JPMorgan Equity Income Managed Account

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

4Q 2022 JPMorgan Equity Income Managed Account

Table of contents

Capabilities

Equity Income

● Expertise

● Portfolio

● Results

Appendix

2Capabilities 3

Equities assets under management

As of December 31, 2022, J.P. Morgan Asset Management’s Equity teams manage USD 678 billion

Equities U.S. Equity

USD 678bn total assets under management USD 439bn total assets under management

USD 112bn

16% $103bn $99bn

23% 23%

USD 127bn

19%

USD 439bn

65% $86bn

20%

$147bn

$4bn 32%

U.S. Equity 1%

Emerging Markets & Asia Pacific Equity Core Value Security Capital Structured Growth

International Equity Group

Source: J.P. Morgan Asset Management. Data includes internal Fund of Funds and joint ventures.

4Expertise 5

An experienced team dedicated to value

The team also leverages the insights of the J.P. Morgan Equity organization, which includes over 20 research analysts

in the U.S. and over 200 analysts globally

Lee Spelman Don San Jose

Managing Director Managing Director

Head of U.S. Equity CIO Value Team

Experience: 47/34 Experience: 26/23

Equity Income Team

Clare Hart Andrew Brandon David Silberman

Managing Director Managing Director Managing Director

Portfolio Manager Co-Portfolio Manager Co-Portfolio Manager

Experience: 30/23 Experience: 25/23 Experience: 34/34

Lerone Vincent Tony Lee

Managing Director Vice President

Research Analyst Research Analyst

Experience: 25/25 Experience: 11/11

Investment Specialist Team

Jaime Steinhardt Jenna Silver Rory Houser

Executive Director Vice President Associate

Experience: 13/13 Experience: 11/11 Experience: 8/8

As of December 2022.

6A team of skilled research analysts with an average of 21 years of experience

David Small Danielle Hines

Managing Director Executive Director

Director of U.S. Research Associate Director of U.S. Research

Experience: 22 / 17 Experience: 14 / 14

Consumer Healthcare

Bartjan

Lisa S. Sadioglu Greg Fowlkes Ryan Vineyard van Hulten Li Boynton

Managing Director Managing Director Managing Director Executive Director Vice President

Consumer Cyclicals Retail Consumer Staples Pharma / Biotech Pharma / Biotech

Experience: 22 / 22 Experience: 23 / 17 Experience: 17 / 10 Experience: 27 / 4 Experience: 9 / 5

Financials REITs

Steven Wharton Brent Gdula David Chan Jason Ko Nick Turchetta

Managing Director Executive Director Executive Director Executive Director Vice President

Banks & Insurance Payments / REITs REITs

Capital Markets Experience: 14 / 14 Business Services Experience: 20 / 20 Experience: 12 / 2

Experience: 27 / 16 Experience: 15 / 4

Telecom, Media & Technology

Nitin

Robert Bowman Eric Cheung Kris Erickson Ryan Vineyard

Bhambhani

Managing Director Managing Director Executive Director Managing Director Managing Director

Semis & Hardware Software and Svcs Software and Svcs Media Telecom & Cable

Experience: 30 / 30 Experience: 29 / 26 Experience: 18 / 1 Experience: 21 / 9 Experience: 17 / 10

Industrials

David

Maccarrone Aga Zmigrodzka Teresa Kim Chris Ceraso Joanna Shatney Andrew Brill

Managing Director Vice President Managing Director Executive Director Executive Director Vice President

Energy/Infrastructure Energy/Infrastructure Utilities Autos and Transport Industrial Cyclicals Industrial Cyclicals

Experience: 28 / 13 Experience: 13 / 2 Experience: 24 / 1 Experience: 22 / 9 Experience: 27 / 8 Experience: 20 / 6

Research Analysts Include VP’s and above. As of December 2022. Years of experience: Industry / Firm.

7Portfolio 8

Investment philosophy

“Our bottom-up fundamental philosophy targets high quality U.S. companies

with attractive valuations and healthy dividend yields.”

1. Quality 2. Valuation 3. Dividend

We focus on quality first: Valuation is critical: Dividend yields:

● Companies with durable franchises ● Quantitative and qualitative judgements ● Enhance total return

● Consistent earnings ● Potential vs. current market value ● Generate income

● Strong management teams ● Modest payout ratio indicates a

disciplined use of capital

Our approach leads to a portfolio that has historically

shown less volatility than the market with less exposure to the downside

For illustrative purposes only. The manager seeks to achieve the stated objectives. There can be no guarantee the objectives will be met. See glossary of investment terms.

