Retail Statement (Addendum) - Proposed Replacement Lidl Store at 390 Shirley Road, Southampton - Proposed Replacement Lidl ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Retail Statement (Addendum)

Proposed Replacement Lidl Store at 390 Shirley Road, Southampton

Prepared on Behalf of Lidl UK

Date: November 2017

Our Ref: JPW0910

RPS

Park House

Greyfriars Road

Cardiff

CF10 3AF

Tel: (0)2920 668 662

Fax: (0)0920 668 622

Email:

rpsca@rpsgroup.com

rpsgroup.com/uk

Quality Management

Prepared by: Chris Tookey

Authorised by: Ross Bowen

Date: 8th November 2017

Revision: v2

Project Number: JPW0910

Document Reference: 171108 R JPW0910 CT Addendum Retail Statement v2

O:\04 JOBS\01 OPEN JOBS\JPW09 xx\JPW0910 - LIDL, SHIRLEY ROAD,

Document File Path: SOUTHAMPTON\5. Reports\2. Final Report\171108 R JPW0910 CT

Addendum Retail Statement v2.docx

COPYRIGHT © RPS

The material presented in this report is confidential. This report has been prepared for the exclusive use of Lidl UK and shall not be

distributed or made available to any other company or person without the knowledge and written consent of RPS.

This document is Printed on FSC certified, 100% post-consumer recycled paper, bleached using an elemental chlorine- free process.

i rpsgroup.com/uk

Amendment Record

Revision No. Date Reason for Change Authors Initials

ii rpsgroup.com/ukContents

Quality Management..................................................................................................................... i

Amendment Record ..................................................................................................................... ii

Contents ...................................................................................................................................... ii

1 Introduction ..........................................................................................................................1

Scope and Purpose .............................................................................................................1

2 The Application Site and the Proposed Development .........................................................2

Site Description ....................................................................................................................2

The Existing Lidl Store .........................................................................................................2

The Proposed Development ................................................................................................3

Lidl’s Business Model ..........................................................................................................3

3 Planning Policy Context .......................................................................................................7

Southampton Core Strategy ................................................................................................7

Southampton Local Plan Review .........................................................................................8

National Planning Policy Framework ...................................................................................8

National Planning Practice Guidance ..................................................................................9

4 Evaluation of Compliance with Retail.................................................................................11

The Sequential Approach to Site Selection .......................................................................11

Impact on Existing, Committed and Planned Public and Private

Investment in Centres Within the catchment Area.............................................................12

Impact on Town Centre Vitality and Viability, Including Local Consumer

Choice and Trade in the Town Centre and Wider Area .....................................................12

5 Summary and Conclusions ................................................................................................14

Appendices

1. Statistical Tables

2. Study Area Plan

ii rpsgroup.com/uk1 Introduction

Scope and Purpose

1.1 This Retail Statement has been prepared by RPS Planning & Development on behalf of Lidl UK

to accompany a planning application ref. 17/01206/FUL that seeks permission for the

development of land at 390 Shirley Road, Southampton to provide a new Lidl foodstore with

dedicated surface level parking: the new store will replace an existing Lidl store currently trading

at 355 Shirley Road. It is an addendum to the Retail Statement (July 2017) that was originally

submitted with the planning application, and it has been produced to take account of changes

that have been made to the development scheme post-submission.

1.2 This report focuses on the retail policy issues associated with the proposed development. It is

intended to assist Southampton City Council in its determination of the application and has been

prepared in accordance with the requirements set out in the National Planning Policy

Framework (NPPF). It seeks to evaluate the proposal against national and local retail planning

policies and considers the retail justification and implications of the proposed development.

1.3 This report is structured as follows:

• Section 2 describes the application site and its context, and the proposed development.

• Section 3 reviews the relevant retail policy background, including national and local

planning policy.

• Section 4 provides an assessment of the proposed development against the key retail

tests ie the sequential approach to site selection and impact on defined centres.

• Section 5 summarises the key considerations in relation to retail policy matters and

presents our overall conclusions.

1 rpsgroup.com/uk2 The Application Site and the Proposed Development

Site Description

2.1 The application site extends to 0.83ha and is bounded to the east by Shirley Road; to the south

by Villiers Road; to the west by the rear of residential properties fronting Heysham Road; and to

the north by the rear of residential properties fronting Mayflower Road and several commercial

units fronting Shirley Road.

2.2 The site essentially comprises three elements:

the eastern part of the site comprises a former Police Station, made up of a detached

three-storey building with single storey elements on its front (east) and southern

sides, and an area of hardstanding to the rear that was previously used for car

parking;

the western part (to the rear of the former police station) comprises a Council depot

that contains a range of buildings of varying size, used for storage, offices and

workshops, as well as areas of open storage and car parking;

the northern part comprises No. 392 Shirley Road (including the property to the rear,

formerly No. 392b), which contains two Class A1 retail units and a Class A3/A5

café/take-away.

2.3 The north and eastern elements of the site lie within Shirley Town Centre, and the north element

is also designated as a secondary shopping area. Accordingly, given the proposed store will be

located on the north-eastern part of the site, with the customer entrance fronting on to Shirley

Road, in practical terms it will constitute a town centre store for the purposes of the sequential

approach to site selection.

The Existing Lidl Store

2.4 The existing Lidl is located at 355 Shirley Road, to the south of the application site. It is within

the boundary of the town centre and the store building is designated as a secondary shopping

area, however it is actually a back land site that fronts on to Church End, to the rear of

properties along Shirley Road (including McDonalds and Tesco Express).

2.5 The store opened in November 1994 (under planning permission 931196/W) and was one of

the first Lidl stores in the UK. Originally it provided 790sq m net sales space but in 2006

planning permission was granted (under 06/00198/FUL) for an extension that increased the

sales area to 991sq m net. It currently provides customer parking for 75 cars including two

disabled spaces.

2.6 As a first generation store the existing building is smaller than Lidl’s current format and so is

unable to provide the offer and quality of shopping experience now delivered by the larger more

modern designs. Lidl wish to allow shoppers in Shirley the opportunity to access the same

quality of shopping as they provide elsewhere in the UK, but given the constricted nature of their

existing site this can only be accommodated through a relocation to a larger store elsewhere.

