STUDY ON POTENTIAL ROLE AND BENEFITS OF LIQUIFIED NATURAL GAS IMPORT TERMINAL IN LATVIA

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

LATVIAN JOURNAL OF PHYSICS

AND TECHNICAL SCIENCES

2022, N 2

DOI: 10.2478/lpts-2022-0010

STUDY ON POTENTIAL ROLE AND BENEFITS OF

LIQUIFIED NATURAL GAS IMPORT TERMINAL IN

LATVIA

A. Ansone*, L. Jansons, I. Bode, E. Dzelzitis, L. Zemite, A. Broks

Riga Technical University,

Faculty of Civil Engineering, Institute of Heat,

Gas and Water Technology,

6B/6A Kipsalas Str., Riga, LV-1048, LATVIA

*e-mail: ansoneance@gmail.com

Natural gas is relatively clean energy source, which emits less greenhouse gases (here-

inafter – GHG), compared to other fossil fuels, such as hard and brown coal, and therefore

it may be the most feasible resource to ensure smooth energy transition towards Europe’s

climate neutrality by 2050. Traditional natural gas can be easily transported and used in lique-

fied (hereinafter – LNG) or compressed form. As for biomethane, in future it also can be used

in liquefied (hereinafter – bioLNG) and compressed form, as well as transported by means of

the current natural gas infrastructure. It can also significantly enhance regional and national

energy security and independence, which has been challenging for the European Union (here-

inafter – EU) over at least several decades.

Issue on energy independence, security of supply, alternative natural gas sources has been

in a hotspot of the Baltic energy policy makers as well. Now, considering Russia’s invasion in

Ukraine, since late February 2022, a problem of the EU natural gas dependency on the Russian

Federation has escalated again and with force never before experienced. The European natural

gas prices also hit records, as the natural gas prices in the Netherlands Title Transfer Facility

reached 345 euros per megawatt-hour (hereinafter – EUR/MWh) in March 2022.

Therefore, LNG import terminal is the only viable option to reduce national dependency

of the so-called pipe gas which in some cases, due to the insufficient interconnections, may

be delivered from very limited number of sources. The European policy makers and relevant

institutions are currently working towards radical EU natural gas supply diversification, where

LNG deliveries coming from outside of Russia will certainly take a central stage.

37

In case of Latvia, the potential benefits of the LNG terminal development in Skulte were

evaluated in order to reduce energy independence of the Russian natural gas deliveries in the

Baltic region and to introduce new ways and sources of the natural gas flows to the Baltics.

LNG terminal in Skulte could ensure significant capital investment cost reduction comparing

to other projects proposed for Latvia in different periods, due to already existing natural gas

transmission infrastructure and the relative closeness to the Incukalns underground gas stor-

age (hereinafter – UGS). Various aspects, such as technical, political and economic ones, were

analysed to assure that Skulte LNG terminal would be a real asset not only to customers of

Latvia, but also to those of the whole Baltic region, where in future it would be possible to

use biomethane for efficient utilisation of existing and developing natural gas infrastructure.

Keywords: Biomethane, energy independence, energy policy, energy security, gas storage,

gas transmission, LNG, security of supply, SoS.

1. INTRODUCTION

The European Green Deal is a set of the fossil gas related activities, should switch to

EU policy initiatives, which was approved renewable gases (hereinafter – RG) by the

in 2020, with the main goal to reach end of 2035 [2]. In the future, where fos-

Europe’s carbon-neutrality by 2050. This sil natural gas might be fully substituted by

requires major changes in energy sector the RG biomethane, potential biomethane

as well, especially considering Fir-for-55 supply could be arranged not only by using

legislation package, which was published current natural gas transmission and distri-

in July 2021, setting policy measures to bution systems, but also by sea in a form of

reduce EU’s GHG emissions by 55 % com- bioLNG [3].

paring to year 1990 [1]. Any LNG can be used in several crucial

Natural gas is also considered to be sus- sectors of the national economy in order

tainable under the EU’s Taxonomy Regula- to provide reliable and clean energy: for

tion delegated act, published in February example, it can help imeet energy needs of

2022, which classifies economic activities freight and maritime transport sectors and

that are sustainable, to help investors and provide environmentally sound and afford-

any other party better shift investments able fuel for electric energy and heat gen-

towards sustainable development. Accord- eration [4]. Especially, in regions where

ing to the European Commission (herein- renewable energy sources are less available

after – EC), the natural gas facilities have or cannot meet high energy demand in win-

to comply with strict rules and, in case of ter season [5]–[7].

2. THE NATURAL GAS SUPPLY RISKS IN THE BALTIC REGION

2.1. Import and Supply Sources

More than a decade ago, the Baltic mise on LNG terminal construction loca-

States asked the EC to help find compro- tion in the Baltic region, but the initiative

38failed to find a common ground on develop- meters (hereinafter – BCM; around 36.64

ment and cost sharing [8]. The only one of terawatt-hours (hereinafter –TWh)) per

the Baltic States, which actually developed year. Unfortunately, 90 % of the Europe’s

its own national LNG import terminal proj- natural gas is imported [9]. Share of each

ect, was Lithuania, and the Klaipeda LNG exporting country in the EU’s natural gas

terminal was commissioned in 2014. Its import is shown in Fig. 1.

import capacity reaches 3.75 billion cubic

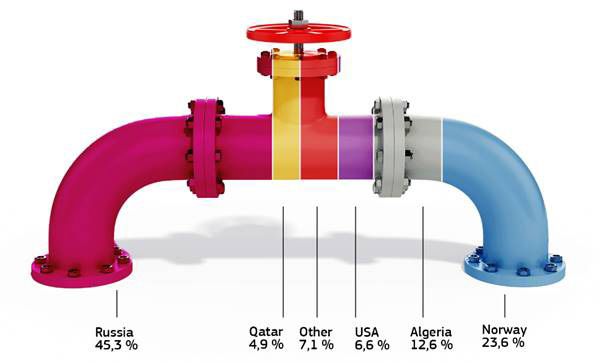

Fig. 1. The EU natural gas imports [10].