9Bottom-up fundamental philosophy

Targeting high quality U.S. companies with attractive valuations and healthy dividend yields

Idea Fundamental Valuation Portfolio

generation analysis analysis construction

Narrow the investment Assess the quality of Valuation is critical to Constructed from the

universe via the company by entry & exit points bottom-up

● Analyst research analyzing ● Metrics are tailored to ● Portfolio of 85-110 names with a

● Business factors each stock: maximum stock weighting of 5%

● Company meetings

at time of initiation

– Low cyclicality – Free cash flow yield

● Industry conferences

● Minimum 2% dividend yield at

– High barriers to entry – P/E1

time of initiation

– Brand leadership – EV/EBITDA2

● Industry group constraints of

and strength benchmark weight +/-10%

Management factors ● Position sizes are

– Disciplined use of determined by:

capital – Strength of conviction

Financial factors – Risk / reward opportunity

Sell discipline:

– Sustainable cash flow – Portfolio considerations

● Overvaluation by the market

– Strong balance sheet of diversification

● Displacement by a better idea

– Steady pattern of ● Company fundamentals have

earnings changed

For illustrative purposes only. The manager seeks to achieve the stated objectives. There can be no guarantee the objectives will be met.

1 Price/Earnings 2 Enterprise value/Earnings before interest, taxes, depreciation, and amortization. See glossary of investment terms.

10Equity Income has top decile performance coupled with bottom decile volatility

JPMorgan Equity Income Strategy as of December 31, 2022

Standard deviation since inception* Batting average since inception***

Lower volatility:

8th percentile standard deviation 60% Alpha consistency:

15.5% 15.4% 1st percentile batting average

13.3%

52%

JPMorgan Equity Income eVestment LCV Median Russell 1000 Value Index

Strategy J.P. Morgan Equity Income Strategy eVestment LCV Median

Down capture potential since inception** Performance

96% Better Performance Equity Income Russell 1000 Value Index

Attractive potential downside protection 9th percentile returns

11th percentile downside capture 10.8%

8.6%

81%

-5.6% -6.6%

-7.7%

-11.3%

J.P. Morgan Equity Income Strategy eVestment LCV Median Down Quarter Down Year Since Inception

Source: J.P. Morgan Asset Management, eVestment. *Inception: 11/30/2002. Supplemental to standardized performance. Past performance is no guarantee of future results.

Risk is measured by standard deviation – a gauge of the variance of a manager's return over its average or mean. ** Down capture measures performance of the manager relative to the index in down markets. ***

Consistency is measured by batting average – calculated by dividing the number of months in which the manager beats or matches the index by the total number of months in the period.

Sourced from eVestment Alliance as of 12/31/2022. Statistics are computed using monthly data. The eVestment ranking is a percentile ranking based on the strategy’s annualized return (gross of fees). Equity Income

was ranked against the following number of institutional products in the eVestment Large Cap Value, for the since inception excess return (9th percentile / 189 observations); Standard Deviation (8th percentile / 189

observations), and information ratio (5th percentile / 189 observation ).

Ranking are calculated based on total returns. See glossary of investment terms.

11Sector positions

JPMorgan Equity Income Portfolio as of December 31, 2022 Benchmark Russell 1000 Value Index

Absolute sector & relative weightings (%)

25

20.4

20 19.0

15 14.0

9.6

10 9.2

8.0

6.9

4.7

5 3.7

2.4 2.1

0

Financials Health Care Industrials Consumer Energy Information Consumer Utilities Materials Communication Real

Staples Technology Discretionary Services Estate

Relative

0.3 1.7 3.4 2.2 0.8 -0.3 0.9 -1.1 -0.6 -4.9 -2.3

Positioning (%)1

Source: J.P. Morgan Asset Management, Frank Russell Company, Wilshire Atlas (excludes cash). For illustrative purposes only. 1Reflects relative position to the benchmark Russell 1000 Value Index. The

Portfolio is an actively managed. Holdings, sector weights, allocations and leverage, as applicable are subject to change at the discretion of the Investment Manager without notice. See glossary of investment

terms.

12Financials: Opportunities to add value in different rate environments

JPMorgan Equity Income Portfolio as of December 31, 2022

1.3%

1.3% 4.6% Diversified Banks

Insurance

20.4% 1.8% Investment Banking & Brokerage

Asset Management & Custody Banks

Regional Banks

Current

Consumer Finance

Financials Weight 1.9%

Financial Exchanges & Data

4.0%

Portfolio diversification Insurance Brokers

across sub-sector

2.7%

2.8%

Source: J.P. Morgan Asset Management, Wilshire Atlas (excludes cash). See glossary of investment terms.

