NORTH CAROLINA A PATHWAY TO A CLEANER ENERGY FUTURE IN - Sierra ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

A PATHWAY TO A CLEANER ENERGY FUTURE IN NORTH CAROLINA Authors: Xiaojing Sun, Ph. D, Matt Cox, Ph. D Prepared for the Sierra Club, August, 2017

TABLE OF CONTENTS

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

CHAPTER 1. North Carolina’s Electricity Future in a Business-as-Usual World. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

1.1 Historical electricity generation in North Carolina . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

1.2 Electricity generation in DEC and DEP in a Business-as-Usual future ��������������������������������������������������������7

1.2.1 Bill Impacts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

1.2.2 Emission Impacts. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

1.3 Peak demand in DEC and DEP in a Business-as-Usual future ����������������������������������������������������������������������� 9

CHAPTER 2. Designing A Cleaner Energy Future for North Carolina. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

2.1 Methodology overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

2.2 Adjusted electricity consumption and demand growth . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

2.3 An economics-driven approach to reduce reliance. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

2.4 Harnessing economically-viable clean energy. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

2.4.1 Energy efficiency programs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

2.4.2 Building codes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

2.4.3 Demand response . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

2.4.4 Enhanced renewable energy penetration. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

2.5 Building a lean, clean and reliable grid under the Cleaner Energy Plan ��������������������������������������������������� 15

2.6 ATHENIA overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

CHAPTER 3. Building A Leaner, Cleaner Electricity Grid in North Carolina. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

3.1 A new electricity production paradigm in North Carolina. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

3.1.1 A grid without coal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

3.1.2 Generation shifts between gas technologies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

3.1.3 The rising relative importance of nuclear power . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

3.1.4 Tripling the clean energy contribution in a decade. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

3.2 Peak Demand in North Carolina . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

A Pathway to a Cleaner Energy Future in North Carolina 1

CHAPTER 4: Economic Benefits to North Carolina Ratepayers and the State Economy ���������������������������������������������������� 20

4.1 Electricity bill savings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

4.2 Economic growth and job creation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

4.2.1 Employment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

4.2.2 Income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

4.2.3 GDP. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

CHAPTER 5: Environmental, Social, and Economic Benefits of North Carolina’s Cleaner Electricity Future ���������������������������������� 22

5.1 Emissions reductions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

5.2 Avoided social and economic damages . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

5.3 Reduction in CO2 emissions and the associated social and economic benefits ����������������������������������� 25

5.4 Savings in water consumption and withdrawals. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

CHAPTER 6. Overall Benefit-cost Analysis. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

6.1 Benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

6.2 Costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

CHAPTER 7. Moving Towards A Clean Energy Future. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

7.1 A lean, clean, and reliable electric grid is within reach in North Carolina ����������������������������������������������� 29

7.2 Harnessing the energy, environmental, and social benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Appendix A. Description of ATHENIA Modules . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Appendix B. Costs Included in the Economic Analysis of Costs to Operate Power Plants ������������������������������������������������������� 34

Appendix C. Expanded Energy Efficiency and Conservation Modeling Details . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

Appendix D. Methodology for Determining Social Damages Associated with Emissions ������������������������������������������������������� 36

A Pathway to a Cleaner Energy Future in North Carolina 2

EXECUTIVE SUMMARY

The state of North Carolina is at a crossroads regarding demand. The results of this study suggest that the

its energy future, facing two dramatically different Cleaner Energy Plan will not only maintain the reliability

paths. Duke Energy, the main electricity provider in of the grid and make electricity service more affordable

the state, calls for 5,617 MW of new fossil and nuclear for North Carolinians, it will reduce the environmental

demand levels diminish the argument

capacity between 2018 and 2028 in its preferred for new fossil andassociated

impact nuclear capacity. Additionally,

with electricity production. all

existingplans.

resource coal-fired generating

Under this capacity can

“Business-As-Usual” be retired in a 10-year period, reducing system costs

(BAU)

D E S I G N I N G A C L E A N E N E R GY F U T U R E

without jeopardizing grid reliability. Finally, the machine

vision, fossil fuel and nuclear generation are front

The Cleaner learning-powered

Energy Plan evaluated simulation results

in this study begins

and center in meeting electricity demand. Although

show that clean energy plays an important

renewable energy and energy efficiency are required to

role in meeting

with realisticdemand and

electricity keep the

consumption grid

and reliable.

peak demand

supply 12.5% of the utility’s sales by 2021, Duke Energy forecasts that align with those of other energy system

does not plan to add any utility-owned solar or wind modeling experts and recent North Carolina history.

The Clean Energy Future Is Economically

capacity to the grid; does not plan to meaningfully

Wiser

The results demonstrate that Duke Energy severely

increase energy efficiency levels (which under Duke’s overestimated both consumption and demand growth.

plans will meet, at most, 0.5% of electricity demand); The realistic growth rates of the Cleaner Energy Plan

Theplans

and Cleaner Energy

to utilize only aPlan

very will

small deliver tangible

amount of demandfinancial benefits to North Carolina electricity

eliminate some of the utilities’ justification for the

ratepayers.

response The reduction in customer electricity demand

programs. constructiondueofto energy

new efficiency,

generating demand

assets. Furthermore,

response, and distributed renewable sources translates

In dramatic contrast to Duke Energy’s fossil fuel-reliant

to lower

the Cleaner overall

Energy consumption

Plan introduces and lower

cost-effective

electricity

vision, bills. Despite

The Greenlink Group (an modest

energybeginnings,

research firm)the savings

automated ramp up quickly

demand responseand eventually

programs reach a

and energy

cumulative

has evaluated savings

a cleaner of $5.4pathway,

energy billion whereby

for Duke Energy customers. Relative to the BAU, residential

efficiency programs, further deepening the reductions

in electricity consumption and peak demand. In

customers

23% will demand

of electricity see an average

is met by $101

resourcesreduction

such in their annual electricity bills; non-residential

addition, the Cleaner Energy Plan would also take

customers will experience a $611 annual electricity

as energy efficiency, distributed and utility-scale solar, bill saving.

full advantage of economical renewable and energy

wind, hydroelectric power, demand response, and

energy storage technologies. In this Cleaner Energy storage technologies, lowering the emissions intensity

of the electricity supply.

Jobs, incomes, and GDP are all higher in the Cleaner Energy Plan than in the BAU. Under the

Plan, none of the new fossil and nuclear capacity that

Duke Energy has proposed to construct over the next

Cleaner Energy Plan, employment would increase,

ten years will be needed, and the seven coal plants

ranging from 109,000 to 157,000 job-years

The proposed clean energy measures would

fundamentally alter the dynamics of electricity demand

betweenon2018

currently Duke’sand 2028.

system willIncomes

be retiredwould

between experience

2018 and asupplynet increase of $4.8 billion to $7.7 billion,

in North Carolina. Their substantial impact

while

and 2027North Carolina’s

because GDP increases

they are unnecessary bysystem

to meet $3.7 billion

on Duke to Energy’s

$8.2 billion (Figure

resource ES-1). Overall,

mix manifests in three

economic development is accelerated dramatically under the Cleaner Energy Plan.

