Participant Guide - Advocis

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Participant Guide

Advocis Continuing Education

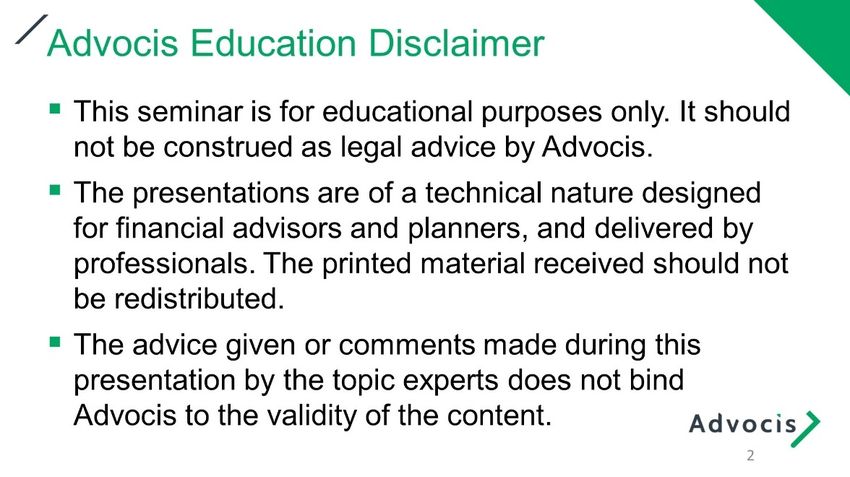

Disclaimer

• This seminar is for educational purposes only. It should not be construed as legal

advice by Advocis.

• The presentations are of a technical nature designed for financial advisors and

planners, and delivered by professionals. The printed material received should not

be redistributed.

• The advice given or comments made during this presentation by the topic experts

does not bind Advocis to the validity of the content.

Note: To be eligible for CE you must be in attendance for the full seminar

today.

Advocis®, The Institute for Advanced Financial Education (The Institute), CLU®, CHS™, CH.F.C.®, PFA™

and APA® are trademarks of The Financial Advisors Association of Canada (TFAAC).

Copyright© 2021 TFAAC. All rights reserved. Unauthorized reproduction of any images or content without

permission is prohibited.

ADVOCIS COPYRIGHT ©2021 TFAAC 2

Table of Content

Presenter Biographies ............................................................................................................... 4

Learning Objective, Moderator and Presenters ......................................................................... 5

Presentation 1: Building an Inclusive Practice ........................................................................... 8

Presentation 1: Building an Inclusive Practice (Pre-Reading) ..................................................... 9

Case Study Activity: Connecting with Clients .......................................................................................... 21

Presentation 2: Planning: Pivot to the New Reality ................................................................. 27

Case Study Activity: The Young Family .................................................................................................... 34

Presentation 3: Customized Solutions for Managing Risk ........................................................ 44

Case Study Activity: Adjusting the Plan for a Small Business Owner ..................................................... 52

Presentation 4: Deeper Connections in a Virtual World ........................................................... 58

Case Study Activity: Customizing Client Connectivity ............................................................................. 67

Advanced Learning Modules ................................................................................................... 71

How to Access Advanced Learning Modules ........................................................................................... 73

Resources Available Online ..................................................................................................... 74

Notes ...................................................................................................................................... 75

ADVOCIS COPYRIGHT ©2021 TFAAC 3

Open to the Future

inclusive | flexible | connected

Christopher Dewdney, CLU®, CFP®, CHS™, CPCA® Back to Table of Contents...

Principal, Dewdney & Co.

Christopher has committed himself to the financial services industry for over a decade. Helping both individuals

and businesses alike, his practice combines all areas of financial management into a unified, detailed, custom

plan to serve each client’s individual objectives. Christopher’s experiences range from risk management to wealth

accumulation. He uses a team approach encompassing a detailed and disciplined financial planning process that

looks at both the quantitative data, as well as the client’s goals and objectives. An active Advocis volunteer,

Christopher is also a member of CALU.

Michele Byrne

Senior Advisor, Ministry of Government and Consumer Services

Michele is a diversity, inclusion and anti-racism diversity practitioner with over 18 years’ experience. Currently

working with the Ministry of Government and Consumer Services, she provides strategic advice on leadership

diversification talent pipelines, curriculum and policy development as well as inclusive organizational culture

change. Previously Michele has held several positions in her field at both the federal and municipal level.

Additionally, she has worked with non-profits and non-federally regulated organizations where she developed

and implemented compliance standards for employment equity and race-based mentorship programs including

an Indigenous Employment and Education Strategy. Michele has a B.A. from McMaster University and a

Professional Certification in Human Rights Theory and Practice from Osgoode Hall Law School.

Cindy Marques, CFP®

Financial Coach, Paper & Coin

Cindy specializes in the millennial demographic with a strong focus on cash flow planning and financial literacy.

