Overview of the Patent Landscape in the Blockchain, Cryptocurrency, and Cryptographic Token Space

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Overview of the Patent

Landscape in the

Blockchain, Cryptocurrency,

and Cryptographic Token

Space

CLIENT ADVISORIES

October 12, 2018

A. Overview of the Analysis

This analysis identified and processed over 8,000 patents and patent applications worldwide

relating to blockchain, cryptocurrencies, and cryptographic tokens as of July 2018. The analysis

did not include patents and applications with a priority date before 1998, with the assumption

that patents have a maximum validity of 20 years and therefore patents with priority dates before

1998 have expired.

1. Blockchain Platform Architecture and Scope of Search

Blockchain, cryptocurrencies, and cryptographic tokens leverage a combination of preexisting

technologies to implement distributed information storage and transaction management

processes, including elliptic curve cryptography (ECC) applied to public and private keys,

cryptographic hashes, Merkle trees, emergent consensus based on distributed inputs, dynamic

adjustments to computing difficulty, proof of work concepts (currently driving Ethereum and

Bitcoin), proof of stake concepts (currently driving some cryptocurrencies and planned for

adoption by Ethereum), and conditional contracts that can self-execute.

These fundamental blockchain technologies are deployed in various configurations for different

applications, and the platforms continue to evolve actively. Consequently, an ecosystem patent

analysis focused on blockchain and cryptocurrencies may choose to be more focused on today’s

implementations, or may try to anticipate where blockchain and blockchain-based business

models will be years in the future. For example, Bitcoin and Ethereum do not currently encrypt

the transaction data while stored across nodes, and the flow of crypto funds can be traced

sequentially by examining the transaction ledger at any time. This means that to maintain

privacy for financial transactions, the accounts themselves must be secured and anonymized, and

data stored within crypto wallets must be encrypted. Techniques exist to transmit or store

encrypted data across the blockchain (e.g., via message payloads, through smart contracts, etc.),

but those are inefficient methods for managing encrypted information and are not logical

applications for the current Bitcoin or Ethereum frameworks. A proposal exists, however, to

deploy encryption more broadly across Ethereum, which would alter the data architecture of the

Ethereum blockchain platform, change the dynamics of privacy, and enable a new class of

blockchain applications centered on encrypted data.

To select the dataset for this analysis, the patent search focused on the fundamental aspects of

blockchain technology, cryptographic currencies, and cryptographic tokens, as currently

implemented in existing blockchain applications and as expected to evolve in the foreseeable

future. The search focused on claims of pending patent applications and issued patents,

Copyright © 2021 Wilson Sonsini Goodrich & Rosati. All Rights Reserved.

worldwide, and sought to identify applications and patents related to blockchain architecture,

distributed ledger technology, competing and parallel consensus algorithms, and smart

contracts.

A broader search identified an additional 5,000 patents and applications by expanding the scope

of the analysis to include patents from related fields while also searching within the

specifications of applications and patents. To achieve a sharper focus on the core aspects of

blockchain, cryptocurrencies, and crypto-tokens, these results were not included in the dataset

analyzed below, but may be considered in a follow-up analysis.

Depending on applications of blockchain, additional applications and patents may be relevant.

For example, a previous analysis of patenting activities in the payments and omnichannel

commerce space identified over one million applications and patents (more details here), and to

the extent that blockchain business models include commerce aspects, a subset of these

application and patents may also be of interest. A follow-up to this analysis may also include

other industry segments in which blockchain and cryptocurrency/tokens are likely to be deployed

in the future.

2. Limitations of this Study

Patents are an indicator of technical innovation and business activities in specific industry areas,

and can be used as a metric for R&D investment (see, e.g., the discussion of the relationship of

patents and R&D here). But it is important to understand that the correlation between patenting

and business operations is imperfect, and therefore patent-based Key Performance Indicators

(KPIs) should not be used as stand-alone metrics to evaluate or compare any entity. Please see

Section C (About This Analysis) below for a deeper discussion of how patent-based metrics can

understate or overstate the business activities and technical innovation of specific entities.

It is also important to understand that any patent search in high-growth areas like blockchain

and cryptocurrencies is just a snapshot in time based on then-current public data, and that the

figures and rankings presented in this study are likely to change significantly within the next 12

months. Rather than focusing on any particular ranking or number, the data below should be

reviewed more for trends. For example, it is interesting to note that entities from the financial

space, like MasterCard, Visa, Bank of America, and Nasdaq, are among the top patent filers in

emerging technology areas like blockchain and cryptocurrencies, along some of the largest

traditional patent holders like Microsoft, Samsung, and Intel, which was not common in the past

in other traditional industries.

