INVESTOR PRESENTATION - SMARTCENTRES

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Investor Presentation

Based on First Quarter 2016

May 2016

Notice to Reader

Readers are cautioned that certain terms used in this Investor Presentation (“Presentation”) such as Funds from

Operations ("FFO"), Adjusted Funds from Operations ("AFFO"), "Gross Book Value", "Payout Ratio", "Interest

Coverage", "Total Debt to Adjusted EBITDA" and any related per Unit amounts used by management to measure,

compare and explain the operating results and financial performance of the Trust do not have any standardized

meaning prescribed under IFRS and, therefore, should not be construed as alternatives to net income or cash flow

from operating activities calculated in accordance with IFRS. These terms are defined in this Presentation and

reconciled to the consolidated financial information of the Trust in the Management’s Discussion and Analysis

(“MD&A”) for the three months ended March 31, 2016. Such terms do not have a standardized meaning prescribed

by IFRS and may not be comparable to similarly titled measures presented by other publicly traded entities.

Certain statements in this Presentation are "forward-looking statements" that reflect management's expectations

regarding the Trust's future growth, results of operations, performance and business prospects and opportunities.

More specifically, certain statements contained in this Presentation, including statements related to the Trust's

maintenance of productive capacity, estimated future development plans and costs, view of term mortgage renewals

including rates and upfinancing amounts, timing of future payments of obligations, intentions to secure additional

financing and potential financing sources, and vacancy and leasing assumptions, and statements that contain words

such as "could", "should", "can", "anticipate", "expect", "believe", "will", "may" and similar expressions and

statements relating to matters that are not historical facts, constitute "forward-looking statements". These forward-

looking statements are presented for the purpose of assisting the Trust's Unitholders and financial analysts in

understanding the Trust's operating environment, and may not be appropriate for other purposes. Such forward-

looking statements reflect management's current beliefs and are based on information currently available to

management. However, such forward-looking statements involve significant risks and uncertainties. A number of

factors could cause actual results to differ materially from the results discussed in the forward-looking statements.

Although the forward-looking statements contained in this Presentation are based on what management believes to

be reasonable assumptions, the Trust cannot assure investors that actual results will be consistent with these

forward-looking statements. The forward-looking statements contained herein are expressly qualified in their entirety

by this cautionary statement. These forward-looking statements are made as at the date of this Presentation and the

Trust assumes no obligation to update or revise them to reflect new events or circumstances unless otherwise

required by applicable securities legislation.

SmartREIT 2

Vision

Creating Exceptional Places to Shop and Work

SmartREIT 3

Smart Real Estate Investment Trust

One of Canada’s premier REITs

$5.4 billion equity capitalization

(unit price of $34.76 as of May 10, 2016)

$8.6 billion total asset value

139 shopping centres across Canada

31.0 million square feet of owned GLA

72% of our properties are anchored by Walmart

SmartREIT 4

Q1 2016 - Solid Performance

98.5% occupancy

Portfolio increased in value by $1.4 billion to $8.5

billion over Q1 2015

FFO per unit increased by 3.8% over Q1 2015

2016 tenant retention already at 70% with an

average rental increase of 6.8%

Construction of the first phase of the Vaughan

Metropolitan Centre now largely complete

SmartREIT 5

Q1 2016 - Solid Performance

March 31 March 31

2016 2015 Change

FFO / unit $0.54 $0.52 +3.8%

AFFO / unit $0.51 $0.48 +6.3%

Payout ratio 81.0% 82.6% -1.6%

Debt to Aggregate Assets 44.6% 43.1% +1.5%

Liquidity: Cash Resources $329.7M $373.7M -11.8%

Unencumbered Asset Pool $2.5B $2.4B +4.2%

Debt to Adjusted EBITDA 8.4X 7.6X +10.5%

Interest Coverage 3.0X 2.8X +7.1%

SmartREIT 6

Growth in Rental Revenue Growth in AFFO / Unit

8.3% CAGR since 2011 6.6% CAGR since 2011

Rental Revenue AFFO / Unit

(in millions of $)

718.5 2.16

670.3 1.99

1.84

607.6 1.71 1.75

546.1 573.0 1.65

511.9

2011 2012 2013 2014 2015 Q1 2011 2012 2013 2014 2015 Q1

2016* 2016*

* Annualized

SmartREIT 7

Growth in Total Assets

39.0% CAGR since 2002

Total Assets

(in millions of $)