She believes that financial literacy is the ultimate tool for building wealth and has built an independent practice

around that model. An experienced life and health insurance broker, Cindy transitioned her practice to a fee-only

Financial ‘Coaching’ model to better serve the otherwise overlooked millennial market. In an ongoing effort to

promote and provide more approachable educational resources, Cindy launched a Financial Literacy program

and YouTube channel ‘Dressed to Invest’ at the start of 2020. Soon after, she partnered with budding Financial

Coaching company ‘Paper & Coin’ and now manages their Financial Coaching program, serving clients nationally

all across Canada.

Mehul Gandhi, CLU®, CFP®

Business Planning Specialist and Senior Insurance Advisor, Westmount Wealth Planning

Mehul specializes in advanced tax and estate planning for business owners and high-net-worth families. His

unique financial plans provide clients with a detailed road map of their financial lives. A senior life insurance

advisor, with expertise in creative insurance planning for incorporated individuals, Mehul believes in lifelong

learning and continuously educating himself in the areas of tax and estate law. An active Advocis volunteer,

Mehul is the 2018 recipient of the Leslie W. Dunstall Award, presented to candidates who achieved the highest

examination marks for all CLU® course subjects.

Wendy Brookhouse, CHS™, QAFP™

CEO, Black Star Wealth™

With the audacious goal of changing one million lives, Wendy is the inventor of the proprietary One Number

Solution™. This unique system is a truly holistic plan that covers spending, debt repayment, saving for the future

and a strong safety net – and simplifies everything down to one number the client can control! This system allows

clients to achieve their financial goals faster and with less stress or anxiety and forms the foundation for retirement

income planning and estate planning. Wendy regularly speaks about money consciousness and how to achieve

lasting financial change because she believes wealth is so much more than a dollar amount, it is about the joys

you have in life and how you live day-to-day.

Back to Table of Contents... Learning Objective, Moderator and Presenters ADVOCIS COPYRIGHT ©2021 TFAAC 5

ADVOCIS COPYRIGHT ©2021 TFAAC 6

ADVOCIS COPYRIGHT ©2021 TFAAC 7

Back to Table of Contents... Presentation 1: Building an Inclusive Practice ADVOCIS COPYRIGHT ©2021 TFAAC 8

Back to Table of Contents... Presentation 1: Building an Inclusive Practice (Pre-Reading) The following reading was prepared by Michele for review prior to watching her video-taped conversation with Update 2021 moderator Christopher Dewdney. Shape of the Canadian landscape COVID-19 has exposed our vulnerability as a global village and has awakened our social responsibility especially as it relates to health, the economy, and social justice. A successful culture of belonging requires leadership commitment, the ongoing practice of inclusion, recognition of unique talents and accomplishments and an environment that fosters the celebration of differences, respect and engagement. A simple diversity and inclusion (D&I) policy will not be effective in solving systemic discrimination and practices within the workplace regardless of whether its intentional or unconscious through implicit bias. We, as Canadians perceive ourselves as socially just in our mindset, fair and open to all the spheres of D&I, open minded, anti-racist, etc. However, many of us were not taught in school that Canada has a history of slavery, women in Canada were only given the right to vote in 1920, until 1960 Indigenous Peoples were not allowed to vote without giving up their treaty rights and the last residential school was closed in 1996 in Saskatchewan. We were taught that Canadians were the author of the Charter of Rights. We pride ourselves on been inclusive, polite, welcoming to all the worlds’ inhabitants and our role as peacekeepers. Surprisingly, in recent study conducted by Northwestern University, Canada has been named the fourth most racist country in the world according to a recent study of 9 countries as it relates to its recruitment practices. The first three countries consecutively were France, Sweden, and Great Britain. In the July 26, 2019 article authored by Allysha House, that referenced the study by Northwestern University, Canada Ranked as One of the Top Countries for Racial Discrimination In The Hiring Process, in Narcity: https://www.narcity.com/en-ca/news/canada-ranked-as-top-racial- discrimination-countries-in-the-world-during-the-hiring-process). Several recent Canadian studies from Catalyst and Boston Consulting Group, Deloitte and Touche and CivicAction, speak to gender inequities and the state of racism in Canada in all business sectors. Along with media, several articles, podcasts, TedX, etc. have discussions on the negative impact of racism throughout Canada. ADVOCIS COPYRIGHT ©2021 TFAAC 9

Terminology

Diversity: When you look at the image of Dimensions of Diversity, you can see yourself reflected in it.

Everyone should be able to find themselves in this diagram. Diversity is not a singular dimension – it

is multi-dimensional.

• The more visible aspects of diversity – things like age, race, gender and ethnicity – are just

part of the many layers that go into describing who we are and how uniquely different we are.

• The inner circle…the inner core that speaks to personality, that’s fixed. We are supposedly

born with certain personality characteristics.

• Around that…are internal dimensions of diversity. For all intents and purposes, those don’t

change, your place of birth, your date of birth, your ethnicity, these do not change.

• Then we have the external layers of diversity. That’s where we see things that change over

time. For example, our marital status, parental status, abilities, etc.

• Organizational dimensions are those dimensions related to our place in the organizational

structure… income, employment status, seniority, professional associations, work location, etc.

• Global dimensions…refers to the political landscape, impacts of world events (COVID-19,

George Floyd,), laws that govern the country, province where you live, etc.