Another important observation when reviewing the results presented below is that some entities

are unexpectedly missing from the rankings or are ranking lower than expected. It is virtually

certain that many prominent companies and organizations have a strong pipeline of patent

applications that were filed in the past 12-18 months, and because those applications were not

public as of the date of the search, they are not reflected in these figures. This means that many

other patent applications in the blockchain and cryptocurrency space will likely be published in

the next few months, and therefore the results shown here will probably evolve rapidly over the

next 12-24 months. Any patent search in high-growth areas like blockchain and cryptocurrencies

should be perceived as a snapshot in time and not as a definitive ranking.

As a final introductory note, this analysis was performed using Boolean searches across large

patent databases and techniques for automated processing of large datasets, without a review of

actual claims. Consequently, individual patents and claims were not reviewed, and therefore no

knowledge of any particular patent or application was acquired.

Section C (About This Analysis) below discusses additional limitations in the data and results of

this study.

B. Discussion

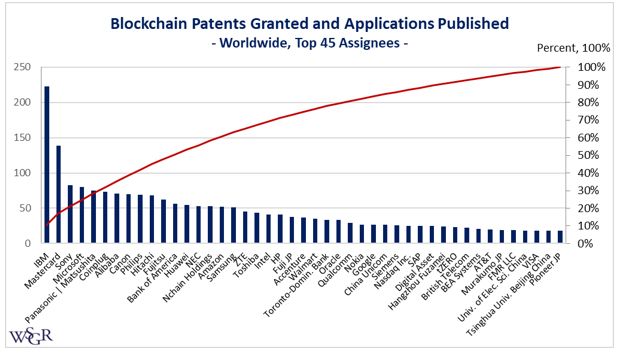

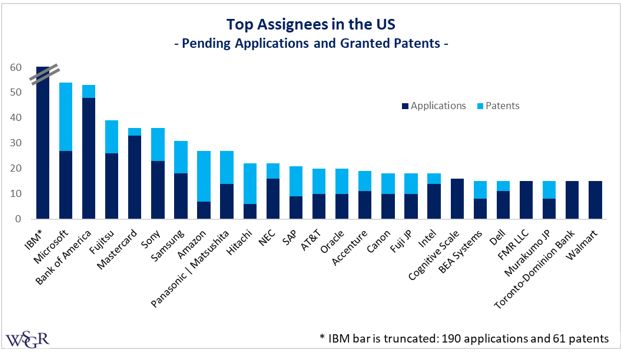

1. Global Patent Landscape

Fig. 1 shows the total number of patents granted and pending patent applications for the top 45

patent filers worldwide as of July 2018.

Copyright © 2021 Wilson Sonsini Goodrich & Rosati. All Rights Reserved.

Fig. 1

Top 45 Worldwide Patent Filers

(Patents Granted and Applications Pending)

Before addressing individual entities from Fig. 1, it is interesting to note that IBM and

Mastercard together account for almost 20 percent of all patents and applications held by the top

45 filers in the blockchain and cryptocurrency/token space. The top five patent filers hold almost

30 percent of the patents and applications shown in Fig. 1, and the top 12 filers hold over 50

percent. In relative terms, this type of concentration is also seen in other technology segments,

with a few prolific patent filers tending to hold a disproportionate percentage of patents and

applications relative to the rest of the industry. This suggests that as the blockchain and

cryptocurrency industries mature, they may also experience strategies and trends similar to

those previously seen in other industries (e.g., licensing programs run by some of the top patent

holders, development of large patent portfolios for deterrence and defensive purposes, patent-

centric technology transactions and acquisitions, offensive and defensive patent assertions and

litigation, etc.).

From Fig. 1, it is noteworthy that financial entities like Mastercard, Visa, and Bank of America

are major patent filers in the blockchain and cryptocurrency spaces. This is a positive surprise

given that financial entities were not patenting heavily in the past. It is not surprising, however,

to see these three companies among the more prolific patent filers since an analysis of

commerce patents from 2017 also identified them as strong patent filers in commerce (see Fig.

