Impact of Inflation and the Current Economy on Valuations

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

7/25/2022

50th Annual Wichita Property Tax

Conference

Impact of Inflation and

the Current Economy

on Valuations July 2022

“Impact of Inflation and the Current Economy on Valuations” 1

• Roger Grabowski,

FASA

Roger Grabowski, FASA

Roger J. Grabowski, FASA, is a Managing Director with Kroll LLC and an Accredited Senior Appraiser and

Fellow (FASA) of the American Society of Appraisers (ASA) (their highest designation), Business Valuation.

He was formerly Managing Director of the Standard & Poor's Corporate Value Consulting practice, a partner

of PricewaterhouseCoopers LLP and one of its predecessor firms, Price Waterhouse (where he founded its

U.S. Valuation Services practice and managed the real estate appraisal practice).

He has directed valuations of businesses, interests in businesses, intellectual property, intangible assets, real

property and machinery and equipment. Roger has been recognized in various courts as an expert on

matters of solvency, the value of closely held businesses and business interests, valuation and amortization

Managing Director of intangible assets and other valuation issues. His testimony in U.S. District Court was referenced in the U.S.

Supreme Court opinion decided in his client's favor in the landmark Newark Morning Ledger case.

Valuation Advisory Services

Chicago, IL Roger is contributing author and co‐editor of Shannon Pratt’s Valuing a Business: The Analysis and Appraisal

roger.grabowski@kroll.com of Closely Held Companies, 6th ed. (McGraw‐Hill, 2022); contributing author to Lost Profits Damages:

Principles, Methods and Applications, 2nd ed. (Valuation Products and Services, 2022); co‐author Valuation

BBA - Bachelor of Business Administration Handbook‐International Guide to Cost of Capital: 2021 Summary Edition (CFA Institute Research Foundation

in Finance Books, 2021); co‐author with Shannon Pratt of Cost of Capital: Applications and Examples, 5th ed. (John

Wiley & Sons, 2014), The Lawyer's Guide to Cost of Capital (ABA, 2014), and Cost of Capital in Litigation:

Applications and Examples (John Wiley & Sons, 2010); author of numerous papers including: “Comparing

ABD- All Doctoral Work Except

Dissertation in Finance Growth Rates Used in Discounted Cash Flow Valuations,” Business Valuation Review (40(1) 2021).

Roger teaches courses for the American Society of Appraisers and lectures for professional associations

around the world.

“Impact of Inflation and the Current Economy on Valuations” 2

1

7/25/2022

Disclaimer

Any positions presented in this session are those of the panelists and do not represent the official position of Kroll, LLC. This material

is offered for educational purposes with the understanding that neither the authors nor Kroll, LLC or its affiliates are engaged in

rendering legal, accounting or any other professional service through presentation of this material.

The information presented in this session has been obtained with the greatest of care from sources believed to be reliable, but is not

guaranteed to be complete, accurate or timely. The authors and Kroll, LLC or its affiliates expressly disclaim any liability, including

incidental or consequential damages, arising from the use of this material or any errors or omissions that may be contained in it.

Name Change to Kroll

As of January 1, 2022, Duff & Phelps, LLC has become, and will henceforth be known as Kroll, LLC.

“Impact of Inflation and the Current Economy on Valuations” 3

Current Economic Environment

How did we get there?

“Impact of Inflation and the Current Economy on Valuations” 4

2

7/25/2022

Where are we?

• The financial markets started 2022 with misalignments, incongruities, and divergences seeking

normalization. The first six months of the year have shown investors and others affected by the financial

markets just how swiftly markets can shift when conditions are vulnerable.

• A "rolling crash" has rippled into almost every market sector. The benchmark S&P 500 Index is down about

20% from its early January peak. And the tech‐heavy Nasdaq Composite Index is down nearly 30% from its

November 2021 peak.

• Why? Inflation‐‐ a measure of the change in purchasing power over time.

Implicit in this definition are two key components:

• What prices are being measured?

Consumer prices OR consumer prices excluding food and energy, OR producer prices, OR

GDP price increases?

• In which country are we measuring inflation?

• The Fed was late to exit ZIRP (zero interest rate policy)/QE (quantitative easing), so they have had to

become more aggressive to address inflation. The consequence has been one of the most dramatic shifts

in interest rates and bond yields in many decades.

“Impact of Inflation and the Current Economy on Valuations” 5

Understanding inflation

Inflation is caused by the failure of aggregate supply to increase to meet increasers in aggregate demand‐‐

too much money chasing too few goods

• Even if demand increases, inflationary pressure may be countered by high unemployment (reducing

wage pressure) or excess production capacity (reducing cost pressure)– these factors are important

in dampening inflation pressure during periods of recession.

• “Structural changes” can reduce inflationary pressure. For example, following the period of extreme

inflation in the U.S. during 1965‐1980, manufacturers in the U.S. moved aggressively to outsource

production to low‐cost China. There goal was to better control and reduce operating costs.