$1,200 20,000

18,000

$1,000

16,000

14,000

$800

Job-Years

Millions $

12,000

$600 10,000

8,000

$400

6,000

4,000

$200

2,000

$0 0

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

Net Job-Years (H) Net Job-Years (L) Net Income (H)

Net GDP (H) Net Income (L) Net GDP (L)

Figure ES-1 Net EconomicFigure ES-1 Net Economic Development Impacts of the Cleaner Energy Plan for North Carolina (2015-$) (H: High, L: Low)

Development Impacts of the Cleaner Energy Plan for North Carolina

(2015-$) (H: High, L: Low)

A Pathway to a Cleaner Energy Future in North Carolina 3

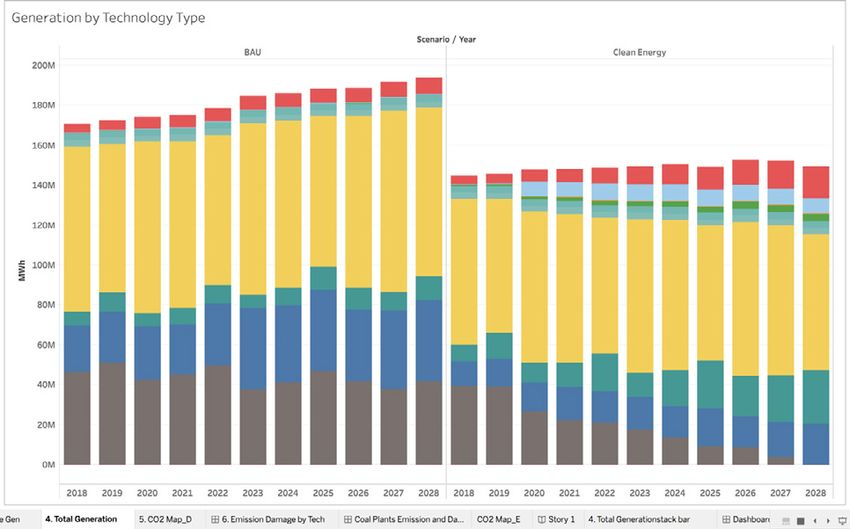

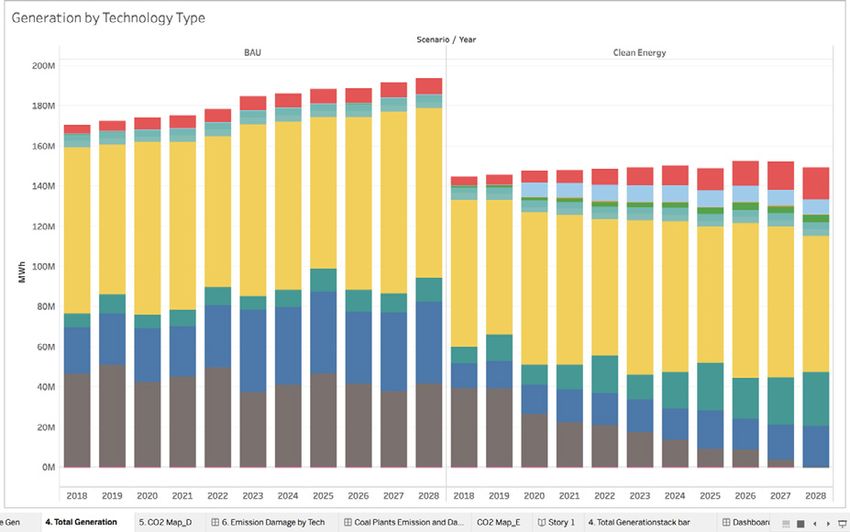

scenario than under the BAU. Overall gas use, however, is lower under the Cleaner Energy Plan

than under the BAU.

16% 17% 22% 22% 25% 28% 29% 31% 30% 32% 35%

Figure ES-2 Electricity Generation in Duke Energy

Figure ES-2 System, BAU invs.

Electricity Generation Cleaner

Duke Energy

Energy System, BAU vs.Plan

Cleaner Energy Plan

(Percentage

(Percentage numbers indicate decrease numbers

in total indicatebased

fossil-fuel decrease in total fossil-fuel

generation in thebased generation

Cleaner in thePlan

Energy Cleaner Energy

over BAU)Plan over BAU)

In contrast

ways. to the

First, under the diminishing

Cleaner Energy role of fossil

Plan, more- generation, cleanwould

Incomes energy resourcesa net

experience experience

increase of $4.8 billion

likely consumption and peak demand levels diminish to $7.7 billion, while North Carolina’s GDP increases

tremendous growth under the Cleaner Energy Plan, meeting 23% of the total Duke Energy

the argument for new fossil and nuclear capacity. by $3.7 billion to $8.2 billion (Figure ES-1). Overall,

system load in 2028. Solar becomes the largest

Additionally, all existing coal-fired generating capacity clean energy source

economic in the isCleaner

development Energy

accelerated Plan,

dramatically

canproducing

be retired nearly 16 million

in a 10-year period, MWh of system

reducing electricity in 2028,

under more than twice

the Cleaner EnergyasPlan.

much as its 2028

contribution in the BAU scenario. New wind capacity in northeastern North Carolina and wind

costs without jeopardizing grid reliability. Finally, the

machine learning-powered simulation results show T H E C L E A N E R E N E R GY P L A N

energy purchases from transmission projects make wind TRAN the

S Fsecond

O R M Slargest

T H E Gclean

R I D energy

that clean energy plays an important role in meeting

resource

demand andinkeepthethe

State (Figure

grid reliable.ES-3). Energy efficiency’s contribution to reducing electricity

A significant fuel mix change will occur for Duke

demand will ramp up from its current level of 0.4% Energy’s to 4% bycentralized-generating system over the course

2028, a ten-fold growth. Albeit

T H E C L E A N E N E R GY F U T U R E I S of the next decade. Compared to the BAU scenario,

E Csmall

O N OinM Ienergy

C A L LYterms,

WISE demand

R response programs come at a critical time when power

the Cleaner Energy Plan creates a significant shift away

Thereductions help to

Cleaner Energy maintain

Plan operational

will deliver reliability and

tangible financial fromcost-effectiveness. The aggressive

coal, nuclear, and combined pursuit

cycle gas generation

benefits to North Carolina electricity ratepayers. The towards clean energy resources such as solar, wind, and

reduction in customer electricity demand due to battery storage (Figure ES-2). Coal-fired power plants

7

energy efficiency, demand response, and distributed are phased out entirely by 2027. While combined cycle

renewable sources translates to lower overall gas plants play a smaller role under the Cleaner Energy

consumption and lower electricity bills. Despite modest Plan, combustion turbine gas units will generate more

beginnings, the savings ramp up quickly and eventually electricity under this scenario than under the BAU.

reach a cumulative savings of $5.4 billion for Duke Overall gas use, however, is lower under the Cleaner

Energy customers. Relative to the BAU, residential Energy Plan than under the BAU.

customers will see an average $101 reduction in their

In contrast to the diminishing role of fossil generation,

annual electricity bills; non-residential customers will

clean energy resources experience tremendous growth

experience a $611 annual electricity bill saving.

under the Cleaner Energy Plan, meeting 23% of the

Jobs, incomes, and GDP are all higher in the Cleaner total Duke Energy system load in 2028. Solar becomes

Energy Plan than in the BAU. Under the Cleaner the largest clean energy source in the Cleaner Energy

Energy Plan, employment would increase, ranging from Plan, producing nearly 16 million MWh of electricity in

109,000 to 157,000 job-years between 2018 and 2028. 2028, more than twice as much as its 2028 contribution

A Pathway to a Cleaner Energy Future in North Carolina 4

North Carolina’s energy mix, as shown in Figure ES-4.