1 here). Additionally, since both Visa and Mastercard have a public track record of strategic

acquisitions, it is possible that they may own additional applications and patents that are not

held under their direct names yet, and therefore the number of applications and patents held by

each of them in the blockchain and cryptocurrency/token segments may be even larger than

shown here.

IBM’s top ranking suggests that the company plans to include blockchain in its patent licensing

program going forward, which is something that other entities operating in the blockchain space

may want to consider as they shape their own patent programs.

Other top filers in Fig.1 are also traditional leading patent holders, including Sony, Microsoft,

Panasonic, Canon, Philips, Hitachi, Fujitsu, NEC, Samsung, and Toshiba. The presence of these

household names among the top blockchain and cryptocurrency/token filers is not surprising and

confirms that these companies are continuing to evolve with new technologies. In particular,

Microsoft’s emergence as a leading cloud player in the past few years and its consistently-high

patenting rate make it a predictable presence on this list.

It is interesting to note the presence of Coinplug among the top filers, a prominent Korean player

in the Bitcoin space that operates a trading platform for Bitcoin and other cryptocurrencies. This

shows that emerging leaders in the blockchain and cryptocurrency segments are learning from

industry leaders in other technology sectors to develop strong patent positions while building

Copyright © 2021 Wilson Sonsini Goodrich & Rosati. All Rights Reserved.

their businesses (e.g., Samsung, also a Korean company, has been a leading patent filer across

many industry segments for years). Of the 73 patents and applications identified for Coinplug, 63

are presently in Korea and 9 are in the U.S., but the proportion of filings outside Korea is likely

to increase as the Korean applications mature into global patent families.

Alibaba and Amazon have been strong patent filers for the past few years in other technology

areas, and given their diversification across additional economic and technology sectors, their

high ranking in the blockchain patent landscape is also not surprising. The geographic

distribution of their patents is quite different, however, with Alibaba showing most patents and

applications in China and Amazon showing most patents and applications in the U.S. It is

interesting to note that Amazon’s portfolio includes filings across a broad range of geographies,

including China, Europe, Japan, Korea, Canada, Australia, and India, which suggests that

Amazon’s business plans are global.

nChain Holdings is not a household name, but is well known within the blockchain industry.

nChain is developing various applications running on top of blockchain. The company was

apparently acquired by a private equity firm in 2017 and continues to execute towards an

“Internet of Transactions.” HP, Intel, and Oracle have always had sophisticated patent programs,

and their leading rankings in this analysis suggest that blockchain and cryptocurrencies/tokens

are definitely part of their future business plans. In particular, it is certainly not unexpected to

see Oracle focused on blockchain given its high patenting rate and increasing focus on

commerce (e.g., consider Oracle’s strong ERP platform and its acquisition of Micros a few years

ago). Same with HP and Intel: as the companies morph into broader technology and services

providers, expanding away from their traditional core offerings, their interest in blockchain,

cryptocurrencies, and cryptographic tokens should be expected.

Google’s broad activities in commerce (e.g., Google Pay) and in other emerging technologies

also make it an expected presence in the top blockchain patent filers. Google’s patent portfolio

shows a particularly broad geographic dispersion compared to other companies, which suggests

that Google is mapping its interests in blockchain at a global scale. This is not surprising since

Google’s business is global in reach already, and new commerce offerings (e.g., Google Pay) are

natural complements to its suite of products and services across all geographies.

Walmart’s presence among the top 45 blockchain patent filers may appear unexpected, but it is

not: Walmart has been investing heavily in digital transformation and omnichannel technologies

over the past few years and has developed a significant patent portfolio in commerce.

Accenture’s high ranking is also not surprising given its strong global activities in technology

development and professional services in the recent past. This suggests that Accenture is

positioning its business to expand across blockchain and cryptocurrencies, so it will likely be a

leading consulting and strategic adviser in this industry for years to come.

Digital Asset is a strong emerging player in the blockchain space, backed by prominent strategic

and financial investors. Digital Asset seeks to deploy a platform leveraging distributed ledger

technology for regulated financial institutions. The company’s patent portfolio is concentrated in

the U.S., but alludes to global business plans given its other filings in China, Europe, Canada,

Australia, and Singapore.

tZERO’s business model seeks to leverage the immutability of blockchain transactions to

develop a securities trading platform. tZERO’s patent portfolio is a bit unusual because the

company appears to be located in the U.S., but its patent portfolio does not include any U.S.

applications of patents based on the records identified in this search. Instead, its portfolio is

dispersed across Australia, Canada, China, Europe, Korea, and Singapore.