ADVOCIS COPYRIGHT ©2021 TFAAC 10Inclusion: Inclusion is active engagement of equity and diversity concepts, the implementation (action oriented) integration in all aspects of your organization, business operations and society. This includes fostering a sense of belonging for all, making individuals feel embraced and celebrated within an organization or society and having those values reflected. Providing equitable access to opportunities and information and enabling individuals to achieve their fullest potential. While diversity refers to representation…Inclusion is the strategic driver for real change. It’s through inclusion that organizations can foster an environment for engagement, respect, building relationships, driving innovation and being relevant in our changing times while integrating diversity. It means creating value from the distinctive skills, experiences and perspectives of all members of our community, allowing us to leverage talent and foster both individual and organizational excellence. Inclusion is the qualitative experience- Do individuals feel that they have equal access to opportunities within their firms? Do they feel that they are able to bring their differences to work and that they can leverage these differences for success? Equity is the guarantee of fair treatment, access, opportunity, and advancement for all. It requires the identification and elimination of barriers that prevent the full participation of some groups. The principle of equity acknowledges that there are historically underserved and underrepresented populations in the societal areas of employment, the provision of goods and services, as well as living accommodations, etc. Removing unbalanced conditions/barriers is needed to achieve equitable opportunities for all groups. Inequity occurs when someone tries to access an opportunity or a service that was not built with them in mind. When somebody encounters a situation where their identity disrupts “the way things are normally done”, we call this a barrier. Racism a belief that race is a fundamental determinant of human traits and capacities and that racial differences produce an inherent superiority of a particular race over another (Merriam Webster). Anti-racism- is a proactive process of change that understands that racism creates privilege for some groups and disadvantages for others. It is about combatting systemic racism and advancing racial equity. Anti-racism targets structures/polices/practices that sustain unequal power dynamics between groups based on race (systemic barriers). ADVOCIS COPYRIGHT ©2021 TFAAC 11

Systemic racism occurs when institutions or systems create or maintain racial inequality. This can

be unintentional and doesn’t infer that the people working within that system or organization are

racist, however if not addressed or removed the negative impact remains.

Systemic racism is often caused by what is hidden, in what appears to be neutral policies and

practices, that based on their design may privilege or disadvantage particular groups based on race.

Intersectionality: the complex, cumulative way in which the effects of multiple forms of discrimination

combine, overlap, or intersect especially in the experiences of historically excluded groups. For

instance, gender and race, age and gender, disability and sexuality, etc.

Microaggressions consist of seemingly innocuous statements (jokes), actions and attitudes, which

can be direct or indirect. They exclude (other) persons who are not part of the dominant group. For

example: You were so confident in the boardroom, your name is hard to pronounce, can I call you

Susan? What do your people think about that? You are so articulate, etc.

Bias: A tendency, inclination, or prejudice toward or against something or someone. Biases are often

based on stereotypes, rather than actual knowledge of an individual or circumstance. Whether it is

positive or negative, such as cognitive shortcuts, bias can result in prejudgments that lead to rash

decisions or discriminatory practices.

Unconscious bias: A bias that we are unaware of, and which happens outside of our control.

Unconscious bias helps us deal with overwhelming amounts of information we encounter. Without

this, we would not be able to navigate through daily activities.

Implicit bias: The process of associating stereotypes or attitudes towards categories of people

without conscious awareness:

• Also known as implicit social cognition, implicit bias refers to the attitudes or stereotypes that

affect our understanding, actions, and decisions in an unconscious manner. These biases,

which encompass both favorable and unfavorable assessments, are activated involuntarily and

without an individual’s awareness or intentional control. Residing deep in the subconscious,

these biases are different from known biases that individuals may choose to conceal for the

purposes of social and/or political correctness.

ADVOCIS COPYRIGHT ©2021 TFAAC 12• The implicit associations we harbour in our subconscious cause us to have feelings and

attitudes about other people based on characteristics such as race, ethnicity, age, and

appearance. These associations develop over the course of a lifetime beginning at a very

early age through exposure to direct and indirect messages. In addition to early life

experiences, the media and news programming are often-cited origins of implicit associations.

(e.g. women and maternity leave, as opposed to men and children/paternity leave, CEOs are

male and white, new immigrants from non-western or European countries have less wealth to

invest vs. their western and European counterparts, people with accents are less educated

than those without, staff who are over 40 years of age are less tech savvy that those between

20-30 years of age, etc.)

Note: This is not the same as explicit bias, conscious racism and other forms of conscious bias

which still exist and need to be addressed. Here, we are talking about people who consciously and

genuinely believe in fairness, equity, and equality, but despite these stated beliefs, hold unconscious

biases that can lead us to react in ways that are at odds with our values. These unconscious biases

can play out in our decision making regarding who we hire for a job or select for a promotion, which

students we place in honours classes and who we send out of the classroom for behaviour

infractions, and which treatment options we make available to patients. We know from extensive

research that this kind of biased decision making plays out all the time in our schools, in hospitals, in

policing, and in places of employment.

Explicit bias: Refers to biases we are aware of on a conscious level (for example, feeling

threatened by another group and delivering hate speech as a result).

“The question is not if it is happening, the question is

when is it happening and what can we do about it?”