• Innovation can dampen inflationary pressures. For example, the innovations in semi‐conductor

capacity and semi‐conductor production have allowed for decreases in the cost of computing power.

Substituting electric arc furnaces for coke fired blast furnaces, reduced the cost of producing a ton of

steel.

• Changes in consumer/investor behavior can dampen inflationary pressures. For example, following the

spiking of gasoline prices in 1973 and again in 1980 in the U.S., energy efficient cars made in Japan

became popular substitutes for Detroit manufactured cars. These imports were priced lower than U.S.

cars and worked to limit increases in U.S. auto price increases.

“Impact of Inflation and the Current Economy on Valuations” 6

3

7/25/2022

Measuring inflation – not so simple or accurate

• Measuring the market “basket”: U.S. Bureau of Labor Statistics tries to get the basket of goods and

services right, there are two fundamental problems: (1) the basket varies widely across consumers and

identifying the representative consumer is inherently subjective; (2) the basket is not stable over time as

consumers adjust to changing tastes and prices to alter what and how much they consume of different

goods and services.

• Measuring the prices of goods and services: Even if you had consensus on the market basket, the prices for

goods and services have to be estimated ‐ U.S. Bureau of Labor Statistics uses sampling techniques to

obtain prices of goods and service from sellers, and double check them against consumer

expenditures. But these are only samples.

• Adjusting for seasonal patterns: Some goods and services with pronounced seasonal patterns in prices.

and U.S. Bureau of Labor Statistics tries to control for the seasonality when measuring changes in pricing

power (i.e., estimate change in prices in excess of seasonal increase).

“Impact of Inflation and the Current Economy on Valuations” 7

Why are we where we are?

“The current inflation episode is just the kind of event that the fiscal theory of

the price level can easily describe. It’s simple. The US government printed up

about $3 trillion of money and sent people checks. It borrowed an additional

$2 trillion of money and sent people more checks.”

John H. Cochrane, Senior Fellow, Hoover Institution, Stanford University

“Impact of Inflation and the Current Economy on Valuations” 8

47/25/2022

Total Assets Held by Major Central Banks Over Time

December 31, 2007 – June 30, 2022

$25.0

% Change USD 24.7 Trillion

After COVID-19

Feb 2020 – Jun

2022

$20.0

Bank of England 77%

Assets Held by Central Banks (in USD trillions)

Bank of Japan 0%

European Central

Bank

82%

$15.0

U.S. Federal

Reserve

114%

$10.0

$5.0

$0.0

Sources: Capital IQ, FRED® Economic Data, Bank of England, Bank of Japan and European Central Bank

“Impact of Inflation and the Current Economy on Valuations” 9

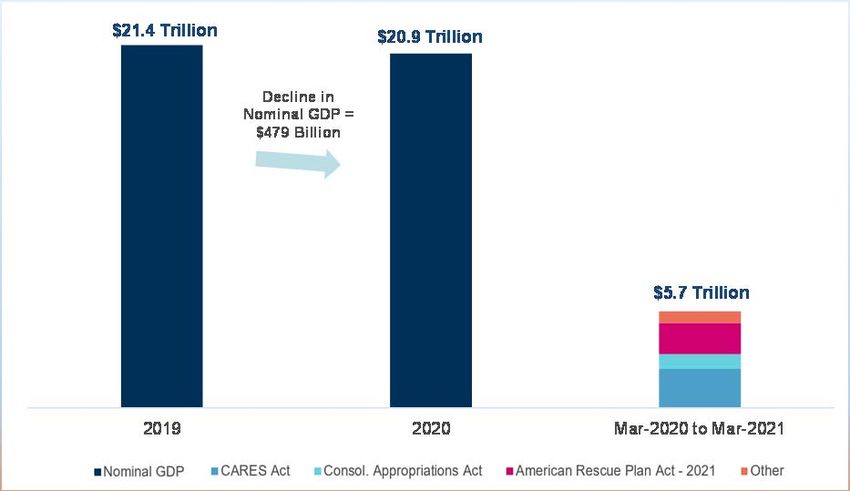

U.S. Fiscal Policy Response to COVID‐19 as a Proportion of Nominal GDP

Size of Combined

COVID-19 Fiscal

Stimulus Packages:

27%

of 2019 Nominal GDP

Sources: U.S. Bureau of Economic Analysis, IMF

“Impact of Inflation and the Current Economy on Valuations” 10

57/25/2022

Global Supply Chain Pressure Index (GSCPI)

January 1998 – May 2022

5.0

4.0

3.0

2.0

1.0

0.0

-1.0

-2.0

May-2022

Jan-1998

Jun-2004

Jan-2005

Jun-2011

Jan-2012

Jun-2018

Jan-2019

Aug-1998

Mar-1999

Oct-1999

May-2000

Jul-2001

Sep-2002

Apr-2003

Aug-2005

Mar-2006

Oct-2006

May-2007

Jul-2008

Sep-2009

Apr-2010

Aug-2012

Mar-2013

Oct-2013

May-2014

Jul-2015

Sep-2016

Apr-2017

Aug-2019

Mar-2020

Oct-2020

May-2021

Dec-2000

Feb-2002

Nov-2003

Dec-2007

Feb-2009

Nov-2010

Dec-2014

Feb-2016

Nov-2017

Dec-2021

Source: Federal Reserve Bank of New York

“Impact of Inflation and the Current Economy on Valuations” 11

Unemployment Rate Holds at 3.6%...

