REAL ESTATE IN ROMANIA & POLAND - 2021 Comparative Market Evolution Office, Retail, Industrial & Residential Financing & Legal Aspects ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

REAL ESTATE IN

ROMANIA & POLAND

2021

Comparative Market Evolution

Office, Retail, Industrial & Residential

Financing & Legal Aspects

Construction & Services

Dear Reader,

Welcome to the 2021 edition of “Real Estate in Romania & Poland”. This report

is the result of over six months of research and interviews with more than one

hundred investors, developers, consultants and key service providers, many a

friendly face on the now extremely familiar Zoom or MS platforms, and some

smiling from behind a mask, across a conference table. We witnessed the

full range of pandemic emotions during our research, from quiet lockdown

patience, to cabin fever-ish anticipation, and eventually regained hope

Business and gratitude for a return to (almost full) freedom. There is one sentiment,

intelligence however, that prevailed throughout, and helped anchor people and maintain

their drive: confidence in their field of work, in both Poland & Romania’s

you can resilient and rapidly developing real estate segments.

trust The following pages will give you a bird’s eye view over the two countries’

potential across the office, retail, industrial and residential segments. Three

decades after the fall of communism, and with a mosaic like architecture,

Poland and Romania are still rebuilding, reshaping and modernizing their

infrastructure to keep up with increasingly sophisticated demands from their

populations.

Generous yields (well above those of Western Europe), coupled with economic

and wage rises, make both countries enviable investment destinations. From

this comparative analysis, Poland’s headstart does emerge (and is visible

enough through its skyline that will boast Europe’s tallest office building as

of this year), offering a mirror into Romania’s future. But the latter also stands

out as a hidden gem, previous weaknesses surfacing now as clear strengths.

get in touch

www.investmentreports.co

info@investmentreports.co

Enjoy the report!

Irina Negoita Sorina Dumitru

Co-Founder & Co-Founder &

Director Lead Editor

table of contents

INTRODUCTION deveoplment & investment

LEGAL ASPECTS

8. A Tale of Two Countries 88. Romania’s Legal Environment

12. Macroeconomics 91. Interview Bucharest City Hall & Interview F&R Worldwide

14. Real Estate Markets at a Glance 92. Poland’s Legal Environment

16. Interview AREI (The Association of Real Estate Investors in Romania)

18. Interview PINK (The Polish Chamber of Commercial Properties)

19. Interview PAD (Polish Association of Developers)

20. Expert Opinion Article: Outlook for 2021, Deloitte Romania

CONSTRUCTION &

KEY SERVICES

96. A Post Pandemic Construction Hype

Market EVOLUTION 98. Interview Concept Structure

24. Romania: Low Risk, High Reward 99. Interview CON-A Group

27. The Office Market in Romania Despite the global pandemic, the Real Estate 100. Interview BTDConstruct & Ambient

29. Interview S IMMO & Interview CA Immo markets of Poland and Romania continue to 101. Interview PORR & Interview Construcții Erbașu

30. Interview Globalworth Group offer enviable returns across all sectors. 102. A Historical Price Surge for Building Materials

31. Interview One United Properties & Interview Forte Partners pp. 24 - 72 104. Interview Etem

32. Interview Speedwell 105. Interview Wienerberger Romania

34. The Retail Market in Romania construction & services 107. Interview Rustler Romania

35. Interview Argo Capital Management Property & Interview IMMOFINANZ 108. Interview KONE ASCENSORUL

36. Interview NEPI Rockcastle & Interview Sonae Sierra

37. Interview AFI Europe & Interview Iulius Group

38. The Industrial Market in Romania

40. Interview CTP & Interview VGP 110. FINAL THOUGHTS

42. Expert Opinion Article: Logistics & Land Development, Crosspoint

44. Interview ARILOG (Romanian Logistics Association)

45. Interview DP World Constanța

46. The Residential Market in Romania 112. COMPANY INDEX

48. Interview Impact Developer & Contractor

49. Interview One United Properties & Interview Hagag Development Europe

50. Poland: Taller by the Day

51. The Office Market in Poland

53. Interview Immobel Poland Poland and Romania host world class

54. The Retail Market in Poland construction giants, a full array of service

56. Interview EPP Group providers and generous workforce.

57. The Industrial Market in Poland pp. 96 - 108

60. Interview Fortress REIT

61. Interview SEGRO

62.

64.

The Residential Market in Poland

Four Major Trends in Real Estate

exclusive interviews

68. Interview Siemens

70. Interview Bright Spaces

71. Interview Sixense Romania

72. Expert Opinion Article: Green Buildings, NAI Romania

INVESTMENT & FINANCING

76. Investment Volumes and Pipeline in Romania & Poland

78. Interview UniCredit Bank

80. Expert Opinion Article: REITs in Romania & Poland

82. Interview Zeus Capital Management Dimitris Raptis Tomasz TRZÓSŁO Magdalena SZULC Fulga DINU

84. Expert Opinion Article: Green Financing, NNDKP CEO CEO Managing Director CE Country Manager RO

Globalworth Group EPP Group SEGRO IMMOFINANZ

p. 30 p. 56 p. 61 p. 35

INTRODUCTION Referring specifically to Romania and Poland, we are extremely selective when it comes to our investment decisions and we always make a thorough assessment of risks and opportunities when starting a new venture. Because these two countries have the biggest and fastest developing markets in CEE, it was a natural decision to run business here. If you factor in the “country risk”, both Romania and Poland are not yet at the safety level of Western European countries, however, property investments have a special profile here. All CEE countries are ahead of other European states from a growth potential point of view because the workforce is not as expensive. In addition, since they are slightly underdeveloped technology wise, we can turn this challenge into an opportunity and build from zero state-of-the-art projects that meet the highest ecological standards (e.g., photovoltaics, use of rainwater, etc.) Maciej TUSZYNSKI Managing Director Europe Fortress REIT

INTRODUCTION investment reports investment reports INTRODUCTION

Allow us to take you on a brief walking

right: Palace of Science and Cultue Warsaw, ©Valik Chernetscki

left: Bucharest Atheneum, © Pelayo Arbues

tour of the two countries’ capitals and

fast growing secondary cities, as part

of the present business assessment

study that looks over the residential,

retail, industrial and office segments

alike. The pandemic that we are all still

navigating naturally had wildly differing

effects on them, that are still rippling

through the industry segments, but by

and large after a few months of “wait

and see” businesses forged ahead, even

thriving in areas such as residential

and industrial. Poland has been in the

limelight more than Romania, however,

by speaking to over 100 savvy

developers, investors and key service

providers, our conclusions clearly show

that both countries’ property markets

A TALE of are still investment-wise diamonds in

the rough, with demand increasingly

TWO COUNTRIES

outstripping supply.