Removing these biases can be a challenge, especially because we often don’t even know they exist,

but research reveals potential interventions and provides hope that levels of implicit biases can be

changed. Our brains are very malleable, and we can actively change our biases through self-

awareness and intentional behavioural change.

ADVOCIS COPYRIGHT ©2021 TFAAC 13The Future

History has shown with each new generation, comes a new way of thinking. Many of us now are used

to learning and socializing in a multi-diverse environment and are descendants of multi-

racial/ethnic/religious families or families that don’t fall within the previous parameters of traditional

families. Many expect organizations, products and services to reflect their values. Whether that’s

climate change, acknowledgement of non-binary expressions of gender identity, sexual orientation,

etc.

In the recent years and months, we have seen global protests in the streets against social injustice,

Anti-Black racism, gender equality and climate change. All generations are represented in these

demonstrations, however for most part; they are being coordinated and led by younger people.

They are using the power of social media to mobilize and amplify their voices for positive change. i.e.

Me-too Movement, Black Lives Matter, Gay Liberation Movement, Truth and Reconciliation, Climate

Change.

Remember a lot of these so-called norms or societal rules were created a long time ago from one

perspective at the exclusion of others, which have been pervasive globally. That mindset has

changed.

The old rule of treating everyone like you would like to be treated is no longer applicable.

“The new approach is the Platinum rule-

Treating people how they would like to be treated,

I.e. legislations - duty to accommodate, OHRC,

Gender equity, racial equity, etc. “

As Canadians we don’t want to believe that we have racist, homophobic, ageist or sexist biases

towards individuals who are different from us. Yet, the evidence shows that these biases do affect

services, housing, education, recruitment, etc. Being self-aware of how our individual actions have

contributed to these inequities is the first step.

As previously mentioned, implicit bias is malleable- we can change our behaviour and the outcomes.

ADVOCIS COPYRIGHT ©2021 TFAAC 14Back to Table of Contents... ADVOCIS COPYRIGHT ©2021 TFAAC 15

ADVOCIS COPYRIGHT ©2021 TFAAC 16

ADVOCIS COPYRIGHT ©2021 TFAAC 17

ADVOCIS COPYRIGHT ©2021 TFAAC 18

ADVOCIS COPYRIGHT ©2021 TFAAC 19

ADVOCIS COPYRIGHT ©2021 TFAAC 20

Back to Table of Contents... Case Study Activity: Connecting with Clients Learning Objective: To help determine potential biases and find ways to ensure the advisor, employees and clients fit seamlessly into the new practice. A: The Facts The Advisor Henry is age 58 and has run his own successful practice for 32 years as a financial planner and insurance advisor in a small town in southern Ontario. He holds his CLU and CFP designations. The town Henry is in has been growing significantly over the past few years as immigrants to Canada are choosing it as their home. There are many businesses in town, and it is close enough to several major cities to commute for work as well. Most clients have been with him from the early days of his business and are in their 50s-80s, and over the past 10+ years he has focused on maintaining his existing clients but not on prospecting or adding new clients to his business. He has not adapted to technology and prefers taking notes with a paper and pen and all his records are in paper format. He has one administrative assistant, Sarah, who has been working with him for 21 years. AUM: $20M and 750 clients Henry is considering a gradual retirement starting at age 60 and phasing in a new advisor over 5 years. He is married and has two children age 28 and 31 who are not working in the insurance and financial services industry. His wife retired 3 years ago from teaching. Henry’s brother lives in Phoenix, AZ and Henry and his wife rent a place there for 2 months in the winter. ADVOCIS COPYRIGHT ©2021 TFAAC 21

Personal Priorities for Retirement

• The importance of having something in his retirement lifestyle that gives him joy

• To be excited about the next 25 or 30 years of his life

• Buy a property in Phoenix, AZ and extend time there to 5 months/year

• Find a cause in which he truly believes and can dedicate his time and energy

• Leave Henry’s own portfolio and personal insurance program in the hands of his successor

Business Succession Priorities

• Commitment to bringing in a successor early on.

• Gradually work with the successor to establish relationships and trust with the clients.

• Ensure the successor will bring a high level of knowledge and expertise to the business.

• Ensure the clients feel comfortable with the successor before he retires completely.

• Traits of the successor – honesty, integrity, smart, open to learn and be mentored, respectful.

• Looking for a strategic successor who is looking for the opportunity to take what Henry has built,

combine it with what they have built and create something greater.

Over the last year Henry has started conversations with advisors he has met at various industry

seminars and events. He has identified two potential candidates; however, he is unsure as they are

very different from him.