The purchase of the application site now provides the opportunity for that relocation, to a new

larger store that will be built to Lidl’s latest sustainable design. As well as a quantitative and

qualitative improvement to Lidl’s offer the new store will also front on to the high street which will

increase the potential for linked shopping trips to other shops in the town centre.

2 rpsgroup.com/ukThe Proposed Development

2.7 The development will involve the demolition of all the existing buildings and structures, and the

construction of a larger replacement Lidl store of 2,207sq m gross internal area with a sales

area of 1,401sq m and parking for 118 cars including 6 disabled spaces and 8 for parent/child.

A singular vehicular access will be taken off Villiers Road, replacing the three accesses

currently in place for the depot and police station.

2.8 The replacement Lidl will be built to Lidl’s latest store specification/design. It will incorporate

more glazing than the existing older format store, and will be more energy efficient and

sustainable. The existing store is a popular shopping destination and as acknowledged in the

Southampton and Eastleigh Retail Study it is trading above its benchmark level. The larger

replacement store is intended to provide qualitative improvements to the shopping environment,

as well as an improved retail offer.

2.9 At the time that the planning application (ref. 17/01206/FUL) was submitted the proposed

development comprised a store of 2480sq m gross and 1,655sq m net sales, with parking for

125 cars. However, the design of the scheme has now been amended to reduce the store

down to 2,207sq m gross, which has allowed the building to be set slightly further back from the

boundary with Shirley Road and the TPO tree on the frontage to be retained. These changes

have been incorporated in order to address comments made on the planning application.

Lidl’s Business Model

2.10 Lidl, along with Aldi, are classed as Limited Assortment Discounters (LADs), a category of

retailer distinct from the mainstream operators. Lidl’s strategy is the provision of smaller stores

at convenient locations within or close to residential areas, which are capable of serving both

the day-to-day top up and main food shopping needs of local residents.

2.11 The company’s operation is based upon a traditional supermarket with very attractive prices.

The range of goods sold is limited and around 80% of all products are Lidl’s own brand. This

retail operation can be achieved by:

Bulk purchasing across the UK and Europe;

Ensuring that distribution costs are kept to a minimum; and

Controlling property and operation costs prudently.

2.12 The Lidl format is a well-established shopping experience in Europe with almost 10,000 stores

across the continent, and their store at Shirley is a popular shopping destination for local

residents.

Product Range and Pricing Structure

2.13 Lidl’s offer is based on providing a limited range of high quality products at very attractive prices.

The limited number of lines, which are significantly less than other mainstream retailers, is to

ensure the lowest possible operating costs. It includes:

A quality range of fresh and frozen pre-packaged meat;

Own-brand dry groceries & frozen foods;

Tertiary branded wines and spirits;

A quality range of loose and pre-packed fruit and vegetable lines; and

3 rpsgroup.com/uk A basic range of non-food household items and twice-weekly (non-food) specials

occupying about 20% of the sales area, such as a limited range of electrical and

gardening products.

2.14 Of more relevance is the range of goods and services that Lidl do not sell. Lidl’s retail offer is

distinct from the large retailers and small convenience stores by not offering the following:

Butchers counter;

Fishmonger;

Dispensing pharmacy;

Dry-cleaning service;

Post office service;

Financial products;

Photography processing;

Café / restaurant; and

Cigarettes and tobacco products

2.15 The above product ranges and services are not offered in Lidl stores as they do not fit with the

core retail concept. This is one way in which Lidl differs from mainstream retailers. The larger

food retailers have all been through a considerable process of diversification over the past

decade. Many offer all of the above services as a ‘one stop’ destination for their customers.

2.16 Large and small retailers alike continue to trade successfully alongside Lidl stores all over the

UK. The format and style that Lidl operate differs significantly from that of other supermarket

traders (only Aldi have a similar business model). This is achieved primarily through the heavily

discounted pricing structure and the strictly limited range of goods. A Lidl store typically stocks

around 1,800 items and the range of goods is significantly smaller than that offered by other

retailers. From our experience we are aware that the major operators, such as Morrison, Tesco,

Asda and Sainsbury, can retail over 35,000 lines, while a Lidl store will provide around 5% of

that. In addition to the limited product range, unlike its counterparts in the retail industry Lidl do

not stock multiple lines of the same product.

2.17 For the above reasons, Lidl stores successfully trade immediately adjacent to larger superstores

and smaller convenience stores in numerous locations across the UK. In Shirley the existing

store sits adjacent to a Tesco Express.

2.18 Lidl stores receive a twice weekly delivery of special non-food offers such as a limited range of

electrical, homewares and gardening products. These products are marketed in the press to

attract customers into the store, and sold on a strictly limited basis. The products sold on this

basis constantly change and therefore do not present potential for sustained impact on existing

centres that may be the case with typical superstore comparison elements which are focused on

clothing and CD/DVD sales.

2.19 Products are often displayed in their original pallets or boxes to minimise unnecessary costs

associated with conventional shelf stacking. This no-frills approach is typical of the commitment

to ensure that products are sold at the lowest possible margins.

2.20 Independent research by the Competition Commission confirmed that the national deep

discounters, Lidl, Aldi and Netto provide a distinct retail offer from the mainstream food retailers

4 rpsgroup.com/uk(although it must be noted that sometime after this research was published Netto ceased

operations in the UK, selling their store portfolio to Asda – they briefly returned in 2014 in a joint

venture with Sainsbury, but that ended in 2016). Prices within the sector are acknowledged to

be “well below the prices of the market leaders, and have a considerably smaller range of

goods” (Competition Commission Report on Supermarkets 2000). It is notable that the former

Netto stores that Asda have converted to their new small supermarket format typically retail

10,000 grocery products, substantially more than the previous deep discount format they

replaced.

2.21 Previous Verdict reports have stated that Lidl and Aldi retail products at prices of 30% lower

than the large retailers.

2.22 In terms of public awareness and perception, Lidl stores are very popular, not only with those on

a limited income but also increasingly with the higher social groupings. Market research

undertaken by Verdict Research shows that the most significant increase in penetration over the

period 2005-2012 has been among more affluent shoppers, with those in the AB social grade

actually having moved from the lowest to the highest visitor share (Verdict’s ‘How Britain Shops

2012’). This is a reflection of the economic downturn where the number of people visiting Lidl

rose as consumers sought to minimise food spending due to reduced levels of disposable

income. More affluent shoppers have realised that the quality of offer available is superior in

many cases to the larger grocery retailers and much cheaper. However Lidl’s existing store at

Shirley is dated and cannot offer the shopping experience provided in their larger current format.