40 153%

139%

35

40 116% 153%

101% 139%

30

35 92% 99% 116%

85% 101%

25

30 71% 85%

92% 99%

72%

20

25 71%

72%

MWhMWh

15

20 7%

5%

10

15 7%

Million

5%

5

10

Million

05

20182018

20192019

20202020

20212021

20222022

20232023

20242024

20252025

20262026

20272027

20282028

20182018

20192019

20202020

20212021

20222022

20232023

20242024

20252025

20262026

20272027

20282028

0

BAU Scenario Clean Energy Scenario

Hydro Solar Pumped

BAUStorage

Scenario Wind Battery Storage Clean

Efficiency Demand Response

Energy Scenario

Hydro

Figure ES-3 Solar Pumped

Electricity Storage

Generation fromWind Battery Storage

Clean Energy Resources, Efficiency

BAU vs. CleanerDemand Energy Response Plan

Figure ES-3numbers

(Percentage Electricity Generation

indicate increase in from Clean

total clean Energy

electricity

Figure ES-3 Resources,

generation

Electricity BAU

in the

Generation from Clean Energyvs.

Cleaner Cleaner

Energy

Resources, vs.Energy

BAUPlan Plan

overEnergy

Cleaner BAU) Plan

(Percentage numbers indicate increase in total clean electricity generation in the Cleaner Energy Plan over BAU)

(Percentage numbers indicate increase in total clean electricity generation in the Cleaner Energy Plan over BAU)

Pumped Battery

Storage Efficiency NGCT Pumped Storage Demand

Pumped

1.8% Battery

0.1% Efficiency Response

0.2% 6.1% Storage

Storage Efficiency NGCT Pumped Storage

Wind Demand

0.1%

Solar 2.3% 2.4%

1.8% 0.2% 6.1% Storage 0.1% Efficiency

5.2% Response

Hydro 4.0% Wind 0.1%NGCT

Solar 2.3% 2.4%

1.6% 5.2% 17.8%

Hydro 4.0% Solar NGCT

1.6% NGCC

10.6% 17.8%

21.1% Solar

NGCC

Hydro10.6%

21.1%

2.0%

Hydro NGCC

2.0% 13.8%

NGCC

Nuclear 13.8%

43.6%

Nuclear

43.6%

Steam Nuclear

Coal 45.5%

Nuclear

Steam

21.6% 45.5%

BAU Coal Clean Energy Scenario

21.6%

BAU Clean

Figure ES-4 Energy

Resource Scenario

Mix in 2028, BAU vs. Clean Energy Scenario

Figure ES-4 Resource Mix in 2028, BAU vs. Clean Energy Scenario

Figure ES-4 Resource Mix in 2028, BAU vs. Clean Energy Scenario

in the BAU scenario. New wind capacity in northeastern critical time when power reductions help to maintain

North Carolina and wind energy purchases from operational reliability and cost-effectiveness. The

transmission projects make wind the second largest aggressive pursuit of energy efficiency and demand 8

clean energy resource in the State (Figure ES-3). response will also reduce peak load on the Duke 8

Energy efficiency’s contribution to reducing electricity Energy system by 18% in 2028. Altogether, clean energy

demand will ramp up from its current level of 0.4% resources become a substantial component of North

to 4% by 2028, a ten-fold growth. Albeit small in Carolina’s energy mix, as shown in Figure ES-4.

energy terms, demand response programs come at a

A Pathway to a Cleaner Energy Future in North Carolina 5

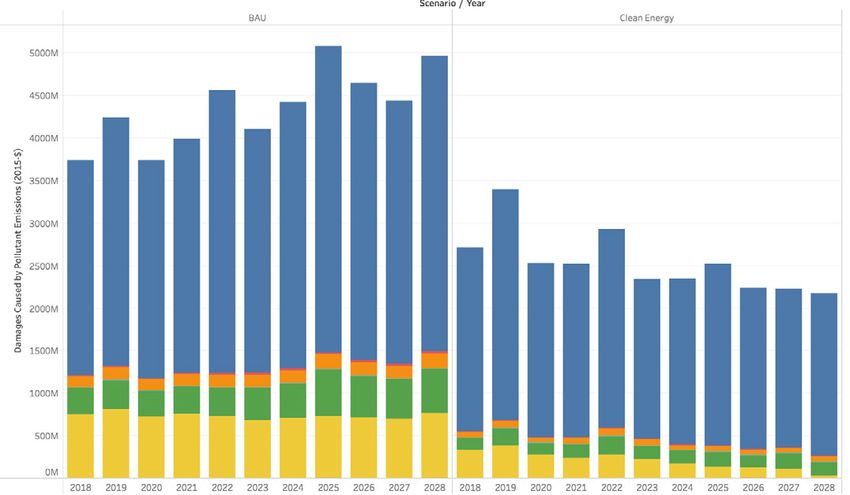

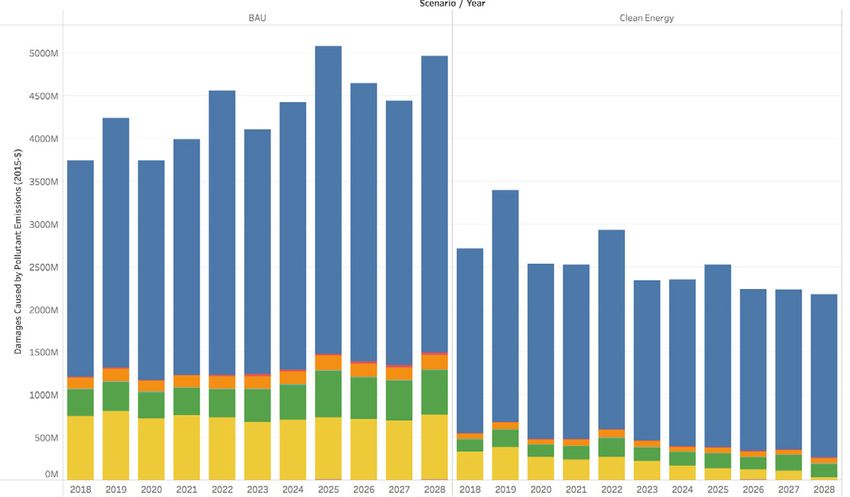

of Carbon). Overall, the Cleaner Energy Plan reduces total damages from electricity generation

by $21 billion between 2018 and 2028, a 45% decline from the BAU scenario (Figure ES-5).

Figure ES-5. Damages from All Pollutant Emissions, BAU vs. Cleaner Energy Plan

Figure ES-5. Damages from All Pollutant Emissions, BAU vs. Cleaner Energy Plan

9

T H E C L E A N E R E N E R GY P L A N B E N E F I T S total damages from electricity generation by $21 billion

THE PUBLIC AND THE ENVIRONMENT between 2018 and 2028, a 45% decline from the BAU

In addition to electricity bill savings, job creation, and scenario (Figure ES-5).

GDP growth, the Cleaner Energy Plan also achieves a

suite of social and environmental benefits. Emissions Because many pollutants travel across state and

of carbon dioxide (CO2), sulfur dioxide (SO2), nitrogen national borders, the public health benefits due to a

oxides (NOx), particulate matter, ammonia, and volatile cleaner grid in North Carolina can be enjoyed in and

organic compounds (VOCs) are lower in the Cleaner beyond the state. Adult mortality declines by 1,200,

Energy Plan than the BAU scenario. Cumulatively, nearly 900 hospital visits for issues like asthma and

over 160 million metric tons of CO2 emissions will be cardiovascular disease are avoided, and society benefits

avoided between 2018 and 2028, equivalent to the from the added productivity of 93,000 missed work

expected emissions of 3.4 million cars over the same days being added back to the economy.

period. Similarly, across the other six pollutants, nearly A C L E A N E N E R GY F U T U R E , A B E T T E R

47% of the emissions will be avoided. FUTURE

The Cleaner Energy Plan designed in this study is a

In addition to better air quality, 53 billion gallons of

much more attractive development pathway for North

water consumption is avoided due to the retirement of

Carolina. Economic opportunities are greatly expanded,

water-intensive coal-plants and the avoided operations

environmental damage is much reduced, and social

of a new nuclear unit.

outcomes are significantly better than under the BAU

A cleaner electricity supply leads to a suite of social, trajectory. It is also significantly more cost-effective

environmental, and economic benefits such as better than the BAU case. The cumulative net monetary

public health, fewer crop failures, and lower extreme- benefits achieved in the Cleaner Energy Plan associated

weather-related risks to the economy. The avoided with the full complement of costs and benefits totals at

CO2 emissions alone produce about $3.6 billion social, $59 billion to $100 billion dollars. Overall, these results

environmental, and economic benefits globally (valued suggest the Cleaner Energy Plan represents a more

using the U.S. Interagency Working Group Social Cost desirable and sustainable future for North Carolina, its

of Carbon). Overall, the Cleaner Energy Plan reduces businesses, and its residents.

