Strategic Combination - Establishing the Premier Pure-Play Pipestone Montney Company - Blackbird Energy Inc.

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Strategic Combination Establishing the Premier Pure-Play Pipestone Montney Company Sustainable long-term condensate growth OCTOBER 2018

Funded growth and increased scale

Blackbird Energy Inc. (“Blackbird”) and Pipestone Oil Corp. (“Pipestone Oil”)

have agreed to combine to form Pipestone Energy Corp. (“Pipestone Energy”)

• Pro forma ownership of 45.1% for • Pipestone Oil will receive 103.75 million

Blackbird shareholders (or 50.8%, common shares of Pipestone Energy (1)

inclusive of all dilutive securities exercised) (1,037.5 million common shares of

Blackbird)

• Insiders and GMT Capital Corp.

(“GMT”), representing 17% ownership • Canadian Non-Operated Resources

of Blackbird, support and will vote in (“CNOR”) (2) has agreed to support and

favour of the arrangement has approved the transaction

All-share combination structured as a plan of arrangement

$111 million • Commitment from CNOR to invest $85 million

(3)

Equity Financing • Commitment from GMT to invest $26 million

• $169 million two-year term loan

$199 million

• $20 million letter of credit facility

Debt Financing

• $10 million revolving credit facility

Superior Market Positioning Material Synergies

Attractive Financial Terms Uplifting Transaction Structure

1. After adjustment for the proposed 10:1 share consolidation.

2. Pipestone Oil is a wholly-owned subsidiary of CNOR, a private energy investment platform managed by Grafton Asset Management.

3. The new directors and officers of Pipestone Energy are anticipated to contribute an additional amount of equity (up to $4.4 million), on a private placement basis. 1

Strategic rationale for Blackbird

Unique opportunity to enhance Blackbird shareholder exposure to top-tier Montney assets

and secure $310 million in equity and debt financing (the “Financings”) to fund development

Superior Market Positioning Material Synergies

Creates the premier Montney growth Increased and high-graded top tier

story with superior economics drilling inventory

Compelling value on integration, Interlocking lands, integration facilitates

relative to area transaction precedents improved development efficiencies

World class scale, wider appeal to Optimization of diversified infrastructure

attract industry / institutional interest and egress solutions

Corporate, G&A and regulatory savings

Attractive Financial Terms Uplifting Transaction Structure

De-risked access to lower cost capital Continued participation for

for development to reach free cash shareholders in a stronger company

flow (1) Accretive on all independent reserve,

Superior alternative to stand-alone resource and NAV fundamentals

equity or debt financing options Tax friendly transaction

Accelerated development plans add net Aligned views to maintain and build on

present value to shareholders established social license

1. Free cash flow, as referred to throughout this presentation is a non-IFRS measure. See “Non-IFRS Measures” for more details. 2

Introducing Pipestone Energy Corp.

Canada’s newest intermediate condensate-rich producer

Transformative Business Combination Pro Forma Perspectives

Exit 2019E

Net Montney

Sales Processing 2P Reserves (1) Business Combination Highlights

acres

Capacity

~22,500 165 >98,000 • Canada’s next high growth condensate producer

boe/d

MMboe net acres • Committed funding to achieve 2019E exit rate of 14,000 to

16,000 boe/d with $145-165 million of run-rate NOI (2)

72,640

net acres • De-risked value proposition through improved business

flexibility, access to capital, midstream diversification,

operating synergies, scale and liquidity

59

~6,500 MMboe

• Continuity of leadership and social license with Blackbird

boe/d Energy Inc. Chairman, CEO and President, Garth Braun and

Paul Wanklyn, President & CEO of Pipestone Energy Corp., to

serve on the new seven member board of directors

Blackbird Pipestone Blackbird Pipestone Blackbird Pipestone Pro Forma Capitalization

Energy Energy Energy

Material increase in 180% increase to Increased inventory Common Shares Outstanding 1.9 billion (3)

processing capacity proved + probable of top tier Montney

Listed Warrants Outstanding 175.2 million (3)

supporting reserve volumes acreage at Pipestone

near-term growth Est. Adjusted Net Debt (Cash) (September 30, 2018) $(60) million (4)

1. Based on Blackbird’s reserve volumes as at July 31, 2018 per McDaniel & Associates Consultants Ltd. and Pipestone Energy’s estimated pro forma reserve volumes as at August 1, 2018 per McDaniel & Associates Consultants

Ltd.

2. Flat US$65/bbl WTI, C$1.90/GJ ($2.00/Mcf) AECO, 0.775 CADUSD. NOI, as referred to throughout this presentation is a non-IFRS measure. See “Non-IFRS Measures” for more details.

3. Before adjustment for the proposed 10:1 share consolidation.

4. Includes estimated transaction costs and proceeds from the Financings. Adjusted net debt, as referred to throughout this presentation is a non-IFRS measure. See “Non-IFRS Measures” for more details. 3

Experienced management and board

Pipestone Energy will have leadership continuity through board representation and

will be led by a team with extensive experience in the Grande Prairie region

Board of Directors Leadership Team

Garth Braun Blackbird nominee Paul Wanklyn President and CEO

President, CEO and Chairman at Blackbird Senior Partner at Grafton Asset Management; President & CEO at

Cequence Energy Ltd.; and CEO at Temple Exploration Inc.

Bill Lancaster Blackbird nominee Bob Rosine COO

President at GMT Exploration Company LLC

COO at Grafton Asset Management; President & CEO at OMERS

Energy Inc.; and Executive Vice President, Business Development at

Geeta Sankappanavar CNOR LP nominee Pengrowth Energy Corporation

Co-Founder & President at Grafton Asset Management

Dave Allen Geoscience

VP Geosciences at Grafton Asset Management; and Vice President,

Robert Tichio CNOR LP nominee Exploration at Pengrowth Energy Corporation

Partner at Riverstone Holdings

Darcy Erickson Operations

Paul Wanklyn CNOR LP nominee VP Operations & Production at Grafton Asset Management; and

Director, Joint Ventures and Drilling & Completions at Pengrowth

President and CEO at Pipestone Energy

Energy Corporation

+ two additional independent nominees Dan van Kessel Corporate Development

process ongoing to identify two of the board of directors, one of which Vice President at Grafton Asset Management; and Investment

will serve as the Chairperson of the Pipestone Energy board of directors Banking Associate at a global investment bank

Note: Current CFO of Blackbird (Travis Belak) and CFO / VP Finance at Pipestone Oil (Eva Kiefer) will continue in their capacities during the interim period while an executive search for a permanent CFO is completed.

