Renewables in Ukraine - KPMG in Ukraine July 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Renewables in Ukraine KPMG in Ukraine July 2019

Table of Contents Foreword 3 A Global Perspective 4 Ukraine Overview 7 A Greener Future for Ukraine 8 International Investment 10 Plans for Growth 12 Investment Opportunities 14 KPMG in Ukraine, Local Knowledge, International Experience 18 Appendix - Macroeconomic Indicators 19 2 Renewables in Ukraine

Foreword

Ukraine’s Renewables Investment still secure the Green Tariff provided should be manageable, subject to the

Boom that projects have obtained land use capacity offered at each auction, as

rights, a grid connection agreement, advances in technology continue to

The Ukrainian government has a construction permit and a power reduce generating costs.

committed to increase renewables from purchase agreement (PPA) in the new

around 4 per cent of the energy mix format by 31 December 2019. We expect the investment climate

today, to 25 per cent by 2035. for Ukrainian renewables to remain

Passing of Ukraine’s Auction Law favourable. Indeed, the government’s

While hydropower dominates the for alternative energy sources in 2035 energy mix target will require

country’s renewable capacity, averaging April 2019 follows a well-trodden significant, and sustained investment

4.6GWp over the last decade, installed path. Use of auctions to manage in new renewable capacity, storage and

wind, solar and bio energy capacity supply to a national grid has become transmission networks.

increased by 54 per cent to 2.1GWp in commonplace in recent years.

2018 alone, with a further 4.6GWp of Overall, the outlook for the renewables

capacity in the pipeline. According to research by the sector in Ukraine looks bright.

International Renewable Energy Development of the sector has been

Much of this growth and pipeline, Agency (IRENA) the number of rapid in recent years, and will continue

particularly in wind and solar, has been countries that have adopted renewable in the years ahead, although investors

fuelled by a rush to secure the Green energy auctions increased from six in should carefully assess the impact of

Tariff, which will be replaced by an 2005 to more than 67 by early 2017, and the new auction regime.

auction-based regime from 2020. continues to rise.

Introduced in 2008, the Green Although the auction regime will

Tariff provides highly attractive and undoubtedly lower returns on

guaranteed Euro-denominated rates investment, compared to those offered

until the end of 2029. Investors can by the Green Tariff, any reductions

Renewables in Ukraine 3

A Global Perspective

Worldwide growth in renewables in 2008-2017 Since the adoption of the Kyoto

Protocol, in 1997, which committed 37

developed nations and the EU-15 to

8.3% CAGR reduce emissions, the international

5,886

5,517 community has set ever more onerous

5,326

5,034 targets for reductions in emissions of

4,723

4,162

4,370 key greenhouse gases. And, despite

3,725 3,857 the USA’s planned withdrawal from the

Paris Agreement, measures to reduce

emissions seem unstoppable.

While hydropower remains the

dominant source of renewable energy,

1,061 1,141 1,228 1,333 1,444 1,566 1,694 1,851 2,011 2,179 with the development of solar and

wind energy, its share has dropped

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

significantly and it currently accounts

Capacity, GWp Production, 1000 GWh Compound annual growth rate for 53 per cent of global renewable

capacity and 69 per cent of power

generation. The share of solar and

Global renewable power Global renewable power

wind has increased to 18 per cent and

capacity generation

24 per cent of total generating capacity

respectively, and we expect these

Hydro 53% 69% numbers to continue to grow.

Plans recently announced by the

Wind 24% 16% European Commission will impose

a range of reforms on the electricity

market from 2025, including an

Solar 18% 6%

end to coal generation subsidies,

and legislative initiatives aimed at

Bio 6% 9% increasing the share of renewable

Total, GWp 2,179 Total, 1,000GWh 5,886 energy to 50 per cent of the generation

mix by 2030.

Note: The difference between renewable capacity and power generation is explained

Globally, the picture is just as positive.

by the different utilisation ratios applicable to each source (approx. 40 per cent for A forecast by the International Energy

hydropower, between 20 per cent and 25 per cent for wind, approx. 10 per cent for solar).

Source: IRENA Agency1, which takes into account

prevailing market conditions and

1

International Energy Agency, 2018

4 Renewables in Ukraine

policy frameworks, expects capacity (LCOE), with the potential to drop to Global levelised cost of electricity

to grow by over one Terawatt (46 per USD0.03 given the right operating (LCOE) generation (USD/kWh)

cent) between 2018 and 2023. Solar conditions. Onshore wind too, has

energy accounts for more than half of seen significant improvement in cost

this expansion, driven by supportive per kWh to a global weighted average 0.36 - 73%

government policies, market and of USD0.06 (LCOE), 23 per cent lower

technological improvements and than 2010, with some projects regularly

0.28

declining capital costs. delivering electricity for USD0.04 per

kWh3 0.22

Long seen as a sector in need

0.18

of subsidy, now, however, those Against this background, worldwide 0.16

technological innovations, enabling investment in renewables has shown 0.13

0.12

policies and economies of scale mean strong growth of 9 per cent CAGR - 23% 0.10

that power generation from renewable from 2010-2017, spurred on in many

sources is increasingly competitive territories by a generous range of 0.08 0 .08 0.08 0.08 0.07 0.07 0.07 0.06

