NTG Morning Comments www.nesvick.com - Thursday, July 7, 2022 - Nesvick Trading Group

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Thursday, July 7, 2022

NTG Morning Comments

www.nesvick.com

Weather

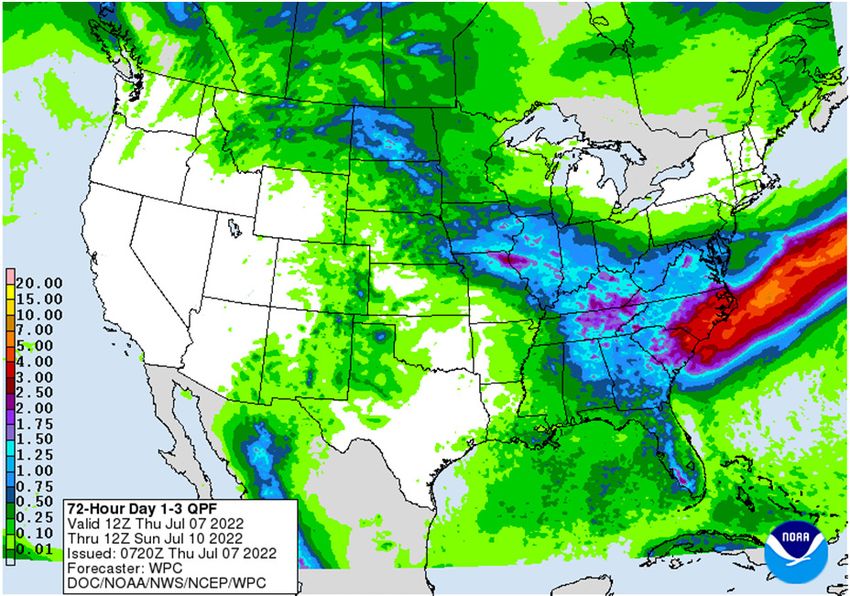

No big changes to the forecast this morning. The first

map at the right shows Days 1-3 and the bulk of the

rains in this map will fall during the next 48 hours.

This will be the best shot of rainfall for the Corn Belt

for the duration of the two week timeframe. The

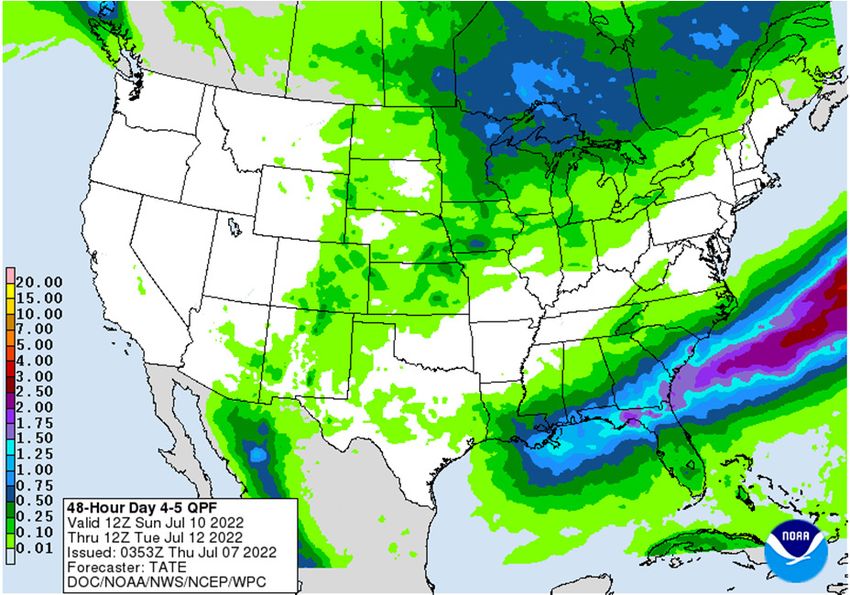

second map shows the Day 4-5 period. Some light

rains will be possible here as a cold front moves

through but probably not going to be a big rain-

maker. Beyond that, there isn’t anything in the

forecast models this morning showing another really

good shot of moisture for the 15-day period. We

should see mostly below normal precipitation for the

Corn Belt during both the 6-10 and 11-15 day periods.

