissions

increase by 579,879 tonnes CO2e in the most recently reported year. Evraz saw the biggest

increase in emissions, at 220,000 tonnes CO2e, which represents just 0.5 per cent of its total

emissions in the previous reporting year.

FTSE 100 companies that increased their emissions in the most recently reported year

Evraz

Smurfit Kappa

D.S. Smith

Fresnillo plc

JD Sports

Ashtead Group

Smiths Group

B&M European Value Retail

Aveva

Segro

Ocado

Whitbread

Phoenix Group

3i

0 50,000 100,000 150,000 200,000

Increase in carbon emissions, tonnes

This is despite the fact that, out of the 14, seven have set public targets to reduce emissions.

Three – Segro, Ocado and Smurfit Kappa – are aiming for net zero emissions by 2030, 2040 and

2050 respectively.

Smurfit Kappa, a packaging company, said its 180,000 tonne increase in CO2e was because it

bought an additional paper mill in the Netherlands. Similarly, D.S. Smith (also in the packaging

business) emitted 60,000 more tonnes of CO2e in 2020 than in 2019 because it bought a paper

mill and a packaging plant. The emissions of Smiths Group, an engineering firm, rose because it

bought a new company called United Flexible.

In partnership with

11 of 19According to publicly available data, JD Sports’ carbon emissions increased 73 per cent between

2019 and 2020 – more than any other FTSE 100 company. But when contacted, the clothing

retailer provided information, to be made publicly available in its next annual report, which

showed it had overestimated this figure, which is actually 16 per cent. The increase, it said, was

because it had opened new shops in the United States.

Property developers Segro said their larger emissions bill was “associated with [their]

development pipeline”, i.e works-in-progress, as well as higher energy costs from its buildings

standing empty. They also noted that most of their emissions come under the Scope 3 heading.

Ocado, which develops software, robotics, and automation systems for online shops, said its

increase was due to the “huge surge in demand [they] saw for deliveries during the period”. Their

emissions per order declined.

Whitbread increased its emissions because it added more hotels and restaurants to its collection.

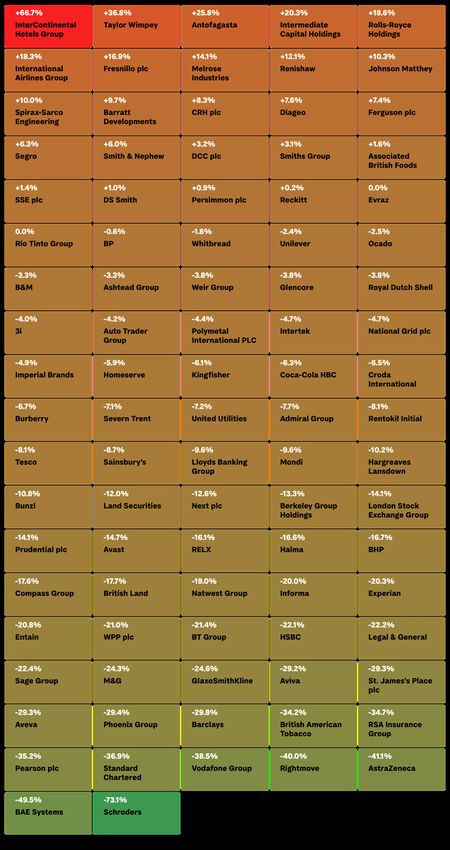

Emissions intensity

Emissions intensity is a measure of the amount of emissions for which a company is responsible,

expressed not as a total, but proportional to another factor that is part of the business. Some

companies will express their emissions intensity against the value of their marketed products i.e.

how many million tonnes of CO2e they generate per £ in revenue, or as a value proportional to

the number of employees at the company.

There is no consistent standard, and the values vary across sectors. Many companies that are

involved in land use, or development, will express their emissions intensity as a figure per square

foot of space. Some extractive businesses will select a metric that shows emissions per tonne of

mineral or ore extracted.

The lack of consistency across the reporting standards means that the comparable metrics

between companies are not the intensity figures themselves, but rather the percentage change in

those figures over time. The Climate100 Index tracks the percentage change in emissions

intensity for each company year on year, showing their performance when it comes to reducing

their impact on the environment proportional to the scale of their operations.

It is important to note that emissions intensity can fall, but overall emissions from a given

company may be rising. This is because the level of emissions per unit of production, for

example, may fall, but the total number of units produced may increase more than

proportionately, meaning that the gross level of emissions could in fact rise.