2.23 Lidl operate on far lower profit margins than the major food store operators and can therefore

pass on the savings to their customers, which instils loyalty and a return to store mind set.

2.24 The Lidl business model inevitably has consequences for the design and layout of stores. The

size and configuration must be compatible with Lidl’s efficient delivery and stock handling and

ability to stock the standard product lines in sufficient depth to meet customer needs and

minimise costs. This inevitably places restrictions on the ability of the business model to be

‘flexible’ in terms of the store format. This has implications in terms of the application of the

sequential approach – a fact that has been widely accepted by Local Planning Authorities,

Planning Inspectors and the Secretary of State in application and appeal decisions across

England. Fortunately, in Shirley the application site provides an opportunity to develop a new

larger store at a location fronting the high street that will be sequentially preferable to their

existing back land site.

Opening hours

2.25 The new store’s opening hours are proposed to be 0800-2000 hours Monday to Saturday and

Bank Holidays, and 1000-1600 on Sundays.

Servicing

2.26 Mindful of the need to minimise disturbance to any neighbouring landowners, each Lidl store

has only 2 or 3 deliveries a day for all its products, including; ambient, fresh, frozen and chilled

goods. Total unloading time is generally only around 45 minutes and vehicle noise is minimised

due to a recessed loading bay, a manual bridging plate and a dock shelter: a close-boarded

timber fence will also be provided along the loading bay to provide acoustic attenuation. The

regime for the proposed new store will essentially be almost identical to the existing store that it

5 rpsgroup.com/ukwill replace and the proximity of the service bay to residential properties will be not dissimilar to

the existing store (which is surrounded on three sides by housing).

2.27 On the issue of waste, Lidl recycle their packaging material, with their merchandising and

display formats being designed to facilitate this. All stores are equipped with either a cardboard

compactor or baler: cardboard waste is compressed to provide a decrease in volume of 400%,

which helps to lower carbon emissions as more cardboard can be transported back to the

Regional Distribution Centres on each lorry. This also results in a reduction in both noise

pollution and congestion. Compacted cardboard is stored on site for daily collection by the

returning HGV, along with all plastic, food waste, wood and all non-recyclable refuse.

2.28 During 2016/17 Lidl recycled over 10,300 tonnes of cardboard and paper, overt 450 tonnes of

plastic and 370 tonnes of metal. The intention is to increase the volume of recycled material

year-on-year. A combination of initiatives enabled the Regional Distribution Centre in Weston-

Super-Mare to recycle 95% of all waste in 2016/17. Total recycling for the UK in 2016/17 was

92% and the company target for 2017/18 is 93%.

2.29 Principles of sustainability are engrained in Lidl’s operation from the efficient construction and

standardised fit-out elements enabling rapid store construction, to energy saving measures

including energy efficient building materials, low energy consumption lighting, motion detectors

and automatic ‘power down’ lighting, electricity and heating in the evenings.

Employment

2.30 Staffing levels have yet to be finalised, however the larger store is likely to give rise to a need

for additional staff in-store. Lidl always seek to source labour locally and provide management

opportunities for staff, the company’s philosophy being to provide all their employees with

opportunities for developing and progressing their careers with the company, with the corporate

strategy being to promote from within.

6 rpsgroup.com/uk3 Planning Policy Context

3.1 This section of the report briefly considers the national and local planning policies of relevance

to the proposed retail development.

3.2 Section 38(6) of the Planning and Compulsory Purchase Act 2004 states that planning

applications must be determined in accordance with the development plan, unless material

considerations indicate otherwise. In this instance the development plan consists of the Core

Strategy (incorporating a partial review) 2015 and the Local Plan Review 2015. There is also

the City Centre Action Plan 2015 and the Bassett Neighbourhood Plan 2016, however neither of

those two development plan documents is relevant to Lidl’s application in Shirley. Other

material considerations include national policies set out in the National Planning Policy

Framework (NPPF) and the National Planning Practice Guidance (NPPG). In 2015 work

commenced on a new Local Plan, however that is currently in abeyance.

Southampton Core Strategy

3.3 The Core Strategy was originally adopted in 2010 with a Partial Review in 2015, and is intended

to guide the development of Southampton up to 2026.

3.4 Section 4.3 sets out the spatial strategy for future development, which includes, inter alia,

supporting the continued vitality and viability of the City Centre, which is to be the focus for

significant new offices, retail, hotel, leisure and residential development. Outside the City

Centre smaller scale retail facilities for residents will be supported and enhanced in Shirley

Town Centre and in the designated district centres.

3.5 The city is divided into five suburban neighbourhoods, of which the West area includes Shirley,

Millbrook, Redbridge and Coxford. Paragraph 4.3.1 states that within this area an additional

1500 homes are planned and it is noteworthy that assuming an average household size of 2.4

(figure for Southampton calculated from the 2011 Census) and a notional per capita

convenience spend of £1950 at 2026 (the average of the figures for Zones 5 & 6 in the

Southampton and Eastleigh Retail Study), this new housing will potentially generate circa £7m

of additional convenience goods expenditure.

3.6 Paragraph 4.3.2 of the Strategy states that the Council will take a positive approach to new

development, reflecting the presumption in favour of sustainable development contained in the

NPPF. Paragraph 4.3.3 says that planning applications that accord with the policies in the

development plan will approved without delay, unless material considerations indicate

otherwise. Paragraph 4.3.4 then goes on to say that where there are no policies relevant to the

application, or they are out of date, the Council will grant permission unless material

considerations indicate otherwise, taking account whether, inter alia, any adverse impacts of

granting permission would significantly and demonstrably outweigh the benefits when assessed

against the policies in the NPPF taken as a whole [our emphasis].

3.7 Policy CS3 covers the town, district and local centres – Shirley is the sole second tier Town

Centre, under the City Centre and above four District Centres and 16 Local Centres. The policy

says that the Council will support the role of the town and district centres in providing shops and

local services in safe, accessible locations. New development should make a positive

contribution to the centre’s viability and vitality and enhance its attractiveness. The aims for,

inter alia, Shirley are to maintain the health of the centre, improve the street scene and

7 rpsgroup.com/uksuccessfully integrate local facilities. The proposed Lidl development accords with this policy in

as much as the new store will be better integrated into the centre, having moved from a back-

land site to one fronting the high street.