Finally, the high global rankings of Chinese patent filers in the blockchain space are noteworthy

and are consistent with the concentration of companies in APAC with activities in the areas of

cryptocurrency, blockchain investments, ICOs, and emerging blockchain-based business models.

Aside from Huawei and ZTE, which are already well-known and leading patent filers across a

broader technology space, a number of newcomers are making a strong patent showing, such as

Hangzhou Fuzamei Technology, University of Electronic Science, and Tsinghua University

Beijing.

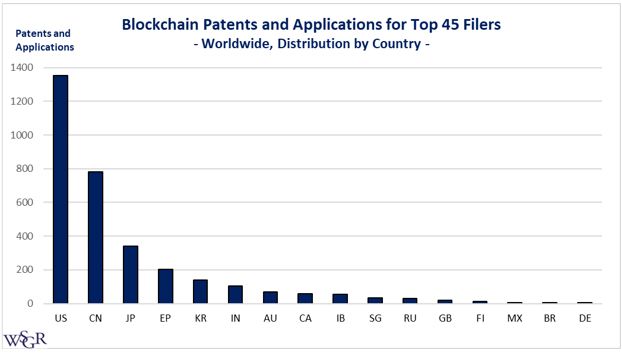

Fig. 2 shows the geographic distribution of patents granted and pending patent applications for

the top 45 patent filers worldwide as of July 2018.

Copyright © 2021 Wilson Sonsini Goodrich & Rosati. All Rights Reserved.

Fig. 2

Top 45 Worldwide Patent Filers

(Patents Granted and Applications Filed, Worldwide, by Filing Country)

Fig. 2 shows that while the U.S. remains the most popular intellectual property framework for

major patent filers, China ranks as a strong number two destination, ahead of the European

Union and Japan. This is consistent with the strong activities in blockchain and cryptocurrencies

shown by Chinese entities over the past three years, including a high concentration of Bitcoin

mining, ICOs and blockchain-centric business models. The total number of filings outside the

U.S. for the top 45 filers shown in Fig. 1 exceeds the U.S. filings, which suggests that any

company with global aspirations for blockchain-related business models will see an intricate

international web of patents in three-to-five years.

Fig. 3 shows the total number of patents granted and pending patent applications relating to

blockchain, cryptocurrencies, and cryptographic tokens, aggregated for all patent filers,

worldwide, by year. The chart shows the number of patents granted and applications published

during each calendar year. The chart starts with 2007 and shows an annualized figure for 2018

using the January-June 2018 numbers. This analysis identified more than 2,800 assignees, which

are included in Fig. 3.

Copyright © 2021 Wilson Sonsini Goodrich & Rosati. All Rights Reserved.

Fig. 3

Patents Granted and Applications Published

(Worldwide, All Filers, by Year of Grant/Publication)

To understand the trends shown in Fig. 3, it is important to remember that the figures shown are

patent publication dates and patent issuance dates, and that the underlying filing dates for each

year shown in Fig. 3 occurred sometime in the preceding five years, depending on the

publication delay for applications and length of the prosecution stage for patents. Consequently,

the figures captured in Fig. 3 are a real-time reflection of patent grants and application

publications by year, but trail by a few years the underlying industry focus on blockchain and

cryptocurrencies that led to those filings. To get a better understanding of the annual investment

rate in blockchain R&D as reflected by patent filings, the numbers shown in Fig. 3 should be

viewed in parallel with application filing dates. Fig. 4 provides that information.

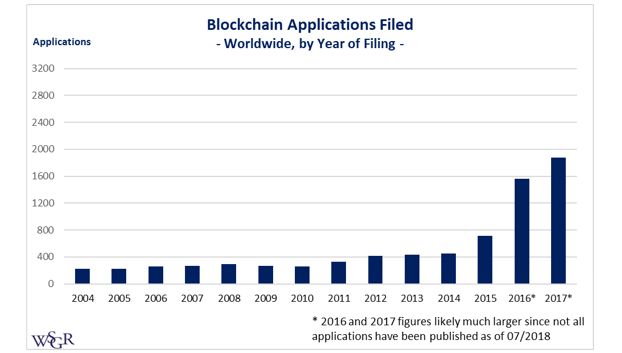

Fig. 4 shows the total number of patent applications relating to blockchain, cryptocurrencies,

and cryptographic tokens, aggregated for all patent filers, worldwide, by filing year. The chart

shows the number of patent applications filed during each calendar year. The chart starts with

2004 and shows annualized figures for 2018 using the January-June 2018 figure.

