MNI Fed Preview: March 2022

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

MNI Fed Preview: March 2022

Meeting Dates: Tue-Wed, 15-16 March

Decision/Statement/Summary Of Econ Projections: Wed 16 March at 1400ET / 1800GMT

Press Conference/Q&A: Wed 16 March at 1430ET / 1830GMT

Minutes: Wed 6 April

Links (likely URLs based on previous meetings):

Statement: https://www.federalreserve.gov/newsevents/pressreleases/monetary20220316a.htm

Summary of Econ Proj: https://www.federalreserve.gov/monetarypolicy/fomcprojtabl20220316.htm

Implementation note (if applicable):

https://www.federalreserve.gov/newsevents/pressreleases/monetary20220316a1.htm

Press Conference: https://www.federalreserve.gov/monetarypolicy/fomcpresconf20220316.htm

MNI Review of Previous FOMC (Jan): https://roar-assets-auto.rbl.ms/documents/13647/FedReviewJan2022.pdf

Contents

• Page 1-5: MNI POV (Point of View) / Summary Of Economic Projections Outlook

• Page 5: MNI Instant Answers

• Page 6: Market Implied Rates / MNI Central Bank….Data Watch

• Page 7-10: Key FOMC Communications / MNI Hawk-Dove Spectrum

• Page 11-17: Analyst Meeting Outlook / Individual Sell-Side Analyst Views

• Page 18-34: MNI Policy Team Insights

MNI POV (Point Of View): Lifting Off Amid New Uncertainty

By Tim Cooper

• The FOMC will hike rates for the first time since 2018 at the March meeting, opting for a 25bp increase.

• The Statement and Chair Powell will signal that this hike is the beginning of a series of increases.

• But solid forward guidance may prove elusive, especially given geopolitical uncertainties.

• The Dot Plot median is likely to show at least 5 rate hikes in 2022, with risks that the median “Dot” is even higher than

that if participants want to bring rates close to “neutral” quickly in the face of high inflation pressures.

• We may get more specifics on balance sheet policy as the Fed eyes reducing its asset holdings beginning in the

coming months.

Coming into 2022, the March FOMC was set to among the most pivotal in years, with the Fed due to hike the Funds rate for the

first time since 2018. It’s still a pivotal meeting in many respects, even if Chair Powell removed the biggest area of uncertainty

by saying that he would be “recommending and supporting” a 25bp increase. That deflated most remaining expectations that the

FOMC would hike by 50bp to kick off its rate hike cycle (an increase of that magnitude was fully priced in at one point in

February). The March decision thus looks straightforward and anything other than a 25bp hike is extremely unlikely.

The medium-term outlook is as uncertain as ever, though, and the

March meeting provides an opportunity for the FOMC to express

how they see the state of play in the economy and the outlook for

both interest rate and balance sheet policy.

One Risk Swapped For Another: Arguing for a clearly hawkish

stance is that inflation is soaring and broadening out, and the very

tight jobs market has largely shrugged off the Omicron wave fears.

Complicating the outlook: geopolitical risks have heightened

significantly since late February with Russia’s invasion of Ukraine.

That’s tightened financial conditions, heightened economic

uncertainty, and produced a huge supply-side commodity price

shock (and exacerbated existing global supply chain concerns). In

effect, one major stagflationary risk to the outlook has been

1

swapped for another one: the accompanying chart shows the Fed-developed Geopolitical Risk Index rising, just as the

impact of Covid petered out. (see our Economic Indicators section below for more discussion on recent developments

and what they might mean for the Fed’s projections.)

Solid Guidance Could Be Elusive: As with other FOMC

participants who spoke following the Russian invasion of Ukraine,

Powell noted that geopolitics posed upside risks to inflation and

downside risks to the growth outlook, but signalled that this didn’t

fundamentally alter the Fed’s policy outlook for the time being: he

still envisaged a “series” of rate hikes beginning in March, with the

Fed simultaneously raising rates and allowing the balance sheet to

run off. While the FOMC continued to expect inflation to decline

over the course of the year, he said that if inflation comes in higher

or is more persistent than expected, the Fed is prepared to hike by

increments greater than 25bp (i.e. 50bp).

Powell is likely to repeat those themes in the post-meeting

press conference. However, any more solid forward guidance

out of this meeting may prove elusive. Current and former Fed

policymakers tell MNI that the FOMC may shy away from explicit rate guidance, emphasizing that decisions are being made on

a meeting-by meeting basis (see our MNI Policy Team insights at the end of this preview, including interviews with SF

Fed Pres Daly and ex-Boston Fed Pres Rosengren).

Statement: Series

(Link to January FOMC statement)

Apart from a surprise to the rate announcement itself, the Statement is unlikely to be a significant catalyst for market reaction at

this meeting. Accordingly, we haven’t included any statement changes in our Instant Answers. But we will be alert for a few

areas that could change (apart from the usual mark-to-market changes on job gains and inflation since the last meeting):

• Forward guidance: The most impactful change to the statement would be any signal of the FOMC’s envisaged rate

hike path. Most likely, the FOMC will opt to take a nimble (to use a Powell-ism), data-dependent, meeting-by-meeting

approach to removing accommodation, and this will be reflected in the statement language.

• The Statement could mention the FOMC expects the March hike to be the first of a “series” of hikes (a term

used by both Powell and Brainard), which would maximize optionality on pace and magnitude as it assesses

incoming inflation data and expectations, while also confirming that multiple increases are envisaged.

• We should note that some on the sell-side expect something that would be interpreted more hawkishly: Deutsche Bank

for instance expects the Fed to say it’s appropriate to hike “at least at a measured pace”.

• The Statement could also include a reference to balance sheet runoff plans, keeping the door open to a start to QT as

soon as the May FOMC should conditions warrant. (See next section for possible additional QT detail.)

• Covid Zero?: “The sectors most adversely affected by the pandemic have improved in recent months but are being

affected by the recent sharp rise in COVID-19 cases” in the opening paragraph, and the second paragraph beginning

“The path of the economy continues to depend on the course of the virus.” As concerns dissipate over the Omicron

wave and the pandemic more broadly, this language is likely to be softened, with potential for the second paragraph to

be eliminated altogether.

• War Time: Expect the statement to insert new language referring to risks to the growth / inflation outlook from

geopolitics / the invasion of Ukraine, potentially supplementing or replacing the language surrounding Covid risks. This

could crib from Chair Powell’s congressional testimony at the start of the month: “The near-term effects on the U.S.

economy of the invasion of Ukraine, the ongoing war, the sanctions, and of events to come, remain highly uncertain.”

• The January statement language “Overall financial conditions remain accommodative” could be tweaked to reflect

the negative impact of geopolitical risk on financial conditions since the Ukraine invasion.

• Any dissents? If the FOMC opts for a 25bp increase, as is overwhelmingly expected, it’s possible we see a dissent

from St Louis Fed Pres Bullard who has eyed a 50bp increase in March, and possibly even Gov Waller as well who has

advocated 100bp in rate hikes by mid-year. But a dissent or two ultimately would not be consequential for markets, and

Bullard, for one, has said he’d defer to Powell to lead the way to a 50bp increase (the Chair has since signalled that his

preference is for a 25bp increase).