In partnership with

12 of 19Emissions Intensity Heatmap

Showing the percentage change in emissions intensity for each company where data is available

In partnership with

13 of 19Energy

The FTSE 100 used a total of 2.8 billion MWh of energy in the last reporting year, approximately

a 40 per cent reduction from the previous year (4.5 billion). Energy use, and the various sources

of energy exploited by the companies is an important factor in their contribution to climate

change. The Climate100 Index measures the total energy consumption of each company, as well

as the percentage of that energy and the resultant electricity consumption which comes from

renewable sources. The total is a measurement of the UK, Global and offshore energy use, and

therefore reflects the total energy footprint of the companies.

Companies with the largest reduction in energy usage

Total reduction in energy consumption (TWh)

0

-20

-40

-60

-80

ro s

BP

l

e

z

eo

c

s

ro ls

up

el

em

G line

ra

or

pl

G ote

Sh

up

ag

up

ro

Ev

nc

an

st

ir

G

H

Di

ch

le

Sy

lA

ic

o

l

ta

G

er

ut

nt

na

E

en

lD

Am

Ti

BA

io

in

o

ya

at

Ri

nt

o

rn

Ro

gl

Co

An

te

r

In

te

In

International Airlines Group has recorded the most significant reduction in energy use of any

company in the FTSE 100, likely because of restrictions to air travel. BP, Royal Dutch Shell and

Glencore also saw sharp drops in energy use. Despite a substantial contraction in the size of the

global economy, the average drop in energy consumption across the FTSE 100 was just 5.2 per

cent throughout the year.

Several companies including athleisure retailer JD Sports, investment company Segro, utilities

supplier National Grid and Sainsbury’s, the supermarket, bucked this trend and increased the

amount of energy they were consuming.

Top and Botton 5 FTSE 100 in terms of percentage change in energy consumption

60

40

20

0

-20

-40

-60

c

s

up s

c

ts

y’s

&G

a

o

o

em

ro e

pl

pl

ev

gr

ge

or

G rlin

r

M

rid

n

Se

bu

Av

Sp

st

a

o

Di

i

Sy

lA

rs

lG

s

JD

in

a

na

E

na

Sa

Pe

BA

io

tio

at

Na

rn

te

In

In partnership with

14 of 19Water

Water consumption and reuse is a critical factor in the process of addressing climate change.

Water extraction can harm ecosystems and reduce the overall resilience of the environment to

warming and other exogenous factors. Water stewardship is, therefore, a vital part of the

responsibility that companies have to protect the environment. 5.9 billion cubic metres of water

were extracted, consumed or otherwise used by FTSE 100 companies in the last reporting year;

nearly double the figure consumed by UK households (3.3 billion).

Waste

The Climate100 Index also reflects the total amount of waste produced by the FTSE 100, and

the way in which this waste is treated. The decomposition of waste is not only a source of

emissions, but also contributes to ecosystem destruction and pollution. The responsible disposal

of waste is another important part of the action that businesses can take to address climate

change. The FTSE 100 produced 771 million tonnes of waste in the most recent reporting year.

The CDP

The CDP 2020 have implemented changes in their methodology, and set more ambitious targets,

causing most ratings to drop. In 2020, CDP updated its scoring methodology “to reflect the

ever-changing nature of environmental management and CDP’s emphasis on continual

improvement”.

The 2020 questionnaire introduced new questions, and changes in scoring of existing ones, that

may have caused a companies’ score to drop if it gave exactly the same responses as in 2019. The

updated version of the CDP framework requires companies to consider climate-related risks and

opportunities in greater detail: where and how they influence business strategy, how they’re

addressed in short, medium and long-term financial planning. Other responses were downgraded

from leadership to management level to incentivise improvement.

The path to net zero

When it comes to the climate, targets are important – but only if they are followed up with

action. This is why the Climate 100 Index tracks both the “Walk” and “Talk” of each FTSE 100

company.

The Climate100 Index collects data on all verbal commitments made by FTSE 100 companies

relevant to decreasing their environmental footprint, so long as those commitments are specific,

time-bound and measurable. In other words, a company promising to “decrease our carbon

footprint” isn’t enough, but a target like “achieving net zero emissions by 2030” would be

recognised.

The global business community is not moving fast enough to divest, decarbonise and limit its

impact on the environment. Only a handful of jurisdictions around the world have laws that

require businesses to reach emissions targets, and many others are more tolerant of pollution

than is compatible with the Paris Agreement.