As Job Openings Continue to Increase

428,000

400,000 390,000

April May

328,000 Unemployment Rate 6.1%

3.6% 3.6%

Change from Prior 0.0% 0.0%

Month

Apr-2022 May-2022

Actual Expected

Sources: Non‐farm payrolls by Bureau of Labor Statistics; CNBC “Payroll growth accelerated by 428,000 in April, more than expected as jobs picture stays strong” May 6, 2022; CNBC “Payrolls rose 390,000 in

May, better than expected as companies keep hiring” June 3, 2022

“Impact of Inflation and the Current Economy on Valuations” 12

67/25/2022

Job Openings vs Number of Employed (thousands)

January 2020 to April 2022

25,000

Job Surplus of

20,000 5.45 million

15,000

10,000

5,000

0

Job openings Unemployment

Source: U.S. Bureau of Labor Statistics

“Impact of Inflation and the Current Economy on Valuations” 13

Wages: CPI for All Urban Wage Earners and Clerical Workers

January 1960 – May 2022

Source: FRED, series from U.S. Bureau of Labor Statistics, Consumer Price Index for All Urban Wage Earners and Clerical Workers: All Items in U.S. City Average

“Impact of Inflation and the Current Economy on Valuations” 14

77/25/2022

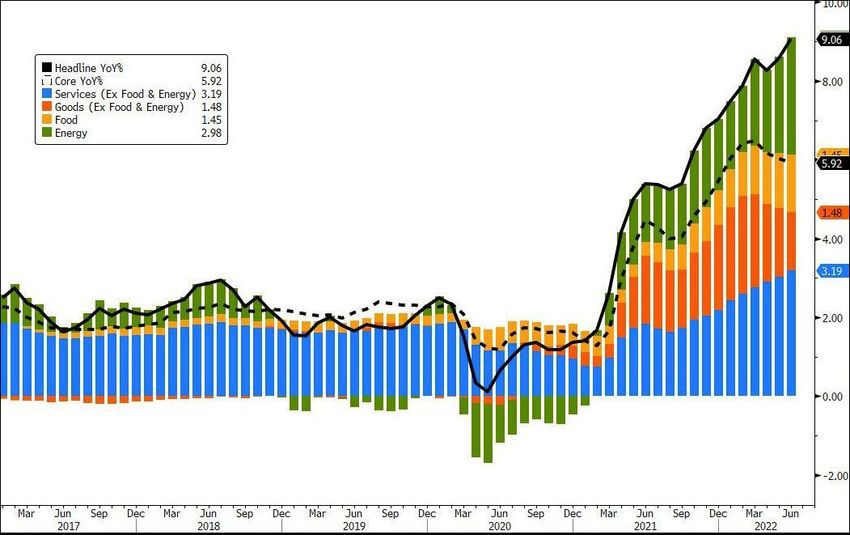

Inflation (YoY%) over the last 5 1/2‐years

“Impact of Inflation and the Current Economy on Valuations” 15

Percent changes in CPI for All Urban Consumers

(CPI‐U): U.S. city average Source: U.S. Bureau of Labor Statistics, July 13, 2022

Seasonally adjusted changes from preceding month Un-

adjusted

Dec. Jan. Feb. Mar. Apr. May Jun. 12-mos.

2021 2022 2022 2022 2022 2022 2022 ended

Jun. 2022

Energy

0.3 2.9 -0.4 1.8 1.3 3.0 3.5 19.4

services

Electrici

0.5 4.2 -1.1 2.2 0.7 1.3 1.7 13.7

ty

Utility

(piped)

-0.3 -0.5 1.5 0.6 3.1 8.0 8.2 38.4

gas

service

“Impact of Inflation and the Current Economy on Valuations” 16

87/25/2022

12‐Month Percentage Change, CPI vs. Core Inflation (%)

December 1981 to June 2022

9.5%

40.6 years as of June 2022 9.1%

7.5%

39.6 years as of Mar 2022

5.5%

5.9%

3.5%

1.5%

-0.5%

-2.5%

CPI 12-Month % Change Core CPI 12-Month % Change

Source: U.S. Bureau of Labor Statistics, Non‐Seasonally Adjusted series

“Impact of Inflation and the Current Economy on Valuations” 17

12‐Month Percentage Change, Core Inflation by Major

Categories (%)

June 2022

41.6%

Last time Food Prices

were this High

Aug 1978

10.4%

Last time Energy Prices

10.4% were this High

9.1%

Jan 1980

5.9%

41.5%

Inflation (All Items) Core Inflation (Ex-Food Food Energy

& Energy)