A Pathway to a Cleaner Energy Future in North Carolina 6

CHAPTER 1. NORTH CAROLINA’S ELECTRICITY FUTURE IN A BUSINESS-AS-USUAL

WORLD

1 .1 H I S TO R I C A L E L E C T R I C I T Y has been hampered by an unfavorable regulatory

G E N E R AT I O N I N N O R T H C A R O L I N A

environment. Although the state has a strong wind

The primary electric service provider in North Carolina

potential in the Appalachian mountain region as well

is Duke Energy, servicing over 70% of North Carolina’s

as the coastal region, the Mountain Ridge Protection

electricity demand. Duke Energy oversees two utility

Act, commonly called the “Ridge Law,” has restricted

companies in North Carolina: Duke Energy Progress

development of wind turbines on mountain ridges. The

(DEP) and Duke Energy Carolinas (DEC). DEC is the

consequence of the Ridge Law is that it has effectively

larger of the two companies, with 2.5 million residential,

banned 75% of the state’s on-shore wind potential from

commercial, and industrial customers, while DEP

being developed. The only wind farm that currently

services approximately 1.5 million customers.

exists in the state is a 200 MW project in Dominion’s

Historically, North Carolina has relied on fossil-based territory along the coast in the northeast corner of the

and nuclear energy as the primary resources for state.

electricity generation. Coal-fired generation was the

Although energy efficiency is a qualifying resource

single largest generation source in the 1990s, being

under the REPS, it has not grown in the resource mix

used to produce 61% of electricity in-state over the

over the past four years relative to demand growth.

decade.1 However, with the economics of natural gas

In 2016, energy efficiency offset 0.5% and 0.4% of the

improving over the past decade, the prominence of coal

generation in DEC and DEP, respectively. The American

decreased. In 2015, coal was the second largest source

Council on an Energy-Efficient Economy (ACEEE) ranks

of generation, after nuclear power and just ahead of

North Carolina 30th in the nation in terms of total-

natural gas by 3%, as shown in Figure 1-1.

percentage-savings from energy efficiency.3 In addition,

Renewable energy has seen significant growth in both utilities place in the bottom quartile in savings

North Carolina since the mid-2000s, due to regulatory achieved from efficiency and rank 31st and 35th out of

dynamics and rapid price reductions. A significant 51 in the ACEEE utility efficiency scorecard.4

CHAPTER

player1.inNORTH bothCAROLINA

aspects ’S Efor the North

LECTRICITY FUTURECarolina

IN A BUSINESS -AS-USUAL WORLD

market

1 . 2 E L E C T R I C I T Y G E N E R AT I O N I N D E C

was the establishment of the Renewable Energy and A N D D E P I N A B U S I N E S S -A S - U S UA L

Energy Efficiency Portfolio Standard (REPS) in 2007, FUTURE

1.1 HISTORICAL ELECTRICITY GENERATION IN NORTH CAROLINA

which requires that by 2021, 12.5% of the prior year’s Phase I of this study conducted a modeling exercise

Theretail

primaryelectricity

electric servicesales

providerfrom investor-owned

in North Carolina is Duke Energy, electric

servicing over 70% of

to understand the electricity landscape in the State of

North Carolina’s

utilities inelectricity

the state demand.

mustDukebeEnergy oversees two

supplied byutility companies in North

eligible

Carolina: Duke Energy Progress (DEP) and Duke Energy Carolinas (DEC). DEC is the larger of

North Carolina. Using the ATHENIA model, the study

the renewable

two companies, withand2.5energy efficiency

million residential, sources.

commercial, Utility-

and industrial customers, while developed a forecast of electricity demand and supply

DEP scale solar

services has led

approximately 1.5the charge

million customers.of renewable energy in Duke Energy Carolinas and Duke Energy Progress

deployment in North Carolina, most of which has been territory between 2017 and 2030 based on both

Historically, North Carolina has relied on fossil-based and nuclear energy as the primary

brought

resources onto generation.

for electricity the gridCoal-fired

as qualified

generationfacilities (QFs),

was the single largest generation utilities’ 2016 Integrated Resource Plans (IRP), referred

making

source thebeing

in the 1990s, stateusedfirst in the

to produce 61% nation for in-state

of electricity over the decade.1

PURPA-enabled to as the business-as-usual (BAU) scenario.

However, with the economics of natural gas improving

solar capacity, both in percentage and actual megawatt over the past decade, the prominence of

coal decreased. In 2015, coal was the second largest source of generation, after nuclear powerUnder the BAU scenario, demand for electricity in North

andterms.

just ahead In contrast, wind capacity

in Figuredevelopment

2

of natural gas by 3%, as shown 1-1.

Carolina will experience modest to strong growth in

Other

the next 15 years, following DEC and DEP’s Integrated

Resource Plans. After considering utility sponsored

Renewables

energy efficiency programs, DEC and DEP anticipate

Nuclear that demand from their customers will grow at 1% and

0.9% annually, respectively. The commercial sector will

Natural Gas

experience the strongest annual demand growth at

Coal 1.3%, followed by the residential sector and industrial

0 10 20 30 40 50 sectors.

Million MWh To meet this demand growth, the Duke utilities call

Figure 1-1 Electricity Generation by Fuel Type in North Carolina, 2015 for an expansion in electricity generating capacity to

Figure 1-1 ElectricitySource:

Generation by Fuel

EIA Form 923Type in North Carolina, 2015

Source: EIA Form 923 maintain demand-supply balance. As of 2016, 57% of

A Pathway to a Cleaner Energy Future in North Carolina 7

1

US Energy Information Administration. 2017. “State Electricity Data System.”

11

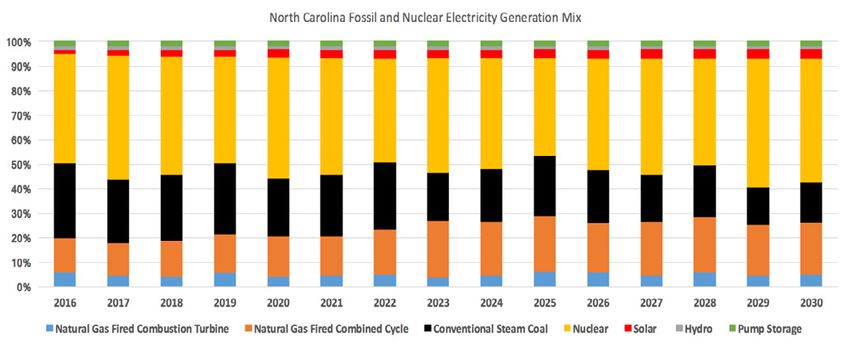

Figure 1-2 Duke Energy

Figure System-wide

1-2 Duke Energy System-wide Electricity Generation

Electricity Generation Mix for FossilMix for Fossil

and Nuclear and

Resources Nuclear

under the Business-as-Usual Scenario

Resources under the Business-as-Usual Scenario

the electricity generation in DEC came from nuclear 1 . 2 .1 B I L L I M PAC T S

1.2.1 BILL IMPACTS

power plants, followed by 25% from coal-fired power Consumers from all sectors in DEC and DEP are

plants; gas accounted for just over 10% of electricity expected to experience increases in their electricity

Consumers from all sectors in DEC and

generation. Although still the largest generation source, DEP are expected to experience

bills, due to upward increases

pressure on in electricity

their rates from

electricity

nuclear bills,fordue

accounts onlyto 39%

upward pressure

of DEP on electricity

generation; gas- rates from the

the planned planned

capacity capacity

and and grid as well as

grid expenditures,

expenditures,

fueled plants edge asout

wellcoal-fired

as growing powerconsumption

plants by 2levels. growing consumption levels.

percentage points to be the second largest electricity

Forecasts conducted in the first phase of this study

generation source in DEP, meeting 28% of demand.