13Stock positioning

JPMorgan Equity Income Portfolio as of December 31, 2022

Portfolio Dividend Portfolio Benchmark Relative

Top 10 holdings Top 5 overweights

Weight (%) Yield (%) weight (%) weight (%) position (%)1

Exxon Mobil 3.10 3.30 UnitedHealth 2.72 0.24 2.48

ConocoPhillips 3.08 1.73 ConocoPhillips 3.08 0.80 2.28

UnitedHealth 2.72 1.24 AbbVie 1.92 0.00 1.92

Air Products & Chemicals 2.21 0.37 1.83

Bristol-Myers Squibb 2.61 3.17

Bristol-Myers Squibb 2.61 0.84 1.78

Raytheon Technologies 2.58 2.18

Air Products & Chemicals 2.21 2.10 Portfolio Benchmark Relative

Top 5 underweights

weight (%) weight (%) position (%)1

Johnson & Johnson 2.06 2.56

Berkshire Hathaway 0.00 3.04 -3.04

Philip Morris 1.98 5.02 JPMorgan Chase & Co2 0.00 2.13 -2.13

General Dynamics 1.97 2.03 Meta 0.00 1.16 -1.16

AbbVie 1.92 3.66 Cisco Systems 0.00 1.07 -1.07

Total 24.23 Thermo Fisher Scientific 0.00 1.03 -1.03

1Reflectsrelative position to the Russell 1000 Value Index. 2Due to regulatory reasons, the portfolio is unable to hold JPMorgan Chase & Co.

Source: J.P. Morgan Asset Management, Frank Russell Company, Wilshire Atlas (excludes cash). Holdings and allocations are subject to change at the discretion of the Investment Manager

without notice. The inclusion of the securities mentioned above is not to be interpreted as recommendations to buy or sell. For illustrative purposes only. See glossary of investment terms.

14Portfolio characteristics

JPMorgan Equity Income Portfolio as of December 31, 2022 Benchmark Russell 1000 Value Index

Portfolio Portfolio Benchmark

BARRA tilts relative to benchmark

P/E Ratio1 14.7x 14.6x Size 0.26

Profitability 0.23

EPS Growth2 11.8% 9.4% Dividend Yield 0.20

Earnings Quality 0.13

Average Market Cap3 $176.7 B $151.4 B Momentum 0.13

Growth 0.00

Number of Holdings 85 840

Leverage -0.02

Current Dividend Yield 2.7% 2.3% Earnings Yield -0.03

Beta -0.18

Dividend Growth4 14.2% 11.0% Value -0.23

Active Share 64.3% N/A

ROE4 23.8% 17.1% Market capitalization weightings3

ROIC4 13.2% 10.8%

Portfolio Benchmark

94%

5

Standard Deviation 17.3% 18.9% 78%

Turnover5,6 17.1% N/A

Tracking Error5 2.82 N/A 13%

5% 1% 7% 2%

0%

5

Beta 0.91 1.00

> $25 B $10 B - $25 B $5 B - $ 10 B < $5 B

Source: J.P. Morgan Asset Management, Frank Russell Company, Bloomberg, BARRA, Wilshire Atlas (excludes cash). The above characteristics are shown for illustrative purposes only, and are subject to

change without notice. Representative the current portfolio holdings. However, it cannot be assumed that these types of investments will be available to or will be selected by the portfolio in the future.

1First Call 12 month forward estimate. 2First Call Growth 1-5 year forward estimate. 3USD. 4Trailing 12 months. 5Trailing 5 years (Annualized). 6As of 11/30/2022. See glossary of investment terms.

15Portfolio activity: 4Q 2022

JPMorgan Equity Income Portfolio as of December 31, 2022

Top buys1 Top sells1

US Bancorp PNC Financial Services

Dominion Energy ConocoPhillips

Lam Research* UnitedHealth

United Parcel Service AmerisourceBergen

AbbVie Citigroup

Source: J.P. Morgan Asset Management

1 Based on change in position size

*Was either initiated or eliminated during the quarter.

Holdings and allocations are subject to change at the discretion of the Investment Manager without notice. The companies/securities above are shown for illustrative purposes only. Their inclusion should not be

interpreted as a recommendation to buy or sell. The Portfolio is actively managed. Holdings, sector weights, allocations and leverage, as applicable are subject to change at the discretion of the Investment Manager

without notice. See glossary of investment terms.