In 2021, around 140 BCM (around the LNG import from the USA and Qatar,

1367.72 TWh*) of natural gas were while in a longer run, it is working towards

imported to the EU by pipelines, while 15 additional alternatives, including locally

BCM (146.54 TWh*) were delivered as produced RGs, such as biomethane or

LNG [11]. The Baltic States and Finland hydrogen. In March 2022, the International

still relied mostly on the natural gas sup- Energy Agency also revealed a plan to

plies from Russia, while Lithuanian natural reduce the EU’s dependency on the Russian

gas supplies were more diverse due to the natural gas supplies, where one of the key

ever-growing natural gas imports though suggestions was to replace Russian pipe-

Klaipeda LNG terminal [12]. line natural gas supplies with non-Russian

Once again, a question on the natural LNG ones. In comparison to 2021, it would

gas supply and Europe’s dependency on be possible to increase LNG import to the

Russian gas has escalated, considering Rus- EU by 50–60 BCM per year, but since sup-

sia’s invasion in Ukraine, which started in pliers were more or less the same, it might

February 2022. The European natural gas result in higher LNG prices worldwide [11].

prices also hit records, as the natural gas On 8 March 2022, the EC introduced com-

prices in the Netherlands Title Transfer munication on a new plan “REPowerEU:

Facility reached 345 EUR/MWh in March Joint European Action for more affordable,

2022 [13]. secure and sustainable energy” to become

In a short-term period, the EC plans independent of Russia’s fossil fuel, which

to minimise Russian natural gas depen- includes LNG import diversification, using

dency by means of increasing the share of a wider range of potential suppliers, includ-

39ing but not limited to Qatar, the USA, Egypt ties of its type in Europe with a capacity of

and West Africa [10]. 2.3 BCM. It can ensure safe storage of the

While diversifying the EU’s natural gas large amounts of natural gas that has been

supplies in a form of LNG, the role of UGSs imported to Latvia and the whole Baltic

is tend to grow in foreseeable future. The region. Therefore, LNG terminal in Latvia

Baltic region has only one such a storage – could not only increase security of supply

Incukalns UGS located in Latvia, which is in our country, but also in the remaining

also one of the most modern UGS facili- Baltic countries and Finland.

2.2. Main Aspects of Analysis of the Baltic Natural Gas Supply Risks

At the end of 2021 and beginning of tions from Russia in March coupled with

2022, the EU natural gas market was under insufficient natural gas reserve in Incukalns

tension, where atypically high natural gas UGS. Among others, it was concluded on

demand was observed. However, at that the national level that the limiting factor of

time it was translated as global economic the natural gas transmission system is the

recovery from the pandemic. While Russia’s cross-border interconnection capacity. The

war against Ukraine escalated, in March amount of active gas stored at the Incukalns

2022 the natural gas flows from Russia via UGS is the most important factor in guaran-

Yamal pipeline (via Belarus and Poland) to teeing both the Latvian and regional secu-

Germany declined sharply. Possible reason rity of the natural gas supply. Lithuania’s

is that keeping Russia’s supplies low would support to Latvia in some crisis scenarios

highlight a need for additional routes, such is limited by the potential volatility of the

as commissioning of currently banned the LNG cargos due to LNG logistics [18].

Nord Stream 2 pipeline project [14]–[16]. An important role in the Baltic natural

There was a hope that the natural gas gas supply is dedicated to the Polish–Lithu-

supply risk plans that were developed under anian natural gas interconnector (hereinaf-

Regulation (EU) 2017/1938 of the Euro- ter – GIPL), which will be commissioned

pean Parliament and of the Council of 25 in mid-2022, ending isolation of the Baltic

October 2017 concerning measures to safe- States from central European natural gas

guard the security of gas supply and repeal- transmission systems, but unfortunately

ing Regulation (EU) No. 994/2010 (here- no plan predicted limited natural gas sup-

inafter – Regulation 2017/1938) would not plies from Russia to the whole Europe

be used in real life, while ongoing war in at the same time, as it is happening now.

Ukraine and the EU sanctions proved that With high geopolitical tensions in relations

scenarios from the preventive action plan with Russia for at least midterm perspec-

and emergency plan could actually came tive, the only viable option for the natural

true in foreseeable future [17]. gas supplies to the Baltic States and Fin-

In a preventive action plan, one of the land is Klaipeda LNG terminal and GIPL.

scenarios simulates a situation where, due In accordance with early warning in the

to the geopolitical crisis, the flow of natu- natural gas supply sector of Latvia that was

ral gas from Russia stops completely within announced on 9 March 2022, the natural

two weeks of peak demand and eight aver- gas deliveries from Klaipeda LNG and via

age winter weeks. The most significant GIPL are regarded as prioritising gas flows

risks identified in the preventive action plan by the Latvian natural gas transmission sys-

are related to the natural gas supply disrup- tem operator (hereinafter – TSO) Conexus

40Baltic Grid [19]. However, before finishing Baltic region in the shortest possible terms.

enhancement of the Latvia–Lithuania inter- A number of traders may seek to diver-

connection (ELLI project) in 2024, current sify supply risks in the market as well.

interconnection capacities and operating However, there is a significant market

pressures are limited between Lithuania power, currently on the part of supplies

and Latvia (known as the bottleneck effect), from Russia, as well as on the part of the

therefore making it challenging to provide Baltic region industrial energy companies,

absolutely sufficient natural gas supplies to which maintain a high level of concentra-

Latvia, Estonia and Finland from the Lithu- tion. Market power discourages invest-

anian and Polish side [20], [21]. ments by private investors, relying solely on

The necessary natural gas reserve of expected demand for the natural gas import

capacity in the region is provided by Incu- capacity. Also, high volatility of the energy

kalns UGS, which allows fully compensat- prices with construction and development

ing for seasonal fluctuations (except for time delays discourages private investors.