ADVOCIS COPYRIGHT ©2021 TFAAC 22Potential Candidate 1 Ashley, age 26, 3 years in the business, 2 yr. Business Administration degree from local college, grew up close by, no designations, licensed for both insurance and investments, single, no children, AUM: $1M, 100 clients, mainly friends and family. Ashley is very tech-savvy and does all her planning with clients using software, keeps her files electronically and likes meeting with clients virtually, however, she continues to meet clients in person at least once per year. Ashley does not have anyone working with her. Potential Candidate 2 Sandeep, age 35, 10 years in the business, graduated from U of T, grew up in Toronto with parents who immigrated to Canada from India. Sandeep recently bought a small property to get out of the city. He holds his CFP and is licensed for both insurance and investments. He is married and has 2 children, age 5 and 3. AUM: $5M, 350 clients, actively marketing and building his business through COIs, referrals and being present in the community. Like Ashley, Sandeep is tech-savvy and enjoys using software and conducting virtual meetings. He switched all his records to electronic a few years ago when he hired an administrative assistant, Alex. Alex has been invaluable to Sandeep, he is well organized, tech-savvy and has excellent ideas for marketing and prospecting. ADVOCIS COPYRIGHT ©2021 TFAAC 23

Back to Table of Contents...

B: Case Study Questions

Q1. What biases and assumptions could Henry explore to make sure he is not making any

decisions based on these?

ADVOCIS COPYRIGHT ©2021 TFAAC 24Q2. What biases do you think Ashley and Sandeep may have that they would need to work through? ADVOCIS COPYRIGHT ©2021 TFAAC 25

Q3. What strategies could Henry use when bringing a successor into his business in order to foster

a better connection between the successor, the employees and the clients?

ADVOCIS COPYRIGHT ©2021 TFAAC 26Back to Table of Contents... Presentation 2: Planning: Pivot to the New Reality ADVOCIS COPYRIGHT ©2021 TFAAC 27

ADVOCIS COPYRIGHT ©2021 TFAAC 28

ADVOCIS COPYRIGHT ©2021 TFAAC 29

ADVOCIS COPYRIGHT ©2021 TFAAC 30

ADVOCIS COPYRIGHT ©2021 TFAAC 31

ADVOCIS COPYRIGHT ©2021 TFAAC 32

ADVOCIS COPYRIGHT ©2021 TFAAC 33

Back to Table of Contents...

Case Study Activity: The Young Family

Learning Objective: To develop cash flow and budgeting recommendations for a

young family in order to stay on track towards their goals.

A: The Facts

The Clients

The clients, Jack and Kaila, have been together for 7 years. They have a young child together, Harry

(4 years old). This is Jack’s second marriage and his son, Jacob (9), also lives with them.

Note: For the purpose and focus of this case study, this case will not deal with the impact of family

property implications.

Name Age Marital Status Employment Annual Income Annual Income

Status Pre-Covid Current Year

Jack 38 Married Employed $88,000 $68,000

– 2nd marriage

Kaila 36 Married Employed $82,000 $82,000

Dependents

Name Age Relationship

Jacob 9 Son of Jack

Harry 4 Son of both Jack & Kaila

Health

Name Health Longevity

Jack Good; no concerns 85 - 90

Kaila Good; no concerns 85 - 90

ADVOCIS COPYRIGHT ©2021 TFAAC 34The clients and Faisal started working together as Faisal made a change to his marketing to focus on

the virtual and social media platforms. Faisal starting working with the couple over the last year.

Things got put on hold given the pandemic.

As the couple’s advisor, Faisal has had discussions with them about financial planning, but they did

not see the benefit of it (even though Jack and Kaila have several objectives that they want to

achieve). Faisal’s belief is that high income earners aren’t the only ones who need financial planning.

Every parent, grandparent, spouse, common-law partner, business or professional person should

have a plan.

Current Financial Situation

Their Advisor, Faisal, sat down virtually with his clients and looked to get an update on the couple’s

situation. As part of his process, he looked to get an updated listing of Asset and Liabilities of his

clients.

Net Worth Statement

Assets Ownership Jack Kaila Joint

Cash in the Bank Joint Account – Average balance $2,800

RRSP Beneficiary – Jack’s previous $34,500 $33,400

spouse. Jack’s account is with

another advisor.

TFSA Successor Owner – Each Other $10,000 $11,600

Beneficiary – Each Other

House Jointly owned $523,000

Liabilities

Debt - Mortgage ($410,000)

Debt – Credit Cards ($10,500)* Minimal

Net Worth: $34,000 $45,000 $115,800

*steadily increased over time.

ADVOCIS COPYRIGHT ©2021 TFAAC 35Insurance Coverage 1. Mortgage Insurance They refinanced their mortgage given the lower interest rates that were available. When they refinanced their mortgage, they purchased mortgage insurance. Making sure the mortgage is paid off when they pass away is a priority for them. 2. Group term Insurance Kaila has Group term life insurance offered at her place of employment; set to expire at age 65. Amount = $100,000 Additionally, the Advisor wanted Jack and Kaila to reassess their household expenses. They had never undertaken this exercise before. They never realized what they were spending their money on. And what if any deficiencies/surplus they had. ADVOCIS COPYRIGHT ©2021 TFAAC 36

Cash Flow Statement

Pre- Current

Covid Year Notes

Non-Discretionary

Utilities $600 $660 Slightly more given more time spent at

home

Mortgage $1,870 $1,660 Decreased due to refinancing at a lower

rate

House Insurance/Property Taxes $550 $550

House Maintenance $120 $120

Credit card interest $130 $160

Car Insurance/fuel/costs $125 $100 Decreased due to less commuting

Childcare/Children Costs $3,400 $1,400 Decreased due to various closures. Help

from parents.

