How Will FinTech Change the Way Challenger Banks Reward and Engage Consumers Mladen Vladic General Manager of Loyalty Services, FIS

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

How Will FinTech Change the Way

Challenger Banks Reward and Engage The CardLinx Association

Consumers

Mladen Vladic CARDLINX WEBINAR 2020 September 9

General Manager of Loyalty Services, FIS

Today’s Agenda

Welcome from Becca

Donahue, Director of

Meeting Services, The Open Q&A From All

CardLinx Association Attendees

9:00 AM 9:10 AM 9:45 AM 10:00 AM

Presentation from CardLinx Meet-Ups

Mladen Vladic, Begin

General Manager of

Loyalty Services at FIS

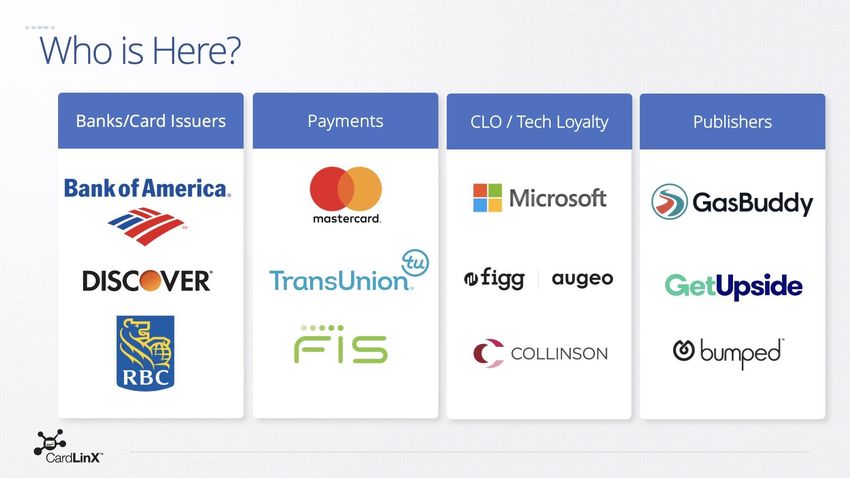

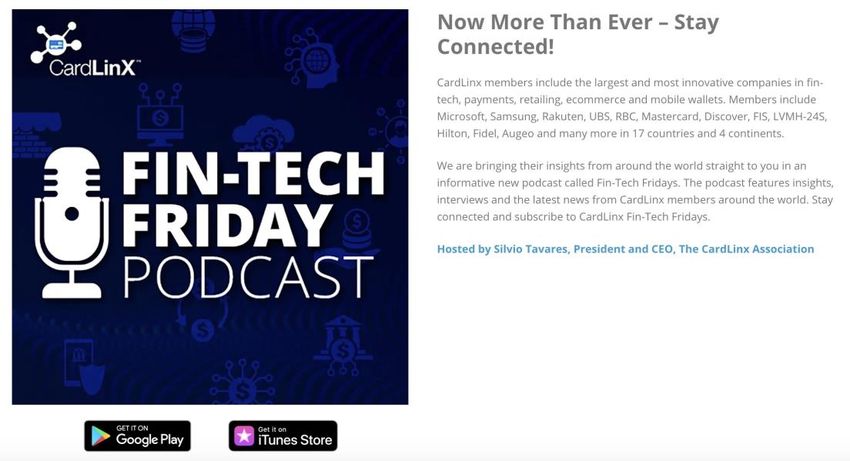

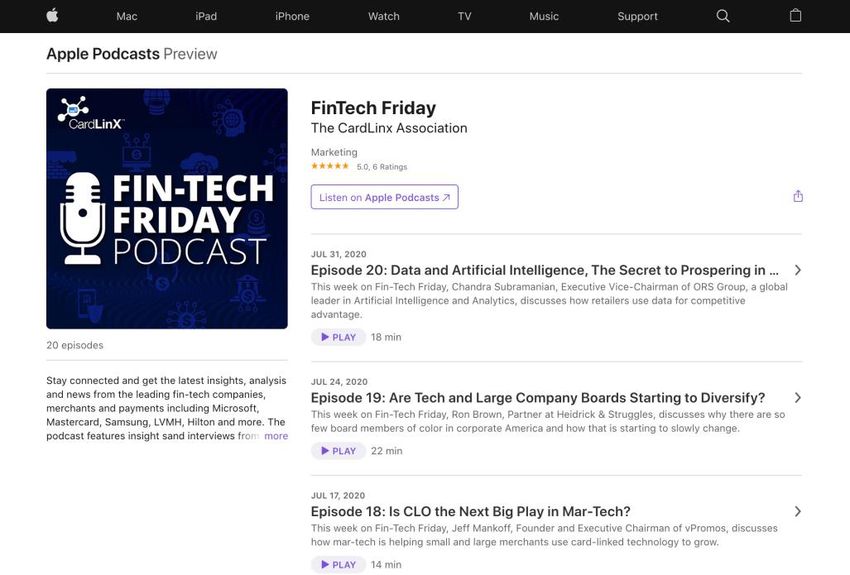

NEW! The FinTech Friday Weekly Podcast

cardlinx.org/podcast

Coming Up In October… https://cardlinx.org/events/webinars/

‘Fiction Becomes

Reality: The New

Age of One-to-

One Marketing’