Finland, which has to adjust the demand for Markets with high levels of concentration

maximum hours to the capacity of Balticco- and/or with signs of market power, show a

nnector). Nevertheless, the total amount of significant increase in risk, which discour-

available capacity at the Klaipeda LNG and ages private capital from making signifi-

GIPL entry points per year may be lower cant investments [22]. Therefore, the Bal-

than demand, depending on climate condi- tics States and Finland, since having high

tions and industrial demand. It addresses an market power from Russia’s gas, have low

important question of necessity to create at chances of fully-private investment in the

least one more LNG import terminal in the natural gas supply diversification projects.

3. TECHNICAL ASPECTS OF LNG TERMINAL

BUILDING PROJECT IN LATVIA

3.1. Site Selection Evaluation for Potential LNG Terminal in Latvia

Latvia, as all the Baltic countries and In general, it is believed that Skulte is

Finland, is located on the shores of the Bal- the best of the three possible locations with

tic Sea, with the coast line more than 450 several significant benefits:

kilometres long. When planning LNG ter- • geographical closeness to Incukalns

minal construction, various aspect should UGS;

be considered, such as closeness of the port • easy access and safe maneuvering of

cities, accessibility of the infrastructure the LNG vessels;

(transmission pipelines) and distance to • adequate terminal and pipeline routing

Incukalns UGS. Therefore, originally three separation from the residential areas;

potential locations of the LNG import ter- • lacking interference with the existing

minal were reviewed in Latvia: Ventspils ship traffic;

(with existing oil pipelines and port), Riga • ice-free port for most of the year;

(port) and Skulte (port). The comparison • no urgent need for LNG storage tanks

of the three chosen locations is shown in (with regard to closeness of Incukalns

Table 1. UGS) [23].

41Table 1. Comparison of Potential Locations of LNG Import Terminal in Latvia

Location Ventspils Riga Skulte

Solution/costs Port infrastructure is suit- Port infrastructure is suitable only

Port location is suitable

able only for onshore solu- for onshore solution, which has for FSU, which is the most

tion that has high CapEx high CapEx effective cost solution

Consumption Potential new consumption Location close to the biggest end Close location to Incu-

by port companies and city consumers in the country kalns UGS that is the key

infrastructure element in

the region

Ice conditions Ice free port Port has the biggest ice coverage Port has average ice cover-

in Latvia age in winter months

Grid Investments are required to Residential area around the port Pipeline distance to Incu-

connection upgrade existing oil trans- makes the pipeline routing to kalns UGS is 30– 35 km.

portation pipeline (200 km) grid (16 km) difficult. Distance to The route is crossing rural

and connection to the grid Incukalns UGS is 50km areas

Vessel traffic Terminal location is in the Terminal location is in the navi- Terminal is located outside

navigable area of the port gable area of the port that makes navigable area

that makes interference with interference with the main traffic

the main traffic

Flexibility Long distance to the Incu- Absence of direct connection to Very high flexibility

kalns UGS makes the low UGS lowers flexibility of supplies. because of direct connec-

flexibility in supplies In winter period, it is possible to tion to Incukalns UGS

absorb the regasified gas in the

natural gas distribution system

Other Process of land rent agreement Substantial support from

allocation lacks transparency port authorities

3.2. Evaluation of Potential LNG Terminal Concepts

Various LNG terminal types were com- Latvia and the Baltic region, and provide

pared in order to find the most suitable LNG relatively low operational costs of the ter-

import terminal solution that could ensure minal. The general estimate is shown in

both security of the natural gas supply for Table 2.

Table 2. Comparison of Potential LNG Import Terminal Concepts

Criterion Onshore terminal Floating Storage Regasifi- Floating Regasification Unit

cation Unit (FRSU) (FRU)

Costs Highest CapEx because of Relatively high CapEx Low CapEx because of simple

extensive ground building because of vessel use and technical solution – floating

(infrastructure and storage storage tank placement on platform with regasification

tanks) the vessel equipment

Operational High operational costs because Relatively high operational Low operational costs because

costs of extensive onshore storage costs because of storage of simple technical solution. No

and infrastructure maintenance tank and vessel maintenance costs on standby mode

Flexibility Low flexibility because of Low flexibility because of High flexibility because of direct

limited storage capacity limited storage capacity connection to Incukalns UGS

Freight It takes 2–3 days to unload the It takes 2–3 days to unload It takes about 6–8 days to

speed LNG vessel LNG vessel unload LNG at planned capac-

ity (can be increased)

Timing The building of such a terminal The building of such a ter- The project execution time is

takes 6 or more years minal takes 4 or more years estimated to be less than 2 years

after final investment decision

42Floating regasification unit (hereinaf- the floater is low compared to the conven-

ter – FRU) could ensure the lowest costs to tional ship shaped or barge solution and thus

the energy consumers, due to the low opera- low steel weight; this has a direct positive

tional costs, relatively simple technology impact on the construction and maintenance

and no need to store the natural gas on site. cost of the floater. Mooring of the floater at

FRU consists of a tubular structure where site could be conventional spread mooring.

the columns contribute most to the buoy- The visiting LNG carriers could be moored

ancy required. Due to the small and distrib- to the floater with conventional ship-to-ship

uted water plane area the floater will have mooring methods. These methods are in

very stable sea keeping characteristics. Due accordance with the tried and tested industry

to the tubular structure the displacement of practices.