8,505 8,562

7,070 7,107

6,480

5,956

4,194 4,237 4,374

3,894

3,584

2,564

1,015

109 229

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Q1

2016*

* Annualized

SmartREIT 8

Total Return to Unitholders

18.0% average annual return since IPO

$1,000

$958.48

$900

$800

$700

$600

$500

$400 $403.79

$300 $310.09

$200

$100

$0

SmartREIT TSX Capped REIT TSX Composite

SmartREIT 9

What Makes SmartREIT Strong

The capabilities of our team

The quality of our portfolio

The quality of our tenants

Our strategic relationships

Our healthy balance sheet

SmartREIT 10The Capabilities of our Team

Integrated team of approximately 300 employees

The most experienced retail development team in

Canada

50 million square feet and in excess of 170 centres

developed and built over the last 20 years

Very experienced and capable leasing, and

operations groups

Exceptional support organization

SmartREIT 11SmartREIT’s Portfolio

31.0 million square feet of shopping centre space

Average age: 12.2 years (youngest in the industry)

Low capital expenditures

Coast to coast locations

84% are urban or near urban markets

Virtually 100% of sites contain both a food store and a

pharmacy, either in a Walmart store or independently

Strong value orientation

Results in high degree of stability:

98.5% occupancy as at March 31

Average occupancy of 99.1% since 2005

SmartREIT 12SmartREIT’s Portfolio

139 Properties*

31.1 million square feet*

Alberta Manitoba

7 3

Saskatchewan Quebec

BC 4 21

13 Atlantic

Ontario 10

81

* Excludes 3 redevelopment properties and 8

development lands totalling 1.4 million square feet upon

completion and an additional 3.5 million square feet of

development density associated with existing centres

72% of our sites are Walmart anchored or shadow-anchored (85%

by total area)

High % of the portfolio focused in Ontario, Quebec and BC, which

are Canada’s fastest growing provinces

SmartREIT 13Stable Cash Flow

AFFO Payout Ratio

Distribution fully funded from

operating cashflow

94.0% 90.3% 88.6% 84.7% 81.1% 81.0% Efficient capital allocation

Efficient and transparent

distribution

2011 2012 2013 2014 2015 Q1 2016* * Annualized

$ per unit

FFO 1.70 1.79 1.85 1.95 2.10 2.16

AFFO 1.65 1.71 1.75 1.84 1.99 2.04

Distributions 1.55 1.55 1.55 1.56 1.61 1.65

Management and the Board have endorsed a target payout range of 77% to 82% as of

February 2016

Management expects the payout ratio to remain in the high 70% to low 80% range

Annual distribution increased in 2014 to $1.60 from $1.55, representing a 3.4% increase,

with a further increase in October 2015 to $1.65, representing a 3.125% increase

SmartREIT 14SmartREIT’s Tenant Base

72% of our sites are Walmart anchored or

shadow-anchored (85% by total area)

92% of our tenants are national

Our top ten tenants generate 50% of our

revenue

Adding exciting new tenants all the time

Results in:

70% tenant retention to date for 2016

renewals, representing 1.2 million square feet

6.8% average rental uplifts excluding anchor

tenants, 4.6% including them

SmartREIT 15Well Tenanted, High Quality Portfolio

The following table illustrates the top ten tenants for SmartREIT’s Property

Portfolio as at March 31, 2016, in terms of their percentage contribution to gross

rental revenues of SmartREIT’s Portfolio:

Average

% of Gross DBRS Credit

Tenant Number of Stores Remaining

Rental Revenues Rating

Lease Term

Walmart 94 27.0 8.6 AA

Canadian Tire, Mark's and FGL Sports 68 4.7 6.5 BBB (high)

Winners, Homesense and Marshalls 44 3.7 5.7

Reitmans 109 2.5 3.1

Best Buy 27 2.3 2.6

Loblaw and Shoppers Drug Mart 19 2.3 7.1 BBB

Sobeys 15 2.2 6.3 BBB (low)

RONA 7 2.0 7.3 BB (high)

Michaels 24 1.6 4.8

Staples 23 1.4 2.6

Total 49.7 7.5

SmartREIT 16Best-in-class Stable Occupancy

99.1% average occupancy since 2005

Occupancy

99.2% 99.3% 99.3% 99.2%

98.9% 99.1% 99.0% 99.0% 99.0% 99.0% 98.7%

98.5%

97.9% 97.8%

96.4%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Q1

2016

SmartREIT 17Stable Income Base

Average lease term of 6.7 years

Average remaining lease term of 8.6 years for Walmart, with multiple renewal options

of up to 80 years

Average remaining lease term excluding Walmart is 5.3 years

2016 average retention rate to date at 70% and lifts on renewals of 6.8%

Average “same property” NOI growth is 1.0% to 1.5% p.a.

