Risk & Reward - e-fundresearch.com

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Risk & Reward

Research and investment strategies

#01

1st issue 2022

Multi-period portfolio selection:

4 a practical simulation-based

framework

Interview: “Simulation has

13 been a focus for me over

much of my career.”

Managing climate risk –

15 a 21st century approach for

commercial real estate

investors

Optimized sampling: ESG

21 integration the smart way

An innovative approach to

26 performance attribution in

fixed income factor portfolios

Earnings conference call

33 tone and stock returns:

evidence across the globe

This magazine is not intended for members of the public or retail investors. Full audience information is available inside the front cover.

Risk & Reward #01/2022

Multi-period portfolio selection: a practical simulation-based

4

framework

Kenneth Blay, Anish Ghosh, Harry Markowitz, Nicholas Savoulides and Qi Zheng

Our simulation-based portfolio selection approach addresses three requirements

for practical multi-period portfolio selection solutions: (1) effective duration

management, (2) incorporation of real-world asset dynamics and (3) consideration

of investment frictions and illiquidity.

“Simulation has been a focus for me over much of my career.”

13

Interview with Harry Markowitz

In this exclusive interview, founding father of modern portfolio theory, 1990

Nobel Laureate and co-author of our feature article, Harry Markowitz, discusses

his work with Invesco on multi-period portfolio selection.

Managing climate risk – a 21st century approach for commercial

15

real estate investors

Louis Wright and Zachary Marschik

With climate risk accelerating around the world, real estate investors need to

consider it’s impacts on their strategies. Learn how we approach these growing

challenges at Invesco Real Estate.

Optimized sampling: ESG integration the smart way

21

Georg Elsaesser, Dr. Martin Kolrep and Michael Rosentritt

Optimized sampling helps preserve the intended portfolio characteristics after

ESG integration, reduces tracking error and limits transaction costs.

An innovative approach to performance attribution in fixed

26

income factor portfolios

Jay Raol, Ph.D., Benton Chambers, Amritpal Sidhu and Bin Yang

Attribution analysis can be adapted for single-factor, multi-factor and factor

target portfolio strategies – three examples that correspond to the three stages

of our factor investment process for fixed income.

Earnings conference call tone and stock returns: evidence

33

across the globe

Tarun Gupta, Ph.D., and Yifei Shea, Ph.D.

Based on evidence from five investment regions, we show how the tone on

display during earnings calls can help predict stock returns.

Important information: The publication is intended only for Professional Clients, Qualified Clients/ Sophisticated investors and Qualified Investors

(as defined in the important information at the end); for Institutional Investors in Australia; for Professional Investors in Hong Kong; for Institutional

Investors and/or Accredited Investors in Singapore; for certain specific sovereign wealth funds and/or Qualified Domestic Institutional Investors

approved by local regulators only in the People’s Republic of China; for certain specific Qualified Institutions and/or Sophisticated Investors only in

Taiwan; for Qualified Professional Investors in Korea; for certain specific institutional investors in Brunei; for Qualified Institutional Investors and/or

certain specific institutional investors in Thailand; for certain specific institutional investors in Indonesia; for qualified buyers in Philippines for

informational purposes only; for Qualified Institutional Investors, pension funds and distributing companies in Japan; and for Institutional Investors in

the USA. The document is intended only for accredited investors as defined under National Instrument 45-106 in Canada. It is not intended for and

should not be distributed to, or relied upon by, the public or retail investors.

Global editorial committee: Chair: Kevin Lyman and Stephanie Valentine. Jutta Becker, Kenneth Blay, Bailey Buckner, Amanda Clegg, Jessica Cole,

John Feyerer, Ann Ginsburg, Tim Herzig, Kristina Hooper, Paul Jackson, Dr. Martin Kolrep, Damian May, Lisa Nell, Jodi L. Phillips, Dr. Henning Stein,

Scott Wolle.

In this edition of Risk & Reward we provide

you broad insight into Invesco’s research

capabilities. From multi-period portfolio

selection to ESG return optimization, new

applications for attribution analysis to

AI-assisted coverage of earnings calls –

our problem-solving approach is as

comprehensive as it is innovative. And there’s

Marty Flanagan one element that ties it all together: effective

President and CEO quantitative investment management.

of Invesco Ltd.

Our lead article addresses common portfolio construction

issues that a conventional one-period approach cannot solve.

Learn how we make use of computing power to effectively

manage duration, account for illiquidities, and maximize

wealth over multi-period investment horizons. And you won’t

want to miss our interview with Nobel Laureate Harry

Markowitz, co-author of the study and pioneer of modern

portfolio theory.

We’ve also included two articles about ESG, the first of which

looks at commercial real estate, the considerable greenhouse

gas emissions associated with the asset class and the

rebounding impacts of global warming on real estate asset

performance. The second article examines how a well-known

technique from passive management – optimized sampling –

can be used to integrate ESG into a portfolio while matching

the tracking error to the original, non-ESG allocation.

And we explore the topic of attribution analysis for fixed

income. Much more than just a reporting tool, attribution

analysis can help investment professionals comprehend

the many complexities involved in translating theoretical

investment concepts into real-world trading strategies –

to ensure that factor portfolios behave as intended.

Finally, we break down the true relationship between the

tone on display in earnings calls and expected stock

performance. A data mining approach helps separate

the signal from the noise.

We hope you enjoy this latest edition of Risk & Reward!

Best regards,

Marty Flanagan

President and CEO of Invesco Ltd.

Multi-period portfolio

selection: a practical

simulation-based

framework1

By Kenneth Blay, Anish Ghosh, Harry Markowitz, Nicholas Savoulides and Qi Zheng

Since the advent of portfolio theory in 1952,

investment researchers have made notable

advances in optimal portfolio selection. However,

research on multi-period portfolio selection

has been limited in its practical application by

‘the curse of dimensionality’ – the exponential

increase in computational requirements with each

additional state variable. Real-world multi-period

problems include numerous state variables that

make the computation of solutions impractical if

not infeasible. And, while relevant computational,

theoretical and numerical methods have improved

significantly, many important aspects of multi-

period investing still remain unaddressed.