16Results 17

Performance

JPMorgan Equity Income SMA Composite as of December 31, 2022

Market value As of 12/2022

Equity Income Strategy $77,716 mm

Since

Annualized performance (%) 4Q 2022 1 year 3 years 5 years 10 years Inception

(11/30/2002)

Equity Income SMA Composite (Gross) 13.03 -1.23 9.13 9.69 12.54 10.83

Equity Income SMA Composite

12.17 -4.19 5.86 6.39 9.17 7.51

(Net of max. allowable fees – 300bps)*

Russell 1000 Value Index 12.42 -7.53 5.96 6.67 10.29 8.55

Excess Returns (Gross) 0.61 6.30 3.17 3.02 2.25 2.28

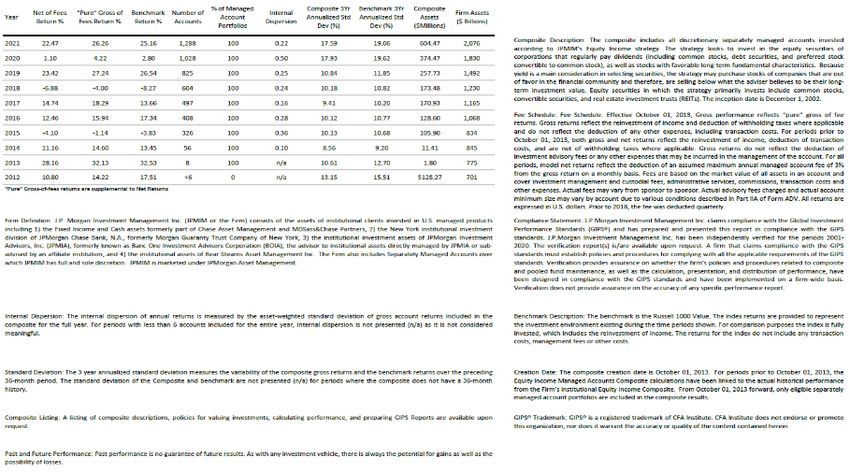

Calendar year performance (%) 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Equity Income SMA Composite (Gross) 19.31 9.08 14.22 32.13 14.60 -1.14 15.94 18.29 -4.00 27.24 4.20 26.25 -1.23

Equity Income SMA Composite

15.91 5.90 10.94 28.47 11.31 -4.08 12.62 14.93 -6.88 23.42 1.10 22.46 -4.19

(Net of max. allowable fees – 300bps)*

Russell 1000 Value Index 15.51 0.39 17.51 32.53 13.45 -3.83 17.34 13.66 -8.27 26.54 2.80 25.16 -7.53

Excess Returns (Gross) 3.80 8.69 -3.29 -0.40 1.15 2.69 -1.40 4.63 4.27 0.70 1.40 1.09 6.30

The performance quoted is past performance and is not a guarantee of future results. Performance includes the reinvestment of income.

Source: J.P. Morgan Asset Management. Please see disclosure page for index definitions. *Please note, actual fees associated with this strategy may be lower. 1Preliminary

Please note, the “net of fee” composite performance returns is calculated using a model investment management fee. It is based on a representative fee applicable to institutional clients looking to invest in the strategy

and it is higher or equal to the weighted average investment management fee of the underlying accounts within the composite at year end. Actual fees may be lower based on assets under management and other

factors. Where fees are lower, “net of fees” performance returns will be higher. As such, “net of fees” performance for actual accounts may differ significantly from the “net of fees” performance shown above. Fees are

described in Part II of the Advisor’s ADV which is available upon request. Please see back page for additional disclosure. The Russell 1000 Value Index is an unmanaged index measuring the performance of those

Russell 1000 companies with lower price- to-book ratios and lower forecasted growth values. The returns are total returns and include the reinvestment of dividends. An individual cannot invest directly in an index.

The index is unmanaged. Please see glossary of investment terms.

18Performance attribution – 4Q 2022

Benchmark Russell 1000 Value Index

JPMorgan Equity Income Portfolio as of December 31, 2022

Stock: -0.13% | Sector: 1.21%

Ending Stock Impact Ending Stock Impact

Top contributors Top detractors

weight (%) return (%) (%) weight (%) return (%) (%)

Air Products & Chemicals 2.21 33.15 0.52 JPMorgan Chase & Co* 0.00 29.49 -0.54

TJX Companies 1.64 28.68 0.42 Berkshire Hathaway* 0.00 15.68 -0.46

ConocoPhillips 3.08 16.44 0.40 Cisco Systems* 0.00 20.18 -0.20

Raytheon Technologies 2.58 24.00 0.39 Gilead Sciences* 0.00 40.31 -0.19

AbbVie 1.92 21.60 0.37 Boeing* 0.00 57.33 -0.16

Note: Stock attribution reflects net contribution vs. benchmark. Stock return displayed for whole period.