Cell Phones/Internet $180 $190

Pet - Ralphie $40 $40

Medical $30 $30

Groceries $600 $800 More meals at home.

Discretionary

Vacations/Travel $500 $100 Decreased due to travel restrictions

Subscription Services (Netflix, $10 $45 Increased due to various lifestyle

Amazon, etc.) restrictions

Entertainment (sporting events, beers $200 $90 Decreased to various health restrictions

with buddies, etc.)

Eating Out $200 $60 Decreased to various health restrictions

Clothing $60 $20 Business clothes purchases have been

less due to working at home.

Total Expenses: $8,615 $6,025

Given their greater time at home, and some of their household expenses have gone down this year,

this may allow the couple to reassess where to re-allocate the surplus cashflow to protect their family

going forward.

ADVOCIS COPYRIGHT ©2021 TFAAC 37The Problem Last year, Jack had a change in his employment given the economic downturn. He had to rely on government programs for a short period of time. Overall, he suffered a drop in his income. For Kaila, her job shifted to her working from home. This meant juggling her work responsibilities with taking care of two small children. They did receive some extra help from Jack’s parents. During their marriage, they have had difficulty with their finances. They have never really put away extra funds in case their financial circumstances changed – such as with the recent pandemic. They have had issues separating wants from needs. Prior to the pandemic, the couple loved going on vacations down to Mexico. They spent money on the latest tech gadgets and beers with the buddies was on the agenda for the weekends. As a result, credit cards debt started to increase over time. They did take advantage of the credit card deferral options offered by the credit card companies. The COVID-19 pandemic has heightened the couple’s anxieties around their physical and financial security. They believe it is time to consider “getting their house in order” and work with Faisal to develop a plan. ADVOCIS COPYRIGHT ©2021 TFAAC 38

Back to Table of Contents...

B: Case Study Questions

Q1. Part A

Now that the Advisor has an updated view of his clients' financial picture, what type of

questions should the Advisor be asking these clients or other clients he has that are now

seeing a pivot to their financial situation?

ADVOCIS COPYRIGHT ©2021 TFAAC 39Q1. Part B

What should be the clients’ priorities given their new focus on financial planning?

ADVOCIS COPYRIGHT ©2021 TFAAC 40Q2. Part A

Establish and outline whether the clients have sufficient life insurance protection. Consider the

life insurance needs for the clients to consider in your recommendation for coverage (based on

current assets and liabilities).

ADVOCIS COPYRIGHT ©2021 TFAAC 41Q2. Part B

Address why mortgage insurance does not provide the appropriate coverage they need.

ADVOCIS COPYRIGHT ©2021 TFAAC 42Q3. Faisal made the shift to using online platforms and other ways to reach his clients. As advisors,

discuss what shifts you could make or have made to attract and retain clients.

ADVOCIS COPYRIGHT ©2021 TFAAC 43Back to Table of Contents... Presentation 3: Customized Solutions for Managing Risk ADVOCIS COPYRIGHT ©2021 TFAAC 44

ADVOCIS COPYRIGHT ©2021 TFAAC 45

ADVOCIS COPYRIGHT ©2021 TFAAC 46

ADVOCIS COPYRIGHT ©2021 TFAAC 47

ADVOCIS COPYRIGHT ©2021 TFAAC 48

ADVOCIS COPYRIGHT ©2021 TFAAC 49

ADVOCIS COPYRIGHT ©2021 TFAAC 50

ADVOCIS COPYRIGHT ©2021 TFAAC 51

Back to Table of Contents... Case Study Activity: Adjusting the Plan for a Small Business Owner Learning Objective: To create strategies for a business owner to reduce their risk, create a succession plan and transfer wealth from their business. A: The Facts Tom Brady grew up in the ‘70’s to the smell of freshly baked donuts as his parents worked 14 hours daily, 7 days a week running their ‘Donuts to Die For’ bakery on the highway to Gravenhurst, Ontario. Being the only child, he was privileged to graduate from private school and then with a Bachelor of Science, Hotel and Food Management degree in 1990. He’d seen how hard his parents worked and was determined to work smart and give his parents a well-deserved retirement. A lesson he learned that stuck in his head was that, you only score if you take the shot. He was not afraid of taking risks. Billy, a friend from high school joined a brokerage and seeing that Billy needed some sales, Tom bought a $250,000 Term 10 life insurance policy and started saving $500 a month investing in stocks Enercare, Blackberry, Royal Bank, Gold Corp and Potash Corp. In 1992, Tom married his childhood sweetheart Josie, and together they embarked on the shared vision to expand Donuts to Die For. Since the towns in Ontario were saturated with coffee shops, Tom and Josie established outlets on various highway routes to cottage country. They expanded their inventory from intense caffeination and glazed delights to everything a trucker or weary travelling family would need on a highway ride. In 1995, they had a son, David, followed by a daughter, Becky, in 1997. When Josie was pregnant with David, she got a $250,000 Term 10 life insurance policy from Billy. A couple times a year, Billy would stop by for fresh coffee and donuts and a half hour meeting with Tom. While they talked about their friendship, family and sports (often about a famous namesake quarterback), Billy avoided discussing business. He thought Tom was doing very well and no doubt guided by other professionals. After all, Tom had never missed a premium payment. Indeed, his policy renewed in 2001, 2011 and was about to renew in 2021. Tom, on the other hand, felt his stock portfolio with Billy had done well. He had gradually increased his monthly savings to $1,500 and was now, by his best estimation, worth a respectable $1,500,000. He’d seen the value swing but thought that was to be expected in the ever-volatile stock market. ADVOCIS COPYRIGHT ©2021 TFAAC 52