4 Risk & Reward #01/2022 | Multi-period portfolio selection: a practical simulation-based framework

We develop a simulation-based portfolio 1. Solutions must evolve allocations and

selection (SBPS) approach that addresses duration over time to align with expected

three requirements for practical multi- cash flows

period portfolio selection solutions: The long investment horizons and

expected cash inflows and outflows of

1. Effective duration management multi-period investing must be reflected in

the evolution of allocations and duration

2. Incorporation of real-world asset profiles across the investment horizon.

dynamics

For example, consider the risk-free asset,

3. Consideration of investment frictions which in a single-period context is usually

and illiquidity cash or US Treasury bills, due to their low

volatility. Over long investment horizons,

We start with an analytical model that these assets are not ‘risk free’ as they

provides intuition and offers some expose investors to meaningful

guiding principles on how allocations uncertainty.

and duration should evolve across a

multi-period investment horizon. We Figure 1 illustrates this, presenting 20

then unveil our SBPS approach and simulated paths for each of three duration

demonstrate how it provides solutions approaches. Of the three options, a 10-year

for common investor objectives that are zero-coupon US Treasury bond has the

intuitive and flexible, and which satisfy lowest risk if held until maturity, despite

our requirements for practical multi- exhibiting material volatility across the

period solutions. investment horizon.

Single-period versus multi-period This demonstrates how essential effective

portfolio selection duration management is to multi-period

A key distinction between single-period solutions. In cases like this, hold-to-

and multi-period portfolio selection is the maturity investments can be the most

consideration of intermediate actions efficient assets to employ. In more complex

within an investment horizon that extends cases, time-varying combinations of short

over many periods. In the single-period and long-duration bond funds may be used

setting, an investor decides how to invest to achieve the desired outcome.

at the beginning of the period and then

waits until the end of the period to assess 2. Solutions must consider real-world asset

the outcome. In practice, however, dynamics

investing is rarely so straightforward. Asset pricing dynamics may exhibit unique

Pension fund managers, retirement characteristics over long horizons, which

investors and other long-term investors can materially impact the performance of

Duration management should fund their portfolios over time and often theoretical solutions when implemented in

be a key consideration for long pursue many objectives across a multi- the real world. For example, equity

horizon optimizations in the stage investment horizon, necessitating a valuations exhibit mean-reverting

variety of intermediate steps. tendencies that result in negative

presence of inflows and outflows.

autocorrelation over longer horizons.

Multi-period portfolio selection must Additionally, fixed income returns may be

therefore consider these intermediate skewed in a low rate environment where

events while seeking to determine rates have limitations as to how low they

efficient, time-varying portfolio allocations can go. For these and other reasons, a

across the investment horizon. log-normal model of asset price dynamics

may produce unrealistic – if not utterly

Requirements for multi-period portfolio implausible – results.

selection

In practice, three requirements must be

fulfilled for practical multi-period portfolio

selection solutions:

Figure 1

Twenty simulated paths of USD 1 invested in three different ways

Portfolio balance (LHS) Asset duration (RHS)

Money market fund Duration targeted (10-year): US Treasury bond index fund 10-year zero coupon: US Treasury bond

USD Years USD Years USD Years

1.6 10 1.6 10 1.6 10

8 8 8

1.4 1.4 1.4

6 6 6

1.2 1.2 1.2

4 4 4

1.0 1.0 1.0

2 2 2

0.8 0 0.8 0 0.8 0

0 1 2 3 4 5 6 7 8 9 10 0 1 2 3 4 5 6 7 8 9 10 0 1 2 3 4 5 6 7 8 9 10

Time (years) Time (years) Time (years)

Source: Invesco.

5 Risk & Reward #01/2022 | Multi-period portfolio selection: a practical simulation-based framework

3. Solutions must consider investment 1. Optimal asset allocation through time

frictions and illiquidity Making some simplifying assumptions, we

Real-world portfolios implemented across derive an analytical solution for optimal

multiple periods may be updated for a asset allocation.2 The analytical solution is

variety of reasons. These updates can best understood in a standard accumulation-

include cash inflows, cash outflows, decumulation problem depicted in figure

the purchase, sale or replacement of 2(a); it shows inflows and outflows, and

investments, and portfolio rebalancing. All how the portfolio balance increases and

such intermediate portfolio management decreases over time.

activities can have transaction cost and/or

tax implications. The optimal analytical solution suggests

that, the dollar risk should stay constant

Over the short term, these real-world through time. In a two-asset context, it

elements may only result in negligible implies that the portfolio dollar allocated to

differences in expected outcomes. Over the high risk asset (equity) stays roughly

the long term, however, significant constant through time. This is depicted in

differences between actual and expected figure 2(b) for three different solutions,

outcomes can arise from not adequately depending on the investor’s risk preference.

accounting for their impact. This constant dollar equity allocation gives

rise to a U-shaped glidepath in the

Analytical framework accumulation-decumulation problem.

To provide intuition for the multi-period

portfolio selection problem in the presence 2. Optimal duration management through

of cash flows, we address two central ideas time

analytically: Similarly, we obtained an analytical solution

for optimal duration. It is driven by four

1) Optimal asset allocation through time components, as shown in figure 3: expected

2) Optimal duration management through cash flows, bonds-equity correlation,

time expected yield curve changes, and yield

curve slope.

To this end, we develop an analytical

solution to the mean-variance problem in Analytically driven guiding principles

the multi-period context with intermediate To better understand the first order impact

cash flows. Our findings are best understood of cash flows and various other parameters

in a two-asset world in which, at any given on allocation and duration decisions,

time, the investor has access to an equity we introduce an example: a standard

asset and a government bond with accumulation-decumulation problem on a

arbitrary duration. shorter timescale. We assume an investor

with a 10-year investment horizon starting

Figure 2

Stylized accumulation-decumulation problem

a) Cash flows and portfolio b) Allocation of portfolio balance for low, medium and high risk solutions

balance

Inflows Portfolio balance Bond Equity

Outflows

Low-risk Medium-risk High-risk

Portfolio balance Portfolio balance Portfolio balance Portfolio balance

0 1 2 3 4 5 6 7 8 9 10 0 1 2 3 4 5 6 7 8 9 10 0 1 2 3 4 5 6 7 8 9 10 0 1 2 3 4 5 6 7 8 9 10

Time (years) Time (years) Time (years) Time (years)

Source: Invesco.

Figure 3

Components driving optimal duration and their directional impact

Duration = Magnitude and timing + Correlation with equity + Yield curve drift + Yield curve slope

of cash flows

Inflows (+) Positive (–) Increasing yields (–) Positive (+)

Outflows (–) Negative (+) Decreasing yields (+) Negative (–)

Source: Invesco.