Balance Sheet: Laying Out The Plan?

Powell has signalled the FOMC would further address balance sheet runoff at the March meeting, though it’s widely thought the

formal announcement and actual implementation date will come later in the year (no sell-side analyst expects a full-blown

announcement this week, with May seen as the earliest date for the Fed to start quantitative tightening, “QT”). We could get

more details this week.

2

• The January FOMC provided a modest surprise with the release of an addendum “Principles for Reducing the Size of

the Federal Reserve's Balance Sheet” which laid out a very basic outline for asset runoff. The FOMC could decide to

add more detail this time on the magnitude of the anticipated runoff pace. If so, this would probably appear in a new

document with language similar to the June 2017 FOMC addendum, which laid the groundwork for QT starting in

October 2017.

• Markets will be attuned to three key details: 1) the initial monthly “caps” for reinvestment above which maturing

proceeds will be allowed to roll off (in 2017 this was $6B for Tsy and $4B for MBS, for $10B total); 2) the pace of cap

ramp-up (in 2017 they upped the caps by $10B total at 3-month intervals over 12 months); and 3) the terminal pace of

caps (in 2017 this was $50B total). We’ve included questions on initial and terminal pace in our Instant Answers.

• In general, consensus is that this round of QT will start by mid-2022, with a quicker ramp-up period and both a faster

initial pace and terminal pace, reflecting the relatively larger size of the balance sheet. Broadly speaking, consensus is

for $20-30B initial pace, with a 3-month ramp-up period, and a terminal pace of $80-100B (mostly Treasuries).

• Other details we could receive could include whether MBS proceeds will be reinvested into Treasuries; whether the bill

portfolio will be maintained or allowed to roll off; and whether the Fed will conduct outright sales of securities. But such

details are likely to have to wait for future meetings, and/or when the Fed makes a formal QT announcement.

Dot Plot: 6+ 2022 Hikes Would Be Hawkish

(Link to December FOMC SEP)

The March Dot Plot will show an upward shift in both median rate

hike expectations and the upper-end of the distribution vs

December’s edition, though MNI also expects a fairly wide

dispersion in rate expectations particularly in 2023-24 reflecting

significant policy uncertainty. Including March, there are 7

meetings remaining this year; note that this Summary of Economic

Projections (SEP) is expected to include 16 participants, not 18 as

in December. Our Instant Answers look for the medians for

2022, 2023, and 2024, as well as the longer-run dot. MNI’s

tentative expectations are in the chart at the right.

For the 2022 Fed funds median, general consensus is that we will

see a rise from 3 hikes (0.9%) in the last SEP to between 4 and 6

hikes (we assume all hikes will be 25bp in size). 5 is MNI’s

baseline, with risks of 6. 4 would be a very dovish surprise; 6

would be a modestly hawkish surprise; 7 or more would be

very hawkish.

There appears to be ample appetite among the FOMC for a robust

opening response to surging inflation before giving way to a

meeting-by meeting, data-driven approach in which inflation

pressures are expected to relent at least somewhat. Consecutive hikes in March, May, and June look very likely as a

starting point for a “series” (per Powell and Brainard’s language) of intended hikes, followed by a slowdown in pace to quarterly

raises in September and December as the outlook is continually reassessed.

But there are mostly upside risks as we could easily see 6 or 7 participants go for 7 rate hikes in 2022 (to 1.75-2.00%).

This would include some of the hawks (Bullard, Waller) but also perhaps some surprises, including doves such as Chicago’s

Evans (who said earlier this month that “If we were to do 25 basis points at each meeting, which may be more than I think is

essential, but if we did it at each meeting, we’ll end the year at 1.75% to 2%. That is close enough to neutral that we could take

quick action if it were necessary. Or we could stick or we could back off if that is what the case was.”)

Our Instant Answers look for the distribution of 2022 hike dots, namely, how many 2022 dots are above 1.375% (ie how

many FOMC participants see more than 5 25bp hikes). Our expectation is for 6, which leans toward the hawkish end of

prevailing expectations given the sell-side previews we’ve read. A large number above 5 without raising the median would

probably skew the market’s interpretation of the Dot Plot in a hawkish direction.

The question for the 2023 and 2024 medians is how quickly the FOMC sees getting to “neutral” after front-loading

hikes in 2022. Consensus expectation is for a further 3 to 4 hikes to be signalled in the 2023 median, with zero to 2 further

hikes in 2024, leaving rates at roughly neutral (the longer-run dot that signifies neutral is between 2.25-2.50%, for most

participants, and is not expected to change this week).

The 2023 Dot median of 2.00-2.25% (ie 200bp of hikes, incl 125bp in 2022 and 75bp in 2023), with a roughly even number on

either side of a 2.00% rate and outliers skewed to the high side. That would leave rates at around neutral by end-2023, leaving

the 2024 hiking outlook at 1-2 hikes (to 2.50%), though with no clear FOMC consensus. By comparison, the December Dot Plot

showed rates ending 2023 at 1.625%, and 2024 at 2.125%.

3

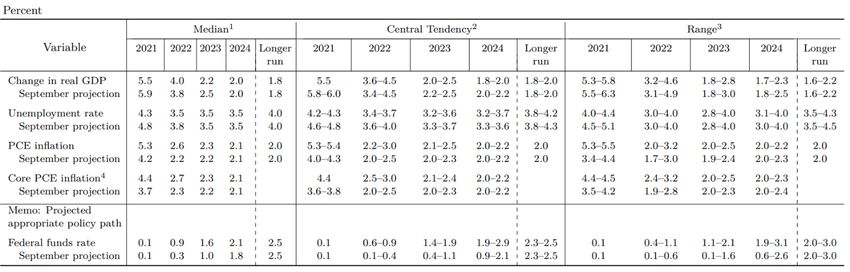

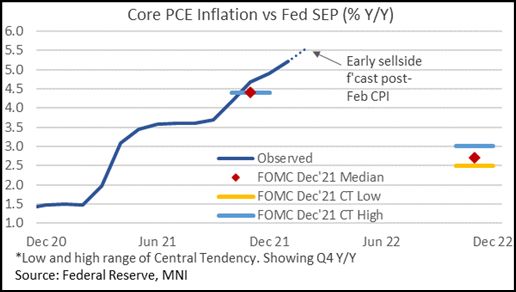

Economic Projections: Inflation Higher, Unemployment Largely Unchanged

By Chris Harrison

Core PCE inflation likely revised up substantially for 2022,

but much less so in 2023? Since the last round of economic

projections at the FOMC’s December meeting, core CPI inflation

has continued its string of rapid price increases, twice exceeding

consensus and more recently in line at more than double the

pace consistent with the 2% inflation target. February’s data

showed a long-awaited moderation in core goods inflation,

potentially as supply side disruption fades, but it comes just as

core service inflation ramps up with the fastest monthly print

since 1992. Core services have been driven by particularly

strong rent inflation due to hot housing and labour markets.

Shelter may have a larger weight in CPI than PCE, but this has

nevertheless seen core PCE surge higher to 5.2% Y/Y in

January and with ~5.5% Y/Y expected in February judging by

early sell-side estimates.