the two DISTINCTIVE SHAPES OF A

most STRONG PORTFOLIO

The year 2019, or the last year of the “before times’’, marked 100 years since Poland and Romania officially

established diplomatic relations. Poland was the first state to recognize the unification with Transylvania, populous

making the two Central and Eastern Europe’s largest population pools. And what a century it has been! Both countries

countries have rich histories, spanning feudal societies, monarchies shattered and reborn, several decades in cee

under the iron first of communism, all culminating with the modern post 1989 era of democratic rule and

In order to understand Poland’s and

gradual internationalization. All these historical shifts left a cookie trail of architectural and infrastructure

Romania’s property and infrastructure

influences, resulting in a true mosaic of the countries’ respective real estate industries. evolution, let’s take a quick look at their

main real estate hubs - their capital

cities. From a bird’s eye view Bucharest

and Warsaw can have a similar vibe

source: Eurostat with their large communist style

boulevards and grey-tinted, imposing

POLAND buildings, mixed with historical and

patrimony ones, meandering streets

and roundabouts. But upon entering

Warsaw one is immediately hit by

popULATION: 37.9 mil the city’s impressive, US reminiscent

GDP/capita: EUR 12.680 skyline, testament to the country’s

MEDIAN MONThLY INCOME: ROMANIA swift economic overhaul of the past

three decades, well ahead of Romania’s

EUR 1.275

that in certain ways looks at Poland

popULATION: 19.3 mil as a mirror to the future. This is

POLAND energy industry 2020

GDP/CAPITA: EUR 8.780 mainly due to the latter’s success in

attracting foreign capital, absorbing

MEDIAN MONThLY INCOME: EU funding and developing a robust

EUR 750 Central Business District and dynamic

industrial ecosystem.

www.simmoag.ro

www.simmoag.at

8 ROMANIA & POLAND REAL ESTATE 2021 ROMANIA & POLAND REAL ESTATE 2021 9

INTRODUCTION investment reports investment reports INTRODUCTION

BUCHAREST WARSAW

A CITY OF CONTRASTS the indestructible phoenix

Bucharest went through a flourishing period Warsaw is notable among Europe’s capital cities not so much for its

in the 19th century, when Western style size, its age, or its beauty but for its indestructibility. It is a phoenix

influences combining romanticism and that has risen repeatedly from the ashes of war.

neoclassical elements earned it the “Little

Paris” label, boasting its very own Arch of Warsaw and Poland’s urban landscape went through a swathe of

Triumph. Emblematic buildings such as the historical phases, with the capital city harboring a number of stories

Atheneum, Cantacuzino Palace, Cotroceni and styles including gothic, renaissance, baroque, and neoclassical. St.

Palace (current presidential abode) or the John’s Cathedral from the 14th century is one of many remarkable

Palace of Justice were erected during this places of worship, and baroque style beauties such as Wilanow Palace

period. The city kept developing in the or Kazimierz Church stand as remnants of the Polish-Lithuanian

interwar period, with Art Deco buildings such kingdom.

as the Telephone Palace and functionalist

ones like the Bucharest North Railway station top: Bucharest, City Center, 1930

© Alex Gâlmeanu, Muzeul de Fotografie

or the National Bank of Romania taking shape. right: Pretzel vendors in uniform in front of Warsaw, 1890

the Arch of Triumph, 1950, © Nicolae Ionescu “Varsovie Le Chateau de Vilanov”, © Monovisions Photo Magazine

The second half of the 20th century bore the mark of The city went through an enlargement

Ceaușescu’s communist ideals, building up residential phase in 1916 when many housing

neighbourhoods to accommodate the cities’ fast paced estates popped up, housing workers,

industrialization and igniting a wave of urban migration. writers and army officials alike. By and

His visits to North Korea and China birthed ambitions large, however, Warsaw is not all that

of wide boulevards and buildings such as the grandiose meets the eye - it suffered great losses

Palace of Parliament, to this date the largest administrative during WWII when most of the city was

building in the world after the Pentagon, for which many bombed, and had to be rebuilt from the

of Southern Bucharest’s historical buildings and center ashes, at times respecting buildings’

top: Warsaw City Center, 1955,

had to be demolished and much of the city rebuilt. The original designs, at others bending © Warsaw Institute

main feature of this epoch, however, are the dull, solemn some according to socialist realist

left: Warsaw, Stary Rynek Market Square, 1945,

and cramped blocks of flats, whose future is boggling the architecture. © ilovepoland.net

minds of present day urban planners.

Bucharest, Palace Hall, 1960, postcard

The post communist era spanning the past BUCHAREST WARSAW

three decades witnessed the rise of glass BUSINESS BUSINESS

and steel architecture and the (slow, initially

Wild West style in the 1990s) rise of office

district district

buildings, malls and retails centers, modern

residential buildings, and more recently Bucharest’s dominant business The Palace of Science and

industrial and logistics centers in the city’s area is located in the Northern Culture, the tallest building

outskirts. This is a period marked by heavy part of the city. The district in Warsaw (230 m) is now

privatization and foreign investment, concentrates most of the city’s surrounded by modern

accelerated by the country’s joining of the upcoming developments. skyscrapers.

EU in 2007. The saying goes that out of

chaos beauty is born - and as poetic as that

sounds, Bucharest’s story finds us in 2021 © The New York Times

in the midst of a jumble of eager, not always Warsaw’s tallest building remains the (in)famous 1950s Palace of Science and Culture, a so-called Communist skyscraper that

well integrated construction projects, and SkyTower, used to tower over an otherwise mostly flat city with its 230 m. The city also makes one stop and stare at the Stalinist style

authorities that bear on their shoulders the the tallest building in large boulevards and brutalist buildings. Starting with the 1990s however, the city slowly developed its own skyline, to rival

Bucharest ( 137m)

mission of rethinking the city’s overall urban that of London, Paris or Frankfurt in height and modernity. The Palace of Science and Culture’s dominance will be overthrown

development future. in 2021, when Varso Tower’s whooping 310 m will make it not only Poland’s but the entire EU’s tallest building.