By 2010, Tom and Josie had 5 franchises . On the advice of their accountant, Tom’s 70+ year old parents did an Estate Freeze and handed the reins over to Tom and Josie. Tom and Josie drew just enough from the business to cover their personal expenses and their accountant did not see the need for them to set up a RRSP. Tom and Josie’s parents are doing well in their retirement. Tom’s Dad had a stroke last year but has recovered almost fully and his Mom and Dad recently decided to move from their 5-acre property into a small bungalow so their maintenance is much easier. They both have long life expectancies as their parents lived into their 90s. Josie’s parents are in their 80s and are also healthy and active. Josie’s sister had breast cancer a few years ago but she was fortunate that it was discovered early and she has been in remission for 2 years. In 2020, COVID hit. As good citizens of the community, Tom and Josie quickly implemented local public health guidelines making their businesses safe for staff and customers. Their wares were limited to take-out and they saw a manageable 10% drop in gross sales. Now aged 49, Tom experienced sharp abdominal pain in September 2020. During the four-day period of seeing their family doctor and going to a hospital, Tom feared the worst. Thankfully, Tom was diagnosed with acute diverticulitis, an entirely manageable condition, and strongly advised to make lifestyle and dietary changes. For the first time, Tom stayed away from work for two weeks and worried about Josie and their children’s future if he had a serious medical condition or worse, if he was no more. His life insurance was good only until he turned 75 and he did not know what he needed to protect his family’s financial future. Their business had a reserve of $5 million and the 5 shops they owned were worth $3 million. They had a business loan outstanding of $1 million and their $2 million estate home in Newmarket had a $250,000 mortgage. Tom had increased payments at the last renewal and planned to pay off the balance in 5 years. Tom shared his fears with Josie and told her that he had searched online and found a Financial Planner in Bradford and arranged a meeting on Zoom this week. ADVOCIS COPYRIGHT ©2021 TFAAC 53

In the introductory meeting, Tom and Josie talk about how they have an enviable business running. Tom tells the financial planner about his medical episode but says he has been cleared and although both of them are a little overweight, they are healthy. He recounts the Estate Freeze that his parents did and wants to know if he should consider doing the same to get David into the business. David has worked in the business every summer throughout school and will soon graduate from business school. Becky is not interested in joining the business and wants to become a Nurse. Tom and Josie want to leave their children an equitable inheritance and want the financial planner to present them with some options. They’ve never had a Retirement and Estate plan documented. They show a recent statement of their Non-reg stock portfolio which still has only 5 Canadian stocks. They want to hang their hats in 5 years and travel which is something they have not been able to do. ADVOCIS COPYRIGHT ©2021 TFAAC 54

Back to Table of Contents...

B: Case Study Questions

Q1. What would you suggest the financial planner recommend to reduce their risk and preserve

their capital?

ADVOCIS COPYRIGHT ©2021 TFAAC 55Q2. What would you suggest the financial planner recommend to preserve their estate and

distribute equitably between their children?

ADVOCIS COPYRIGHT ©2021 TFAAC 56Q3. What would you suggest the financial planner recommend for their business succession

planning? What if David decides he does not want to keep the business and they find a buyer

5 years from now?

ADVOCIS COPYRIGHT ©2021 TFAAC 57Back to Table of Contents... Presentation 4: Deeper Connections in a Virtual World ADVOCIS COPYRIGHT ©2021 TFAAC 58