Bloomberg consensus puts Q4 core PCE inflation at 3.6% Y/Y in 4Q 2022, requiring a significant mark-to-market from

the 2.7% in the median FOMC forecast. However, the Bloomberg survey is unlikely to fully capture the impacts from the

continued war in Ukraine, and it’s here that the FOMC’s forecasts will be particularly interesting, especially in 4Q 2023, to see

how it weighs up the shocks from demand destruction and further supply side disruption.

DECEMBER 2021 FOMC: Economic projections of Federal Reserve Board members and Federal Reserve Bank presidents, under their

individual assumptions of projected appropriate monetary policy. Source: Federal Reserve

Little change in the unemployment rate projection expected: The FOMC had November data at its last round of projections

and since then payrolls have increased by a huge 1.75mln over the subsequent three months. Gains have been even larger in

the household survey but there has also been an increasingly fast recovery in participation as businesses and households alike

adapt to work in the pandemic era. This limited the rate of decline in the unemployment rate, especially during recent Omicron

disruption.

At just 3.8% in February, the unemployment rate is already close to the 3.7% from the high end of the FOMC’s central

tendency range for 4Q2022 and not far from the 3.5% median. However, Bloomberg consensus expect much slower

progress in the unemployment rate ahead and is exactly in line with the FOMC median come the end of the year. Substantial

revisions are therefore unlikely for 2022, and 2023-24 medians will probably remain relatively steady (also 3.5%).

4

Growth outlook to reflect substantial tightening in financial conditions since

last SEP: Even prior to the uncertainty around the medium-term global growth

impact from the war in Ukraine, the domestic growth outlook will be weighed on by

the significant tightening in financial conditions since the last SEP. 10Y Treasury

yields have increased more than 60bps, which with 2Y yields rising 115bps over

the same period has seen the curve flatten to March 2020 flats, and equities are

down more than 10%.

A large part of this has come from a significantly steeper Fed rate path being priced

in, with an additional 65bps up to and including the June meeting and four

additional hikes through 2022 compared to the Dec 15 meeting. Changes since

the last FOMC decision on Jan 26 have unsurprisingly been less pronounced but

significant nevertheless – see the table at right.

MNI Instant Answers:

The questions that we have selected for this meeting are:

• Federal Funds Rate Range Maximum

• Median Projection of Fed Funds Rate at End of 2022

• Median Projection of Fed Funds Rate at End of 2023

• Median Projection of Fed Funds Rate at End of 2024

• Median Projection of longer run Fed Funds Rate

• How many 2022 dots are above 1.375 (more than 5 hikes)?

• If the FOMC gives details on QT, what is the amount capped per month INITIALLY (Treasuries and MBS)?

• If the FOMC gives details on QT, what is the amount capped per month by the end of the ramp-up period

(Treasuries and MBS)?

(Formerly Human Readable Algo) The markets team have selected a subsection of questions we think could be most market moving and will publish the

answer to all of these questions within a few seconds of the Fed statement being released. These questions are subject to change; clients will be

informed of any changes via our Edge and Bullets services. A comprehensive list of questions is available on the MNI Monitor (available via the

website here: https://www.marketnews.com/realdisplay?product=AFM

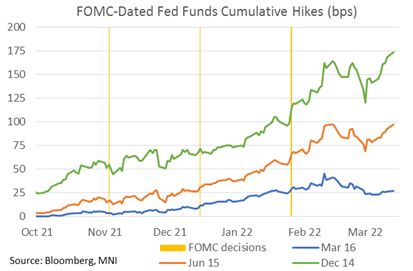

5Market-Implied Rate Outlook

Source: Bloomberg, MNI Market News. Updated March 14, 2022

Rate futures markets are pricing in roughly 175bp of Fed funds increases in 2022, up from around 100bp at the

January FOMC. By the June FOMC, markets are pricing just under 100bp of increases (vs under 75bp priced

at the Jan meeting). Conversely, while liftoff is still seen at the March meeting (as had been priced after the

January FOMC), markets have backed off pricing a 50bp March increase which was the case briefly in

February.

• Since the January FOMC, the growth outlook has weakened even as inflation and wage growth have remained

very strong. Uncertainty over the war in Ukraine has tightened financial conditions. (Updated Mar 11, 2022)

6Key Inter-Meeting FedSpeak – Mar 2022

Chair Powell set the expectations for the March 15-16 FOMC during his congressional testimony at the start of the

month, saying the Fed would have to be “alert and nimble” in setting policy going forward.

• Coming into the month, FOMC participants had all but unanimously concurred that rate liftoff would occur

at the March meeting.

• Powell made it clear that he would be “recommending and supporting” a 25bp rate hike at the March 15-16

FOMC, effectively closing the case for a 50bp increase. However, he also said that the Fed could move in

increments greater than 25bp in future meetings should conditions warrant.

• Powell, and Gov Brainard in February, both indicated that the FOMC would begin a “series” of rate hikes.

• As with other FOMC participants who spoke following the Russian invasion of Ukraine, Powell noted that

geopolitics posed upside risks to inflation and downside risks to the growth outlook, but signalled that this

didn’t fundamentally alter the Fed’s policy outlook for the time being.

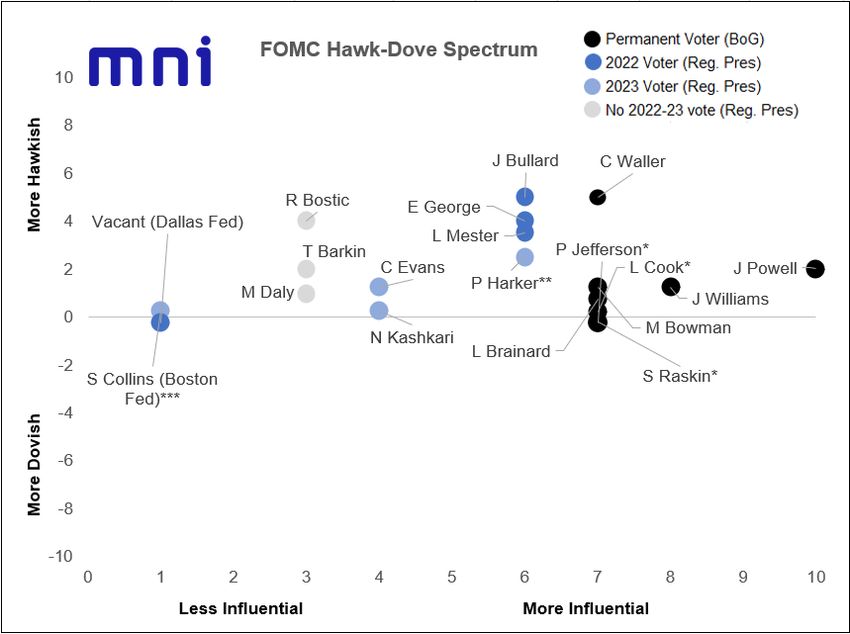

• Some notable inter-meeting commentary came from both ends of the Hawk-Dove spectrum.