10 ROMANIA & POLAND REAL ESTATE 2021 ROMANIA & POLAND REAL ESTATE 2021 11

INTRODUCTION investment reports investment reports

EASE OF DOING BUSINESS

GDP GROWTH RATE - VOLUME %

100

8 80 100 100

7 87.7 82.9 82.3 85.2

60 80.0 75.0 76.4 76.5

6 76.4 75.0 63.9 72.2 64.4

5 62.0 66.0 59.1

4

40

58.4 53.7

3 20

2

0

1

0 Starting BUILDING Getting Registering Getting Protecting Paying Trading Enforcing Resolving

-1 a Business Permits Electricity Property Credit Minority Taxes across Contracts Insolvency

-2 Investors Borders

-3

-4 source: World Bank Group

-5

-6

-7

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 POLAND ROMANIA

40 76.4 Scores lowest on: 55 73.3 Scores lowest on:

Registering property (63.9) - 135 days Getting electricity (score 53.7)

POLAND ROMANIA EU

DB RANK DB score Protecting minority investors (score 66.0) DB RANK DB score Dealing with construction permits (score 58.4)

24 different procedures and 260 days.

Scores highest on: Scores highest on:

source: Eurostat Trading across borders (score 100) Trading across borders (score 100)

Starting a business (score 82.9) - 37 days Starting a business (87.7) - less than 30 days

CORRUPTION

KEY LEU (RON)

EUR = RON 4,92

INDEX

FIGURES ZŁOTY (PLN)

EUR = PLN 4,54

ROMANIA

RANK: 69/180

SCORE: 44/100

absorption of EU SHARE IN EU POPULATION (%) INFLATION POLAND

funds by 2020 RO : 4.3 RATE RANK: 45/180

(out of the 2014-2020 PL : 8.5 SCORE: 56/100

Inflation in the eurozone rose

multiannual financial

sharply in May 2021 to 2% - just

COVID-19 VACCINATIONS

framework) POPULATION EVOLUTION (2020, PER THOUSAND) above the European Central (as of june 2021)

RO : -5.0 Bank’s target. As economies

recover from the pandemic-driven

ROMANIA PL : -0.4

downturn, inflation is climbing.

29%

POLAND POPULATION PROJECTION (2050, aPPROX.)

43.5% RO : 16.2 MIL ROMANIA

ROMANIA

EU AVERAGE PL : 33.8 MIL 3.5% (Q2 2021)

8.9 mil

37.7%

National Bank of Romania (NBR)

23% of population

UNEMPLOYEMENT RATE (Q1 2021) POLAND

RO : 6.1 % 3.1% (MARCH 2021) POLAND

Source: Transparency International

PL : 6.3 % National Bank of Poland (NBP) The Corruption Perceptions Index 28.9 mil

EUROZONE ranks 180 countries and territories by 38% of population

their perceived levels of public sector

2% (MAY 2021) corruption, according to experts and

European Central Bank (ECB) business people. source: Reuters

source: Eurostat

12 ROMANIA & POLAND REAL ESTATE 2021 ROMANIA & POLAND REAL ESTATE 2021 13

development hotspots investment reports investment reports development hotspots

ROMANIA POLAND

INVESTMENT TURNOVER 2020 office & retail

office & retail

bucharest SQM (Q1 2021) The office segment represented EUR 770 MILLION an all-time record The industrial segment accounted for EUR 2.7 billion becoming warsaw SQM (Q1 2021)

for this market segment. the most traded asset class for the first time in history.

2.99 mil 6 mil

OVERALL : EUR 892.5 mILLION OVERALL : EUR 5,6 BILLION

1.17 mil 1.98 mil

industrial industrial

7.00 4.50

nationwide SQM (Q1 2021)

5.08 mil

YiELDS

(%) - Q4 2020

7.25 5.25

nationwide SQM (Q1 2021)

21.4 mil

8.00 5.75

≈ 2.500

price per sqm

in warsaw

(RESIDENTIAL, Q1 2021)

Poland accounted for more than

half of the total volume transacted

across CEE in 2020 (EUR 5,9 bn out of

a total of EUR 9,7 bn). Despite being a

point of interest for investors for many

years now, the country keeps leading

most charts in the region, with intense

activity taking place in Warsaw but

also its already highly developed

secondary markets.

Romania’s yields stand well above the European average,

presenting a very appealing investment prospect. The

≈ 1.500 business community is mainly concentrated around Bucharest

price per sqm (it hosts for instance 3 million of the country’s total 4 million

in BUCHAREST sqm of office space), however, this is rapidly changing with

(RESIDENTIAL, Q1 2021) cities such as Iasi, Cluj-Napoca, Timisoara or Brasov offering

expansion alternatives for companies.

14 ROMANIA & POLAND REAL ESTATE 2021 ROMANIA & POLAND REAL ESTATE 2021 15

INTRODUCTION investment reports

As Romania’s leading association Municipal Mayor’s decision to suspend zonal urban plans

dedicated to real estate, what is the (ZUPs), we were pleasantly surprised by the openness of

driving force pushing you forward mayors in Districts 2 and 6 towards working together to

and overarching mission? find a solution to the urgent urbanism problem.

Bottom line, the main issue

A.C.: AREI’s main purpose is to

defend the rights of its members and is the lack of procedure and

advance an equitable and just legal consistency. The most recent What is your vision for how the Bucharest of the future

environment. It is our mission to “lead legislative proposal is to put should look?

by example” – while remembering that

all real estate laws under A.C.: First and foremost, Bucharest should have better

real estate industry players are after

all a vital part of urban development a single roof, known as the planned integrated projects that give the urban scenery

across all its sectors, putting together Construction Code. a smoother, more consistent look. Developers alongside

Antoanela

the offices we work in, the houses we authorities must acknowledge that the city is already busy

live in, and the establishments where enough and there are areas where you simply cannot build

we shop and go for entertainment. anymore. Reducing traffic is a top priority and by following

COMȘA V.L.: One focal point in AREI’s

the large shopping centers after the

lockdown period. Likewise, Law 50

European solutions (bigger taxes, no parking on main

streets, etc.), one that should be easy enough to solve.

mission is to build a transparent and regarding building permits should

comprehensive perception of the be more flexible regarding the time V.L.: I would like to see more green areas and bicycle

President real estate industry, emphasizing the frame developers have to obtain all lanes in Bucharest, there are still very few compared to

AREI business value and moral code that

our members already follow. We

the documents needed for utilities

connection (water, electricity, sewage,

what could, and hopefully will be. This is in line with what

all industries nowadays are focusing on, namely more

do see outside of our association etc.) since providers usually act after sustainable business practices.

examples in the market that do not their own internal laws.

play by the book and, unfortunately, From your professional perspective how does the

AREI (The Association of Real Estate any sideslip of a real estate developer We were present when the draft was Romanian real estate market compare to other markets of

Investors in Romania) represents reflects upon our association and the conceived and we fully support a set CEE, and what trends should international investors keep

the voice of all four sectors: office, industry itself. of updated laws and regulations, much an eye out for? AREI

needed by the rapidly evolving real

residential, industrial and retail –

in relationship with the national What are the most ardent legislation estate sector. A.C.: From a bird’s eye view, in Romania it is in fact much