with, and in many cases, less costly subsidies and tariffs, and welcoming

than fossil based or nuclear power.2 regulatory environments. While 2010 2011 2012 2013 2014 2017

developed and industrialised countries

Solar photovoltaic (PV) modules have led the way, emerging economies

Solar Onshore Cumulative

declined in price by more than 80 per have also been active. Investors expect photovoltaic wind decrease

cent between 2010 and 2017 and with to see valuations grow across all

it, the average cost per kWh generated sectors but particularly in solar and

has tumbled by 73 per cent to USD0.10 wind. Source: IRENA

Renewable energy penetration (2017) and growth (2010-2017)

Renewable power capacity, GWp 0% 10% 20% 30% 40% 50% 70% 100%

Asia Europe North South Eurasia Other World

America America Share of renewable energy production in 2017, % of total energy production

Capacity in 2010 389 323 232 149 70 66 1,228

Change 528 189 116 54 27 36 951

Capacity in 2017 917 512 348 203 96 102 2,179 0% 4% 8% 12 % 16% over

CAGR in renewable energy capacity in 2010-2017

2

IRENA (2018) Renewable power: Climate-safe energy competes on cost alone.

3

IRENA (2018) Renewable power: Climate-safe energy competes on cost alone.

Renewables in Ukraine 5

Global M&A in the renewables sector based 1,218-megawatt (MWp) offshore USD5 million, the deal value

has focused on Europe and North wind farm, from Orsted A/S (Denmark) threshold for our database. In 2018

America, which attracted 37 per cent for GBP4.46 billion; Canadian group, the only large deal of the year saw

and 30 per cent respectively of all Brookfield Asset Management’s Syvashenergoprom, which is due to

deal-making activity between 2010 and purchase of Saeta Yield, the Spanish construct a wind plant with a capacity of

2017, despite their significantly lower listed renewable energy company; the between 250 and 330MWp, acquired by

share of installed renewable capacity acquisition of an undisclosed majority Norwegian renewable energy company

(23 per cent and 16 per cent), perhaps stake in Spanish wind farms to solar NBT AS. Post-acquisition activity

reflecting the higher cost base in these photovoltaic plant development has, however, been strong across the

developed markets. The sector attracts and construction business, Eolia sector and we have seen debt raising

interest from both private and public Renovables de Inversiones, S.C.R. S.A. and capital investment measured in

sector investors, who accounted for by Alberta Investment Management hundreds of millions of US dollars,

70 per cent and 30 per cent of M&A Corporation (AIMCo), for EUR600 and as the sector grows we expect

activities respectively. Over 68 per cent million and the acquisition of RTR to see increased activity as local and

of investments were cross-border. Rete Rinnovabile S.r.l. an Italian solar international operators compete for

generator and distributor, by F2i SGR dominance.

A 2017 KPMG Survey4 predicted SpA, an Italian private equity and

that the EMEA region would attract venture capital firm for EUR1.3 billion. However, among the positives, a 2017

up to half of all investment in the KPMG survey5 of 200 senior level

renewable sector in 2018 and indeed By comparison, deals in Ukraine were investors in renewable energy did

approximately 40 per cent of M&A significantly more modest. Interest identify some potential problems,

activities in the renewable sector in in the power and utilities sector has noting that the switch from feed-in

2018 were in this region. Among the however has been predominantly tariffs to an auction-based system

largest deals were the acquisition by focused on renewables. A number was, occasionally, an uncomfortable

Global Infrastructure Partners (GIP), of pre-construction projects secured transition and that valuations were

the US-based private equity firm, of a foreign investment through M&A, creeping up as more and more focus

50 per cent stake in Hornsea 1, the UK- activity but the majority fell below was placed on the industry.

M&A actvities, EURm

11% 11% 6% 4% 8% 13% 11% 24% 12% 15%

19% 14% 21% 16%

26%

36%

24% 31% 20%

46% 44% 9%

34%

32% 35% 35%

39%

55% 32%

54% 36% 31%

55

45

40

29 28

14 14

9

2010 2011 2012 2013 2014 2015 2016 2017

M&A activities, EUR billion Asia Europe North America Rest of the world

Source: Mergermarket, KPMG analysis

4

KPMG, Great Expectations: deal making in the renewable energy sector 2017

5

KPMG, Great Expectations: deal making in the renewable energy sector 2017

6 Renewables in Ukraine

Ukraine Overview

At present, Ukraine generates just 4 per Windtechnology, dominate the Elsewhere, the Solar Chornobyl project

cent of its electricity from renewable Ukrainian wind power market. In should be revered for both its ambition