3.3. Technical Aspects of Potential LNG Terminal in Latvia

For the Skulte LNG import terminal, that LNG shall be pressurized, vaporized

natural gas storage is considered to be at the and sent-out to a medium pressure sub-

Incukalns UGS. This, in principle, makes sea gas pipeline and onshore gas pipeline

the requirement for on-site LNG storage to Incukalns UGS. The project also would

redundant and thus brings down the project include the subsea pipeline and the onshore

capital expenditures (hereinafter – CapEx) pipeline carrying natural gas from the ter-

to as low as 1/3 to 1/4 of the other projects minal to either existing gas transmission

proposed in the Baltic Sea region. system or the UGS facility. The general

Implementation of Skulte LNG import technical information of Skulte LNG termi-

terminal, using FRU solution, will mean nal is summarised in Table 3.

Table 3. General Technical Information of Skulte LNG Terminal [23]

Terminal capacity Up to 3 million tonnes/year

Regasification capacity 600 million standard cubic feet of gas per day

Storage Existing UGS at Incukalns Latvia with capacity of 2.3. BCM

Supply LNG carrier size 40 000 m3 to 170 000 m3

Carried offload time 4 to 8 days at full capacity

The key element of the Skulte LNG capacity and gas transportation pressure in

import terminal concept is direct pipeline to the grid. The preliminary technical param-

Incukalns UGS, whose technical parameters eters for pipeline are provided in Table 4.

must be in line with terminal regasification

Table 4. Preliminary Technical Parameters for Pipeline Connecting Skulte LNG and Incukalns UGS

Transmission capacity 15–20 million m3/ day

Pressure 55 bar

Diameter 0.7 m

434. SITUATION EVALUATION IN THE BALTIC REGION

4.1. The Overview of Natural Gas Market

In the Baltic region, the natural gas fluctuations. The natural gas consumption

demand is historically dominated by power in the Baltics between 2015 and 2020 is

and heat generation and industrial con- shown in Fig. 2.

sumption, thus creating sensitivity to price

Fig. 2. The natural gas consumption in the Baltic States (2015–2020) [24].

Source: Eurostat

The largest natural gas consumers in increase and penetrate brand new sectors

the Baltic States are AB Achema (latgest of the national economies. There is a large

fertilizer producer in Baltic States, located potential for LNG to be used as truck fuel

in Lithuania), JSC Latvenergo (state-owned – a cleaner alternative comparing to diesel

energy company that generates about 70 % [4].

of the electric energy in Latvia), AB Lietu- It is not easy to assess the future posi-

vos Elektrinės (the owner of the Elektrėnai tion that natural gas will play in the energy

Power Plant in Lithuania), JSC Nitrofert mix of the Baltic States. The trends of natu-

(the only fertilizer producer in Estonia), ral gas consumption are influenced by the

JSC Rigas Siltums (the district heating overall development of the national econ-

company of Riga, Latvia), and other district omy, building energy efficiency develop-

heating companies. However, future trends ment, the use of modern and economical

of the natural gas consumption in the Bal- gas burning equipment and gradual replace-

tics could be affected by increased LNG ment of the natural gas with RGs [25].

use. Namely, the usage of natural gas could

444.2. Evaluation of LNG Projects in the Baltic Region

According to various sources, at least • an onshore storage tank costs are 1 mil-

ten potential LNG import terminal loca- lion EUR per 1000 m3 of storage capac-

tions were considered throughout the Bal- ity;

tic region: Liepaja, Ventspils, Riga, Skulte/ • regasification unit costs are 50 million

Lilaste (all in Latvia), Paldiski, Muuga, EUR;

Sillamae (all in Estonia), Inkoo and Turku • mooring costs are 10 million EUR

(both in Finland). Five projects (Skulte, regardless of type of technology used;

Paldiski, Talinn, Muuga and Inkoo) have • transmission network upgrades and

reached a certain development maturity connection to UGS are covered by sys-

stage to foresee a possibility to be actually tem charges and EU financial instru-

implemented [26]. ments (with 50 % gap) and not by LNG

Some projects are dependent on the terminal operator;

EU funding, therefore, need to meet Proj- • unloading freight time is included in

ects of Common Interest criteria. From case of floating regasification unit tech-

these potential projects, only Skulte LNG nology;

terminal has an immediate effect on the • 20-year period is used for financial cal-

natural gas supply portfolio of the Baltic culation, except for Klaipeda (10-year

region, both in terms of security of supply lease);

and supply diversification. It is located in • 8 % annual return rate for investments

the middle of the Baltic region, and it can is used for all terminals;

supply natural gas to its neighbouring coun- • 10-ship scenario is used as a base sce-

tries immediately after its commissioning nario for regasification cost comparison

without major investments in the additional and 20–5 ship scenario is used to dem-

natural gas pipeline infrastructure. onstrate flexibility cost of the terminal

In order to outline competitiveness of (penalty for low utilisation compared to

Skulte LNG terminal project, four existing high utilisation);

and planned LNG terminal projects were • Freight cost is assumed to be 60 000

compared in accordance with several cri- EUR per day.

teria, summarised in Table 5. These termi- Based on assumptions explained

nals are: floating storage and regasification before, Table 1 indicates that since Skulte

terminal in Klaipeda, onshore terminal with LNG terminal would not need storage tank

lowered storage capacity in Riga, float- (since it is possible to efficiently use Incu-

ing regasification terminal in Skulte and kalns UGS, if transmission interconnection

onshore terminal with full storage capacity is built), it would reach total costs of about

in Paldiski/Inkoo. EUR 60 million, while other projects would

Since three different technologies are cost from EUR 260 to 430 million, making

involved, for clarity purposes the following Skulte LNG significantly cheaper and more

assumptions are made: cost-effective than other LNG terminal

projects under review in the Baltic region.