ASSOCIATION

authorities. issues AREI aims to solve, and easier and faster to obtain a building permit than in Western

European countries. For instance in Spain it can take up

OF REAL ESTATE

solutions that could help level the Regarding the discussions you had

real estate market? with authorities - what are some of to seven years. Similarly, in other countries it’s mandatory INVESTORS

your most important wins and are to design the entire infrastructure of the project before

A.C.: In the past few months, we there any notable standstills? applying for the building permit. If you are a law-abiding

focused on Law 114 - a 1996 piece investor, Romania has a market full of opportunities, The most significant community of

of legislation regarding housing A.C.: The bright side is that during our especially in the residential sector where there is a stock real estate investors in Romania.

standards and norms. Law 114 discussions with central authorities of over 50% ageing apartments in need of a makeover.

suffers from a great deal of gaps that we were always met with respect and Regardless of all the challenges mentioned before, the

www.arei.ro

result in mixed interpretations from they showed genuine interest towards Romanian market is a lot more lenient and welcoming than

the authorities. During the period solving the problems we were raising. other countries in CEE.

affected by the pandemic, we worked For example, the inspectorate for

on and advanced some important emergencies immediately took note V.L.: From my point of view, Romania has a fast maturing

initiatives such as: AREI guidelines and understood our deadlocks that market that is more than open to savvy investors. At the

on workforce re-entry measures for rose from the daily implementations moment we are curating an incipient legislative project

offices; Legislative initiative on the of the pieces of legislation under that will impact REITs (Real Estate Investment Trusts).

Voichița postponement of rent payments,

instead of exemption for both retail

review. By contrast, local authorities

(especially Bucharest’s City Hall) are

This piece of legislation should put Romania on the map

alongside other EU countries. Also, green projects are

LEFTER and offices, during the state of more rigid and it’s hard to establish a becoming a priority, with dedicated laws for parking spots

emergency; and contributed with our clear cut relationship with them. for electric vehicles, the revitalization of national railways,

expertise to endorse the Government among many other shifts.

initiative on the state aid scheme for V.L.: Indeed, we’re bumping into

partial payment of rents for retail. the reluctant attitude of some local

Secretary General We also had a very constructive mayors, but sometimes the day is

AREI dialogue with the Government that saved by counselors who are eager

was conducive to the re-opening of to find solutions. Following the

16 ROMANIA & POLAND REAL ESTATE 2021

INTRODUCTION investment reports investment reports INTRODUCTION

Would you say that, nowadays, the In Poland, the real estate market

level of taxation is encouraging to is dominated by international

real estate businesses in Poland? investors (more than 90%) - why do

you think this trend exists and is

The Polish Association of

Developers is a nationwide

Konrad

Certainly, in the past there were less

regulations strictly focused on real

there a blockage that prevents local

companies from investing?

industry organization

operating for 18 years

PŁOCHOCKI

estate and for the last four years, we and associating over 200

have been trying to close the gap 15 years ago, in Poland there was

development companies from

regarding the special income tax. not enough local capital and we

The main goal is to make the rules don’t have a regime which allows

all over the country. Managing Director

well balanced from the industry’s the creation of vehicles for private Polish Association of

perspective, but some of the investors (like a REIT). As the market

Developers (PAD)

regulations are still too burdensome matured, it naturally became a place

for the players, creating a certain level for international players because the

of uncertainty in the market. investments were too significant for

Paweł local ones. The current real estate

market is the result of a historical

You have been at the helm of the

Polish Association of Real Estate

Poland is a mature market that is

drawing much attention but it only

TOŃSKI lack of Polish capital coupled with

defective institutional laws. There is

Developers for over nine years,

how have you been supporting your

has so many sqm…

also a psychological reason behind members throughout this time? Every year we put our mark That would be our third challenge: the

this trend, since, in the past, Polish lack of investment plots. Short supply

on some 25-30 legislative

The level of taxation is not individual investors preferred the Lobbying activities are a natural part in this area impacts developers’ future

President of the residential sector because they of our value proposition, but not the projects that affect real planning and profitability, considering

as dire as it used to be, but

couldn’t grasp the particularities of only one. Training and lobbying each estate. I am proud to say that that we are getting less in terms of

Management Board we still have to explain the commercial market. make up for around 40%, whereas PR our opinions are considered spatial development plans and zoning

PINK Association to the authorities that and marketing count for around 20% decisions. In the last five years, the

in almost 80% of the cases, a

the uncertainty of “how What would be some of the of PAD’s activities. We issue 10 to 15 average price for an investment

challenges the pandemic posed to reports a year as a reference source clear sign that we should industrial plot went up by 80%. This

much” and “when” needs to

your members and how did you help for the government and our members. carry on. affects industrial more than other

completely disappear in order mitigate them? For example, a hot topic in 2020 was real estate sectors, as warehousing

PINK Association (The Polish

Chamber of Commercial Properties)

for transactions to how to reach energy efficiency in facilities created a steady demand

brings together developers, investors work smoothly. PINK has joined forces with developers buildings. For this job we joined forces during the pandemic.

and office investors to promote the with top professionals like universities,

and commercial service providers.

importance of office activities and law firms and other associations. Could you highlight two or three main What are PAD’s top priorities for the

The main goal of the association is to how they are vital in a well-functioning challenges the industry is facing, next two to three years?

influence the legislative action that society. Even though working from We are successful in getting people and ways in which you are trying to

directly affect its members. Are there any specific pieces of home is a perfectly adapted solution to work together by giving them address them? I want to establish our association

legislation that you are fighting for at to the current context, we want to also something first. We share information as a knowledge hub and a platform

this point in time, to improve upon? emphasize on the benefits of working which we know has problem-solving Our number one challenge is going for coming up with environmentally

from an office. Retail owners have potential in the present as well as the green. Balance must be found so friendly development solutions.

We started working with the suffered a lot during the pandemic immediate future. Typically, people that neither the environment nor Business knowledge in terms of past

government on the REITs regime and we continually tried to sustain our reciprocate and trust is formed. the end user suffers. Poland doesn’t mistakes, proposed solutions, or

(again) because this was an ardent members, though the authorities need have a legal environmental standard projections is essential for developers

issue for members and we wanted to to also play their part. for real estate developers to abide to seek and be able to find. Last but

solve it. The authorities put together by. However, we don’t wait for not least, we will invite more local and

an inter-ministerial technical team regulators to tell us what to do. governmental representatives to our

that will introduce the new regulations Instead, we created an internal culture thematic groups, hoping to achieve a

in the near future, this being a positive of sustainability among our members critical mass able to spread awareness

signal from their part. A slightly by training them on how to contribute and join efforts to solve the problems

smaller, but still troubling issue of the to reforestation. Our second main that developers are facing today in

industry is represented by the new set challenge lies in achieving fairness in Poland.

of rules that allow telecommunication taxation by convincing the authorities

providers to enter buildings without to charge end users on a number of

owners’ approval. While we bought sqm basis.

understand the need for direct access,

this regulation is detrimental, to say

the least.