6 Risk & Reward #01/2022 | Multi-period portfolio selection: a practical simulation-based framework

with USD 1,000 of initial capital, yearly that the instantaneous yield for the bond

inflows (contributions) of USD 500 for the asset starts at 2% with no drift and exhibits

first five years and outflows (withdrawals) an annualized volatility of 1%.

of USD 500 for the last five years. The

investor seeks to maximize mean terminal Based on the analysis and the example

wealth, subject to a given level of risk as presented, we make the following key

measured by its variance. observations:

Figure 4 presents the optimal equity-bond 1. Allocations should shift to safer (riskier)

allocation and optimal duration profile over allocations as inflows (outflows) occur

time. Specifically, we consider the sensitivity As we have shown, the lowest-risk solution

of the solution to different levels of yield has 100% allocation to bonds and exhibits

curve slope and bond-equity correlation. zero risk. For higher-risk solutions, the

analytical solution suggests an approximately

For this example, we will assume the equity constant dollar allocation to equity through

asset has an average 6% annual return and time. To maintain such a constant dollar

annualized volatility of 15%. We also assume allocation, the investor will allocate

Figure 4

Maximizing mean terminal wealth in the analytical model

Inflows, outflows, and terminal wealth

Inflows Outflows Terminal wealth

Cash flow (USD)

1,500

1,000

500

0

-500

?

-1,000

-1,500

0 1 2 3 4 5 6 7 8 9 10

Time (years)

Asset allocation and duration for nine combinations of asset class correlation (ρ) and yield curve slope

Bond (LHS) Equity (LHS) Bond duration (RHS) Portfolio duration (RHS)

ρ = -0.25 ρ=0 ρ = 0.25

% Years % Years % Years

100 30 100 30 100 30

75 75 75

20 20 20

Slope = 2%

50 50 50

10 10 10

25 25 25

0 0 0 0 0 0

0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9

Time (years) Time (years) Time (years)

% Years % Years % Years

100 30 100 30 100 30

75 75 75

20 20 20

Slope = 0%

50 50 50

10 10 10

25 25 25

0 0 0 0 0 0

0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9

Time (years) Time (years) Time (years)

% Years % Years % Years

100 30 100 30 100 30

75 75 75

20 20 20

Slope = -2%

50 50 50

10 10 10

25 25 25

0 0 0 0 0 0

0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9

Time (years) Time (years) Time (years)

Source: Invesco.

7 Risk & Reward #01/2022 | Multi-period portfolio selection: a practical simulation-based framework

conservatively when the portfolio balance is asset returns may offer guidance on

high and aggressively when it is low. This adjusting portfolio durations.

results in a U-shaped allocation to risk assets

across the investment horizon. As the Simulation-based portfolio selection

probability of running out of money (SBPS)

increases because of extended or higher Traditional approaches to solving multi-

withdrawals, allocations shift back to safer period problems employ dynamic

assets. programing. SPBS builds on much of the

traditional thinking to date on long-horizon

2. Asset duration should match the multi-period investing but diverges in that

investment horizon when there are no it does not employ this technique. Instead,

cash flows we propose a much more flexible

In the case with no yield curve slope and framework that decomposes the multi-

no correlation between bond and equity period problem into three distinct parts:

assets, the duration of the bond mirrors the

remaining investment horizon. This follows 1. The objective function (the investment

from the cash flow contribution of the objective)

duration equation. 2. Simulation

3. Optimization

In this simple example, the desired duration

profile could be implemented with a This provides substantial flexibility in

buy-and-hold strategy using a duration- addressing the central challenges of

matched zero-coupon US Treasury bond. implementing and managing portfolios

Notice the contrast with liability-driven across a multi-period investment horizon.

investing (LDI), which focuses on managing The approach allows us to consider any

funding ratio volatility, seeking to match objective function and incorporate

the portfolio’s overall duration to the real-world asset dynamics and investment

investment horizon and leading to longer frictions through advanced simulation

duration targets than are suggested here. methods. At the core of SBPS is the

While the LDI approach makes sense for a optimization algorithm that incorporates

plan fiduciary, it may be overly restrictive simulated investment outcomes (based

and suboptimal for an investor seeking to on the objective function selected and the

maximize terminal wealth. simulation engine used) and optimizes

all the asset weight vectors through time

3. Duration should be extended (shortened) all at once. This stands in contrast to

with expected inflows (outflows) dynamic programming approaches

When inflows and outflows are introduced, where consideration of many real-world

we see a very dramatic change to the aspects of multi-period portfolio

duration profile. By extending (or shortening) management would likely require a

duration, the investor can effectively lock non-trivial reformulation of the solution

in buying (selling) bonds with future to be used.

inflows (outflows) at today’s rate.

Examples and key insights

The implications are profound, particularly We present unconstrained SBPS solutions

in situations with prolonged inflows, for the investor problem introduced in the

where optimal solutions could require analytical section. Instead of optimizing

dramatic duration extensions. While this the mean versus variance objective, here

might seem counterintuitive, in the we are interested in the median versus

absence of directional views on interest median -5% value at risk objective. The

rates, this will lead to more efficient investment opportunity set includes

long-term results. US equity, international developed equity,

emerging market equity, and 1-year to

4. Duration should be adjusted based on 30-year maturity STRIPS indexes (separate

the slope of the yield curve, expected trading of interest and principal securities).

correlation of bond and equity assets Figure 5 shows cash flows, the efficient

and expected yield curve changes frontier, and the optimal allocations

If the yield curve is positively sloped, and durations for three selected solutions

duration should be extended. This allows on the frontier: low, medium, and high

investors to earn higher returns by risk.

investing in higher-yielding parts of the

yield curve. And it provides the opportunity The SBPS-based optimization results,

to potentially earn additional roll-down coupled with our analytical intuition from

returns. If yields are positively correlated the previous section, leads us to the

with equity returns (that is, if bond returns following observations:

are negatively correlated with equity

returns), duration should be extended, 1. SBPS generates allocations and

in line with standard diversification seeking duration profiles aligned with analytical

to exploit negative correlations. If yields expectations

are expected to increase, duration should All the key principles derived from our

be shortened so that assets can be analytical examples still hold true.

