Monro, Inc. Investor Presentation - EARNINGS CALL MAY 20, 2021 - March 2022

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Monro, Inc.

FOURTH QUARTER

InvestorFISCAL

Presentation

2021

EARNINGS

March 2022CALL MAY 20, 2021

Safe Harbor Statement and Non-GAAP Measures

Certain statements in this presentation, other than statements of historical fact, including estimates, projections, statements

related to our business plans and operating results are forward-looking statements within the meaning of the Private

Securities Litigation Reform Act of 1995. Monro has identified some of these forward-looking statements with words such

as “anticipates,” “believes,” “expects,” “estimates,” “is likely,” “predicts,” “projects,” “forecasts,” “may,” “will,” “should,” and

“intends” and the negative of these words or other comparable terminology. These forward-looking statements are based

on Monro’s current expectations, estimates, projections and assumptions as of the date such statements are made, and are

subject to risks and uncertainties that may cause results to differ materially from those expressed or implied in the forward-

looking statements, to include the significant uncertainty relating to the duration and scope of the COVID-19 pandemic and

its impact on our customers, executive officers and employees. Additional information regarding these risks and

uncertainties are described in the Company’s filings with the Securities and Exchange Commission, including in the “Risk

Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections of our

most recently filed periodic reports on Forms 10-K and Form 10-Q, which are available on Monro’s website at

https://corporate.monro.com/investors/financial-information/. Monro assumes no obligation to update or revise these

forward-looking statements for any reason, even if new information becomes available in the future.

In addition to including references to diluted earnings per share (“EPS”), which is a generally accepted accounting

principles (“GAAP”) measure, this presentation includes references to adjusted diluted earnings per share, which is a non-

GAAP financial measure. Monro has included a reconciliation from adjusted diluted EPS to its most directly comparable

GAAP measure, diluted EPS in Slide 10. Management views this non-GAAP financial measure as a way to better assess

comparability between periods because management believes the non-GAAP financial measure shows the Company’s

core business operations while excluding certain non-recurring items and items related to store closings as well as our

Monro.Forward or acquisition initiatives.

This non-GAAP financial measure is not intended to represent, and should not be considered more meaningful than, or as

an alternative to, its most directly comparable GAAP measure. This non-GAAP financial measure may be different from

similarly titled non-GAAP financial measures used by other companies.