Source: U.S. Bureau of Labor Statistics, Non‐Seasonally Adjusted series

“Impact of Inflation and the Current Economy on Valuations” 18

97/25/2022

Food Prices under Strain –

Ukraine Exports as Percent of Global Exports

2021/2022 Marketing Year

Sunflower Meal 58%

Sunflower Oil 47%

Rapeseed 20%

Barley 17%

Corn 14%

Wheat 10%

Sunflower 5%

Source: USDA, updated March 9, 2022

“Impact of Inflation and the Current Economy on Valuations” 19

S&P Global “The Global Food Shock Will Last Years, Not

Months”

June 1, 2022

Executive Summary

Rising food prices and diminishing supplies will last through 2024 and possibly beyond

Fertilizer shortages, export controls, disrupted global trade, and escalating fuel and

transport costs will all exert upward pressure on the cost of staples

The food shock will drag on GDP growth, fiscal performance, and social stability, and

could lead to rating actions, depending on the response by governments and

international organizations

“Impact of Inflation and the Current Economy on Valuations” 20

107/25/2022

Gasoline Prices (U.S. Dollar per U.S. Gallon)

June 6, 2022

Top 20 Countries

with most expensive

Gas at the pump

Source: www.globalpetrolprices.com. The prices for the countries with a * are updated weekly. The data for the remaining countries are updated monthly.

“Impact of Inflation and the Current Economy on Valuations” 21

12‐Month Percentage Chang (%) Consumer Price Inflation (CPI) Index

(YOY) – World, Advanced Economies, Emerging Markets

January 2000 – March 2022

10.0

Record High in this time

period for the World and

Advanced Economies

8.0

6.8

6.7

6.0 6.3

4.0

2.0

11-year record

for Emerging

Markets

0.0

-2.0

Mar-22

Jan-00

Jul-00

Jan-01

Jul-01

Jan-02

Jul-02

Jan-03

Jul-03

Jan-04

Jul-04

Jan-05

Jul-05

Jan-06

Jul-06

Jan-07

Jul-07

Jan-08

Jul-08

Jan-09

Jul-09

Jan-10

Jul-10

Jan-11

Jul-11

Jan-12

Jul-12

Jan-13

Jul-13

Jan-14

Jul-14

Jan-15

Jul-15

Jan-16

Jul-16

Jan-17

Jul-17

Jan-18

Jul-18

Jan-19

Jul-19

Jan-20

Jul-20

Jan-21

Jul-21

Jan-22

Emerging Markets World Advanced Economies

Source: IHS Markit, May 17, 2022

“Impact of Inflation and the Current Economy on Valuations” 22

117/25/2022

12‐Month Percentage Change (%) In Consumer Price Inflation (CPI)

Index (YOY)

May 2022 (%) Comments

United States 8.6% New 40-year record high.

April 2022 reading. Record in 31 years, largely driven by food, energy,

Canada 6.8% and transportation prices.

April 2022 reading. Record high CPI 12-month inflation rate in the

National Statistics series, which began in January 1997. Based on

United Kingdom 9.0% recently-published modeled consumer price inflation data for earlier

periods, inflation would have been higher in 1982, 40 years ago.

Record since the German reunification in 1990, 31 years ago. May 2022

Germany* 7.9% preliminary indication of 7.9%, if confirmed, would be the highest since

1973/1974, almost half a century ago.

Record since series creation in January 1997 (25 years ago), just prior

Eurozone 8.1% to the launch of the euro, driven primarily by unprocessed food and

energy prices. May 2022 is a preliminary indication

Source: U.S. Bureau of Labor Statistics, Statistics Canada, U.K. Office for National Statistics, Germany’s Destatis Statistisches Bundesamt, Eurostat.

* Non-harmonized measure.

Valuation, Inflation & Cost of Capital

“Impact of Inflation and the Current Economy on Valuations” 23

What can happen when inflation spirals out of control?

Inflation hit 5.97% in 1970. By 1974, inflation hit more than 11%. Inflation finally peaked at 13.5% in 1980.

From 1964 to 1980 the cumulative rate of inflation was 165.8% (Source U.S. Inflation Calculator)

“Impact of Inflation and the Current Economy on Valuations” 24

127/25/2022

Industry Trends

“Impact of Inflation and the Current Economy on Valuations” 25

2022 YTD Best and Worst Performing Industries Within the

S&P 500 Index

December 31, 2021 to June 30, 2022

S&P 500 - Energy Sector Index

80%

S&P 500 Index (Total Returns)

S&P 500 - Consumer Discretionary Sector

60% Index

40%

31.8%

20%

0%

-20% -20.0%

-32.8%

-40%

Source: CapitalIQ

“Impact of Inflation and the Current Economy on Valuations” 26

137/25/2022

2022 YTD Industry Performance in the S&P 500 Index (Total

Returns)

December 31, 2021 to June 30, 2022

Industry 2022 YTD (%)

Energy 31.8

Utilities -0.6

Consumer Staples -5.6

Healthcare -8.3

Industrial -16.8

Materials -17.9

Financials -18.7

Information Technology -26.9

Communications -30.2

Consumer Discretionary -32.8 Source: Capital IQ

“Impact of Inflation and the Current Economy on Valuations” 27

Impact of market drivers on beta

• The beta estimate for a specific company may underestimate that company's true beta if the market index

used during the look‐back period is overweighted by a specific industry. The theory is that the market index

should reflect the overall economy. But at times the market value for a particular segment of the economy

will take over the market index (e.g., FAANG stocks in recent years or in developing economies where one

or two stocks dominate the stock market capitalization).