reinvested at increasingly higher rates. Specifically, allocations shift to safer

(riskier) assets as inflows (outflows)

Although it is difficult to develop occur and duration is extended

expectations about future yields, the (shortened) in the presence of future

general shape of the yield curve and the inflows (outflows).

correlation of its movements with equity

8 Risk & Reward #01/2022 | Multi-period portfolio selection: a practical simulation-based framework

2. SBPS allows for long-term real-world slightly positive correlation over the past

asset dynamics decade. Details such as these can

We can model assets more flexibly and meaningfully affect our solutions.

realistically than with the more simplistic

analytical model. For example, SBPS prices 3. SBPS allows for the consideration of

fixed income instruments based on investment frictions and illiquidity

simulated interest rate curves. This results Simulation also lets us consider real-world

in more consistent pricing while better investment challenges, including assumed

reflecting current market realities. For transaction costs (we assume 50 bps per

example, in a low rate environment, when transaction). This not only incorporates

bond returns are materially skewed, the the impact of transaction costs on

simulator is better aligned with market expected outcomes but also encourages

realities. Additionally, correlations between the optimization process to produce

rates and equities in SBPS are assumed to solutions with lower turnover.

be slightly negative, as opposed to their

Figure 5

Maximizing median terminal wealth with SBPS

Inflows, outflows and terminal wealth

Inflows Outflows Terminal wealth

Cash flow (USD)

1,500

1,000

500

0

-500

-1,000 ?

-1,500

0 1 2 3 4 5 6 7 8 9 10

Time (years)

Efficient frontier

Median terminal wealth (USD)

2,750

2,500

Medium risk High risk

2,250

2,000

Low risk

1,750

1,500

0 500 1000 1500 2000 2500 3000

Median terminal wealth with 5% VaR (USD)

Optimal allocations and durations

Bonds (STRIPS): 1yr 2yrs 3yrs 4yrs 5yrs 6-10yrs 10+yrs

Equities: Emerging markets Developed markets US

Low risk Medium risk High risk

Allocation (%) Allocation (%) Allocation (%)

100 100 100

75 75 75

50 50 50

25 25 25

0 0 0

0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9

Time (years) Time (years) Time (years)

Optimal bond duration (years) Optimal bond duration (years) Optimal bond duration (years)

30 30 30

20 20 20

n/a

10 10 10

0 0 0

0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9

Time (years) Time (years) Time (years)

Source: Invesco.

9 Risk & Reward #01/2022 | Multi-period portfolio selection: a practical simulation-based framework

SBPS for the income investor As before, the investment opportunity set

To demonstrate the flexibility of our SBPS includes US equities, non-US developed

approach, we now consider the retirement market equities, emerging market equities

The goal of income maximization income problem. We consider a 40-year- and 1-year to 30-year maturity STRIPS

is to identify the solution that old investor who plans to retire at age 60, indexes. In addition, 1 to 30-year TIPS

leads to the highest probability at which time he expects to withdraw a indexes (Treasury inflation protected

fixed annual income for 20 years. We securities) are also available. Note that we

of success for a given level of

assume: can work with both nominal cash flows

income. (contributions) and real cash flows (income

• An initial investment of USD 100,000 withdrawals). In real dollar terms, nominal

• Annual inflows of USD 50,000 (nominal) contributions have less value as we go out

for 20 years towards retirement into the future. The ability to convert

• Annual outflows (real) beginning in nominal dollars into real dollars and vice

year 20 and continuing to year 40 versa allows us to work in one single unit.

Figure 6

SBPS for the income investor

Inflows and outflows

Inflows (nominal expressed as real) Outflows (real)

Cash flow (real USD 1,000)

100

Accumulation

50

Consumption

0

-50

-100

40 42 44 46 48 50 52 54 56 58 60 62 64 66 68 70 72 74 76 78 80

Age (years)

Efficient frontier

Distribution (real USD 1,000)

300

200

High risk

Medium risk

Low risk

100

0

0 10 20 30 40 50 60 70 80 90 100

1 – probability of success (%)

Optimal allocations and durations

Bonds (STRIPS): 1-30yrs

Bonds (TIPS): 1-2yrs 3-5yrs 6-10yrs 11-20yrs 20+yrs

Equities: Emerging markets Developed markets US

Low risk Medium risk High risk

Allocation (%) Allocation (%) Allocation (%)

100 100 100

75 75 75

50 50 50

25 25 25

0 0 0

0 5 10 15 20 25 30 35 0 5 10 15 20 25 30 35 0 5 10 15 20 25 30 35

Time (years) Time (years) Time (years)

Real bond duration (years) Real bond duration (years) Real bond duration (years)

30 30 30

20 20 20

10 10 10

0 0 0

0 5 10 15 20 25 30 35 0 5 10 15 20 25 30 35 0 5 10 15 20 25 30 35

Time (years) Time (years) Time (years)

Source: Invesco.

10 Risk & Reward #01/2022 | Multi-period portfolio selection: a practical simulation-based frameworkThe goal of income maximization is to Conclusion: SBPS is more intuitive,

identify the solution that leads to the flexible, and adaptable

highest probability of success for a given We first presented the results of an

level of income. Figure 6 shows the cash analytical framework we developed that

flows in real dollar terms, the income provides a theoretical foundation for

investor’s efficient frontier, and the optimal multi-period portfolio selection and lends

allocations and real durations for three intuition for how portfolio allocations and

selected solutions on the frontier: low, duration should evolve over time. We then

medium, and high risk. present SBPS and demonstrate how it

addresses the three key requirements we

From our results, we can see the following: laid out for multi-period portfolio selection

solutions: (1) It produces solutions that

1. Low-risk solutions seek duration early align portfolio durations with expected

on and diversify with growth assets in cash flows, (2) it incorporates real-world

later years asset dynamics, and (3) it considers

In the low-risk allocation, the solution investment frictions and illiquidities. It

focuses on duration assets with extended also allows for the inclusion of individual

durations early in the investment horizon. hold-to-maturity and defined-maturity

At this stage, it is most important to investments.

eliminate the interest rate risk associated

with future purchases (and dispositions) SBPS provides substantial flexibility in

SBPS provides substantial of bonds that may be required from (for) addressing the major challenges of

flexibility in addressing the major upcoming inflows (outflows). As the implementing and managing portfolios

challenges of implementing and portfolio progresses through the investment across multi-period horizons. Decomposing

horizon and expected outflows increasingly the multi-period problem into three

managing portfolios across multi-

outweigh expected inflows, allocations distinct parts (the objective function,

period horizons. gradually shift to shorter duration bonds simulation, and optimization) also

and introduce equity exposures for facilitates further research into multi-

diversification. period portfolio selection, as innovations

in any of these three areas can easily be

2. High-risk solutions focus early on incorporated into our framework.

growth assets, with duration added

in later years Finally, SBPS readily accommodates new

In the high-risk solution, instead of methods of leveraging advances in

maintaining a 100% allocation to equity computing and optimization algorithms

assets through time, the solution moves to to solve multi-period portfolio selection

safer assets as outflows begin. Intuitively, problems using a simulation-based

during inflows, the solution seeks maximum approach.

return and, consequently, maximum risk.