The Carbon Trust states that to reach a state of net zero emissions for companies would require

two main conditions:

To achieve a scale of value-chain emission reductions consistent with the depth of abatement

achieved in pathways that limit warming to 1.5 degrees celsius or with no limited overshoot

To neutralise the impact of any source of residual emissions which remains unfeasible to be

eliminate by permanently removing an equivalent amount of atmospheric carbon dioxide

In partnership with

15 of 19In order to meet the 1.5°C global warming target in the Paris Agreement, global carbon

emissions must reach net zero by the middle of the century. As the FTSE 100 represents a large

proportion of global carbon emissions, it is important to hold them accountable to ensure

meaningful change within the UK by the mid-century deadline.

In line with this global goal, 64 of the FTSE 100 have set targets to reach net zero between now

and 2050, a handful more have outlined their intention to set targets in the future.

64 companies have set net zero targets with deadlines between 2020 and 2060

36 companies have not set any net zero targets

St. James's Place plc

Whitbread

The Weir Group

Tesco

Standard Life Aberdeen

Standard Chartered

SSE plc

Smurfit Kappa

Schroders

Royal Dutch Shell

Rolls-Royce Holdings

Rio Tinto Group

Rightmove

Renishaw

Ocado

National Grid plc

London Stock Exchange Group

Legal & General

Kingfisher plc

Intertek

International Airlines Group

Homeserve

Glencore

DCC plc

Croda International

CRH plc

British American Tobacco

BP

BHP

Barclays

Antofagasta

Admiral Group

BT Group

Vodafone Group

Spirax-Sarco Engineering

Rentokil Initial

Reckitt Benckiser

Burberry

Barratt Developments

Aviva

Anglo American plc

Unilever

Flutter Entertainment

3i

United Utilities

Segro

Prudential plc

Pearson plc

M&G plc

Lloyds Banking Group

Land Securities

Informa

HSBC

GlaxoSmithKline

Evraz

Diageo

British Land

Berkeley Group Holdings

BAE Systems

WPP plc

Phoenix Group

Natwest Group

AstraZeneca

RELX

2020 2030 2040 2050 2060

Net Zero target date

In partnership with

16 of 1929 companies have also set out targets to specifically reduce their Scope 1 and 2 emissions, with

deadlines ranging from 2022 and 2050. Assuming the same year-on-year decline in emissions, in

absolute terms, that we counted in the most recent data, Tortoise analysis suggests that at least

five of the FTSEs will miss their targets. The companies’ planned trajectories may be different,

and the real trajectories might change, for better or for worse. It’s important to remember that

the pandemic has given companies a head-start to reduce their emissions; for many, the real

challenge will come when worldwide Covid-19 restrictions ease and production ramps up once

more.

Currently, there is no authority to hold companies accountable for missing them. No CEO will

lose their job – many won’t even lose their bonus. Tortoise analysis in 2020 showed that 63

companies published details on how they allocate bonuses, but only five included environmental

performance as an incentive. The Science Based Targets Initiative, seen as a standard-keeper on

emissions targets linked to climate science, quietly removes a company from its website if it fails

to keep its word.

Inside the Index

Below we have outlined the “Walk” indicators that this Index uses to capture the climate

performance of the FTSE 100. The indicators that comprise the Climate100 have been selected

with the aims of:

– Reflecting publicly-available information rather than proprietary sources

– Speaking to the 2030 Sustainable Development Agenda and the various targets that it sets

– Providing a comprehensive portrait of each company according to the available data in order to

establish comparability

Each indicator is weighted according to its relevance and reliability. We use a system consisting

of four weights, each with an equal impact on the overall weighting of the indicator. The data is

assessed first for engagement, second for impact, then for relevance and lastly according to its

reliability and comprehensiveness.

The results in the Climate pillar are heavily weighted towards reducing total greenhouse gas

emissions because reaching net zero emissions is of critical importance to the planet.