Southampton Local Plan Review

3.8 The Local Plan Review was adopted in March 2006; a revised version was produced in 2010

following the adoption of the Core Strategy (which detailed the policies ‘saved’ by Direction of

the Secretary of State), and a further updated version in 2015 after the adoption of the City

Centre Action Plan and the partial review of the Core Strategy.

3.9 On the Proposals Map the northern and eastern parts of the application site lie within the

defined boundary of Shirley Town Centre - the western Council depot site was not included in

the centre boundary, presumably because at the time the Plan was prepared it was not a ‘town

centre use’. However it is noteworthy that adjoining the site on the southern side of Villiers

Road the centre boundary does extend as far back from the high street as the western end of

the application site, taking in the car park serving the Royal Mail delivery office and easyGym.

3.10 The northern part of the site is also designated as a secondary shopping area, as is the existing

Lidl store off Church End. It is clear that given the new store building will lie within the town

centre boundary, and a designated shopping area, it will function as a town centre store and

satisfies the sequential approach to site selection.

3.11 Paragraph 1.20 of the Local Plan recognises that it must make adequate provision for the

conduct of business in the 21st Century, including being flexible to accommodate the changing

nature of business. In that respect the reason behind the proposed development is to enable

Lidl to upgrade their offer in Shirley to take on board changes and improvements that have been

made to their store designs over the last 22 years.

National Planning Policy Framework

3.12 NPPF Paragraph 7 advises that there are three dimensions to sustainable development:

• An economic role – the planning system should contribute to building a strong,

responsive and competitive economy, by ensuring that sufficient land of the right type is

available in the right places and at the right time to support growth and innovation; and

by identifying and co-ordinating development requirements, including the provision of

infrastructure;

• A social role – planning should support strong, vibrant and healthy communities, by

providing the supply of housing required to meet the needs of present and future

generations; and by creating a high quality built environment, with accessible local

services that reflect the community’s needs and support its health, social and cultural

well-being; and

• An environmental role – the system should contribute to protecting and enhancing our

natural, built and historic environment, including using natural resources prudently,

minimising waste and pollution and mitigating and adapting to climate change,

including moving to a low carbon economy.

3.13 NPPF Paragraph 14 makes clear that “At the heart of the National Planning Policy Framework is

a presumption in favour of sustainable development, which should be seen as a golden thread

8 rpsgroup.com/ukrunning through both plan-making and decision-taking”. It is also made explicit that in making

decisions on planning applications this means:

• “approving development proposals that accord with the development plan without

delay; and where the development plan is absent, silent or relevant policies are out-of-

date, granting permission unless:

• any adverse impacts of doing so would significantly and demonstrably outweigh the

benefits, when assessed against the policies in the Framework taken as a whole; or

• specific policies in the Framework indicate development should be restricted”.

3.14 Paragraph 17 of the NPPF sets out the core planning principles that should underpin both plan-

making and decision taking. These state that planning should, inter alia: proactively drive and

support sustainable economic development to deliver the homes, business and industrial units,

infrastructure and thriving local places that the country needs. Every effort should be made

objectively to identify and then meet the housing, business and other development needs of an

area, and respond positively to wider opportunities for growth; and promote mixed-use

development, and encourage multiple benefits from the use of land in urban and rural areas.

3.15 Paragraphs 18 and 19 state that the Government is committed to securing economic growth in

order to create jobs and prosperity, and to ensuring that the planning system does everything it

can to support sustainable economic growth. Planning is expected to encourage and not act as

an impediment to sustainable growth, and significant weight should therefore be placed on the

need to support economic growth through the planning system.

3.16 Paragraph 24 states a sequential approach to selecting sites for main town centre uses (which

include retail development, hotels, restaurants and bars) should be applied where they are not

in an existing centre or in accordance with an up-to-date Local Plan. If no suitable sites are

available within a town centre, edge of centre sites should be considered. If no suitable edge of

centre sites cannot be identified then out-of-centre sites at accessible locations should be

considered. Sites must be suitable and available, and both developers and LPAs should

demonstrate flexibility on issues such as format and scale.

3.17 Paragraph 26 states that for retail development outside a town centre and not in accordance

with an up-to-date Local Plan, an impact assessment will be required that should consider:

• The impact of the proposal on existing, committed and planned public and private

sector investment in a centre or centres within the catchment area of the proposal;

and

• The impact on town centre vitality and viability, including local consumer choice and

trade in the centre and wider area.

3.18 Paragraph 27 confirms that where an application satisfies the sequential test and is unlikely to

have significant adverse impact it should be approved.

National Planning Practice Guidance

3.19 The National Planning Practice Guidance (NPPG) supports the NPPF and its section ‘Ensuring

the vitality of town centres’ replaces the guidance previously contained within ‘Planning for

Town Centres: Practice Guidance on Need, Impact and the Sequential Approach’ issued in

December 2009.

9 rpsgroup.com/uk3.20 The NPPG states that local planning authorities should plan positively to support town centres in

order to generate local employment and promote beneficial competition.

3.21 Paragraph 008 (in the ‘ensuring the vitality of town centres’ section) summarises the sequential

test, where the first preference is to be town centre locations, followed by edge-of-centre

locations and only then out-of-centre locations with a preference for accessible sites that are

well connected to a town centre. The application site lies partly within the boundary of Shirley

Town Centre and part is designated as an existing secondary shopping area. Half of the

proposed store building will lie within the centre and half immediately outside, however that is a

result of the existing centre boundary having been drawn to exclude the Council depot. In

practice the replacement Lidl will function as a town centre store, with the customer entrance

accessible off the high street; following the completion of the development the boundary of the

town centre can be amended as part of the review of the Local Plan, to include the rear of the

site within the centre boundary.

3.22 Paragraph 010 provides guidance in relation to the application of the sequential test when

determining planning applications. The application of the test should be proportionate and

appropriate for the proposed development, with sites assessed as to their suitability and

availability. In assessing sites regard should be had to the requirement to demonstrate

flexibility, and the local planning authority should support the applicant and share any relevant

information they may have. In considering flexibility it is not necessary to demonstrate that a

potential town centre or edge-of-centre site can accommodate precisely the scale and form of

development being proposed, but rather to consider what contribution more central sites are

able to make individually to accommodate the proposal. If there are no sequentially preferable

locations the test is passed.