18 ROMANIA & POLAND REAL ESTATE 2021 ROMANIA & POLAND REAL ESTATE 2021 19expert opinion article investment reports investment reports expert opinion article

What Will 2021 Bring for

Romania’s Real Estate Market?

Deloitte is the largest

integrated professional services Alexandru

organization, and conducted the

very first audit in the world. Real REFF

by Alexandra Smedoiu, Tax Partner and Real Estate Industry Leader, Deloitte Romania, estate is a key industry sector,

and Irina Dimitriu, Partner, Reff & Associates, Deloitte Legal and in collaboration with their

Romania’s real estate market has evolved beyond legal branch Reff & Associates, Country

expectations in 2020 and the prospects for 2021 are Deloitte assisted some of the

moderately optimistic, given the strong connections country’s largest real estate Managing Partner

between this sector and the industries it serves. The transactions. Deloitte Romania

economy rebounded by 5.8% in Q3 and by 4.8% in

Q4, after a 12.2% contraction in the second quarter of

2020. Private consumption, the main driver of last year’s

What was the idea behind setting Other than the digital tools, what are What are some of the main challenges

growth, is expected to recover strongly from the second

up Reff & Associates? How does it the main services you provide to the to the sector, if fiscal policy is not

half of 2021 as the rollout of vaccinations should allow

complement Deloitte’s work? real estate sector? among them?

for a gradual lifting of restrictions and investment is set

to remain strong over the next years, supported by the

Deloitte has been widely diversifying, We are particularly passionate about I think it is fair to say that Romania’s

construction sector.

it’s not uncommon, and a legal ad- real estate, no doubt about it and we fiscal environment has all in all been

on just made sense. We set up Reff & approach it through a multidisciplinary advantageous to investors, despite

As a general remark, 2020 was not a bad year for the Romanian real estate market. Romania’s economy Associates in 2006 as a separate entity, dedicated team coordinated by some occasional hiccups. Rather, the

In fact, strictly from the transactions’ perspective, it was one of the best years of

rebounded that works in alliance with Deloitte to Alexandra Smedoiu, Tax Partner problem has been one of political

the last decade, with a volume rising close to the benchmark of EUR 1 billion. Even

though most of the deals closed last year were started before March 2020, and

by 5.8% in Q3 serve clients who more often than not at Deloitte Romania and our real credibility and perceived corruption.

by 4.8% in Q4 2020. also need legal counseling, and that also estate industry leader. We advise This is linked to the infamous

the total volume was significantly influenced by one or two large transactions, the

works as an independent law house. developments and transactions alike. infrastructure challenges, a hurdle

signals received earlier this year show an increase in investor confidence in the

Where parties put their trust in resilient to investments across the board.

Romanian real estate market.

projects, price adjustment mechanisms One side of the practice we have been The fiscal practice is focused on direct Likewise, the country has had a hard

were negotiated (i.e. additional amounts focused intently on is digitalization and indirect taxation for real estate time attracting capital, be it private,

Mature investors are certainly prudent in these turbulent times, but are, at the

received by the seller in several years, under the umbrella of what we call transactions. In Financial Advisory, we European funds and so on, and access

same time, looking at the big picture before taking any major business decisions.

to the extent to which the project met legal management consulting. Tech have two teams relevant for real estate, to capital markets is weaker than in

This is the reason why prices for attractive projects have not dropped, COVID-19

certain key performance indicators). is opening up a new world, so we a transaction services team focused Western Europe.

related issues have very cautiously and wisely been brought to the negotiation

are assisting clients to optimize their on due diligence and advice on sales

table and deals that were frozen during the first months of the national lockdown

Mixed Feelings on Commercial RE internal processes and embrace new contracts, and a corporate finance team On the other hand competition is

are now being revived.

technologies. This involves using who are rather “deal makers” and take lower than in investor-crowded Poland

Since the beginning of the COVID-19 solutions like RPA (robotic process overall responsibility for structured or Czech Republic, for instance, and

It may appear as a surprise that the re-shaping of investment plans performed

pandemic, commercial real estate automation) and other tools, some transaction processes. yields are significantly higher. We have

last year has attracted more focus on real estate, in the sense that players with

players in Romania faced various specifically tailored to certain industries clients who want to liquidate Western

successful businesses in other fields are looking to invest their profits in quality

strategic and operational risks, with (retail, property, financial services). In management consulting we also European assets in order to invest more

projects (office, residential and logistic), while traditional real estate developers

notable differences between market support clients in various ways – one in Romania.

became more inclined to capitalize on their operating assets (via sale-purchase or

segments. In the following years, they For instance, we digitized compliance interesting segment is comprised of

joint venture) and use the proceeds for financing their on-going projects.

need to pay attention to tenants’ with regulatory requirements applicable non specialized real estate owners,

and final users’ needs and respond to commercial property owners and such as state institutions or other

All the above have generated new (and somehow unexpected) opportunities.

accordingly. Most of the owners, retailers, based on a comprehensive legacy companies, who own property

On the one hand, players have become more creative and showed flexibility in

developers and investors in this field inventory of existing regulations and but need advice on how to strategize

conceiving deal structures meant to accommodate silent partners and generally

consider contractual adjustments and automated features such as self- around it. There are many very valuable

joint ventures. On the other hand, once the lockdown was over, it was generally

flexibility to be the main attributes that review, remedial project management property portfolios (central buildings

accepted that the pandemic challenge cannot and should not stop the transactions.

will count for tenants and end-users and updates based on new legislation, or lands), breaking even or even

when the health crisis ends. expiration or changes in requirements incurring losses. The military or utilities

for permits etc. companies, for example, have buildings

2020 saw In conclusion, the real estate market with immense potential provided they

real estate transactions can still yield surprises, but it looks like, find the right investors to repurpose

them.

with both ups and downs, it managed

near the eur 1 bil mark to navigate the pandemic year and

come out in relatively good shape.