2

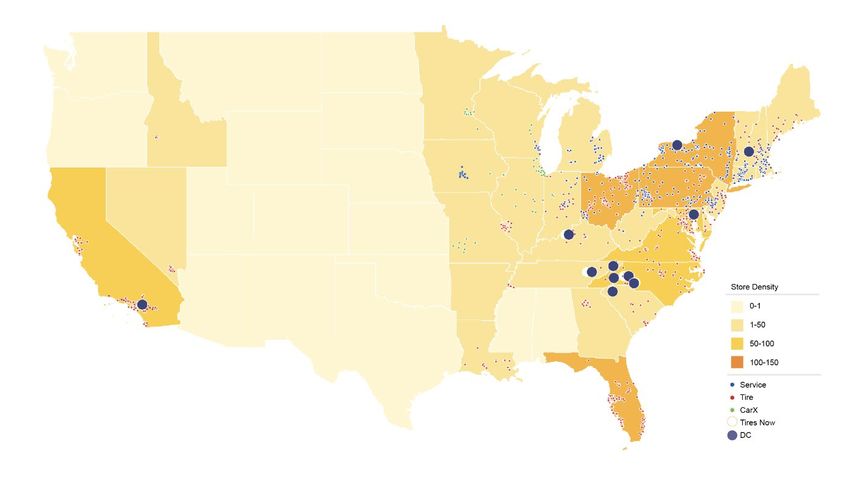

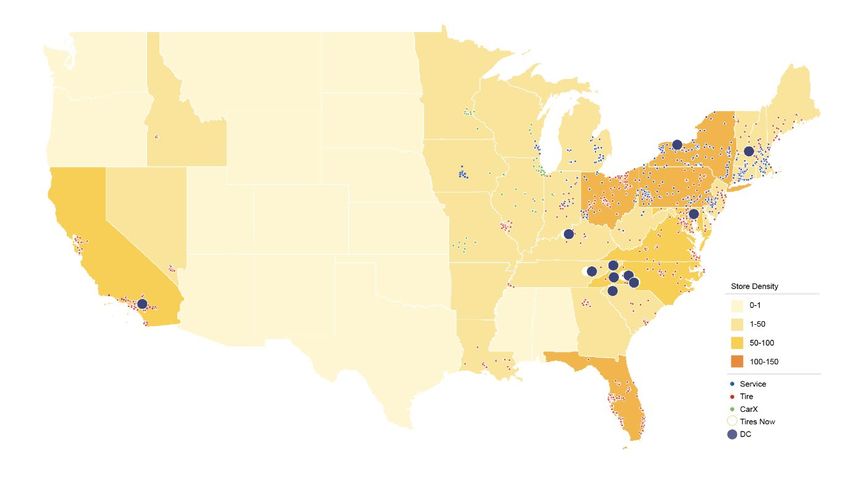

Company Overview

A Leading Chain of Independently Owned and Operated Tire and Auto Service Locations

Dominant in the Northeastern U.S. and expanding in Southern and

Western markets

Fiscal 2021 sales of $1,125.7 million

1,303 company operated stores in 32 states and 80 franchised

locations as of March 2, 2022

40 acquisitions in the past 9 fiscal years, adding 535 locations,

$730 million in revenue and entry into 13 new states

Operating two store formats in key markets

−Service brand stores – 438 stores

Store locations as of 3/2/22

• 75% maintenance service, 25% tires

• $675,000 a year in sales per store

−Tire brand stores – 865 stores (excluding wholesale)

• 55% tires, 45% maintenance service

• $1.0 million a year in sales per store

7 wholesale locations and 3 retread facilities

3

A Unique Operating Model

Monro Has a Diversified Supply Chain, Sourcing High Quality, Low-Cost Parts Direct and a Strong Portfolio of Tire Brands

PARTS

Monro sources these parts from leading Secondary parts distribution:

aftermarket parts suppliers:

Brake Rotors and Pads

Filters

Steering and Suspension

Wipers

Belts

TIRES

Store locations as of 3/2/22 4

Investment Thesis

Leading national

Focus on operational Scalable platform with

automotive service and Commitment to driving

excellence to increase significant growth opportunity

tire provider with 1,303 Monro.Forward Responsibly

customer lifetime value in acquisitions

locations in 32 states

Well-positioned to capitalize Delivering consistent

Low-cost operator with solid Strong balance sheet and

on a favorable industry shareholder returns through

operating margins operating cash flow

backdrop dividend program

5

A Favorable Industry Backdrop

Favorable Industry Backdrop for Automotive Services

Despite a Decrease in Miles Traveled in 2020 Resulting from the COVID-19 Pandemic

U.S. Annual Light Vehicle Sales U.S. Light Vehicles in Operation (VIO)

290,000

20

18 280,000

16

270,000

14

12 260,000

10

250,000

8

6 240,000

4

230,000

2

0 220,000

05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Source: FRED Economic Data, Light weight Vehicle Sales: Autos and Light Trucks (annual data) Source: Auto Care Association Factbook

Annual Vehicles Miles Traveled Key Highlights

3,300,000

3,225,000 Although a slight decrease in VIO for 2021, an overall

3,150,000 growing trend in total vehicle population related to

3,075,000

consumers owning vehicles longer

3,000,000 270+ million vehicles on the road

2,925,000 Increasing age of vehicles (average of ~12 years)

2,850,000 Increasing complexity of vehicles

2,775,000 Vehicle miles traveled recovering from 2020 lows

2,700,000

05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21

Source: FRED Economic Data, Moving 12-Month Total Vehicle Miles Traveled 6

A Favorable Industry Backdrop

Monro is Well-Positioned to Capitalize on Positive Industry Trends,

with Our Sweet Spot Experiencing the Fastest Growth in Vehicles in Operation

Vehicles in Operation – 0 to 5 Years Vehicles in Operation – 6 to 12 Years

120 120

110 +6.56% CAGR -.03% CAGR 110 -3.97% CAGR +3.90% CAGR

100 100

90 90

80 80

70 70

60 60

50 50

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Vehicles in Operation – 13+ Years Key Highlights