Walk indicators

Total Scope 1 & Scope 2 Greenhouse Gas Emissions (Tonnes CO2e)

Reduction in emissions intensity (% change)

Total Area Conserved or Protected (Square Metres)

Total Water Consumption (Cubic Metres)

Proportion of Total Energy Usage from Renewable Sources (%)

Proportion of Total Electricity Usage from Renewable Sources (%)

Total Energy Consumption (MWh)

Percentage (%) Reduction in Total Energy Use

Proportion of Total Waste to Landfill (%)

Proportion of Total Waste Recycled or Re-used (%)

Proportion of Total Materials Used sourced from Sustainable Sources (%)

CDP Climate Rating

CDP Timber & Forestry Rating

CDP Water Security Rating

Proportion of Total Revenue donated as Disaster Relief (%)

Proportion of Total Water Consumption Recycled (%)

Total Waste Produced (Tonnes)

Total Scope 3 Greenhouse Gas Emissions (Tonnes CO2e)

Total Value of Donations to Disaster Relief (£)

Total Volume of Water Recycled (Cubic Metres)

Total Energy Consumption (MWh) in Previous Year

Existence of Dual Reporting

Presence of Scope 3 Greenhouse Gas Emissions Reporting

In partnership with

17 of 19Guiding Principles

Below we have detailed the key methodological principles and steps that underpin the

Climate100 Index.

– Publicly available: All the data we include in the Index must be publicly available, either from

published company reports or open third-party sources, such as Companies House.

– Recent: As different companies will publish their annual and sustainability reports at different

times of the year, the data underlying The Climate100 Index is drawn from a range of years

rather than only the year of this edition. In order to ensure that the Climate100 Index can be

reasonably considered to be “up to date”, we apply a limit of only including data sets that are

less than, or equal to, three years old. In this report, that means from 2017 or later.

– Relevant: The Climate100 aims to be agnostic about a company’s sector and we have chosen

metrics with this in mind: in most cases our indicators are relevant to the majority of the

companies.

– Relative: We often collect data in a raw or absolute form: for example, the “Proportion of Total

Waste Recycled or Re-used”. In order to fairly compare companies of different sizes – in terms

of their total revenue or employees – we will calculate a relevant relative measure: for example

“Total Scope 1 & 2 Emissions per Employee”.

The Climate100 Index rewards not only positive action such as reduction in emissions, but also

comprehensive reporting. Without measurement of key factors across a company’s activities it is

difficult to understand where the problems actually lie. As such, the Climate100 takes the

absence of data, on a factor such as “Percentage of Total Electricity Consumption from

Renewable Sources”, to mean that the company has not measured and therefore doesn’t know

the underlying factors.

Companies that do include data on each indicator, whatever their actual performance may be,

should be recognised for promoting transparency and accountability. Only then can the process

of encouraging better performance begin.

Talk vs Walk

Company reports often declare a commitment to sustainability goals alongside profit – but these

pledges are rarely followed up fully or, in some cases, at all. The Climate100 answers this

problem by directly comparing a company’s commitments – in the form of their “Talk” score –

with their actions – their “Walk” score.

Our Walk indicators reflect the reality of the action that companies are undertaking, and

measure their actual performance. Each Walk indicator can be quantified and incorporated into

the overall scoring either as a gross, or relative metric. In the cases where a value is missing for a

particular company, where the data provided is ambiguous, or where a company has not clarified

to us what their submission means, the value is recorded as missing. In many cases this means

that the company is awarded the “worst-case scenario” value for that indicator i.e. 0 for

“Percentage of Total Electricity Consumption from Renewable Sources”. Overall, this means that

it is no longer good enough for a company to mention that they are aiming to reduce their

carbon footprint; they must also disclose by how much and by when.

Our Talk indicators measure the rhetoric around the reality of action. In a world where green-

washing is common, we believe that actions speak louder than words. And yet, it is important to

monitor the commitments, pledges and aims that these companies make, so that we can hold

them accountable. Our Talk indicators look at whether companies are signing up to group

pledges and engaging with membership organisations such as the RE100. We also look at the

targets that companies are setting themselves and monitor their progress in committing to

science-based targets. In essence, by measuring “Talk” separately to “Walk”, we seek to reveal

not only the biggest “Talkers” and “Walkers” in the FTSE 100, but also those with the largest

gap between the two.

In partnership with

18 of 19If you have any questions about the Climate100 Index or the content of this

report, please contact a member of our team.

Alexandra Mousavizadeh, alexandra@tortoisemedia.com

Kim Darrah, kim.darrah@tortoisemedia.com

Patricia Clarke, patricia.clarke@tortoisemedia.com

Ellen Halliday, ellen.halliday@tortoisemedia.com

Serdar Korur, serdar@tortoisemedia.com

Luke Gbedemah, luke.gbedemah@tortoisemedia.com

In partnership with

19 of 19You can also read