20 ROMANIA & POLAND REAL ESTATE 2021 ROMANIA & POLAND REAL ESTATE 2021 21MARKET

EVOLUTION

In each crisis we have a letter tracing the line of recovery; 2008’s

was W and now K is being used to mirror the divergent paths

varying industries are taking, creating multiple crossroads. The

retail and office segments are clearly affected in the short to

medium term, while residential and logistics are on the rise. But

beyond this, there will be successful and unsuccessful players and

projects within each of the four segments, based on their respective

fundamentals, so I expect divergence within, not just between

segments of the industry.

Alexandru REFF

Country Managing Partner

Deloitte Romaniamarket evolution - romania investment reports

photo: Bucharest from above

ROMANIA

low risk, high reward

by Alexandru David, Head of Research, JLL Romania

Romania is a rapidly developing country, and an established EU and NATO member. In 2019, the World

Bank promoted Romania in the High-income group of countries, with a gross national income (GNI)

per capita of EUR 10,600. For 2021, the European Commission projects that Romania will enjoy the

third highest GDP growth rate in the EU, of 5.1%. This trend is most likely to continue in the medium

term, considering that Romania will benefit during 2021-2027 from almost EUR 80 billion worth of EU

investments from the Multiannual Financial Framework and the Recovery and Resilience Fund.

Economic development was also

average net wages romania (EUR/month) reflected in the purchasing power of

the local population. Between 2016

800 and 2020 the average net wages in

700 the country have increased by almost

600 43%, from approximately EUR 525

500 to EUR 750. International companies

400

opening offices in Romania or

300

establishing production facilities here

had an important role to play in this.

200

100

0 In 2019, the World Bank

2016 2017 2018 2019 2020

promoted Romania in the

High-income group of

source: JLL Research, based on data from the National Institute of Statistics countries

with a gross national income

(GNI) per capita of

EUR 10.600

24 ROMANIA & POLAND REAL ESTATE 2021market evolution - romania investment reports investment reports market evolution - romania

Romania Real Estate

Market Overview

The Romanian commercial real estate market provides

OFFICES

opportunities in all segments, both in terms of development and

Multinational companies are increasingly targeting Romania due to the country’s human capital, with strong foreign

investment. Historically, the market has been driven mainly by

Aurelia LUCA language skills, as well as the availability of quality office products at competitive pricing. Romania currently has a total

local or regional developers, but, especially in the last seven years,

Executive VP Operations modern (A and B class) office stock to lease of approx. 4 million sqm, including Bucharest and the four major regional cities

we have seen increasing interest from international institutional

Hungary & Romania of Cluj-Napoca, Timișoara, Iași and Brașov. However, Bucharest alone accounts for almost 3 million sqm of modern offices.

players. Some of the international office developers with a track

Skanska record in Romania are: Globalworth, Skanska, AFI Europe, GTC,

office buildings delivered

IMMOFINANZ, CA Immo. In the retail sector, NEPI, AFI Europe,

Sonae Sierra, S IMMO or IMMOFINANZ have been active. The in bucharest (sqm GLA)

industrial sector has been shaped by developers such as CTP, P3, 44%

WDP, VGP and Alinso Group. drop in total

office demand 350.000

The pandemic brought to light how important The main office developments are located in Bucharest and the

in 2020

300.000

it is to work outside of our homes from a top secondary cities with strong university centers that can offer 250.000

mental health point of view, but also from a the relevant labour force with higher education. Retail developers 200.000

community and socializing one. The offices have targeted most of the 42 county capitals in Romania, focusing 150.000

of the future will have a strong accent on mainly on those with a high population density and high disposable During the last five years, approx. 100.000

wellbeing, safety and human connection incomes. There are industrial projects throughout the country, 1 million sqm GLA of offices were 50.000

through larger common spaces, leisure rooms however access to good infrastructure and proximity to either delivered in Bucharest, marking a 50% 0

and top-notch facilities. During the pandemic Bucharest or, CEE and the rest of Europe, has directed investors increase of the office stock. Another 2016 2017 2018 2019 2020

we introduced the Care for Life Office Concept, interest mainly towards the Western part of the country (Timișoara, 256,000 sqm are expected to be source: JLL Research

focused on tenants’ safety and wellbeing. Arad, Cluj-Napoca, Sibiu) or to the Central-South (Bucharest delivered in 2021.

Greater Area, Ploiești, Pitești) and more recently towards the East,

namely Bacău and Iași to cover the Moldavian part of the country. Many international companies have

chosen Bucharest in recognition of

its extended infrastructure and due to Bucharest experienced a strong demand for office spaces during 2016-2019, on

the availability of skilled workforce. In average over 360,000 sqm being leased in total on a yearly basis. However, the

particular, high office space demand COVID-19 pandemic had a detrimental impact for the local economy and for

comes from IT&C companies, such office space demand. 2020 marked a 44% drop in total demand compared to

as Microsoft, IBM, HP, Oracle, Intel, the previous year. At the same time, the vacancy rate increased from 7.7% at the

Adobe or Siemens, amongst others. end of 2019, prior to the onset of the pandemic, to 11.3% at the end of 2020.

A workplace built to give you the ground

TO CREATE,TO INSPIRE,

TO BREATHE. Few realize just how much Bucharest has grown, 2.5 million people including

the outskirts, meaning that fighting congestion has become a priority for the

authorities and people alike. When we presented the “Timpuri Noi Square”

concept to potential tenants we wanted to keep it short and sweet – Timpuri

Noi is connected to Bucharest’s two main metro lines, which gets you within 30

minutes just about anywhere. It is also one of the city’s main residential areas,

Antoniu PANAIT and if you want to be successful you build your office not close to the GM’s

Managing Director house, but to where most of your employees live. People have started valuing

VASTINT Romania family time over commutes, even over company allegiance or salary grade.

Timpuri Noi Square is now nearly 100% leased, and Orhideea is at 75% after

Vastint is an international real NTT’s recent addition. The quality speaks for itself, as even this year we were

estate organization spanning able to sign nearly 10,000 sqm. That being said, of course the pandemic has hit

30 years. Present in Romania everyone, ourselves included. But make no mistake, the pandemic will not mark

since 2008, they developed the end of the office era. We are deeply rooted social beings, we need to work

emblematic projects, such as together and feel that sense of “normalcy” and purpose.

Business Garden Bucharest.

26 ROMANIA & POLAND REAL ESTATE 2021 ROMANIA & POLAND REAL ESTATE 2021 27investment reports market evolution - romania

Market rents in Bucharest were stable during the last

5 years, at around EUR 12.5 per sqm per month in the

During the past few years CA Immo exited several CEE

non-central areas, EUR 15 per sqm per month in the

markets (Bulgaria, Croatia, Slovakia, etc.) - how does

semi-central areas, and EUR 18.5 per sqm per month

Romania fit into the company’s portfolio?

in the Central Business District (CBD) of the city.