Fig. 4

Copyright © 2021 Wilson Sonsini Goodrich & Rosati. All Rights Reserved.

Patent Applications Filed

(Worldwide, All Filers, by Filing Year)

The 2004-2006 years, which are the starting point for Fig. 4, were intentionally selected to

predate by one-to-three years the first data point shown in Fig. 3, and should be a representative

metric for the economic activity that led to the patents granted and applications published in

2007 shown in Fig. 3. This correlation window continues for the figures shown in Fig. 4 relative

to Fig. 3, such that the 2014-2016 numbers from Fig. 4 should be an indicator for the global

investment in blockchain R&D that led to the 2017 number in Fig. 3. Indeed, a higher filing rate

in 2014-2015 coupled with a significant jump in 2016 filings as shown in Fig. 4 explain the jump

in 2017 patent grants and application publications shown in Fig. 3. Analogously, the acceleration

of application filings in the 2015-2017 period shown in Fig. 4 explains the large increase in 2018

grants and publications shown in Fig. 3.

As a side note, the predictive value and the accuracy of the data shown in Fig. 4 ends in 2017,

because many of the patent applications filed in 2017 and most of the applications filed in 2018

have not been published yet and are still confidential as of the date of this article (July 2018),

which is why the 2018 datapoint is not shown in Fig. 4.

Overall, considering the data from Fig. 3 and Fig. 4 together, it is clear that patenting in the

areas of blockchain, cryptocurrencies, and crypto tokens ramped up substantially starting in

2015, and it is safe to predict that when the full figures will be available for 2018, they will show

a further jump in patent grants and application publications.

2. U.S. Patent Landscape

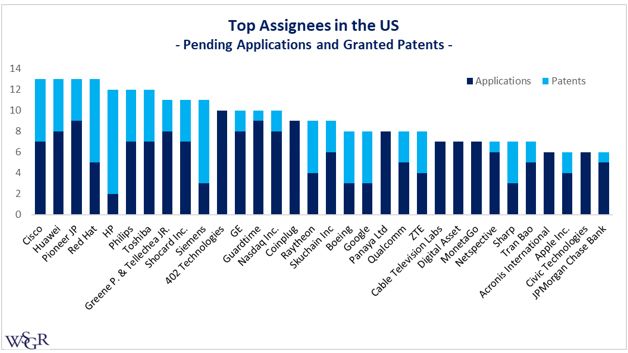

Figs. 5-a and 5-b show the total number of patent applications relating to blockchain,

cryptocurrencies and cryptographic tokens, aggregated for all patent filers, in the U.S., as of July

2018. The charts show the number of patent applications pending and the number of patents

issued for each assignee as of July 2018. The ranking sample was selected to include the top 57

U.S. assignees, ordered based on the total number of U.S. applications and patents. For

convenience, the dataset was split in two, with Fig. 5-a showing the top 25 assignees and Fig. 5-

b showing the next 32 assignees.

It is important to note that the numbers shown in Figs. 5-a and 5-b do not include published

applications filed under the Pacific Patent Cooperation Treaty (PCT) system, many of which were

likely filed in the U.S. For example, Visa has 10+ pending PCT applications that were filed in the

U.S. and were not included in this dataset, which would make Visa one of the largest filers in the

U.S. In Figs. 5-a and 5-b, however, only applications directly filed in the U.S. were considered to

narrow down the scope of the analysis and to avoid parsing out PCT application filings. The PCT

applications are included in the numbers from Fig. 1, and therefore Fig. 1 shows all global

applications and patents across individual countries and the PCT framework.

Copyright © 2021 Wilson Sonsini Goodrich & Rosati. All Rights Reserved.

Fig. 5-a

Top Assignees in the US (1-25)

(U.S. Applications Pending and Patents Granted, Excluding PCT/WIPO Applications)

Fig. 5-b

Top Assignees in the U.S. (26-57)

(U.S Applications Pending and Patents Granted, Excluding PCT/WIPO Applications)

As a high-level observation, the presence in this U.S. top ranking of leading commerce and

financial entities like Bank of America, Mastercard, Visa, Amazon, and Walmart is consistent

with their strong global showing in Fig. 1. Also, the top rankings for IBM, Microsoft and other

traditional large patent filers are also not surprising.