3.23 This requirement to show flexibility has been taken by some to constitute a need to consider the

disaggregation of development schemes, where units in a scheme may be split up onto one or

more sequentially preferable sites. However the judgement of the Supreme Court in Tesco v

Dundee City Council (November 2012) and recent decisions by the Secretary of State (most

notably the call-in decision at Rushden Lakes in 2014) have clarified the application of the

sequential test in development management, and made clear that there is no requirement for an

applicant to consider the disaggregation of their scheme when undertaking a sequential

assessment. In any event, as already detailed above the application site is considered to be a

town centre site and the proposed store will have superior linkage to the high street than the

existing store off Church End.

10 rpsgroup.com/uk4 Evaluation of Compliance with Retail

4.1 Section 2 of the National Planning Policy Framework (NPPF) relates to retail development and

the vitality of town centres, and requires the following assessments for developments proposed

outside defined retail centres and not in accordance with an up to date development plan:

• Sequential test.

• Retail impact, comprising:

o Impact on existing, committed and planned public and private investment

in centres within the catchment area.

o Impact on town centre vitality and viability, including local consumer

choice and trade in the town centre and wider area.

4.2 Paragraph 27 of the NPPF is clear that where an application fails to satisfy the sequential test or

is likely to have a significant adverse impact [our emphasis], it should be refused.

The Sequential Approach to Site Selection

4.3 It is important to note that this application relates to the replacement of Lidl’s existing store,

which is a popular destination for grocery shopping within Shirley - the household survey

conducted for the Southampton and Eastleigh Retail Study 2011 indicates that it trades above

the company’s benchmark level. The store was developed over 20 years ago and is smaller

than Lidl’s current format and cannot provide the same breadth or quality of retail offer to its

customers. Lidl wish to provide quantitative and qualitative improvements to their store,

including an uplift in both floorspace and parking provision - a larger building will allow

qualitative improvements to the retail offer including increased aisle widths and circulation

space; and increased natural light (which provides an opportunity to reduce power

consumption). This is geared to providing a more efficient store operation and an improved

shopping environment and offer for existing customers: it is not expected that the additional

floorspace will result in any significant increase in customer traffic.

4.4 The constrained nature of their site means that an extension of the existing building is not

practical, however an opportunity presented itself for Lidl to acquire the former Police Station

and Council Depot, which were marketed in 2016 as a single site with re-development potential.

Subsequent to that contracts have also been exchanged on the adjoining 392 Shirley Road –

together this results in a larger and more rectangular development site with improved frontage

on to the high street, and provides the space necessary to accommodate the larger store and

car park.

4.5 In terms of the sequential approach to site selection the first preference has to be sites within or

adjoining a defined centre. The application site fully accords with this, since half the site lies

within the defined town centre and partly within a designated secondary shopping area. The

new store will therefore function as a town centre shop with better linkage on to the high street

than the existing Lidl.

4.6 The larger replacement store will provide Lidl with an additional 410sq m of sales space, the

primary purpose of which is to enable them to improve their existing retail offer, to better meet

their customers’ needs: providing the additional floorspace elsewhere would therefore not

address this objective. Their requirement is for a store of 2,207sq m gross area with a 1,401sq

m sales floor.

11 rpsgroup.com/ukImpact on Existing, Committed and Planned Public and Private

Investment in Centres Within the catchment Area

4.7 While the rear of the application site falls outside the defined town centre boundary that is solely

because when the boundary was drawn it excluded the Council Depot as a non-town centre

use. The proposed Lidl will clearly function as a town centre store, with the customer entrance

directly off Shirley Road. Accordingly it will constitute a significant investment in the centre and

any impact will be positive.

4.8 We are not aware of any other committed or planned foodstore developments within Shirley

Town Centre, but in any case the impact of a town centre development on other proposed town

centre developments would amount to valid commercial competition, and one of the roles of the

planning system is to contribute towards a competitive economy (NPPF paragraph 7).

4.9 Notwithstanding the above, in terms of the financial impact of the proposed development the

additional turnover that will be generated will modest. The impact assessment set out later in

this report is based around benchmark turnovers, since we have no detailed information on the

actual turnover of existing stores in Shirley (the detailed results of the household survey having

been omitted from the Southampton & Eastleigh Retail Study) – the notional increase in

turnover from the larger store will be in the order of £1.3m for convenience goods and £0.2m for

comparison. However in practice the existing store is known to be trading above its benchmark

level, as referenced in the text of the Southampton & Eastleigh Retail Study (paragraph 9.13).

The replacement store will address this and bring the store turnover down to around the

company average, with the additional floor area providing qualitative improvements such as

improved circulation space. Lidl’s existing customers are expected to switch to the new store

and while the improvements may attract some new shoppers that trade diversion is expected to

be minimal. The development will largely be geared towards providing an improved shopping

experience for Lidl’s existing customers.

Impact on Town Centre Vitality and Viability, Including Local

Consumer Choice and Trade in the Town Centre and Wider Area

4.10 As a starting point it should be acknowledged that as the proposed Lidl will in practical terms be

a town centre store, the requirement to assess its impact is not mandatory. Paragraph 26 of the

NPPF is clear in saying that an impact assessment is required “when assessing applications for

retail, leisure and office development outside of town centres…” [our emphasis]. The proposed

development comprises the relocation of an existing town centre store to another town centre

site, which will actually have a better linkage to the high street.

4.11 Notwithstanding the above, we have undertaken a broadbrush impact assessment, using data

taken from the Council’s ‘Southampton & Eastleigh Retail Study 2011’. This analysis is

provided in the statistical tables included as Appendix 1 of this report.

4.12 The price base adopted for our analysis is 2009, as in the ‘Southampton & Eastleigh Retail

Study’. The design year is 2022, five years ahead being the standard period for impact

assessments.