Sector attribution (%)

Stock Selection Sector Allocation

0.6%

0.3% 0.3% 0.3% 0.2% 0.2% 0.2%

0.1% 0.1%

0.0% 0.1% 0.1% 0.0%

0.0% 0.0% 0.0% 0.0%

-0.1% -0.1% -0.1%

-0.5% -0.5%

Communication Information Consumer Consumer Real Estate Materials Industrials Energy Utilities Financials Health Care

Services Technology Discretionary Staples

Past performance is no guarantee of future results. Source: J.P. Morgan Asset Management, Frank Russell Company, Wilshire Atlas (excludes cash). The securities highlighted above

have been selected based on their significance and are shown for illustrative purposes only. They are not recommendations. The portfolio is an actively managed. Holdings, sector weights,

allocations and leverage, as applicable are subject to change at the discretion of the Investment Manager without notice. *Underweight relative to benchmark. Due to regulatory reasons, the

portfolio is unable to hold JPMorgan Chase & Co. Gross of fees. See glossary of investment terms.

19Performance attribution – 2022

Benchmark Russell 1000 Value Index

JPMorgan Equity Income Portfolio as of December 31, 2022

Stock: 3.84% | Sector: 2.42%

Average Stock Impact Average Stock Impact

Top contributors Top detractors

weight (%) return (%) (%) weight (%) return (%) (%)

ConocoPhillips 2.98 71.45 1.23 Home Depot 1.42 -21.98 -0.44

EOG Resources 1.87 56.89 0.72 Microsoft 1.22 -28.02 -0.42

Walt Disney* 0.00 -43.91 0.56 PPG Industries 1.41 -25.69 -0.39

Intel* 0.03 -46.65 0.45 Dover 1.45 -24.35 -0.39

Meta Platforms* 0.00 -64.22 0.45 Seagate Technology 0.56 -51.41 -0.38

Note: Stock attribution reflects net contribution vs. benchmark. Stock return displayed for whole period.

Sector attribution (%)

1.3% 1.3% 1.4% Stock Selection Sector Allocation

1.2%

0.6% 0.5% 0.5%

0.2% 0.3% 0.2% 0.2%

0.1% 0.0%

0.0% -0.1% 0.0% 0.0% -0.1% 0.0%

-0.2% -0.3%

-0.6%

Information Health Care Industrials Communication Energy Consumer Consumer Real Estate Materials Utilities Financials

Technology Services Staples Discretionary

Past performance is no guarantee of future results. Source: J.P. Morgan Asset Management, Frank Russell Company, Wilshire Atlas (excludes cash). The securities highlighted above

have been selected based on their significance and are shown for illustrative purposes only. They are not recommendations. The portfolio is an actively managed. Holdings, sector weights,

allocations and leverage, as applicable are subject to change at the discretion of the Investment Manager without notice. *Underweight relative to benchmark. Due to regulatory reasons, the

portfolio is unable to hold JPMorgan Chase & Co. Gross of fees. See glossary of investment terms.

20Executive summary

JPMorgan Equity Income Strategy as of December 31, 2022

Expertise Portfolio Results

Experienced team coupled with Bottom-up stock selection Our investment approach has

proprietary insights from our targeting high quality U.S. delivered strong and consistent

seasoned research group companies at attractive valuations risk-adjusted returns over time

● Experienced investment team with lead ● Targets quality companies with ● Has generated top decile performance

PM Clare Hart managing the Strategy consistent earnings, strong and bottom decile volatility since lead

since inception.* management teams and a dividend portfolio manager change*

yield of 2% or more

● Supported by two co-PMs and two ● Attractive combination of performance

dedicated analysts ● Fundamental bottom-up approach and less exposure to the downside

to stock selection that is not

● Leveraging the fundamental insights of ● Dividend yield enhances the portfolio’s

benchmark driven

a team of over 20 U.S. Equity career total return

analysts averaging over 20 years of ● Fully invested with cashAppendix 22

Dividends have been an important contributor to total returns over time

As of December 31, 2022

Total Return Decomposition – Ibbotson Associates SBBI U.S. Large Company Stocks Index

25%

Dividends Capital Appreciation

20%

15%

13.9% 13.6%

10% 12.6% 15.3%

3.0% 11.6%

6.1%

5% 4.4% 1.6% 5.9%

4.7% 5.4% 6.0% 5.1%

3.3% 4.2% 4.4% 3.8%

2.5% 1.8% 2.1% 1.7%

0%

-2.7%

-5.3%

-5%

-10%

1927-1929 1930s 1940s 1950s 1960s 1970s 1980s 1990s 2000s 2010s 2020s 1927 -

Present

Past performance is not a guarantee for future results. Source: Morningstar. Shown for illustrative purposes only. There is no guarantee that companies will declare, continue to pay or increase dividends.

See glossary of investment terms.