sources other than hydroelectric the solar renewables sector, CNBM and symbolism. The 1986 Chornobyl

power, and the market opportunities New Energy Engineering, and Rengy disaster was the world’s worst nuclear

for investors are in practical terms, Development are the largest suppliers, accident, leaving thousands of square

limitless, given the country’s stated controlling almost one third of the kilometres of Ukraine and Belarus

desire in the National Energy Strategy, market. uninhabitable, leading to one of

to increase the renewables mix to the largest forced mass-migrations

25 per cent by 2035. This ambitious In both wind and particularly solar, in Europe since the Second World

strategy will require significant outside of the key players, whose War. In a sign of things to come, in

investment in the development of growth plans have thus far been largely early 2018, Solar Chornobyl, a joint

power storage capacity to reduce organic, the market is fragmented and venture between Ukraine’s Rodina and

losses to the grid and imbalances characterised by smaller operators and Germany’s Enerparc AG, brought a

between supply and demand, but we start-ups, many of whom have yet to small solar plant (1MWp) into operation

expect this to be largely resolved upon generate their first megawatt. in the Chornobyl exclusion zone and

liberalisation of the market. Currently, later that year signed an agreement

power storage facilities in Ukraine are During 2018, installed solar power to increase its capacity to 100MWp.

limited to approximately 1,500MWp of capacity increased by 646MWp (87 per Once completed, the project will see

pumped-storage hydroelectricity. cent). Wind power capacity increased Chornobyl restored to the power mix of

by 68MWp (15 per cent) and biofuel by Ukraine, and Solar Chornobyl become

DTEK Wind Power, the renewables arm 13MWp (33 per cent), driven mainly by one of the largest solar power plants in

of the local energy giant, and Wind the Green Tariff mechanism, increased the country.

Parks of Ukraine, which additionally interest from foreign investors, debt

builds equipment under licence financing and insurance cover provided

from German supplier, Fuhrlander by international financial institutions.

Renewables in Ukraine 7

A Greener Future

for Ukraine

In Ukraine, with its dated infrastructure The government stopped importing desire to capitalise on its undoubted

and reliance on fossil fuel generation, gas from the Russian Federation in natural advantages, Ukraine is carving

the ecological case for renewables November 2015 and has since relied on out a niche as a destination for

could not be clearer. Coal fired heating local production, supplies from Europe investment in renewable energy, and in

and electricity generating plants, and and other fuel sources for power and particular, wind and solar power. While

diesel engines, emit tiny particulates heat generation. As early as 2008, the nation’s published energy strategy

that lodge in the lungs and can lead to the government started to stimulate assumes significant development of

serious respiratory illness. In Ukraine, development of wind, solar, biofuel new facilities, there is already much

levels of these PM2.5 particulates, and small hydro energy projects, opportunity for more risk adverse

so-called as they are 2.5 microns or introducing a special Green Tariff, tax investors to take a stake in projects

smaller in size, are, on average, almost and customs reliefs, and incentives for currently in planning or in operation,

twice World Health Organisation (WHO) purchasing locally made equipment. in order to take advantages of the

limits6. Ukraine has pledged to cut its government-backed Green Tariff, which

greenhouse gas emissions by at least Driven both by the necessity to seek sets Euro-linked tariffs through to the

40 per cent from 1990 levels by 2030, alternative energy supplies and by a end of 2029.

under the 2015 Paris Agreement.7

Ukraine's growth in renewable power capacity in 2008-2017

2,118

68

98

1,344

1,079

64

945 961

73 1,419

788 56

47 53 59

558 43 49 52 742

24 531

41 422 428

6 353

124 168

52 60

49 465 533

29 343 368 428 428 433

40 19 25

- 88

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Source: IRENA, NERC (National Commission for State Regulation of Energy and Public Utilities)

Notes: (a) Hydropower capacity includes only capacity from small hydro plants (98MWp) which receive Green Tariff payments, and excludes large scale hydro

generation plants (4,571MWp) and hydro pumped-storage capacity (circa 1,500MW) which are owned and operated by Ukrhydroenergo, a government-

owned generator.

(b) Capacities of renewable energy plants exclude wind and solar plants located on the Crimean peninsula (circa 500MWp), but include the wind farms,

which are not currently operating, in the territories in Eastern Ukraine, currently outside the government’s control.

6

Word Bank, DataBank Micro Data Catalog (2015 data).

7

Reuters, Ukraine cities gear up to run on local clean energy by 2050

8 Renewables in Ukraine

From the outset, local operators were guarantees provided by organisations further investment in storage capacity

keen to start developing renewable such as the European Bank for to ensure that both investors and the

projects to take advantage of the Green Reconstruction and Development government can reap the benefits.