An interesting name among the top U.S. patent filers is Red Hat, a leading advocate for Open

Source software. This is not surprising, however, since Red Hat has been active in the

blockchain space, including its focus on a Blockchain-as-a-Service platform based on Ethereum.

More generally, Open Source is an active field in blockchain—see for example Hyperledger, an

industry-wide umbrella project of Open Source blockchains and related tools initiated by the

Linux Foundation. Open Source has a natural synergy with public blockchains given that they

Copyright © 2021 Wilson Sonsini Goodrich & Rosati. All Rights Reserved.

share inherent characteristics such as distributed development, transparency to review, and trust

premised on community policing.

With the exception of IBM, the absolute ranking of the companies shown in Figs. 5-a and 5-b is

not meaningful because the total numbers do not vary much among entities next to each other.

Instead, Figs. 5-a and 5-b should be studied for more general trends, such as the types of

entities that are patenting in the blockchain segment (e.g., traditional large filers vs. financial

institutions vs. pure blockchain/cryptocurrency players vs. newcomers).

A deeper analysis of the U.S. blockchain patent filers is deferred to a follow-up study, including

a segmentation by Cooperative Patent Classification (CPC) classes, patent-based KPIs, and

activities in other industry segments related to applications of blockchain and

cryptocurrencies/tokens.

3. Financial Institutions

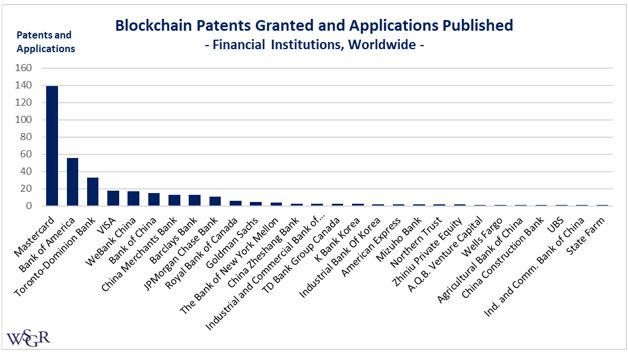

Fig. 6 shows the total number of patent applications relating to blockchain, cryptocurrencies,

and cryptographic tokens filed by financial institutions, aggregated globally, as of July 2018. The

chart shows the number of patent applications pending and the number of patents issued

globally for a number of entities whose primary business can be determined to fall within the

financial space.

Fig. 6

Top Financial Institution Assignees

(Worldwide, Applications Pending, and Patents Granted)

Fig. 6 shows that financial institutions have embraced patenting in the blockchain,

cryptocurrency, and cryptographic token industries. This is not a surprise given the strong

showing of financial institutions in commerce patent rankings (see, e.g., this article). Banks and

other financial institutions outside the U.S. are heavily represented in this ranking, which is

consistent with the global interest in blockchain applications for financial applications. As banks

and financial institutions experiment with blockchain as a platform for transfer and settlement of

funds across geographies, patenting activities by banks and other financial entities are likely to

increase further and quickly, both in the U.S. and outside the U.S.

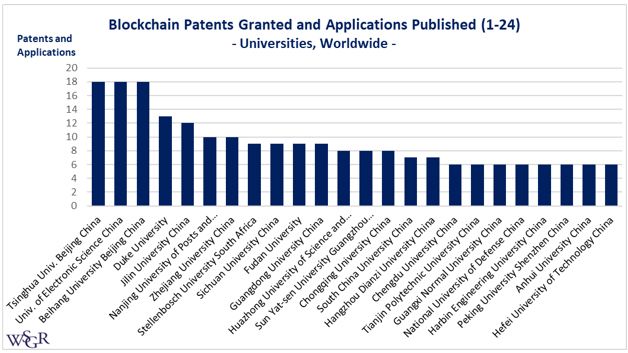

4. Universities

Figs. 7-a and 7-b show the total number of patent applications relating to blockchain,

cryptocurrencies, and cryptographic tokens filed by universities, aggregated globally, as of July

2018. The charts show the number of patent applications pending and the number of patents

issued globally for a number of academic institutions. Due to the large number of assignees

identified, the results are shown only for universities with at least three applications and

patents, and were divided into two different charts for clarity.