23Dividend sustainability is critical

Dividend Yield and Dividend Growth Rate of Equity Income vs Russell 1000 Value Index – Trailing Twelve Months

Higher dividend yield Consistent dividend growth More dividend increases

Gross Dividend Yield Trailing 12 Month Dividend Growth Trailing 12 Month Dividend Increase**

3.5% 100.0%

92%

20.0% 90.0%

3.0%

2.7%

80.0%

2.5% 2.3% 70.0%

15.0% 14.2%

60.0%

2.0% 54%

11.0%

50.0%

10.0%

1.5%

40.0%

1.0% 30.0%

5.0%

20.0%

0.5%

10.0%

0.0% 0.0% 0.0%

Equity Income Russell 1000 Value Equity Income Russell 1000 Value Equity Income Russell 1000 Value

Index Index Index

Source: J.P. Morgan Asset Management, Factset. As of December 31, 2022. Dividend yield is calculated by taking the sum-total dividend yield of each stock held in the portfolio. The dividend yield for each

stock is the most recent dividend payout annualised and divided by the share price. Dividend growth calculates the annualized average rate of increase in the dividends paid by stock held in the portfolio.

**Refer to dividend increase during the time period as a percentage of holdings. ***Refer to dividend cuts and suspensions during the time period as a percentage of holdings. The Equity Income Portfolio and

the Russell 1000 Value Index dividend yield and dividend growth rates are calculated in the same manner. For illustrative purposes only. Yield is not guaranteed and may change over time. See glossary of

investment terms.

24A long track record of consistent outperformance

JPMorgan Equity Income Portfolio as of December 31, 2022

JPMorgan Equity Income Strategy: 5 Year and 10 Year Rolling1 Excess Returns vs. Russell 1000 Value Index

6%

5 Year Rolling Excess Return 10 Year Rolling Excess Return

5%

Equity Income has outperformed:

94% of rolling 5-year periods

100% of rolling 10-year periods

4%

3%

2%

1%

0%

-1%

Nov-07

Nov-08

Nov-09

Nov-10

Nov-11

Nov-12

Nov-13

Nov-14

Nov-15

Nov-16

Nov-17

Nov-18

Nov-19

Nov-20

Nov-21

Nov-22

May-08

May-09

May-10

May-11

May-12

May-13

May-14

May-15

May-16

May-17

May-18

May-19

May-20

May-21

May-22

Past performance is no guarantee of future results. Excess returns are against the Russell 1000 Value Index. Indices do not include fees or operating expenses and

are not available for actual investment. 1Rolling excess returns since PM inception: 11/30/2002 for the J.P. Morgan Equity Income composite (Gross of Fees). See glossary of investment terms.

25Investment team biographies

Clare Hart Tony D. Lee

Managing Director Vice President

Is a portfolio manager in the U.S. Equity Group. An employee since 1999, Clare is the lead Is an investment analyst on the JPMorgan Equity Income and U.S. Value Funds within the U.S.

portfolio manager of the JPMorgan Equity Income Fund and the JPMorgan U.S. Value Fund. Prior Equity Group. An employee since 2012, Tony is a generalist analyst who covers multiple sectors.

to joining the team, Clare was with Salomon Smith Barney’s equity research division as a research Prior to joining the team in 2018, Tony was a member of our U.S. Equity Research team covering

associate covering Real Estate Investment Trusts. She began her career at Arthur Andersen, healthcare and insurance industries. Tony holds B.S. in Hotel Administration with concentrations

working as a public accountant while earning both an M.S.A. from DePaul University and a in Real Estate and Finance from Cornell University. He is a CFA charterholder.

C.P.A. granted by the State of Illinois. Clare also holds a B.A. in political science from the

University of Chicago.

Andrew Brandon

Managing Director

Is a portfolio manager in on the JPMorgan Equity Income and the JPMorgan U.S. Value Funds

within the U.S. Equity Group. An employee since 2000, Andrew joined the investment team in

2012 as an investment analyst on the JPMorgan Equity Income and Growth and Income Funds.

Prior to joining the team, Andrew was a member of our US equity research team covering the

financial industry. Andrew has also worked in the JPMorgan Private Bank supporting portfolio

managers of both the U.S. large cap core equity product, and the U.S. large cap value product.

Andrew obtained a B.A. in economics from the University of Virginia, and an M.B.A. from the

University of Florida. He is a CFA charterholder.

David Silberman

Managing Director

Is a portfolio manager on the JPMorgan Equity Income and the JPMorgan U.S. Value Funds within

the U.S. Equity Group. An employee since 1989, David assumed his current role in 2019.