• Chicago Fed’s Evans, a noted dove, said that he could see the Fed bringing rates up to close to neutral by

end-2022. Likewise, SF Fed’s Daly pointed to potential for more than 4 hikes in 2022.

• On the hawkish end, Gov Waller and St Louis’s Bullard advocated for 100bp of tightening by mid-2022.

• Overall though, FOMC members were fairly non-committal on the path and magnitude of hikes ahead,

pointing to the need for data-dependence: particularly regarding inflation.

• KC’s George (a hawk and 2022 voter) suggested that balance sheet reduction could substitute for rate

hikes to some extent in the removal of accommodation.

Our matrix uses the following methodology based on the MNI Markets Team`s subjective analysis. Hawkish/Dovish

scores indicate MNI`s subjective assessment of each member`s stance on monetary policy. -10 implies member

believes aggressive easing warranted; +10 is most hawkish, implies member believes aggressive tightening

warranted. Scores around -2 to +2 considered relatively neutral. On Influence, the x-axis runs from 0 ('least

influential') to 10 ('most influential'). Voters in the current year receive a minimum score of 6; the Chair receives a 10

and Board of Governors members receive at least 7. Those who are not voters in the current year are limited to a

score of 4; among them, those due to vote next year receive higher influence scores (rising towards end of current

year), and vice-versa. * Board of Governors nominees awaiting confirmation; monetary policy bias assumed for now

to be neutral. ** Harker expected to vote at Mar 2022 FOMC in place of interim Boston Fed President. *** Collins

assumes Boston Fed presidency on July 1.

Voter

Member Role Monetary Policy Commentary Since January FOMC

‘22 ‘23

Powell’s comments from the Mar 2-3 Semi-Annual Monetary Policy Testimony:

BOG,

J Powell X X On a March rate hike: “With inflation well above 2 percent and a strong labor market, we expect it will be

Chair

appropriate to raise the target range for the federal funds rate at our meeting later this month.” “I would be

7Voter

Member Role Monetary Policy Commentary Since January FOMC

‘22 ‘23

recommending and supporting a one quarter of 1% increase”…”To the extent that inflation comes in higher or is

more persistently high than that, then we would be prepared to move more aggressively by raising the federal

funds rate by more than 25 basis points at a meeting or meetings.”

On monetary policy: “We need to be alert and nimble as we make decisions.” “What we’re very much about to

do is both raise interest rates and allow the balance sheet to shrink and run off.” “Before the [Ukraine] invasion

we were planning to make a series of interest rate increases, that is still the case.”

On geopolitical risks: “The near-term effects on the U.S. economy of the invasion of Ukraine, the ongoing war,

the sanctions, and of events to come, remain highly uncertain…I do think it’s going to be appropriate for us to

continue to proceed along the lines that we had mind before the Ukraine invasion happened and that was to

raise interest rates at the March meeting and continue through the course of the year…in this very sensitive time

at the moment, I think it’s appropriate for us to be careful in the way we conduct policy simply because things are

so uncertain and we don’t want to add to that uncertainty.”

On inflation: “We continue to expect inflation to decline over the course of the year as supply constraints ease

and demand moderates because of the waning effects of fiscal support and the removal of monetary policy

accommodation.”

On balance sheet reduction: [The FOMC] “will proceed in a predictable manner primarily through adjustments

to reinvestment”…[will take] “in the range of three years” [to reach Fed’s desired size]… this is the

meeting we're going to have in two weeks…We’re going to set a pace at which runoff will happen subject to

caps”.

On the terminal rate: “We talk about getting to neutral, which is a neutral rate which would be somewhere

between 2% and 2.5%. It may well be that we need to go higher than that. We just don’t know.”

On a March rate hike: “We clearly have opportunities to take policy actions over this year starting in March.

Personally, I don’t see any compelling argument to take a big step at the beginning.” – Feb 18

On rate hikes: [Following rate hike in March, sees], “steadily raising the federal funds rate toward more normal

NY levels” … I’m not saying the market has everything right, the point is what I see out there in market expectations

J Williams Fed, V X X is consistent with the basic viewpoint that I have of where we need to be moving.” [If inflation more persistent

Chair than expected] “we have the ability to adjust interest rates higher”. – Mar 3

On balance sheet reduction: [Will occur] “more or less in the background” [and begin this year]. – Mar 3 “more

quickly” and “sooner relative to liftoff” [vs previous cycle]. [MBS sales are a] “question for the future…if we do

that, we would discuss it thoroughly”. – Feb 18

On a March rate hike: “Given we have seen quite strong data, I do anticipate it will be appropriate at our next

meeting to initiate a series of rate increases.” – Feb 18

L Brainard BOG X X

On balance sheet reduction: “We have a recovery today that is much stronger and faster than in the last cycle.

So I do believe it will be appropriate to commence that runoff in the next few meetings.” - Feb 18

On a March rate hike: “I support raising the federal funds rate at our next meeting in March and, if the economy

evolves as I expect, additional rate increases will be appropriate in the coming months…I, as all of my colleagues

will as well, will be watching the data closely to judge the appropriate size of an increase at the March

meeting…[whether 25bp or 50bp] is one [question] that we will address at the upcoming FOMC meeting.” – Feb

21

On rate hikes: ““Looking beyond this spring, my views on the appropriate pace of interest rate increases and

M Bowman BOG X X balance sheet reduction for this year and beyond will depend on how the economy evolves…my intent would be

to take forceful action to help reduce inflation, bringing it back toward our 2% goal, while keeping the economy on

track.” – Feb 21

On balance sheet reduction: “[Recent data] have only increased the urgency to get on with the process of

normalizing our interest rate stance and significantly reducing the size of the Federal Reserve’s balance

sheet…in the coming months, we need to take the next step, which is to begin reducing the Fed’s balance sheet

by ceasing the reinvestment of maturing securities already held in the portfolio.” – Feb 21

On rate hikes: “My preference is to increase the target range 100 basis points by the middle of this year.” – Feb

24

On a March rate hike: “One possibility is that the target range is raised 25 basis points at each of our next four

meetings…[but if inflation readings are above-expected] “a strong case can be made for a 50 basis-point hike in

March.” – Feb 24

C Waller BOG X X

On geopolitical risks: “Far too early [to assess impact of Ukraine-Russia conflict]… it is possible that the state

of the world will be different in the wake of the Ukraine attack, and that may mean that a more modest tightening

is appropriate, but that remains to be seen.” – Feb 24

On the terminal rate: “With the economy at full employment and inflation far above target, we should signal that

we are moving back to neutral at a fast pace.” – Feb 24

Vacant BOG X X Unoccupied, confirmation pending

Vacant BOG X X Unoccupied, confirmation pending

Vacant BOG X X Unoccupied, confirmation pending

8Voter

Member Role Monetary Policy Commentary Since January FOMC

‘22 ‘23

On a March rate hike: “Starting with 25 followed by further increases in coming months I think puts us in a good

position.” -Mar 3

On monetary policy: “We are going to be looking at the data and using the data to inform our outlook. If by the

middle of the year after we have taken those actions to move the funds rate up and to start removing

accommodation or the size of our balance sheet – if we don’t see inflation moving back down, that would be a

Clev.