Copyright © 2021 Wilson Sonsini Goodrich & Rosati. All Rights Reserved.Fig. 7-a

Top University Assignees (1-24)

(Worldwide, Applications Pending, and Patents Granted)

Fig. 7-b

Top University Assignees (25-49)

(Worldwide, Applications Pending, and Patents Granted)

Fig. 7-a and 7-b show that blockchain, cryptocurrency, and cryptographic token innovation is

occurring in academia on a global scale. The strong presence of Chinese universities in these

rankings is noteworthy and suggests that the Chinese economy will play a major role in adopting

blockchain technologies in the future and shaping the evolution of the industry.

5. Unknown Assignees

A classic problem in any patent search is the inability to accurately identify all assignees for the

patents and applications included in the analysis dataset. The issue may arise either

inadvertently or intentionally. The inadvertent omission or misidentification of assignees can

occur due to innocuous issues that occur during the patent prosecution process, such as delayed

identification of the actual assignee after the application filing, listing inventors as assignees or

Copyright © 2021 Wilson Sonsini Goodrich & Rosati. All Rights Reserved.joint assignees, or mistakes made by the Patent Office in the receiving country or in other

countries. The intentional omission or misidentification of assignees can occur when a company

seeks to obscure the fact that it is indeed the owner of the patents, in which case patents could

be assigned to a shell entity with an unrelated name or the assignee name may be intentionally

omitted during the prosecution process.

There are techniques to identify the real assignees in interest (e.g., parsing out the applications

and patents by CPC classes and subject matter, searching by inventors, running parallel

corporate entity searches to establish parent-subsidiary relationships, etc.), but such techniques

require significant efforts that go beyond the scope of this project. In this analysis, efforts were

made to consolidate easily ascertainable related entities into a single corporate assignee, but

no attempt was made to identify missing assignees or to correct for unknown entity names.

The inability to identify assignees accurately triggers two immediate concerns. The first concern

is that the patent holdings of any particular entity may be understated. For example, looking at

some of the household names shown in the rankings in Fig 5-b and known to be prolific patent

filers in other technology segments, some of the figures shown are surprisingly low. It is

certainly possible that some of those companies only ramped up their blockchain patenting

efforts in the past 18 months, and therefore their recent applications are not publicly known yet.

But it is also possible that some of those companies already have significant patent portfolios in

the blockchain and cryptocurrency space, whether organically developed or acquired, and they

cannot be identified fully without a concerted effort to identify and consolidate unknown

assignees.

A second concern about unknown assignees is that patents may be aggregating under the control

of entities that could later assert them broadly across the industry, seeking to extract mass

royalties or possibly even injunctions, without early industry visibility.

How significant is the issue of unknown assignees in the blockchain and cryptocurrency/crypto-

token space? The search retrieved 355 U.S. patents and 1,115 worldwide patents and

applications with unknown assignees, which is more than 12 percent of the total holdings in both

cases. Many of these missing assignees will be added over time, as applications are prosecuted

towards issuance, but a significant level of uncertainty regarding patent ownership will almost

certainly remain in the blockchain and cryptocurrency industries.

It is also worth mentioning that that there are 425 Chinese applications and patents that do not

identify any assignee as of July 2018, so even more than in the U.S. Because many Chinese

companies pursue a China-first filing strategy with subsequent expansion into the U.S. and other

countries through the Patent Cooperation Treaty (PCT), these applications and patents are likely

to further compound the level of assignee uncertainty in the U.S. and in other countries around

the world, depending on how many of those families will eventually add accurate assignee

information.

Overall, the issue of patent ownership will likely be a concern for the blockchain and

cryptocurrency industries given these early datapoints, and the industry should consider taking

steps to address this issue sooner rather than later.

6. The Extended Blockchain and Cryptocurrency Patent Landscape

The search discussed in this study identified 8,000 patents and patent applications worldwide

relating to blockchain, cryptocurrencies, and cryptographic tokens as of July 2018, and a broader

search that traded specificity for overinclusion identified an additional 5,000 patents and patent

applications worldwide that have some direct nexus with blockchain technology and architecture.

It is important to understand, however, that a comprehensive analysis of the blockchain patent

landscape needs to consider a much broader patent dataset. For example, since cryptocurrency

transactions rely heavily on encryption, patents relating to elliptic curve cryptography,

cryptographic hashes, and other techniques for efficient data encryption using public and private

keys would also need to be considered as fundamental enabling blocks. Some pioneering

patents that relate to technologies that underpin blockchain have expired, but others remain in

effect and may be relevant.