Lease Maturity by Area

(in millions of square feet)

2.3 3.1 3.1 3.1 3.0 2.6

1.9 1.9

1.4

0.7

0.3 0.5

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 Month- Vacant

to-month

Average roll of 2.3 million square feet annually (7.3% of total GLA per year)

SmartREIT 18Transformation Transforming into a leading, fully-integrated REIT with best-in-class capabilities SmartREIT 19

Transformational SmartCentres Acquisition Positions

SmartREIT for Growth

Transaction Highlights

1. Acquired a large, high quality

portfolio of real estate

2. Created a fully-integrated real

estate platform

3. Provides enhanced growth

opportunities

SmartREIT 20Transformation of Calloway into SmartREIT

1 2

Calloway Then SmartREIT Now

1. 27.4M square feet of GLA 1. 31.0M square feet of GLA

2. 129 properties 2. 150 properties

3. 98.6% occupancy 3. 98.5% occupancy

4. Weighted average lease term 6.7 years 4. Weighted average lease term 6.7 years

5. 2.7M square feet of potential 5. 5.0M square feet of potential retail

retail development3 development3

6. $7.2B of Total Assets 6. $8.5B of Total Assets

7. Best-in-class internal property and 7. Fully-integrated property, asset development

asset management capabilities and leasing management capability

8. New Brand – Calloway rebranded itself

SmartREIT, trading under a new ticker:

SRU.UN, and leveraging SmartCentres’

considerable brand equity and our new

combined strengths

1 As of March 31, 2015

2 As of March 31, 2016

3 Excludes development opportunities with Mezzanine loans

SmartREIT 21Financing of Transaction

Purchase price within formal valuation range

Approximately $645.5 million of assumed debt at

a weighted average interest rate of 2.5%

Issuance of $174.2 million in Class B LP units of

SmartREIT subsidiary partnerships to certain

vendors, exchangeable for REIT units on a one-

for-one basis

Net proceeds from an offering of $230 million of

subscription receipts in a bought-deal financing

Remainder financed by cash on hand

SmartREIT 22Acquisition Involved a Large, High Quality Real Estate

Portfolio

Acquisition Properties SmartREIT GLA at Share

Province % Acquired Occupancy Major Tenants1

Shopping Centres (SF 000s)

Future

In Place Development Total

Earnout

Alliston SmartCentre ON 100% 171 165 --- 336 100% Walmart Supercentre, Dollarama, Tim Hortons

Aurora North SmartCentre2 ON 50%2 249 --- 8 257 100% Walmart Supercentre, RONA, Best Buy, Golf Town, LCBO

Blainville SmartCentre QC 100% 176 39 --- 215 100% Walmart Supercentre, Dollarama, Bulk Barn, BNS, RBC

Bracebridge SmartCentre ON 100% 142 62 --- 204 100% Walmart Supercentre, Dollar Tree, Boston Pizza, Bulk Barn

Bradford SmartCentre ON 100% 238 184 --- 422 100% Walmart Supercentre, GoodLife Fitness, Dollarama, CIBC

Bramport SmartCentre (II) ON 100% 38 --- --- 38 100% No Frills

Brampton Northeast SmartCentre ON 100% 210 48 --- 258 100% Walmart Supercentre, GoodLife Fitness, LCBO, CIBC

Cornwall SmartCentre ON 100% 164 32 --- 196 100% Walmart Supercentre, Dollar Tree

Laval Centre SmartCentre QC 100% 160 102 --- 262 100% Walmart Supercentre

Markham East SmartCentre ON 40% 69 --- 69 138 100% Walmart Supercentre, Dollar Tree, CIBC

Mascouche North SmartCentre QC 100% 51 61 --- 112 100% Jean Coutu, Structube, McDonald’s, Bulk Barn

Mississauga (Go Lands) SmartCentre ON 50%3 56 --- 3 59 100% Toys R Us, Marshalls, Dollarama

Montreal Premium Outlet (Mirabel) QC 25%4 91 --- 25 116 90% Hudson’s Bay Outlet, Polo, Old Navy, Nike

Oakville SmartCentre ON 100%5 445 --- 110 555 100% Walmart Supercentre, Loblaws, CIBC, The Beer Store

Oshawa North SmartCentre (II) ON 100% 160 --- 20 180 100% Home Outfitters, Winners, PetSmart, Party Packagers