4.13 Table 1 sets out the benchmark turnover of both the existing and proposed Lidl stores. The

existing store has 991sq m net sales space and assuming Lidl’s company average sales density

(derived from Global Data/Verdict), it’s notional turnover at 2022 is £3.7m, of which £3.2m would

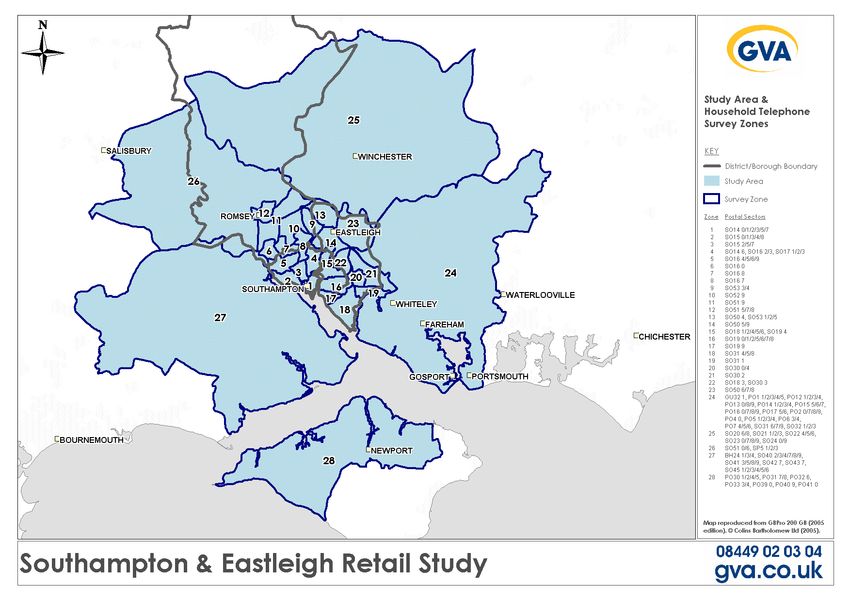

be from convenience goods and £0.5m from comparison. The proposed replacement store will

be 1,401sq m net and will turnover £5.2m at 2022, £4.5m from convenience goods and £0.7m

12 rpsgroup.com/ukfrom comparison. The notional uplift in turnover will therefore be £1.3m for convenience goods

and £0.2m for comparison.

4.14 Table 2 sets out the available convenience goods expenditure across the study area utilised in

the Southampton & Eastleigh Retail Study – this is an area broken down into 28 zones, with

Shirley Town Centre being located within Zone 3. A plan detailing the extent of the study area

is included as Appendix 2.

4.15 Available convenience goods expenditure in each zone for the years 2011, 2016, 2021 and

2026 are taken directly from Table 3 in Appendix 3 of the Southampton & Eastleigh Retail

Study. The figures for 2017 and 2022 have been interpolated by RPS. It can be seen that the

forecast growth within Shirley’s home zone (Zone 3) is £4.3m over the next five years, which will

be well in excess of the £1.3m additional turnover in the larger Lidl.

4.16 Tables 3 and 4 go on to detail Shirley Town Centre’s share of the total expenditure generated

across the study area, in percentage (Table 3) and monetary terms (Table 4). The percentage

market shares in Table 3 are taken directly from the Southampton & Eastleigh Retail Study and

where derived from a household survey undertaken in 2011. From Table 4 it can be seen that

the total spending captured by Zone 3 will grow by £1.99m over the next five years, which is

greater than the £1.3m uplift in Lidl’s turnover.

4.17 Table 5 provides a rough estimate of the impact on Shirley Town Centre from the additional

£1.3m of convenience goods turnover that will be diverted to the larger Lidl store. Such analysis

should normally be undertaken against the actual turnover of existing stores, but in this instance

that data is not included in the Southampton & Eastleigh Retail Study (the results of the

household survey are not appended and none of the capacity tables provide a detailed

breakdown of the survey derived turnover of existing stores). Table 32 in Appendix 3 of the

retail study does provide floorspace and benchmark turnovers for individual stores in each

centre, and we have therefore utilised those turnover figures, projecting them forward to 2017

and 2022 using Experian’s forecast changes in convenience sales densities (from their Retail

Planner Briefing Note 14).

4.18 We assume that all the existing Lidl’s trade will transfer across to the new store, which leaves

£1.3m of additional turnover to be diverted from other shops. This is a worst-case scenario

since in practice the additional floorspace provided in the larger store will in part be used for

qualitative improvements that will improve the shopping environment but may not result in an

uplift in turnover. We estimate that £0.8m of this £1.3m will come from the Sainsbury store,

£0.1m from the Tesco Express and £0.24m from other shops in the centre (which will include

the Iceland). The remaining £0.19m is expected to come from stores outside Shirley. None of

the resulting impacts are significant, with the highest being -4.3% on the Sainsbury. It should

also be noted that the table excludes the Co-op on Shirley Road, which was included in the

retail study but has since closed. The turnover of that store is likely to have been redistributed

to other shops within the centre, which will assist in ameliorating any impact from the new Lidl.

4.19 In relation to comparison goods, the uplift in turnover in the larger Lidl will be in the order of

£0.2m. The likely trade diversion from any existing stores will be minimal and swiftly offset out

by the growth in comparison spending within the City.

4.20 Overall it can be seen that the proposed development will not result in any significant impact on

the vitality or viability of existing stores or centres, while at the same time it will provide a

quantitative and qualitative improvement to Lidl’s offer in Shirley Town Centre.

13 rpsgroup.com/uk5 Summary and Conclusions

5.1 This retail assessment has been prepared by RPS Planning and Development on behalf of Lidl

UK, to accompany a planning application for the replacement of their existing foodstore fronting

Church End in Shirley. The existing store provides 991sq m net sales area and the proposed

new store will increase that to 1,401sq m net.

5.2 With regard to the retail policy elements of the proposal the pertinent facts are as follows:

• The application site is brownfield land within a location accessible by public transport

and walking/cycling and a retail use would therefore conform to national and local

planning policies encouraging sustainable development.

• The proposal complies with the sequential approach to site selection, since:

o The larger store is required in order to provide qualitative improvements to

Lidl’s existing offer, and as a consequence it cannot be disaggregated;

o The application site lies partly within the town centre boundary and one area is

designated as a secondary shopping area;

o The replacement store proposed on the application site will be superior to the

existing store inasmuch as it will have a direct customer access off the high

street, whereas the existing store is on a back-land site. The potential for linked

shopping trips will therefore be greater.

• The larger store will result in only a modest uplift in Lidl’s turnover. Since it will function

as a town centre store any trade diverted from other shops within the centre will be valid

commercial competition and not a reason for refusing planning permission.