• For example, if one computed beta estimates using historical returns over a look‐back period or obtained

beta estimates from data sources, the risks for basic manufacturing companies appeared to have gone

down in recent years because the beta estimates of these companies decreased. Prior to the run‐up in

prices of FAANG stocks, basic manufacturing companies represented significant weight in the stock indices.

Prior to the runup of technology and specifically FAANG stocks, the returns on basic manufacturing stocks

were highly correlated to the changes in the stock indices.

• As technology stocks began to dominate indices, the returns on the stocks of basic manufacturing

companies were significantly less correlated with returns in the market indices, making it appear that their

risks had been reduced. The underlying risks of basic manufacturing companies had not in fact changed.

But their observed betas then looked low compared with their long‐term average betas.

“Impact of Inflation and the Current Economy on Valuations” 28

147/25/2022

FAANG

December 31, 2021 to June 30, 2022

10% Apple Inc. Microsoft Amazon Meta (Facebook) Netflix

0%

-10%

-20%

-23%

-24%

-30%

-36%

-40%

-50%

-52%

-60%

-70% -71%

-80%

Source: CapitalIQ

“Impact of Inflation and the Current Economy on Valuations” 29

Projected Economic Growth

Short‐Term and Long‐Term

“Impact of Inflation and the Current Economy on Valuations” 30

157/25/2022

Real GDP Growth (%) Estimates (Median)

Data as of May 20, 2022

WORLD

2021

5.8

2022

2023

3.4 3.2

2020

-3.4

Sources: OECD, International Monetary Fund, World Bank, Blue Chip Economic Indicators, Consensus Economics, Economic Intelligence Unit, Fitch Ratings, IHS Markit, Moody's Analytics, Oxford Economics and S&P Global Ratings

“Impact of Inflation and the Current Economy on Valuations” 31

Real GDP Growth (%) Estimates (Median)

Data as of May 20, 2022

U.S. 2021

5.7

2022

2023

2.8

2.1

2020

-3.4

Sources: OECD, International Monetary Fund, World Bank, Blue Chip Economic Indicators, Consensus Economics, Economic Intelligence Unit, Fitch Ratings, IHS Markit, Moody's Analytics, Oxford Economics and S&P Global Ratings

“Impact of Inflation and the Current Economy on Valuations” 32

167/25/2022

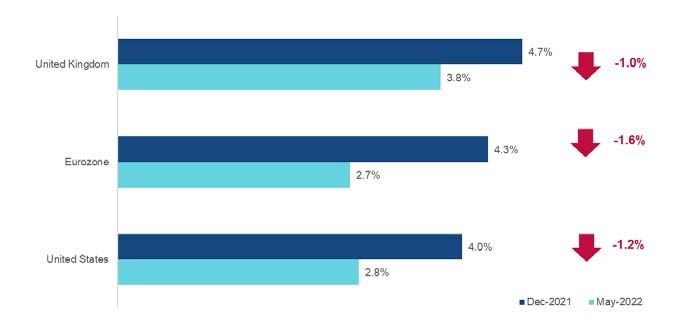

2022 Real GDP Growth Rates of U.S., Eurozone, and UK

Median Estimates

Estimates as of December 1, 2021 and as of May 2022

Sources: OECD, International Monetary Fund, World Bank, Blue Chip Economic Indicators, Consensus Economics, Economic Intelligence Unit, Fitch Ratings, IHS Markit, Moody's Analytics, Oxford Economics and S&P Global Ratings

“Impact of Inflation and the Current Economy on Valuations” 33

Real GDP Growth (%) Estimates (Median)

Data as of May 20, 2022

CHINA

2021

8.1

2023

2022

5.3

4.6

2020

2.2

Sources: OECD, International Monetary Fund, World Bank, Blue Chip Economic Indicators, Consensus Economics, Economic Intelligence Unit, Fitch Ratings, IHS Markit, Moody's Analytics, Oxford Economics and S&P Global Ratings

“Impact of Inflation and the Current Economy on Valuations” 34

177/25/2022

Long‐term Projected Real GDP Growth (%)

Data as of June 30, 2022

SOURCE Long-Term Average (%)

Blue Chip Economic Indicators 2.5

Blue Chip Financial Forecasts 2.2

Consensus Economics 2.6

IHS Markit 2.5

Livingston Survey 2.2

Oxford Economics 2.6

Survey of Professional Forecasters 2.5

Range of Real GDP Growth Estimates

2.2% – 2.6%

Median 2.5%

“Impact of Inflation and the Current Economy on Valuations” 35

Long‐Term U.S. Inflation Expectations (5 to 10 Years Ahead)

Estimates as of June 30, 2022 (approximately)

SOURCES Long-Term Average (%)

What was the median

Aruoba Term Structure of Inflation Expectations 2.4 estimated long-term

Blue Chip Economic Indicators 2.8 inflation as of

Blue Chip Financial Forecasts 2.8 June 30, 2020?