L Mester X signal to me that we have to remove accommodation at a stronger pace, at a faster pace, because inflation isn’t

Fed

moving down as we expected.” -Mar 3

On geopolitical risks: [Ukraine-Russia conflict] “has implications for the economic outlook -- adding upside risk

to inflation even as it puts downside risk to the growth forecast.” – Mar 1

On the terminal rate: ““We are going to have to do what we need to do to get inflation under control. It could

very well be that interest rates will have to move up above that long-run level [2.5%]”. – Mar 3

On monetary policy: “More aggressive action on the balance sheet could allow for a shallower path for the

policy rate…alternatively, combining a relatively steep path of rate increases with relatively modest reductions in

the balance sheet could flatten the yield curve and distort incentives for private sector intermediation, especially

K.C. for community banks, or risk greater economic and financial fragility by prompting reach-for-yield behavior from

E George X

Fed long-duration investors.” – Jan 31

On balance sheet reduction: ““The potential costs associated with an excessively large balance sheet should

not be ignored…A large balance sheet has the potential to intertwine fiscal and monetary policy in the public’s

eyes and could unintentionally pose risks to the Fed’s independence and authority.” - Jan 31

On a March rate hike: “I wouldn’t want to prejudge the March meeting at this point. We have more data to come

in before March. Based on the data I have today, I’d like to see 100 basis points in the bag by July 1. The exact

timing of that I don’t think is as critical as the idea that we begin to move on removing accommodation soon…

There was a time when the committee would have reacted to something like this by just having a meeting right

now and doing 25 basis points right now.” – Feb 11

On rate hikes: “I was already more hawkish but I have pulled up dramatically what I think the committee should

do.” – Feb 11 “We need to front load more of our planned removal of accommodation than we would have

previously…” – Feb 14

On geopolitical risks: “The direct linkages to the U.S. economy are minimal so I wouldn’t expect that much

St.

impact directly on the U.S. economy…of course, we will have to watch this very carefully and see what happens

J Bullard Louis X

in days ahead.” - Feb 25

Fed

On the terminal rate: “If you wanted to put downward pressure on inflation, you’d actually have to get to neutral

[Bullard sees this at around 2%] – go beyond neutral…and I think that’s a major concern of mine -- we’re not

really in a position to do that right now, but we have to get in a position to do that”. – Feb 17

On balance sheet reduction: “I would also like to see the balance sheet runoff start in the second quarter. I’d

like to get that issue resolved at the committee. Hopefully we can get that implemented during the second

quarter….as a general principle, I see no reason why you can’t remove accommodation just as fast as you added

accommodation, especially in an environment where you have the highest inflation in 40 years…I would very

much like the committee to consider [asset sales in a second phase of balance sheet reduction] as a possibility,

so we can do that if we need to – because inflation is not decelerating as we had hoped.” – Feb 11

Bos. Susan M. Collins will assume the Boston Fed presidency on July 1. No monetary policy commentary

Vacant X

Fed from interim President Kenneth C. Montgomery, First VP And COO Of Boston Fed

On a March rate hike: “I would be supportive of a 25 basis-point increase in March. Could we do 50? Yeah.

Should we? Well, I’m a little less convinced of that right now…But we’ll see how the data turn out in the next

couple of weeks…if inflation stays where it is right now and continues to start to come down, I don’t see a 50

Phil basis-point increase. But if we see a spike, then I think we might have to act more aggressively.”

P Harker ** X

Fed – Feb 1

On rate hikes: “Right now, I think four 25 basis-point increases this year is appropriate but there’s a lot of risk

here…this is where we need to keep flexible with respect to policy. We can’t define a path right now and just stick

to it. We’ve got to look at the data.” – Feb 1

On a March rate hike: ““We haven’t raised interest rates yet but we have signaled that we’re likely to begin that

process soon. That would then not tap the brakes on the economy, but it would let our foot off the accelerator just

Minn.

N Kashkari X a little bit.” – Jan 28

Fed

On rate hikes: “If we raise rates really aggressively, we run the risk of slamming the brakes on the economy,

putting the economy in recession…My caution to my colleagues and myself is let’s not overdo it.” – Feb 16

Dall. Dallas Fed Pres Kaplan announced his resignation Sep 27. No monetary policy commentary from interim

Vacant X

Fed President Meredith Black, First VP And COO Of Dallas Fed

On a March rate hike: “"We're going to get going early at the next meeting, next several meetings, for sure.” –

Mar 2

On rate hikes: “If we were to do 25 basis points at each meeting, which may be more than I think is essential,

but if we did it at each meeting, we’ll end the year at 1.75% to 2%. That is close enough to neutral that we could

take quick action if it were necessary. Or we could stick or we could back off if that is what the case was.” – Mar

Chic.

C Evans X 4 “If inflation doesn’t come down, we can raise rates more quickly”. – Mar 2 "We'll probably get more rate

Fed

increases in succession than I previously thought [4 in 2022], then see if we're on our way for a much larger

number than four."

On the economic outlook: "The inflationary environment is more intense than I was expecting as of December.

The employment improvement has been better and smoother than last year.” – Mar 2

On balance sheet reduction: "We'll want to start reducing the size of our balance sheet. It's very large…if there

9Voter

Member Role Monetary Policy Commentary Since January FOMC

‘22 ‘23

are good arguments for adjusting the balance sheet sooner I will be listening intently.” – Mar 2

On a March rate hike: “The chairman gave some testimony yesterday that suggested that the time to lift rates

was coming soon.” – Mar 3

On monetary policy: “I see both the rate moves and the balance sheet announcements as just signaling that

the worst of the pandemic is behind us. The economy is growing strongly…I hope we can get back toward

prepandemic levels of rates relatively quickly. Because when we do, we will be ready to act in whatever way we

need to.” – Mar 3

Rich.

T Barkin On the terminal rate: “Let’s say you take rates up to 2.5% or 3% and we still have inflation at this kind of level.

Fed

Is there a risk you would have to restrain the economy to do that? And the answer is sure, that is always a risk.

We’ll have to see.” – Mar 3

On balance sheet reduction: “What happens to mortgages over time depends an awful lot on prepayments.