ADVOCIS COPYRIGHT ©2021 TFAAC 59

ADVOCIS COPYRIGHT ©2021 TFAAC 60

ADVOCIS COPYRIGHT ©2021 TFAAC 61

ADVOCIS COPYRIGHT ©2021 TFAAC 62

ADVOCIS COPYRIGHT ©2021 TFAAC 63

ADVOCIS COPYRIGHT ©2021 TFAAC 64

ADVOCIS COPYRIGHT ©2021 TFAAC 65

ADVOCIS COPYRIGHT ©2021 TFAAC 66

Back to Table of Contents... Case Study Activity: Customizing Client Connectivity Learning Objective: To consider how advisors can set up and conduct in-person and virtual meetings and prepare for and deal with unexpected issues in a compliant way. A: The Facts The Situation You are an insurance-only advisor who has built a practice working collaboratively with other Financial Advisors and accounting firms to offer comprehensive insurance planning for their clients. You have built a digital practice, meetings are primarily conducted using virtual technology, all records are electronic, and the firm is completely paperless. At the beginning of the pandemic, you moved to working from your home office and have continued to do so. The Client You have been referred to Dr. Shawna Johnson and her husband Mr. Simon Shields. They are both 72 years old and been married for 45-years. Dr. Johnson is a family doctor who spends much of her time at her busy walk-in clinic. She has no plans to retire and will work until she is no longer physically able. Mr. Shields has been retired from teaching for a couple of years and spends most of his time around the house, where he invites friends/family to enjoy their large backyard. COVID has presented some major challenges for Dr. Johnson and Mr. Shields. Dr. Johnson has not been able to work at the clinic (she’s high risk and not seeing patients until a vaccine is available). She finds herself puttering around the house, not really sure what to do with herself. With the extra time on her hands, Dr. Johnson decides that she’s going to spend time organizing/managing her financial affairs. The Problem When Dr. Johnson sits down at her home office, she has boxes filled with unopened mail from investment dealers and insurance companies. She’s overwhelmed and feels paralyzed to get anything accomplished. The meeting is booked for 2-weeks from now and she needs a crash course on technology. ADVOCIS COPYRIGHT ©2021 TFAAC 67

B: Case Study Questions

Q1. What are some tasks that can/should be completed pre-meeting for a client with limited

technological knowledge?

ADVOCIS COPYRIGHT ©2021 TFAAC 68Q2. What are some tools/techniques that can be used during a virtual meeting? ADVOCIS COPYRIGHT ©2021 TFAAC 69

Q3. What technology/processes can be implemented or executed post-meeting? ADVOCIS COPYRIGHT ©2021 TFAAC 70

Back to Table of Contents...

Advanced Learning Modules

1. Building an Inclusive Practice

Learning Objective: To examine how to effectively reduce implicit prejudice and encourage

inclusion and diversity in our new remote environment.

Reading List:

Title: Reducing Implicit Prejudice

Author: Calvin K. Lai, Kelly M. Hoffman and Brian A. Nosek

Source: Social and Personality Psychology Compass

Title: Sustaining and strengthening inclusion in our new remote environment

Author: Diana Ellsworth, Ruth Imose, Stephanie Madner, and Rens van den Broek

Source: McKinsey & Company

CE Credit: 1.0 Ethics

2. Planning: Pivot to the New Reality

Learning Objective: To consider how financial advisors and financial planners can help their

clients (with a focus on individuals and small business owners) pivot to the new reality, take

action, and revise their financial plans while keeping sight of their goals.

Reading List:

Title: How entrepreneurs are adapting to the pandemic

Author: Sylvia Ratte and Isabelle Bouchard

Source: BDC

Title: Knowledge Bureau 2020 Fall Economic Report

Source: Knowledge Bureau

CE Credit: 2.0

ADVOCIS COPYRIGHT ©2021 TFAAC 713. Customized Solutions for Managing Risk

Learning Objective: An exploration of how financial advisors and financial planners can

continue to help clients (with a focus on individuals and small business owners) reach their

financial goals while taking decisive action to mitigate risk.

Reading List:

Title: Get the Most from the Canada & Quebec Pension Plans by Delaying Benefits

Authors: Bonnie-Jeanne MacDonald, PhD, FCIA, FSA, National Institute on Ageing, Ryerson

University

Source: National Institute on Ageing, Ryerson University and FP Canada

CE Credit: 2.0

4. Deeper Connections in a Virtual World

Learning Objective: Embracing new ways of staying connected with clients to meet their shifting

support needs while fostering the ongoing development of a trust-based relationship.

Title: Meet the Next Normal Consumer

Author: Victor Fabius, Sajal Kohli, Sofia Moulvad Veranen, and Bjorn Timelin

Source: McKinsey & Company

Title: How COVID-19 has pushed companies over the technology tipping point – and

transformed business forever

Author: McKinsey & Company

CE Credit: 1.0

ADVOCIS COPYRIGHT ©2021 TFAAC 72Back to Table of Contents...

How to Access Advanced Learning Modules

Login to advocis.ca using your Advocis ID and password and click on Update 2021 in the Continuing

Education section of your Dashboard.

Step 1: Login

Step 2: Click on Update 2021

Update 2021

ADVOCIS COPYRIGHT ©2021 TFAAC 73Back to Table of Contents...

Resources Available Online

Individuals registered for the Update 2021 seminar can access the following resources that

supplement the Update 2021 seminar presentations (available via the Update 2021 Advanced

Learning Modules):

Diversity & Inclusion pre-reading – created by Michele Byrne

Diversity & Inclusion resource list – curated by Michele Byrne

Canada’s Economic Response Plan – tips for helping clients, prepared by Cindy Marques

Whiteboard to video demo for client communication – short video, created by Wendy

Brookhouse

Video production tips – resource from Sun Life

Video Marketing Guide – resource from Sun Life

Upon completion of the seminar, individuals will also be able to access the following:

Solutions to the Case Study Activities

Advocis CE Certificate

ADVOCIS COPYRIGHT ©2021 TFAAC 74Back to Table of Contents... Notes ADVOCIS COPYRIGHT ©2021 TFAAC 75

ADVOCIS COPYRIGHT ©2021 TFAAC 76

ADVOCIS COPYRIGHT ©2021 TFAAC 77

ADVOCIS COPYRIGHT ©2021 TFAAC 78

You can also read