Forecast models are still showing a shift where rainfall

chances favor more southern portions of the country

than the Corn Belt. That said, overnight models have

turned a little drier in even the southern portions of

the country.

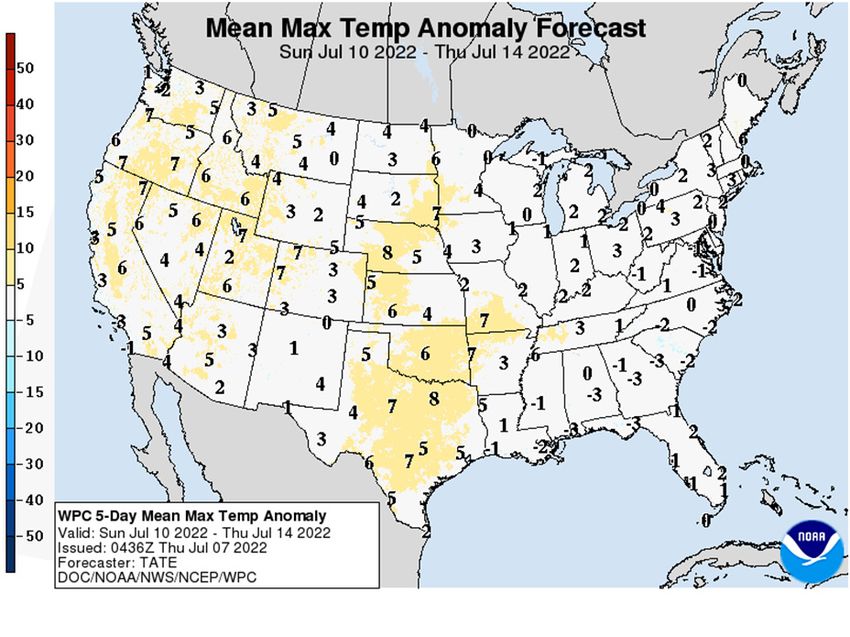

Temps will continue to be hot in the next few days.

The majority of the Corn Belt could see temps return

to near-normal levels by early next week. The Plains,

however, could continue to see above normal temps,

as shown in the map at the bottom right. Some

models are hinting at a possible return of above

normal temps in the Corn Belt by the 11-15 day

period.

Crops

Today we’ll look at wheat production guesstimates.

Let’s start by looking at winter wheat objective yield

data. The two charts below are fairly similar. These

look at July NASS reported heads/sf and the implied

head weights vs. the condition index. The highlighted

2022 figures are using numbers from the June Crop

Production report with current condition ratings. I

find it interesting that the estimate on heads/sf would seem relatively inline with what you’d expect given the

condition index. However, the implied head weight from June seems a bit optimistic relative to conditions.

Obviously smaller head counts should lead to higher average weights, but the difference this year might be a bit

stretched, no? All else equal, this would imply some potential downside to winter wheat production next week.

Admittedly, I’m not sure how much faith to put into these scatters…they’re hardly slam dunks. Informa/IHS is

actually calling for slightly higher winter wheat production.

1

Thursday, July 7, 2022

NTG Morning Comments

www.nesvick.com

July NASS Winter Wheat Objective Yield Data

Heads/SF vs. Conditions Index

75 2010 2019 2016

2012

70 2020

2017

Early July Condition Index

2008 2021

65 2015

2018

60

2011

2013

2014

2022

55

50

R² = 0.1974

45

37 39 41 43 45 47 49

Heads per Square Foot

July NASS Winter Wheat Objective Yield Data

80 Implied Head Weight vs. Condition Index

75 2016

2010 2019

2012 2020

70 2017

Early July Condition Index

2021

65 2015

2018

60

2011

2013

2014 2022

55

50

45

y = 72.876x + 17.391

R² = 0.3046

40

0.50 0.55 0.60 0.65 0.70 0.75

Implied Head Weight

What to expect for spring wheat? We don’t have much to work with at this point in time…other than condition

ratings. The chart below plots the July NASS spring wheat yield vs. the current condition index. This year’s

condition index is represented by the red line. You can see that in the past few years (last year excluded) we’ve

2

Thursday, July 7, 2022

NTG Morning Comments

www.nesvick.com

seen the July yield come in higher than the trendline on the chart would imply. I would expect something similar

to be seen this year. If we assume something around a 43.5 bpa yield on spring wheat, the June NASS harvested

area estimate would imply something around a 465-470 mil bu spring wheat crop. This is a bit smaller than

what Informa/IHS gave us yesterday.