45Table 5. Evaluation of LNG Projects in the Baltic Region

Location, Technol- Storage Unload Supply agree- Financial Total gap Total cost at 1

Annual ogy tank costs ments structure BCM scenario

regasifica-

tion capac-

ity (50 %

utilisation

rate)

Klaipeda, FSRU 170 000 Indirect – ToP agreements 10-year finan- NA Total cost:

2 BCM shutdown are crucial – no cial lease with EUR 430 million;

of other flexibility available a mandatory regasification cost:

terminals in for the terminal market share 46 EUR/1000m3

the port (additional storage

capacities of flex-

ible consumption)

Riga, Onshore 200000 No costs To achieve reason- Not defined 195 million Total cost:

2 BCM associated able capacities ToP but consid- EUR EUR 260 million;

agreements are erable gap regasification cost:

needed for opera- (75 %) of 26.4 EUR/1000m3

tion but partly it financial Regasification cost

could be operated resources with covered gap:

on the opportunis- should be cov- EUR 11.85/1000m3

tic basis ered by public

funding

Skulte, FRU N/A Unloading Opportunistic Commercial 20 million Total cost:

2 BCM freight costs trade mainly, due offtake cover- EUR EUR 60 million;

to low cost of flex- age with lim- regasification cost:

ibility and ability ited (33 %) or EUR 12.4/1000m3

to operate with favourably no Regasification cost

irregular shipment market gap for with covered gap:

schedule optimal level EUR 10.6/1000m3

of utilisation

Inkoo, Onshore 300000 No costs ToP agreements Not defined, 120 million Total cost:

2 BCM associated mainly and limited but existing EUR EUR 360 million,

amount of oppor- available regasification cost:

tunistic trading market for EUR 35.4/1000m3

power genera- Regasification cost

tion, industrial with covered gap:

and trans- EUR 24.6/1000m3

port sector;

nevertheless,

gap (33 %)

of financial

resources

should be cov-

ered by public

funding

5. POLITICAL AND REGULATORY

PERSPECTIVES OF LNG DEVELOPMENT IN LATVIA

5.1. Energy Market Regulation

Most of energy market activities are heating industries shall obtain license from

regulated businesses in Latvia. Market the Public Utilities Commission. LNG ter-

operators in power, natural gas and district minal operation, the natural gas transmis-

46sion and the natural gas trade are among market [27]. Framework of the natural gas

licensed activities. Currently there are 28 market in Latvia is shown in Fig. 3.

natural gas traders in the Latvian natural gas

Fig. 3. Framework of the natural gas market in Latvia [28].

Source: JSC Conexus Baltic Grid

If developed, Skulte LNG terminal will the cooperation capability of several neigh-

need to acquire LNG operation license and bouring countries. The common natural gas

the natural gas transmission license to oper- market is characterised by unified entry-exit

ate FRU and connector pipeline to Incu- tariff area, and single Estonian–Latvian bal-

kalns UGS. Since 2020, when the single ancing zone, while continuously cooperat-

natural gas market in the Baltics has been ing would ensure deeper integration with

launched, it unites the natural gas TSOs prospects of Lithuania joining the market as

of Finland, Latvia, and Estonia – Gasgrid well [29].

Finland, Elering, and Conexus, confirming

5.2. Access to the Infrastructure

The Energy Law (hereinafter – EL) pro- Due to a high level of infrastructure

vides non-discriminatory, tariff-based third- integrity and importance of security of

party access to the natural gas infrastructure the natural gas supplies for the national

[30]. Capacity allocations, congestion man- economy, prices for the natural gas infra-

agement and different capacity reservation structure services are regulated by tariffs in

products are provided by the national trans- accordance with the Law On Public Utili-

mission and storage network code. Selling ties Regulators [31]. Tariff structures are

capacity reservation products in secondary changing from cost plus to revenue cap pat-

market is allowed. For the time being short- terns with numerous variations.

term capacity reservation products (up to The EL also provides an exemption

one year) are the most popular in the mar- from general third-party access regime for

ket. However, long-term capacity reserva- new infrastructure projects. Conditions for

tion products can be designed by the TSO such an exemption are as follows:

should there be interest from market partici- • the investment must enhance com-

pants. petition in the natural gas supply and

enhance security of supply;

47• the level of risk attached to the invest- The national regulatory authority grants

ment must be such that the investment the exemption, if ex ante verification from

will not take place unless an exemption the EC is received. Detailed procedure and

is granted; evaluation criteria for the exemption are

• the infrastructure must be owned by a stipulated in Directive 2009/73/EC of the

natural or legal entity that is separate at European Parliament and of the Council

least in terms of its legal form from the of 13 July 2009 concerning common rules

system operators, in whose systems that for the internal market in natural gas and

infrastructure will be built; repealing Directive 2003/55/EC [32].

• charges must be levied on users of that Skulte LNG Terminal operator may

infrastructure; need to secure third-party access to the ter-

• the exemption must not be detrimental minal and the natural gas transmission via

to competition or the effective function- a connector pipeline. Therefore, it is to be

ing of the internal market in natural gas, decided whether Skulte LNG terminal proj-

or the efficient functioning of the regu- ect operator will apply for derogation from

lated system, to which the infrastructure third-party access or not.

is connected.

5.3. LNG Project Characteristics and Risks

LNG projects possess characteristics depend upon the long-term stability and

and risks that tend to amplify the poten- predictability of regulatory, political and

tial for high value disputes. Such projects economic environments [33], [34].

are highly technically challenging (includ- For liquefaction and regasification proj-

ing floating LNG technology) and require ects in particular, the risks associated with

a myriad of sub-contractors, often based them include: project economics, environ-

across multiple jurisdictions. They are envi- mental approvals and regulation, political

ronmentally sensitive and subject to strin- risks, joint venture risks, technical engi-

gent regulatory requirements. LNG projects neering, procurement and construction

are often politically sensitive and subject challenges, feedstock challenges and end

to significant public scrutiny. LNG proj- product marketing and contracting. All of

ects involve very significant upfront capi- the above risks can affect heavily an LNG

tal expenditure, with essentially no income project and lead to disputes. Successfully

generation prior to project commissioning addressing project implementation chal-

[33]. Moreover, the overall viability of an lenges on all levels can be critical to pros-

LNG project, which may have an expected pects of every LNG import project [35].

lifetime exceeding 30 years, will often

5.4. Construction of the Infrastructure Objects

There are a number of stages (phases) • construction of related infrastructure

to any LNG terminal project, which com- (connecting pipelines);

monly include, but are not limited to: • commissioning and handover;

• planning and regulatory approvals; • post-commissioning operations [35].