4

Investment highlights of Pipestone Energy

A premier high growth pure-play condensate rich Montney company

Dominant pure-play Pipestone Montney company in the “sweet spot” of the condensate fairway

• Over 98,000 net acres of contiguous Montney lands in the condensate-rich corridor of the Alberta Montney at Pipestone

• Montney formation is thick and laterally continuous across land base, with four prospective development horizons

• 2P Reserves of ~165 MMboe (~$1.2 billion before tax NPV 10%) and 2C Risked Resource of ~221 MMboe (~$0.8 billion before tax

NPV 10%), with 555 booked 2P and 2C drilling locations (1)

Fully funded to realize peer-leading growth profile

• Committed funding to achieve 14,000 to 16,000 boe/d by the end of 2019

• 20 wells will be tied into new facilities by year end 2019

• Development expenditures fully funded by the Financings and forecast cash flow from operations

• Forecast 2019 exit annualized NOI of ~$145 to $165 million ($28 per boe netback) (2)

Superior economics

• Strong initial test results with rates of 900 to 3,100 boe/d (average ~1,800 boe/d) and condensate gas ratios of up to 300 bbl/MMcf

(average ~170 bbl/MMcf) (3)

• Half-cycle IRRs greater than 95% with a payout period of ~13 months at flat pricing (2)(4)

Positioned for significant long-term growth

• 16 wells to be drilled and 14 completed from October 1, 2018 to year end 2019

• Current restricted production behind pipe of ~9,000 boe/d to support near-term growth

• Contracted natural gas processing and egress solutions to support production growth to 30,000 boe/d by 2022E

• Sustained production potential of over 50,000 boe/d from two Montney development intervals, with upside from the Montney A and

Lower Montney

Decades of drilling inventory

• Up to 1,450 potential drilling locations identified across four prospective Montney horizons

• Land base is well delineated with 31 horizontal wells drilled, completed and tested across the property

• Currently delineating Lower Montney development horizon

1. Based on McDaniel & Associates Consultants Ltd. reserves and resource evaluations effective August 1, 2018, utilizing the McDaniel July 1, 2018 price deck.

2. Flat US$65/bbl WTI, C$1.90/GJ ($2.00/Mcf) AECO, 0.775 CADUSD. IRR and operating netback, as referred to throughout this presentation is a non-IFRS measure. See “Non-IFRS Measures” for more details.

3. Represents production over the last 24 hours of a production test.

4. Type curve represents the McDaniel VRGC2 Montney B type curve, assuming a 2,500 metre lateral length. Capital costs reflect current internal estimates based on recent drilling and completion activities. 5

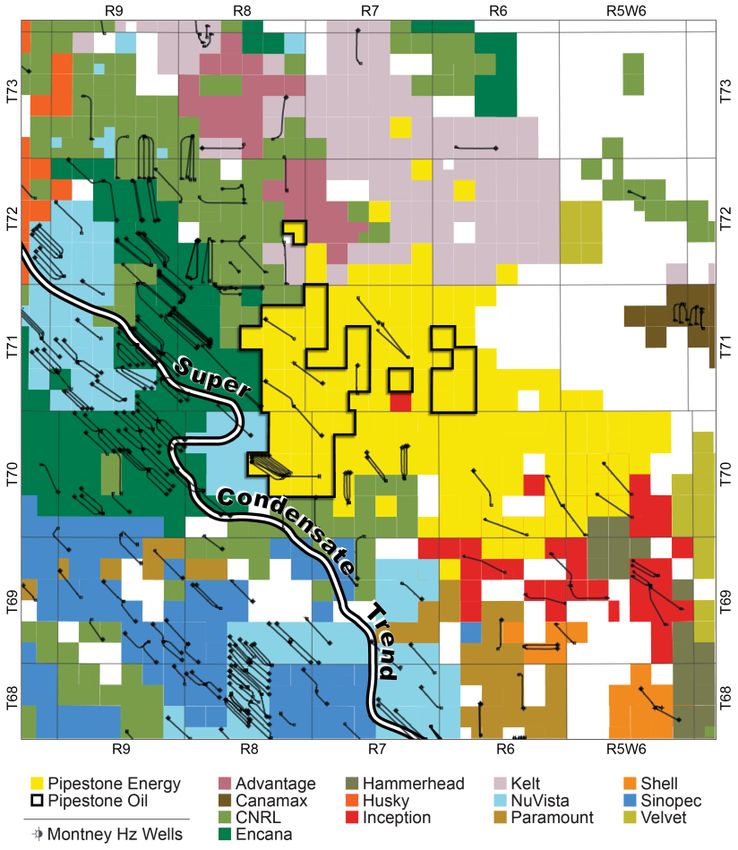

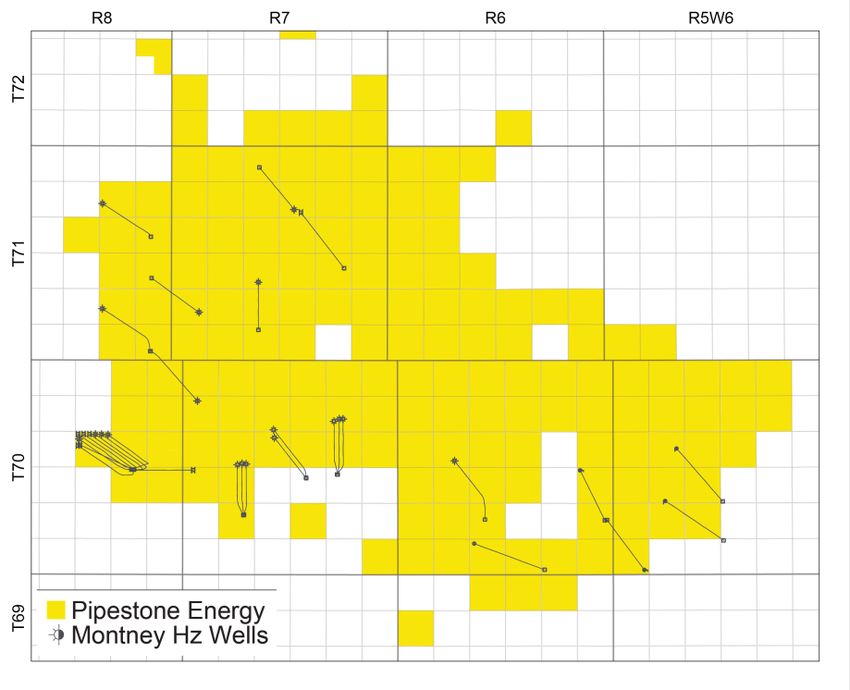

The perfect fit

Combination of highly complementary acreage creates pure-play

Pipestone Montney company with the largest land holding in the area

Pipestone Montney Area Map Pipestone Montney Acreage Holders (1)