Notwithstanding that, the potential levels of trade diversion are not expected to result in

any significant impact on the vitality or viability of any defined centre.

• The improved store will help to sustain Lidl’s important role as a main food shopping

destination in this part of the City.

• The NPPF provides a presumption in favour of economic development that will provide

new employment opportunities. The proposed development will meet these policy

objectives, since the enlarged store is likely to give rise to a need for additional staff, as

well as further job opportunities during the construction phase. Lidl’s policy is, where

possible, to make positions available to local people.

5.3 Having regard to the above conclusions, it can be seen that the proposed development would

conform to both national and local planning policies. Paragraph 27 of the NPPF states that

where an application fails to satisfy the sequential test or is likely to have a significant adverse

impact, it should be refused. Conversely that suggests where it has been demonstrated that

there the development satisfies the sequential test and that there will be no significant adverse

impact, then planning permission should be granted. That would conform to the NPPF’s

fundamental presumption in favour of sustainable development (at paragraph 14), which it says

should be the golden thread running through decision-taking. Since the development satisfies

the sequential test; it is located at an accessible location; it involves a substantial investment in

Shirley and will provide local residents with a larger and more modern store built to the latest

sustainable design; it is likely to create additional jobs; and as it will not result in any significant

14 rpsgroup.com/ukadverse impact on any defined centre, it is clear that the benefits of the scheme clearly

outweigh any adverse impact and consequently in accordance with the NPPF planning

permission should be granted.

15 rpsgroup.com/ukAppendix 1

Lidl UK

Proposed Replacement Store at 390 Shirley Road, Southampton

Table 1: Turnover of the Proposed Development

Turnover of proposed replacement Lidl store

Gross internal floorspace (sq m) 2207

Net sales area (sq m) 1401

Convenience sales area (sq m) 1121

Comparison sales area (sq m) 280

Convenience sales density 2017 (£/sq m) 4035

Comparison sales density 2017 (£/sq m) 2310

Convenience turnover 2017 (£m) 4.5

Comparison turnover 2017 (£m) 0.6

Total turnover 2017 (£m) 5.2

Convenience sales density 2022 (£/sq m) 4003

Comparison sales density 2022 (£/sq m) 2555

Convenience turnover 2022 (£m) 4.5

Comparison turnover 2022 (£m) 0.7

Total turnover 2022 (£m) 5.2

Turnover of existing Lidl store

Gross floorspace (sq m) 1323

Net sales area (sq m) 991

Convenience sales area (sq m) 793

Comparison sales area (sq m) 198

Convenience sales density 2017 (£/sq m) 4035

Comparison sales density 2017 (£/sq m) 2310

Convenience turnover 2017 (£m) 3.2

Comparison turnover 2017 (£m) 0.5

Total turnover 2017 (£m) 3.7

Convenience sales density 2022 (£/sq m) 4003

Comparison sales density 2022 (£/sq m) 2555

Convenience turnover 2022 (£m) 3.2

Comparison turnover 2022 (£m) 0.5

Total turnover 2022 (£m) 3.7

Net increase in turnover from larger store at 2022

Convenience (£m) 1.3

Comparison (£m) 0.2

Notes:

Notional sales density of proposed store is Lidl company average at 2017

derived from Global Data 2017 (formerly Verdict Research), with allowance

for forecast changes in retail sales densities 2017-2022 (derived from

Experian Retail Planner Briefing Note 14).

Expressed in 2009 prices.

JPW0190/171108/Tables v2

08 November 2017Lidl UK

Proposed Replacement Store at 390 Shirley Road, Southampton

Table 2: Available Convenience Goods Expenditure

Zone 1 Zone 2 Zone 3 Zone 4 Zone 5 Zone 6 Zone 7 Zone 8 Zone 9 Zone 10 Zone 11 Zone 12 Zone 13 Zone 14 Zone 15 Zone 16 Zone 17 Zone 18 Zone 19 Zone 20 Zone 21 Zone 22 Zone 23 Zone 24 Zone 25 Zone 26 Zone 27 Zone 28 Total

(£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m)

2011 36.21 31.07 43.12 60.63 57.49 3.16 22.38 12.81 26.07 13.50 2.77 33.75 52.83 28.87 60.75 68.73 27.45 33.84 4.16 23.54 26.71 20.68 39.17 677.83 163.91 51.57 231.34 140.02 1994.35

2016 39.37 32.53 46.92 67.23 60.06 3.37 23.54 13.07 28.35 14.12 2.90 35.26 54.45 31.51 62.87 71.78 28.98 35.26 4.24 24.16 28.00 21.47 40.46 720.62 175.25 53.62 246.34 150.29 2116.01

2017 40.11 32.94 47.76 68.58 60.97 3.42 23.91 13.21 28.92 14.33 2.94 35.76 54.91 32.06 63.68 72.83 29.47 35.64 4.27 24.38 28.32 21.65 40.83 731.86 178.35 54.16 250.23 153.04 2148.53

2021 43.22 34.61 51.29 74.24 64.77 3.63 25.44 13.79 31.30 15.19 3.08 37.81 56.81 34.34 67.03 77.19 31.49 37.21 4.39 25.30 29.62 22.39 42.34 778.62 191.32 56.35 266.42 164.54 2283.72

2022 43.99 35.10 52.09 75.58 65.81 3.68 25.85 13.93 31.87 15.38 3.12 38.31 57.23 34.91 68.02 78.43 32.03 37.60 4.42 25.50 30.06 22.56 42.71 790.35 194.69 56.93 270.39 167.33 2317.87

2026 47.19 37.13 55.43 81.16 70.16 3.88 27.55 14.51 34.25 16.14 3.27 40.38 58.95 37.28 72.15 83.60 34.26 39.22 4.53 26.32 31.90 23.27 44.21 839.05 208.78 59.31 286.85 178.99 2459.70

Notes:

Taken from Appendix 3 Table 3 in 'Southampton & Eastleigh Retail Study' (GVA, July 2011). Figures for 2017 and 2022

have been interpolated by applying compound growth rates 2016-2021 and 2021-2026.

Expressed in 2009 prices.