Speaker:

Ryan Wuerch, CEO

Tuesday, October 20

9am-10am PST

CardLinx West | October 7, 2020 | via Zoom

https://cardlinx.org/events/cardlinx-west-2020/

Ashwin Raj, Paul Siegfried

VP of Payments Senior Vice President

Lyft TransUnion

Ryan Wuerch Mehmet Sezgin

Chief Executive Officer CEO

Dosh myGini

CardLinx East | December 8, 2020 | via Zoom

‘Looking Beyond 2021: The Age of Digital Commerce Post Covid-19’

To Pre-Register:

Email Rebecca@

cardlinx.org

Bruno Chauvat Darby Sieben

Sarah McCrary Chi ef Executive Officer

Chi ef Executive Officer Tra vel sify

Head of Ampli

Ga s Buddy RBC Ventures

HOW WILL FINTECH CHANGE THE WAY CHALLENGER BANKS REWARD AND ENGAGE CONSUMERS? Mladen Vladic, General Manager - Loyalty, FIS September 9, 2020

COVID-19 Global Influence

FIS CEO, Gary FIS was involved in Involved in EU / UK Partnered with Successfully Lobbied Partnered with

Norcross was successful lobbying payments advisory Government lobbied for Congress to U.S. Treasury

appointed a for deferrals of groups to increase Banking Service in waiver of ensure all to help and

member of the Payment Network, contactless the UK to provide excessive channels could engage in

White House April tech changes transaction NHS workers chargeback, be used to operationalizing

Great American and cost increases threshold amounts grocery supplies, fraud penalties distribute relief to economic relief

Economic Revival until July along with to aid in social waiving and and fees for the small businesses. for individuals

Industry Group. some cost changes distancing. reducing fees. travel sector. and businesses.

deferring until

October.

10Transformative Forces

BIG DATA

Analyzing complex data to reveal patterns, trends, and

associations that provide new customer insights.

EXPERIENCE

Delivering simple personalized digital experiences and loyalty

driven value across multiple channels.

NETWORK EFFECT

Leveraging componentized platforms to initiate instantaneous adoption.

PACE OF CHANGE

A constantly accelerating time to market for new technology.

11Rapidly Changing Payments Landscape

Confluence of factors driving rapid pace of

innovations benefiting consumers!

• Changing consumer behavior trends accelerated by COVID-19

• Shift to eCommerce spend

• Use more online/mobile banking instead of in-branch servicing

• Increased use of call center/chat services

• Rise of contactless payments

• Online payments and bank transfers/wire

• Remote financial adviser services

• Rise of digital payments and the slow decline of plastic

• Rise of nontraditional financial service providers

• Faster payments

12Rewards have dramatically evolved

Disrupting the traditional loyalty landscape by creating a new type of currency

Pay with Points

Acceleration of this trend by

consumers looking to access and

monetize loyalty currency for an

immediate benefit

Consumers expect full flexibility and

dynamic value exchange

Premium

Airline Retailers

Miles

Utility Based

Diners

Rewards

Club POS & Ecom m erce

Experience Post Transaction

Based Redem ption

Rewards Connected Car Paym ents

Source: Deloitte Center f or Financial Serv ices analy sisAs consumer needs change, the cost to meet

those needs is driving down ROI

Rewards Expense vs. Card ROI Reasons for using Cards 3

$180 6%

$168

Rewards, offers, and

$150 $140

$145

$155

72% discounts

4.4%

$120

4.0%

3.8%

4%

53% Not having to carry cash

$90 3.4%

Buying things I could not

$60 2%

36% afford without credit

2015 2016 2017 2018

Average issuer rewards expense1 (M) ROI of large US card issuers2 (%)

Source: (1) Federal Financial Institutions Examination Council, Consolidated Reports of Condition and Income (Call Reports), (2) Bureau of Consumer Financial

Protection, "The Consumer Credit Card Market," August 2019. (3) Deloitte Center f or Financial Serv ices. Pay ments survey among US consumers, 2019.The impact of COVID-19 has rapidly

accelerated trends that we have

been seeing for years in terms of

banking and digital payments.

Go forward strategy:

✓ Reassess your go-to-market

strategy and value proposition

✓ Adjust as needed

✓ Execute

15Q&A

At this time, we will open the meeting up

to Q&A. If you have a question please

unmute yourself or type the question in the

chat box at the bottom of the screen.Event Feedback Survey

A 4-question survey will pop up on

your screen. Please fill out this survey

as it helps us understand how to

better prepare for virtual events in the

future.

All answers are confidential.CardLinx Meet Ups

At this time, you will now be paired up for

CardLinx Meet Ups in a private breakout room.

You will have 15 minutes to connect. The

meeting will conclude once Meet Ups are over.THANK YOU The CardLinx Association

You can also read