# of sections in the super condensate trend

180

160

140

120

100

80

60

40

20

-

Pipestone Kelt CNRL Encana NuVista Advantage

Energy

1. Land positions based on the map shown and sourced from public disclosure / geoSCOUT. 6

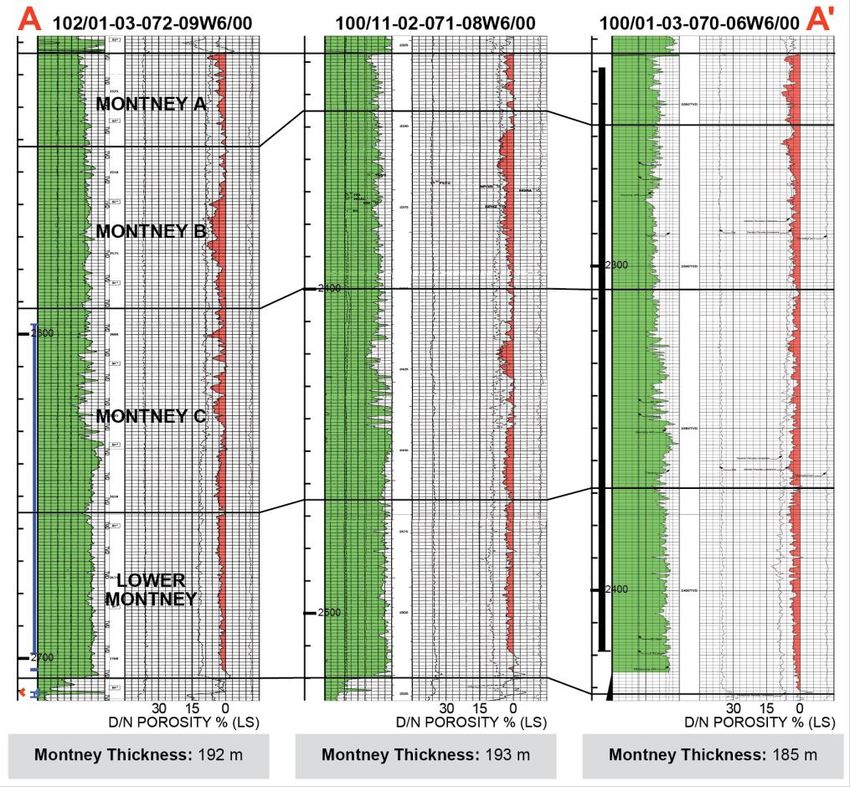

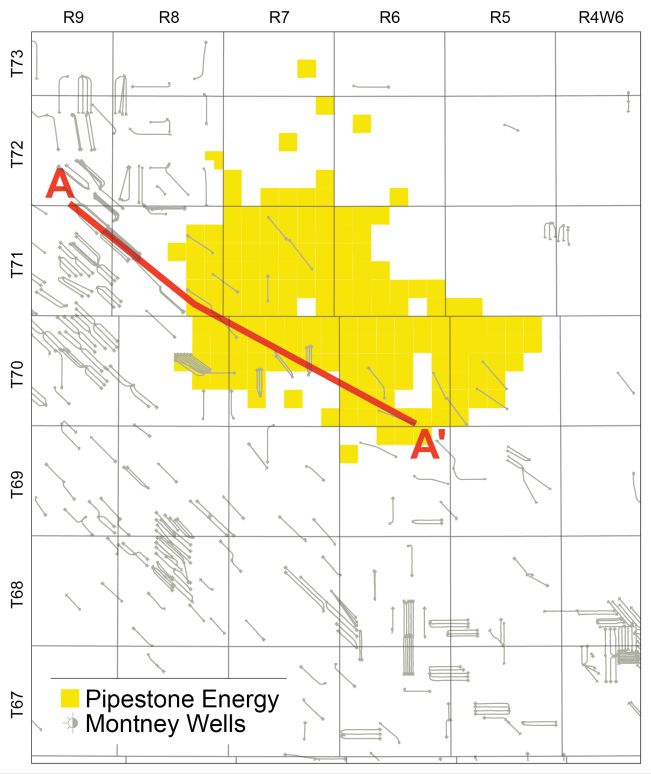

Consistent geology

Across Pipestone Energy’s land base, the Montney is thick, high quality,

and laterally continuous with four prospective development layers

Pipestone Area Cross Section

Encana Pipestone Energy

• Tested by offset

operators

• Proven on

Pipestone

Energy lands

• Commercially

proven by offset

operators

• Q4 2018E

Pipestone

Energy testing

• Proven by

offset operators

7In the sweet spot

173 gross sections of contiguous lands, all located in the super condensate trend

Large scale new

investment in regional

natural gas and liquids

processing capacity by

high quality midstream

operators

Pipestone Energy’s

lands are on trend with

recent drilling activity

from established

operators in the

condensate-rich

Montney fairway

8Strong recent well results to date

Average last 24-hour test results from Pipestone Oil wells in the Montney ‘B’ of 2,200 boe/d

(50% C5+), and first Montney ‘C’ test of 1,300 boe/d (19% C5+)

Recent Well Test Results (1) Pipestone Energy Lands

Condensate Yield

1 265 bbl/MMcf

2 215 bbl/MMcf

3 201 bbl/MMcf

3

4 299 bbl/MMcf 12

5 317 bbl/MMcf

7

2 6

6 150 bbl/MMcf

7 143 bbl/MMcf

1

8 111 bbl/MMcf 4

9 8

11

10 5

9 96 bbl/MMcf

10 153 bbl/MMcf

11 40 bbl/MMcf

12 67 bbl/MMcf

- 500 1,000 1,500 2,000 2,500 3,000 3,500

Production (boe/d)

Condensate Raw Gas

Note: Pipestone Energy cautions that short-term test rates are not necessarily indicative of long-term well or reservoir performance or of ultimate recovery.

1. Pipestone Energy wells represent production over the last 24 hours of a production test, with an average test duration of ~6 days. 9Supportive offset well performance

Pipestone Montney operators have demonstrated very strong

natural gas productivity with high condensate gas ratios

Pipestone Montney Very Rich Gas Condensate Historical Well Results

Calendar Day Raw Gas Production (Mcf/d)

10,000

McDaniel Pipestone Raw Gas Type Curve (1)

Offset Well Results (2)

8,000

Based on public disclosure and accessible

test data, wells within this data set have

initial CGRs of 100 – 300+ bbl/MMcf

6,000

4,000

2,000

-

0 4 8 12 16 20 24 28 32 36

Normalized Months

1. Type curve represents the McDaniel VRGC2 Montney B type curve, assuming a 2,500 metre lateral length. Capital costs reflect current internal estimates based on recent drilling and completion activities.