Table 3: Shirley Town Centre Convenience Goods Market Share

Zone 1 Zone 2 Zone 3 Zone 4 Zone 5 Zone 6 Zone 7 Zone 8 Zone 9 Zone 10 Zone 11 Zone 12 Zone 13 Zone 14 Zone 15 Zone 16 Zone 17 Zone 18 Zone 19 Zone 20 Zone 21 Zone 22 Zone 23 Zone 24 Zone 25 Zone 26 Zone 27 Zone 28

(%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%) (%)

2011 2.7 45.9 45.8 0.0 21.8 0.0 1.9 7.9 0.8 1.6 0.0 0.0 0.8 0.0 0.8 1.2 0.0 0.8 0.0 0.8 0.0 0.8 0.0 0.0 0.0 0.4 0.0 0.0

2016 2.7 45.9 45.8 0.0 21.8 0.0 1.9 7.9 0.8 1.6 0.0 0.0 0.8 0.0 0.8 1.2 0.0 0.8 0.0 0.8 0.0 0.8 0.0 0.0 0.0 0.4 0.0 0.0

2017 2.7 45.9 45.8 0.0 21.8 0.0 1.9 7.9 0.8 1.6 0.0 0.0 0.8 0.0 0.8 1.2 0.0 0.8 0.0 0.8 0.0 0.8 0.0 0.0 0.0 0.4 0.0 0.0

2021 2.7 45.9 45.8 0.0 21.8 0.0 1.9 7.9 0.8 1.6 0.0 0.0 0.8 0.0 0.8 1.2 0.0 0.8 0.0 0.8 0.0 0.8 0.0 0.0 0.0 0.4 0.0 0.0

2022 2.7 45.9 45.8 0.0 21.8 0.0 1.9 7.9 0.8 1.6 0.0 0.0 0.8 0.0 0.8 1.2 0.0 0.8 0.0 0.8 0.0 0.8 0.0 0.0 0.0 0.4 0.0 0.0

2026 2.7 45.9 45.8 0.0 21.8 0.0 1.9 7.9 0.8 1.6 0.0 0.0 0.8 0.0 0.8 1.2 0.0 0.8 0.0 0.8 0.0 0.8 0.0 0.0 0.0 0.4 0.0 0.0

Notes:

Taken from Appendix 3 Table 6 in 'Southampton & Eastleigh Retail Study 2011' (data derived from household survey,

January 2011).

Table 4: Shirley Town Centre Convenience Goods Spending Allocation

Zone 1 Zone 2 Zone 3 Zone 4 Zone 5 Zone 6 Zone 7 Zone 8 Zone 9 Zone 10 Zone 11 Zone 12 Zone 13 Zone 14 Zone 15 Zone 16 Zone 17 Zone 18 Zone 19 Zone 20 Zone 21 Zone 22 Zone 23 Zone 24 Zone 25 Zone 26 Zone 27 Zone 28 Total

(£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m) (£m)

2011 0.98 14.26 19.75 0.00 12.53 0.00 0.43 1.01 0.21 0.22 0.00 0.00 0.42 0.00 0.49 0.82 0.00 0.27 0.00 0.19 0.00 0.17 0.00 0.00 0.00 0.21 0.00 0.00 51.95

2016 1.06 14.93 21.49 0.00 13.09 0.00 0.45 1.03 0.23 0.23 0.00 0.00 0.44 0.00 0.50 0.86 0.00 0.28 0.00 0.19 0.00 0.17 0.00 0.00 0.00 0.21 0.00 0.00 55.17

2017 1.08 15.12 21.87 0.00 13.29 0.00 0.45 1.04 0.23 0.23 0.00 0.00 0.44 0.00 0.51 0.87 0.00 0.29 0.00 0.20 0.00 0.17 0.00 0.00 0.00 0.22 0.00 0.00 56.02

2021 1.17 15.89 23.49 0.00 14.12 0.00 0.48 1.09 0.25 0.24 0.00 0.00 0.45 0.00 0.54 0.93 0.00 0.30 0.00 0.20 0.00 0.18 0.00 0.00 0.00 0.23 0.00 0.00 59.55

2022 1.19 16.11 23.86 0.00 14.35 0.00 0.49 1.10 0.25 0.25 0.00 0.00 0.46 0.00 0.54 0.94 0.00 0.30 0.00 0.20 0.00 0.18 0.00 0.00 0.00 0.23 0.00 0.00 60.45

2026 1.27 17.04 25.39 0.00 15.29 0.00 0.52 1.15 0.27 0.26 0.00 0.00 0.47 0.00 0.58 1.00 0.00 0.31 0.00 0.21 0.00 0.19 0.00 0.00 0.00 0.24 0.00 0.00 64.20

Notes:

Application of market share (from Table 3) to available spending (from Table 2).

Expressed in 2009 prices.

JPW0190/171108/Tables v2

08 November 2017Lidl UK

Proposed Replacement Store at 390 Shirley Road, Southampton

Table 5: Impact on Shirley Town Centre (Convenience Goods)

Conv Turnover Conv Turnover Trade Draw to Resultant Impact

2017 2022 New Lidl Turnover

(£m) (£m) (£m) (£m) (%)

Sainsbury, Redcar Street 18.9 18.8 0.8 18.0 -4.3

Tesco Express, Shirley Road 2.3 2.3 0.06 2.2 -2.6

Existing Lidl, Church End 3.2 3.2 3.2 0.0 -100.0

Proposed replacement Lidl - - - 4.5 -

Other shops in Shirley Town Centre 7.8 7.7 0.24 7.5 -3.1

Stores outside Shirley 0.19

Total 4.5

Notes:

Turnovers of named stores are derived from convenience sales areas in Appendix 3 Table 32 of the 'Southampton

& Eastleigh Retail Study 2011', multplied by 2017 company average sales densities derived from Global Data

(formerly Verdict) that have been projected forward to 2022 using Experian's forecast growth rates for changes in

convenience sales densities (from Retail Planner Briefing Note 14). Sales density of other shops is based on figure

in Appendix 3 Table 32 of the 'Southampton & Eastleigh Retail Study 2011', projected forward to 2017 and 2022.

Turnover of existing and proposed Lidl stores assume the company average sales density for 2017 from Global

Data, projected forward using Experian growth rates (as per Table 1).

Totals may not tally due to rounding.

Expressed in 2009 prices.

JPW0190/171108/Tables v2

08 November 2017Appendix 2

You can also read