Tariff, and once the benefits became (EBRD), the European Investment Bank

clear, from around 2014, international (EIB), the US-based Overseas Private Alongside Ukraine’s clear natural

operators have seized the opportunity Investment Corporation (OPIC), the advantages, particularly for solar and

to invest in this fast growing sector in International Finance Corporation wind generation, the government is

Ukraine. (IFC), and other smaller lenders and committed to generating 25 per cent

investors, including German banks, of the nation’s power from renewable

By the end of 2018, some 2,117MWp of who together have contributed over sources by 2035. The country also has a

renewable capacity had been installed USD1.4 billion since 2009. fast-maturing regulatory environment,

and further facilities with a combined access to international finance and

capacity of over 3,000MWp are either The recently introduced law, On a workforce with the necessary

at the pre-development or construction Amendments to Some Laws of Ukraine skills and experience to implement

stage, with the aim of capitalising on on Ensuring Competitive Conditions complex projects. Output from wind

the Green Tariff. for Production of Electricity from and solar is expected to grow at 15

Alternative Energy Sources, No. 8449-d per cent (CAGR) to reach 25,000GWh

In the first quarter or 2019, Ukraine (the Auction Law), looks set to continue in 2035, up from 1,600GWh in 2015.

added 861MWp of renewable to keep the momentum up, providing Growth in hydroelectric power will be

capacity, five time more than during for new auction-based tariffs, a more modest but should still reach

the same period in 20188, of which coherent market and a clear strategy for 13,000GWh by the same date, following

almost 700MWp was solar. Investors integrating renewables into the overall overhaul of existing equipment and

worldwide, from Norway’s Scatec, energy mix. A planned integration construction of new generating units at

to China’s CNBM Engineering are with the European grid also raises existing government-owned plants.

recognising the opportunities. They the prospect of international energy

are being helped with funding and sales. The market will however require

Ukraine's power generation in GWh Investment from donors (2009-2018)

25,000

USD639 million

13,000

7,000 USD392 million

1,600

USD203 million

2015 2035

USD73 million

Other

donors USD118 million

Total USD1,425 million

8

Ukraine Business News

Renewables in Ukraine 9

International Investment

International investors are already key of Zophia, will be the largest onshore One of the largest domestic renewables

players in the renewables market, chief wind power plant in Europe. A further operators in the Ukrainian market is

amongst them are CNBM Engineering 4.6GWp of renewable capacity is vertically-integrated energy giant DTEK

with an estimated 22 per cent share currently planned or under construction which, alongside its fast developing

of the solar market in Ukraine with the aim of coming on stream in wind and solar interests is also the

(excluding plants in Crimea) and Rengy the coming years in order to secure nation’s largest coal miner, fossil fuel

Development, a multinational working the highly advantageous Green Tariff. electricity generator and the largest

in Kazakhstan, Armenia and Ukraine, Additionally, NBT, French group, private gas producer. DTEK Wind

which has a 10 per cent share. Total Eren SA and China Power have Power has approximately 40 per cent

agreed to invest USD450 Million in share of the Ukrainian wind energy

Norway-based NBT has signed an construction of a 250MWp wind farm market10. DTEK plans to invest EUR750

agreement with the Unit Venture in Kherson Region, Norway’s Scatec Million in 2018 and 2019 in construction

Investment Fund to develop a EUR1 will shortly bring on line an 83MWp of solar and wind power plans, with

billion, 742MWp wind power plant solar facility, and other local and total generating capacity of 740MWp11.

along the northern shore of the Sea international investors will bring on line

of Azov, in Yakymivka district. This as much as 500MWp of wind power in

development, with the working name the coming years9.

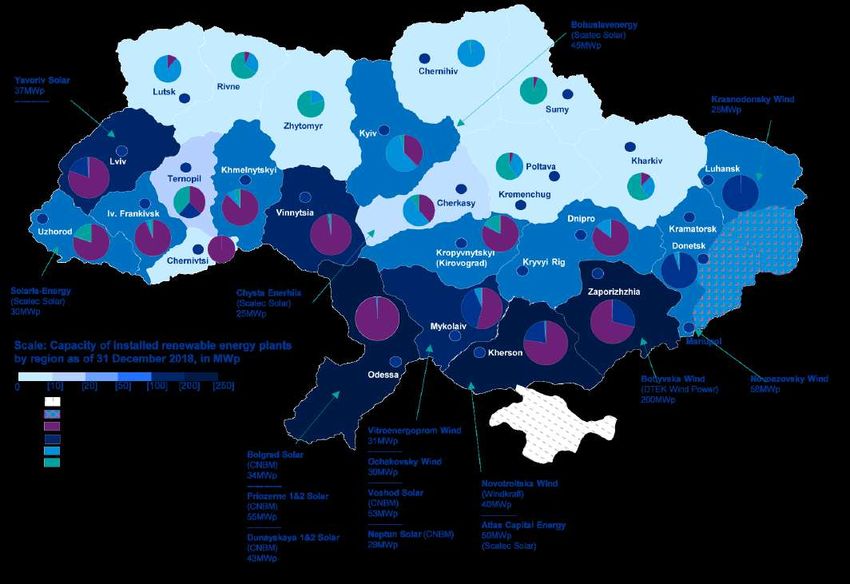

Installed capacity and key projects

Pipeline

Source: NEURC

9

Business News Europe, Ukraine's Renewable Rush

10

Biowatt, Alternative energy, who is interested, where are they investing?