2. Sourced to Geoscout, October 2018. Includes Pipestone Montney wells drilled since 2014 in the “Very Rich Gas Condensate” window (100 – 300 bbl/MMcf IP30 condensate-gas-ratio). 10Attractive type curve economics

Pipestone Montney wells deliver highly competitive half-cycle returns with

forecasted paybacks of ~13 months and IRRs of >95%

Pipestone Very Rich Gas Condensate (Montney B) Type Curve Economics (1)(2)(3)

Volume (Mboe) / CGR (bbl/MMcf) Payback Period (Months)

600 18

Type Curve Inputs 20

15 13

DCET Capital $9.7 MM 10

10

500 Raw Gas EUR (Bcf) 4.2

5

Cond. EUR (Mbbls) 392

-

Hz Length (metres) 2,500 $55 | $1.50 $65 | $1.90 $75 | $2.25

400 Prop. Loading (t/m) WTI (US$/bbl) | AECO ($/GJ)

2.5

IRR (%)

13 Month payout @ US$65 200%

WTI | $1.90 GJ AECO 143%

300 150%

96%

100%

51%

50%

200

-

$55 | $1.50 $65 | $1.90 $75 | $2.25

WTI (US$/bbl) | AECO ($/GJ)

100 NPV10% ($MM)

$15 $13.1

$9.8

- $10

$5.5

0 4 8 12 16 20 24 $5

Months

Total Production Condensate CGR -

$55 | $1.50 $65 | $1.90 $75 | $2.25

1. Pipestone Energy Corp. type curve as assigned by McDaniel & Associates Consultants Ltd. WTI (US$/bbl) | AECO ($/GJ)

2. Single well economics calculated using a flat price deck with no inflation. Utilizes a 0.775 CADUSD FX rate. Operating costs include third party compression, gathering, and processing costs.

3. Type curve represents the McDaniel VRGC2 Montney B type curve, assuming a 2,500 metre lateral length. Capital costs reflect current internal estimates based on recent drilling and completion activities. 11Significant reserves & resource recognition

Pipestone Energy has ~165 MMboe of 2P reserves (47% liquids) and 221 MMboe of

Best Estimate Contingent resource (46% liquids)

Condensate Total

Volume / Oil NGLs Liquids NPV 10% (B-Tax) (1)

(MMboe) (%) (%) (%) ($MM)

PDP Reserves 3 32% 7% 39% $44

PDNP Reserves 11 32% 11% 43% $96

Proved Reserves 79 36% 11% 47% $555

2P Reserves 165 36% 11% 47% $1,170

2C Resources

221 36% 10% 46% $810

(Risked)

~58% of Lands Booked with Reserves and Resources Number of Booked Undeveloped Locations (2)

# of Locations

400 383

19% 350

2P 300

42% 250

Total Sections: 2C

200 172

170

Unbooked 150

100

39%

50

-

2P 2C (Risked)

1. Based on McDaniel reserves and resource evaluations effective August 1, 2018, utilizing the McDaniel July 1, 2018 price deck.

2. Management has identified a total of up to 1,450 potential locations. 12Decades of drilling inventory

Up to 1,450 potential remaining wells in inventory, providing decades of condensate-rich

development potential and free cash flow generation for investors

Future Development Locations Multiple Layers Within the Montney at Pipestone

# of Montney Well Locations

2%

1,600

12%

Dev.

1,400 Total 2P

Locations: 2C

26%

60% 1,450

Unbooked

1,200

1,000 All current reserves and resource

870

bookings only include the Montney

‘B’ and ‘C’; testing a Lower

Montney well in Q4 2018

800 Up to

1,450

581

600

400 383

581

198

200

172 172

26

-

Developed Dev. + 2P Dev. + 2P + 2C Future Booking Total Potential

Locations Locations Potential Locations

Note: See “Advisories – Drilling Locations” for more details. 13Processing and egress solutions

Pipestone Energy has diversified processing and egress solutions in place

Processing Capacity Egress

Tidewater Pipestone Montney Gas Plant Alliance Keyera Wapiti Gas Plant

• Blackbird has firm access to 20 MMcf/d through the • 5 MMcf/d (current)

Tidewater Pipestone Gas Plant beginning in Q3 • 6 MMcf/d (Q3 2019)

2019E, ramping to 30 MMcf/d by 2021E

• Blackbird has the option to acquire up to a 20% TCPL

working interest in the facility, which would significantly • 3.5 MMcf/d (Q3 2019)

reduce processing fees

• 39.5 MMcf/d (Q4 2019)

Keyera Wapiti Gas Plant • 54.5 MMcf/d (Q1 2021)

• Pipestone Oil has firm access to 60 MMcf/d of natural

• 79.5 MMcf/d (Q2 2021)

gas gathering, compression and processing through

the Keyera Wapiti Gas Plant beginning in Q4 2019E • 94.5 MMcf/d (Q4 2021)

• There is an option to increase to 90 MMcf/d at

Tidewater Natural Gas Storage Facility

Pipestone Oil’s election

• Pipestone Energy will maintain preferred access to the

Tidewater gas storage facility

14Positioned for significant long-term growth

Pipestone Energy has natural gas and egress solutions confirmed to

support >30,000 boe/d by 2022

Sales Gas

(MMcf/d) (1)

150 TCPL

Alliance Pipestone Energy has firm

Tidewater Pipestone Montney Gas Plant access to natural gas

Keyera Wapiti Gas Plant

~33,000 boe/d (2)

processing and egress

125

Tidewater + Keyera + CNRL (Sales Processing solutions to support

Capacity) production of greater than

30,000 boe/d by 2022

100

~24,000 boe/d (2)

(Sales Processing

Capacity)

The McDaniel reserves and

75 Keyera option to resource reports supports

Preferential access to increase to

Tidewater gas storage facility 79.2 MMcf/d until 2029

production potential of

greater than 50,000 boe/d

50

52.8 MMcf/d (Keyera)

TransCanada / Alliance are

25 25.2 MMcf/d (Tidewater)

open for new natural gas

16.8 MMcf/d (Tidewater)

takeaway contracts past

21.0 MMcf/d (Tidewater)

5.3 MMcf/d (CNRL) 2021, and storage can be

utilized as an alternative for

-

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 excess production

2018 2019 2020 2021 2022

Note: Raw gas processing volumes are 6 MMcf/d for CNRL; 20 MMcf/d at Tidewater beginning Q3 2019, increasing to 30 MMcf/d in Q1 2021; and 60 MMcf/d at Keyera beginning Q4 2019, with the option to

increase to 90 MMcf/d until 2029 beginning in Q2 2021.

1. CNRL, Tidewater, and Keyera processing volumes converted to sales gas assuming shrinkage of 12.5%, 16%, and 12%, respectively.

2. Estimated operating netback of ~$28.00/boe, calculating using US$65/bbl WTI, $1.90/GJ ($2.00/Mcf) AECO, 0.775 CADUSD. 15Pipestone Energy Corp.

Strategic combination of two neighbouring, contiguous Pipestone Montney assets

under a single well-capitalized, high growth company

+ Dominant pure-play Pipestone Montney company in the “sweet spot” of the condensate fairway

+ Fully funded to realize peer-leading growth profile

+ Superior economics

+ Positioned for significant long-term growth

+ Decades of drilling inventory

= both set of insiders and major shareholders fully support the transaction

The Board and management of Blackbird recommend Blackbird

shareholders vote in favour of the transaction

16Capitalized to grow to >14,000 boe/d

The planned capital expenditures are fully funded by the Financings and

forecast cash flow from operations

Capitalization (Prior to the Proposed 10:1 Share Consolidation)

Common Shares Outstanding 1.9 billion

Listed Warrants Outstanding 175.2 million

Estimated Adjusted Net Debt (Cash) as at September 30, 2018 (1) $(60) million

Preliminary Guidance

Capital Expenditures:

Q4 2018E $110-120 million

2019E $110-140 million

Forecast Production and Netback:

Average 2019E 3,000 to 3,500 boe/d

Exit 2019E 14,000 to 16,000 boe/d

Exit 2019E Estimated Liquids Weighting ~35-40% Condensate + ~5-10% NGLs

Operating Netback (2) ~$28/boe

1. Includes estimated transaction costs and proceeds from the Financings. Adjusted net debt, as referred to throughout this presentation is a non-IFRS measure. See “Non-IFRS Measures” for more

details.