Oshawa South SmartCentre ON 50%2 268 --- 9 277 100% Walmart Supercentre, Lowe’s, Sail, CIBC, Dollarama

Port Elgin SmartCentre ON 100% 116 --- --- 116 100% Walmart Supercentre

Stoney Creek SmartCentre ON 100% 263 100 --- 363 100% Walmart Supercentre, Toys R Us, Dollar Tree, CIBC

Sylvan Lake SmartCentre AB 100% 125 125 --- 250 100% Walmart Supercentre, Dollarama

Vaudreuil SmartCentre QC 100% 15 39 --- 54 100% Brunet, Coco Fruitti

Vaughan Northwest SmartCentre ON 100% 163 344 --- 507 100% Walmart Supercentre, CIBC

Waterloo SmartCentre ON 100% 181 76 --- 257 100% Walmart Supercentre, Value Village, Mark’s, Dollarama

Total - Shopping Centres 3,551 1,376 244 5,172 99.7%

Note: Data as at March 31, 2015. (1) Includes committed leases. (2) SmartREIT previously held a 50% leasehold interest in this property. Following the Transaction, SmartREIT owns a 50% freehold interest and

continues to have an option to acquire the remaining 50% freehold interest at the end of the term of the existing lease. (3) Following the Transaction, SmartREIT owns 100% of this property as it previously owned

the other 50%. (4) Following the Transaction, SmartREIT owns 50% of this property as it previously owned a 25% interest. (5) SmartREIT entered into a lease for this property with an option to acquire the

freehold interest at the end of the lease term. (6) Development Properties expected to close 12-24 months post initial closing.

SmartREIT 23Governance Rights and Non-Compete Agreement

Reflective of Mitchell Goldhar’s significant ownership position and his ongoing relationship with the REIT, certain governance rights of Mitchell

Goldhar and related entities (“MG Entities”) have been amended and extended, and he has entered into a non-compete agreement.

Provision Description

Pre-Transaction Right to appoint Trustees based on the following ownership levels: Ownership >= 5%: appoint 1 Trustee, max. Trustees 8; Ownership >= 15%:

Trustee appoint 2 Trustees, max. Trustees 8; and Ownership >= 25%: appoint 3 Trustees, max. Trustees 9

Appointment

Post-Transaction Ownership thresholds extended to include holdings of Mitchell Goldhar and MG entities

Pre-Transaction Right to vote 25% of votes at a meeting of unitholders to July 1, 2015, as long as Mitchell Goldhar owns the lesser of (i) 20 million Units or (ii)

20% of the Units

Voting Top-up

Right Post-Transaction Expiry extended to July 1, 2020

Ownership extended from Mitchell Goldhar to include MG Entities

20 million Units must represent at least 10% of the outstanding Units

Pre-Transaction NA

Special

Committee Post-Transaction So long as MG Entities own 5% of the Units, until his death Mitchell Goldhar will have the right to appoint 1 member of any special committee

reviewing strategic transactions where MG Entities are not an interested party

Pre-Transaction NA

Board of Post-Transaction Until the earlier of July 1, 2025 or MG Entities no longer owning 10% of the Units, Mitchell Goldhar has the right to be the Non-Executive

Trustees Chair Chairman

If Mitchell Goldhar is the Non-Executive Chairman, the Board will elect a Lead Independent Trustee

Pre-Transaction Mitchell Goldhar has the right to appoint 1 member as long as he owns 15% of Units

Corporate

Governance and Post-Transaction Committee has right to appoint and remove the Chief Operating Officer (“COO”) and Chief Development Officer (“CDO”)

Compensation From closing until the earlier of (i) 5 years post closing; (ii) MG Entities owning less than 10% of the Units; or (iii) Mitchell Goldhar’s death

Committee All decisions require unanimous approval

MG Entities have the right to appoint 1 member of the Committee

Demand & Pre-Transaction NA

Registration

Rights Post-Transaction As long as MG Entities own 10% or more they will have Demand; Piggy-Back; and Pre-Emptive Rights

Pre-Transaction NA

Post-Transaction Later of 3 years post closing or the Voting Top-up Right no longer being applicable. Contains exclusions for certain minority and passive

Non-Compete investments or if SmartREIT does not exercise first right below.

Effectively limits Mitchell Goldhar from acquiring new retail assets of a similar nature to SmartREIT's. Mitchell Goldhar must first offer

SmartREIT the opportunity to purchase them (subject to certain exclusions relating to OneREIT and other existing investments).