11

Na chasi, Renewable Energy

10 Renewables in UkraineWind energy Solar energy

Installed capacity Pipeline Installed capacity Pipeline

DTEK and

DTEK 200 Zophia 742 CNBM 301 CMEC solar plant 200

Windkraft Ukraine 75 Eurocapewind farm 600 Rengy Development 130 Scatec solar plant 200

Ochakivskiy Wind Pokrovsk solar power

Park 49 Sivashenergoprom 250 Euroimex 21 plant 200

Prychornomorskiy Prychornomorskiy Prychornomorskiy

Wind Park 23 Wind Park 500 Leader 20 Wind Park 100

Other 186 Other 1,360 Other 946 Other 403

Total (MWp) 533 Total (MWp) 3,452 Total (MWp) 1,419 Total (MWp) 1,103

Small hydro Bioenergy

Installed capacity Pipeline Installed capacity Pipeline

None

Synelnykowe

Energiya-1 9 Biogasenergo 18 bioenergy plant 76

Voda Donbassu 4 Smilaenergopromtrans 9 Total (MWp) 76

Other 56 Oriel-Leader 6

Total (MWp) 68 Singa Energis 5

Other 60

Total (MWp) 98

Sources: information in the public domain, NEURC

Renewables in Ukraine 11Plans for Growth

In June 2017, backed by assistance development without significantly or approval by state bodies13. According

from the governments of Germany, affecting domestic bills. Pilot auctions to some estimates, this legislation will

Switzerland and Slovenia, Zhytomyr are due to be held by 31 December result in UAH5-10 billion in cost savings

became the first Ukrainian city to 2019. Regular biannual auctions are for renewable energy providers.

adopt a target of using 100 per cent planned from 2020.

renewable energy by 2050, with plans Work is already in hand to synchronise

for a solar plant generating up to In a further boost for the sector, other the Ukrainian power grid with

30MWp. Three other Ukrainian cities, recently introduced changes to the Europe’s ENTSO-E14 which alongside

Kamianets-Podilskyi, Chortkiv and Lviv Tax Code of Ukraine additionally grant providing much needed redundancy

have since come on board12. VAT exemption on imports of certain in the system, will also allow effective

wind and solar equipment (wind power competition in the domestic electricity

Ukraine plans to increase energy from units, PV cells, certain liquid dielectric market, with inflows from international

renewable sources from 4 per cent transformers and static convertors). providers, while providing access to EU

in 2015 to 12 per cent by 2025 and to markets for Ukraine’s nuclear power

25 per cent by 2035. This growth is There are also changes to land zoning, plants and renewable generators.

dependent on necessary developments such that until 31 December 2022, Completion of these works would

to the regulatory environment and developers of solar and wind projects enable Ukraine to disconnect power

access to international finance. Growth will no longer have to seek change of links with the Russian Federation.

so far has been driven in large part use designation for land previously

by the adoption of a Green Tariff, designated as industrial, transport, This internationalisation of the

introduced in 2008, which guarantees telecommunications or military. Further, market will increase the investment

prices until the end of 2029 for construction of wind plants has been attractiveness of Ukraine’s power

electricity from renewable sources, given an SS1 classification, meaning sector and hence encourage investors

brought online before the end of 2019. that work can be undertaken without a to commit to new renewable energy

Thereafter, the recently introduced specific construction permit and works operations.

Auction Law will drive further undertaken are not liable for inspection

12

Reuters, Ukraine cities gear up to run on local clean energy by 2050

13

EBA, VAT exemption for import of certain wind and solar

14

Ukrenergo, Integration to ENTSOE

12 Renewables in UkraineForecast power generation (billion kWh)

185 195

178 25

164 164 18

12 Nuclear

2 9

12 13 13

7 10

63 Coal thermal

68 64 63

60

Hydro

88 85 91 93 94

Solar and Wind

2015 2020 2025 2030 2035

Forecast structure of Ukraine’s energy supply

4% 8% 12% 17% 25% Solar and Wind

1.2% 2.4%

5.5% Heat and Geothermal

4.9% 10.4%

11.6% 6.9%

11.5% 8.8%

9.2% Hydro

8.2% 11.5%

25.5% 7.3%

29.3% Biofuels and waste

32.2%

29.7%

25.0%

Oil products

28.9%

29.3% Nuclear

31.0% 30.8% 30.2%

Natural Gas

30.0%

22.0%

16.1% 14.3% 12.5% Coal

2015 2020F 2025F 2030F 2035F

Total renewable energy sources

Source: Energy Strategy of Ukraine through to 2035

Renewables in Ukraine 13Investment Opportunities

Investors looking to enter the Ukrainian energy auctions increased from six in – The introduction of wind and solar

market have two options: either invest 2005 to more than 67 by early 2017, and power into the system is likely to

into existing projects benefitting from the process continues. create imbalances, as output is

the Green Tariff, or invest into projects dependent on weather conditions.