Other Spring Wheat July Yield Forecast

vs. Condition Index

50

2018

2019

2015

2020

2016

2014

2010

45 2013 2005

2011

2017 2012

July NASS Yield

2007

40 2009

2004

2008 2003

2000 2001

35 2006

2002

2021

30

R² = 0.3249

25

45 50 55 60 65 70 75 80 85

Week #26 Condition Index

Livestock

Late yesterday afternoon I heard some talk that 151 was traded in IA to a major. Not sure of what sort of

volume we’re talking about. Would expect that NE would be somewhere close to that whenever they get

around to trading. Obviously the south is still going to be a big discount.

The weekly broiler hatchery update isn’t something I normally spend much time on, but with retail chicken

prices still very high it is something we should casually monitor in the weeks and months ahead. Charts on eggs

set and chick placements follow on the next page. We’ve seen eggs set totals score lots of new record highs this

year, but chick placements have not been able to reach record levels until just recently. This continues to speak

to the poor hatchability that seems to be a never-ending problem for the industry. You can also see we’re

nearing our seasonal downturn in both categories.

3

Thursday, July 7, 2022

NTG Morning Comments

www.nesvick.com

Broiler Eggs Set in Incubators

245,000

240,000

235,000

230,000

225,000

220,000

215,000

210,000

1-Jan 1-Feb 1-Mar 1-Apr 1-May 1-Jun 1-Jul 1-Aug 1-Sep 1-Oct 1-Nov 1-Dec

2017 2018 2019 2020 2021 2022

Chicks Placed for Meat Production

195,000

190,000

185,000

180,000

175,000

170,000

165,000

160,000

1-Jan 1-Feb 1-Mar 1-Apr 1-May 1-Jun 1-Jul 1-Aug 1-Sep 1-Oct 1-Nov 1-Dec

2017 2018 2019 2020 2021 2022

Financials

Looking at the last Dot Plot projection from the Fed is a good way of seeing how the market’s expectations have

shifted in the past few weeks. The Dot Plot isn’t even a month old, but the market’s implied rate projections

4

Thursday, July 7, 2022

NTG Morning Comments

www.nesvick.com

have posted huge shifts. The Bloomberg version of the Dot Plot is below. The yellow dots are the various FOMC

member projections and the orange line is the weighted average for each projection. The blue line shows what

the Fed Funds futures were implying as of the release of these dots (6/15). For this year, Fed Funds were

actually stronger than the average FOMC guesstimate. For 2023 and beyond, Fed Funds were not quite as

aggressive as the FOMC, but they were still close. Fast forward to yesterday (when I pulled this chart) and the

white line shows what Fed Funds are implying right now. Fed Funds are implying less hiking than the June FOMC

for this year and is now pricing in rate cuts for 2023 and beyond. What a difference just a few weeks makes.

We’ve gone from needing the Fed to hike aggressively to counter inflation to “OMG the economy is in

shambles” in record speed. I’m of the opinion we’re overshooting the slowdown (for now). Thoughts

appreciated.

The big news overnight is that China’s Ministry of Finance is apparently considering a major stimulus package.

As usual for China, the package would be aimed at infrastructure funding. It sounds like what the Chinese are

doing are pulling forward regularly-scheduled debt sales for 2023 and allowing them to take place this year. The

focus on infrastructure spending is of course mainly geared towards hitting the government’s GDP targets.

Whether or not that is truly helpful for the Chinese economy is certainly open for debate. You can see this is

having a big impact on certain commodities, such as copper and soybeans. Oil is higher, but honestly not as

much as I might have expected.