The pace of that, I think, we are going to have to see…we have said we want to be primarily Treasuries. If

natural market forces don’t take you there, I wouldn’t have a problem with choosing to sell them, but I think that’s

pretty far out”. – Mar 3

On a March rate hike: ““I am still in favor of a 25 basis point move at the March meeting.. One data point that I

am looking at in particular is month-to-month change in inflation. To the extent we start to see that trend down,

then I will be comfortable pretty much with a 25 basis point move. If that continues to persist at elevated levels, or

even moves in the other direction, then I am really going to have to look at a 50 basis point move for March.” –

Feb 28

Atl. On rate hikes: “We do not need to have our policy in maximally accommodative stance… If the data points us to

R Bostic

Fed needing to act more strongly [than 3 rate hikes in 2022], I will be comfortable with that”. – Mar 1 ““Historically,

over the last 10 years or so our moves have been in 25 basis point increments…I was hearing and getting a

sense that many expected that was the only type of move we could do. I actually think that is wrong. We need to

make sure people have different levels of move in mind, and awareness of those are possibilities… “Every

meeting is live for us…as data comes in, we will have to make judgments about what happens at every stage of

the way.” – Feb 28

On a March rate hike: "My own view is that March is the live meeting when we would raise interest rates for the

first time, and I could imagine raising at subsequent meetings as well, but I just want to see the data.” – MNI

Interview, Feb 10 “I don’t see anything right now that would disrupt our plans to move the rate up… absent any

significant negative surprises.” – Feb 23

On rate hikes: “Raising rates at least four times [in 2022], at least, would be my preference. But it most likely will

mean more than that unless of course we get the Ukraine and Russia situation pulling back demand.” – Feb 23

On monetary policy: “It is time to move away from the extraordinary support that the Fed has been providing

during the pandemic and bring monetary policy in line with the challenges of today… I’m committed to inflation to

S.F. be coming down and getting demand and supply in balance.” – Feb 23

M Daly

Fed On geopolitical risks: “I see the geopolitical situation, unless it would deteriorate substantially, as part of the

larger uncertainty that we face in the United States and our U.S. economy and we’ll have to navigate that as we

go forward.” – Feb 23

On balance sheet reduction: “"We know it's an important tool but it is a background tool…. fiddling with it in a

surgical way is not optimal when you're thinking about trying to achieve this soft landing with the economy…

we've committed to have the funds rate be our primary tool, have the balance sheet support full employment and

price stability, and have it be reduced in a predictable fashion so that once we've made the plans, we're not going

to be using it as some surgical adjustment tool. We have much less experience with the balance sheet."” – MNI

Interview, Feb 10

10Analyst Views – Fed Outlook

• All 27 analysts’ previews reviewed by MNI expect the FOMC to hike by 25bp at the March meeting.

• The general consensus for the Dot Plot is for 4-6 hikes to be signalled by the 2022 median, with a terminal

rate median in 2024 around 2.00-2.50%.

• On the upper end of Dot Plot expectations is UBS, which sees a 7-hike 2022 median, and an end-2024

median of 3.125%.

• Consensus is that the Summary of Economic Projections will show slower growth, particularly for 2022,

with a significant increase in both core and headline inflation projections this year. However, unemployment

forecasts are not expected to be greatly altered.

• Several expect the Fed to offer specifics on balance sheet reduction (including Credit Suisse,

Deutsche Bank and Morgan Stanley) at the March meeting, possibly via an addendum to the monetary

policy statement, but none expects QT to be formally announced or launched at the March meeting.

• Balance sheet reduction is expected by most to be announced in May or June, beginning in June or July.

• Some see the Fed starting with caps as low as $15B/month and gradually ramping up over several months,

while others see an initial pace as high as $40B, with a short phase-in (eg 2 months) afterward. Views on

the eventual “terminal” pace of runoff range from roughly $40B/month to $100B/month.

Analysts’ Key Comments

Note summaries in alphabetical order of institution.

ANZ: Market Terminal Rate Expectations Are Too Low

ANZ expects the Fed to hike 25bp at its March meeting, while updating details on plans for balance sheet

normalisation

• SEP/Dot Plot: Fed will need to make “significant upward revisions” to inflation forecasts for “credibility

purposes”. Median headline PCE in 2022 around 4.5%; core 2.7% “clear upside risks”; modest for 2023.

• GDP to be revised down on weaker disposable incomes.

• Dot plot to show 125-150bp in 2022 hikes. The number of dots at 3.0% or higher will rise; market’s

expectation of cycle topping out at 2.00% is too low.

• Press conference: Powell to allude to scope to hike 50bp at a meeting(s) if warranted.

Barclays: Potential For Reinvestment Policy Announcement

Amid “stagflationary pressures and uncertainty complicating policy”, Barclays sees the FOMC hiking by 25bp at the

March meeting, while signalling “additional (data-dependent) hikes over the medium term”.

• Barclays also expects the Fed to signal that QT will begin at upcoming meetings. With a runoff

announcement unlikely in March, however, Barclays expects the Fed to announce a reinvestment strategy:

rolling over MBS back into agency MBS, and rolling maturing Tsys over at auction.

• But could opt to reinvest MBS principal into T-bills to increase runoff pace once underway.

• SEP/Dot Plot: 5 2022 hikes, 4 in 2023 – so higher, despite likely GDP growth downgrade.

• Press conference: Powell to offer some guidance on runoff pace; as with the statement, to send the

message that normalization is coming despite the need to remain nimble amid higher uncertainty.

• Future action: 5 hikes in 2022 (Mar, May, Jun, Sep, Dec), 2 more in 2023 (ie lower than Fed dots).

• Formal QT announcement in May, beginning in June. Low initial caps, increased fairly quickly, with QT

terminal runoff rate of $80B/month ($50B Tsy / $30B MBS), risks of faster pace of $90-100B.

BNP Paribas: Sticking To Plan

BNP sees the Fed sticking to its plan to hike 25bp at the March meeting and signalling more increases to come,

with inflation remaining the “predominant concern”.

• Fed to frame tightening such that guaranteeing price stability is best way to preserve max employment.

• But Fed will mention it is ready to do more if needed, with an eye on inflation data and price expectations.

11• SEP/Dot Plot: 2022 growth downgraded slightly, inflation upgraded significantly; unemployment anchored.

• 5 2022 hike median (risk of 6) though distribution skewed to the upside. 4 in 2023, flat in 2024.

• Possible limited upward shift in 2024 median dot.

• Press conference: Powell to nuance his message in a less hawkish direction than his congressional

testimony, due to heightened Ukraine uncertainty. Powell to downplay significance of SEP.

• Could deliver additional colour on QT, with more info coming in the minutes.

• Future action: 6 25bp hikes in 2022, QT announced in June.

BofA: Better Late Than Never

BofA sees the Fed lifting off with a 25bp hike at the March meeting, while also providing specifics on unwinding the

balance sheet.

• Fed to release an addendum to their “principles” for balance sheet reduction alongside decision.

• Statement: Several changes, incl acknowledgments of drop in Covid cases, rising oil/commod prices, new

geopolitical risks.

• Fwd guidance to include that FOMC expects further gradual adjustments to normalize policy; “The timing

and size of future adjustments will depend on the Committee's assessment of realized and expected

economic conditions relative to its objectives of maximum employment and 2% inflation”

• SEP/Dot Plot: 5 2022 hike median; 4 in 2023; 1 in 2024 for 10 total hikes (to 2.50-2.75%).

• Growth and unemployment revised lower; inflation higher.

• Press conference: Powell to deliver a hawkish message: “will likely reiterate that the Fed needs to get

serious about price stability, though we think he will flag risks to the outlook from the Russia/Ukraine

conflict and higher commodity prices.”

• Future action: 7 hikes in 2022, 4 more in 2023 (to 2.75-3.00%).

• QT to start In May. 3-month ramp up, $100B total caps ($60B Tsy, $40B MBS, no cap on bills).

• Deteriorating UST liquidity conditions increase risk of shift in reinvestment strategy from MBS to USTs,

potentially announced this week.