2. Flat US$65/bbl WTI, C$1.90/GJ ($2.00/Mcf) AECO, 0.775 CADUSD. 17Advisories

Forward-Looking Statements

In the interest of providing shareholders of Blackbird and potential investors information regarding Blackbird, Pipestone Oil and Pipestone Energy (the combined company proposed by the announced strategic

combination of Blackbird and Pipestone Oil (the “Transaction”)), this presentation contains certain information and statements (“forward-looking statements”) that constitute forward-looking information within the meaning

of applicable Canadian securities laws. Forward-looking statements relate to future results or events, are based upon internal plans, intentions, expectations and beliefs, and are subject to risks and uncertainties that may

cause actual results or events to differ materially from those indicated or suggested therein. All statements other than statements of current or historical fact constitute forward-looking statements. Forward-looking

statements are typically, but not always, identified by words such as “anticipate”, “estimate”, “expect”, “intend”, “forecast”, “continue”, “propose”, “may”, “will”, “should”, “believe”, “plan”, “target”, “objective”, “project”,

“potential” and similar or other expressions indicating or suggesting future results or events.

Forward-looking statements are not promises of future outcomes. There is no assurance that the results or events indicated or suggested by the forward-looking statements, or the plans, intentions, expectations or

beliefs contained therein or upon which they are based, are correct or will in fact occur or be realized (or if they do, what benefits Pipestone Energy may derive therefrom).

In particular, but without limiting the foregoing, this presentation contains forward-looking statements pertaining to: expected timing to complete the Transaction; anticipated strategic, financial and operational benefits of

the Transaction, including, but not limited to, 2019E sales processing capacity and production, estimated capital expenditures, and forecast cash flow from operations; operating netbacks, Pipestone Energy’s IRR’s;

preliminary guidance; and Pipestone Energy’s proposed drilling locations.

With respect to the forward-looking statements contained in this presentation, Blackbird and Pipestone Oil have assessed material factors and made assumptions regarding, among other things: future commodity prices

and currency exchange rates, including consistency of future oil, natural gas liquids (NGLs) and natural gas prices with current commodity price forecasts; the ability to integrate Blackbird’s and Pipestone Oil’s businesses

and operations and realize financial, operational and other synergies from the Transaction; the ability to obtain regulatory approvals and meet other closing conditions for the Transaction; Pipestone Energy’s continued

ability to obtain qualified staff and equipment in a timely and cost-efficient manner; the predictability of future results based on past and current experience; the predictability and consistency of the legislative and

regulatory regime governing royalties, taxes, environmental matters and oil and gas operations, both provincially and federally; Pipestone Energy’s ability to successfully market its production of oil, NGLs and natural gas;

the timing and success of drilling and completion activities (and the extent to which the results thereof meet expectations); Pipestone Energy’s future production levels and amount of future capital investment, and their

consistency with Pipestone Energy’s current development plans and budget; future capital expenditure requirements and the sufficiency thereof to achieve Pipestone Energy’s objectives; the successful application of

drilling and completion technology and processes; the applicability of new technologies for recovery and production of Pipestone Energy’s reserves and other resources, and their ability to improve capital and operational

efficiencies in the future; the recoverability of Pipestone Energy's reserves and other resources; Pipestone Energy’s ability to economically produce oil and gas from its properties and the timing and cost to do so; the

performance of both new and existing wells; future cash flows from production; future sources of funding for Pipestone Energy’s capital program, and its ability to obtain external financing when required and on

acceptable terms; future debt levels; geological and engineering estimates in respect of Pipestone Energy’s reserves and other resources; the accuracy of geological and geophysical data and the interpretation thereof;

the geography of the areas in which Pipestone Energy conducts exploration and development activities; the timely receipt of required regulatory approvals; the access, economic, regulatory and physical limitations to

which Pipestone Energy may be subject from time to time; and the impact of industry competition.

Information and statements regarding Pipestone Energy’s reserves and resources also are forward-looking statements, as they involve the implied assessment, based on certain estimates and assumptions, that the

reserves and resources exist in the quantities predicted or estimated and can be profitably produced in the future. In addition, with respect to the type curves and test rates, there is no certainty that future wells will

generate results to match type curves or test rates presented herein.

The forward-looking statements contained herein reflect management's current views, but the assessments and assumptions upon which they are based may prove to be incorrect. Although Blackbird and Pipestone Oil

each believe that its underlying assessments and assumptions are reasonable based on currently available information, undue reliance should not be placed on forward-looking statements, which are inherently uncertain,

depend upon the accuracy of such assessments and assumptions, and are subject to known and unknown risks, uncertainties and other factors, both general and specific, many of which are beyond Pipestone Energy’s

control, that may cause actual results or events to differ materially from those indicated or suggested in the forward-looking statements. Such risks and uncertainties include, but are not limited to, volatility in market prices

and demand for oil, NGLs and natural gas and hedging activities related thereto; the ability to obtain approvals for the Transaction; the ability to successfully integrate Blackbird’s and Pipestone Oil’s businesses and

operations; general economic, business and industry conditions; variance of Pipestone Energy’s actual capital costs, operating costs and economic returns from those anticipated; the ability to find, develop or acquire

additional reserves and the availability of the capital or financing necessary to do so on satisfactory terms; and risks related to the exploration, development and production of oil and natural gas reserves and resources.

Additional risks, uncertainties and other factors are discussed in Blackbird’s current annual information form, annual and interim management’s discussion and analysis, and other documents filed by it from time to time

with securities regulatory authorities in Canada, copies of which are available electronically on SEDAR at www.sedar.com.

The forward-looking statements contained in this presentation are made as of the date hereof and Blackbird and Pipestone Oil assume no obligation to update or revise any forward-looking statements, whether as a

result of new information, future events or otherwise, unless required by applicable securities laws. All forward-looking statements herein are expressly qualified by this advisory.

18Advisories (Continued)

Non-IFRS Measures

This presentation contains references to “free cash flow”, “operating netback”, “IRR” or “internal rate of return”, “adjusted net debt” and “NOI” or “net operating income”, which are terms commonly used in the oil and

natural gas industry but without any standardized meaning or method of calculation prescribed by International Financial Reporting Standards (“IFRS”) or applicable law. Accordingly, Blackbird’s and Pipestone Oil’s

determination of these metrics may not be comparable to similar measures presented by other issuers.