that will operate under the new Auction The Auction Law, introduced in April Nevertheless, winning bidders

Law. 2019, has the following key features: will bear limited or no liability for

imbalances between 2020 and 2030

Green Tariff – Regular biannual auctions are if their projects are commissioned

planned from 2020. Pilot auctions prior to the introduction of a

Introduction of the Green Tariff in 2008 are due to be held by 31 December liquid intra-day market or 2024,

kick-started Ukraine’s alternative energy 2019. Quotas will be set annually whichever is sooner.

market, by providing guaranteed Euro for the following five years and

denominated prices per kWh until the will be split into wind, solar and – There will be no retrospective

end of 2029. other RES. In the meantime, legislative changes for power

the government may conduct plants commissioned before 2020.

However, in order to secure the technology neutral auctions

attractive Green Tariff (currently or introduce special quotas for – The Green Tariff will be reduced by

EUR0.15 per kWh for ground solar particular projects. 25 per cent for solar plants in 2020

plants, EUR0.16 for rooftop solar and a further 2.5 per cent annually

plants, and EUR0.10 per kWh for wind – From 2020, solar power plants between 2021 and 2023. For wind

farms of more than 2MWp) investors with a generating capacity plants the reduction will be 10 per

must ensure that power plants are exceeding 1MWp and wind cent in 2020 with no further annual

commissioned by 31 December 2019. plants exceeding 5MWp (unless reduction. The Green Tariff will be

operating three or fewer turbines) further reduced for solar and wind

Even if commissioned after 31 must take part in auctions. Those projects commissioned from

December 2019, certain large solar and plants subject to the grandfathering 1 January 2024.

wind projects can still benefit from the rule (see left) are excluded from

Green Tariff, albeit at reduced rates. these requirements. Annual power production quotas for

Large solar and wind projects are not renewables will be set by the Cabinet

required to participate in auctions, – Auctions will use the ProZorro of Ministers, based on proposals

under the grandfathering rule, provided platform. Bidders will submit from the Ministry of Energy and the

they have secured rights to land closed bids which contain a Coal Industry, which will themselves

plots, a grid connection agreement, a technical bid (noting the capacity be founded on consultations with

construction permit and a PPA in the bid for) and bid price (per kWh) Ukrenergo, the electricity Transmission

new format in place by 31 December with the key criteria being System Operator (TSO), and the State

2019. Such developments have two price. Auction prices may never Agency on Energy Efficiency and

years (solar) and three years (wind) exceed those paid on the Green Energy Saving of Ukraine. The new

to complete construction in order to Tariff. These prices will be valid system should ensure that the TSO

benefit from the Green Tariff. for 20 years from the date of is better able to manage the already

commissioning of the power plant. discernable constraints related to the

Auction Law integration of renewable supplies with

– Bidders must provide a bank the power system. Ukrenergo has

Use of auctions to manage supply guarantee equivalent to EUR5,000 outlined three scenarios for the amount

to a national grid have become for every 1MWp bid for, before the of solar and wind energy the system

commonplace in recent years. start of the auction and a further could absorb and which balancing

According to research by the EUR15,000 for every 1MWp as a power generating capacities would be

International Renewable Energy performance bond, if they win the needed in the system.

Agency (IRENA) the number of auction.

countries that have adopted renewable

14 Renewables in UkrainePower Production Quotas

Scenario A Scenario B Scenario C

In this scenario, electricity generation The share of nuclear power plants Forecasting and management

by wind and solar power plants would in total power generation would be systems and 2.5GWp of balancing

be constrained, whilst additional limited and the growth of balancing capacities (gas piston plants and

balancing capacities are installed. The power generation capacity would be batteries) would be installed,

ability of the system to forecast and ensured by means of coal-fired power giving unhindered development of

manage variability in power generation plants. The development of ‘green’ renewable energy. Nuclear generation

would remain unchanged. generating capacipty would be not would increase and coal power plants

limited. reduce output.

Ukrenergo favours Scenario C, which they believe will meet the needs of both consumers and suppliers, and restrain

electricity tariffs for domestic and industrial consumers. Ukrenergo estimate the investment required to put this scenario

into operation is UAH55 billion (USD2 billion), with a 6-year payback period.

Project development map under the Green Tariff

Project development map under the Auction Law

Source: KPMG analysis

Renewables in Ukraine 15The EMEA region is expected to show A joint venture or investment in an Green Tariff and Auction Law, the

the biggest increase in M&A in the existing licenced solar or wind operator, grid is obliged to take every MWh

worldwide renewables industry in 2019. even one not yet generating (as long generated.