• front end engineering and design

(FEED); However, in many cases, they can be

• construction; reduced to only two general phases – the

48exploration / engineering and construction therefore, it is expected that it will be sub-

phase (also associated with pre-final invest- jected to, at least, an initial assessment of

ment decision (FID) and post-FID phases environmental risks. Positive conclusion of

[36]). Execution of both phases is regulated initial or full environmental assessment is a

by specific laws, and Skulte LNG terminal prerequisite for further project implementa-

project implementation shall include both tion.

phases. Building of the natural gas transmission

Exploration phase for the LNG termi- pipeline is an activity with a material envi-

nal and underwater floating regasification ronmental impact according to the EIA.

unit connection to pipeline begins with the At the same time, the EL confers to

acquisition of seabed exploration permit. energy infrastructure operators a right to

The National Sea Environment Protec- use third-party land to set up an infrastruc-

tion and Management Law [37] provides ture object. It prescribes two options on the

that right to exploit and, consequently, to acquisition of such a right. The first option

explore seabed that shall be tendered. How- is to contract with landowners on the right

ever, according to Ports Law [38] no ten- to use their land. The second option is the

dering is applicable if seabed exploitation acquisition of the right to use the land irre-

is planned within sea territory allocated spective of landowners’ consent, if one of

as territory of the port. Location of Skulte following requirements is met:

LNG terminal is planned within territory • building of an infrastructure object is

of Skulte Port subject to an agreement with provided in a zoning plan of a respec-

the port authorities. It is expected that no tive municipality;

tendering procedures will be necessary to • municipality has confirmed that an

gather seabed exploration permit and fur- infrastructure object is of public interest

ther exploitation of a respective area. and particular land plots are necessary

Construction and operation of the LNG to build it;

terminal may have a direct and material • an infrastructure object has status of an

impact on the environment. Environmen- object of the national interest. The EL

tal Impact Assessment Law (hereinafter – provides that in all above cases land-

EIA), provides two types of environmental owners shall get compensation from

impact assessment, initial assessment and infrastructure developers for use of their

full assessment [39]. The EIA provides a property [30]. Amount of remuneration

list of activities that are subject to a par- is calculated according to regulations of

ticular type of assessment. However, fur- the Cabinet of Ministers.

ther full assessment of a potential activity

may be required if results of initial assess- Possible routes of Skulte LNG connec-

ment reveal the need for that. Initial assess- tor pipeline are planned mainly through

ment is executed by the state institution, agricultural land plots. Major part of private

Regional Environmental Administration, land plots to be crossed by the pipeline is

within 20 days from the receipt of all docu- used for farming purposes and most of them

ments from activity promoters. Full assess- shall remain as agricultural land after pipe-

ment shall be executed by a licensed asses- line is built. Landowners therefore shall not

sor. Usually, it takes about 8–12 months to suffer material damages and legal restric-

complete. Operation of LNG terminal is an tions to use their property.

activity with advanced safety requirements; Design and construction of underwater

49floating regasification unit connection and gle building permit shall be issued by the

connector pipeline is subject to the Con- State Construction Control Bureau of Lat-

struction Law [40] and regulations, which via for objects of the national interest with

specify that building permits shall be issued no right for municipalities to object.

by relevant municipalities. However, a sin-

5.5. Object of the National Interest

According to the Spatial Development thus, recent geopolitical developments in

Planning Law of Latvia (hereinafter – Russia and Ukraine have exposed vulner-

SDPL), objects of national interest are ability and volatility of this source.

objects securing material public interests, Skulte LNG terminal project would

protection and sustainable use of the natural allow sourcing LNG from various suppli-

resources. Skulte LNG terminal and trans- ers worldwide, such as Norway, the USA,

mission pipeline might qualify for the status Qatar, Algeria, Nigeria, Trinidad and others.

[41]. Currently major part of natural gas for Two of the most likely routes could be from

the Baltic countries is sourced in Russia; the USA or Norway, as shown in Fig. 4.

Fig. 4. Potential import routes from North America and Hammerfest, Norway.

Source: JSC Skulte LNG Terminal

The SDPL provides that the Cabinet of land for building of an object of national

Ministers may confer status of an object interest. Such a status would ensure faster

of the national interest upon proposal of a and smoother project development, which

competent ministry [41]. For Skulte LNG would be valuable in circumstances, when

project, it is the Ministry of Economics. all the Russian gas import must be reduced

The main advantages of having this status to the bare minimum or even completely

are as follows: challenging building per- ceased. In this case, LNG import terminal

mits for such an object does not stop the development in Skulte would ensure fast

building process, energy supply companies and efficient natural gas supply routes and

acquire statutory right to use third-party source diversification for Latvia [42].