Once outflows begin, they are assumed to

be constant. There is also no utility to any

remaining portfolio balance following

outflows. The result is that, for a given

outflow amount, the successful paths

will have no remaining upside and will

be exposed only to the risk of becoming

insolvent. To mitigate this effect, once

the outflows begin, the portfolio gradually

moves to some duration assets.

Notes

1 The full version of this article was published in the fourth quarter 2020 issue of The Journal of Investment Management.

Charts and content used with permission from the Journal of Investment Management.

2 For more details and the analytical solutions, please refer to the full version of this article.

References

K. Blay, A. Ghosh, S. Kusiak, H. Markowitz,

N. Savoulides and Q. Zheng (2020): Multi-

Period Portfolio Selection: A Practical

Simulation-Based Framework”, Journal of

Investment Management 18(4), pp. 94-129.

11 Risk & Reward #01/2022 | Multi-period portfolio selection: a practical simulation-based frameworkAbout the authors

Kenneth Blay Anish Ghosh

Head of Research Senior Analyst, Research and Analytics

Invesco Global Thought Leadership Invesco Investment Solutions

Kenneth Blay works closely with investment Anish Ghosh is responsible for driving

teams and researchers to lead the quantitative research and analysis. This

development of original research, the involves carrying out and publishing

authorship of white papers and articles for innovative original research, providing

publication in practitioner journals, and the in-depth research presentations to internal

creation of innovative investment content and external teams, and building out new

focused on strengthening Invesco’s profile research and technological functionalities

as a global thought leader in asset in Invesco Vision.

allocation, risk management, systematic

and factor investing, and portfolio

implementation.

Dr. Harry Markowitz Nick Savoulides

Economist, Nobel Laureate, and Head of Research & Portfolio Analytics

Invesco Investment Solutions Research Invesco Investment Solutions

Partner Nicholas Savoulides leads the development

Harry Markowitz is a consultant in the of Invesco Vision – a cloud-based portfolio

area of finance. In 1990, he was awarded research and analytics platform that

the Sveriges Riksbank Prize in Economic encompasses analytical and optimization

Sciences in Memory of Alfred Nobel for capabilities that facilitate the identification

his groundbreaking work in portfolio of portfolio solutions that address client-

theory. In 1989, he received the Jon specific investment objectives. As part

von Neumann Theory Prize from the of this effort, Nicholas engages with both

Operations Research Society of America internal and external investors and sets

for his work on portfolio theory, sparse the direction for future research and

matrix techniques, and the SIMSCRIPT development.

simulation programming language.

Qi Zheng

Senior Analyst, Research and Analytics

Invesco Investment Solutions

Qi Zheng is responsible for conducting

quantitative research and analysis

within the multi-asset solution space,

as well as developing and enhancing

various investment frameworks and

tools for asset allocation and portfolio

construction in Invesco Vision.

12 Risk & Reward #01/2022 | Multi-period portfolio selection: a practical simulation-based framework“Simulation has been a focus for me

over much of my career.”

Interview with Harry Markowitz

Risk & Reward

Dr. Markowitz, your 1952 Portfolio Selection

paper has been called the big bang of

modern finance and presented a single

period portfolio selection framework. In

your 1959 Portfolio Selection book, you

build out the theory on the single-period

framework and briefly discuss multi-period

portfolio selection. What is the difference

between single-period and multi-period

portfolio selection?

Harry Markowitz

As the name implies, the single-period

framework considers optimal action over a

single, finite period. However, the investor

can take no intermediate action over that

period. Consider the problem of maximizing

a series of cash flows. This can’t be

accomplished over a single period. Now,

the length of the period could be 30 years,

one decade, one month – or anything you

In this edition of Risk & Reward, we are proud to present an exclusive like. And you might approach the problem

interview with Dr. Harry Markowitz, father of modern portfolio theory, by optimizing a sequence of single periods

and withdrawing cash flows in between

1990 Nobel Laureate and co-author of our feature article on multi-

each. But, for a number of reasons, this

period portfolio selection. wouldn’t be the optimal solution. That

requires a multi-period approach which

optimizes outcomes while considering the

entire length of the investment horizon,

portfolio inflows and outflows, transaction

costs and other frictions – as well as an

investor’s intermediate actions.

Risk & Reward

In your 1959 book, you point to dynamic

programming to solve multi-period

problems. But in your work with the Invesco

team, you use a simulation-based approach

instead. Why?

Harry Markowitz

Let me first point out that, while most

people know me for my portfolio selection

work and the Nobel Prize that resulted

from it, I was also awarded the John von

Neumann Theory Prize in 1989 for my work

on simulation, the development of the

SIMSCRIPT simulation programming

language, portfolio theory and sparse

matrix techniques. So, simulation has been

a focus for me over much of my career.

The general approach for implementing

dynamic programming is to work backwards

through time. You begin by determining

the best action for each of the possible

13 Risk & Reward #01/2022 | Interview with Harry Markowitz: “Simulation has been a focus for me over much of my career.”circumstances in the last period, then the multi-period investment horizons for

next to last, and so on until you work your different asset classes, investment types

way back to the first period. The problem (active and passive) and account types

is that the possible circumstances in each (taxable, tax-deferred and tax-exempt).

period increase exponentially as you We then optimized the net present value

consider additional variables. This is what (NPV) of those outcomes. That work

is known as the curse of dimensionality. addressed the taxation question – and it

And this is also the reason we have yet also considered multi-period investment

to see full-fledged implementations of horizons.

dynamic programming solutions to

practical multi-period problems. Dynamic The SBPS framework we developed with

programming methods are certainly used Invesco significantly evolved that work

to inform portfolio construction. But the and, more importantly, generalized it to

number of variables that have to be address a number of other practical realities

considered continues to be a key limiting of multi-period investing – like duration

factor. Moreover, customizing dynamic management over long investment horizons,

programming solutions is a non-trivial investment frictions and real-world asset

exercise that can require a complete dynamics. The Invesco framework also

reformulation of the problem being allows for the incorporation of individual

considered. bonds in developing solutions.