Research commissioned by KPMG16, as the project has an agreed pre-

exploring the views of business leaders PPA) is a viable option for an investor The government’s stated aim that

and industry experts showed that fully looking to secure access to Green Tariff by 2035, 25 per cent of all electricity

47 per cent saw Europe as the focus advantages. Those looking to develop will be generated from renewables

of worldwide growth, and we expect a greenfield operation should take a should ensure that auctions, whilst

Ukraine to play its part in that growth. longer term view of the market and competitive should not be too onerous,

be aware of the administrative and although this will of course depend on

During 2018 Ukraine’s renewable legislative hurdles. the capacity put out for tender at each

sector (excluding hydropower) saw 54 auction, and whilst return on capital

per cent growth in terms of installed An investment in a ready-to-build employed is currently exceptional for

power capacity, from 1,375MWp as at 1 pre-approved solar project, could see Green Tariff operators, auctions would

January to 2,117MWp at 31 December. power generation inside six months, deliver tougher competition to the

This capital investment and the at a cost of around USD750,000 or less market. Ukraine’s recently introduced

introduction of further capacity in 2019 per megawatt installed. Auction Law is a continuation of the

is sure to generate increasing interest global trend, following significant

in M&A activities in the sector. Without doubt, however, wind projects experience from other countries such

must be planned on a longer timescale. as Mexico, Argentina, Chile, Brazil,

The market is complex but at KPMG By their very nature, many of the Peru, Germany, UAE, Zambia, India,

we have the skills and experience prime locations for wind energy are China, and the Russian Federation, that

to guide you smoothly through the often remote and difficult to access, have made the switch to auctions, to

acquisition process, providing you with presenting the operator with logistical ensure that the system runs smoothly.

comprehensive advice at all stages of challenges unlike those for a solar

the process, including identification and project. Additionally, lead times for However, as renewables make up an

evaluation of investment opportunities, feasibility studies and fabrication of increased share of power generation,

conducting legal, financial and tax due towers and turbines can be lengthy and significant investment will be required

diligence of selected opportunities, delivery to site may require changes to into the grid and power storage

pricing analysis, support in negotiation local transport infrastructure. projects, and if growth is to remain

of the deal and related transaction unconstrained by technical bottlenecks,

documents (e.g. sale and purchase Both wind and solar plants however, the government will need to approve

agreement) and post-acquisition are guaranteed a connection to the storage and balancing plans, such as

support. electricity grid and under both the those favoured by Ukrenergo.

16

Great Expectations: Deal making in the renewable energy sector

16 Renewables in UkraineInvesting in any market is a complex Potential entry options

decision, irrespective of existing

international footprint and risk appetite Establishing a new company from The most time-consuming

a business may have. Before entering scratch (greenfield). This requires, option which requires

as a first step, a search for land with substantial contracting

the Ukrainian market, an investor 1 easy access to the electrical grid and workflows and a thorough

should develop a clear investment obtaining land lease agreements from understanding of the limitations

local communities or state authorities of the existing power grid

strategy, based on a thorough

assessment of not only country risks

but also the commercial, financial

and project risks specific to each

This option may allow an

opportunity. All investment strategies investor to take advantage of

Acquiring an existing company that

have their own set of specific risks and already has some of the required land the Green Tariff if a pre-PPA has

2 been signed. Time to market

rewards, and it is important that all use agreements and permissions

should be substantially shorter

stakeholders, including the board and than option 1

shareholders, are aligned.

In the Ukrainian renewable energy

market, investors should be particularly This option allows an

investor to generate return on

aware of the timing of their investment, Acquiring an operating renewable investment immediately and

3

given the change from the Green Tariff energy plant, already supplying power benefit from the Green Tariff.

to the grid However returns are likely to

and its associated guarantees and be lower

incentives, to the new Auction Law.

Whichever route you decide to take, it is essential to engage suitably qualified professional advisors to navigate you through

the investment process. Legal, financial and tax advisors with a deep understanding of the local business environment and

extensive experience in the renewables sector are a prerequisite to ensure that investors mitigate risks and avoid common

pitfalls, and maximise opportunities during the investment process and throughout the entire lifecycle of their investment.

Different investment options are associated with different risks and rewards for an investor

1 year

Launch from

Entry options: Buy Joint venture

scratch

Financial options: Equity vs. loans

Feasibility study

M&A process

Environmental assessment

Land allocation

Grid connection agreement

Due diligence

pre-PPA

Approval of the project

Project development:

Equipment purchase

Valuation

Raise required additional capital

Construction of a plant

Connection

Deal structuring

Obtain electricity production licence and green tariff

Maintenance

Project operation:

Reports

Sell/refinance debt on Operate during the

Exit options Gradual sale

the plant’s launch lifecycle

Renewables in Ukraine 17KPMG in Ukraine

Local Knowledge,

International Experience

KPMG has been present in Ukraine you throughout the process. We can knowledge, while our international

since 1992, and works closely with both support you, from market entry strategy network of member firms provides

project owners and investors in the and identification of suitable targets, access to the latest developments and

renewables sector. through to legal, financial and tax due insights from the global renewables

diligence, as well as preparation and sector.