120 +4.27% CAGR +1.47% CAGR Monro’s targeted market segment is the 6-12 year

110 cohort

100 Strong growth in new vehicles (0-5 years) between 2012

90 and 2017 is creating a significant tailwind for the 6-12

80 year old vehicle cohort for the next couple of years

70 6-12 year cohort expected to grow the fastest at +3.9%

60 CAGR for the period 2017-2022

50

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Source for all data: Lang, IHS Markit, 2018 7A Favorable Industry Backdrop

Monro Operates in the $252 Billion Do-It-For-Me* Segment of $325 Billion U.S. Automotive Aftermarket Industry

Automotive Aftermarket DIFM vs. DIY Sales % %

2010 2020 CAGR

(outlets) (outlets)

350,000

Dealers 18,460 14.3% 16,623 12.5% (1.0%)

300,000

General Repair

250,000 76,108 58.8% 82,454 62.1% 0.8%

Garages

200,000

Tire Dealers 18,675 14.4% 20,327 15.3% 0.9%

150,000

Specialty Repair 8,663 6.7% 6,137 4.6% (3.4%)

100,000

50,000

Oil Change/Lube 7,518 5.8% 7,305 5.5% (0.3%)

0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 Total 129,424 100.0% 132,846 100.0%

DIFM DIY

Source: Auto Care Association Factbook Census data for 2012; estimates for 2013-2020; 2021 forecast Source: Auto Care Association Factbook

DIFM vs. DIY Trends Key Highlights

DIFM continues to account for a significant percentage Industry still highly fragmented, with significant

of the automotive aftermarket opportunities for further consolidation

Vehicle complexity continues to drive shift to DIFM from

DIY

Future technology advances expected to accelerate

shift to DIFM

* Includes Replacement Tire Segment 8Third Quarter Fiscal 2022 Highlights

Delivered Third Consecutive Quarter of Double-Digit Comparable Sales Growth; Topline Exceeded Pre-Pandemic Levels

Quarterly Comparable Store Sales Trends Monthly Comparable Store Sales Trends

34.5% 17.5%

13.8%

9.0%

14.8% 13.8% 3.1%

1.0%

9.4%

-6.4%

-12.3%

-13.0% -18.2%

1

Q3FY21 Q4FY21 Q1FY22 Q2FY22 Q3FY22 October November December January

FY21 FY22

Q3FY22 Q3FY22

Key Highlights Key Highlights

Sales increased 20.1% to $341.8M Double-digit comps in all product and service categories

Comparable store sales increase of 13.8%; Brakes: 28%

preliminary fiscal January ~4% above pre-COVID Alignments: 28%

performance

Front End/Shocks: 14%

Sales from new stores added $18.5M, primarily from

recent acquisitions Service: 11%

Generated strong operating cash flow of ~$127M Tires: 11%

driven by profitability and working capital Service categories increased to ~44% of total sales

management compared to ~43% in prior year period

1Preliminary results through January 22, 2022 9Third Quarter Fiscal 2022 Results

Solid Results Reflect Demand Recovery and Strong Operational Execution

Q3FY22 Q3FY21 Δ FY22 YTD FY21 YTD Δ

Sales (millions) $341.8 $284.6 20.1% $1,031.3 $820.2 25.7%

Same Store

13.8% -13.0% 2,680 bps 20.3% -16.8% 3,710 bps

Sales

Gross Margin 35.3% 33.8% 150 bps 36.6% 35.1% 150 bps

Operating

8.0% 5.5% 250 bps 8.7% 6.3% 240 bps

Margin

Diluted EPS $.48 $.20 140.0% $1.56 $.67 132.8%

Excluded

$.01 $.02 $ .10 $.09

Costs1

Adjusted

$.49 $.22 122.7% $1.66 $.77 115.6%

Diluted EPS2

1 Excluded costs in Q3FY22 include $.01 per share related to Monro.Forward initiatives. Excluded costs in Q3FY21 include $.02 per share related to Monro.Forward initiatives and a benefit related to the reversal of a reserve for potential litigation. Excluded costs for

FY22 YTD include $.08 per share related to one-time litigation settlement costs, $.03 per share of acquisition due diligence and integration costs and Monro.Forward initiatives and $.01 per share of benefit from an adjustment to the estimate for prior year store

closing costs. Excluded costs in FY21 YTD include $.06 per share related to store closing costs and $.04 per share related to Monro.Forward initiatives and management transition and $.01 per share benefit related to a reserve for potential litigation that is no longer

necessary.