Note: The above table sets forth a summary of highlights of the rights and non-compete agreement for Mitchell Goldhar. For comprehensive information on these matters and other rights not

summarized above, please refer to the Management Information Circular posted to Sedar. MG Entities include Mitchell Goldhar, his family members, their spouses, his heirs and executors and

their affiliates and other entities such as trusts established for the benefit of those referred to prior.

SmartREIT 24Strategic Relationships

Walmart

Mitchell Goldhar

Simon Property Group

SmartREIT 25Strategic Relationship - Walmart Canada

Walmart Canada Number of Walmart Stores

attributes

Value pricing and fresh

food generates huge

traffic 214 296

Other

Dominant retailer Shadow

14 SmartREIT

Has benefited from the 13

89 94

closure of Target

76% of Canadians live Supercentres Total Walmart

(316)* Stores (404)*

within 10 km of a Walmart * Company source as at May 10, 2016

SmartREIT 26Strategic Relationship - Mitchell Goldhar

JV Partner

Vaughan Metropolitan Centre

StudioCentre Site

Salmon Arm

Consultant on mixed use projects

Board Chair, Trustee and Investment Committee

member

Ad hoc advice and council on shopping centre

portfolio

Multiple on-going business relationships as

service provider

SmartREIT 27Strategic Relationship - Simon Property Group

Largest public real estate company in the U.S.

Engaged primarily in retail real estate properties

including regional malls, Premium Outlets and

The Mills®

Exceptional relationships with the world’s largest

retailers

Canada is part of a continuing global expansion

SmartREIT 28Our Balance Sheet is Strong

Unencumbered pool at $2.5 billion

Ready access to mortgage and unsecured debt

capital when needed

Key ratios improving

Payout ratio declined to 81.0% in Q1 2016,

within updated target range of 77% to 82%

Renewing interest rates much lower than

maturing rates

Our focus over the last year has been to move

towards secured financing, but we will continue

to access the unsecured market as appropriate

SmartREIT 29Debt Maturity / Leverage

Debt Maturity

(in millions of $)

4.6%

4.2% 4.3% 4.2% 4.3% 4.2%

3.7% 3.9%

3.7%

3.4%

90 100 3.1% 160

150 150

0 200

150 150 0

0

133 238 332 338 115 121 225 146 25 325 111

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 Thereafter

Secured Debt Unsecured Debentures Average Int. Rate

Lower interest costs on refinancing available with 10 year unsecured rates around 3.5% and secured rates

below that

Interest Coverage: 3.0X Target: 2.5 - 2.75X

Debt to EBITDA: 8.4X Target: 7.25 - 7.5X

Debt to GBV: 52.1% Target: 50 - 60% long-term trend to continue to de-lever

Unencumbered pool: $2.5 billion (2.1X) Target: 1.5X unsecured coverage

Weighted Avg Interest Rate (Secured Debt): 3.86%

Weighted Avg Term to Maturity (Secured Debt): 5.3 yrs

DBRS rating of BBB with a Stable trend

SmartREIT 30Leverage Profile

Dec. 31 Dec. 31 Dec. 31 Mar. 31

2013 2014 2015 2016

Debt to Aggregate Assets(1) 43.8% 42.8% 44.7% 44.6%

Secured Debt to Aggregate Assets(2) 28.1% 24.7% 31.2% 31.1%

Unencumbered Assets $1.5B $2.4B $2.5B $2.5B

Debt to Adjusted EBITDA(1) 8.1X 7.4X 8.4X 8.4X

Interest Coverage 2.5X 2.7X 3.0X 3.0X

Liquidity: Cash Resources $338M $324M $345M $330M

Weighted Average Interest Rate(3) 5.17% 5.03% 3.87% 3.86%

Weighted Average Term to Maturity(3) 5.5 yrs 5.3 yrs 5.4 yrs 5.3 yrs

(1) Leverage increased during 2015 in support of the transformative SmartCentres Platform transaction

(2) Significant rate spread between unsecured and secured debt led management to increase secured debt

financing during 2015

(3) Secured Debt

SmartREIT 31Conservative Capital Structure

Total Enterprise Value – $8.7 Billion

Secured Mortgage Financing

28.3% Amount - $2.6 billion

Weighted Avg Interest Rate – 3.86%

Weighted Avg Term to Maturity – 5.3 years

Unsecured Debentures Focused on:

12.5% Amount - $1.2 billion

Weighted Avg Interest Rate – 3.94% Lowering interest rates on renewals

Weighted Avg Term to Maturity – 5.2 years

Maintaining maximum flexibility

Equity

58.7% Units Outstanding – 155 million Reducing leverage over time

Share Price – $34.76 as at May 10, 2016

Market Capitalization – $5.4 billion

Operating Lines / Outstanding LC’s

0.5% Operating Line – $20 million

Letters of Credit – $29 million

SmartREIT 32SmartREIT’s Key Challenges and Opportunities

Our core platform has great stability, resulting in

inherent growth in same property income of 1%

to 1.5%

Over time, our cost of capital is expected to climb

as interest rates rise

Acquisition supply is slowing, with more

competitive bidding from pension funds and

other institutions

We needed to diversify our income sources to

manage risk

SmartREIT 33Key Growth Principles We Are Following

Growth will come from a wide variety of areas

Risk management will be a key consideration as

we allocate capital

We will take a reasoned and disciplined

approach for the long term

We will continue to work with key partners to

drive growth

SmartREIT 34SmartREIT’s Growth Drivers

1. Unique portfolio of department store-anchored

value-focused retailers

Improve organic same property growth

above 1%

2. Retail intensification of approximately 310,000

square feet in existing portfolio

Place Bourassa

South Oakville

Other sites to be identified

SmartREIT 35SmartREIT’s Growth Drivers (cont’d)

3. Premium Outlet Malls

Value oriented sites, principally in fashion

segment

Market dynamics currently very supportive

4. Internal Growth Pipeline

Approximately 5.0 million square feet of

future development and earnouts across

multiple sites

SmartREIT 36SmartREIT’s Growth Drivers (cont’d)

5. Vaughan Metropolitan Centre

GTA’s largest future mixed used

development

6. Other mixed use opportunities identified and

moving through the zoning process

SmartREIT 37SmartREIT’s Growth Drivers (cont’d)

7. Walmart JV

SmartREIT has stepped into SmartCentres’

role to provide planning, development,

leasing and other services to Walmart in

Canada

SmartCentres has built over 170 shopping

centres over the last 20 years and we expect

to continue that business into the future

We are at the very early stages of exploring

opportunities in the US market with Walmart

SmartREIT 38SmartREIT’s Growth Drivers (cont’d)

8. Platform Leverage

Over and above the various development

opportunities noted, we have acquired the

most experienced retail development

platform in Canada. We will be looking for

third party development and redevelopment

opportunities to maximize the platform

capabilities

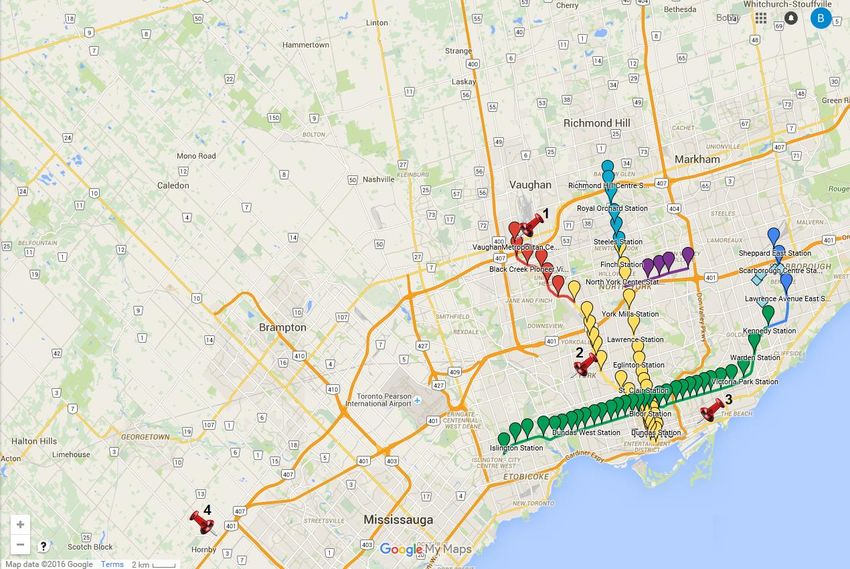

SmartREIT 39Greater Toronto Area

Key development area for SmartREIT

Population of 6.1 million as of

the 2011 Census

Map highlights existing and proposed TTC subway stations

1. Vaughan Metropolitan Centre

2. Westside Mall

3. StudioCentre

4. Toronto Premium Outlets

SmartREIT 40Premium Outlets

Toronto Premium Outlets (Halton Hills)

JV with Simon Property Group

500,000 SF when all phases are completed

Phase I opened August 1, 2013

Stabilized yield will be in the double digits

Montreal Premium Outlets (Mirabel)