Consensus Economics 3.0

Federal Reserve Bank of Cleveland 2.4

2.0%

IHS Markit 2.7

Livingston Survey (Federal Reserve Bank of Philadelphia) 2.5

Oxford Economics 2.6

Survey of Professional Forecasters (Federal Reserve Bank of

Philadelphia)

2.8

University of Michigan Survey 5-10 Year Ahead Inflation Expectations 3.1

Range of Inflation Estimates 2.4% – 3.1%

Median 2.8%

“Impact of Inflation and the Current Economy on Valuations” 36

187/25/2022

g = Long‐Term Growth Rate (Nominal)

Estimates as of early June 2022 (approximately)

The Long‐Term Growth Rate is calculated using the following formula:

1

Long-Term (1 + Long-

(1 + Long-

Growth Rate Term Real

Term Inflation

GDP

(Median) Forecast

Forecast)

5.4% = ( 1 + 2.5% ) ( 1 + 2.8% ) – 1

“Impact of Inflation and the Current Economy on Valuations” 37

Cost of Capital Ramifications

from Higher Inflation

“Impact of Inflation and the Current Economy on Valuations” 38

197/25/2022

Rising Inflation and Impact on Cost of Capital Inputs

“Impact of Inflation and the Current Economy on Valuations” 39

10‐Year Government Bond Yields for Canada, U.S., U.K., and

Germany

December 31, 2007 – June 30, 2022

6%

Canada Government Debt - 10 Year

5% United States Treasury Constant Maturity - 10 Year

United Kingdom Government Debt - 10 Year

Germany Government Debt - 10 Year

4%

3.2%

3% 3.0%

2.3%

2%

1.3%

1%

0.3%

0%

-1%

Sources: Capital IQ, NBER, ECRI

“Impact of Inflation and the Current Economy on Valuations” 40

207/25/2022

U.S. 20‐Year Treasury Yield, Including 10‐Year Trailing Average

December 31, 2007 – June 30, 2022

Spot 20-Year U.S.

Treasury Yield on

July 15, 2022

3.3%

Sources: Capital IQ, NBER

“Impact of Inflation and the Current Economy on Valuations” 41

Nominal vs Real Risk‐Free Rate

Conceptually, the risk-free rate can be illustrated as the return on the following two components:*

Risk-free Expected

Real Rate

Rate Inflation

* This is a simplified version of the “Fisher equation”, named after Irving Fisher. Fisher’s “The Theory of Interest” was first published by Macmillan (New York), in 1930. The Fisher

equation is formally expressed as (1 + Nominal Rate) = (1 + Real Rate) x (1 + Expected Inflation). When rates are low, there is very little difference between the simple form and the

Fisher equation. Various academic research papers show that the decomposition of the nominal rate into a real rate and expected inflation should include an additional component

excluded from the Fisher equation: the inflation risk premium. This premium reflects the risk that actual inflation may vary significantly from expected inflation, and it can be positive or

negative, with some academic estimates at close to 0%. In the current environment, the inflation risk premium could be a meaningful positive number.

“Impact of Inflation and the Current Economy on Valuations” 42

217/25/2022

Real Rate Estimates

Several academic studies have suggested the long-term real risk-free rate to be somewhere

in the range of -1.1% to 2.0% based on the study of inflation swap rates, yields on long-term

U.S. Treasury Inflation-Protected Securities (TIPS), OLG, DSGE and other econometric

models *

-1.1 % Long-term Real Rate 2.0%

* Based on academic studies issued between 2015 and 2021. In academic literature, this is also sometimes called the natural rate of interest, the neutral rate, or the equilibrium rate.

OLG = Overlapping Generational Model

DGSE = Dynamic Stochastic General Equilibrium Model

“Impact of Inflation and the Current Economy on Valuations” 43

Long‐Term U.S. Inflation Expectations (5 to 10 Years Ahead)

Estimates as of June 30, 2022 (approximately)

SOURCES Long-Term Average (%)

What was the median

Aruoba Term Structure of Inflation Expectations 2.4 estimated long-term

Blue Chip Economic Indicators 2.8 inflation as of

Blue Chip Financial Forecasts 2.8 June 30, 2020?

Consensus Economics 3.0

Federal Reserve Bank of Cleveland 2.4

2.0%

IHS Markit 2.7

Livingston Survey (Federal Reserve Bank of Philadelphia) 2.5

Oxford Economics 2.6

Survey of Professional Forecasters (Federal Reserve Bank of

Philadelphia)

2.8

University of Michigan Survey 5-10 Year Ahead Inflation Expectations 3.1

Range of Inflation Estimates 2.4% – 3.1%

Median 2.8%

“Impact of Inflation and the Current Economy on Valuations” 44

227/25/2022

Current inflation expectations measured by interest rates

(Source: Crestmont Research)

• Although short‐term interest rates are still incongruous with the current level of inflation, longer‐term

interest rates are closely tracking the overall market's expectation for future inflation.