506. CONCLUSIONS

LNG import terminal would help reduce Low cost will be benefitting costumers,

dependency on the pipeline natural gas sup- while price effect will ensure flexibility of

plies which, in some cases, due to the insuf- supply provided by terminal direct con-

ficient interconnections, may be delivered nection to Incukalns UGS that will ensure

only from one or limited number of sources. direct impact on the price. In addition, it

In the context of Latvia, it was evaluated will provide possibility for potential traders

that there was a potentially beneficial role to buy LNG in spot market in the favour-

of the LNG terminal development in Skulte, able time periods.

which would help strengthen energy inde- FRU is the most suitable terminal solu-

pendence of the whole Baltic region as tion for Latvia because of low CapEx, high

well as introduce new natural gas delivery flexibility and fast project execution time.

sources in a cost-efficient way. Direct pipeline connection to Incukalns

LNG terminal in Skulte could also UGS can provide possibility to avoid build-

ensure significant capital investment cost ing LNG storage tanks onshore that is often

reduction compared to other LNG proj- the major part of import terminal costs.

ects in the region, due to already existing To sum up, there is a need for additional

infrastructure and the relative closeness of natural gas delivery sources, and LNG ter-

Incukalns UGS. It can also be characterised minal in Latvia would help the Baltic region

by easy access and safe manoeuvring of the with it. If the natural gas security of sup-

LNG vessels, adequate terminal and pipe- ply is a national priority, there is a need for

line routing division from the residential public investment in LNG import projects,

areas. which can be implemented in the shortest

The main benefits of Skulte LNG proj- possible terms, with ability to guarantee

ect are low CapEx compared to other proj- stable, secure and diversified natural gas

ects proposed in the neighbouring counties. supplies.

ACKNOWLEDGEMENTS

The research has been supported by Latvian Gas Infrastructure Development”

the National Research Programme project (LAGAS) (No. VPP-EM-INFRA-2018/1-

“Trends, Challenges and Solutions of 0003).

REFERENCES

1. Delliote. (n.d.). Fit for 55 Package. EU ec.europa.eu/commission/presscorner/

Legislative Action for the Climate. Available detail/en/QANDA_22_712

at https://www2.deloitte.com/lv/en/pages/ 3. Savickis, J., Zemite, L., Zeltins, N., Selickis,

consulting/solutions/Fit-for-55-package.html A., & Ansone, A. (2020). The Biomethane

2. EC. (2022). Questions and Answers on the Injection into the Natural Gas Networks:

EU Taxonomy Complementary Climate The EU’s Gas Synergy Path. Latvian

Delegated Act Covering Certain Nuclear Journal of Physics and Technical Sciences,

and Gas Activities. Available at https:// 57 (4), 34–50. doi: 10.2478/lpts-2020-0020

514. Savickis, J., Ansone, A., Zemite, L., Bode, EuropeanUnionsRelianceonRussianNatura

I., Jansons, L., Zeltins, N. … & Dzelzitis, lGas.pdf

E. (2021). The Natural Gas as a Sustainable 12. ACER. (n.d.). EU Gas Wholesale Mar-

Fuel Alternative in Latvia. Latvian Journal kets 2015-2020. Available at https://

of Physics and Technical Sciences, 58 (3), app.powerbi.com/view?r=eyJrIjoiMjJ

169–185. doi: https://doi.org/10.2478/lpts- mYWQ4NjctYWIwNC00NzNjLWI5M

2021-0024 mMtODVmOTQ0M2Q5YmI4Iiwid

5. Hauser, P., & Most, D. (2015). Impact of C I 6 I m U 2 M j Z k O T B j LTc w Y W U t N

LNG imports and shale gas on a European G R m Y y 0 5 N m J h LTAy Z j E 4 Y 2 M w M

natural gas diversification strategy. In 12th DA3ZSIsImMiOjl9

International Conference on the European 13. Trading Economics. (2022). EU Natural

Energy Market (EEM), (pp. 1–5), 19–22 Gas, TTF Gas. Available at https://

May 2015, Lisbon, Portugal. tradingeconomics.com/commodity/eu-

6. Meza, A., Koc, M., & Saleh Al-Sada, natural-gas

M. (2022). Perspectives and Strategies 14. Euractiv. (2022). Russian Gas Flows

for LNG Expansion in Qatar: A SWOT via Yamal Pipeline to Germany Decline

Analysis. Resources Policy, 76. https://doi. Sharply. Available at https://www.euractiv.

org/10.1016/j.resourpol.2022.102633 com/section/global-europe/news/russian-

7. Najm, R., & Matsumoto, K. (2020). gas-flows-via-yamal-pipeline-to-germany-

Does Renewable Energy Substitute decline-sharply/

LNG International Trade in the Energy 15. France24. (2022). Russian Gas Supplies

Transition? Energy Economics, 92. https:// to Europe Decline Sharply. Available at

doi.org/10.1016/j.eneco.2020.104964 https://www.france24.com/en/tv-shows/

8. Euractiv. (2011). Baltic Countries Ask EU business-daily/20220303-russian-natural-

to Solve LNG Terminal Row. Available at gas-supplies-to-europe-decline-yamal-

https://www.euractiv.com/section/energy/ pipeline

news/baltic-countries-ask-eu-to-solve-lng- 16. Energypost. (2022). Yamal-Europe Gas

terminal-row/ Pipeline Shows how EU Competition Rules

9. Euractiv (2022). LEAK: EU Drafts Plan Backfire during a Shortage. Available at

to Ditch Russian Gas. Available at https:// https://energypost.eu/yamal-europe-gas-

www.euractiv.com/section/energy/news/ pipeline-shows-how-eu-competition-rules-

leak-eu-drafts-plan-to-ditch-russian-gas/ backfire-during-a-shortage/

10. Communication from the Commission to the 17. Ministry of Economics. (2020). Latvian

European Parliament, the European Council, Preventive Action Plan for Natural Gas.

the Council, the European economic and Available at https://docplayer.lv/211717165-

social committee and the Committee of Latvijas-prevent%C4%ABv%C4%81s-

the regions. REPowerEU: Joint European r%C4%ABc%C4%ABbas-pl%C4%81ns-

Action for more affordable, secure and dabasg%C4%81zei.html

sustainable energy, COM/2022/108. Final. 18. Ekonomikas ministrija. (2020). Dabasgāzes

Available at https://eur-lex.europa.eu/legal- apgādes drošums. Available at https://www.

content/EN/TXT/?uri=COM%3A2022%3 em.gov.lv/lv/dabasgazes-apgades-drosums

A108%3AFIN 19. Conexus. (2022). Announced an Early

11. International Energy Agency. (2022). A Warning in the Natural Gas Supply

10-Point Plan to Reduce the European Sector. Available at https://www.conexus.