Romania is a core market that kept steady, amounting to

Currently, the office market in Bucharest is in a

about 7-8% of the total global portfolio of CA Immo. At the

recovery process, as companies return to normal and

moment, we are consolidating the projects that are on the

reassess their strategies following the pandemic.

roll, since 2020 was such a challenging year for everyone.

Signing new leasing contracts was difficult, as in most other

One important event for the office market in 2020 Daniela Friedrich global jurisdictions, but we registered a very good appetite

was the EU’s decision to locate in Bucharest the

headquarters of the future European Cybersecurity

BĂDULESCU WACHERNIG for renewals. Overall, Romania’s turnover fared well and

was at the same level as in 2019.

Industrial, Technology and Research Competence Country Manager RO Group COO

Center. This move is expected to stimulate S IMMO AG S IMMO AG

The plan is to stay on the Romanian market for the long-

technological research and innovation and to

run. We have numerous projects with zero vacancy over

consolidate the cybersecurity within the Union.

How relevant is the business you do in Romania within the last decade and we are proud to say that many tenants

Moreover, the Center will become the main EU body

the company’s international portfolio? have been with us since the delivery of the building and

to manage the European funds dedicated to research

have been telling us it is an ideal work environment for

in the field of cybersecurity, available through two

FW: Approximately one third of our portfolio is based in their activities ever since.

EU financing programs, Digital Europe and Horizon

Europe. In terms of office demand, this will likely CEE and the remaining two thirds in Germany & Austria.

Since it’s still in a transition process, the Romanian market Bucharest’s office sector is continually expanding and

attract to Bucharest IT and cybersecurity companies

has massive room to catch up with western standards and changing - can new development opportunities still be

from all over Europe in the short and medium term.

this is why it occupies a special place in our portfolio. found here?

We expect to see more growth in the upcoming years

also in the 4 regional cities of Cluj-Napoca, Timisoara,

The office sector is suffering from some disruptions on Looking at the big picture, the market potential is immense

Iasi and Brasov, currently concentrating around one

the background of the global pandemic. How are these and in the following years the only limitation will be

million sqm of modern offices in total and providing

impacting you? represented by the available workforce. The equation is

expansion alternatives for companies.

simple: more employees in the work field require more

DB: At the beginning of the pandemic we braced for office spaces. Besides Bucharest, Cluj-Napoca, Iași and

2020 marked an important milestone for the regional

impact and we were happy to find out that the occupation Timișoara are strong university centers and their pool of

markets, when the American giant Amazon pre-

rate dropped only by 10%. We expect it to grow back by talented graduates will lead to more job creation, in turn

leased over 30,000 sqm GLA in Iași. This is the largest

3-4% in the near future - some companies will be pressured rising the demand for office spaces.

historical deal recorded in the regional cities and the

second largest in Romania overall. to reduce their costs, but overall we managed to bite the

bullet and mitigate most of our losses. Are you considering expanding beyond Bucharest to

capture these growing opportunities?

What is the number one issue that keeps you up at night

We are most interested in liquid markets and this aspect

MARKET RENTS when doing business here?

is not as strongly represented in other cities as it is, at this

(Bucharest, sqm/month) F.W.: First of all, I have been doing business in Romania for point, in Bucharest. A dynamic environment where exits

are commonplace is attractive both for local and foreign

many years now and I sleep quite well. Even though there’s

still a long way to go, a lot of things have improved since investors because they can be sure their investment will

1996, when I first arrived here. Problems are easily solved not be blocked in a stationary market.

through communication and palpable examples of how

things can be done better. For example, infrastructure was

EUR 12.5 a notorious problem of the Romanian real estate market,

but fortunately the odds have been changing in the past

non central areas few years.

EUR 15 Marian

DB: Looking back at how the real estate market looked

ROMAN

semi-central areas like 10-20 years ago, important improvements have been

achieved. The bureaucracy is less convoluted, infrastructure Managing Director

EUR 18.5 develops at a fast and steady pace and the relationship

with local authorities has become more open. However,

CA Immo

central business district predictability is still an aspect that needs to be addressed.

ROMANIA & POLAND REAL ESTATE 2021 29market evolution - romania investment reports investment reports market evolution - romania

was to overcome some of the hurdles we

met in Romania, and gain access to new

forms of capital. Mihai PĂDUROIU

CEO

Romania’s biggest problem is branding – One United Properties

we have had so many partners, clients, (Office Division)

investors coming here and not believing

their eyes, as they have been negatively

predisposed by a number of stereotypes From a historical perspective, the Romanian real estate market evolved in

and clichés. It is a shame to suffer from a highly positive way and past challenges (e.g., infrastructure) that seemed

this unfair perception. insurmountable are now mere distractions along the way. All in all, from our

perspective the office market shows great maturity and stability.

Globalworth Square is one of the most

technologically advanced buildings in

Dimitris

RAPTIS

Investors that make direct contact with the Romanian market are instantly

the country, which I am sure does not seduced by the opportunities found here. Bucharest presents competitive

come cheap – why prioritize this? advantages that cannot be found anywhere else - the biggest talent pool and the

most advantageous tax levels - which makes it by far one of the most attractive

People have been talking about smart

CEO destinations for investment in Europe. This view is backed by the impressive

buildings for some time now, and real number of big players (both investors and tenants) that do business here.

estate has honestly speaking been Globalworth Group

a dinosaur in terms of embracing

technological progress. Strange, given

that it is one of the world’s dominant

total volume of office transactions

industries, with high pressure to Globalworth is a publicly listed

evolve. The coronavirus pandemic has in bucharest (sqm GLA)

leading real estate company

accelerated the way people think about

operating across Romania and 400.000

this topic and turned thoughts into

action.

Poland, that acquires, develops 300.000

and manages commercial 200.000

As an example, at Globalworth Square properties, mainly in the office 100.000

we have touchless access into the segment. 0

2016 2017 2018 2019 2020

building, a simple yet key aspect. And last

source: JLL Research

but not least, tech is closely interwoven

with sustainability by helping us build

more energy efficient buildings, from

Globalworth employs a long term, lower emissions to car charging stations. In some cases we had to offer “rent

here-to-stay vision so it is all the At Globalworth Square we are also holidays”, concessions, deferrals in

more important how you choose your producing our own energy through exchange for extensions for the future.