• One of the best indications of intermediate‐term inflation is the 5‐Year, 5‐Year Forward Inflation

Expectation Rate. The measure is provided by the Federal Reserve Bank of St. Louis. The rate reflects the

market's expectation for average inflation over a five‐year period that starts five years ahead. Today, the

expected rate of inflation for 2028‐2032 is approximately 2.08%.

• Intermediate and long‐term bonds are aligned with inflation expectations, assuming that the market is

accurately assessing inflation risk. That's a significant assumption.

“Impact of Inflation and the Current Economy on Valuations” 45

Expected inflation

• Interest rates: The link between expected inflation and interest rates is explained by the Fisher equation,

where a nominal risk‐free interest rate (e.g., treasury bond rates) can be broken down into expected

inflation and expected real interest rate components:

(1 + risk‐free rate) = (1 + real interest rate) (1 + expected inflation rate + inflation risk premium)

where inflation risk premium = risk that inflation expectations are wrong – the greater the risk that

inflation measures are inaccurate, the greater the inflation risk premium

• Inflation surveys: Surveys (e.g., Michigan survey) report measures of expected inflation, obtained by

surveying economic experts or consumers.

• Exchange rates: Using a base currency where you can estimate expected inflation (e.g., U.S. dollar or Swiss

Franc) and forward exchange rates in the currency of another country, one can estimate inflation

embedded in that country’s currency.

“Impact of Inflation and the Current Economy on Valuations” 46

237/25/2022

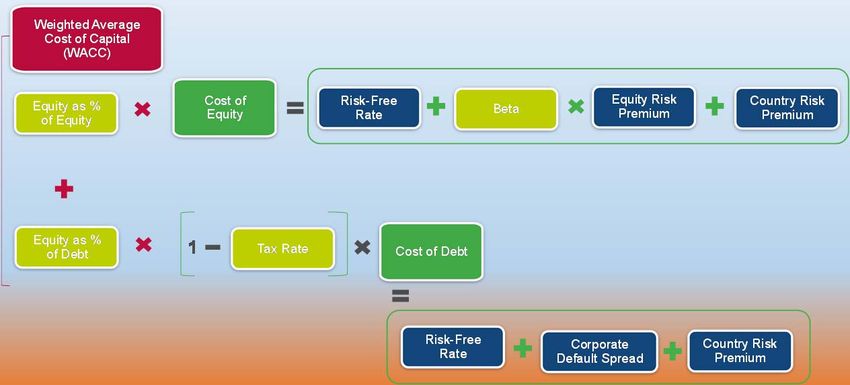

Build up of Nominal Risk‐free Interest Rate

• The risk‐free rate reflects three components:

• Rental rate.

• Inflation.

• Maturity risk or investment rate risk.

• All three of these economic factors are embedded in the yield to maturity for any given maturity length.

• It is not possible to observe the market consensus about how much of the yield for any given maturity is attributable

to these factors.

• Exception is expected inflation, which can be estimated based on Treasury inflation‐protected securities [TIPS]).

• In the U.S., there are a number of well‐established surveys providing consensus estimates for expected inflation.

• Combining the range of long‐term real rates PLUS the range of expected inflation forecasts gives us an estimated build‐

up of the risk‐free interest rate.

“Impact of Inflation and the Current Economy on Valuations” 47

Issues with Risk‐free rate and ERP during times of crisis –

examining a build‐up of the risk‐free interest rate is

important

“Impact of Inflation and the Current Economy on Valuations” 48

247/25/2022

Risk‐Free Rate Normalization – United States

As of June 30, 2022

-1.1% Long-term Real Rate 2.0%

+ +

Spot 20-Year U.S.

2.4% Long-term Expected Inflation 3.1% Treasury Yield on

July 15, 2022

= =

3.3%

1.3% Long-term Normalized Risk-Free Rate 5.1%

• Fisher Equation: Midpoint = 3.2% / Median = 3.4%

• LT Average: 10-Year Trailing Average of 20-Year U.S. Treasury Yield = 2.5%

Concluded Normalized Rf = 3.5%

“Impact of Inflation and the Current Economy on Valuations” 49

Corporate Debt Spreads

U.S. High Yield Corporate Bond Yields over U.S. Investment Grade Corporate Bond Yields

December 2007 – June 2022

16.0%

December 15, 2008

14.4%

(Record High)

Series1 Longer Term Average Series2

14.0%

12.0%

March 25, 2020

6.6%

10.0%

February 11, 2016

(D&P increases

ERP to 6.0% from

July 15, 2022

6.2%

5.0%)

8.0% December 9, 2020

2.7%

(D&P lowers ERP to

5.5% from 6.0%)

3.8%

6.0% June 30, 2022

4.0%

4.0% 3.7%

2.0%

December 19, 2019

2.4%

(D&P lowers ERP to 5.0% from 5.5%)

0.0%

Sources of underlying data: FRED

“Impact of Inflation and the Current Economy on Valuations” 50

257/25/2022

Where are we?