2 Adjusted EPS is a non-GAAP measure that excludes certain non-recurring items and items related to our Monro.Forward or acquisition initiatives. A reconciliation of net income to adjusted net income and diluted EPS to adjusted diluted EPS is included in our

earnings release dated January 26, 2022.

Note: The table may not add down +/- due to rounding.

10Solid Financial Position

Strong Operating Cash Flow Supports Growth Strategy and Cash Dividends to Shareholders

Disciplined Capital Allocation Strong Balance Sheet and Liquidity

YTD Fiscal 2022

Capex of ~$17M Generated ~$127M of operating cash flow during

YTD fiscal 2022

Paid ~$83M for acquisitions

Net bank debt of ~$185M as of December 2021

Spent ~$29M in principal payments for financing

leases Net bank debt-to-EBITDA ratio as of December

2021 of 1.0x

Paid ~$26M in dividends

Liquidity position of ~$385M as of December

2021

11Strategic Priorities

Take Advantage of Growing Retail Demand to Sustain Long Term Growth

Improve in-store operational execution with a focus on the “Big Five” - Staffing, Scheduling,

Training, Attachment Selling and Outside Purchase Management

Execute store reimage program with current focus on recent West Coast acquisitions

Continue to be the acquirer of choice for family-owned businesses with our easily scalable platform

Further integrate Corporate Responsibility efforts into our strategy and operations

12Focus on In-Store Execution

Attachment Outside Purchase Store Reimage

Staffing Scheduling Training

Selling Management Program

Sustainable Comp Sales Growth

Gross Profit Operating Margin Acquisition

Improvement Expansion Growth

Creates Additional Value for Shareholders through:

Enhanced Significant Higher Returns

Earnings per Cash on Invested

Share (EPS) Generation Capital

13Monro.Forward Progress Update

Focused on Aspects of Business Within Our Control to Drive Profitable Growth and Operational Excellence

Focused on advancing vision to be a best-in-class field-led service organization to increase

Improve Customer the overall lifetime value for customers

Experience

Outperformance of rebranded and reimaged stores reinforces strength of strategy

Optimized marketing spend towards higher ROI channels to drive improved SEO

Enhance Customer- performance in tires and key service categories

Centric Engagement Leveraging modernized store infrastructure and phone system to improve customer

execution

Optimize Product & Dynamically tracking demand trends to drive tire volume and margin expansion

Service Offering Focused on category management to capitalize on service attachment opportunities

Well-positioned to drive labor productivity

Accelerate Productivity

Focused on leveraging Monro University and in-store training and providing the Automotive

& Team Engagement

Service Excellence certification to drive operational excellence and improved in-store execution

14A Scalable Platform: Recent Acquisitions

Executing Disciplined M&A Strategy to Capitalize on Significant Opportunities for Consolidation in the Aftermarket

Acquisitions

Completed the previously announced acquisitions of 17 stores, including six in Southern California

and 11 in Iowa

Further expands the Company’s geographic footprint in the Midwest and Western United States

Represents ~$25M in annualized sales

Brings fiscal year-to-date acquisition total to 47 stores and ~$70M in annualized sales

Fiscal 2022 Acquisition Outlook

Financial flexibility to continue to roll up attractive opportunities in a highly fragmented industry

Significant growth prospects in the attractive and dynamic Western region

Evaluating a robust pipeline of attractive M&A opportunities that support our strategy while

maintaining strong financial discipline

15Appendix

16Fiscal 2022 Outlook – Financial Assumptions

Financial Assumptions as of January 26, 2022 Q4 Outlook Considerations

Tire and Oil Costs Increase y/y

Preliminary fiscal January comps increased

~1% and were ~4% above pre-COVID levels

Interest Expense ~$25M to ~$27M

Expect continued investments in store labor

Depreciation and Amortization ~$82M to ~$85M and gross margin improvement versus prior

year as service category sales strengthen

Tax Rate ~25%

Capital Expenditures ~$30M to ~$40M

Weighted Average Number of Diluted

~34M

Shares Outstanding

17You can also read