We hold about 15-20% of the office market in Bucharest and, at present, we

markets. Why Romania and Poland, and rooftop PV panels. Some of the smaller tenants we simply

are developing 90,000 sqm of spaces. Ever since we started Forte, our main

how do they contrast in your view? helped out. And at the end of the day we

goal was to bring a breath of fresh air to the urban landscape because I firmly

How badly has the pandemic hit your stayed robust.

believe that developers have the responsibility to shape the city in the most

Romania is pure legacy, Globalworth’s office business and how does that

aesthetically pleasing way possible.

founder Ioannis Papalekas was already contrast to your other assets, in the Logistics is a different ball game – we

in business here since 2001 and saw a industrial space for instance? have three locations across Romania and

Moreover, part of the strategy was to reconsider the commute time spent by

market opportunity again in 2012-2013, we are seeing great demand, broadly

our tenants and therefore our focus went on to shorten the time spent in traffic.

when I also joined him from London. Yes, the office model is currently being from two industries – e-commerce and

As a result, we placed most of our office buildings near the neighborhoods

Poland was also an obvious choice for questioned, it sits somewhere in the F&B retailing. There is also some pharma

where 80% of the employees reside. In this way, not only the North of the city

us, as the largest and most sophisticated middle between the badly hit retail/ but the bulk of the demand comes

benefits from office buildings, but also the South and the West.

market in CEE, we were confident we hotels and the thriving logistics spheres. from the automotive industry. Renault

could compete there. Both countries also The impact for us has not been too recently extended their lease in their

have key geo-political positions. significant so far, however we needed to facility outside of Bucharest, thanks to

have many discussions with our tenants its strategic location close to their main

Geo MĂRGESCU

As for the differences, some are quite and mitigate risks together. This is where factory.

Co-founder & CEO

visible – starting with infrastructure, our model helped us, the long term

Forte Partners

from airports, motorways, rail, where relationships helped negotiate and find

Romania still lags considerably behind. common ground.

One of the reasons we entered Poland

30 ROMANIA & POLAND REAL ESTATE 2021 ROMANIA & POLAND REAL ESTATE 2021 31market evolution - romania investment reports

You describe yourselves as “atypical Sustainability is a big trend nowadays,

developers”, what sets you apart from what motivates you to pursue this

the crowd more specifically? direction and how do you see it

reflecting in the local market?

When evaluating a plot of land we always

create a masterplan design that shows Sustainability is more than marketing

how the finished product will fit into for us, because we seek to invest only in

the area. Only when we feel it is going projects that bring quality of life, adding

to be a suitable project we move into the measures of sustainability that are

financial phase, so we have a backwards actually useful to the users. In residential,

method, different from other developers, it is still challenging to implement these

that first do the math and then start measures because people are not yet

Didier designing. In the end, we build less, but of

a much higher quality hence benefitting

prepared to pay for them even though

they are highly interested in using all

BALCAEN both the users of our projects as our

profitability, and this approach helped

the facilities that come as a result. On

the other hand, offices are following

us especially during the pandemic. This international standards because they

mindset is starting to spread throughout cater to multinational companies, so it’s

the market and many of our colleagues common practice to develop sustainable

CEO & Co-founder are embracing it. projects in that sector.

Speedwell You work in various sectors: Do you have a final message about the

residential, office and retail - how do Romanian real estate market based on

each of them contribute to your wider your experience here?

portfolio?

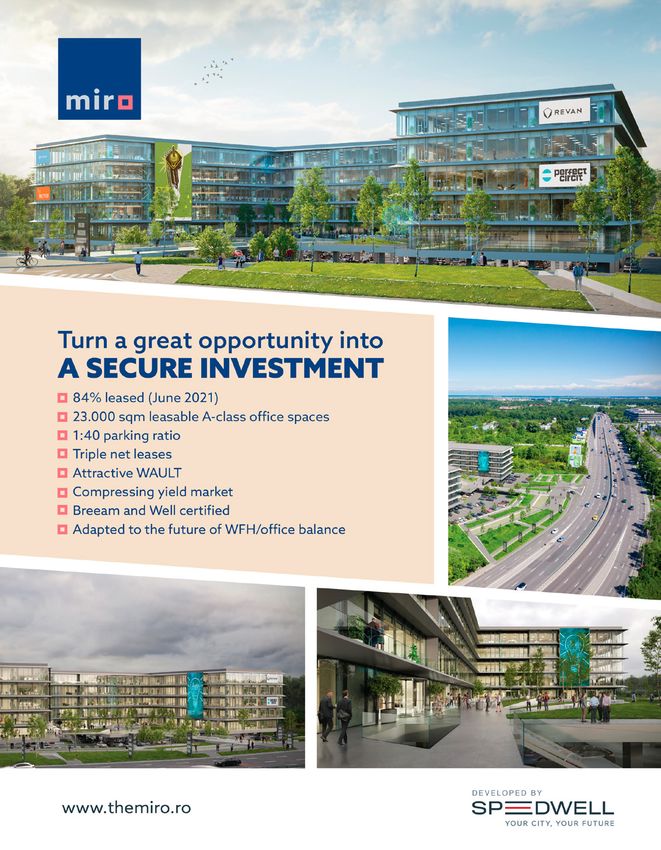

Speedwell is a real estate developer Our MIRO office project, demonstrates

that specializes in mixed-use, The goal is to have a mix, but from a that the market offers a Western-grade

residential, office and retail projects. financial point of view the foundation is A-class office project with Triple-A

They put their mark on state-of-the- definitely the residential sector (60-70% tenants such as KPMG at much higher

art buildings like MIRO Office, The of the portfolio) because the product is yields than Western or even other

Ivy Residential and Record Park, etc. the least dependent on macro-economic Eastern-European capitals. Therefore

factors (yields) in the long-term, given investors get a prime asset with the

that Romania is a market of primary best tenants at an unbeatable price.

buyers (buying to live, not to invest). We Overlooking the Romanian market is

do concentrate our attention on projects therefore no less than a professional

with functions that add to the existing error if you’re an (institutional) investor.

mix, but always keep a safe foundation

based on residential buildings.

Interestingly, your work in Romania

expands well beyond the capital city.

What drew you towards regional

markets?

We didn’t actually conduct any in-depth

“Unknown is Unloved” applies

Jan studies, but acted on our instincts and

when we identified a good plot of land, to Romania. Many investors

DEMEYERE we simply went for it - in Cluj-Napoca, and bankers not familiar with

Timisoara or wherever it was located. the market often classify it as

Since in Romania regional cities are

risky and stay away, without

smaller than in Poland, for example,

liquidity for commercial projects remains even looking deeper if there

is an objective reason for the

Architect & Co-founder a point of attention, but if you develop a

good product you can always lease and “risk” perception.

Speedwell sell it at a good price.

32 ROMANIA & POLAND REAL ESTATE 2021You can also read