• Despite inflation reaching multidecade highs and no clear end in sight for today's market

negativity, the U.S. government appears reluctant to declare that we're nearing a recession.

• But the government might not officially declare that we're in a recession for months.

• The term "recession" is a backward‐looking designation.

• U.S. GDP fell by an annualized 1.6% in the first quarter of 2022.

• Assume that the 1.6% decline carried through the entire year. That 1.6% loss would translate to

around $384 billion in lost economic activity.

“Impact of Inflation and the Current Economy on Valuations” 51

What’s Ahead?

“Recession looks very imminent… When you get spot commodity prices

dropping while the inflation rate is accelerating, you've got a recession on

your hands. The reason copper and gold and lumber and all those are

dropping is because the demand for them is going down. It's not like rents

and all these other things that are rising at high rate. So we've got the worst

of all possible worlds.”

Economist Art Laffer

“Impact of Inflation and the Current Economy on Valuations” 52

267/25/2022

U.S. Recessions since 1980

“Impact of Inflation and the Current Economy on Valuations” 53

What’s Ahead? U.S. Recessions since 1980

Time since Peak GDP decline

Period Duration

Name previous recession unemploy (peak to

Range (months)

(months) ment trough)

Jan 1980–July 4 years 7.8%

1980 recession 6 months −2.2%

1980 10 months (July 1980)

July 1981–Nov 1 year 10.8%

1981–1982 recession 1 year −2.7%

1982 4 months (Nov 1982)

July 1990–Mar 7 years 7.8%

Early 1990s recession 8 months −1.4%

1991 8 months (June 1992)

Mar 2001–Nov 6.3%

Early 2000s recession 8 months 10 years −0.3%

2001 (June 2003)

Dec 2007–June 1 year 6 years 10.0%

Great Recession −5.1%

2009 6 months 1 month (October 2009)

Feb 2020–April 10 years 14.7%

COVID-19 recession 2 months −19.2%

2020 8 months (April 2020)

“Impact of Inflation and the Current Economy on Valuations” 54

277/25/2022

What’s Ahead?

• From 1980 through today, all six recessions in the U.S. lasted less than two years. And

four recessions didn't even carry on for an entire year.

• In the second quarter, the stock market declined further. As a result, normalized P/E

decreased to 32.2. The Adjusted P/E (based upon Shiller's CAPE P/E10 method) is 28.2.

Both normalized values are significantly above the As Reported P/E of 18.8.

• The stock and bond markets appear to have accepted (for now) that the recent surge in

inflation will moderate back to near 2% within the next five years. Inflation at that level

would justify P/E in the low‐ to mid‐20s. (Source: Crestmont Research, July 11, 2011)

• Will Fed’s actions be sufficient to halt the increasing rate of inflation? Will we enter a

recession?

“Impact of Inflation and the Current Economy on Valuations” 55

Projecting Company Cash Flows

Potential Impact from Inflation

“Impact of Inflation and the Current Economy on Valuations” 56

287/25/2022

Projecting Company Cash Flows

• There is no “one size fits all” when understanding how inflation will impact a specific company

• What is the sensitivity of your company’s pricing to inflation? How easy is it for your company to raise prices?

• What is the sensitivity of your company’s operating costs to inflation? Can you control rising costs?

• The difference in these sensitivities will determine if your margins will be squeezed. Recession will likely cause

increased variance in operating profit margins which will result in increased cost of equity.

• Is your company in the midst of any large capital projects? Can you change the project timeline to stagger phases

of the project if inflationary costs spiral? What is your flexibility?

• Is your company planning any large capital expansions? Can you phase the project to better control required

investments as costs rise?

• As inflation increases, there is more uncertainty, which will further increase interest rates and equity premiums.

• Are your financing costs fixed or are they variable? When will refinancing of existing debt be required? The cost

of debt financing will go up as inflation continues/increases.

• The cost of equity will increase as interest rates increase and volatility of profit margins increase (see graph

showing relationship documented by the Kroll Risk Premium – Risk Study).

“Impact of Inflation and the Current Economy on Valuations” 57

Kroll Risk Premium Report – Risk Study

available via the Kroll on‐line Cost of Capital Navigator

Increasing risk premium as variability of operating margin increases

Smoothed Premium vs. Unadjusted Average

20%

18%

16%

14%

Equity Premium

12%

10%

8%

6%

4%

2%

0%

-1.8 -1.6 -1.4 -1.2 -1.0 -0.8 -0.6 -0.4 -0.2 0.0 0.2 0.4

Log of Median CV(Operating Income)

“Impact of Inflation and the Current Economy on Valuations” 58

297/25/2022

Questions?

Contact information:

Roger.Grabowski@kroll.com

“Impact of Inflation and the Current Economy on Valuations” 59

30You can also read