JV with Simon Property Group

Phase I – 350,000 SF

Opened October 30, 2014

Additional 75 acres of potential retail development

adjacent to the site

Actively sourcing other locations

SmartREIT 41Premium Outlets SmartREIT 42

Toronto Premium Outlets (“TPO”) – Expansion SmartREIT 43

TPO Expansion – Pedestrian Bridge & Parking Deck SmartREIT 44

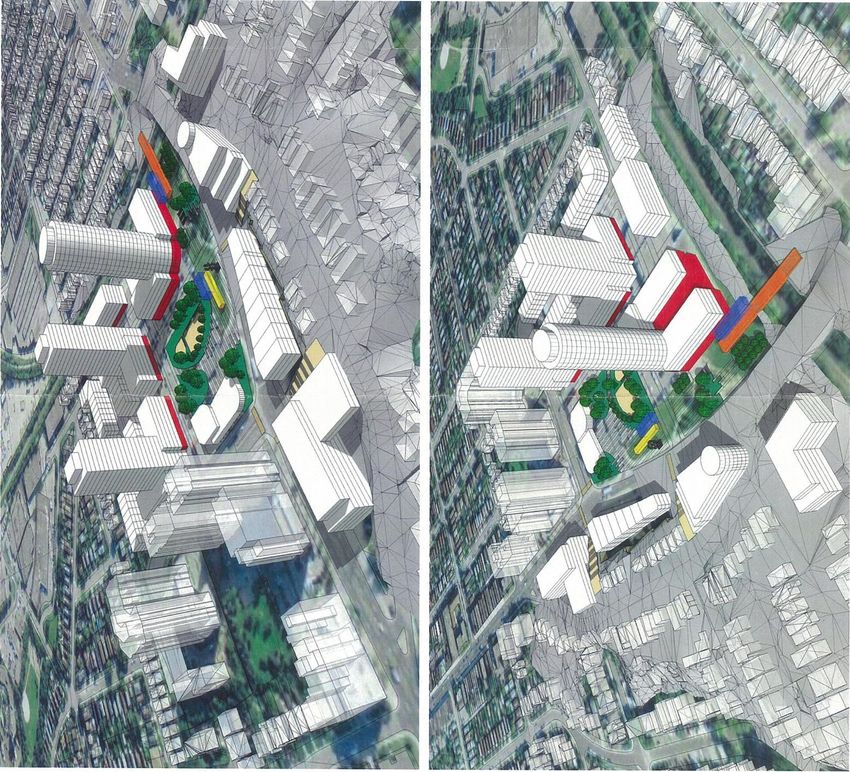

Vaughan Metropolitan Centre (“VMC”)

A long term build (10 – 15 years)

A 50:50 JV between SmartREIT and SmartCentres

Potential density of 8-10 million square feet of

residential, office and retail development

First development completed – KPMG tower complex

with 365,000 SF of LEED Gold space, opening in 2016

Second office tower with YMCA, Library and community

space confirmed for 100,000 SF and an office tenant in

final negotiations for another 80,000 SF

Transit infrastructure, including TTC subway, VIVA bus

and York regional bus, to open in 2017 – now fully funded

and updated schedule in place

Exceptional opportunity to develop a new city centre for

one of Canada’s fastest growing communities

SmartREIT 45VMC – Phases 1 & 2 of Development SmartREIT 46

VMC Today – Under Construction Construction of the KPMG Tower: nearly complete SmartREIT 47

VMC – Aerial SmartREIT 48

VMC – Major Construction Projects in Vicinity SmartREIT 49

VMC - Rapid Transit to Downtown Toronto SmartREIT 50

Additional Mixed Use Potential Opportunities

StudioCentre (Lakeshore Boulevard East)

1.2 million square foot site owned jointly with

SmartCentres

Received council approval in November 2015 relating

to the rezoning application

Westside Mall Toronto (Eglinton and Caledonia)

Shopping centre redevelopment leveraging new LRT

station

South Keys Ottawa

Redevelopment of shopping centre leveraging new

transit hub

Hwy 7 & Hwy 400 (Vaughan)

Redevelopment of current shopping centre site to

leverage proximity of Vaughan Metropolitan Centre

Various other sites under investigation

SmartREIT 51StudioCentre SmartREIT 52

StudioCentre Architect’s rendering of potential new site layout SmartREIT 53

StudioCentre SmartREIT 54

StudioCentre

StudioCentre is a brownfield

location next to Toronto’s eastern

waterfront. A former industrial site,

today it is an underutilized film

production centre

SmartREIT and SmartCentres

intend to revitalize the centre,

adding new production, office, and

retail opportunities

A rezoning exercise is underway,

seeking right to build 1.2 million

square feet at the centre. Approval

from the City of Toronto was

received in November 2015

Leasing activity for new media

businesses has already started –

over 30,000 square feet leased for

2015

SmartREIT 55Westside Mall Toronto

Current density - 143,800

square feet

City of Toronto proposed

density for site: 4.5x coverage =

approximately 2.15 million

square feet

Buildings height of up to 33

storeys

LRT to open by 2020;

construction well underway.