“Free cash flow” should not be considered an alternative to, or more meaningful than, cash flow – operating activities as determined in accordance with IFRS, as an indicator of financial performance. Free cash flow is

presented to assist management and investors in analyzing operating performance by the business in the stated period. Free cash flow equals cash flow – operating activities plus change in non-cash working capital less

capital expenditures.

“IRR” or “internal rate of return” is a rate of return measure used to compare the profitability of an investment and represents the discount rate at which the net present value of costs equals the net present value of the

benefits. The higher a project’s IRR, the more desirable the project.

“Operating netback” equals the total of petroleum and natural gas sales less royalties, operating expenses and transportation and processing expenses calculated on a per boe basis. Operating netback is utilized by

Pipestone Energy to analyze the performance of its oil and natural gas assets at the field-level by isolating the impact of changes in production volumes.

“Adjusted net debt” is a non-GAAP measure that equals total debt less current assets plus current liabilities (excluding any amounts included in total debt), and includes transaction costs and the Financings. Total debt is

calculated as long-term debt, long-term debt due within one year and short-term debt. Net debt is considered to be a useful measure in assisting management and investors to evaluate Pipestone Energy’s financial

strength.

“NOI” or “net operating income” represents revenue net of royalties and operating, sales and transportation expenses. Management believes that net operating income is a useful supplemental measure to analyze

operating performance and provides an indication of the results generated by Pipestone Energy’s principal business activities prior to the consideration of other income and expenses.

Third Party Information

This presentation contains statistical data, market research and industry forecasts that were obtained from government or other industry publications and reports or are based on estimates derived therefrom and

management’s knowledge of, and experience in, the markets in which Blackbird and Pipestone Oil operate. Government and industry publications and reports generally indicate that they have obtained information from

sources believed to be reliable, but do not guarantee its accuracy or completeness. Often, such information is provided subject to specific terms and conditions limiting the liability of the provider, disclaiming any

responsibility therefor, and/or limiting a third party’s ability to rely thereon. No author of any such publication or report has consulted for or advised or counselled Blackbird or Pipestone Oil or is in any way associated with

the companies. Further, organizations that are proponents of the Canadian oil and gas industry may present information in a manner that is different from, and potentially more favourable to the industry than, information

presented by an entirely independent source. Actual outcomes may vary materially from those forecast in such reports or publications, and the prospect for material variation can be expected to increase as the length of

the forecast period increases. Market and industry data is subject to variation and cannot be verified due to limits on the availability and reliability of data inputs, the voluntary nature of the data gathering process, and

other limitations and uncertainties inherent in any survey. Blackbird and Pipestone Oil have not verified any data from third party sources referred to in this presentation or assessed any underlying assumptions relied

upon by such sources.

Reserves and Resources Disclosure

General

Information in this presentation regarding Blackbird’s and Pipestone Oil’s estimated reserves and resources, net present value of related future net revenue, and production is expressed on a net Blackbird and Pipestone

Oil (as applicable) interest basis, being their respective working interest (operating and non-operating) share after deduction of royalty obligations plus any royalty interest. Estimates of future net revenue are after

deduction of forecasted royalties, operating costs, estimated well abandonment and reclamation costs and estimated future development costs, but without any provision for interest costs, debt service charges or general

and administrative expenses.

Reserves and resources volumes attributed to Blackbird’s and Pipestone Oil’s properties and related future net revenue are estimates only. There is no assurance that the estimated reserves and resources can or will be

recovered or that estimated future net revenues will be realized. Actual reserves and resources may be greater or less than those estimated, and the difference may be material. Similarly, estimated net present values of

related future net revenue attributed to reserves and resources do not represent fair market value of those reserves or resources (whether or not risked). There is no assurance that the forecast prices and cost

assumptions applied in evaluating the reserves and estimating related future net revenue will be attained, and variances between actual and forecast prices and costs may be material. An estimate of risked NPV of future

net revenue of contingent resources is preliminary in nature and is provided to assist the reader in reaching an opinion on the merit and likelihood of Blackbird or Pipestone Oil proceeding with the required investment. It

includes contingent resources that are considered too uncertain with respect to the chance of development to be classified as reserves. There is uncertainty that the risked NPV of future net revenue will be realized.

The determination of oil and gas reserves and resources involves estimating subsurface accumulations of oil, condensate NGLs and natural gas that cannot be exactly measured. The preparation of estimates is subject

to an inherent degree of associated risk and uncertainty, including factors that are beyond Blackbird’s or Pipestone Oil’s, as applicable, control. The estimation and classification of reserves and resources is a complex

process involving the application of professional judgment combined with geological and engineering knowledge to assess whether specific classification criteria have been satisfied. It requires significant judgments based

on available geological, geophysical, engineering, and economic data as well as forecasts of commodity prices and anticipated costs. As circumstances change and additional data becomes available, whether through

the results of drilling, testing and production or from economic factors such as changes in product prices or development and production costs, reserves estimates also change. Revisions may be positive or negative.

19Advisories (Continued)

Reserves and Resources Disclosure

Blackbird

Figures provided in this presentation as to Blackbird’s reserves volumes and net present value of future net revenue attributable thereto are estimates of such volumes and values as at July 31, 2018 based on an

evaluation by McDaniel & Associates Consultants Ltd. (“McDaniel”), Blackbird's independent qualified reserves evaluator. Figures provides in this presentation as to Blackbird’s resources volumes and net present value

of future net revenue attributable thereto are estimates of such volumes and values as at May 1, 2018 based on an evaluation by McDaniel. McDaniel’s evaluations were in accordance with National Instrument 51-101

Standards of Disclosure for Oil and Gas Activities (“NI 51-101”) and, pursuant thereto, the Canadian Oil and Gas Evaluation Handbook (“COGE Handbook”).

Certain contingencies currently prevent the classification of Blackbird’s contingent resources as reserves. The 221.3 MMboe of 2C Resources of the combined company disclosed in this presentation include Blackbird’s

Best Estimate Development Pending Contingent Resources of 135.9 MMboe in the Pipestone / Elmworth Montney area in Alberta. The corresponding estimate of risked before tax NPV of future net revenue for Best

Estimate Development Pending Contingent Resources, using a discount rate of 10% per year, is $587.3 million. The product types associated with Blackbird’s contingent resources include crude oil, natural gas,

condensate, and NGLs. Contingent resources are defined in the COGE Handbook as those quantities of petroleum estimated, as of a given date, to be potentially recoverable from known accumulations using

established technology or technology under development, but are not currently considered to be commercially recoverable due to one or more contingencies. Contingencies may include factors such as economic, legal,

environmental, political and regulatory matters or a lack of markets. It is also appropriate to classify as contingent resources the estimated discovered recoverable quantities associated with a project in the early

evaluation stage.

Pursuant to the COGE Handbook, there are three classification levels of contingent resource estimates: Low Estimate, Best Estimate and High Estimate. Best estimate is considered to be the best estimate of the quantity

that will be actually recovered. It is equally likely that the actual remaining quantities recovered will be greater or less than the best estimate. If probabilistic methods are used, there should be at least a 50% probability

that the quantities actually recovered will equal or exceed the best estimate. Pursuant to the COGE Handbook, contingent resources are sub-classified based on project maturity. All of Blackbird’s contingent resources

disclosed in this presentation have been sub-classified as “Development Pending”, which applies in circumstances where resolution of the final conditions for development is being actively pursued and indicates a

relatively high chance of development versus the other sub-classifications.