Forecasts conducted in the first phase

Renewable energy accounts for less than 7% for both

of this study find

findthat onon

that average, residential

average, residentialcustomers

customersinin DEC will

DEC will

utilities. Morepay $119 pergenerating

fossil-based month for capacity

their electricity

will be use in 2017, but that will increase by 62% to

pay $119 per month for their electricity use in 2017, but

reachto$194

added in 2030

the DEC (bothsystems,

and DEP in nominal dollars).

according The bill that

to the

will increase by 62% to reach $194 in 2030 (both in

increase is more pronounced in DEP, as

nominal dollars). The bill increase is more pronounced

theBetween

IRPs. average 2017

residential

and 2030,customer is projected

DEC plans to add oneto see their monthly bills go up by 85% between

in DEP, as the average residential customer is projected

new gas combustion turbine (NGCT) plant rated at 468

2017 and 2030. Non-residential customers will also see toasee sizable

their increase in their

monthly bills electricity

go up by 85% between 2017

MW, one new gas combined cycle (NGCC) plant rated

bills. In both DEC and DEP, industrial

at 1221 MW, and two 1117 MW-rated nuclear units. Over

and commercial and customers will pay

2030. Non-residential 55% more

customersevery

will also see a

themonth

same for electricity in 2030 compared to 2017. Although non-residential customers inbills.

DECIn both DEC and

sizable increase in their electricity

period, DEP plans to add six new NGCT plants

DEP, industrial and commercial customers will pay 55%

payatless

rated perMW

2,158 kWh, their average

capacity, along withelectricity

two newconsumption

NGCC is 68% higher than their DEP

more every month for electricity in 2030 compared to

counterparts.

plants that have Consequently,

a combined rated thecapacity

electricity bill for

of 1,781 MW.an average non-residential customer in DEC

2017. Although non-residential customers in DEC pay

Asisa estimated

result of the to capacity

reach $1,471 per month

expansion, in 2030.

the utilities planAverage

lessnon-residential electricity

per kWh, their average bills in consumption

electricity DEP is

onaregasapproximately

to play a more 22% lower than in DEC, reaching $1,148

important role in meeting Duke’s 68% higher by 2030.

than their DEP counterparts. Consequently,

future electricity demand. The combined generation the electricity bill for an average non-residential

from NGCT and NGCC plants in 2030 will account for customer in DEC is estimated to reach $1,471 per month

1.2.2 E MISSION IMPACTS

over 27% of system-wide generation, seven percentage in 2030. Average non-residential electricity bills in DEP

points higher than the 2016 contribution. In the are approximately 22% lower than in DEC, reaching

ATHENIA

meantime, the tracks the byproducts

prominence of coal-firedof power

fossil-based

plants electricity

$1,148 generation,

by 2030. including six localized

willpollutants – SO2, NOx,

decline significantly PMnext

in the 2.5, PM 10, VOCs,

13 years; only and

14% NH

of 3 – as well as greenhouse gas emissions of

theCO 1 . 2 . 2 E M I S S I O N I M PAC T S

2. Previous analysis found that SO2, NOx, PM2.5, and CO2 are the four major air pollutants

electricity demand in 2030 will be met by coal-fired

power plants, down 26 percentage points from 2016 ATHENIA tracks the byproducts of fossil-based

levels. The majority of the fuel switch between coal electricity generation, including six localized 14pollutants

and gas happens between NGCC and coal-fired plants – SO2, NOx, PM2.5, PM10, VOCs, and NH3 – as well as

because they have similar generating profiles. greenhouse gas emissions of CO2. Previous analysis

found that SO2, NOx, PM2.5, and CO2 are the four

A Pathway to a Cleaner Energy Future in North Carolina 8coal plants such as Roxboro, Belews Creek, and Marshall have the largest damages associated

with their operations (Figure 1-3).

Dan River

Mayo

Marshall

Ashville CC

Cliffside

Figure 1-3 Cumulative Damages Caused by Criteria

Figure Pollutants

1-3 Cumulative Between

Damages Caused by Criteria 2017

Pollutantsand 2030

Between 2017 and 2030

Accounting for the full, global scope of pollutant impacts, the single largest source of social and

economic

major damage

air pollutants thatfrom thefor

account Duke

98% fleet

of theis CO2. Again, coal-fired

Cumulative power

emissions plants

across DECare theDEP

and largest

between

total damages associated with electricity generation 2017 and 2030 are slightly above 820 million metric

emitters of CO2 and are therefore responsible for the largest damages. Cumulative emissions

emissions in North Carolina. Within the localized tons, causing a cumulative damage of over $3 trillion

acrossfamily,

pollutant DEC NOx

and isDEP between

the single 2017

largest and of

source 2030 are(undiscounted)

slightly aboveover 820the million

next 14metric

years. tons,

causinginaterms

emissions cumulative damage

of tonnage. of over

However, $3 trillion (undiscounted) over the next 14 years.

the public

health and the environmental damage caused by 1.3 PEAK DEMAND IN DEC AND DEP IN A

B U S I N E S S -A S - U S UA L F U T U R E

a ton of NOx is significantly less than that caused

One key indicator that Duke Energy uses in their

by SO2 and PM2.5, due to the more severe public

resource planning is forecasted system peak demand

health consequences related to the latter two. In the

because they are obligated to build enough resources

projection, SO2 is initially the worst offender, causing

to reliably meet system demand. According to the

more than $470 million in damage in 2016. Coal- 15

BAU forecast conducted in the first phase of this study

fired power plants are the largest emitters of SO2.

using Greenlink’s proprietary model, both DEC and

Fortunately, as the share of electricity generated from

DEP’s peak demand will occur in winter time by 2028.

coal declines over time, the amount of SO2 and its

The highest electricity demand on the Duke system

associated damages also shrinks between 2016 and

(DEC and DEP combined) occurs at 8am on a January

2030. However, PM2.5, an air pollutant associated with

morning. Close to 34,000 MW of electric power needs

the combustion of both coal and natural gas, sees a

to be produced and delivered to the customers at

sharp increase between 2022 and 2028, due to the

that hour, a value approximately 7% higher than the

added NGCC and NGCT capacity in both DEC and DEP.

summer peak demand, which occurs around 5pm in

The projection finds that it will overtake SO2 in 2023

July. Although DEC and DEP experience their system

to be the most damaging air pollutant. In 2028, PM2.5

peaks on different days, because DEC’s system load

will cause more than $440 million in public health and

is 40% higher than that of DEP, the total Duke system

environmental damage; the damage value will decline

peak corresponds with DEC’s peak day. The predicted

slightly to $360 million by 2030. Large coal plants such

system-wide summer peak hour is around 5pm, which is

as Roxboro, Belews Creek, and Marshall have the largest

different from both utilities’ individual peak hours.

damages associated with their operations (Figure 1-3).