CIBC: Statement Will Have To Sound “Very Hawkish”

CIBC sees the Fed delivering a 25bp hike at the March meeting. The Russian invasion of Ukraine has not changed

the rate needed to moderate the economy enough to bring inflation “down to earth, while not sending the economy

into recession in the process”.

• Statement: “Will have to sound very hawkish, since [the Fed] needs to justify [a 25bp] move and warn of a

lot more to come.”

Commerzbank: Short-Term War Inflation Impact Trumps Uncertainties

Commerzbank expects a 25bp hike at the March FOMC meeting, saying that while the Russia-Ukraine war has

significantly increased uncertainty/growth prospects, “from the Fed's perspective, the short-term additional

inflationary impulse probably dominates.”

• SEP/Dot Plot: Inflation forecasts to be raised; 2022 “likely” to be “well above 5%”, with core above 4%.

• Future action: 150bp of hikes in 2022; another 75bp by end-Q2 2023.

Credit Suisse: No Broader Hawkish Surprises

With geopolitical tensions and recent tightening of financial conditions, Credit Suisse sees the FOMC opting for a

25bp rather than 50bp hike at the March meeting. CS doesn’t expect “any broader hawkish surprises”.

• “Likely” the Fed releases a policy plan for balance sheet runoff along with the policy statement.

• Statement: To acknowledge the recent strong readings in inflation and possible further acceleration due to

energy prices; will likely add that geopolitical developments add uncertainty to the economic outlook and

the Fed will closely monitor global and financial market developments.

• SEP/Dot Plot: Median Dot to show 6 hikes in 2022, 4 in 2023 (to 2.625%), 1 in 2024 (to 2.875%).

• Higher inflation and lower GDP estimates for 2022.

• Press conference: Powell to provide more details on balance sheet plans. Likely to reiterate rhetoric from

his congressional testimony re being cautious about overtightening / nimble about policy responses.

• Future action: Balance sheet runoff to start in July, at initial $20B ($12B Tsy, $8B MBS) monthly pace.

12Danske: 200bp Hikes In 2022

Danske sees the FOMC hiking by 25bp at the March meeting, having previously expected 50bp (“but the

uncertainty from the war in Ukraine will make the Fed a tad more cautious in our view”.

• Future action: 200bp of hikes total in 2022.

Deutsche: Rates To Rise “At Least At A Measured Pace”

Deutsche sees the Fed hiking by 25bp at March’s meeting, signalling 6 25bp increases for 2022 in the dot plot, and

providing significant guidance on balance sheet shrinkage.

• Statement: Several changes reflecting QE ending and rate liftoff; accompanied by an addendum outlining

the QT plan but stopping short of announcing the start of QT.

• The language on financial conditions to note "have tightened due to the invasion of Ukraine”, while the

risks portion will include "Risks to the economic outlook remain, including from new variants of the virus as

well as geopolitical events."

• Key to the statement will be the usage of the following language, which will tie the pace of tightening to

inflation progress without the Fed locking itself into a set pace of 25bp hikes, Deutsche says, expecting:

"With inflation well above 2 percent and a strong labor market, the Committee expects it will be appropriate

to raise the target range for the federal funds rate at least at a measured pace. In determining the timing

and size of future adjustments to the target range for the federal funds rate, the Committee will assess

realized and expected progress toward its objective of 2% inflation."

• The Fed will also announce runoff caps, with Deutsche pointing to Powell’s congressional testimony and

Brainard’s prior comments on runoff. This would likely be accompanied by “a data-dependent signal that

QT is likely to be announced in the coming meetings”.

• SEP/Dot Plot: Median 2022 dot at 1.625% (6 hikes, with risk of 5 hikes); 2023 another 3-4 hikes to 2.5%.

• Core 2022 PCE up to 3.6% (2.7% prior), 2023 2.5% (vs 2.3%), 2024 unch at 2.1%. Unemp revised slightly

lower, GDP much lower for 2022 (3.0% vs 4.0% prior), 2023-2024 down 0.1pp each.

• Press conference: On Ukraine impact on monetary policy, Powell to reiterate that effects remain “highly

uncertain”, perhaps note tighter financial conditions, impact on consumer spending. To express risk of

higher commodity prices upwardly pressuring inflation expectations.

• Could note that Ukraine uncertainty argued for a “careful” first hike (ie 25bp and not 50bp) but that the Fed

stands ready to move by larger increments (Deutsche sees significant risks of this at coming meetings).

• Powell likely reiterate a “series” of hikes and a need to return policy to neutral/restrictive by 2023. Could

downplay dot plot due to geopolitical uncertainty.

• Future action: Fed to hike by 175bp in 2022 with hikes at each meeting; 3 hikes in 2023 to 2.50-2.75%.

• QT announced in May, commencing in June; Initial caps set at $20B Tsy / $15B MBS, rising by those

amounts over 2-month periods, to $60B/$45B max caps by October. Bills ($325B total) to mature without

being subject to the cap structure. Grand total of $1.9T runoff by end-2023.

Goldman Sachs: Looking Beyond Liftoff

With the FOMC’s liftoff set to be of a 25bp magnitude, Goldman Sachs says March’s meeting “will be watched

mostly for clues about the pace of tightening after March in the statement, the dot plot, and the Chair’s comments

about the war.”

• Goldman doesn’t expect the war in Ukraine to knock the Fed off a 25bp per meeting tightening path,

though “we suspect that the FOMC will be reluctant to consider a 50bp hike until downside risks to the

global economy from the war diminish.”

• Statement: “likely to avoid appearing to commit to a specific pace of tightening”. Could adapt Powell’s

recent comment, “We will use our policy tools as appropriate to prevent higher inflation from becoming

entrenched while promoting a sustainable expansion and a strong labor market.”

• SEP/Dot Plot: 2022 median Dot to show 6 hikes, but risks tilted to the downside, “especially if FOMC

participants view balance sheet reduction as equivalent to multiple rate hikes”. 4 more hikes in 2023, zero

in 2024; terminal rate 2.5-2.75%.

• 9 participants to show terminal rate above neutral (up from 5 in Dec).

• 2022 GDP downgrade “quite large”; core PCE up to 3.7%, 2023 to 2.4%.

• Future action: 7 25bp hikes in 2022, 4 quarterly hikes in 2023 for a terminal rate of 2.75-3.00%. “With

inflation likely to remain uncomfortably high all year, the FOMC will probably only pause if it thinks further

13tightening risks pushing the economy into recession.” If Ukraine downside risks recede, 50bp options likely

back on the table.

• FOMC to finalize and publish its QT plan at the May meeting; announcement of start in June.

• $100B peak monthly pace ($60B Tsy / $40B MBS) with “at most a brief ramp-up period”; shrinking B/S

from just under $9T to just over $6T by 2025. Could allow uncapped MBS runoff though that would have

almost no impact on runoff relative to $40B cap; compromise on FOMC to those advocating MBS sales.

ING: 6 Hikes The Base Case For 2022

ING sees a 25bp hike at the March FOMC, which will be undeterred by uncertainty/volatility caused by Russia’s

invasion of Ukraine.

• Fed could “under hike” on the reverse repo rate (20bp rather than 25bp).