The simulation approach we’ve taken Risk & Reward

provides a way around the dimensionality Could you tell us a bit more about the

problem. By decomposing the problem collaboration with Invesco?

into three distinct parts – the objective

function, simulation and optimization – Harry Markowitz

we also gain a great deal of flexibility in The team at Invesco has done a tremendous

the types of problems that can be solved job. They’ve successfully developed the

and in the ability to develop solutions that analytical intuition for how portfolio

address specific investor needs. allocations should evolve over time given

different objectives and in developing the

Risk & Reward optimization algorithm for computing

How would you characterize Simulation- these types of problems. That isn’t easy

Based Portfolio Selection, or SBPS for work. And they not only made it work for

short, the latest iteration of your portfolio our research effort, but they’ve also made

selection work with Invesco? the capability accessible to their clients

through the Invesco Vision portfolio risk

Harry Markowitz and research platform. This is a great

Our SBPS research builds on previous work example of theory turned into practical

in both portfolio selection and simulation. application.

Specifically, it expands on an article I wrote

together with Kenneth Blay back in 2013.1 Risk & Reward

Based on the insight that the impact of Dr. Markowitz, thank you very much for

taxes is path-dependent, we simulated your time!

after-tax investment outcomes over

Note

1 Blay, K. and H. Markowitz. 2016. “Tax-Cognizant Portfolio Analysis: A Methodology for Maximizing After-Tax Wealth.”

Journal of Investment Management, Vol 14, no. 1, 26-64.

14 Risk & Reward #01/2022 | Interview with Harry Markowitz: “Simulation has been a focus for me over much of my career.”Managing climate risk -

a 21st century approach

for commercial real

estate investors

By Louis Wright and Zachary Marschik

Not only is real estate a major contributor to CO2

emissions, as an asset class it is also suffering

increasingly from the very natural disasters

global warming brings about. With climate risk

accelerating around the world, real estate investors

need to consider the impact on their strategies.

Read on to learn how we approach these growing

challenges at Invesco Real Estate (IRE).

15 Risk & Reward #01/2022 | Managing climate risk – a 21st century approach for commercial real estate investorsPopulations around the globe face As figure 2 shows, global temperature

heightening climate risk. In 2021 alone, anomalies have risen considerably over

the world witnessed severe flooding in the last 100 years, and there is consensus

Western Europe and China, ice storms that this is the main reason for the rise in

in Texas and wildfires in California – the frequency and severity of natural

all of which exacted enormous economic disasters. Though governments, not-for-

and human costs. profit organizations and the private sector

have joined the fight against climate

Re-insurance data highlights the increasing change, even the most drastic of

cost of such disasters: Global economic interventions will require many years to

Global economic losses losses from natural and man-made reverse the global warming trend, and

from natural and man-made catastrophes totaled USD 202 bn in 2020, the cost of extreme weather is expected

catastrophes totaled USD 202 bn up from USD 150 bn in 2019.1 Figure 1 to continue climbing into the foreseeable

shows global losses broken down in line future.

in 2020. with the industry standard categorization

of climate events into primary perils and Real estate and the climate challenge

secondary perils. Primary perils are natural Real estate is a major contributor to global

disasters with known severe loss potential CO2 emissions. In 2020, the built

for the insurance industry, such as environment was estimated to be

tropical cyclones or earthquakes, responsible for 75% of annual global

whereas secondary perils are smaller greenhouse gas emissions,3 with buildings

to moderate events or the secondary alone accounting for about half of this

effects of a primary peril. Examples include amount.4 Around 50% of emissions from

river flooding, torrential rainfall, drought, new buildings are embedded in the

wildfire, thunderstorms and tsunamis. construction materials. The other half

Secondary perils are often not modeled arises from operation of the building.5

and have historically received little This sets the real estate industry before

monitoring from the insurance industry. the dual challenge of creating spaces that

Though the annual costs of both types are more efficient in use while reducing

of climate event are increasing, the share the up-front carbon emissions involved

represented by secondary perils is growing. in construction and refurbishment. This

should be kept in mind as we concentrate

The overwhelming majority of climate on identifying climate risks for existing

scientists and academics agree that global assets.

warming is caused by human activity.2

Figure 1

Global insured losses from climate events

Primary perils Secondary perils/effects of primary perils Total 5-year moving average

USD bn (2020 prices)

140

120

100

80

60

40

20

0

2012

2016

2000

2002

2004

2006

2008

2010

2014

2018

1990

1994

1992

1996

1998

1980

1984

1982

1986

1988

2020

Source: Swiss RE (2021); “In 5 charts: natural catastrophes in a changing climate”,

https://www.swissre.com/risk-knowledge/mitigating-climate-risk/sigma-in-5-charts.html

Figure 2

Annual global temperature anomalies since 1820

Degrees Celsius

2.0

1.5

1.0

0.5

0.0

-0.5

-1.0

-1.5

1830

1870

2010

1850

1880

1920

2000

1940

1910

1960

1990

1900

1820

1930

1840

1970

1860

1890

1950

1980

2020

Source: Berkley Earth; temperature anomalies relative to the Jan 1951-Dec 1980 average.

16 Risk & Reward #01/2022 | Managing climate risk – a 21st century approach for commercial real estate investorsFigure 3

Buildings and construction share of global energy and energy-related CO2 emissions (2020)

Energy Emissions

Residential 22% 17%

Non-residential 8% 10%

Energy Emissions Buildings construction industry 6% 10%

Other construction industry 6% 10%

Other industry 26% 23%

Buildings and Buildings and

Transport 26% 23%

construction construction

share in total: 42% share in total: 47% Other 6% 6%

Source: IEA (2021a).