Also, since blockchain is being deployed globally as a platform that supports a wide range of

business models, patents, and applications that relate to each such business model may deserve

consideration on a case-by-case basis. For example, a 2017 patent landscape analysis focused

on commerce identified over one million patents and applications relating to a wide range of

commerce technologies and business models (see, e.g., this article), and some of those may be

Copyright © 2021 Wilson Sonsini Goodrich & Rosati. All Rights Reserved.relevant to specific applications of blockchain, cryptocurrencies, and cryptographic tokens in the

commerce space.

C. About This Analysis

1. Limitations of Patent-Based KPIs

Using patents as a metric for the business activities of individual companies in the technology

space must be cross-checked against other factors to establish its relevance and accuracy.

Without additional analysis, the patenting rate for any specific company may understate or

overstate the company’s investment in technology development.

For example, some companies may spend more on R&D while patenting less, in which case a

patent-based KPI would understate their R&D efforts. Conversely, some companies may be

prolific patent filers while spending comparatively less on R&D, in which case a patent-based

KPI would overstate R&D activities. In either case, however, the exclusionary value of patents

and the potential to monetize patent portfolios in the future will likely tend to counterbalance

both under-patenting and over-patenting in the long term. For example, a company that patents

at a higher rate than its natural R&D activities may find out in the long term that its larger

volume of patents are narrower and only incrementally more valuable than a smaller and more

targeted portfolio (e.g., statistically, they may experience ongoing complications with

enablement, double patenting disclaimers, and overlapping claims) or that the return from

patenting is lower than expected, so it may eventually decrease its patent filing rate.

Analogously, a company that patents below its natural R&D investment rate may find in the long

term that its competitors are making more inroads in its R&D space while facing fewer patent

challenges, and may eventually reexamine its patenting strategy, particularly if it becomes the

target of patent infringement litigation and finds itself with limited counterclaim options. As a

special class of patent holders, entities that look at patents as a revenue-generating mechanism

may also find themselves overinvesting in patents relative to their normal revenue-generating

business activities, and while they may be able to indeed generate revenue from patent licensing

and sustain a higher rate of patenting, the sophistication needed and peripheral costs for such

patenting and licensing programs are high. Consequently, in general, the patenting rate is an

imperfect predictor or metric for actual business activities and/or technical innovation for

individual companies at any particular point in time, and therefore patenting rates should not be

used as a stand-alone metric to compare or evaluate any entity.

2. Limitations in Data Accuracy

As another observation about the limitation of patent searches, it is interesting to note that some

entities are unexpectedly missing from these rankings or are ranking lower than expected.

Square, for example, has developed a robust patent program in the past few years and ranked

very high in a 2017 commerce patent analysis (see Fig. 1 here). In parallel, Square has been

expanding its business to cover blockchain and cryptocurrency segments, including obtaining a

virtual currency license from the New York Department of Financial Services that permits N.Y.

users of Square’s Cash app to trade Bitcoin in New York. Consequently, it is highly likely that

Square has filed a meaningful number of patent applications relating to blockchain and/or

cryptocurrencies, which were not identified though this search. This means that those

applications are likely to publish in the next few months, when they would become publicly

known for the first time. This likely also applies to other entities that are ranking lower than

expected in these charts, such as Google and Apple. Consequently, any patent search in high-

growth areas like blockchain and cryptocurrencies should be perceived as a snapshot in time

and not as a definitive ranking, and the figures and rankings presented in this study are likely to

change significantly within the next 12 months.

3. Search Details

This analysis was performed using Boolean searches across large patent databases and

techniques for automated processing of large datasets, without a review of actual claims.

Consequently, individual patents and claims were not reviewed, and therefore no knowledge of

any particular patent or application was acquired.

Note:

The opinions in this article are limited to the scope of this article and to the dataset used

for this analysis, and do not necessarily reflect the author’s opinions in general, the

Copyright © 2021 Wilson Sonsini Goodrich & Rosati. All Rights Reserved.opinions of Wilson Sonsini Goodrich & Rosati (WSGR) or of any attorneys or other

personnel affiliated with WSGR, or the opinions of any WSGR clients or partners.

If you would like to discuss any aspect of this article please do not hesitate to contact Marius

Domokos at mdomokos@wsgr.com or any attorney in WSGR’s technology transactions, patents

and innovations, or blockchain and cryptocurrency practices.

Copyright © 2021 Wilson Sonsini Goodrich & Rosati. All Rights Reserved.You can also read