• SEP/Dot Plot: 2022 GDP revised down to around 3%; inflation forecasts “inevitably raised” (3.5% core, but

down to 2.0% in 2023); no major changes to unemployment projections.

• 5 2022 hikes median in Dot Plot; 3 more in 2023; 2 more in 2024.

• Future action: 6 25bp hikes this year, 2 more in 2023. Balance sheet shrinkage to begin late Q2.

JPMorgan: Straightforward Case For 25bp Hike

JPMorgan sees “straightforward” case for a 25bp hike at the March meeting, with the FOMC pointing to 6 2022

hikes in the Dot Plot.

• Statement: Likely to add a reference to geopolitical risks; inflation discussion broadened to include

pressures from energy/commodity prices and resource utilization.

• Previous 2 statements dropped fwd guidance; “perhaps Powell thinks the dots are good enough” but if they

want to convey a consensus view on the rate path then “would make sense to insert something about

expecting further increases”.

• Some arguments for adjusting ON/RRP rate by less than 25bp, but “simpler to communicate a parallel

adjustment … technical adjustments can be made later if needed”.

• SEP/Dot Plot: Median 2022 Dot “could” show 6 hikes (though at least a few Dots with 7); 2023 and 2024

to show 3 and 2, respectively. Though “there may be some reluctance to show a tight policy setting”.

• Headline/core PCE looking “much too low” in SEP (new headline could be>4%).

• GDP for 2022 likely to come down; unemp projection is “less off-base”, but “will be interesting to see if

there is an upward drift in estimates of the natural rate of unemployment”.

• Press conference: “The natural venue” for more details on QT incl the size of monthly runoff caps/phase-

in period/conditions that will warrant QT beginning. Though signals of progress on QT could be in

addendum to the Statement.

Lloyds: Outlook Beyond March Has Become Cloudier

While “the Ukrainian crisis has undoubtedly raised the level of uncertainty” for the economy and policy, Lloyds

expects the Fed to hike by 25bp at the March FOMC, “but what happens after that has become cloudier”.

• Fed may provide further detail on QT in the March statement.

• Dot plot to show 125bp of hikes (5 25bp moves) in 2022, with further rises in 2023-24.

• Future action: 125bp of hikes in 2022. “The possibility that rates will not be raised again in 2022 after

March cannot be ruled out.” QT to begin in H2 2022; Fed will want to have hiked at least 2-3 times prior.

Morgan Stanley: Proceeding With Care

Morgan Stanley says the FOMC will hike by 25bp at the March meeting, while both the Statement and Press

Conference ‘will avoid defining the pace or magnitude of tightening following the March hike. The Fed favors

flexibility, even more so amid new risks, and so deliberate vagueness serves it well.”

• Fed to provide “formal guidance” on monthly runoff caps: $50B Tsy / $30B MBS.

• SEP/Dot Plot: 150bp in Dot Plot hikes in 2022, 100bp more in 2023; “a good number” of dots showing

further tightening above neutral in 2024.

• Core 2022 PCE inflation median 3.9% (vs 2.7% prior); 2023 marked up 0.1pp and 2024 unchanged. 2022

headline PCE to 4.2% vs 2.6% prior.

• Unemp rate forecast marked down for 2022 (3.4% vs 3.5% previously), to 3.3% in 2023-24.

• Real GDP revised down for 2022, modest in 2023-24.

14• Press conference: Powell may stress that the magnitude of the 25bp March hike should not be taken as a

signal of the size of future adjustments.

• Future action: 150bp in hikes in 2022, another 100bp in 2023 (to 2.625%).

• QT announced at May meeting (to begin mid-May). 2-month phase-in.

NatWest: Liftoff, With Uncertainty

NatWest sees the FOMC hiking by 25bp at the March meeting, with Powell reiterating expectations for a “series” of

rate increases this year. They also “suspect” we could get an addendum on QT plans.

• Statement: To drop language re “variants of the virus” as a risk to the outlook, but could add something on

uncertainty about Ukraine.

• On forward rate guidance, “The Committee expects that economic conditions will evolve in a manner that

will warrant a series of increases in the federal funds rate this year.”

• On QT, to add a line to suggest will commence “soon” (a nod to May).

• Bullard to dissent in favor of 50bp hike.

• SEP/Dot Plot: 2022 Dot to rise to 1.375% (5 hikes), with most dots clustered around 4 or 5; nearly all

(Kashkari an exception) to see at least 3 hikes.

• For 2023, all officials to see between 50-75bp of hikes, with the median showing 2, one less than in Dec’s

Dot Plot and reflecting the faster 2022 hiking pace. So, median 1.875% (7 cumulative hikes).

• For 2024, one hike, with median ending at 2.125% (same as in Dec’s Dot Plot).

• 2022 median core PCE at least 3.3% (from 2.7% prior) and 2.4% in 2023 (from 2.2%), 2024 unch at 2.1%.

• GDP lower in 2022-23; unemployment not meaningfully revised.

• Press conference: Powell likely to re-emphasize that policy will continue to be driven by data; base case

is "a series of raises expected for this year", while acknowledging uncertainty due to Ukraine/Russia war.

• Powell could suggest balance sheet run-off could happen as early as Q2.

• Future action: 5 hikes in 2022 (Mar, May, Jun, Sep, Dec), 4 in 2023. QT to begin in Q2.

Nordea: 25bp Hike, But Then What?

Nordea’s assumption is that the Fed will hike at every meeting starting in March, “until it sees convincing signs that

inflation pressures are abating. If the inflation outlooks becomes even more challenging, it may hike by 50bp, and if

financing conditions are tightening faster than the Fed would like, the central bank could pause.”

• Too early for Powell to give more info on balance sheet reduction.

• SEP/Dot Plot: Dots “sure to migrate considerably higher” with the range of expectations widening.

• Future action: 25bp hikes more likely than 50bp; risks tilted toward a longer Fed hiking cycle than is

currently being priced in. Decision on QT in the summer.

RBC: Inflation Pressures Trimph Over Geopolitical Headwinds

The FOMC will hike at the March meeting, writes RBC, “as very low unemployment and firming inflation pressures

offset increased geopolitical headwinds tied to the Russian invasion of Ukraine.”

• Future action: 5 25bp hikes in 2022 (to 1.25-1.50%).

Scotiabank: A Partially Set Table

Scotiabank says that while the “script has already been written” for the March FOMC (incl 25bp hike), it could prove

impactful “and with a probable hawkish slant”.

• To further discuss but not finalize balance sheet plans, won’t have a decision ready this week.

• The Fed tentatively believes it has the infrastructure in place to manage shock risks related to Ukraine-

Russia war, incl repo facilities.

• SEP/Dot Plot: Expectations is that maybe a couple of dots are added to 2022, “but the risk could very well

slant toward both higher and earlier than previously anticipated.”

• Press conference: Powell could guide direction of risks on pace/level of hikes over time, and color on

FOMC discussions on QT.

SEB: Hiking Cycle Begins Amid 1970s Stagflationary Challenges

SEB sees a 25bp hike at the March meeting, with the FOMC evaluating policy on a meeting-by-meeting basis.

• Too early for specific QT timing to be announced.

15You can also read