Financial impacts of climate risk volatility, higher insurance costs, lower

on real estate capital growth, higher financing rates

Determining the financial impact of and reduced liquidity for commercial

extreme weather on real estate is complex properties (table 1). In the most severe

Determining the the financial and extends far beyond calculating the cases, a property could become a

impacts of extreme weather potential repair costs of a building. Climate stranded asset with its capital value

on real estate is complex. risk can influence real estate pricing via reduced to zero.

various channels, with effects varying in

severity and longevity. A recent United The UNEPFI report found that the financial

Nations Environment Programme Finance consequences of climate risk to real estate

Initiative (UNEPFI) report presents a depend on multiple conditions. One key

meta-analysis of research into such finding was that access to information on

impacts as reduced rental income, longer risks is a contributing factor in valuation

re-leasing times, greater cash flow and pricing, with evidence that better

Table 1

Potential effects of climate risk on commercial real estate asset performance

Broad Transmission Specific financial consequences

impact channel

Effects on Income • Reduced rent from fall in demand

cash flow • Reduced occupancy rate from fall in demand

• Longer to re-let space/weaker tenants

• Changes to feasible uses impacting on income

Outgoings • Increased operating costs (building services)

• Increased capital costs (repair/restoration)

• Higher insurance premiums to reflect higher risks

• Higher property taxes (clean up and mitigation

costs)

Effects on Risk • Greater cash flow volatility

capitalization premiums • Reduced liquidity/saleability of asset

rate • Reduced insurability of asset

• Greater site and location risks

Expected • Reduced rental prospects for location

growth • Increased depreciation for non-resilient buildings

• Reduced future occupancy rates

• Increased operating and capital costs, taxes, etc.

Effects on Cost of • Higher margins stemming from increased risk

financing finance • Higher DSCRs to cover cash flow volatility

Availability • Reduced willingness to lend in location

of finance • Lower amounts lent/more security sought

• Fewer potential equity partners

Source: Clayton J, van de Wetering J, Sayce S & Devaney S (2021); UNEPFI report “Climate risk and commercial property

values: a review and analysis of the literature”.

17 Risk & Reward #01/2022 | Managing climate risk – a 21st century approach for commercial real estate investorsinformation leads to greater awareness, Subcategory metrics are also available,

acceptance and integration of climate such as the expected flood return period

impacts on transacted prices. (i.e., flood frequency in years), rainfall

intensity and inundation level from a

Measuring climate risk 1-in-100-year flood.

Climate risk is not a singular metric, but

refers to multiple, interacting risks that can Democratizing climate risk data

compound and cascade, making it very The Moody’s tool can be used to evaluate

difficult to estimate. Measuring climate risk the climate risk of almost any location

requires quantifying both the likelihood across the globe, including IRE’s entire

and consequences of climate change in a direct real estate holdings, which comprise

particular location. Here, we focus on the more than 500 commercial assets across

physical elements of climate risk rather North America, Asia, Oceania and Europe.

than ’transition risks’, i.e., the potential

costs from moving towards a less polluting, Moody’s subscription-based model allows

greener economy. Though still important, users to generate location-specific climate

transition risks have fundamentally risk scorecards. These reports are detailed

different characteristics to physical climate and valuable, but optimizing their use at

risks and should therefore be modeled and IRE required building additional tools to

analyzed separately. better visualize and disseminate the data.

The information could not be easily

Assessing a specific location’s vulnerability accessed by the wider IRE teams who did

to future climate events has traditionally not have a Moody’s ESG login. So, in order

been the remit of a handful of highly skilled to leverage the information for better

professionals such as actuaries or investment and asset management

academics, and it required access to decision making, we needed to democratize

private datasets plugged into specialized our climate risk process – in particular

software. But growing awareness of and streamlining the delivery of information to

interest in climate risk have broadened teams involved in the appraisal of asset

demand for these tools. Recent acquisitions (transaction teams) and those

advancements in geospatial modeling managing existing assets and funds (asset

techniques coupled with the emergence of and fund managers).

open-source data and software has helped

proliferate climate risk services available to The solution found by IRE’s Strategic

businesses and organizations. Analytics team was a Climate Risk

Dashboard, which links directly to Moody’s

To understand the exposure of IRE’s global database and allows users to instantly

property portfolio to climate change, we identify the climate risk exposure of each

needed a tool with consistent and robust address they enter. The dashboard displays

scoring across various countries, regions the risks pertaining to our portfolio assets

and sectors. Moody’s ESG Solutions and summarizes and filters risks by fund,

(previously Four Twenty Seven) is a leading using maps and charts to highlight key

provider of physical climate and information.

environmental risk analysis with a climate

risk application well-suited for a globally Benchmarking asset risk

diversified asset manager like IRE. Investments do not happen in a vacuum.

While the clear first step in contextualizing

Moody’s methodology is deeply data climate risk is to democratize the asset-

driven and leverages large public and level data, further understanding can be

Moody’s methodology is private databases to generate more than achieved by considering how one

deeply data driven. 25 underlying risk indicators, each linked investment compares to another for insight

to known business consequences of into the relative risk. This can be done by

climate change. Scoring is forward looking benchmarking, or matching an asset’s

and focuses on thresholds near the tail end climate risk against other locations in the

of the risk distribution because such surrounding area. For instance, a well-

events are the most likely sources of located property with access to plenty of

disruption and damage – especially as amenities might see its locational benefits

extreme events grow in severity and/or outweigh its climate risk. However, it may

frequency. High-level risk indicators in still be more ideal to own a relatively less

Moody’s service include exposure to risky asset in the same area to minimize

floods, heat stress, hurricanes and the climate risk while enjoying the benefits

typhoons, sea level rise, water stress, of the amenities.

wildfires, and also earthquakes (which are

technically a geological hazard rather than Our benchmarking is achieved by utilizing

a climate risk but have also been included Moody’s ESG scoring on strategically

due to increasing client demand). generated sample points within a

boundary of interest (submarket, block

Moody’s risk scores are standardized group, etc.). With a series of sample

(ranging from 0 to 100) and globally points now available, the scores can be

comparable. The assigned risk levels summarized at the defined boundary

(none, low, medium, high, red flag) aid levels, and scores of individual assets

interpretability. For example, a flood risk of interest can be placed within the

score of 70/100 equates to a high risk level distribution. Figure 4 shows a building in

and means a location is susceptible to Tokyo and how its flood risk compares to

some flooding and inundation during the surrounding area. In this location, the

rainfall or riverine flood events. low score conveys that the asset is not

18 Risk & Reward #01/2022 | Managing climate risk – a 21st century approach for commercial real estate investorsFigure 4

A benchmarking example

Risk: Red Flag High Medium Low None

Benchmark count

100

Asset and benchmark scores

75

50

25

0

25 50 75

Score (lower is better)

Source: IRE Strategic Analytics.