In summary, under the business-as-usual scenario,

Accounting for the full, global scope of pollutant

electricity demand in North Carolina will continue to

impacts, the single largest source of social and

grow between now and 2030; Duke Energy intends to

economic damage from the Duke fleet is CO2. Again,

respond to this by adding more electricity generating

coal-fired power plants are the largest emitters of CO2

capacity – the overwhelming majority of which will be

and are therefore responsible for the largest damages.

A Pathway to a Cleaner Energy Future in North Carolina 9gas. The results of this trajectory are higher system significant clean energy resources that can supplement

expenditures, higher electricity bills for customers, or even displace its current fossil- and nuclear-driven

worse air quality, growing CO2 emissions, and greater centralized electricity generation model. The remaining

stress on water resources, none of which are desirable sections of this report articulate a cleaner energy vision

outcomes for the public. that ensures the reliability of the grid and reduces

environmental externalities, while simultaneously saving

Fortunately, the business-as-usual scenario is not the

North Carolina ratepayers money.

only pathway available to North Carolina. The state has

CHAPTER 2. DESIGNING A CLEANER ENERGY FUTURE FOR NORTH CAROLINA

Using the BAU scenario as a baseline, Greenlink the pressure on utilities to finance and build many new

evaluated the possibility of a cleaner energy future for generating assets to meet demand and meet reliability

the state that does not involve significant spending on requirements.

building or maintaining fossil-based generating plants.

The rest of this chapter and its associated appendices

In this Cleaner Energy Plan, a significant portion of

explain the process of avoiding capacity expansions,

the future electricity demand will be met by a diverse

retiring existing centralized generation, and the

set of clean energy resources, including customer-

approach for adding new clean energy resources.

side solutions such as energy efficiency, demand

Core to this approach is the retirement of expensive

response, and distributed solar, as well as utility-scale

generation as made feasible through other efforts

technologies such as utility-scale solar, onshore wind,

evaluated in the study. Expensive generation is

grid-facing energy storage, and more. A more realistic

identified as incurring plant-level total operating

demand growth forecast is also envisioned, derived

expenses greater than $20 million in any given year

from the Energy Information Administration (EIA)’s

between 2018 and 2028 and costing over $10,000

2017 Annual Energy Outlook.5 In combination, these

per MW of capacity annually to maintain. Generation

resources can be utilized to offset the need for new

satisfying these criteria are retired, starting with the

fossil plants and the continued operation of costly

most-costly, as the reserve margin and loss-of-load-

existing fossil plants while still meeting state-wide

hour analysis permits, to ensure reliability. Overall, this

electricity demand over the next 10 years, i.e. between

allows for a lower-cost system to come into being in

2018 and 2028.

North Carolina.

2 .1 M E T H O D O LO GY OV E R V I E W Lastly, economically feasible energy efficiency and

The Cleaner Energy Plan in this study brings a

renewable energy resources will be deployed at scale

new approach to electricity supply and demand in

to cost-effectively meet demand as well as to displace

North Carolina. It begins with rethinking electricity

marginally more-expensive electricity production

consumption and peak demand forecasts and asks

coming from the remaining fossil and nuclear fleet

whether the growth trajectories proposed by the

in DEC and DEP territory. The overarching goal of

utilities are appropriate. After comparing the utilities’

this approach is to use economically-viable clean

reported growth rates with historical data and

energy resources to replace costly fossil plants while

predictions from other reputable sources, it is apparent

maintaining grid reliability.

that the growth rates in the two utilities’ IRP filings are

the most optimistic among all reviewed sources. If a 2 . 2 A DJ U S T E D E L E C T R I C I T Y

more likely growth forecast is adopted, the demand C O N S U M P T I O N A N D D E M A N D G R OW T H

for new generating assets is significantly less than in A N D T H E I R I M PAC T O N C E N T R A L I Z E D

G E N E R AT I N G C A PAC I T Y A D D I T I O N S

the BAU scenario. For the purpose of modeling the

Over the past four years, DEC’s electricity consumption

Cleaner Energy Plan, this study chooses to ground

growth has been relatively flat. However, the Company

the assumptions about the growth rates on historical

projects annual consumption growth of 1.1% per year

data using EIA Form 861 (formerly Form 826) and the

(1.0% after accounting for utility energy efficiency

assumptions used in Annual Energy Outlook 2017. As

programs), with the greatest growth coming from

a result, electricity consumption and peak demand

the commercial sector. Like DEC, DEP’s electricity

growth rates are reduced by more than 50% from DEC

consumption growth has been relatively flat, while the

and DEP forecasts. Lower growth rates relieve some of

A Pathway to a Cleaner Energy Future in North Carolina 10Table 2-1 Unnecessary Fossil-based and Nuclear Generating Capacity after Adjusting Demand

Growth and Accounting for Clean Energy

Utility Plant Type Capacity Proposed Online

(MW) Year

DEC Natural Gas Combined Cycle (NGCC) 1221 2023

DEC Natural Gas Combustion Turbine (NGCT) 468 2025

DEC Nuclear 1117 2027

DEP Natural Gas Combined Cycle (NGCC) 1221 2022

DEP Natural Gas Combustion Turbine (NGCT) 468 2023

DEP Natural Gas Combustion Turbine (NGCT) 186 2024

DEP Natural Gas Combustion Turbine (NGCT) 468 2026

DEP Natural Gas Combustion Turbine (NGCT) 468 2028

Table 2-1 Unnecessary Fossil-based and Nuclear Generating Capacity after Adjusting Demand Growth and Accounting for Clean Energy

2.3 AN ECONOMICS-DRIVEN APPROACH TO REDUCE

utility projecting a 1.1% pre-energy efficiency growth

RELIANCE ON EXISTING FOSSIL-BASED

is modeled as growing slightly less than 0.6% per year.

rate and a 0.9% post-efficiency growth rate. Both

PLANTS

utilities expect their peak demand to grow at a faster

Combined with an expansion of renewable energy

resources, described in Section 2.4, a slower growth in

rate than electricity consumption, at 1.3% per year.

demand for electricity makes clear that building seven

Besides

After avoiding

considering recentbuilding

historicalnew fossil-

patterns andand nuclear-based

other generating

fossil plants capacity,

and one nuclear unit isthis

not study also

unnecessary

seeks to understand the ability to cost-effectively reduce North Carolina’s use of fossil-based

projections, this study does not use the growth rates (Table 2-1).

from the IRPs, as they project growth increasing

generating

improbably capacity.

rapidly. An evaluation

The primary counterpoint of the operating

2 . 3 cost

A N of

E Ceach

O N Ocoal-fired

M I C S - D R Iand

V E Ngas-fired plant

A P P R OAC H

TO R E D U C E R E L I A N C E O N E X I S T I N G

determines

grounding which existing

this analysis plants

is the demand are the most expensive

projection F O S S I L-for

B ANorth

S E D PCarolina

L A N T S ratepayers to keep

for the VACAR SERC region (which is dominated by

on the system. Operating cost is defined as the total costavoiding

Besides required to operate,

building maintain,

new fossil- and

and nuclear-based

Duke Energy and Dominion), produced by the Energy generating capacity, this study also seeks to understand

retain environmental

Information Administrationcompliance forAnnual

as a part of the a plant. Thethemaintenance cost for each plant is calculated

ability to cost-effectively reduce North Carolina’s

basedOutlook

Energy on FERC Form

(AEO). 6

This1report

data. isApublished

list of the cost categories

and that aregenerating

use of fossil-based included capacity.