The other interesting news of the evening is that UK PM Boris Johnson has finally succumbed to pressure to

resign. The BP is trading modestly higher at the time of writing this morning, though I’m not sure the PM’s

resignation is the primary cause. Johnson apparently is hoping to remain in the spot until October while the

party elects a new leader, but it seems unlikely that is going to happen.

5

Thursday, July 7, 2022

NTG Morning Comments

www.nesvick.com

Energy

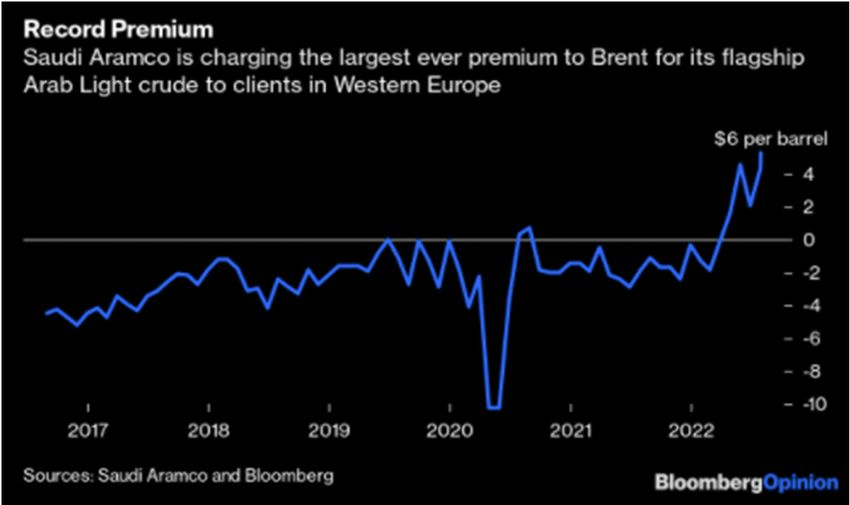

Not much new information to pass along this morning. As mentioned above, oil futures are bouncing a bit this

morning – perhaps in response to the news on Chinese stimulus. I noted yesterday that calendar spreads were

not confirming the move lower in oil, and in

yesterday’s flat price weakness we continued to

see calendar spreads trade firm. Additionally,

as the chart to the right shows, the Saudis are

charging a record large premium to their

benchmark to customers…which hardly seems

indicative of slowing demand due to poor

economic growth. I’m of the opinion the oil

selloff has been a bit overdone…though I’m

certainly willing to entertain other opinions.

Today’s Calendar (all times Central)

• Trade Balance – 7:30am

• Jobless Claims – 7:30am

• EIA Natural Gas Storage – 9:30am

• EIA Petroleum Inventories – 10:00am

• Several Fed speakers

Thanks for reading.

David Zelinski

dzelinski@nesvick.com

901-766-4684

Trillian IM: dzelinski@nesvick.com

DISCLAIMER:

This communication is a solicitation for entering into derivatives transactions. It is for clients, affiliates, and

associates of Nesvick Trading Group, LLC only. The information contained herein has been taken from trade and

statistical services and other sources we believe are reliable. Opinions expressed reflect judgments at this date

and are subject to change without notice. These materials represent the opinions and viewpoints of the

author and do not necessarily reflect the opinions or trading strategies of Nesvick Trading Group LLC and its

subsidiaries. Nesvick Trading Group, LLC does not guarantee that such information is accurate or complete and it

should not be relied upon as such.

Officers, employees, and affiliates of Nesvick Trading Group, LLC may or may not, from time to time, have long

or short positions in, and buy or sell, the securities and derivatives (for their own account or others), if any,

referred to in this commentary.

There is risk of loss in trading futures and options and it is not suitable for all investors. PAST RESULTS ARE NOT

NECESSARILY INDICATIVE OF FUTURE RETURNS. Nesvick Trading Group LLC is not responsible for any

redistribution of this material by third parties or any trading decision taken by persons not intended to view this

material.

6

Thursday, July 7, 2022

NTG Morning Comments

www.nesvick.com

7

You can also read