Previously, David was the Head of the Equity Investment Director and Corporate Governance

teams globally and the lead U.S. Equity Investment Director since 2008. Before that, he was a

portfolio manager in the U.S. Equity Group where he managed equity portfolios for private clients,

endowments and foundations. He has also worked in the Emerging Markets Derivatives Group

and attended the J.P. Morgan training program. David holds a B.A. in economics and political

science from the State University of New York at Binghamton and an M.B.A. from the Stern School

of Business at New York University.

Charles “Lerone” Vincent

Managing Director

is a research analyst on the JPMorgan Equity Income and U.S. Value Funds within the U.S. Equity

Group. Previously, he was a research analyst on the U.S. Equity Core team focusing on large and

mid-cap basic materials companies. An employee since 1998, Lerone served as an analyst on

the Mid-Cap Value team focusing on industrials, technology, utilities and basic materials

companies. Prior to this, he served as a generalist on the Tax Aware Large Cap Core Strategy,

before that, Lerone was a research assistant covering the technology and telecom sectors, and

before that, he was an associate and analyst in the Diversified Industries and Consumer Products

group at the firm's Investment Bank. Lerone holds a B.S.M. from Tulane University and is a CFA

charterholder.

26Investment team biographies

Don San Jose

Managing Director

Is the Chief Investment Officer of the U.S. Value Team and a portfolio manager within the U.S.

Equity Group. An employee since 2000, Don is responsible for managing the J.P. Morgan Small

Cap Active Core and SMID Cap Core Strategies. Prior to joining the Small Cap Team, Don was an

analyst in the JPMorgan Securities' equity research department covering capital goods

companies. Prior to joining the firm, Don was an equity research associate at ING Baring

Furman Selz. Don holds a B.S. in Finance from The Wharton School of the University of

Pennsylvania. He is a member of both the New York Society of Security Analysts and The CFA

Institute, and a CFA charterholder.

Jaime H. Steinhardt

Executive Director

Is an investment specialist within the U.S. Equity Group. An employee since 2012, Jaime is the

head of the investment specialist team that is responsible for communicating investment

performance, outlook, and strategy positioning to institutional and funds clients for the firm’s U.S.

Equity Value platform. She holds a B.A. in economics from Georgetown University and holds the

Series 7 and 63 licenses. She is a member of both the New York Society of Security Analysts and

the CFA Institute, and a CFA charterholder.

Jenna B. Silver

Vice President

Is an investment specialist in the U.S. Equity Group. An employee since 2013, Jenna is

responsible for communicating investment performance, outlook, and strategy positioning to

institutional and funds clients for the firm’s U.S. Equity Value platform. Jenna previously worked in

Asset Management's Product Strategy team, focusing on the fixed income landscape, industry

trends, product development, and competitive positioning. Jenna holds a B.B.A. in Finance and

Strategy from the University of Michigan, Stephen M. Ross School of Business. She also holds the

Series 7 and 63 licenses and is a CFA charterholder.

Rory T. Houser

Associate

is an investment specialist within the U.S. Equity Group. An employee since 2015, Rory is

responsible for communicating investment performance, outlook, and strategy positioning to

institutional and funds clients for the firm’s U.S. Equity Value platform. He started his career

working in J.P. Morgan’s Private Bank, partnering with family offices, endowments, and

foundations to develop investment strategies and identify the opportunities that shape their

portfolios and long-term investment goals. Rory holds a B.S. in finance and entrepreneurship from

the University of the Dayton, and holds the Series 7 and 63 licenses. He is a CFA charterholder.

27Equity Income Managed Accounts Composite December 31, 2021 Publication date: 10/10/2022 28

Glossary of Investment Terms

Active Share - a measure of the percentage Free cash flow yield - a financial solvency ratio that Turnover Ratio - Percentage of holdings in a mutual

of stock holdings in a manager's portfolio that differs compares the free cash flow per share a company is fund that are sold in a specified period.

from the benchmark index. expected to earn against its market value per share.

Up-Market Capture – a statistical measure of an

The ratio is calculated by taking the free cash flow per

Alpha - The amount of return expected from an investment manager's overall performance in up-

share divided by the current share price.

investment from its inherent value. markets.

Fundamental analysis - attempts to measure a

Information ratio (IR) – A ratio of portfolio returns Valuation - An estimate of the value or worth of a

security's intrinsic value by examining related

above the returns of a benchmark to the volatility of company; the price investors assign to an individual

economic and financial factors including the balance

those returns. stock.

sheet, strategic initiatives, microeconomic indicators,

Bottom-up investing - an investment approach that and consumer behavior. Value investing - A strategy whereby investors

focuses on the analysis of individual stocks and de- purchase equity securities that they believe are selling

Growth investing - Investment strategy that focuses

emphasizes the significance of macroeconomic cycles below estimated true value. The investor can profit by

on stocks of companies and stock funds where

and market cycles. buying these securities then selling them once they

earnings are growing rapidly and are expected to

appreciate to their real value.