in the calculation can

An evaluation

updated annually to incorporate the best information

be found in Appendix B.

the federal government has on the current state of

of the operating cost of each coal-fired and gas-fired

plant determines which existing plants are the most

the entire energy system and projects future demands expensive for North Carolina ratepayers to keep on

based on peer-reviewed published methodologies. the system. Operating cost is defined as the total cost 19

The model used for the Annual Energy Outlook is the required to operate, maintain, and retain environmental

same one used to analyze energy policy proposals for compliance for a plant. The maintenance cost for each

Congress and other interested parties within the federal plant is calculated based on FERC Form 1 data. A list of

government. the cost categories that are included in the calculation

In the Reference Case of the 2017 AEO, net energy for can be found in Appendix B.

load in the electric power sector in the VACAR SERC Using the Coal Asset Valuation Tool (CAVT), this study

region grows by 0.4% per year from 2017 through 2028. calculates the environmental compliance costs of the

Since AEO does not report peak demand growth, it is coal plants in DEC and DEP territory.7 Compliance costs

calculated by taking the ratio between growth in peak center on three areas: cooling water circulation, CCR,8

demand and growth in total consumption provided by and effluent discharges. The compliance costs for each

the utilities in the IRP filings and comparing this to the plant are first amortized and then added to the annual

growth in total consumption. As a result, peak demand maintenance costs to derive final operating costs.

A Pathway to a Cleaner Energy Future in North Carolina 11$20 million annual in operating costs and maintenance 2 . 4 .1 E N E R GY E F F I C I E N C Y P R O G R A M S

costs of $10,000 per MW are the criteria chosen to Energy efficiency in electricity use is evaluated sector-

define costly fossil plants. Plants requiring greater than by-sector. Estimates for naturally-occurring or federally-

these levels of investment to remain functional are driven energy efficiency improvements are derived

usually old plants with pollution control technologies from the 2017 Energy Information Administration

that are in need of upgrades in order to comply with Annual Energy Outlook Reference Case.9

current or upcoming environmental regulations.

ToUsing theoperating

continue Coal Asset Valuation

plants Tool

of this kind (CAVT), thisCost-effective

means study calculates the improvements

efficiency environmental for the demand

sectors are identified

7 and modified from studies by the

compliance

high costs

system costs thatofare

the coal plants

ultimately passedin on

DECto and DEP territory. Compliance costs center on

National Renewable Energy Laboratory (NREL) and

three areas: cooling water circulation, CCR8, and effluent

ratepayers. In the Cleaner Energy Plan, they are retired

the Americandischarges. The

Council for ancompliance costs

Energy- Efficient for

Economy

from the generating fleet, which produces ratepayer

each plant

savings; someare first amortized

of these plants were and then

already added

slated for to the annual maintenance costs to derive final

(ACEEE). The modeling approach starts with the

10,11

current annual energy efficiency levels achieved by the

operatingreflecting

retirement, costs. that this is not a wholly new

utilities, and captures ten percent of the achievable

approach to utility operations. Table 2-2 shows the

efficiency potential each year, such that these territories

$20 million

plants meeting annual

these cost in criteria.

operating costs

In the and Energy

Cleaner maintenance costs of $10,000 per MW are the criteria

have reached their potential by 2026. Afterwards, these

Plan, these plants are phased out of the generating

chosen to define costly fossil plants. Plants requiring greater

efforts than these

are maintained to levels

ensure of investment

there to

is no backslide

mix between 2018 and 2028, after considering system

remain functional are usually old plants with pollution

reliability. control

throughout thetechnologies

remainder of thethatmodeling

are in need of For

horizon.

more details, please see Appendix C.

upgrades in order to comply with current or upcoming environmental regulations. To continue

2 . 4 H A R N E S S I N G E C O N O M I C A L LY-V I A B L E

Coperating

L E A N E Nplants

E R GYof this kind means high system costs

2 . 4 .that

2 BU are

ILDultimately

I N G C O Dpassed

ES on to ratepayers.

New buildings also present an opportunity to improve

In Cleaner

The the Cleaner Energy

Energy Plan, they

Plan evaluates are retired from the generating fleet, which produces ratepayer

the economic

viability of increased reliance on renewable resources energy performance when building codes are adopted

savings; some of these plants were already

and energy efficiency as compared to the BAU case.

slated for

and retirement,

implemented. reflecting

New that

building this

code is not

standardsa are

wholly

These newenergy

include approach to utility

efficiency, operations.

demand response,Table 2-2 shows

issued on a the plantsthree-year

consistent meeting these cost states

basis. Several

have now passed legislation that updates the state

criteria.

solar In the Cleaner

photovoltaics, Energy

wind (both Plan,

in-state andthese plants are phased out of the generating mix between

out-of-

state projects), and energy storage. A brief summary of building codes when a new standard is issued by the

2018 and 2028, after considering system reliability. national and international authorities (ASHRAE and

the methodology for evaluating each of these resources

to derive an economic potential follows. IECC. Similar actions in North Carolina would improve

Table 2-2 Costly Fossil Plants in the DEP and DEC Generating Fleet

Plant Utility Plant Annual Amortized Total Maintenance

Type Maintenance Environmental Operating Cost

Cost Compliance Cost ($/MW)

Cost

Marshall DEC Steam 38,973,890 35,588,921 74,562,811 19,304

Coal

Belews DEC Steam 35,884,251 33,625,069 69,509,320 16,218

Creek Coal

Roxboro DEP Steam 33,246,288 33,278,126 66,524,414 14,403

Coal

Allen DEC Steam 18,428,679 29,055,468 47,484,147 15,976

Coal

Cliffside DEC Steam 17,914,907 10,255,269 28,170,176 15,031

Coal

Asheville DEP Steam 10,972,135 10,002,147 20,974,282 27,504

Coal

Mayo DEP Steam 13,121,549 7,702,420 20,823,969 20,171

Coal

Table 2-2 Costly Fossil Plants in the DEP and DEC Generating Fleet

7

The Coal Asset Valuation Tool (CAVT) was developed by Synapse Energy Economics. It aggregates data from

A Pathway to a Cleaner Energy Future in North Carolina 12

publically available sources. Environmental compliance costs come from a variety of public sources.new building energy efficiency through technology PVWatts model outputs to observed generation in

and shell improvements, and are generally considered Southeastern contexts. This assumption applies for

cost-effective.12 The energy savings associated with a solar in both utility-scale and distributed generation

code advancement vary. In this case, it is assumed that configurations. Panel technical performance is assumed

there is 2% annual building turnover,13 consistent with to degrade at 0.5% per year while new panel efficiency

national averages. The first code update assumes that improves at 0.25% per year.15

building codes will provide the average savings of the

Distributed solar capacity is deployed in accordance

past two code updates, as assessed by the Department

with the revealed consumer behaviors in North

of Energy. Each subsequent update occurs every three

Carolina. The price elasticity of demand for consumers

years, and is modeled as advancing the code by the

observed over the past several years is used to project

lower savings level of the previous two code updates.

future demand in light of projected declines in total

In total, there are four code updates modeled in this

installed cost for this customer segment.16 In addition,

manner.

a short-lived psychological response to achieving

2.4.3 DEMAND RESPONSE grid-parity, observed in more than a dozen other

Demand response programs currently exist within the states, is incorporated into the modeling of distributed

Duke territory, but do not currently make use of critical generation photovoltaic adoption.

peak pricing and technological approaches that are

Utility-scale solar deployments in North Carolina

now proven leading programmatic designs to establish

have been largely dictated by regulatory and policy

price sensitivity and ensuring smart grid integration as

decisions. Both Duke utilities are expected to add

a power-saving tool. The vast majority of customers

significantly to their solar portfolios to keep track with

served by Duke have been provided advanced metering

the North Carolina Renewable Energy and Energy

infrastructure (more than 90% of residential and

Efficiency Portfolio Standard requirements. However,

commercial customers in both DEC and DEP), but there

instead of stalling after the REPS targets have taken full

are no critical peak pricing programs.14

effect, the Cleaner Energy Plan continues to add to the

Since new technologies must be deployed to take solar portfolios of both utilities, as the recent Daymark

advantage of this potential, the realization of the Energy Advisors study has shown is economic.17 By

savings are phased in over a ten-year period, similar 2028, Duke Energy Carolinas is anticipated to have

to energy efficiency. The cost of direct load control roughly 4 gigawatts of solar capacity integrated onto

technologies and installations are taken from industry their system, while Duke Energy Progress is modeled as

suppliers (such as Cooper Industries) and program achieving 6.7 gigawatts.

and administrative costs reported for other efficiency

Wind

programs by Duke.