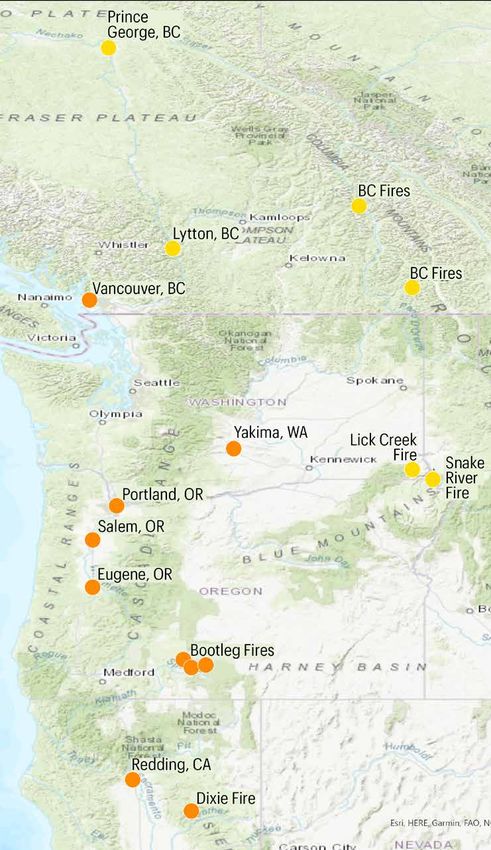

very exposed to flood risk. However, as North American wildfires

the distribution in figure 4 shows, there In the summer of 2021, several areas in

are parts of Tokyo with high risk values, western North America experienced

meaning that the sample building might historic wildfires while much of the region

be a well-positioned asset, close to experienced record high temperatures.

All areas with the largest wildfires

amenities but far enough away from To test the utility of the Moody’s ESG

had been properly scored as the low-lying areas to avoid being too scores using a real-world example, we

high-risk locations. risky. looked at the Moody’s wildfire scores for

locations in the Pacific Northwest. The

Recent extreme weather events: results proved encouragingly accurate:

Two case studies Apart from medium risk scores in British

Finally, we assess the validity and accuracy Columbia, all areas with the largest

of Moody’s ESG scores with the help of wildfires had been properly scored as

two case studies of recent climate events. high-risk locations (figure 5).

Figure 5 Figure 6 Figure 7

Moody’s wildfire scores Moody‘s heat scores Moody’s future extreme temperatures

sub-scores

Source: IRE Strategic Analytics. Source: IRE Strategic Analytics. Source: IRE Strategic Analytics.

19 Risk & Reward #01/2022 | Managing climate risk – a 21st century approach for commercial real estate investorsAdditionally, we analyzed Moody’s heat a large river running through its center.

scores to see if the record-high temperatures Almost all the sample points near a river

were something that could have been and/or at relatively low elevation had a

foreseen. While overall heat scores high or red flag risk level in Moody’s

(figure 6) did not seem to be good scoring system. Equally, sample locations

predictors, the subcategory score for with medium-to-low flood risk were

future change in extreme temperatures sufficiently distanced from a river and/or

(figure 7) seemed to provide a warning had much higher land elevations.

that extreme heat is only going to get

worse. This sub-score provides valuable Conclusion

information for investors, and the high Many real estate investors still ignore

scores for future change are supported extreme weather events as they are

by the events of summer 2021. unpredictable and difficult to quantify.

Nonetheless, climate-related events are

European floods expected to become more common and

In July 2021, a number of Western more severe, calling into question this style

European countries experienced extreme of approach: Investors can no longer afford

flooding. Worst affected were Germany, to leave climate risk information out of

Belgium, Netherlands and Austria. A total their decision making. IRE’s Climate Risk

of 242 deaths are attributed to the Dashboard is designed to deliver timely

Investors can no longer afford flooding, of which 196 were in Germany. and reliable information to identify and

to leave climate risk information To test the validity of Moody’s ESG scores, mitigate, or completely avoid, potential

we sampled flood risk scores across five climate risk exposure. This will ultimately

out of their decision making. towns devastated by the floods (Schönau help us better preserve and grow capital

am Königssee, Hagen, Schuld and Bad and deliver stronger and more secure

Neuenahr in Germany, and Hallein in returns for our clients.

Austria). Unsurprisingly, each town had

Notes

1 Swiss RE (2021) Natural catastrophes in 2020: secondary perils in the spotlight, but don’t forget primary-peril risks.

Sigma 1/2021.

2 For instance, Carbon Brief (2021) Mapped: How climate change affects extreme weather around the world. https://

www.carbonbrief.org/mapped-how-climate-change-affects-extreme-weather-around-the-world; NASA (2021)

Scientific Consensus: Earth’s Climate Is Warming. https://climate.nasa.gov/scientific-consensus/

3 Architecture 2030 (2021) The 2030 Challenge. https://architecture2030.org/2030_challenges/2030-challenge/

4 39% of CO2 emissions according to Architecture 2030; 37% of CO2 emissions and 36% of global energy

consumption according to the UN Environment Programme.

5 World Green Building Council (2021) Beyond the Business Case report 2021. https://www.worldgbc.org/business-

case

About the authors

Louis Wright Zachary Marschik

Associate Director, Global Strategic Analytics Associate Director, Global Strategic Analytics

Invesco Real Estate, London Invesco Real Estate, Dallas

Louis Wright is a real estate data scientist Zachary Marschik is a real estate data

and research analyst, responsible for scientist who develops data-driven models

covering real estate markets in France and and applications, in particular geospatial

Iberia as well as developing investment analyses, to reveal investment and

insights through data-driven models and operational insights. Zachary works with

applications, including geospatial analyses. IRE’s US investment professionals to

Louis works with IRE’s European investment further understanding of thematic trends

professionals to make sense of the themes on real estate markets and enable targeted

and trends facing real estate markets adjustment at asset level.

as well as exploring granular locational

differentiation.

20 Risk & Reward #01/2022 | Managing climate risk – a 21st century approach for commercial real estate investorsYou can also read