Whether you are considering negotiation of transaction documents.

investment into a greenfield or existing At KPMG we focus on helping our

project, KPMG in Ukraine has the Our teams of specialists combine clients to maximise the value of their

experience and expertise to advise local experience with deep sector investment, both on entry and exit.

Credentials

Scatec Solar European Investor Chinese Investor Czech investor Turkish industrial

group

Financial due diligence Financial, tax and legal Financial, tax and legal Due diligence on two Pre-investment legal

on five solar power due diligence on seven due diligence on a wind solar power generating due diligence on

generating plants in solar power generating power generating plant plants in Ukraine construction projects

Ukraine plants in Ukraine. in Ukraine for solar power

M&A support generating plants in

Ukraine

2018 2018 2018 2018 2018

IB Vogt Wind Power LLC Confidential DTEK DTEK

DTEK

Legal and tax support Legal, financial and tax pre- Full-scope tax due Comprehensive tax Analysis of, and

for the acquisition and investment due diligence diligence on companies diagnostics on selected comments on, tax

development of a solar for a construction projects operating wind and companies belonging assumptions in a

power plant in Ukraine for a wind power plant solar power plants to the largest Ukrainian financial model for debt

with expected capacity energy holding raising purposes

300MWp

2018 2015 2018 2017-2018 2017-2018

Primorskaya Wind Confidential DTEK Confidential

Electric Plant Mainstream

Valuation services Financial, tax, legal and Assistance in Valuation services Financial and tax due

provided to customs due diligence connection with diligence on three

Primorskaya Wind on three solar power debt financing for solar power generating

Electric Plant LLC generating plants in the purposes of plants in Ukraine

Russia construction of a wind

park

2017 2017 2017 2018 2016

18 Renewables in UkraineAppendix

Macroeconomic Indicators

Ukraine's macroeconomic indicators1 2016 2017 2018 2019 2020 2021 2022

Real GDP growth, per cent y.o.y. 2.4 2.5 3.3 2.8 2.1 2.6 2.7

Nominal GDP, USD billion 93.4 112.2 127.9 138.2 157.6 178.0 199.9

UAH/USD exchange rate (end-period) 27.2 28.1 27.7 28.8 29.3 29.5 29.7

Consumer price index, per cent y.o.y 12.4 13.7 10.3 7.8 8.0 7.5 6.8

Population, million residents 42.5 42.4 42.2 42.0 41.8 41.7 41.5

Net direct investments, USD billion 3.3 2.6 2.8 3.2 3.7 4.6 5.6

FDI stock, USD billion 69.0 59.9 54.9 53.4 49.3 46.5 44.4

Total foreign debt, USD billion 114.7 113.3 116.8 119.1 122.2 124.9 128.5

Doing Business Index2 83rd 80th 76th 71st

Global Competitiveness Index3 85th 89th 83rd n/a

Moody’s Sovereign Debt Rating 4

Caa3 Caa2 Caa1 Caa1

EBA Investment Attractiveness Index5 2.85 3.03 3.07

Sources:

1

Economist intelligence unit

2

The World Bank - Ease of doing business index

3

WEF – Global Competitiveness Report

4

Moody’s Sovereign Debt Rating

5

EBA Investment Attractiveness Index

Glossary

Wind energy Solar energy Hydro energy Bioenergy

CAGR – Compound annual growth rate

GWh, MWh, kWh – Units measuring power generation output: Gigawatt hours, Megawatt hours, Kilowatt hours

GWp, MWp – Units measuring power generation capacitiy: Gigawatt Peak, MegaWatt Peak.

LCOE – Levelised cost of electricity is the ratio of lifetime costs to lifetime electricity generation, both of which are discounted

back to a common year using a discount rate that reflects the average cost of capital (according to IRENA data)

IRENA – The International Renewable Energy Agency, an intergovernmental organisation

M&A – Mergers and acquisitions

PPA – Power Purchase Agreement

pre-PPA – Preliminary Power Purchase Agreement

RES – Renewable Energy Sources

TSO – Transmission System Operator

DSO – Distribution System Operator

Renewables in Ukraine 19Contacts

Dmytro Shchur Yuriy Katser

Director, Director,

Transaction Services Tax and Legal

dshchur@kpmg.com ykatser@kpmg.ua

+380 44 490 5507 x34195 +380 44 490 5507 x34051

Peter Latos Maksym Zavalnyy

Partner Director,

Head of Advisory, KPMG in Ukraine Tax and Legal

peterlatos@kpmg.ua mzavalnyy@kpmg.ua

+380 44 490 5507 x34150 +380 44 490 5507 x34566

kpmg.ua

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity.

Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is

received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a

thorough examination of the particular situation.

© 2019 KPMG-Ukraine Ltd., a company incorporated under the Laws of Ukraine, a member firm of the KPMG network of independent member firms

affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity.

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

20 Renewables in UkraineYou can also read