All of Blackbird’s contingent resources have been risked using an 80% chance of development. For contingent resources, the chance of development is the estimated probability of a project being commercially viable,

and development proceeding in a timely fashion. Determining chance of development requires consideration of each applicable contingency and quantifying them so as to arrive at an overall development risk factor. In

quantifying the chance of development, the factors that were assessed quantitatively to be less than one in the development risk calculation included the economic status, the project evaluation scenario status, and the

development time frame. The chance of development multiplied by the unrisked resource volume estimate yields the risked resource volume estimate. As many of these factors have a wide range of uncertainty and are

difficult to quantify, the chance of development is an uncertain value that should be used with caution.

Continuous development through multi-year exploration and development programs and significant levels of future capital expenditures are required in order for additional resources to be recovered in the future. The

principal risks that would inhibit the recovery of additional reserves relate to the potential for variations in the quality of the Montney formation where minimal well data currently exists, access to the capital required to

develop the resources, low commodity prices that would curtail the economics of development and the future performance of wells, regulatory approvals, access to required services at an appropriate cost, and the

effectiveness of well fracturing technology and applications. For contingent resources to be converted to reserves, Blackbird must ascertain commercial production rates, then develop firm plans, including with respect to

timing, infrastructure and the commitment of capital. Confirmation of commercial productivity is generally required before Blackbird can prepare firm development plans and commit required capital for the development of

the contingent resources. Additional contingencies relate to the current lack of infrastructure required to develop the resources in a relatively quick time frame. As continued delineation occurs, some resources currently

classified as Contingent Resources are expected to be re-classified to reserves.

The estimated cost reflected in McDaniel’s evaluation of Blackbird’s contingent resources to bring on commercial production from the Best Estimate Development Pending contingent resources for all four product types is

approximately $1,833 million (when discounted at 10%, the estimated cost is approximately $668 million). The expected timeline to bring these resources on production is between the years 2021 and 2042. Best Estimate

Development Pending Contingent Resources are expected to be recovered using the same technology of horizontal drilling and multi-stage fracturing that Blackbird has already proven to be effective in its

Pipestone/Elmworth Montney play.

The estimates of contingent resources provided herein are estimates only and there is no guarantee that the estimated contingent resources will be recovered. Actual contingent resources may be greater or less than the

estimates provided in this presentation, and the differences may be material. The estimates of contingent resources and future net revenue for individual properties may not reflect the same confidence level as estimates

of contingent resources and future net revenue for all properties, due to the effects of aggregation. There is no assurance that the forecast price and cost assumptions applied by McDaniel in evaluating Blackbird’s

contingent resources will be attained and variances could be material. There is uncertainty that it will be commercially viable to produce any portion of the contingent resources described herein, or that Blackbird will

produce any portion of the volumes currently classified as contingent resources.

20Advisories (Continued)

Reserves and Resources Disclosure

Pipestone

Unless otherwise indicated: (i) reserves and resources estimates have been prepared by McDaniels, Pipestone Oil’s independent qualified reserves evaluators in accordance with the COGE Handbook, have an effective

date of July 1, 2018 and represent Pipestone Oil’s working interest share; (ii) drilling locations have been derived from reports by McDaniels; and (iii) projected and historical production volumes provided represent

Pipestone Oil’s working interest share before royalties.

Certain contingencies currently prevent the classification of Pipestone Oil’s contingent resources as reserves. The 221.3 MMboe of the combined company’s 2C Resources disclosed in this presentation include Pipestone

Oil’s Risked Best Estimate Development Pending Contingent Resources of 85.4 MMboe in the Pipestone / Elmworth Montney area. The corresponding estimate of risked before tax NPV of future net revenue for Best

Estimate Development Pending Contingent Resources, using a discount rate of 10% per year, is $232.0 million. The product types associated with Pipestone Oil’s contingent resources include crude oil, natural gas,

condensate, and NGLs.

All of Pipestone Oil’s contingent resources disclosed in this presentation have been sub-classified as “Development Pending”, which applies in circumstances where resolution of the final conditions for development is

being actively pursued and indicates a relatively high chance of development versus the other sub-classifications.

All of Pipestone Oil’s contingent resources have been risked using an 80% chance of development. In quantifying the chance of development, the factors that were assessed quantitatively to be less than one in the

development risk calculation included the economic status, the project evaluation scenario status, and the development time frame. The chance of development multiplied by the unrisked resource volume estimate yields

the risked resource volume estimate. As many of these factors have a wide range of uncertainty and are difficult to quantify, the chance of development is an uncertain value that should be used with caution.

Continuous development through multi-year exploration and development programs and significant levels of future capital expenditures are required in order for additional resources to be recovered in the future. The

principal risks that would inhibit the recovery of additional reserves relate to the potential for variations in the quality of the Montney formation where minimal well data currently exists, access to the capital required to

develop the resources, low commodity prices that would curtail the economics of development and the future performance of wells, regulatory approvals, access to required services at an appropriate cost, and the

effectiveness of well fracturing technology and applications. For contingent resources to be converted to reserves, Pipestone Oil must ascertain commercial production rates, then develop firm plans, including with

respect to timing, infrastructure and the commitment of capital. Confirmation of commercial productivity is generally required before Pipestone Oil can prepare firm development plans and commit required capital for the

development of the contingent resources. Additional contingencies relate to the current lack of infrastructure required to develop the resources in a relatively quick time frame. As continued delineation occurs, some

resources currently classified as contingent resources are expected to be re-classified to reserves.

The estimated cost reflected in McDaniel’s evaluation of Pipestone Oil’s contingent resources to bring on commercial production from the Risked Best Estimate Development Pending Contingent Resources for all four

product types is approximately $1,126.2 million (when discounted at 10%, the estimated cost is approximately $267.9 million). The expected timeline to bring these resources on production is between the years 2027 and

2040 (in accordance with a pre-development study). Best Estimate Development Pending Contingent Resources are expected to be recovered using the same technology of horizontal drilling and multi-stage fracturing

that Pipestone Oil has already proven to be effective in its Pipestone/Elmworth Montney play.

The estimates of contingent resources provided herein are estimates only and there is no guarantee that the estimated contingent resources will be recovered. Actual contingent resources may be greater or less than the

estimates provided in this presentation, and the differences may be material. The estimates of contingent resources and future net revenue for individual properties may not reflect the same confidence level as estimates

of contingent resources and future net revenue for all properties, due to the effects of aggregation. There is no assurance that the forecast price and cost assumptions applied by McDaniel in evaluating Pipestone Oil’s

contingent resources will be attained and variances could be material. There is uncertainty that it will be commercially viable to produce any portion of the contingent resources described herein, or that Pipestone Oil will

produce any portion of the volumes currently classified as contingent resources.