Barra Risk Factor Analysis – A multi-factor model, continue growing.

created by Barra Inc., used to measure the overall risk Weighted Average Market Capitalization - Most

Large-cap - The market capitalization of the stocks of

associated with a security relative to market indexes are constructed by weighting the market

companies with market values greater than $10 billion.

performance. The model incorporates >40 data capitalization of each stock on the index. In such an

metrics and measures risk factors via three main Mid-cap - The market capitalization of the stocks of index, larger companies account for a greater portion

components: industry risk, company-specific risk and companies with market values between $3 to $10 of the index. An example is the S&P 500 Index.

risks from exposure to investment themes. billion.

Beta - A measurement of volatility where 1 is neutral; Performance attribution - a set of techniques that

above 1 is more volatile; and less than 1 is less performance analysts use to explain why a portfolio's

volatile. performance differed from the benchmark.

Down-Market Capture - a statistical measure of an Price/Earnings (P/E) 12-month forward - price of a

investment manager's overall performance in down- stock divided by its projected earnings for the coming

markets. year.

Earnings Per Share (EPS) - The portion of a Small-cap - The market capitalization of the stocks of

company's profit allocated to each outstanding share companies with market values less than $3 billion.

of common stock. EPS serves as an indicator of a

Tracking Error (TE) - The active risk of the portfolio.

company's profitability.

It determines the annualized standard deviation of the

Excess Return (ER) – portfolio returns achieved excess returns between the portfolio and the

above and beyond the return of its benchmark. benchmark.

29J.P. Morgan Asset Management This is a promotional document and is intended to report solely on investment strategies and opportunities identified J.P. Morgan Asset Management or any of its affiliates and by J.P. Morgan Asset Management and as such the views employees may hold positions or act as a market maker in contained herein are not to be taken as advice or a the financial instruments of any issuer discussed herein or recommendation to buy or sell any investment or interest act as the underwriter, placement agent or lender to such thereto. This document is confidential and intended only for issuer. The investments and strategies discussed herein the person or entity to which it has been provided. Reliance may not be appropriate for all investors and may not be upon information in this material is at the sole discretion of authorized or its offering may be restricted in your the reader. The material was prepared without regard to jurisdiction, it is the responsibility of every reader to satisfy specific objectives, financial situation or needs of any himself as to the full observance of the laws and regulations particular receiver. Any research in this document has been of the relevant jurisdictions. Prior to any application investors 0903c02a8276458a obtained and may have been acted upon by J.P. Morgan are advised to take all necessary legal, regulatory and tax Asset Management for its own purpose. The results of such advice on the consequences of an investment in the research are being made available as additional information products. and do not necessarily reflect the views of J.P. Morgan Asset Management. Any forecasts, figures, opinions, The Russell 1000 Value Index measures the performance of statements of financial market trends or investment those Russell 1000 companies with lower price-to-book techniques and strategies expressed are those of J.P. ratios and lower forecasted growth values. The performance Morgan Asset Management, unless otherwise stated, as of of the index does not reflect the deduction of expenses the date of issuance. They are considered to be reliable at associated with a mutual fund, such as investment the time of production, but no warranty as to the accuracy management fees. By contrast, the performance of the Fund and reliability or completeness in respect of any error or reflects the deduction of mutual fund expenses, including omission is accepted, and may be subject to change without sales charges if applicable. An investor can not invest reference or notification to you. directly in an index. Investment involves risks. Any investment decision should If you are a person with a disability and need additional be based solely on the basis of any relevant offering support in viewing the material, please call us at 1-800-343- documents such as the prospectus, annual report, semi- 1113 for assistance. annual report, private placement or offering memorandum. J.P. Morgan Asset Management is the brand for the asset For further information, any questions and for copies of the management business of JPMorgan Chase & Co. and its offering material you can contact your usual J.P. Morgan affiliates worldwide. Asset Management representative. Both past performance and yields are not reliable indicators of current and future Telephone calls and electronic communications may be results. There is no guarantee that any forecast will come to monitored and/or recorded. pass. Any reproduction, retransmission, dissemination or Personal data will be collected, stored and processed by other unauthorized use of this document or the information J.P. Morgan Asset Management in accordance with our contained herein by any person or entity without the express privacy policies at https://www.jpmorgan.com/privacy. prior written consent of J.P. Morgan Asset Management is © 2023 JPMorgan Chase & Co. All rights reserved. strictly prohibited. 30

You can also read