Union’s Reliance on Russian Natural Gas. lv/aktualitates-sistemas-lietotajiem-

Available at https://iea.blob.core.windows. eng-575/izsludinats-agrinais-bridinajums-

net/assets/1af70a5f-9059-47b4-a2dd- dabasgazes-apgades-nozare

1b479918f3cb/A10-PointPlantoReducethe

5220. Amber Grid. (2022). Amber Grid Signs Works 28. Conexus Baltic Grid. (2019). Medium Term

Contract for Project ELLI in Preparation Strategy 2019-2023. Available at https://

for Doubling Gas Transmission Capacity www.conexus.lv/uploads/filedir/Media/

between Lithuania and Latvia. Available conexus_mid_term_strategy.pdf

at https://www.marketscreener.com/quote/ 29. Zemite, L., Ansone, A., Jansons, L., Bode,

stock/AB-AMBER-GRID-44154872/news/ I., Dzelzitis, E., Selickis, A., & Vempere,

AB-Amber-Grid-Amber-Grid-signs-works- L. (2021). The Creation of the Integrated

contract-for-project-ELLI-in-preparation- Natural Gas Market in the Baltic Region

for-doubling-gas-tra-37836684/ and its Legal Implications. Latvian Journal

21. Esmaeili, M., Shafie-khah, M., & Catalao, of Physics and Technical Sciences, 58 (3),

J. (2022). A System Dynamics Approach 201–213. DOI: https://doi.org/10.2478/lpts-

to Study the Long-Term Interaction of the 2021-0026

Natural Gas Market and Electricity Market 30. Enerģētikas likums. (1998). Available at

Comprising High Penetration of Renewable https://likumi.lv/ta/id/49833-energetikas-

Energy Resources. International likums

Journal of Electrical Power & Energy 31. Par sabiedrisko pakalpojumu regulatoriem.

Systems, 139. https://doi.org/10.1016/j. (2000). Available at https://likumi.lv/ta/

ijepes.2022.108021 id/12483-par-sabiedrisko-pakalpojumu-

22. Borenstein, S., Bushnell, J.B., & regulatoriem

Wolak, F. A. (2002). Measuring 32. Directive 2009/73/EC of the European

Market Inefficiencies in California’s Parliament and of the Council of 13 July

Restructured Wholesale Electricity Market. 2009 concerning common rules for the

American Economic Review, 92 (5). doi: internal market in natural gas and repealing

10.1257/000282802762024557 Directive 2003/55/EC. Available at https://

23. WoodMakenzie. (2022). Gas and LNG: eur-lex.europa.eu/legal-content/EN/

Predictions for 2022. Available at https:// ALL/?uri=celex%3A32009L0073

w w w. w o o d m a c . c o m / n e w s / o p i n i o n / 33. Ruester, S. (2015). Financing LNG Projects

gas-and-lng-predictions-for-2022-2022- and the Role of Long-Term Sales-and-

outlook/ Purchase Agreements. Available at https://

24. Skulte LNG terminal. (n.d.). The project. globallnghub.com/wp-content/uploads/

Available at https://www.skultelng.lv/en/ attach_84.pdf

the_project/ 34. Stern, J. (2019). Challenges to the Future

25. EC. (2022). Supply, Transformation and of LNG: Decarbonisation, Affordability

Consumption of Gas. Available at https:// and Profitability. Oxford Institute for

ec.europa.eu/eurostat/databrowser/view/ Energy Studies. Available at https://www.

NRG_CB_GAS__custom_2274868/ oxfordenergy.org/wpcms/wp-content/

default/table?lang=en uploads/2019/10/Challenges-to-the-Future-

26. Booz&Co. (2012). Analysis of Costs and of-LNG-NG-152.pdf

Benefits of Regional Liquefied Natural 35. NRF. (2018). LNG Construction Arbitration –

Gas Solution in the East Baltic Area, From the Beginning to the End. Available

Including Proposal for Location and at https://www.nortonrosefulbright.com/

Technical Options under the Baltic Energy en/knowledge/publications/de6861c4/

Market Interconnection Plan Final Project lng-construction-arbitration---from-the-

Report. Available at https://energiatalgud. beginning-to-the-end%20

ee/sites/default/files/images_sala/1/16/ 36. PwC. (2014). The Progression of an LNG

Booz%26Co_LNG_in_the_East-Baltic_ Project. Canadian LNG Projects. Available

region.pdf at https://www.pwc.com/gx/en/mining/

27. Public Utilities Commission. (2022). Gas publications/assets/pwc-lng-progression-

Trader List. Available at https://www.sprk. canada.pdf

gov.lv/content/registresanalicencesana

5337. Marine Environment Protection and 41. Spatial Development Planning Law. (2011).

Management Law (2010). Available at Available at https://likumi.lv/ta/en/en/

https://likumi.lv/ta/en/en/id/221385 id/238807

38. Law on Ports. (1994). Available at https:// 42. Savickis, J., Zemite, L., Jansons, L., Zeltins,

likumi.lv/ta/en/en/id/57435 N., Bode, I., Ansone, A., … & Koposovs, A.

39. On Environmental Impact Assessment. (2021). Liquefied Natural Gas Infrastructure

(1998). Available at https://likumi.lv/ta/en/ and Prospects for the Use of LNG in the

en/id/51522 Baltic States and Finland. Latvian Journal

40. Construction Law. (2013). Available https:// of Physics and Technical Sciences, 58 (2),

likumi.lv/ta/en/en/id/258572 45–64. doi: 10.2478/lpts-2021-0011

54You can also read