The generation characteristics for wind are derived

2 . 4 . 4 E N H A N C E D R E N E WA B L E E N E R GY from the Wind Prospector tool developed by the

P E N E T R AT I O N National Renewable Energy Laboratory (NREL). New

Many types and configurations of renewable energy are wind capacity is modeled both in North Carolina and

modeled to meet electricity demand in North Carolina wheeled in from other states; in North Carolina, wind

in both the Business-As-Usual and the Cleaner Energy generation profiles for northeastern coastal North

Plan. In the Cleaner Energy Plan, solar, wind, and energy Carolina are utilized, while wheeled power profiles are

storage are added to the system above BAU levels taken from Stillwater, Oklahoma, and near Lubbock,

to meet electricity demand in a least-cost fashion, Texas. Current costs for power purchase agreements

albeit with some technical, economic, and regulatory are taken from U.S. DOE’s Wind Technologies Market

restrictions on their deployment. The assumptions Report, while costs for in-state builds are taken from

behind each of these resources and their deployment the 2016 EIA Capital Cost report.18

trajectory follows.

In-state Development

Solar New wind capacity is added to the Duke Energy

The hourly generation of solar sited in North Carolina Progress territory, reviewing NREL estimates of cost-

is determined using the PVWatts model developed by effective coastal locations. While there is a cost-

the National Renewable Energy Laboratory. The lower effective wind resource in western North Carolina,

bound of the generation range produced by the model current regulations limit development prospects and

is used in this study due to experience in comparing amendments to these regulatory barriers are not

A Pathway to a Cleaner Energy Future in North Carolina 13Table 2-3 Duke Energy Carolinas (DEC) Generating Capacity and Reserve Margin under the Cleaner Energy (CE) Plan

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

BAU – System Total

Capacity (MW)* 22,722 22,735 22,839 22,835 22,857 24,153 24,232 24,126 24,179 25,294 25,292

CE – Avoided Plant 1221 468 1117

and Capacity (MW)

NGCC NGCT Nuclear

CE – Retirement 1,996 1,080 1,080 1,151 571 571

Plant and Capacity

(MW) Belews Belews

Marshall G.G.Allen Cliffside Cliffside

Creek Creek

Unit 1-4 Unit 1-5 5 6

Unit 1 Unit 2

CE – Total Added

Clean Resource

1,565 2,112 2,926 3,532 4,162 4,821 5,510 6,228 6,975 7,689 6,604^

Capacity (MW)**

CE – Total System

Capacity (MW) 20,726 20,739 19,763 18,679 18,701 17,621 17,129 16,555 15,698 15,696 15,694

CE – Total System

Peak Demand (MW) 17,324 16,874 16,158 15,650 15,119 14,559 13,970 13,352 12,706 12,093 13,280

CE – Reserve Margin

19.6% 22.9% 22.3% 19.3% 23.7% 21.0% 22.6% 24.0% 23.6% 29.8% 18.2%

Notes:

* Total system capacity according to DEC Table 2-3

2016 DukeIRPEnergy Carolinas (DEC) Generating Capacity and Reserve Margin under the Cleaner Energy (CE) Plan

* Total system capacity according to DEC 2016 IRP

** Clean energy resources include energy efficiency, distributed and utility scale solar, Clean Line wind, and demand response

** Clean energy resources include energy efficiency, distributed and utility scale solar, Clean Line wind, and demand response

^ The reduction in total added clean resource capacity in 2028 relative to 2027 is due to the change in the timing of peak demand.

^ The reduction in total added clean resource capacity in 2028 relative to 2027 is due to the change in the timing of peak demand. Until 2027, DEC system is expected to experience peak demand

duringUntil

summer2027, DECsolar’s

time, where system is expected

contribution topeak

to meet the experience peak demand

is higher compared to a winter during summer

peaking system. time,

In 2028, DECwhere solar’s

is expected to shift contribution

to winter peaking.to Asmeet

a result,the peak

solar’s is

contribution

higher compared to a winter peaking system. to meetingInthe2028, DECwhich

peak shrinks, is expected to shift

leads to the drop in theto winter

total peaking.

added clean resourceAs a result,

capacity solar’s

as it counts in thecontribution to

reserve margin analysis.

meeting the peak shrinks, which leads to the drop in the total added clean resource capacity as it counts in the reserve margin analysis.

Table 2-4 Duke Energy Progress (DEP) Generating Capacity and Reserve Margin under the Cleaner Energy (CE) Plan

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 26

BAU – System Total

16,892 16,958 16,359 16,404 16,811 16,825 17,021 17,026 17,499 17,502 17,738

Capacity (MW)*

CE – Avoided Plant and 1221 468 186 468 468

Capacity (MW) NGCC NGCT NGCT NGCT NGCT

380 673 698 711 746

CE – Retirement Plant

and Capacity (MW) Roxboro Roxboro Roxboro Roxboro

Mayo

Unit 1 Unit 2 Unit 3 Unit 4

CE – Total Added Clean

Resource Capacity 872 1,186 1,671 2,009 2,437 2,796 3,168 3,551 3,946 4,085 4,233

(MW)**

CE – Total System

16,512 15,905 14,608 14,653 13,839 13,385 12,684 12,689 12,694 11,951 11,719

Capacity (MW)

CE – Total System Peak

12,361 12,123 11,714 11,453 11,102 10,820 10,526 10,222 9,905 9,845 9,777

Demand (MW)

CE – Reserve Margin 33.6% 31.2% 24.7% 27.9% 24.7% 23.7% 20.5% 24.1% 28.2% 21.4% 19.9%

Notes:

* Total system capacity according to DEP Table20162-4 Duke

IRPEnergy Progress (DEP) Generating Capacity and Reserve Margin under the Cleaner Energy (CE) Plan

**Clean energy resources include energy efficiency, distributed and utility scale solar, coastal wind, Clean * Total system

Linecapacity according toCross

and Southern DEP 2016 IRP

**Clean

wind, energy resources

grid-facing include

battery energy efficiency,

storage, and demand distributed and utility scale solar, coastal wind, Clean Line and Southern Cross wind, grid-facing battery storage, and demand response

response

incorporated into the modeling. New wind in Duke Delivered Wind

Energy Progress is timed to maximize financial benefits, In addition to the capacity available for development

aiming to take advantage of anticipated cost declines within North Carolina, utilities could also procure wind

while still receiving the maximally-beneficial tax resources through transmission projects currently

treatment, targeting developments that break ground in underway, intended to deliver Midwestern wind

the 2018-2019 time frame. resources to the Southeastern United States. In this

case, both utilities are modeled as making significant27

A Pathway to a Cleaner Energy Future in North Carolina 14You can also read