Tunnel boring is complete in

front of the centre. Station

construction not yet started

Zoning and approvals will be a

lengthy process

Architect’s rendering of potential intensification site plan

SmartREIT 56Laval Centre

The City of Laval has designated these lands as

their “centre-ville” due to its central location on the

island of Laval as well as its excellent access to

regional highways and public transportation.

These locational advantages make the site an

excellent mixed-use development with

unparalleled access to a host of retail,

entertainment and institutional uses. The lands

can easily be accessed by 2 major interchanges

from the 2 major highways that cross the City,

being autoroute 15 that gives north-south access

to the City of Montreal and north to the

recreational destinations of the Laurentians, and

autoroute 440 which crosses the island in an

east-west direction. The site is also served by 5

different bus routes on the 3 surrounding streets

(boul St-Martin, boul Daniel-Johnson and boul

Chomedey) with easy access to the nearby Metro

subway station as well as express access to

select Montreal destinations.

These benefits make Laval Centre an ideal

location for retail, as well as office and residential

uses, as evidenced by the tremendous growth in

high-rise residential construction in the area over

the last 5 years.

A 160,000 square foot Walmart Supercentre

currently anchors the centre, with an additional

100,000 square feet in the planning stages. And

zoning amendments are underway to permit

higher densities so as to accommodate 250,000

square feet of office, 1 million square feet of

residential as well as seniors’ housing.

SmartREIT 57Other Issues We Are Monitoring

In the coming years, retailers’ businesses will be affected

by:

E-commerce

Aging population

Urbanization and the move to more convenient

shopping

Changing ethnic mix of population

We will continue to monitor the impact of these issues

and will adjust our business model accordingly, always

remembering:

The quality of our sites

The value we provide our tenants

The strength and capabilities of our partners

SmartREIT 58E-commerce Response – Penguin Pick-Up

Penguin Pick-Up located at Scarborough (1900 Eglinton) SmartCentre

SmartREIT 59E-commerce Responses

Penguin Pick-Up:

Initiative driven by SmartCentres

Convenient locations for consumers to pick up

products ordered online

Drives traffic to shopping centres and supports

tenants

Five SmartREIT locations currently part of the

initiative

Piloting free Wi-Fi at select Western Canadian sites

Launching digital signage at select locations

Further initiatives in the planning stage

SmartREIT 60The Best Offense Starts With a Strong Defense -

SmartREIT

Best-in-Class Portfolio

Newest retail portfolio amongst all Canadian peers.

84% located in urban or near urban locations, with

strong national tenants as anchors

Strong Financial Position

Strong balance sheet and strong credit metrics.

Growing unencumbered pool provides increased

financial flexibility. Access to multiple sources of

capital

Growth Prospects Increasing, particularly after acquisition

Portfolio of growth opportunities from smaller local

intensification to Vaughan Metropolitan Centre,

amongst Canada’s largest potential mixed use

developments

SmartREIT 61Appendix SmartREIT 62

July 2015 Acquisition – Haney Place Mall

Address: 11900 Haney Place, Maple Ridge, BC

Major Intersection: Lougheed Highway & 224th street

Site Area: 227,000 square feet

Occupancy: 97%

Major Tenants: Walmart Supercentre, Thrifty Foods, Dollar Tree,

Rexall Pharmacy, Westminster Savings

SmartREIT 63SmartCentres Acquisition - Oakville SmartCentre

Address: 234 Hays Boulevard, Oakville, ON

Major Intersection: Highway 5 & Trafalgar Road

Site Area: 445,000 square feet

Occupancy: 100%

Major Tenants: Walmart Supercentre, Real Canadian Superstore

(Loblaws), LCBO, CIBC

SmartREIT 64SmartCentres Acquisition - Oshawa South SmartCentre

Address: 680 Laval Drive, Oshawa, ON

Major Intersection: Stevenson Road & Laval Drive

Site Area: 540,000 square feet

Occupancy: 100%

Major Tenants: Walmart Supercentre, Lowe’s, Sail, CIBC

SmartREIT 65You can also read