Initial Production Rates and Short-Term Test Rates

This presentation includes disclosure on initial production (IP) rates for certain wells over a 30-day (IP30), measurement period. It also discloses test rates of production for certain wells over short periods of time, which

are preliminary and not determinative of the rates at which those or any other wells will commence production and thereafter decline. Initial production rates and short-term test rates are not necessarily indicative of long-

term well or reservoir performance or of ultimate recovery. Although such rates are useful in confirming the presence of hydrocarbons, they are preliminary in nature, are subject to a high degree of predictive uncertainty

as a result of limited data availability, and may not be representative of stabilized on-stream production rates.

Production over a longer period will also experience natural decline rates, which can be high in the Montney play and may not be consistent over the longer term with the decline experienced over an initial production

period. Initial production or test rates may also include recovered “load” fluids used in well completion stimulation operations. Actual results will differ from those realized during an initial production period or short-term test

period, and the difference may be material.

21Advisories (Continued)

Drilling Locations

This presentation discloses future development drilling locations, including future booking potential and total risked locations. Drilling locations refers to Pipestone Energy’s total proved, probable and risked contingent

(best estimate) locations, which are derived from reports prepared by McDaniel. Proved locations and probable locations account for drilling locations in Pipestone Energy’s inventory that have associated proved and/or

probable reserves. 2C locations account for drilling locations in Pipestone Energy’s inventory that have associated 2C resources. Future booking potentials (or unbooked locations) are internal estimates based on

Pipestone Energy’s prospective acreage and an assumption as to the number of wells that can be drilled based on industry practice and internal review. Of the 1,450 potential drilling locations identified in this press

release, there are up to 870 potential unbooked locations. Unbooked locations do not have attributed reserves or resources. Unbooked locations have specifically been identified by management as an estimation of

Pipestone Energy’s multi-year drilling activities based on evaluation of applicable geologic, seismic, engineering, production and reserves data on prospective acreage and geologic formations. The drilling locations on

which we actually drill wells will ultimately depend upon the availability of capital, regulatory approvals, seasonal restrictions, oil and natural gas prices, costs, actual drilling results and other factors.

Oil and Gas Measures

Barrels of Oil Equivalent – This presentation discloses certain production information on a barrels of oil equivalent (“boe”) basis with natural gas converted to barrels of oil equivalent using a conversion factor of six

thousand cubic feet of gas (mcf) to one barrel (bbl) of oil (6 mcf:1 bbl). Condensate and other NGLs are converted to boe at a ratio of 1 bbl:1 bbl. Boe may be misleading, particularly if used in isolation. A boe conversion

ratio of 6 mcf:1 bbl is based roughly on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at Blackbird’s and Pipestone Oil’s sales point. Although

the 6:1 conversion ratio is an industry-accepted norm, it is not reflective of price or market value differentials between product types. Based on current commodity prices, the value ratio between crude oil, NGLs and

natural gas is significantly different from the 6:1 energy equivalency ratio. Accordingly, using a conversion ratio of 6 mcf:1 bbl may be misleading as an indication of value.

CGR - References herein to “CGR” mean condensate/gas ratio and is expressed as a volume of condensate and NGLs (expressed in barrels) per million cubic feet (mmcf) of natural gas.

This document includes estimates of net pay thickness. The estimates were prepared internally. The risks and uncertainties associated with recovery of resources include, but are not limited to: that Pipestone Energy

may encounter unexpected drilling results; the occurrence of unexpected events in the exploration for, and the operation and development of, oil and gas; delays in anticipated timing of drilling and completion of wells;

geological, technical, drilling and processing problems; and other difficulties in producing petroleum reserves

Notice to United States Readers

The petroleum and natural gas reserves contained in this news release have generally been prepared in accordance with Canadian disclosure standards, which are not comparable in all respects to United States or other

foreign disclosure standards. For example, the United States Securities and Exchange Commission (the "SEC") requires oil and gas issuers, in their filings with the SEC, to disclose only "proved reserves", but permits the

optional disclosure of "probable reserves" and "possible reserves" (each as defined in SEC rules). Canadian securities laws require oil and gas issuers disclose their reserves in accordance with NI 51-101, which requires

disclosure of not only "proved reserves" but also "probable reserves" and permits the optional disclosure of "possible reserves". Additionally, NI 51-101 defines "proved reserves", "probable reserves" and "possible

reserves" differently from the SEC rules. Accordingly, proved, probable and possible reserves disclosed in this news release may not be comparable to United States standards. Probable reserves are higher risk and are

generally believed to be less likely to be accurately estimated or recovered than proved reserves. Possible reserves are higher risk than probable reserves and are generally believed to be less likely to be accurately

estimated or recovered than probable reserves.

In addition, under Canadian disclosure requirements and industry practice, reserves and production are reported using gross volumes, which are volumes prior to deduction of royalty and similar payments. The SEC rules

require reserves and production to be presented using net volumes, after deduction of applicable royalties and similar payments.

Pipestone Energy advises investors that although contingent resources are recognized by Canadian securities regulations under NI-51-101, the SEC does not recognize this term. Consequently, this news release

contains disclosure regarding resources that a U.S. company would not be permitted to include in its filings with the SEC. As a result, the disclosure regarding Pipestone Energy’s properties is materially different than

disclosure provided by U.S. companies in their filings with the SEC. Investors are cautioned not to assume that any part or all of any resource will ever be converted into a reserve.

All amounts in this news release are stated in Canadian dollars unless otherwise specified.

22Advisories (Continued)

Analogous Information

Certain information in this presentation may constitute “analogous information” within the meaning of NI 51-101, including information relating to areas, wells or operations that are in geographical proximity to or believed

to be on-trend with lands held by Pipestone Energy and production information in respect of wells that are believed to be on trend with Pipestone Energy’s properties. Such information has been obtained from

governmental or other public sources, regulatory agencies or other industry participants that are independent of Pipestone Energy. Pipestone Energy does not, though, know whether any such information contained

herein that constitutes “analogous information” was prepared in accordance with the COGE Handbook or by a qualified reserves evaluator or auditor under NI 51-101, as applicable, and cannot verify its accuracy. While

believed to be reliable, third party data relied upon by Pipestone Energy may be in error.

Management believes such information may be relevant to Pipestone Energy’s efforts to understand and predict reservoir characteristics of properties in which Pipestone Energy may hold or intend to acquire an interest,

and it is presented to help demonstrate the basis for Pipestone Energy's business plans and strategies. There is, however, no assurance that the qualities, characteristics or results suggested by or inferred from

analogous information are or will be similar to or otherwise representative of the qualities or characteristics of properties in which Pipestone Energy has or intends to acquire an interest or the results that Pipestone

Energy may achieve or realize from any operations thereon. Such information is not, and should not be construed or relied upon as, an estimate or predictor of resource potential or future production levels.

TSX Venture Exchange Disclaimer

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of the information contained

in this presentation.

23You can also read